Brazil Consumer Credit Market Size, Share, Trends and Forecast by Credit Type, Service Type, Issuer, Payment Method, and Region, 2026-2034

Brazil Consumer Credit Market Overview:

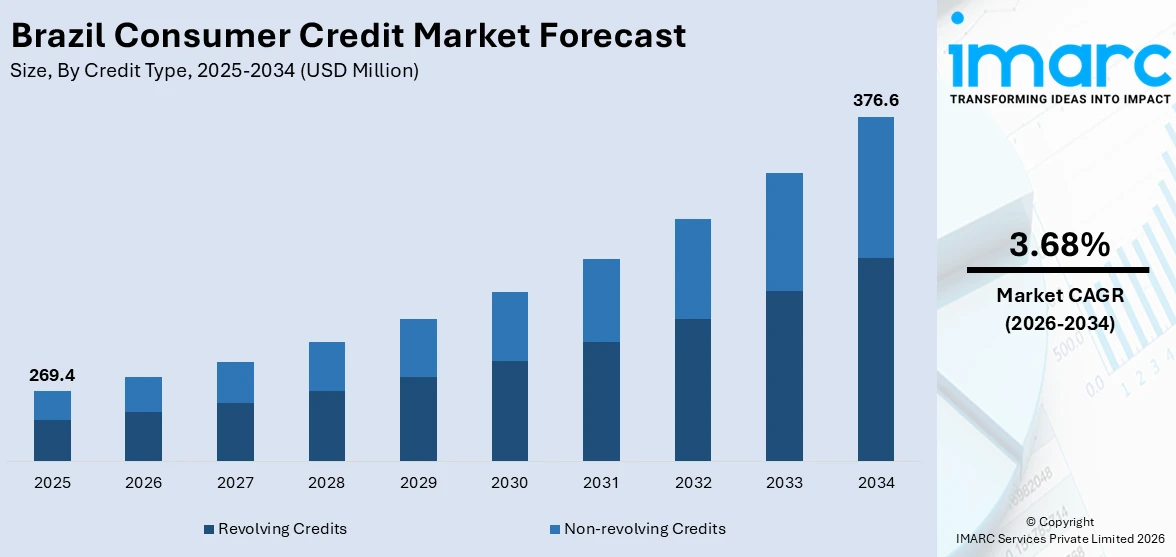

The Brazil consumer credit market size reached USD 269.4 Million in 2025. Looking forward, the market is expected to reach USD 376.6 Million by 2034, exhibiting a growth rate (CAGR) of 3.68% during 2026-2034. The market is fueled by increasing digitalization, growing fintech presence, and demand for credit among previously excluded groups. The prevalence of smartphone usage and internet penetration also facilitates easier loan application and credit card application through digital channels. Public sector financial inclusion policy and open banking reforms have enhanced credit availability, especially among informal workers and younger consumers. Banks and fintechs are becoming more innovative to address changing consumer needs, further driving credit expansion and the Brazil consumer credit market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 269.4 Million |

| Market Forecast in 2034 | USD 376.6 Million |

| Market Growth Rate 2026-2034 | 3.68% |

Brazil Consumer Credit Market Trends:

Expansion of Fintech Credit and Alternative Channels of Lending

One significant trend in Brazil is the very quick development of fintech firms and alternative lenders filling in the gaps where the traditional banking institutions are less present. These sites are more and more providing consumer credit digitally, frequently with quicker time to decision, more versatile terms, and more convenient application procedures. Most of these Brazilians who were hitherto underbanked by big banking institutions, particularly in far-flung areas, peripheral suburbs in large cities, or among young consumers, are using these fintech products for consumer or revolving credit. The trend is also facilitated by more internet penetration and extensive smartphone coverage, facilitating access to credit online. In addition, regulatory efforts that facilitate licensing or oversight of these types of entities have provided fintech lenders with greater legitimacy and consumer acceptance, driving growth. Conventional banks are responding by either collaborating with fintechs, creating their own digital credit offerings, or improving user experience to compete, which further accelerates the Brazil consumer credit market growth.

To get more information on this market Request Sample

Consumer Culture Shaped by Installment Payments Culture

The growing adoption of Real Time Payments in Brazil is strongly influenced by Brazil’s long-standing culture of instalment-based purchasing for durable goods, electronics, furniture, and other high-cost items, as consumers continue to rely heavily on credit cards offering multiple instalment plans, often with zero-interest or extended payment options over several months. Both consumer expectation and retailer supply are shaped by this. Retailers construct credit deals, loyalty schemes, and payment schedules around instalamento conventions, as numerous consumers like to spread payments instead of paying in full in advance. In addition, most purchases in e‑commerce or big physical stores are designed so the instalment choices are made apparent at checkout. This habit shapes product design of credit lines: card issuers and distributors compete not just on interest rates but on number of instalments, whether interest is charged (or postponed), and what fees are bundled. Since customers are used to this parcelamento system, any credit product that does not follow these conventions is resistant or has low uptake.

Role of Instant Payments, Digital Infrastructure, and Regulatory Shifts

A second important trend relates to the digitization of payment systems, digital infrastructure, and regulatory reforms impacting consumer credit availability and price. Brazil's real-time payments scheme has developed to enable functionality more than straightforward transfers like installation capabilities in payments, eroding the distinction between pure payments and credit. Enhanced credit reporting, alternative digital behavior-based scoring, mobile know-your-customer (KYC) procedures, and open banking technology have made it possible for lenders (fintechs and banks alike) to originate credit more effectively and serve customers with thin formal credit history. Regulator-wise, there has been a push to enhance consumer protection, to normalize disclosure of interest rates, fees, and default risk, particularly in the wake of high interest rates for unsecured consumer credit. Additionally, regulators are looking into the increasing levels of default or delinquency in credit lines such as credit cards and payroll‑deductible loans, leading to more stringent regulation in lending standards. These all contribute to the direction of the consumer credit market toward greater transparency, risk management, and greater access on terms suited to local digital behavior and payment expectations.

Brazil Consumer Credit Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on credit type, service type, issuer, and payment method.

Credit Type Insights:

- Revolving Credits

- Non-revolving Credits

The report has provided a detailed breakup and analysis of the market based on the credit type. This includes revolving credits and non-revolving credits.

Service Type Insights:

Access the comprehensive market breakdown Request Sample

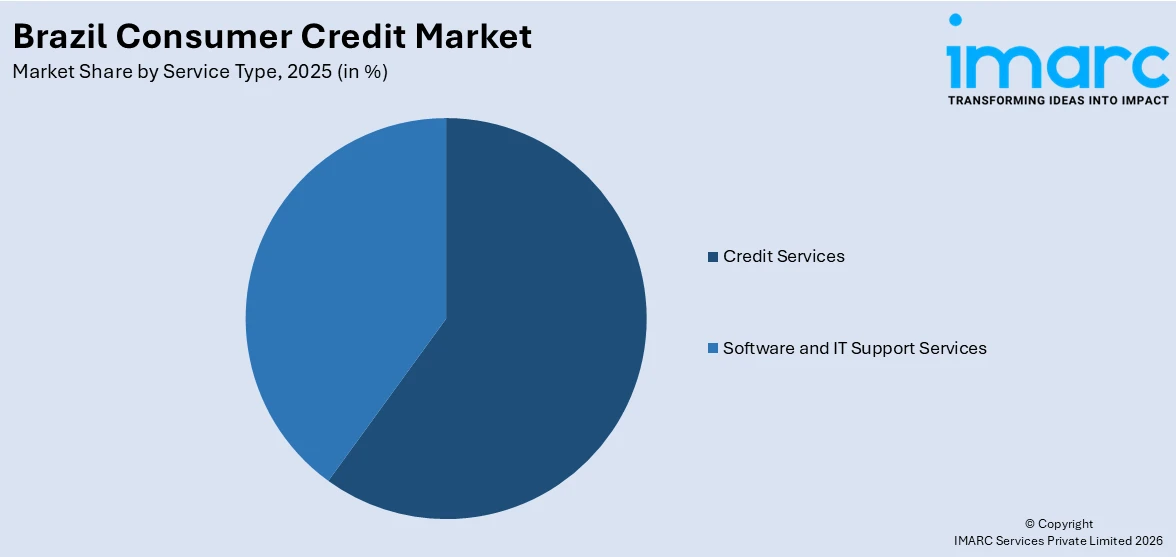

- Credit Services

- Software and IT Support Services

A detailed breakup and analysis of the market based on the service type have also been provided in the report. This includes credit services, and software and IT support services.

Issuer Insights:

- Banks and Finance Companies

- Credit Unions

- Others

The report has provided a detailed breakup and analysis of the market based on the issuer. This includes banks and finance companies, credit unions, and others.

Payment Method Insights:

- Direct Deposit

- Debit Card

- Others

A detailed breakup and analysis of the market based on the payment method have also been provided in the report. This includes direct deposit, debit card, and others.

Regional Insights:

- Southeast

- South

- Northeast

- North

- Central-West

The report has also provided a comprehensive analysis of all the major regional markets, which includes Southeast, South, Northeast, North, and Central-West.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Brazil Consumer Credit Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Credit Types Covered | Revolving Credits, Non-revolving Credits |

| Service Types Covered | Credit Services, Software and IT Support Services |

| Issuers Covered | Banks and Finance Companies, Credit Unions, Others |

| Payment Methods Covered | Direct Deposit, Debit Card, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Brazil consumer credit market performed so far and how will it perform in the coming years?

- What is the breakup of the Brazil consumer credit market on the basis of credit type?

- What is the breakup of the Brazil consumer credit market on the basis of service type?

- What is the breakup of the Brazil consumer credit market on the basis of issuer?

- What is the breakup of the Brazil consumer credit market on the basis of payment method?

- What is the breakup of the Brazil consumer credit market on the basis of region?

- What are the various stages in the value chain of the Brazil consumer credit market?

- What are the key driving factors and challenges in the Brazil consumer credit market?

- What is the structure of the Brazil consumer credit market and who are the key players?

- What is the degree of competition in the Brazil consumer credit market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil consumer credit market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil consumer credit market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil consumer credit industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)