Brazil Data Integration Market Size, Share, Trends and Forecast by Component, Organization Size, Deployment, Application, and Region, 2026-2034

Brazil Data Integration Market Summary:

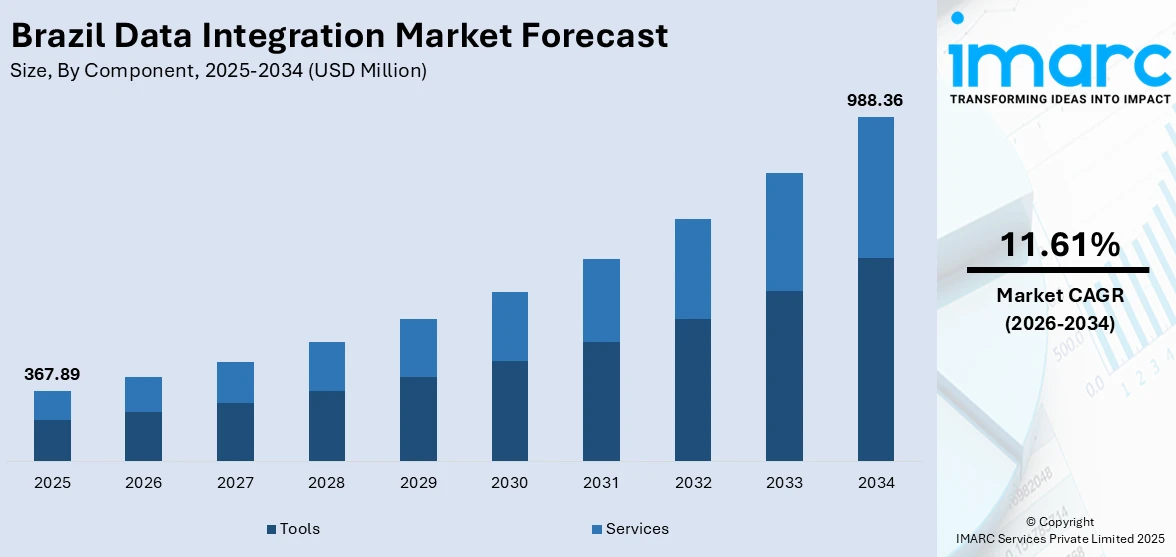

The Brazil data integration market size was valued at USD 367.89 Million in 2025 and is projected to reach USD 988.36 Million by 2034, growing at a compound annual growth rate of 11.61% from 2026-2034.

The Brazil data integration market is gaining significant momentum as enterprises accelerate digital transformation initiatives and modernize legacy infrastructure. Expanding cloud adoption, rising demand for real-time analytics, and increasing regulatory compliance requirements under the LGPD are driving organizations to invest in comprehensive data integration platforms. Advancements in artificial intelligence, open finance frameworks, and supply chain digitalization are reshaping how businesses manage and unify disparate data sources, strengthening the Brazil data integration market share.

Key Takeaways and Insights:

- By Component: Tools dominates the market with a share of 58.6% in 2025, owing to enterprise preference for comprehensive, feature-rich integration platforms that consolidate ingestion, transformation, and analytics workflows. Rising cloud-native ETL adoption is fueling the expansion.

- By Organization Size: Large enterprises lead the market with a share of 54.2% in 2025. This dominance is driven by established IT budgets, complex multi-system environments, and regulatory compliance demands that require enterprise-grade data integration capabilities.

- By Deployment: Cloud represents the largest segment with a market share of 61.8% in 2025, reflecting the accelerating shift toward scalable, cost-effective cloud-based integration platforms that support hybrid architectures and real-time data processing.

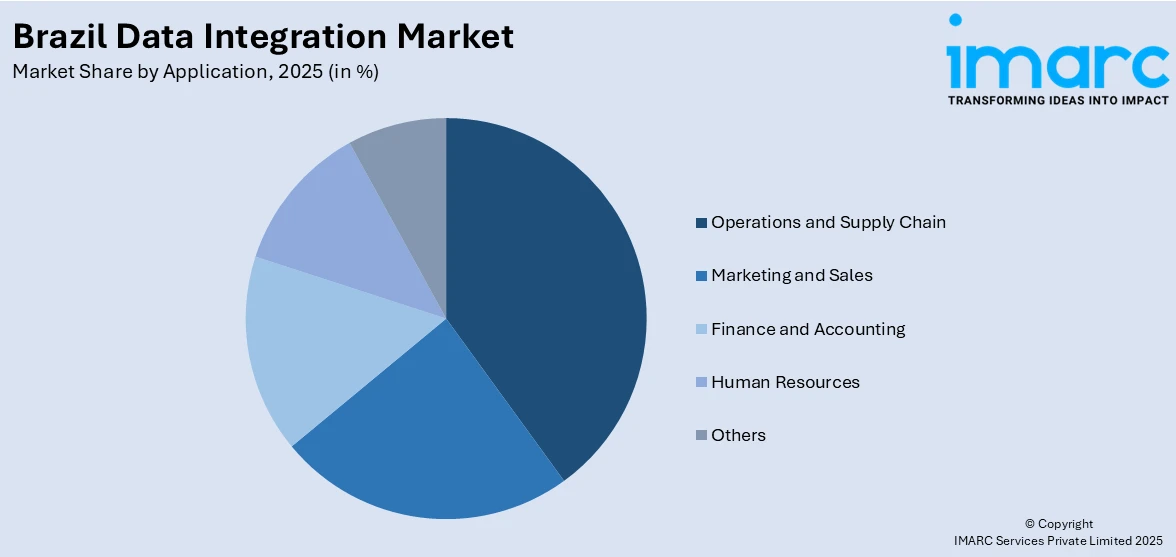

- By Application: Operations and supply chain prevails the market with a share of 32.9% in 2025, owing to growing enterprise investment in real-time visibility, logistics optimization, and end-to-end supply chain digitalization across manufacturing and retail sectors.

- By Region: Southeast comprises the largest region with 46.4% share in 2025, driven by the concentration of technology enterprises, financial institutions, and hyperscale data center infrastructure in São Paulo and Rio de Janeiro metropolitan areas.

- Key Players: Key players drive the Brazil data integration market by expanding cloud-native platform capabilities, investing in AI-powered automation, strengthening data governance frameworks, and forging strategic partnerships with hyperscalers to enhance real-time integration and ensure regulatory compliance across diverse enterprise segments.

To get more information on this market Request Sample

The Brazil data integration market is advancing as organizations across financial services, manufacturing, retail, and government sectors prioritize unified data management to enhance operational efficiency and regulatory compliance. A major driver shaping this progress is the country’s rapidly expanding cloud infrastructure, which provides the scalable foundation necessary for modern integration workloads. For instance, in September 2024, Microsoft announced a USD 2.7 Billion investment in cloud and AI infrastructure in Brazil, one of the largest technology commitments in Latin American history. This investment is establishing new availability zones and computing capacity that enable enterprises to deploy data integration platforms with lower latency and enhanced data residency compliance. The convergence of open finance mandates, growing e-commerce volumes, and Industry 4.0 manufacturing initiatives is creating sustained demand for data integration solutions that can unify structured and unstructured data across hybrid cloud environments. Policy frameworks and digital government programs are further reinforcing market momentum.

Brazil Data Integration Market Trends:

Cloud-Native Data Integration Platform Adoption

Brazilian enterprises are rapidly migrating to cloud-native data integration platforms as hyperscaler investments expand local infrastructure capacity. For instance, in May 2025, Patria Investimentos launched Omnia, a USD 1 Billion hyperscale data center platform focused on AI and cloud services in Brazil. The platform targets major global technology firms and utilizes exclusively renewable energy. Cloud-first strategies are enabling organizations to bypass legacy infrastructure constraints, supporting the Brazil data integration market growth through scalable, pay-as-you-go deployment models that reduce capital expenditure requirements.

Open Finance and Real-Time Data Integration Expansion

Brazil’s position as operator of the world’s largest open banking ecosystem is generating substantial demand for real-time data integration capabilities. For example, the Pix instant payment system processed over 63 Billion transactions in 2024, while the Open Finance framework surpassed 60 Million active consents. The launch of Pix Automático in June 2025 for recurring payments further intensifies requirements for automated data workflows. Financial institutions and fintechs are investing in API-centric integration architectures to unify payment, customer, and transactional data streams.

AI-Powered Supply Chain Data Management

Enterprises are embedding artificial intelligence and machine learning into supply chain data integration workflows to achieve real-time operational visibility. According to the 2024 ISG Provider Lens Supply Chain Services report for Brazil, organizations are implementing remote sensing devices, integrated software platforms, and control towers to harness supply chain data more effectively. Investments in ERP modernization, advanced planning systems, and predictive analytics are enabling manufacturers and logistics providers to optimize inventory management and demand forecasting across complex distribution networks.

Market Outlook 2026-2034:

Brazil’s data integration market is positioned for sustained expansion, supported by accelerating cloud migration, regulatory modernization, and enterprise-wide digital transformation initiatives. In accordance with this, increasing hyperscaler investments in local data center infrastructure, coupled with growing demand for AI-driven analytics and open finance compliance, are expected to drive higher adoption rates. As such, Brazil could attract over BRL 60 Billion in data center investments by 2030, with projects totaling up to 2GW. AI, cloud growth, tax incentives, and clean energy drive interest, despite high power costs and complex taxes challenges. Moreover, enterprise modernization programs spanning financial services, manufacturing, and public sector organizations will continue expanding the addressable market for data integration platforms across both cloud and hybrid deployment environments. The market generated a revenue of USD 367.89 Million in 2025 and is projected to reach a revenue of USD 988.36 Million by 2034, growing at a compound annual growth rate of 11.61% from 2026-2034.

.webp)

Brazil Data Integration Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Component |

Tools |

58.6% |

|

Organization Size |

Large Enterprises |

54.2% |

|

Deployment |

Cloud |

61.8% |

|

Application |

Operations and Supply Chain |

32.9% |

|

Region |

Southeast |

46.4% |

Component Insights:

- Tools

- Services

Tools dominates with a market share of 58.6% of the total Brazil data integration market in 2025.

The tools segment encompasses software platforms that automate extract, transform, and load processes alongside data quality management, metadata cataloging, and API-based connectivity. Brazilian enterprises are increasingly consolidating disparate data workloads onto multipurpose integration suites offered by major hyperscalers with São Paulo and Rio de Janeiro availability zones. Cloud-based ETL solutions now represent roughly two-thirds of deployments worldwide, a pattern mirrored in Brazil’s expanding digital economy.

Demand for unified toolchains spanning ingestion to machine learning is accelerating as enterprises seek to reduce vendor fragmentation and operational complexity. The growing adoption of open-source integration frameworks such as Apache Airflow, Airbyte, and dbt provides cost-effective alternatives that complement proprietary platforms. For example, in November 2025, SAP and Microsoft announced SAP Business Data Cloud Connect for Microsoft Fabric, enabling bi-directional, zero-copy sharing of semantically rich data products for advanced analytics and AI. This type of interoperability between enterprise resource planning systems and cloud analytics platforms is driving increased tool adoption across Brazilian financial services, retail, and manufacturing sectors.

Organization Size Insights:

- Large Enterprises

- Small and Medium-sized Enterprises

Large enterprises lead the market with a share of 54.2% of the total Brazil data integration market in 2025.

Large enterprises command the majority of market revenue by leveraging established IT departments, substantial budgets, and complex multi-system environments that necessitate sophisticated integration capabilities. These organizations maintain critical relationships with global technology providers and invest in enterprise-grade platforms to manage data flows across ERP, CRM, and financial systems.

The regulatory compliance landscape further reinforces large enterprise dominance, as LGPD enforcement and open finance mandates require robust data governance frameworks that only sizable organizations can readily implement. Accordingly, Itaú Unibanco’s plan to migrate 60–70% of its systems to AWS under a 10-year agreement signed in 2020, with 30% already on the cloud and a 45% target by year-end, highlights how major Brazilian corporations are investing in large-scale data integration and analytics infrastructure to support digital growth and cost efficiency. Large enterprises are also prioritizing managed security services, as integration platforms increasingly incorporate security and compliance automation.

Deployment Insights:

- Cloud

- On-premises

Cloud is the largest segment, accounting for 61.8% of the total Brazil data integration market in 2025.

Cloud-based data integration platforms are expanding rapidly as Brazilian organizations embrace scalable, flexible deployment models that reduce infrastructure costs and accelerate time-to-value. The elasticity of cloud environments supports rapid scaling for Open Finance APIs that must respond to third-party requests instantaneously. The substantial infrastructure growth also directly supports the adoption of integration-as-a-service offerings and data pipeline automation platforms.

Hyperscaler expansion in Brazil continues to reinforce cloud deployment momentum. An estimated 54% of Brazilian enterprises already operate across multiple public cloud platforms, surpassing regional norms and creating demand for vendor-neutral integration connectors and cross-cloud orchestration tools. Besides this, the government’s sovereign cloud initiative, which channels significant public investment into secure infrastructure for classified data processing, is further broadening the addressable market for cloud-based integration solutions.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Operations and Supply Chain

- Marketing and Sales

- Finance and Accounting

- Human Resources

- Others

Operations and supply chain holds the largest share at 32.9% of the total Brazil data integration market in 2025.

Operations and supply chain applications drive the largest share of data integration spending as Brazilian enterprises invest in end-to-end visibility, logistics optimization, and predictive analytics across complex distribution networks. The growing e-commerce sector, projected to reach BRL 224.7 Billion in 2025, is compelling logistics companies to modernize their data infrastructure for real-time inventory management and demand forecasting. Manufacturing facilities, particularly automotive clusters in Minas Gerais, are utilizing real-time SCADA analytics and augmented reality-assisted maintenance facilitated by edge computing nodes integrated with private networks.

The digital supply chain solutions market in Brazil is experiencing substantial investment as organizations adopt cloud-based platforms, ERP integration, and control tower architectures. Furthermore, rapid integration of the Pix instant payment rail, into supply chain payment workflows is creating additional demand for automated data pipelines that connect financial, logistics, and inventory management systems.

Regional Insights:

- Southeast

- South

- Northeast

- North

- Central-West

Southeast represents the leading region with a 46.4% share of the total Brazil data integration market in 2025.

The Southeast region dominates Brazil’s data integration market, anchored by São Paulo’s position as the country’s premier technology and financial hub. São Paulo commanded a substantial share of Brazil’s data center market capacity, supported by a dense enterprise base, and access to a skilled technology workforce. The metropolitan area hosts more than 40 existing and over 20 upcoming data center facilities, providing the physical infrastructure foundation for enterprise data integration deployments. São Paulo also concentrates 56% of Brazil’s fintech companies, creating intense demand for real-time data integration to support open finance compliance and digital payment processing.

Rio de Janeiro complements the region’s dominance with strategic port facilities and growing data center capacity. Belo Horizonte’s expanding industrial base, including the San Pedro Valley innovation community, adds further technology sector depth to the Southeast. The concentration of manufacturing, financial services, and technology headquarters in these metropolitan areas creates a self-reinforcing ecosystem where enterprise demand for integration platforms attracts hyperscaler investment, which in turn reduces latency and improves service availability for data integration workloads.

Market Dynamics:

Growth Drivers:

Why is the Brazil Data Integration Market Growing?

Regulatory Compliance and Data Governance Requirements

Brazil’s General Data Protection Law, the LGPD, has fundamentally transformed the data management landscape by imposing stringent requirements on how organizations collect, process, and transfer personal data. Enforcement by the ANPD continues to intensify, with mandatory breach notification requirements and expanded data subject rights compelling enterprises to implement comprehensive data governance frameworks. For example, in August 2024, the ANPD issued its International Data Transfer Regulation establishing Standard Contractual Clauses with a compliance deadline of August 2025, requiring organizations to map all cross-border data flows and update contractual arrangements. These evolving regulatory mandates are driving significant investment in data integration platforms that provide automated data lineage tracking, consent management, and policy enforcement across distributed systems.

Hyperscale Cloud Infrastructure Expansion

The unprecedented scale of hyperscaler investment in Brazilian data center infrastructure is creating a robust foundation for cloud-based data integration adoption. Global technology leaders are committing multi-billion-dollar capital expenditures to establish and expand availability zones across the country. Furthermore, the infrastructure buildout reduces latency, addresses data residency requirements, and enables enterprises to deploy integration workloads closer to their operational environments. For instance, the National Bank for Economic and Social Development launched a BRL 2 Billion credit line specifically for data center investments in September 2024, further accelerating capacity expansion. Brazil’s renewable energy generation mix of approximately 85% provides a sustainability advantage that attracts environmentally conscious technology investments and supports green data center certification programs.

Digital Transformation Across Industries

Broad-based digital transformation across Brazil’s industrial sectors is generating sustained demand for data integration platforms that connect legacy systems with modern cloud applications. Similarly, enterprise modernization is particularly pronounced in financial services, where open finance mandates and instant payment integration require seamless data flows across banking, insurance, and investment platforms. Likewise, e-commerce growth is driving backend integration projects that connect payment processors, inventory systems, and customer analytics platforms. The National Digital Transformation Index climbed from 3.3 in 2023 to 3.7 in 2024, indicating accelerating adoption that continues to trail mature economies and underscoring the substantial growth runway remaining for data integration investments.

Market Restraints:

What Challenges the Brazil Data Integration Market is Facing?

Complex regulatory environment

Brazil’s data integration market operates under a dense web of federal, state, and municipal regulations that affect data handling, logistics, taxation, and technology procurement. Compliance demands vary by sector, making it harder for organizations to deploy and scale integration platforms while staying aligned with financial services, healthcare, and telecom requirements. Furthermore, import duties, permitting processes, and currency fluctuations add uncertainty to long-term technology investments.

Data silos and legacy system fragmentation

Many Brazilian organizations continue to rely on fragmented legacy systems that limit seamless data integration. Weak digital maturity across parts of the enterprise sector leads to inconsistent data capture and modeling practices. Likewise, heightened scrutiny around data protection and stricter enforcement of privacy regulations have also made organizations cautious about sharing data internally, reinforcing siloed structures and raising the cost and duration of integration initiatives.

Skilled workforce shortages and implementation complexity

The adoption of data integration solutions is constrained by a shortage of professionals with expertise across cloud infrastructure, data engineering, governance, and security. Many companies struggle to translate advanced data and AI ambitions into practical system integration strategies. At the same time, the need for multidisciplinary skills increases project complexity, slows execution, and places upward pressure on implementation costs.

Competitive Landscape:

The Brazil data integration market exhibits moderate competition with several established global technology providers maintaining significant market positions. Companies are differentiating through expanded cloud-native capabilities, AI-powered automation features, and enhanced data governance functionalities. Strategic partnerships between enterprise software providers and hyperscalers are accelerating product innovation and expanding market reach. The growing adoption of open-source integration frameworks is introducing new competitive dynamics, as organizations seek flexible, vendor-neutral solutions. Providers are increasingly emphasizing local data residency compliance, Portuguese-language support, and regional customer success programs to strengthen their competitive positioning in Brazil’s expanding data integration landscape.

Recent Developments:

- In October 2025, Qlik launched a Brazil-based cloud region on AWS to support local AI, analytics, and data integration workloads. The move enables LGPD compliance, lowers latency, and improves performance for regulated sectors, while supporting public and private digital initiatives, local jobs, partnerships, and Portuguese-language customer support.

- In October 2025, Aduna accelerated commercialization of CAMARA-compliant network APIs in Brazil with Vivo, Claro, and TIM Brasil, targeting a Q4 2025 launch. The collaboration enables unified, secure access to fraud prevention and network intelligence APIs, simplifying enterprise integration and supporting Brazil’s fast-growing digital banking and mobile commerce ecosystem.

Brazil Data Integration Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Components Covered |

Tools, Services |

|

Organization Sizes Covered |

Large Enterprises, Small and Medium-sized Enterprises |

|

Deployments Covered |

Cloud, On-premises |

|

Applications Covered |

Operations and Supply Chain, Marketing and Sales, Finance and Accounting, Human Resources, Others |

|

Regions Covered |

Southeast, South, Northeast, North, Central-West |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Brazil Data Integration Market Report

The Brazil data integration market size was valued at USD 367.89 Million in 2025.

The Brazil data integration market is expected to grow at a compound annual growth rate of 11.61% from 2026-2034 to reach USD 988.36 Million by 2034.

Tools dominated the market with a share of 58.6%, driven by enterprise demand for comprehensive cloud-native integration platforms that consolidate ETL, data quality, and API management functionalities into unified toolchains.

Key factors driving the Brazil data integration market include intensifying LGPD compliance requirements, hyperscale cloud infrastructure expansion, accelerating digital transformation across industries, open finance mandates, and growing enterprise investment in AI-powered analytics.

Major challenges include complex multi-layered regulatory requirements, persistent data silos across legacy systems, skilled workforce shortages, high IT hardware import duties, currency volatility affecting procurement contracts, and implementation complexity across hybrid cloud environments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)