Brazil eHealth Market Size, Share, Trends and Forecast by Product, Services, End User, and Region, 2026-2034

Brazil eHealth Market Overview:

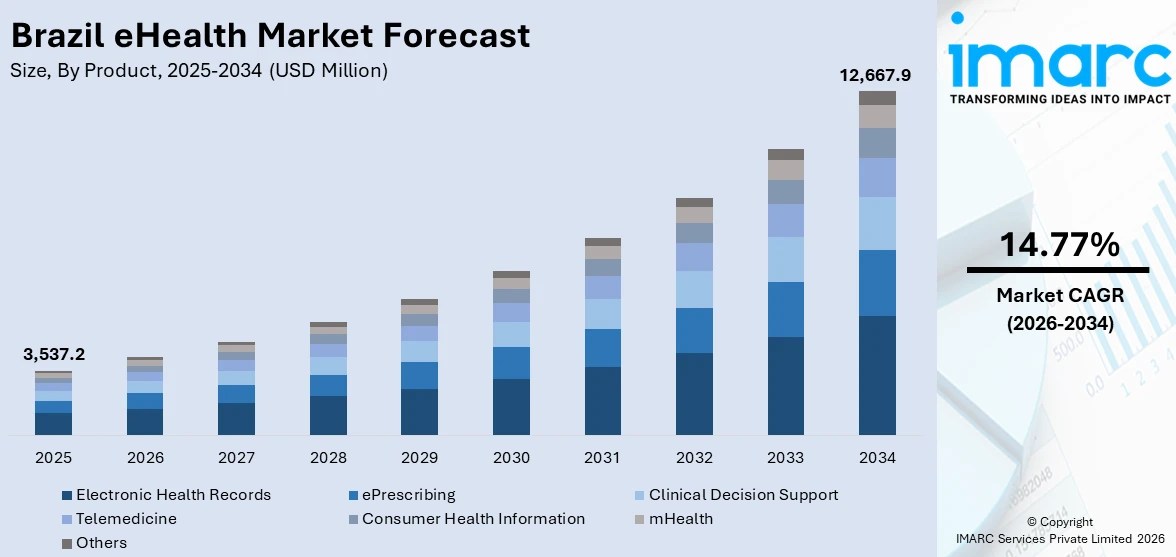

The Brazil eHealth market size reached USD 3,537.2 Million in 2025. The market is projected to reach USD 12,667.9 Million by 2034, exhibiting a growth rate (CAGR) of 14.77% during 2026-2034. The market is driven by government-led digital health infrastructure development through initiatives which facilitates seamless interoperability across healthcare facilities nationwide. Additionally, the rapid expansion of telemedicine services following permanent regulatory approval is significantly increasing accessibility to specialized care across Brazil's geographically diverse regions. Furthermore, the heightened adoption of electronic health records (EHRs) and cloud-based healthcare solutions by both public and private healthcare institutions is expanding the Brazil eHealth market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 3,537.2 Million |

| Market Forecast in 2034 | USD 12,667.9 Million |

| Market Growth Rate 2026-2034 | 14.77% |

Brazil eHealth Market Trends:

Government-Led Digital Health Infrastructure Development and National Integration

The Brazilian government is emerging as the primary catalyst for digital health transformation through comprehensive policy frameworks and substantial infrastructure investments. The National Digital Health Strategy (2020-2028), established by the Ministry of Health, outlines seven strategic priorities centered on digitalization across all three levels of healthcare delivery, specifically promoting electronic health record adoption and hospital management system integration throughout the country. At the foundation of this transformation is the National Health Data Network (RNDS), a groundbreaking initiative designed to create unified and interoperable health information systems connecting hospitals, clinics, laboratories, and primary care facilities across Brazil's vast geography. This network enables seamless patient data exchange at the national level while maintaining robust data privacy and security ideals in compliance with Brazil's General Data Protection Law (LGPD). In 2024, the São Paulo State Government, in partnership with Hospital das Clínicas da Faculdade de Medicina da Universidade de São Paulo, inaugurated the Centro Líder de Inovação em Saúde Digital, representing a flagship example of government-academic collaboration in digital health innovation. These coordinated efforts are establishing Brazil as a regional leader in public sector digital health transformation and creating a robust foundation for sustained market expansion.

To get more information on this market Request Sample

Rapid Expansion of Telemedicine and Remote Care Services

The telemedicine segment is experiencing unprecedented growth following Brazil's permanent legalization of telemedicine services in 2022, fundamentally transforming healthcare delivery across the nation's geographically dispersed population. The comprehensive and supportive regulatory framework has unleashed significant innovation and investment in virtual care platforms, with telehealth becoming particularly critical for Brazil's estimated 164 million citizens who rely exclusively on the Unified Health System (SUS). In June 2024, the World Bank-supported Salvador Social Project successfully deployed the Vida+ electronic registry system across 175 healthcare locations, surpassing initial deployment targets and demonstrating both the demand for and feasibility of large-scale digital health implementations. Mobile health (mHealth) applications are emerging as particularly promising, leveraging Brazil's rising number of mobile internet users to deliver remote vital sign monitoring to chronic disease management solutions, thereby supporting the Brazil eHealth market growth.

Growing Adoption of EHRs and Cloud-Based Healthcare Solutions

HER systems have become central to Brazil's healthcare digitalization strategy, with both government mandates and practical benefits driving accelerating adoption across public and private healthcare institutions. São Paulo's pioneering SIGA Health Information System, an open-source EHR platform, serves as an exemplary model, managing data for over 20 million patients from 700 health facilities annually while supporting 14 million registered patients with regular care visits. This implementation has yielded measurable improvements, including a major increase in patient visits and an improvement in patient satisfaction scores, validating the clinical and operational value proposition of comprehensive EHR adoption. The market is witnessing a decisive shift toward cloud-based EHR solutions. This preference reflects the compelling advantages of cloud infrastructure: dramatically reduced upfront capital requirements, enhanced accessibility enabling healthcare providers to access patient records from any location with internet connectivity, simplified system maintenance and automatic updates, and superior scalability to accommodate growing data volumes and user bases. In April 2025, plans were announced for Brazil's first fully digital public hospital, which will integrate artificial intelligence (AI), telemedicine, big data analytics, and 5G connectivity to create an advanced digital healthcare environment. Private healthcare institutions are similarly embracing digital transformation, with several major hospital groups obtaining international certifications for digital data management and paperless operations. Academic institutions are also contributing to EHR advancement through research partnerships and prototype development, fostering innovation in areas such as data security, system interoperability, and clinical decision support integration.

Brazil eHealth Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on product, services, and end user.

Product Insights:

- Electronic Health Records

- ePrescribing

- Clinical Decision Support

- Telemedicine

- Consumer Health Information

- mHealth

- Others

The report has provided a detailed breakup and analysis of the market based on the product. This includes electronic health records, ePrescribing, clinical decision support, telemedicine, consumer health information, mHealth, and others.

Services Insights:

- Monitoring

- Diagnostic

- Healthcare Strengthening

- Others

A detailed breakup and analysis of the market based on the services have also been provided in the report. This includes monitoring, diagnostic, healthcare strengthening, and others.

End User Insights:

Access the comprehensive market breakdown Request Sample

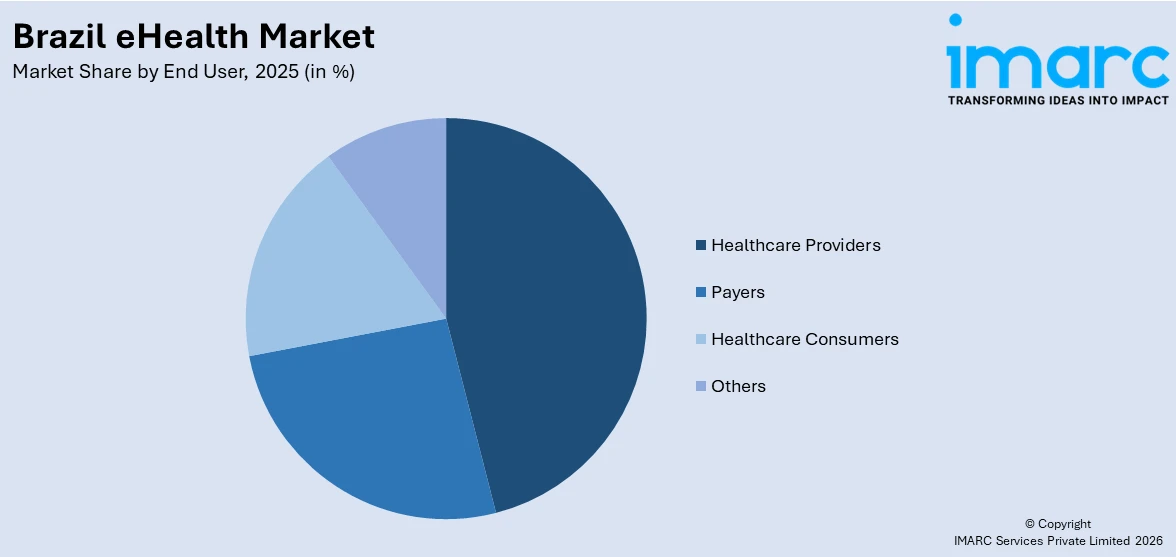

- Healthcare Providers

- Payers

- Healthcare Consumers

- Others

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes healthcare providers, payers, healthcare consumers, and others.

Regional Insights:

- Southeast

- South

- Northeast

- North

- Central-West

The report has also provided a comprehensive analysis of all the major regional markets, which include Southeast, South, Northeast, North, and Central-West.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Brazil eHealth Market News:

- July 2024: Philips Foundation, aiming to deliver quality healthcare access to 100 million individuals annually in underserved areas by 2030, along with SAS Brasil, announced the establishment of an innovation lab focused on digital health education. The program aims to enhance healthcare access in distant communities throughout Brazil. It offers top-notch training, utilizes ultrasound technology, and will function as a testing site for examining the effects of emerging healthcare technologies and promoting policy reforms to enhance primary care.

Brazil eHealth Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Electronic Health Records, ePrescribing, Clinical Decision Support, Telemedicine, Consumer Health Information, mHealth, Others |

| Services Covered | Monitoring, Diagnostic, Healthcare Strengthening, Others |

| End Users Covered | Healthcare Providers, Payers, Healthcare Consumers, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Brazil eHealth market performed so far and how will it perform in the coming years?

- What is the breakup of the Brazil eHealth market on the basis of product?

- What is the breakup of the Brazil eHealth market on the basis of services?

- What is the breakup of the Brazil eHealth market on the basis of end user?

- What is the breakup of the Brazil eHealth market on the basis of region?

- What are the various stages in the value chain of the Brazil eHealth market?

- What are the key driving factors and challenges in the Brazil eHealth market?

- What is the structure of the Brazil eHealth market and who are the key players?

- What is the degree of competition in the Brazil eHealth market?

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil eHealth market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil eHealth market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil eHealth industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)