Brazil Fertility Services Market Size, Share, Trends and Forecast by Cause of Infertility, Procedure, Service, End-User, and Region, 2026-2034

Brazil Fertility Services Market Summary:

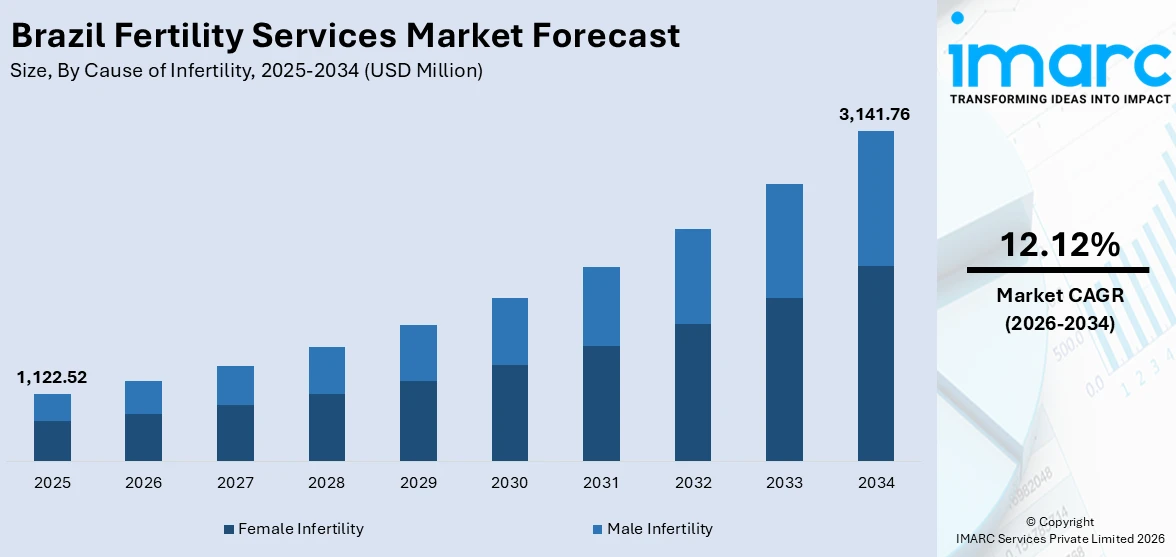

The Brazil Fertility Services market size was valued at USD 1122.52 Million in 2025 and is projected to reach USD 3141.76 Million by 2034, growing at a compound annual growth rate of 12.12% from 2026-2034.

The Brazil fertility services market is experiencing robust growth, underpinned by rising rates of female and male infertility, increasing societal acceptance of assisted reproductive technologies, and a supportive regulatory environment established by the Federal Medical Council (CFM). Delayed childbearing trends among urban professional women, a high incidence of conditions such as endometriosis and polycystic ovary syndrome, and the expanding network of specialized fertility clinics are collectively fueling consistent demand and expanding the Brazil fertility services market share across the country.

Key Takeaways and Insights:

- By Cause of Infertility: Female infertility dominates the market with a share of 62.5% in 2025, driven by the high and rising prevalence of endometriosis, polycystic ovary syndrome, and tubal factor infertility among Brazilian women, compounded by the trend of delayed childbearing that accelerates age-related decline in ovarian reserve.

- By Procedure: IVF with ICSI leads the market with a share of 46.8% in 2025, reflecting its established superiority in treating both severe male factor infertility and complex female infertility conditions, including cases involving poor ovarian response and advanced endometriosis, where conventional IVF alone is insufficient.

- By Service: Fresh non-donor is the largest segment with a market share of 31.4% in 2025, representing the most commonly adopted service type as couples seek to utilize their own gametes in initial treatment cycles before exploring donor or preservation alternatives.

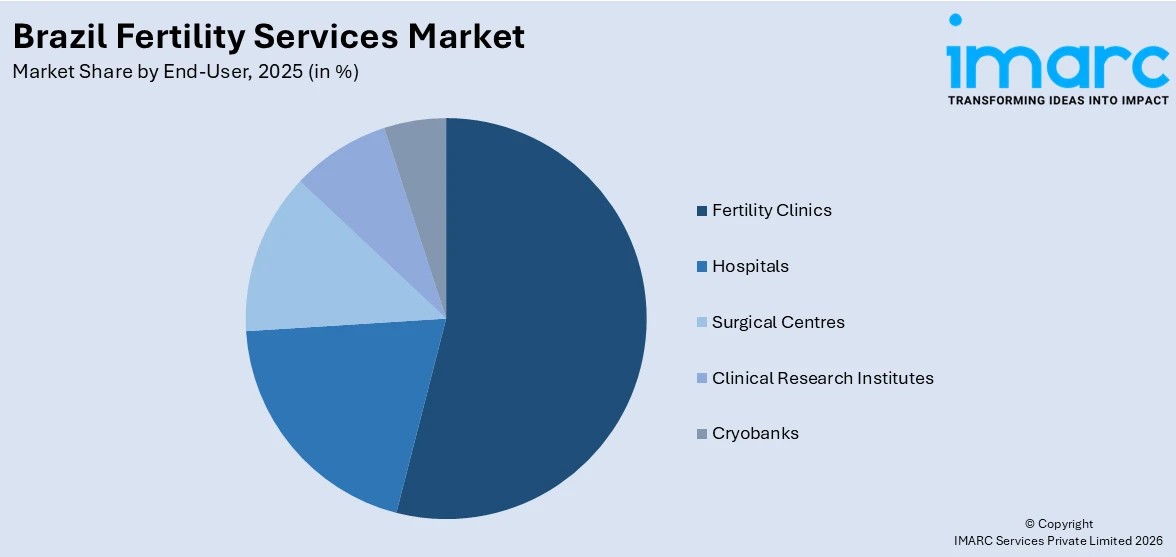

- By End-User: Fertility clinics exhibit a clear dominance in the market with 54.2% share in 2025, reflecting the highly privatized structure of Brazil’s assisted reproduction industry and the concentration of advanced reproductive technology infrastructure in specialized, standalone fertility centers rather than hospital settings.

- By Region: Southeast comprises the largest region with 58.7% share in 2025, driven by the dense concentration of Brazil’s assisted reproduction centers in São Paulo and Rio de Janeiro, higher per capita income, superior healthcare infrastructure, and the greatest availability of experienced reproductive medicine specialists in the country.

- Key Players: The market is competitive, featuring private clinics, reproductive technology centers, and international providers. Differentiation hinges on advanced technologies, success rates, cost transparency, and personalized care, with strategic partnerships and expanded service portfolios shaping market positioning and patient choice.

To get more information on this market Request Sample

The Brazil fertility services market is structurally shaped by the country’s unique combination of high infertility prevalence, a supportive ethical and regulatory framework, and a largely privatized service delivery model. Brazil is home to approximately 193 registered assisted reproduction centers (ARCs), as documented in ANVISA’s National Embryo Production System (SisEmbrio) reports, with the State of São Paulo alone accounting for 34.2% of all registered centers, followed by Minas Gerais at 11.9% and Rio Grande do Sul at 8.3%. The market is further driven by high clinical standards and strong success rates in assisted reproductive technologies, enhancing patient confidence. Inclusive regulations allowing access to fertility treatments regardless of marital status, sexual orientation, or gender identity expand the patient base. Moreover, growing awareness of reproductive health, rising demand for personalized fertility solutions, and advancements in assisted reproductive technologies also support market growth.

Brazil Fertility Services Market Trends:

Rising Adoption of AI-Powered Reproductive Technologies in Fertility Clinics

Artificial intelligence is rapidly transforming clinical decision-making and laboratory workflows across Brazil’s fertility services sector. AI-powered tools for embryo evaluation, oocyte quality assessment, and cycle optimization are gaining adoption as clinics seek to improve IVF success rates and differentiate their service offerings. As such, in April 2024, FertGroup Medicina Reproductiva, backed by XP Private Equity, partnered with Future Fertility to deploy VIOLET and MAGENTA AI-powered oocyte assessment software across its expanding clinic network, the first Brazilian fertility network to implement this technology, marking a significant milestone in the country’s integration of data-driven reproductive medicine into routine clinical practice.

Private Equity-Led Consolidation and Network Expansion

The Brazil fertility services market is witnessing accelerated consolidation driven by private equity investment, as investors capitalize on the fragmented clinic landscape and strong growth dynamics of the assisted reproduction sector. Private equity-backed networks are acquiring established clinics and building regional scale, enabling centralized investment in advanced laboratory technology, standardized clinical protocols, and integrated patient management systems. For example, XP launched a consolidation platform in Brazil’s assisted reproduction market, acquiring five clinics across major cities. The BRL 200 Million investment targets a fragmented, growing sector, strengthening market presence and creating a scalable fertility services network, illustrating the pace and ambition of this consolidation wave reshaping the market’s competitive structure.

Growing Demand for Social Fertility Preservation Among Working Women

An increasing number of Brazilian women are seeking elective fertility preservation, particularly oocyte cryopreservation, driven by the trend of delayed childbearing linked to higher educational attainment, career advancement, and financial planning. This demand is particularly pronounced in urban Southeast Brazil, where professional women are postponing motherhood into their mid-to-late thirties. The alignment of clinical evidence supporting vitrification success rates, combined with expanded clinic capacity and improving affordability, is creating a new patient segment for fertility clinics. Between 2020 and 2023, 284,232 embryos were frozen in Brazil according to ANVISA’s SisEmbrio report, with 67.2% concentrated in the Southeast region.

Market Outlook 2026-2034:

The Brazil fertility services market is positioned for sustained and robust expansion throughout the forecast period, anchored by rising infertility rates, a broadening patient population, and ongoing investments in advanced assisted reproductive technologies. The continued prevalence of endometriosis, PCOS, and age-related infertility, conditions that are particularly pronounced in Brazil, will sustain a durable demand base across IVF with ICSI, IUI, and fertility preservation services. Concurrently, private equity-led clinic consolidation is accelerating the modernization of fertility clinic networks, improving geographic access and standardizing clinical quality. WHO’s issuance of its first global guideline on infertility in November 2025 is expected to influence policy development across Brazil’s Ministry of Health, potentially guiding improvements in public sector access to ART. The parallel growth in medical tourism, with 80% of Brazilian fertility clinics already registering international patients, further augments revenue potential. These dynamics collectively underpin a strong and diversified market growth trajectory throughout the forecast period. The market generated a revenue of USD 1,122.52 Million in 2025 and is projected to reach a revenue of USD 3,141.76 Million by 2034, growing at a compound annual growth rate of 12.12% from 2026-2034.

Brazil Fertility Services Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Cause of Infertility |

Female Infertility |

62.5% |

|

Procedure |

IVF with ICSI |

46.8% |

|

Service |

Fresh Non-Donor |

31.4% |

|

End-User |

Fertility Clinics |

54.2% |

|

Region |

Southeast |

58.7% |

Cause of Infertility Insights:

- Male Infertility

- Female Infertility

Female infertility dominates the market with a market share of 62.5% of the total Brazil Fertility Services market in 2025.

Female infertility holds the dominant position in Brazil’s fertility services market, reflecting the high and rising burden of gynecological conditions that impair reproductive function across the country’s female population of reproductive age. The most prevalent causative factors include endometriosis, tubal factor infertility, polycystic ovary syndrome, and advanced maternal age, all of which are increasing in Brazilian women. A cross-sectional observational study conducted at a public primary care outpatient clinic in São Paulo, Brazil, the first such study in Latin America utilizing real-world data, found the prevalence of deep endometriosis at 6.4% in women of reproductive age and 34.2% in those presenting with pelvic pain, with infertility documented to be 6.5 times more common in women with endometriosis than in those without the condition.

The growing propensity of Brazilian women to delay childbearing has introduced age-related infertility as a significant driver within this segment. As women in urban Southeast Brazil increasingly pursue higher education and career development before starting families, the progressive decline in oocyte quality and ovarian reserve from the mid-thirties onward is producing a larger cohort of patients requiring advanced fertility interventions. Furthermore, Brazil recorded the fastest global increase in the age-standardized prevalence rate of uterine fibroids between 1990 and 2021, with an estimated annual percentage change of 1.23, according to a 2025 analysis of the Global Burden of Disease Study 2021 published in PLOS One, underscoring the expanding burden of female-specific reproductive conditions driving demand for fertility services across the country.

Procedure Insights:

- In Vitro Fertilization with Intracytoplasmic Sperm Injection (IVF with ICSI)

- Surrogacy

- In Vitro Fertilization Without Intracytoplasmic Sperm Injection (IVF without ICSI)

- Intrauterine Insemination (IUI)

- Others

IVF with ICSI leads the market with a share of 46.8% of the total Brazil Fertility Services market in 2025.

IVF with intracytoplasmic sperm injection (ICSI) occupies the leading position in Brazil’s fertility procedure landscape, a pattern consistent with the country’s history as an early adopter of this technique across its reproductive medicine centers. ICSI enables fertilization in cases of severe male factor infertility, including azoospermia, oligozoospermia, and asthenozoospermia, and is also the procedure of choice in cases involving poor ovarian response, advanced endometriosis, and prior fertilization failure with conventional IVF.

The dominance of IVF with ICSI is further reinforced by Brazil’s regulatory framework, which mandates that all ICSI-performing clinics register with ANVISA’s National Embryo Production System (SisEmbrio). This mandatory registration ensures consistent quality monitoring and has supported the development of a robust, accountable clinical ecosystem for advanced ART procedures. Brazil’s national IVF fertilization success rate of 77.77% in women under 35 years, above the international benchmark of 65%, demonstrates that ICSI cycles performed in Brazilian fertility centers achieve internationally competitive clinical outcomes, a quality assurance that encourages continued patient confidence and utilization of this procedure as the preferred approach to achieving successful conception.

Service Insights:

- Fresh Non-Donor

- Frozen Non-Donor

- Egg and Embryo Banking

- Fresh Donor

- Frozen Donor

Fresh non-donor accounts for the highest revenue with a market share of 31.4% of the total Brazil Fertility Services market in 2025.

Fresh non-donor services represent the most commonly adopted first-line treatment path for infertile couples in Brazil, as patients and clinicians typically prefer to utilize autologous gametes, fresh oocytes retrieved and immediately fertilized during the same cycle, before exploring donor or cryopreserved alternatives. This approach aligns with both clinical protocols and patient psychological preferences, as the use of one’s own genetic material carries significant personal and cultural importance within Brazilian society. Fertility clinics across Brazil have invested substantially in ovarian stimulation protocols and real-time oocyte retrieval capabilities to support the high throughput of fresh non-donor cycles, cementing this service type’s position as the market’s largest revenue contributor.

The continued primacy of fresh non-donor services is also shaped by Brazil’s regulatory framework governing gamete use and embryo cryopreservation. While the freeze-all strategy is growing in adoption for clinical reasons, particularly to avoid ovarian hyperstimulation syndrome and optimize endometrial receptivity, many cycles in Brazil still incorporate fresh embryo transfer as the initial preferred approach. The success rate achieved through fresh non-donor cycles remains a key clinical benchmark, underscores the strong clinical foundation supporting this service type, and the ongoing investment by private equity-backed fertility networks in advanced laboratory infrastructure is expected to further improve fresh cycle outcomes over the forecast period.

End-User Insights:

Access the comprehensive market breakdown Request Sample

- Fertility Clinics

- Hospitals

- Surgical Centres

- Clinical Research Institutes

- Cryobanks

Fertility clinics are the largest segment with a market share of 54.2% of the total Brazil Fertility Services market in 2025.

Fertility clinics are the dominant end-user in Brazil’s fertility services market, a structural reality rooted in the country’s highly privatized ART delivery model. Unlike several European countries where IVF is partially covered by public health systems, Brazil’s SUS does not fund high-complexity ART procedures, making specialized private fertility clinics the primary gateway to advanced reproductive care for the vast majority of patients. Specialized fertility clinics offer the full spectrum of services, including IVF with ICSI, oocyte cryopreservation, preimplantation genetic testing, and embryo banking, under one integrated clinical and laboratory roof, providing a patient-centered experience that hospitals and surgical centers cannot match in terms of specialization and scale.

The ongoing consolidation of Brazil’s fertility clinic sector under private equity-backed networks is accelerating the modernization of the end-user landscape. Likewise, increasing investment signals a broader trend of technology-driven differentiation among specialized fertility clinics, which are increasingly positioned as premium, evidence-based centers of reproductive excellence capable of attracting both domestic patients and a growing share of international medical tourists seeking high-quality ART services at significantly lower cost than comparable procedures in the United States or Western Europe.

Region Insights:

- Southeast

- South

- Northeast

- North

- Central-West

Southeast exhibits a clear dominance with a 58.7% share of the total Brazil Fertility Services market in 2025.

The Southeast region dominates Brazil’s fertility services market, serving as the country’s economic, demographic, and healthcare hub. It hosts the highest concentration of assisted reproduction centers, advanced IVF laboratories, and cryogenic storage facilities, making it the most clinically equipped region in Latin America. This concentration supports a significant share of the nation’s fertility activities, including embryo storage and complex reproductive procedures, highlighting the region’s leadership in technological capability, infrastructure, and clinical expertise.

The Southeast’s market dominance is further reinforced by income-driven demand dynamics: higher per capita income in São Paulo, Rio de Janeiro, and Minas Gerais enables households to access premium private fertility services without financial support from the public health system. Brazil’s fertility care is predominantly privately financed, and the affluence of Southeast Brazil’s urban professional class supports sustained utilization of high-cost ART procedures. For example, Chedid Grieco Fertility Clinic in São Paulo, helped deliver 8,780 babies. Backed by a BRL-level international license held by only eight clinics outside the U.S., it offers cost-effective IVF and In Vitro Maturation treatments. The region is also the epicenter of Brazil’s medical tourism in fertility care, with Brazilian fertility clinics having registered international patients, particularly from the United States and Angola, who are drawn to the Southeast’s combination of world-class clinical expertise and significantly lower treatment costs compared to developed-country markets.

Market Dynamics:

Growth Drivers:

Why is the Brazil Fertility Services Market Growing?

Rising Burden of Female Infertility Conditions

The escalating prevalence of female infertility conditions is a primary structural driver of growth in Brazil’s fertility services market. Endometriosis, polycystic ovary syndrome, tubal factor infertility, and age-related decline in ovarian reserve collectively affect a large and growing segment of Brazil’s 53 million women of reproductive age. Clinical observational study in São Paulo highlighted a significant prevalence of deep endometriosis among reproductive-age women, particularly those experiencing pelvic pain, with infertility notably more common among affected patients. Brazil has also seen a marked rise in uterine fibroid prevalence over recent decades, further enlarging the potential patient base for fertility services. Coupled with delayed childbearing trends among urban women pursuing higher education and careers, these factors are steadily expanding demand for comprehensive fertility evaluation, treatment, and preservation services nationwide.

Enabling Regulatory Framework and Expanding Inclusivity of ART Access

Brazil’s regulatory environment for assisted reproductive technologies is among the most inclusive in Latin America, providing a stable and legally permissive foundation for market growth. The Federal Medical Council’s Resolution No. 2.320/2022, the most recent governing framework for ART in Brazil, permits access to fertility treatments regardless of marital status, sexual orientation, or gender identity, substantially broadening the patient pool eligible for IVF, IUI, and surrogacy services. Brazil is also one of the few countries globally to permit anonymous egg donation under ANVISA oversight, providing clinics with a broad donor pool while maintaining regulatory compliance. The National Justice Council’s Provision No. 83 of 2019 established clear civil registration procedures for children born through ART, providing legal certainty that encourages patients to pursue fertility treatment with confidence. These enabling legal frameworks reduce adoption barriers and sustain demand among diverse family-building populations, including same-sex couples, single parents, and individuals pursuing fertility preservation before medical treatments such as chemotherapy.

Technology-Driven Improvements in IVF Success Rates and Patient Experience

Continuous innovation in assisted reproductive technology is expanding the market by improving clinical outcomes, reducing treatment cycle failures, and attracting new patient cohorts who previously considered ART a last resort. Advanced embryo evaluation systems, AI-powered oocyte quality assessment, vitrification techniques, and preimplantation genetic testing are collectively raising fertilization and live birth rates across Brazilian fertility clinics. The adoption of time-lapse imaging and AI-driven embryo selection tools is enabling more personalized treatment planning, reducing the number of failed cycles and associated costs for patients. Private equity-backed clinic consolidation is accelerating the diffusion of these technologies across Brazil’s fertility clinic network. Improved success rates and patient-centric digital tools are reducing psychological barriers to ART adoption and encouraging earlier treatment-seeking behavior among infertile couples nationwide.

Market Restraints:

What Challenges the Brazil Fertility Services Market is Facing?

Prohibitive Costs and Absence of Public Health System Coverage for Advanced ART

The high out-of-pocket cost of advanced fertility services remains the primary barrier to access in Brazil’s market, as the Unified Health System does not cover high complexity assisted reproductive procedures such as IVF and ICSI. As a result, most patients must finance treatments independently, with private health insurance rarely offering comprehensive reimbursement. This financial burden disproportionately affects lower-income populations, particularly in less affluent regions, limiting equitable access to care. Consequently, market growth is largely concentrated among higher-income groups, restricting broader penetration across Brazil’s diverse socioeconomic landscape and constraining the overall addressable market for fertility services nationwide.

Severe Geographic Inequality in Fertility Services Infrastructure

Brazil’s fertility services infrastructure is heavily concentrated in its wealthiest states, resulting in pronounced geographic disparities in access to assisted reproductive technologies. The majority of specialized clinics and advanced laboratories are located in the Southeast and South, while large areas of the North and other underserved regions have very limited availability of fertility centers. This uneven distribution forces many patients to travel significant distances to obtain diagnostic evaluations or advanced procedures such as IVF. The associated financial, logistical, and time burdens restrict participation among patients outside major urban hubs, limiting equitable access and slowing the development of a more geographically balanced national fertility services market.

Regulatory Uncertainty and Absence of Comprehensive Legislation for ART

Brazil’s ART sector operates without comprehensive national legislation, relying instead on Federal Medical Council (CFM) ethical resolutions and ANVISA technical guidelines as its primary governance framework. While CFM resolutions provide ethical guidance for practitioners, they lack the force of law, creating regulatory ambiguity in contested areas such as surplus embryo disposition, commercial surrogacy, and the rights of donor-conceived children to know their genetic identity. This absence of formal legislation limits institutional investor confidence in certain market segments and creates ongoing uncertainty for patients and clinicians navigating complex family-building scenarios. Pending legislative bills related to ART regulation have been repeatedly shelved by the Brazilian Congress, perpetuating a regulatory environment that may slow the entry of new service providers and the introduction of novel reproductive technologies requiring clear legal frameworks.

Competitive Landscape:

The Brazil fertility services market presents a moderately fragmented competitive landscape undergoing rapid consolidation through private equity investment. Standalone fertility clinics historically dominated the market, but the emergence of private equity-backed networks is reshaping the competitive structure by creating scale advantages in laboratory technology, clinical standardization, and operational efficiency. Key strategic priorities include AI-driven treatment optimization, geographic network expansion into underserved markets, and international patient acquisition through medical tourism channels. The concentrated geographic distribution of clinical expertise in the Southeast creates both competitive barriers and expansion opportunities for networks targeting secondary cities and underserved Brazilian states.

Recent Developments:

- In November 2025, the European Investment Bank signed a EUR 20 Million loan with Overture Life to advance automation and AI-driven IVF technologies. The funding supports R&D, manufacturing scale-up, and commercialization of the DaVitri platform, which has already launched in Brazil following regulatory clearances. Backed by the InvestEU programme, the initiative strengthens fertility innovation in Europe while expanding access and technological capacity in Brazil’s growing assisted reproduction market.

- In May 2025, Oya Care, founded by Stephanie von Staa Toledo, continued expanding its women’s health platform in Brazil. After raising USD 3 Million in seed funding, the startup reported strong quarterly revenue growth, driven primarily by fertility procedures like egg freezing, while broadening services into obstetrics, gynecology, and menopause care.

Brazil Fertility Services Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Causes of Infertility Covered |

Male Infertility, Female Infertility |

|

Procedures Covered |

IVF with ICSI, Surrogacy, IVF without ICSI, IUI, Others |

|

Services Covered |

Fresh Non-Donor, Frozen Non-Donor, Egg and Embryo Banking, Fresh Donor, Frozen Donor |

|

End-Users Covered |

Fertility Clinics, Hospitals, Surgical Centres, Clinical Research Institutes, Cryobanks |

|

Regions Covered |

Southeast, South, Northeast, North, Central-West |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Brazil Fertility Services Market Report

The Brazil Fertility Services market size was valued at USD 1,122.52 Million in 2025.

The Brazil Fertility Services market is expected to grow at a compound annual growth rate of 12.12% from 2026-2034 to reach USD 3,141.76 Million by 2034.

Female infertility dominated the market with a share of 62.5%, reflecting the high prevalence of endometriosis, PCOS, tubal factor infertility, and age-related ovarian decline among Brazilian women of reproductive age, compounded by delayed childbearing trends in urban Brazil.

Key factors driving the Brazil Fertility Services market include rising female infertility conditions, an inclusive regulatory framework permitting ART access regardless of marital status or sexual orientation, ongoing AI-driven improvements in IVF success rates, private equity-led clinic network expansion, and growing medical tourism from international patients seeking quality ART at lower cost.

Major challenges include prohibitive out-of-pocket costs due to the absence of public health system coverage for advanced ART, severe geographic concentration of fertility services infrastructure in the Southeast, and regulatory uncertainty stemming from the lack of comprehensive national legislation governing assisted reproduction practices.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)