Brazil Health Insurance Market Size, Share, Trends and Forecast by Provider, Type, Plan Type, Demographics, Provider Type, and Region, 2026-2034

Brazil Health Insurance Market Size, Share, Trends & Forecast (2026-2034)

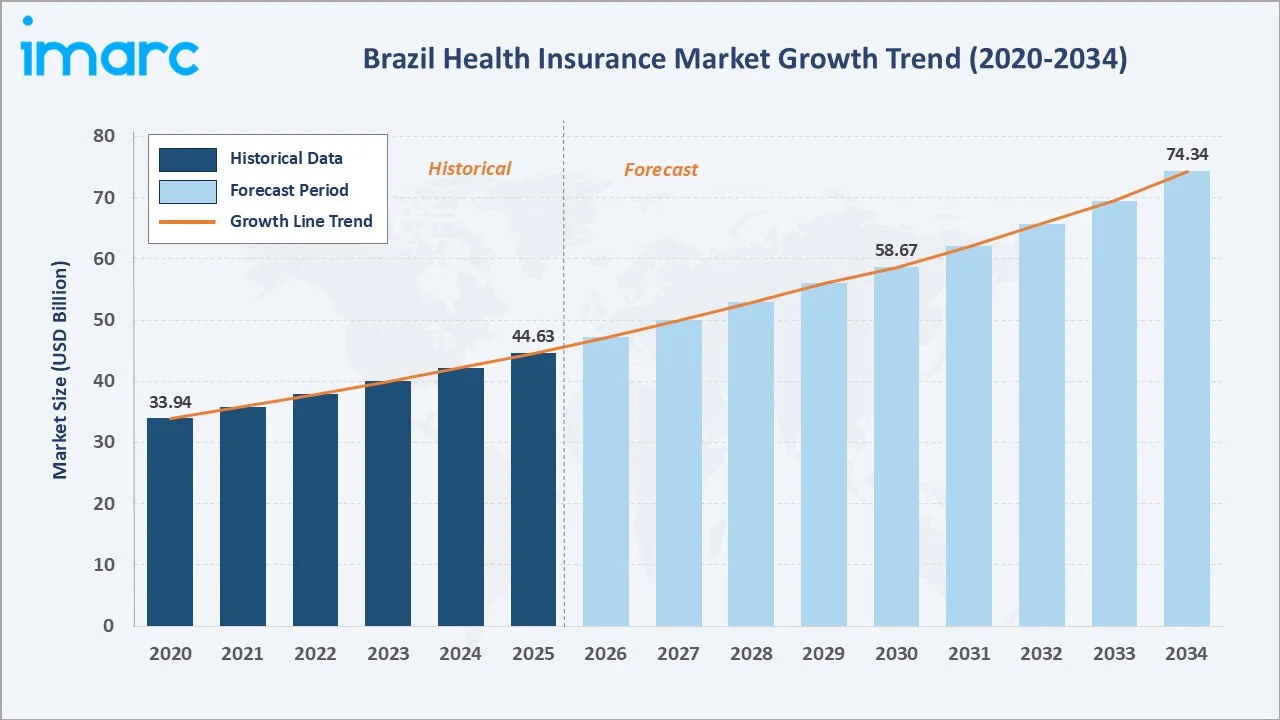

The Brazil health insurance market reached USD 44.63 Billion in 2025 and is projected to reach USD 74.34 Billion by 2034, growing at a CAGR of 5.63% during 2026-2034. The market is driven by rising healthcare costs, growing demand for private coverage, regulatory reforms, and Brazil's expanding middle-class workforce.

Private Providers dominate at 68.0%, Life-Time Coverage leads at 57.0%, and the Southeast region accounts for 42.0% of total market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 44.63 Billion |

|

Forecast Market Size (2034) |

USD 74.34 Billion |

|

CAGR (2026-2034) |

5.63% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Provider |

Private Providers (68.0%, 2025) |

|

Dominant Type |

Life-Time Coverage (57.0%, 2025) |

|

Leading Region |

Southeast (42.0%, 2025) |

The market expanded from USD 33.94 Billion in 2020 to USD 44.63 Billion in 2025 anchored at USD 58.67 Billion in 2030 and forecast to reach USD 74.34 Billion by 2034. Structural SUS capacity constraints and rising medical cost inflation are the primary demand accelerators sustaining this growth trajectory.

To get more information on this market, Request Sample

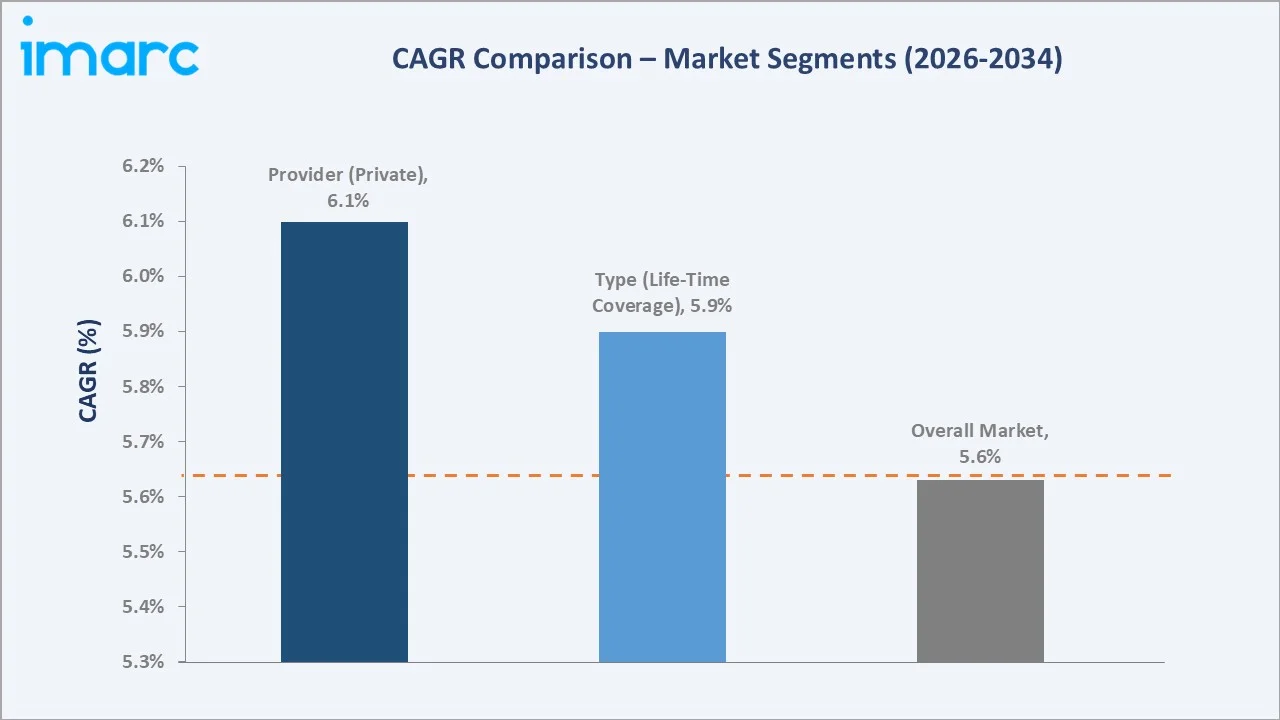

Life-Time Coverage grows at ~5.9% CAGR as Brazil's ageing population increases demand for permanent health protection. Private Providers grow fastest at ~6.1% CAGR driven by employer-sponsored corporate plan expansion, bancassurance channel growth, and digital health platform integration.

Executive Summary

The Brazil health insurance market reached USD 44.63 Billion in 2025, representing Latin America's largest supplementary health insurance market, driven by structural healthcare demand growth and progressive private coverage expansion across employer-sponsored and individual plan segments. The market is projected to reach USD 74.34 Billion by 2034.

Private Providers at 68.0% dominate by capturing employer-sponsored plans, corporate group insurance, and cooperative health networks. Life-Time Coverage at 57.0% leads through consumer preference for permanent protection. The Southeast at 42.0% leads regionally through Brazil's concentration of economic activity and private hospital infrastructure.

Key Market Insights

|

Insight |

Data |

|

Dominant Provider |

Private Providers - 68.0% share (2025) |

|

Dominant Type |

Life-Time Coverage - 57.0% market share (2025) |

|

Leading Region |

Southeast - 42.0% market share (2025) |

|

Market Opportunity |

Digital health platforms; micro-insurance for informal workers; Northeast expansion; senior citizen plans |

Key Analytical Observations Supporting The Above Data:

- Private Providers at 68.0%: Private providers dominate through employer-sponsored group plans, individual supplementary policies, and cooperative networks. Growing formal workforce participation and corporate benefit competition reinforce private provider market leadership across all five Brazilian regions.

- Life-Time Coverage at 57.0%: Life-time coverage leads due to consumer preference for comprehensive, permanent protection against chronic illness and hospitalisation. Brazil's ageing demographic profile and rising incidence of non-communicable diseases reinforce lifetime plan demand over term alternatives.

- Southeast at 42.0%: The Southeast leads through São Paulo and Rio de Janeiro's concentration of corporate headquarters, higher per-capita incomes, and Brazil's highest density of private hospital and diagnostic infrastructure, creating a structurally larger insurable population base.

Brazil Health Insurance Market Overview

The Brazil health insurance market encompasses private and public supplementary health coverage plans across individual, family, and group modalities, regulated by the Agência Nacional de Saúde Suplementar (ANS). The market serves over 52.9 million beneficiaries in health plans as of mid-2025, complementing the SUS universal public health system.

The ecosystem integrates private insurers, cooperative health networks, public plan administrators, hospital networks, diagnostic laboratories, specialist clinics, and employer benefit managers. Macroeconomic factors include rising healthcare costs, SUS infrastructure limitations, workforce formalisation, and population ageing driving supplementary coverage demand.

Market Dynamics

To evaluate market opportunities, Request Sample

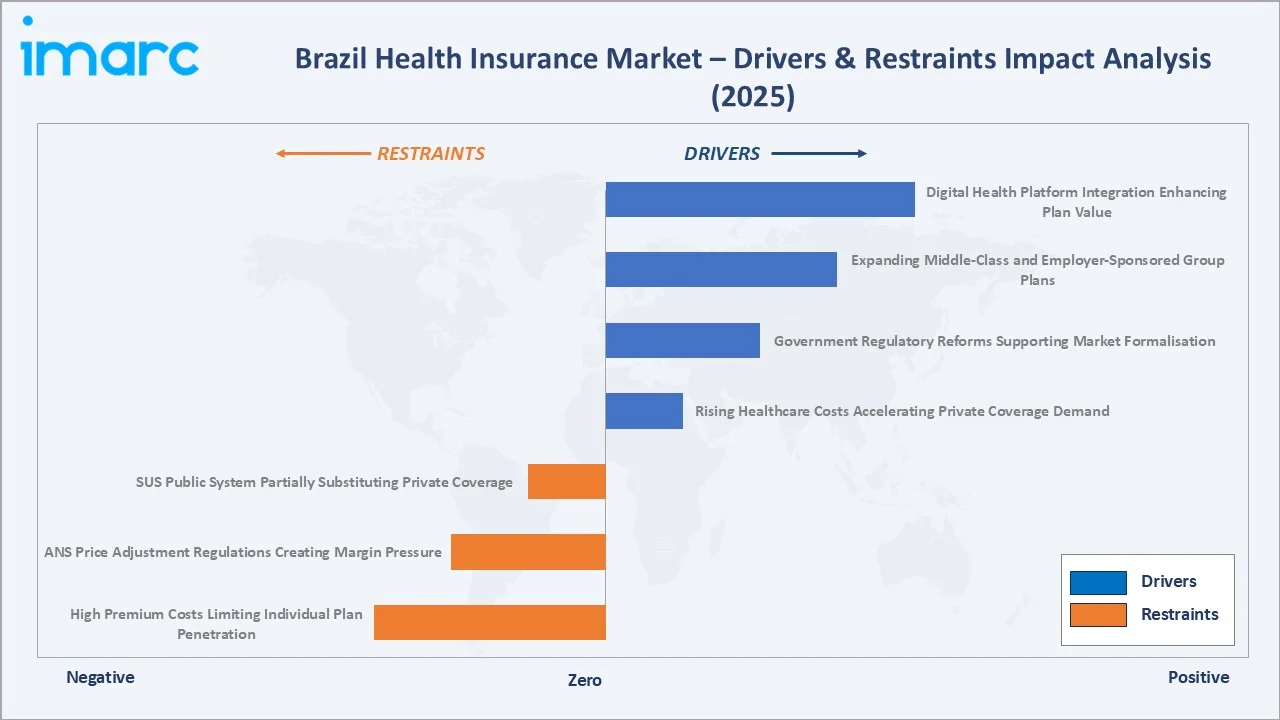

Market Drivers

- Rising Healthcare Costs Accelerating Private Coverage Demand: Escalating medical treatment costs, specialist fees, and hospital admission rates compel households and employers to seek supplementary private insurance. Persistent SUS capacity constraints increase perceived value of private plans, directly driving new policyholder acquisition across all income brackets.

- Government Regulatory Reforms Supporting Market Formalisation: ANS regulatory updates mandating minimum coverage standards, portability rules, and price-adjustment frameworks increase consumer trust in private health plans. Simplified plan and micro-insurance regulations extend market reach to previously underserved lower-income and informal-sector segments.

- Expanding Middle-Class and Employer-Sponsored Group Plans: Brazil's expanding formal workforce creates sustained demand for employer-sponsored group health plans. Corporations increasingly offer health insurance as a key employee retention benefit, expanding policyholder volumes and boosting private insurer premium revenues across the corporate segment.

- Digital Health Platform Integration Enhancing Plan Value: Integration of telemedicine, digital consultations, and health monitoring within private insurance plans improves service delivery and member engagement. Digital-first plan features attract younger consumers and lower claims management costs, supporting sustainable premium growth across all plan tiers.

Market Restraints

- High Premium Costs Limiting Individual Plan Penetration: Elevated individual health insurance premiums relative to average household income restrict market penetration among lower and lower-middle income segments. ANS-regulated annual adjustment caps further constrain insurer pricing flexibility, increasing policy cancellation rates during periods of high medical cost inflation.

- ANS Price Adjustment Regulations Creating Insurer Margin Pressure: ANS-regulated caps on individual plan annual premium adjustments limit insurer ability to fully pass through medical inflation to policyholders. This creates earnings volatility when healthcare utilisation rises faster than approved rate adjustments, dampening capacity expansion investment.

- SUS Public System Partially Substituting Private Coverage: Brazil's SUS public health system provides constitutionally mandated universal free healthcare, partially substituting private insurance for lower-income households. SUS availability limits the addressable market for private plans among segments relying primarily on public facilities for routine and emergency care.

Market Opportunities

- Micro-Insurance and Simplified Plan Formats for Informal Workers: Simplified plan regulations and micro-insurance formats enable access for previously uninsured informal-sector workers and low-income households, extending total addressable market well beyond formal employment boundaries across Brazil's five regions.

- Northeast and North Regional Expansion into Underpenetrated Markets: The Northeast at 16.5% and North at 10.0% represent Brazil's most underpenetrated health insurance regions, offering substantial growth potential as workforce formalisation and income growth progressively expand the insurable population base.

Market Challenges

- Vertical Integration Race Creating Structural Cost Disadvantage for Non-Integrated Insurers: Hapvida and GNDI's vertically integrated hospital and diagnostic network model creates 15-20% lower medical cost ratios versus non-integrated operators. Non-integrated insurers face escalating network cost pressure as hospital consolidation reduces their negotiating leverage over service costs.

- Medical Cost Inflation Exceeding ANS-Regulated Premium Adjustments: Medical cost inflation driven by new treatment technologies, ageing population utilisation, and pharmaceutical cost increases consistently exceeds ANS-regulated individual plan adjustment caps. This structural gap creates persistent loss-ratio pressure for insurers serving the individual plan segment.

Emerging Market Trends

1. Telemedicine-Integrated Health Plans Redefining Service Delivery

Insurers are embedding telemedicine consultations and digital triage into standard plan benefits, reducing in-person claims frequency and lowering operational costs. In 2025, leading insurers reported 25-30% of consultations conducted via telemedicine, becoming a primary plan differentiation factor in competitive corporate and individual market segments.

2. Micro-Insurance and Simplified Plan Formats Expanding Market Access

Simplified plan regulations and micro-insurance formats are enabling access for previously uninsured informal-sector workers and low-income households. These formats offer limited but meaningful hospital coverage at accessible price points, extending the total addressable market beyond formal employment and driving beneficiary growth in the Northeast and North.

3. Consolidation Among Private Providers Creating Integrated Health Systems

Major operators are pursuing vertical integration by acquiring hospital networks, diagnostic laboratories, and specialist clinics to control the healthcare delivery chain. Integrated health systems create network density advantages, reduce third-party claims costs, and reshape the competitive landscape toward large integrated operators with structurally superior margins.

4. Corporate Wellness Plans and Preventive Care Benefit Expansion

Employers are expanding group health plan benefits to include wellness programmes, mental health coverage, and chronic disease management. Preventive care integration reduces hospitalisation rates and long-term claims costs, creating a positive feedback loop for plan sustainability and reinforcing health insurance as a primary corporate talent retention benefit.

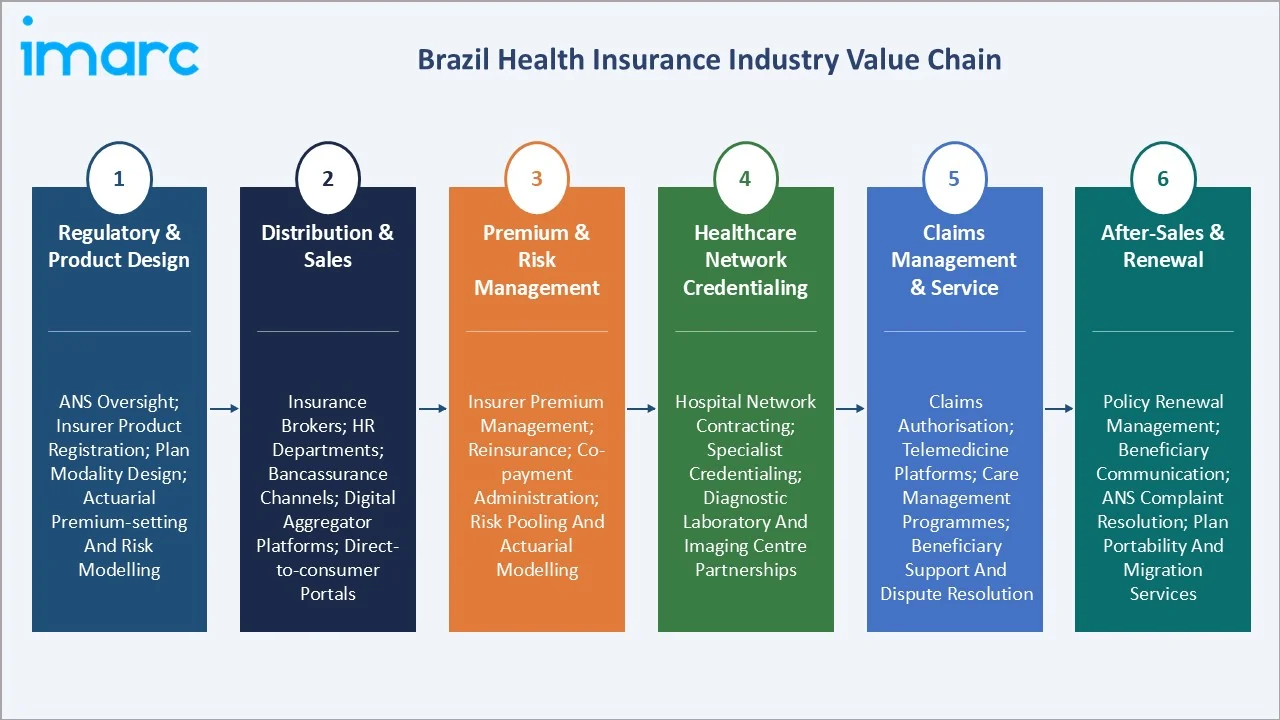

Industry Value Chain Analysis

The Brazil health insurance value chain integrates regulatory compliance, product design, premium collection, network credentialing, claims management, and reinsurance arrangements. ANS oversight governs each stage from product registration to beneficiary relations, ensuring minimum coverage standards across all plan modalities and provider types.

|

Stage |

Key Participants |

|

Regulatory & Product Design |

ANS oversight; insurer product registration; plan modality design; actuarial premium-setting and risk modelling |

|

Distribution & Sales |

Insurance brokers; HR departments; bancassurance channels; digital aggregator platforms; direct-to-consumer portals |

|

Premium & Risk Management |

Insurer premium management; reinsurance; co-payment administration; risk pooling and actuarial modelling |

|

Healthcare Network Credentialing |

Hospital network contracting; specialist credentialing; diagnostic laboratory and imaging centre partnerships |

|

Claims Management & Service |

Claims authorisation; telemedicine platforms; care management programmes; beneficiary support and dispute resolution |

|

After-Sales & Renewal |

Policy renewal management; beneficiary communication; ANS complaint resolution; plan portability and migration services |

The distribution and sales tier is the most commercially dynamic stage, with bancassurance cross-selling, digital aggregator platforms, and employer HR benefit channels competing for policyholder acquisition. The claims management tier is experiencing the most rapid technology transition with AI-driven adjudication and telemedicine triage replacing traditional workflows.

Technology Landscape in the Brazil Health Insurance Industry

AI-Driven Underwriting and Claims Management Technology

Artificial intelligence applications in underwriting risk scoring, fraud detection, and claims adjudication are improving operational efficiency and loss ratio management. AI-powered predictive modelling and automated claims processing reduce administrative costs, improve turnaround times, and support insurer profitability across individual and group plan segments.

Digital Health and Telemedicine Platform Technology

Telemedicine platform integration within health plan benefits is transforming service delivery by enabling remote consultations, digital prescriptions, and chronic disease monitoring. In 2025, Hapvida and SulAmérica reported that embedded telemedicine reduced emergency-room utilisation by 15-20% among members actively using digital health services.

Health Data Analytics and Population Health Management

Advanced health data analytics enables insurers to identify high-risk policyholder cohorts, deploy targeted preventive care interventions, and manage chronic disease populations more cost-effectively. Population health management platforms are becoming core operational competencies for leading Brazilian health insurers seeking to control long-term claims costs.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Provider |

Private Providers |

68.0% |

2025 |

|

Type |

Life-Time Coverage |

57.0% |

2025 |

|

Plan Type |

🔒 |

🔒 |

2025 |

|

Demographics |

🔒 |

🔒 |

2025 |

|

Provider Type |

🔒 |

🔒 |

2025 |

|

Region |

Southeast |

42.0% |

2025 |

By Provider

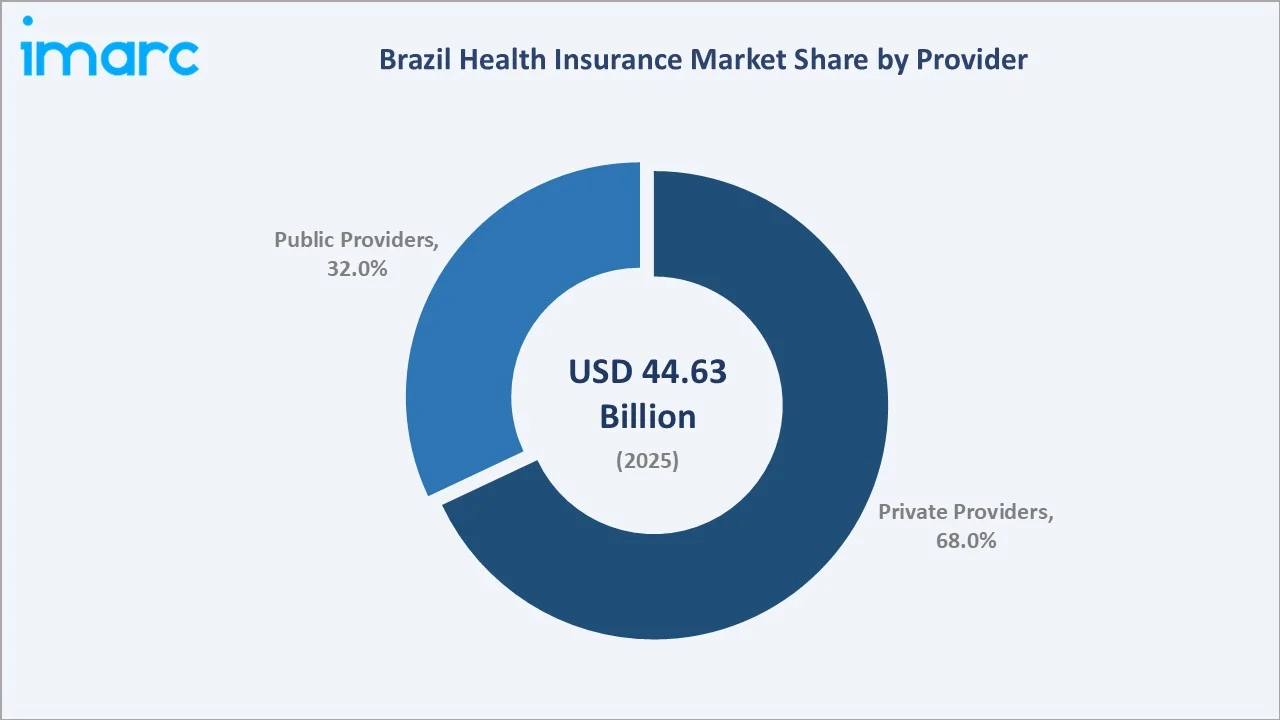

Private Providers lead at 68.0% in 2025, reflecting the dominance of employer-sponsored plans, corporate group insurance, and individual supplementary policies across Brazil's supplementary health market. The private provider segment benefits from structural demand growth as the formal workforce expands and corporate health benefit competition intensifies.

To access detailed market analysis, Request Sample

Public Providers at 32.0% represent government-administered supplementary plans and public employee health benefit schemes. The private-public ratio reflects Brazil's constitutional SUS commitment complemented by robust private supplementary insurance, with the private segment growing faster as employer-sponsored and individual coverage penetration increases across all regions.

By Type

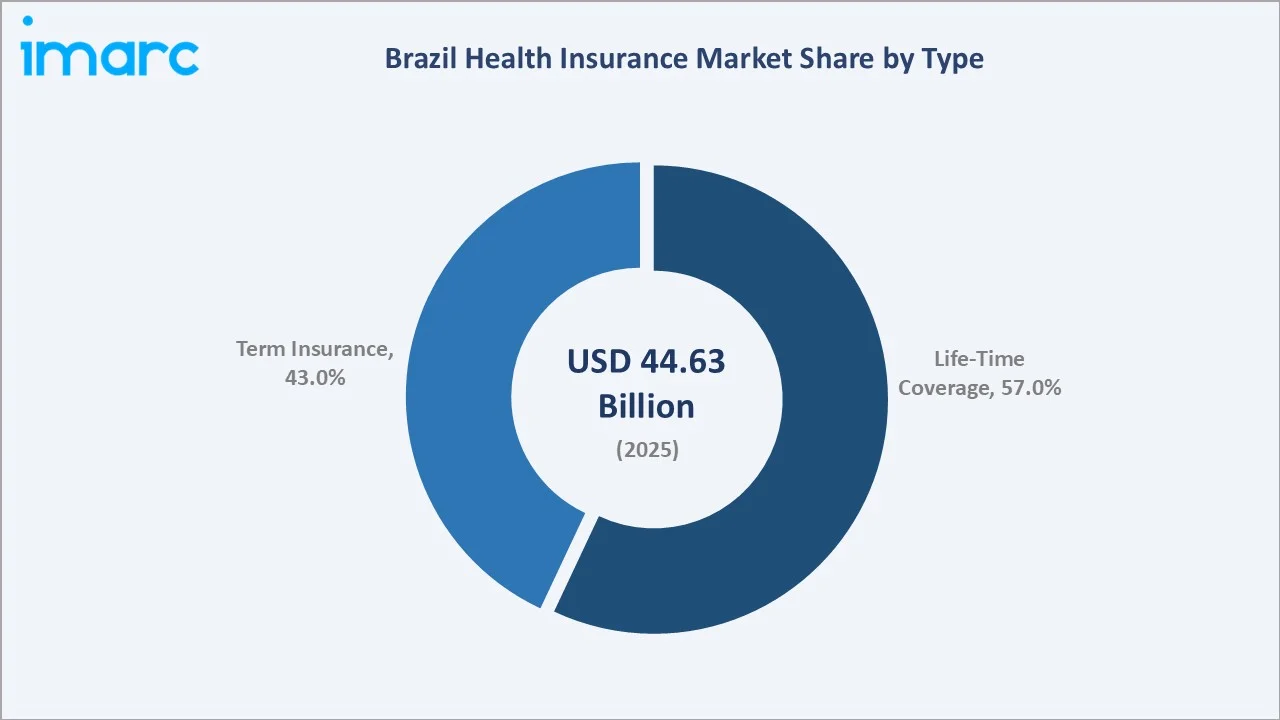

Life-Time Coverage leads at 57.0% through consumer demand for permanent health insurance protecting against chronic illness, hospitalisation, and long-term medical expenses. Brazil's ageing population profile, with increasing prevalence of diabetes, cardiovascular disease, and oncology conditions, reinforces demand for comprehensive lifetime protection plans.

Term Insurance at 43.0% captures demand for cost-effective, time-limited health coverage among younger policyholders and cost-conscious corporate buyers. Term plans are particularly popular in employer-sponsored group segments where annual plan renewal and cost benchmarking are primary considerations for corporate procurement and HR benefit decisions.

Regional Market Insights

|

Region |

Share (2025) |

Key Health Insurance Market Drivers & Characteristics |

|

Southeast |

42.0% |

Driven by high corporate density, elevated income levels, and Brazil's highest concentration of private hospital and diagnostic infrastructure |

|

South |

20.5% |

Driven by industrialised economy, high formal employment ratio, strong cooperative health network presence, and above-average per-capita insurance penetration |

|

Northeast |

16.5% |

Growing through workforce formalisation, federal social programme expansion, and rising private insurance access in major urban centres across the region |

|

Central-West |

11.0% |

Supported by agribusiness-driven income growth, Brasília public sector employment base, and expanding private healthcare infrastructure investment |

|

North |

10.0% |

Emerging market with early-stage private health insurance penetration; growth driven by urban population expansion, income growth, and improving healthcare infrastructure |

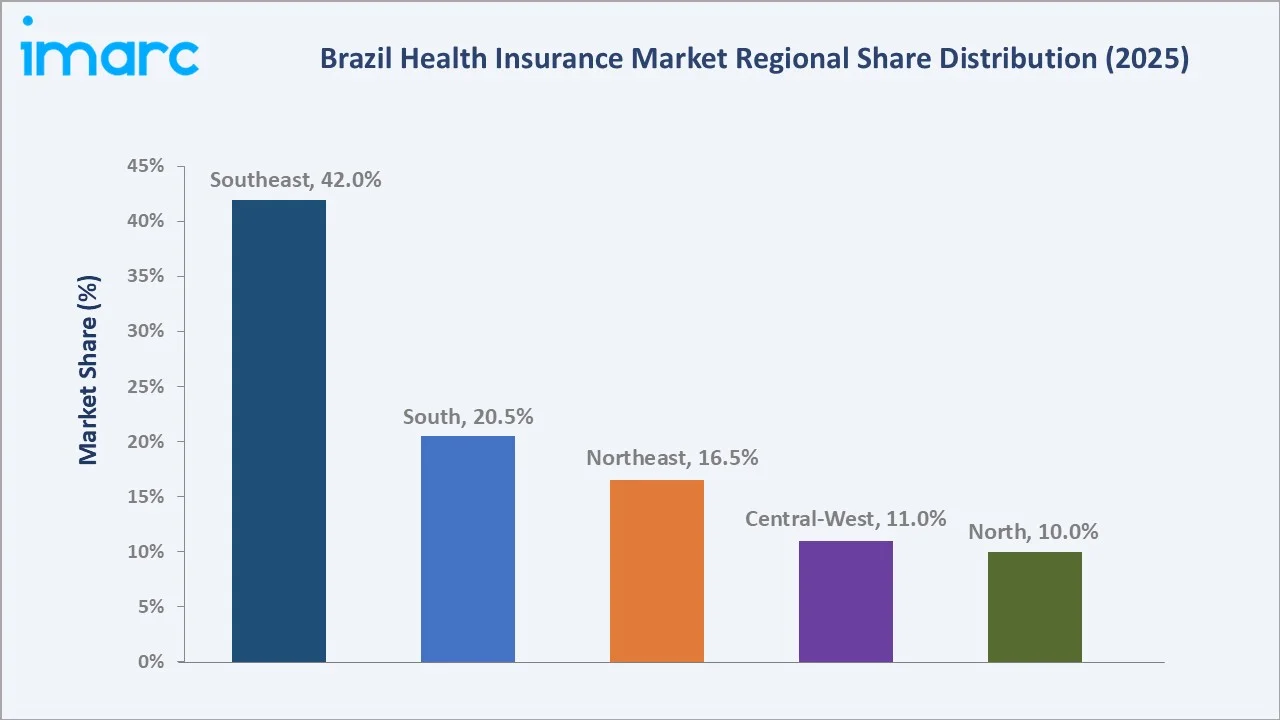

Southeast, at 42.0%, leads through São Paulo's role as Brazil's economic capital and highest private health plan penetration market. South, at 20.5%, reflects the region's high formal employment ratio and mature cooperative health network infrastructure of Unimed and similar operator models.

Northeast, at 16.5%, represents the most significant growth market as formalisation and income growth expand the insurable population. Central-West at 11.0% benefits from Brasília's public sector employment, while North at 10.0% remains at early-stage penetration with high long-term potential as infrastructure investment accelerates through the forecast period.

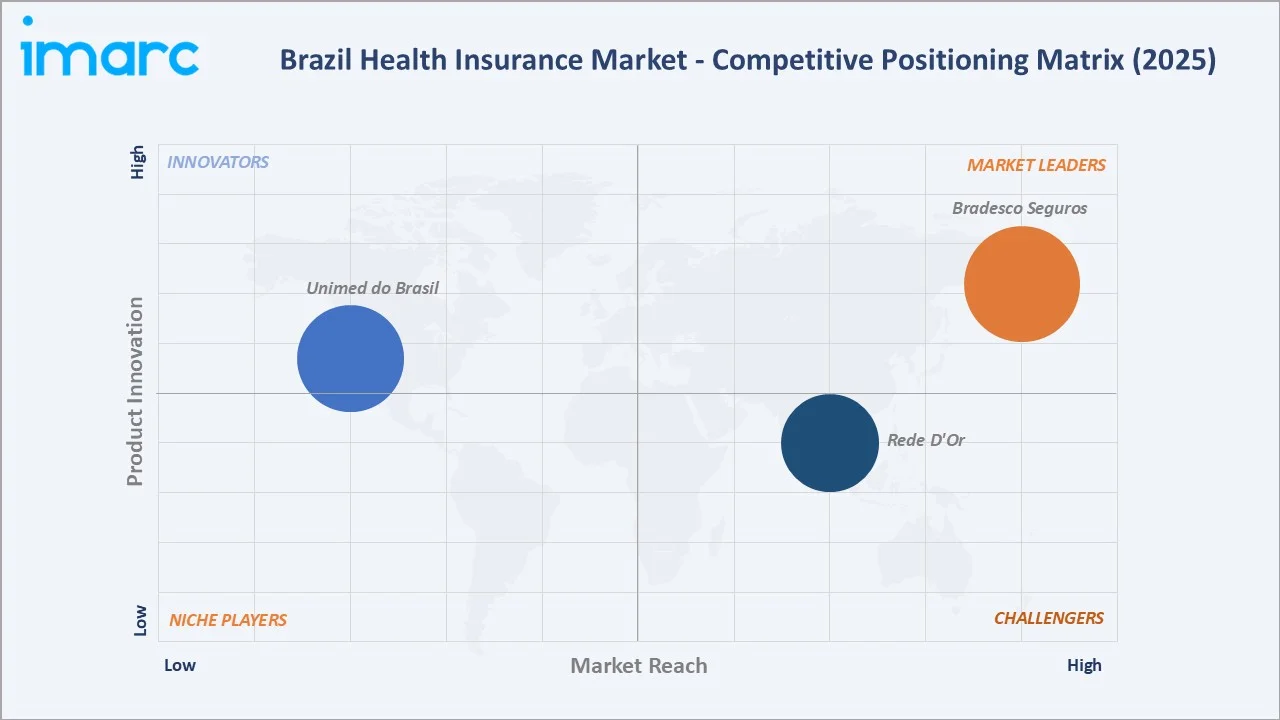

Competitive Landscape

The Brazil health insurance competitive landscape is moderately concentrated, with two distinct competitive tiers: large integrated health operators and diversified financial services insurers competing for employer-sponsored and individual plan segments, alongside cooperative networks commanding significant beneficiary loyalty across all five Brazilian regions.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Bradesco Seguros |

Individual, family, and corporate health plans; premium and mid-tier coverage |

Market Leader |

Consolidating all healthcare assets — health insurance, dental, primary care clinics, oncology, and health technology |

|

Rede D'Or |

Classic, Especial, and Prestige-tier individual and group plans; dental benefits |

Strong Challenger |

Growing the SME and corporate employer-sponsored segment through flexible bundled plan offerings combining health, dental, and life insurance, targeting the high-growth formal employment market across all Brazilian regions |

|

Unimed do Brasil |

Cooperative individual, family, and group health plans; dental plans |

Established Player |

Driving digital health adoption across the cooperative system through telemedicine platforms, AI-powered symptom checkers, and the Doctor-U network of 24/7 remote consultation kiosks to extend reach into geographically remote and underserved regions |

Key players include Bradesco Seguros, Rede D'Or, Unimed do Brasil, and others.

Key Company Profiles

Bradesco Seguros

Bradesco Seguros is Brazil's largest insurance holding group and the parent of Bradesco Saúde S.A., the country's leading corporate health insurer, serving a large base of beneficiaries across individual, family, and employer-sponsored plans. The group operates through Banco Bradesco's nationwide bancassurance network and is reorganising its healthcare assets under a newly consolidated platform, Bradsaúde S.A.

- Key Products: Individual, family, and corporate health plans; premium and mid-tier coverage

- Strategic Focus: Consolidating healthcare assets under the listed Bradsaúde S.A. platform to unlock standalone valuation and improve capital efficiency; leveraging Banco Bradesco's extensive bancassurance distribution network to deepen corporate group plan penetration; expanding vertical integration across hospital, primary care, oncology, and health technology assets to build a full-care-journey model; and deploying digital health infrastructure to connect insurers, providers, and pharmacies through analytics and automation.

Rede D'Or

Rede D'Or São Luiz S.A. is Brazil's largest publicly traded integrated healthcare group, operating an extensive hospital network alongside its health insurance subsidiary SulAmérica, creating a vertically integrated platform spanning hospital services, health and dental insurance, oncology, diagnostics, and health technology.

- Key Products: Classic, Especial, and Prestige-tier individual and group plans; dental benefits

- Strategic Focus: Deepening vertical integration by channelling SulAmérica beneficiaries into Rede D'Or's owned hospital and oncology network to reduce third-party costs and improve the consolidated loss ratio; expanding into underpenetrated regional markets through lower-cost, regionally restricted plan formats; growing health and dental beneficiary volumes through SME and corporate employer-sponsored bundled plan offerings; and continuing loss ratio improvement through tighter claims authorisation, fraud prevention, and network rationalisation across the combined insurance and hospital platform.

Market Concentration Analysis

The Brazil health insurance market is moderately concentrated. The five largest groups collectively account for approximately 30% of total beneficiaries, with the top ten groups reaching 41%.

Market concentration is expected to increase over the forecast period as vertical integration advantages widen the competitive gap between integrated operators and standalone insurers.

Investment & Growth Opportunities

Highest Growth Segments

Northeast regional expansion (~8-10% CAGR from low base), micro-insurance for informal workers, digital health-integrated plan formats, dental-health bundled coverage, corporate wellness programme integration, senior citizen coverage products, and telemedicine-first plan models represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

The informal worker and lower-income segment represent Brazil's largest untapped health insurance market. ANS-approved simplified plan formats at R$150-300/month price points could add 10-15 million new beneficiaries over the forecast period, creating significant volume growth for operators with cost-efficient distribution models and lean network architectures targeting this demographic.

Investment Themes

- Vertical integration of hospital and diagnostic networks for long-term claims cost control: Hapvida's integrated model demonstrates 15-20% lower medical cost ratios versus non-integrated operators. Hospital and diagnostic clinic acquisition creates a sustainable cost advantage that cannot be replicated by competitor’s dependent on external network procurement in a consolidating provider market.

- Digital health platform investment for plan differentiation and member retention: Telemedicine-integrated plans with AI-driven preventive care analytics create measurable reductions in emergency-room utilisation and long-term claims costs. Proprietary digital health platforms create differentiation supporting premium pricing and superior retention in the competitive corporate employer segment.

Future Market Outlook (2026-2034)

The Brazil health insurance market is projected to grow from USD 44.63 Billion in 2025 to USD 74.34 Billion by 2034, delivering a CAGR of 5.63% during 2026-2034. The market's anchor value of USD 58.67 Billion in 2030 reflects an industry at a critical inflection point of digital health adoption and regional expansion.

Three structural forces define market growth through 2034. The chronic disease burden expansion is increasing average claim severity and driving demand for comprehensive private plans. The corporate benefits competitive landscape is sustaining group plan volume growth above GDP. The digital health transformation is enabling insurers to serve previously cost-prohibitive lower-income segments through simplified telemedicine-first plan formats.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including Chief Actuarial Officers; private health insurer strategy leads; ANS regulatory affairs specialists; hospital network procurement managers; and corporate HR directors overseeing employee health benefit programmes across Brazil's five regions.

Secondary Research

Secondary research encompassed ANS beneficiary and claims data; IBGE demographic projections; company annual reports; Brazil Ministry of Health expenditure data; RankingsLatAm.com competitive tracking studies; and IMARC Group proprietary databases. Over 55 secondary sources reviewed across regulatory, industry, and financial reporting domains.

Forecasting Models

Market revenue forecasts developed using a bottom-up model: (i) beneficiary population forecast by segment and region; (ii) average annual premium per beneficiary by coverage type and provider; (iii) medical cost inflation and claims frequency adjustments; (iv) technology and digitalisation premium uplift by plan category through 2034.

Brazil Health Insurance Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Providers Covered | Private Providers, Public Providers |

| Types Covered | Life-Time Coverage, Term Insurance |

| Plan Types Covered | Medical Insurance, Critical Illness Insurance, Family Floater Health Insurance, Others |

| Demographics Covered | Minor, Adults, Senior Citizen |

| Provider Types Covered | Preferred Provider Organizations (PPOs), Point of Service (POS), Health Maintenance Organizations (HMOs), Exclusive Provider Organizations (EPOs) |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Bradesco Seguros, Rede D'Or, Unimed do Brasil, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil health insurance market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil health insurance market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil health insurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Health Insurance Market Report

The Brazil health insurance market reached USD 44.63 Billion in 2025, driven by Private Providers at 68.0%, Life-Time Coverage at 57.0%, and Southeast region at 42.0%, with 52.9 million health plan beneficiaries recorded as of mid-2025.

The market grows at a CAGR of 5.63% during 2026-2034, reaching USD 74.34 Billion by 2034, driven by workforce formalisation, rising healthcare costs, digital health integration, and expanding corporate group plan penetration across Brazil's formal employment sector.

Private Providers lead at 68.0% in 2025, capturing employer-sponsored group plans, corporate coverage, and individual supplementary health policies across all income segments, driven by SUS capacity constraints and rising demand for faster and more comprehensive private care.

Life-Time Coverage leads at 57.0% through consumer preference for permanent protection against chronic illness, hospitalisation, and long-term healthcare costs, reinforced by Brazil's ageing population demographic and rising prevalence of non-communicable diseases across all regions.

The Southeast leads at 42.0% through São Paulo and Rio de Janeiro's concentration of corporate employment, higher per-capita incomes, and the highest density of private hospital and diagnostic infrastructure in Brazil.

Leading companies include Bradesco Seguros, Rede D'Or, Unimed do Brasil, and others.

The market is projected to reach USD 58.67 Billion by 2030, driven by Northeast and North regional expansion, digital health platform integration, micro-insurance growth for informal workers, and corporate wellness benefit expansion across Brazil's formal employment sector.

Three priority investment opportunities: vertical integration of hospital and diagnostic networks for long-term claims cost control; digital health platform development for plan differentiation and member retention; and simplified plan product development targeting Brazil's large informal worker population across underserved regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)