Brazil Heavy-Duty Automotive Aftermarket Size, Share, Trends and Forecast by Replacement Part, Vehicle Type, Service Channel, and Region, 2026-2034

Brazil Heavy-Duty Automotive Aftermarket Overview:

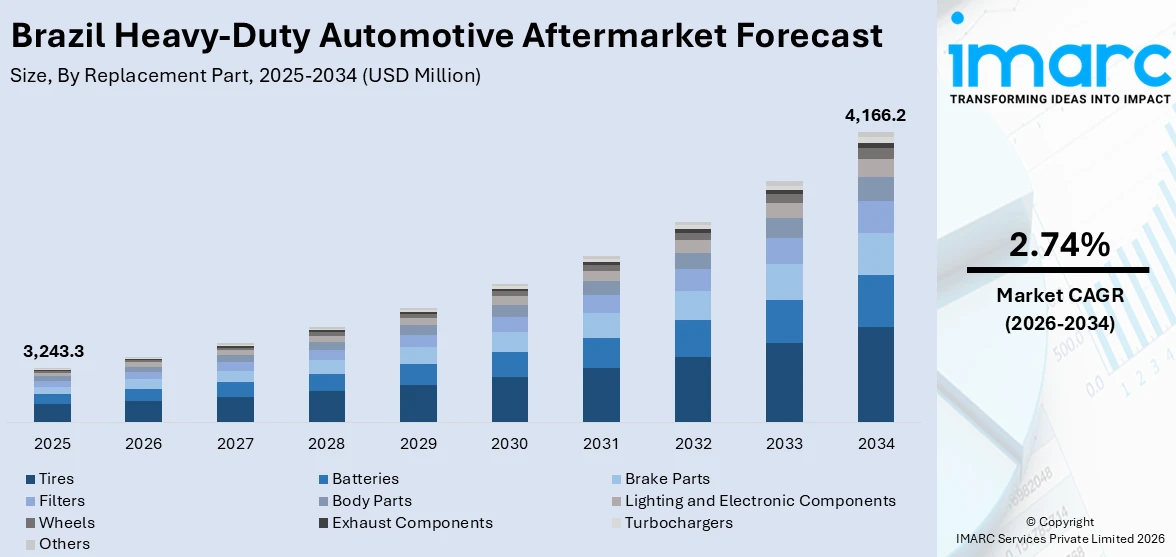

The Brazil heavy-duty automotive aftermarket size reached USD 3,243.3 Million in 2025. The market is projected to reach USD 4,166.2 Million by 2034, exhibiting a growth rate (CAGR) of 2.74% during 2026-2034. The market is driven by the implementation of stricter emission regulations requiring advanced aftermarket components, substantial infrastructure investments expanding freight transport operations, and the widespread adoption of digital fleet management technologies, including telematics and predictive maintenance systems. Additionally, the growing complexity of heavy-duty vehicles and increasing fleet sizes across logistics and transportation sectors are supporting the Brazil heavy-duty automotive aftermarket share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 3,243.3 Million |

| Market Forecast in 2034 | USD 4,166.2 Million |

| Market Growth Rate 2026-2034 | 2.74% |

Brazil Heavy-Duty Automotive Aftermarket Trends:

Stringent Emission Standards Accelerating Component Replacement

Brazil's heavy-duty automotive aftermarket is undergoing significant changes due to the introduction of PROCONVE P-8 emission standards, which became mandatory in January 2023. These regulations, comparable to Euro VI standards, impose stringent emission requirements on the commercial vehicle sector, requiring advanced emission control technologies. Fleet operators must now upgrade older vehicles with components like diesel particulate filters, selective catalytic reduction units, and advanced diagnostic systems to ensure compliance and efficiency. The new rules have led to increased demand for specialized aftermarket parts, including fuel injection systems, turbochargers, and emission sensors. Maintenance intervals for emission-related components have become more frequent and require specialized tools and technicians. Additionally, the adoption of ultra-low sulfur diesel fuel, which requires compatible components, has grown. Parts distributors and service providers have invested in training and diagnostic equipment to manage these complex systems. As the fleet modernizes, the aftermarket is benefiting from higher parts complexity, increased component values, and more frequent replacements due to advanced emission technologies.

To get more information on this market Request Sample

Infrastructure Development Expanding Freight Operations and Maintenance Requirements

Brazil's extensive infrastructure modernization is reshaping the heavy-duty automotive aftermarket by boosting vehicle utilization and maintenance demands. The government has committed $25.9 Billion for highway development from 2023 to 2027, with additional investments from multilateral banks and private investors targeting port, railway, and logistics hub expansion. In 2023, the Inter-American Development Bank approved a $480 million loan to upgrade key state highways, improving Brazil's transportation integration. These infrastructure improvements are increasing freight volumes, extending operational hours, and intensifying duty cycles for heavy-duty trucks, especially in agricultural export regions. As a result, component wear has accelerated, driving higher demand for brake systems, tires, suspension parts, and powertrains. The growth in logistics complexity is also fueling demand for mobile maintenance services and strategically located parts distribution centers. Additionally, foreign investments from manufacturers like Stellantis are expanding the vehicle fleet, further supporting aftermarket growth. This infrastructure boom is creating a strong foundation for the continued expansion of the Brazil heavy-duty automotive aftermarket growth.

Digital Technologies Revolutionizing Fleet Maintenance Practices

Brazil’s heavy-duty automotive aftermarket is being transformed by rapid digital adoption as fleet operators embrace telematics, predictive maintenance, and AI-driven diagnostics to reduce costs and maximize uptime. What were once premium tools have become essential, especially with modern emission-compliant vehicles. Telematics systems now deliver real-time data on engine health, fuel use, tire pressure, and brake wear, enabling proactive maintenance scheduling and minimizing breakdowns. Predictive systems supported by IoT sensors alert service centers to upcoming issues, allowing them to prepare parts and tools in advance. Machine learning models further analyze fleet-wide data to pinpoint common failure patterns and suggest preventive actions suited to local operating conditions. Digital platforms are also revolutionizing inventory management, automating parts ordering, and linking diagnostics directly to suppliers. Drivers benefit from mobile apps providing alerts and digital work orders, while manufacturers use connected-vehicle data to improve parts design. Cloud-based maintenance systems give fleet operators unified oversight, standardized service practices, and transparent cost tracking across multiple sites.

Brazil Heavy-Duty Automotive Aftermarket Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on replacement part, vehicle type, and service channel.

Replacement Part Insights:

- Tires

- Batteries

- Brake Parts

- Filters

- Body Parts

- Lighting and Electronic Components

- Wheels

- Exhaust Components

- Turbochargers

- Others

The report has provided a detailed breakup and analysis of the market based on the replacement part. This includes tires, batteries, brake parts, filters, body parts, lighting and electronic components, wheels, exhaust components, turbochargers, and others.

Vehicle Type Insights:

Access the comprehensive market breakdown Request Sample

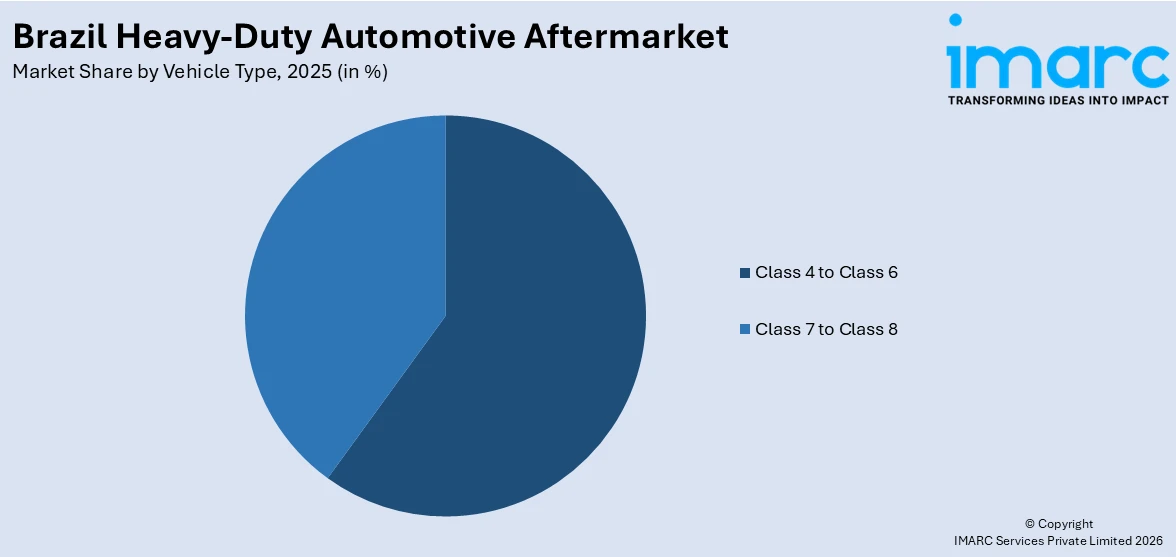

- Class 4 to Class 6

- Class 7 to Class 8

A detailed breakup and analysis of the market based on the vehicle type have also been provided in the report. This includes class 4 to class 6 and class 7 to class 8.

Service Channel Insights:

- DIY

- OE Seller

- DiFM

The report has provided a detailed breakup and analysis of the market based on the service channel. This includes DIY, OE seller, and DiFM.

Regional Insights:

- Southeast

- South

- Northeast

- North

- Central-West

The report has also provided a comprehensive analysis of all the major regional markets, which include Southeast, South, Northeast, North, and Central-West.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Brazil Heavy-Duty Automotive Aftermarket News:

- September 2025: Mopar launched an extensive line of locally manufactured accessories for the 2025 Ram Heavy-Duty truck lineup in Brazil, featuring electric bed covers, retractable side steps, trailer cameras, and themed accessory packages designed and validated by Stellantis and Mopar engineers to enhance vehicle customization and aftermarket appeal.

- February 2025: Cummins Inc. introduced its X10 engine platform as part of the HELM fuel-agnostic engine lineup, designed for heavy and medium-duty vehicle applications in global markets, including Brazil. The X10 engine replaces both the L9 and X12 platforms, delivering enhanced performance, durability, and efficiency for vocational, regional haul, and transit bus fleet customers.

- March 2024: Stellantis announced a comprehensive investment of $6.07 billion in Brazil scheduled between 2025 and 2030, with strategic plans to launch more than 40 new vehicle models and introduce hybrid-flex technology specifically designed for Brazilian market conditions and commercial vehicle applications.

Brazil Heavy-Duty Automotive Aftermarket Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Replacement Parts Covered | Tires, Batteries, Brake Parts, Filters, Body Parts, Lighting and Electronic Components, Wheels, Exhaust Components, Turbochargers, Others |

| Vehicle Types Covered | Class 4 to Class 6, Class 7 to Class 8 |

| Service Channels Covered | DIY, OE Seller, DiFM |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Brazil heavy-duty automotive aftermarket performed so far and how will it perform in the coming years?

- What is the breakup of the Brazil heavy-duty automotive aftermarket on the basis of replacement part?

- What is the breakup of the Brazil heavy-duty automotive aftermarket on the basis of vehicle type?

- What is the breakup of the Brazil heavy-duty automotive aftermarket on the basis of service channel?

- What is the breakup of the Brazil heavy-duty automotive aftermarket on the basis of region?

- What are the various stages in the value chain of the Brazil heavy-duty automotive aftermarket?

- What are the key driving factors and challenges in the Brazil heavy-duty automotive aftermarket?

- What is the structure of the Brazil heavy-duty automotive aftermarket and who are the key players?

- What is the degree of competition in the Brazil heavy-duty automotive aftermarket?

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil heavy-duty automotive aftermarket from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil heavy-duty automotive aftermarket.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil heavy-duty automotive aftermarket industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)