Brazil Home Appliances Market Size, Share, Trends and Forecast by Product, Distribution Channel, and Region 2026-2034

Brazil Home Appliances Market Size, Share, Trends & Forecast (2026-2034)

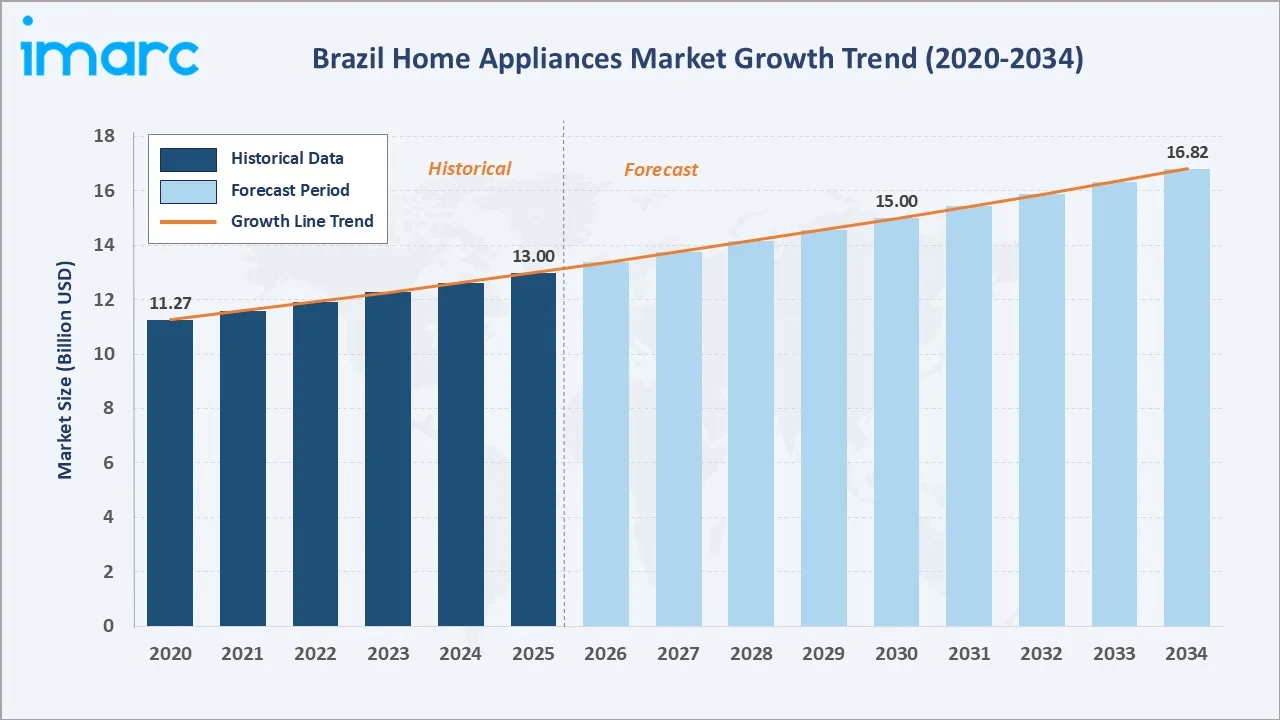

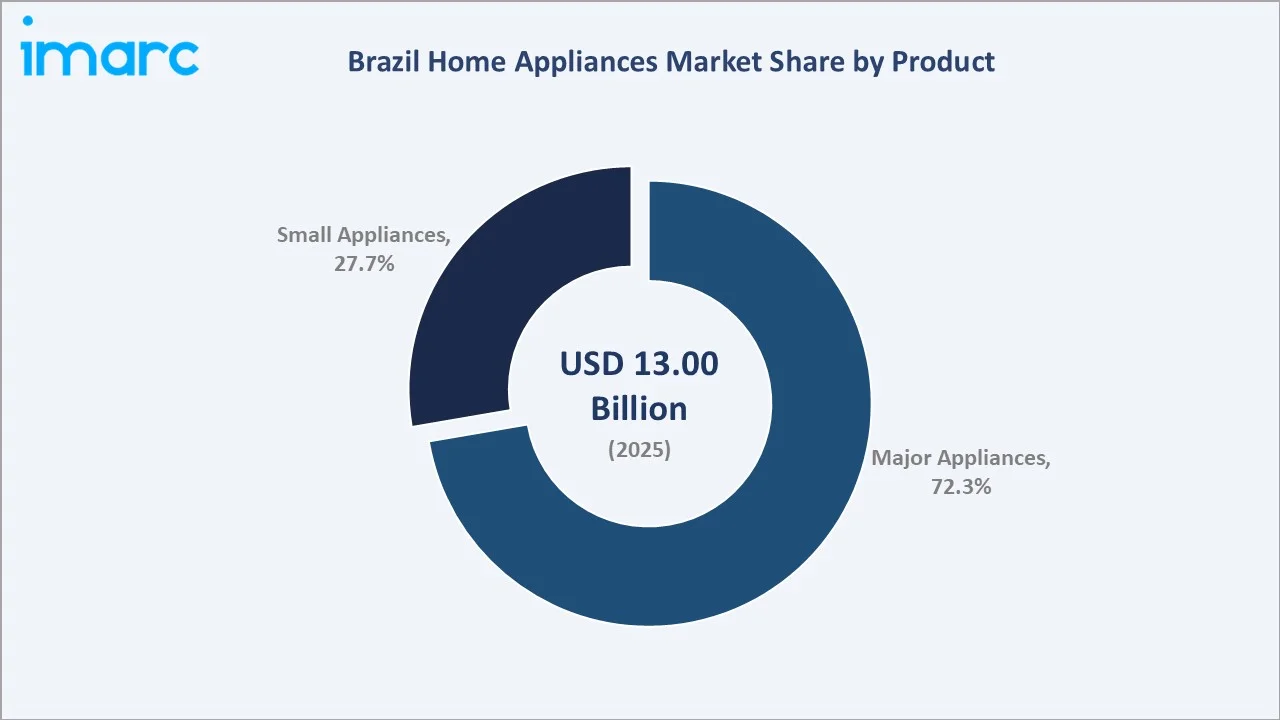

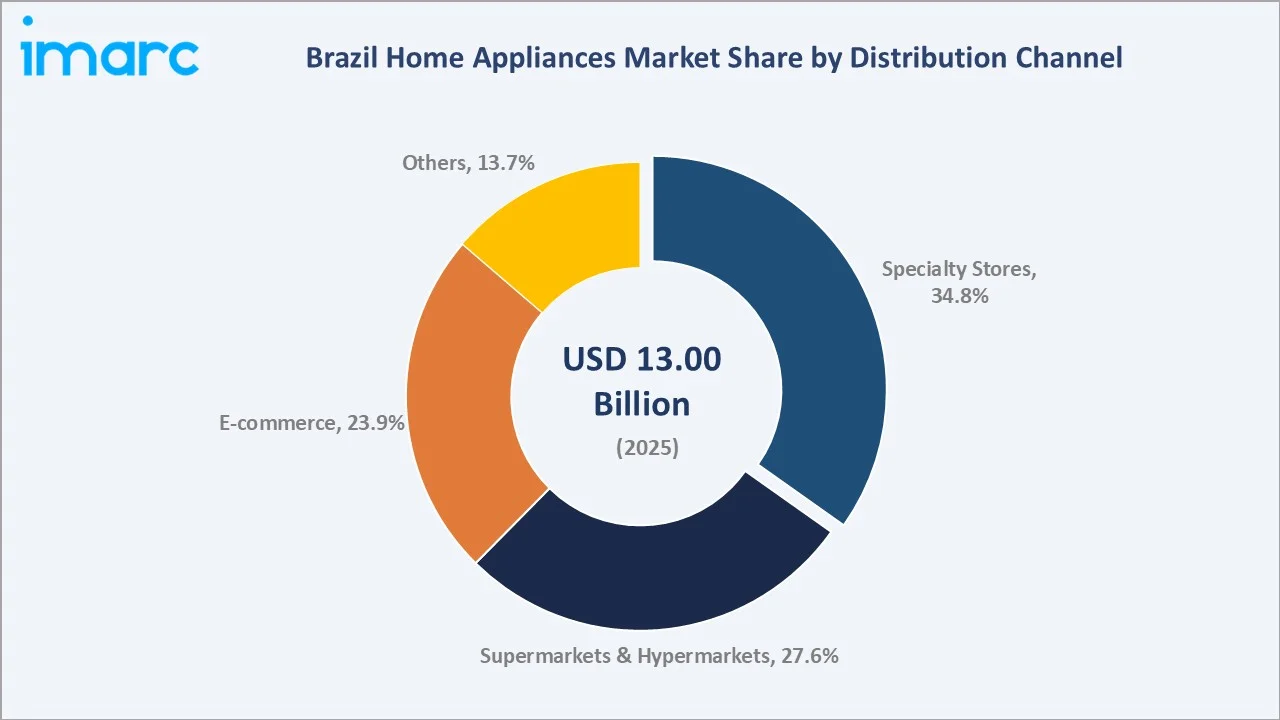

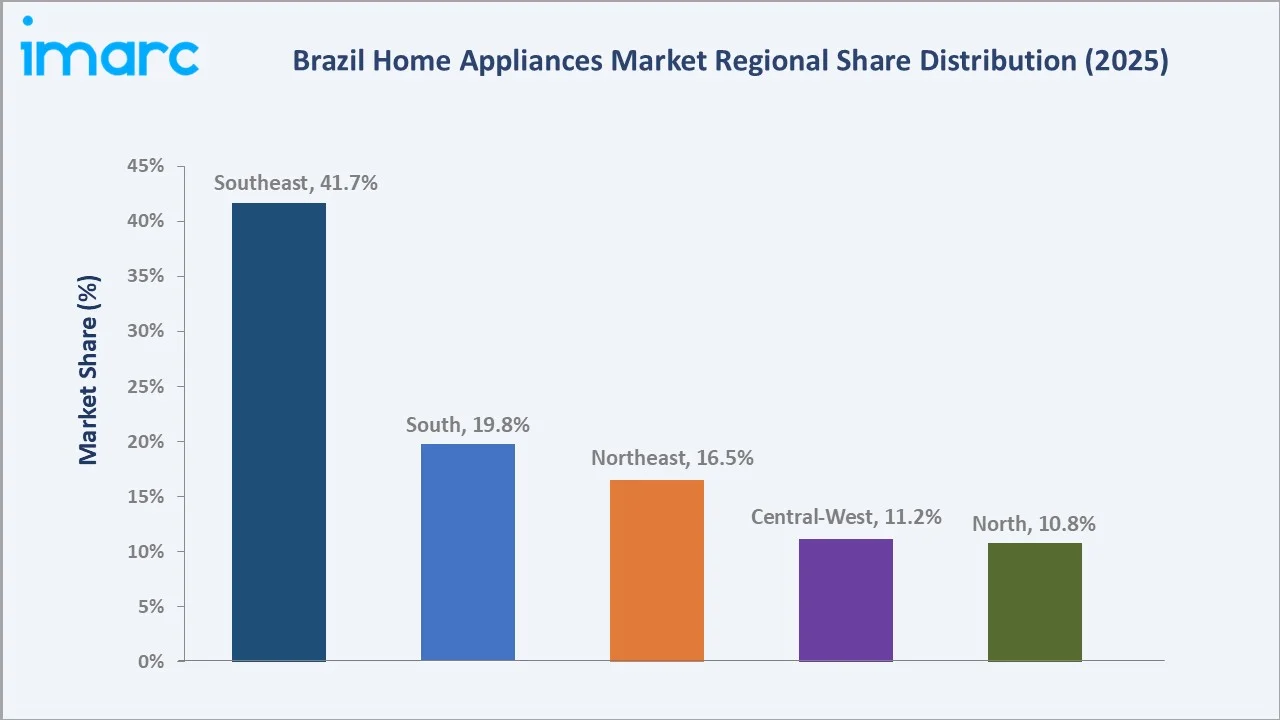

The Brazil home appliances market reached USD 13.00 Billion in 2025 and is projected to reach USD 16.82 Billion by 2034, growing at a CAGR of 2.90% during 2026-2034. More than 87% of Brazil’s 203 million residents were already living in urban areas in 2022, with the urban population projected to reach 90% by 2050. This supports the home appliances market by increasing demand for refrigerators, washing machines, air conditioners, cooking appliances and other household products in urban homes and apartments. The market is driven by rising urbanization, growing disposable incomes, expanding middle-class households, and increasing replacement demand for energy-efficient and smart appliances. Growth is also supported by housing development, e-commerce expansion, and the adoption of connected home technologies. Major appliances dominate at 72.3%. Specialty stores lead distribution at 34.8%. The Southeast commands 41.7% of the national market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 13.00 Billion |

|

Forecast Market Size (2034) |

USD 16.82 Billion |

|

CAGR (2026-2034) |

2.90% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product |

Major Appliances (72.3%, 2025) |

|

Dominant Distribution Channel |

Specialty Stores (34.8%, 2025) |

|

Leading Region |

Southeast (41.7%, 2025) |

The market expanded from USD 11.27 Billion in 2020 to USD 13.00 Billion in 2025, anchored at USD 15.00 Billion in 2030, and forecast to reach USD 16.82 Billion by 2034. E-commerce appliance sales are supported by the adoption of instant-payment methods, which have expanded online payment options.

To get more information on this market, Request Sample

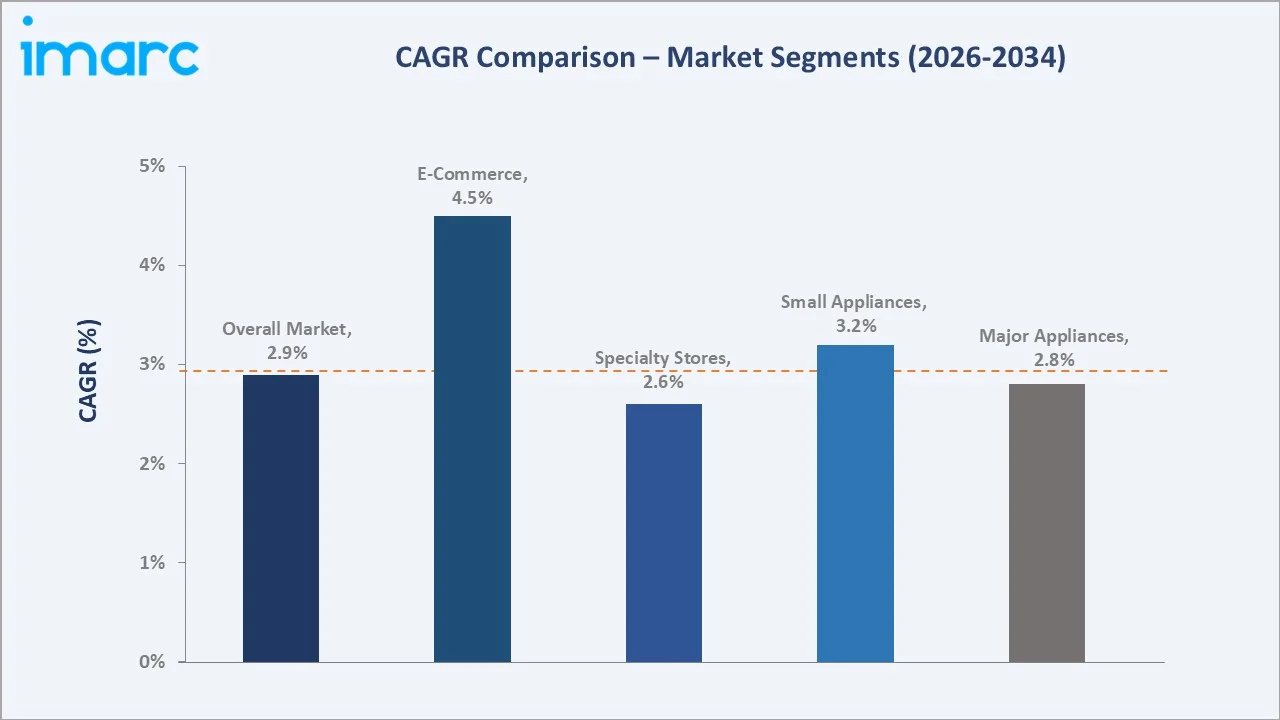

Small appliances grow fastest at ~3.2% CAGR driven by Brazil's air fryer boom, premium coffee machine adoption, personal care device expansion, and the broader premiumization of kitchen small appliances among Brazil's growing upper-middle class. E-commerce is the fastest-growing distribution channel at ~4.5% CAGR as e-commerce progressively extends reliable 2-person delivery for major appliances beyond the Southeast and into secondary Brazilian cities.

Executive Summary

Brazil's home appliances market reached USD 13.00 Billion in 2025, representing Latin America's largest national home appliance market. Brazil's appliance industry operates within a distinctive institutional framework. The market encompasses major appliances (refrigerators, washing machines, dryers, dishwashers, air conditioners, ranges, microwaves) and small appliances (blenders, pressure cookers, air fryers, coffee machines, toasters, personal care devices, irons, fans). The market is projected to reach USD 16.82 Billion by 2034.

Major appliances at 72.3%, supported by demand for essential products such as refrigerators and washing machines. Specialty Stores at 34.8% lead distribution through nationwide physical store presence, delivering the trusted installment credit experience that Brazilian consumers depend on.

Key Market Insights

|

Insight |

Data |

|

Dominant Product |

Major Appliances - 72.3% share (2025) |

|

Dominant Distribution Channel |

Specialty Stores - 34.8% market share (2025) |

|

Leading Region |

Southeast - 41.7% market share (2025) |

|

Market Opportunity |

Smart connected appliances; energy-efficient products; Northeast and North regional expansion; air fryer and small appliance premiumization |

Key Analytical Observations Supporting the Above Data:

- Major Appliances at 72.3%: The major appliances segment dominates due to the essential household need for refrigerators, washing machines, cookers and air conditioners. Rising urban housing, replacement demand and preference for energy-efficient appliances further support segment growth.

- Specialty Stores at 34.8%: The specialty stores segment dominates because consumers prefer expert guidance, product demonstrations, warranty support, and after-sales services when buying high-value appliances. Wide brand availability and financing options also strengthen their position as a preferred retail channel.

- Southeast at 41.7%: The Southeast region dominates due to its large urban population, higher income levels, and concentration of major cities such as São Paulo and Rio de Janeiro. Strong retail networks, housing activity, and consumer spending further support appliance demand.

Brazil Home Appliances Market Overview

Brazil's home appliances market encompasses the full spectrum of household electrical products for cooking, food preservation, laundry, climate control, and personal care sold through OEM direct and retail channels to Brazilian consumers.

The appliance ecosystem integrates Brazilian manufacturers, international brands with Brazilian manufacturing, imported brands, component suppliers, retail channels, and consumer finance infrastructure. Macroeconomic factors include improving household incomes, urban housing growth, consumer credit availability, and rising replacement demand.

Market Dynamics

To evaluate market opportunities, Request Sample

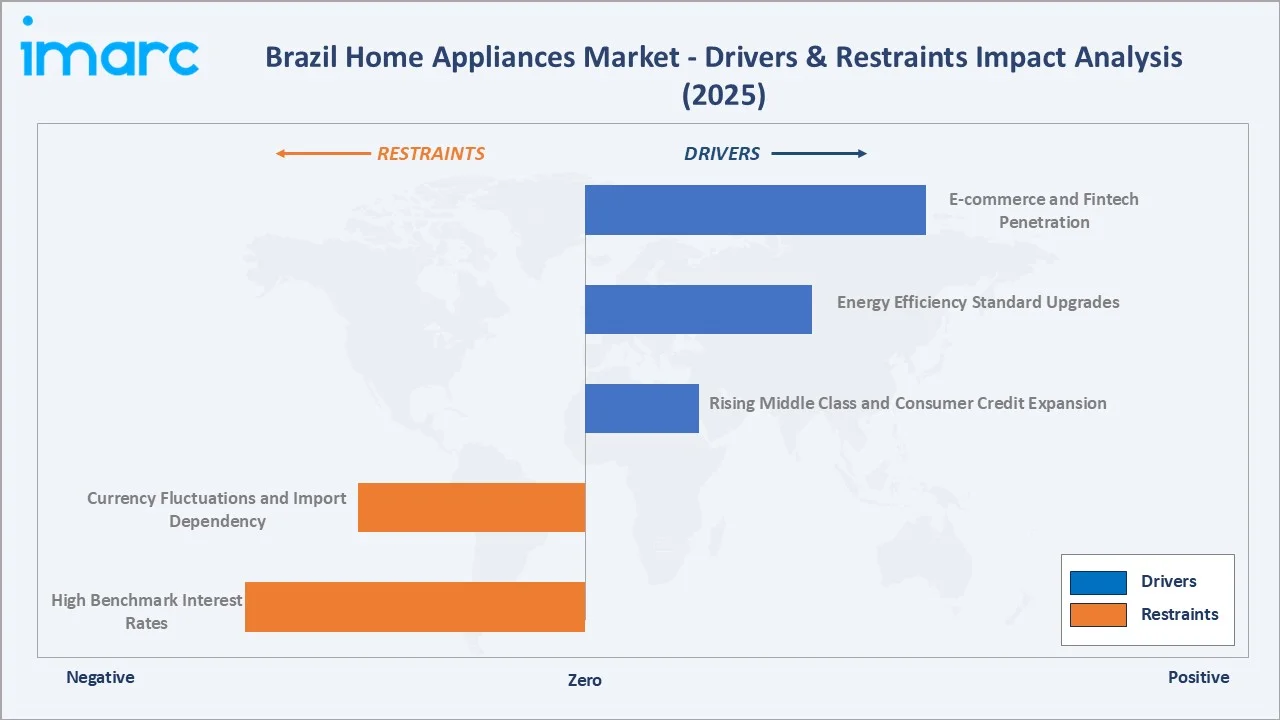

Market Drivers

- Rising Middle Class and Consumer Credit Expansion: According to the study conducted by Tendências Consultoria, Brazil regained middle-class status in 2024, with Class C and above households representing 50.1% of total households. This share is expected to rise to 54.8% by 2034. This rising middle-class income and wider access to consumer credit are making home appliances more affordable for Brazilian households. Financing options, installment payments and retail credit encourage consumers to purchase or upgrade refrigerators, washing machines, air conditioners and cooking appliances. This supports both first-time appliance ownership and replacement demand. As purchasing power improves, consumers are also shifting toward premium, energy-efficient and smart appliances.

- Energy Efficiency Standard Upgrades: Energy efficiency standard upgrades encourage households to replace older, high-energy-consuming products with more efficient models. Stricter efficiency labels and performance requirements push manufacturers to develop advanced refrigerators, washing machines, air conditioners and cooking appliances. Consumers are also attracted by lower electricity costs and better long-term savings. This supports demand for modern, premium and eco-friendly appliances across urban households.

- E-commerce and Fintech Penetration: E-commerce and fintech penetration are making products easier to compare, purchase and finance online. Digital marketplaces expand brand reach beyond physical stores, while fintech-enabled payments, installments and instant credit improve affordability. This encourages consumers to buy both essential and premium appliances through online channels. As digital shopping and flexible payment adoption grow, appliance sales become more accessible across urban and regional markets.

Market Restraints

- High Benchmark Interest Rates: High benchmark interest rates increase the cost of consumer financing and installment-based purchases, which are widely used for appliance buying. Higher borrowing costs reduce affordability for products such as refrigerators, air conditioners and washing machines. Consumers may delay upgrades or shift toward lower-priced models, affecting premium appliance sales. Elevated interest rates also weaken overall retail demand and discretionary spending.

- Currency Fluctuations and Import Dependency: Currency fluctuations and import dependency are increasing the cost of imported components, electronics, compressors and finished products. Exchange-rate volatility raises production and procurement expenses for manufacturers, which can lead to higher retail prices. This reduces appliance affordability and may delay consumer purchases or upgrades. Manufacturers also face margin pressure and supply uncertainties due to fluctuating import costs.

Market Opportunities

- Smart Connected Appliances with AI Integration: Smart connected appliances with AI integration present a significant opportunity as consumers increasingly seek convenience, automation and energy efficiency. AI-enabled refrigerators, air conditioners, washing machines and kitchen appliances offer features such as remote monitoring, predictive maintenance and personalized settings. Growing smart home adoption further supports demand for connected devices. This trend creates opportunities for manufacturers to expand premium product portfolios and digital ecosystems.

- Northeast and North Regional Appliance Market Expansion Through E-commerce Logistics and Increasing Formal Employment: Expansion of appliance demand in Brazil’s Northeast and North regions through improving e-commerce logistics and rising formal employment presents a major market opportunity. Better delivery networks and digital retail access are increasing appliance availability in previously underserved areas. At the same time, growth in formal employment supports household income and purchasing power, encouraging first-time appliance purchases and upgrades. This creates new growth avenues for manufacturers and retailers beyond Brazil’s major urban centers.

Market Challenges

- Competition from Low-Cost and Unorganized Products: Competition from low-cost and unorganized products is creating strong price pressure on established brands. Informal or low-priced products can attract cost-conscious consumers, especially during periods of weak purchasing power. This affects margins for organized players and makes it harder to promote premium, energy-efficient and smart appliances. It may also impact consumer trust if lower-quality products lead to poor durability or limited after-sales support.

- Environmental Appliance Disposal Infrastructure Gaps: Environmental appliance disposal infrastructure gaps are limiting safe recycling and disposal of old refrigerators, washing machines and other large appliances. Weak collection and reverse-logistics systems can slow replacement cycles and raise compliance costs for manufacturers and retailers. Improper disposal also increases environmental concerns linked to metals, plastics and refrigerants. As sustainability expectations rise, companies may need greater investment in take-back programs and circular-economy solutions.

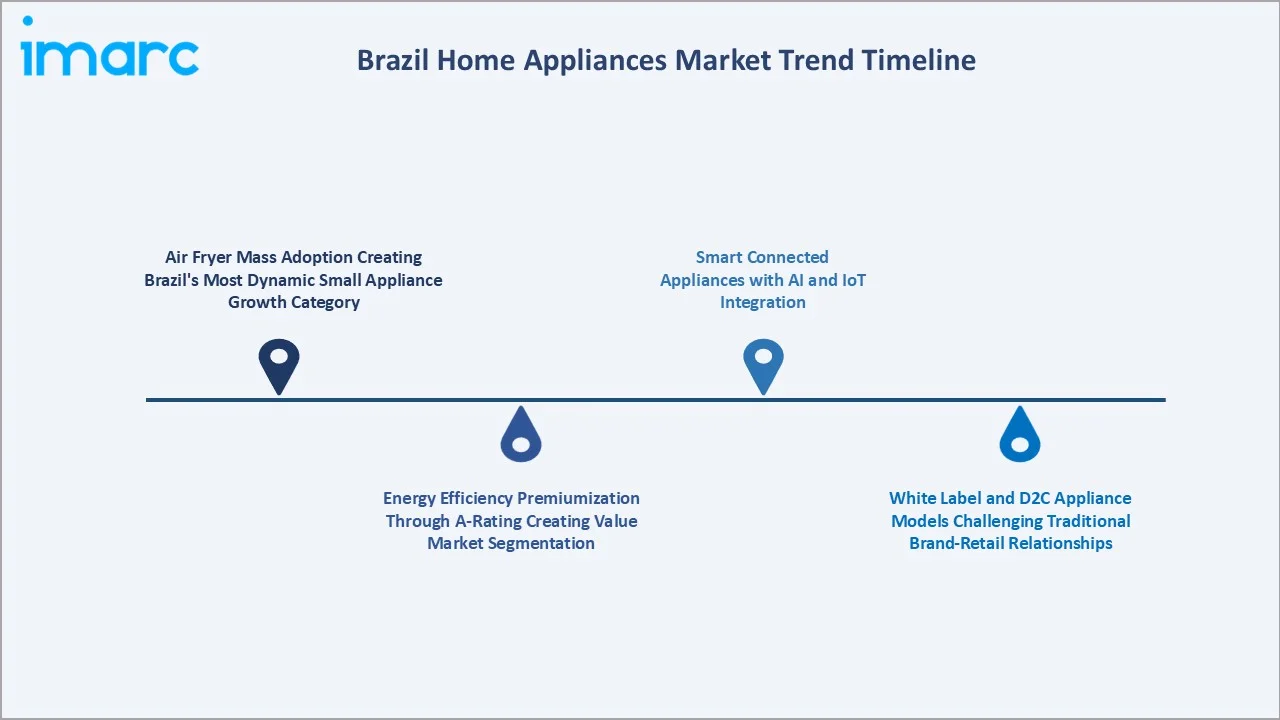

Emerging Market Trends

1. Air Fryer Mass Adoption Creating Brazil's Most Dynamic Small Appliance Growth Category

Air fryer mass adoption is making the category one of the fastest-growing areas within small appliances. Consumers are increasingly choosing air fryers for convenience, faster cooking, healthier meal preparation and compact kitchen use. Strong retail visibility and frequent product innovation are encouraging upgrades to larger, multifunctional and smart models. This trend is helping manufacturers expand small appliance portfolios and capture higher-value consumer demand.

2. Energy Efficiency Premiumization Through A-Rating Creating Value Market Segmentation

Energy efficiency premiumization through A-rating, creating clear value-based product segmentation. Consumers are increasingly willing to pay more for highly efficient appliances that reduce electricity consumption and long-term utility costs. This encourages manufacturers to launch premium refrigerators, washing machines, air conditioners and kitchen appliances with advanced energy-saving technologies. As efficiency becomes a purchase priority, A-rated products are strengthening differentiation and brand positioning.

3. White Label and D2C Appliance Models Challenging Traditional Brand-Retail Relationships

White-label and D2C appliance models allow retailers and manufacturers to sell appliances directly under their own brands. This reduces dependence on traditional brand-retail partnerships and increases price competition. D2C channels also help companies control customer data, pricing, promotions and after-sales engagement. As a result, established appliance brands must strengthen differentiation, service quality and digital sales strategies.

4. Smart Connected Appliances with AI and IoT Integration

Smart connected appliances with AI and IoT integration are emerging as consumers increasingly adopt connected home technologies. AI-enabled appliances offer features such as remote control, energy optimization, predictive maintenance and personalized usage settings through mobile applications and voice assistants. Manufacturers are expanding smart portfolios across refrigerators, air conditioners, washing machines and kitchen appliances. In May 2024, Tuya Smart partnered with Hometree Casa Inteligente LTDA to develop cutting-edge smart whole-house solutions, revolutionize traditional living spaces, and offer Brazilian users a comprehensive smart living experience.

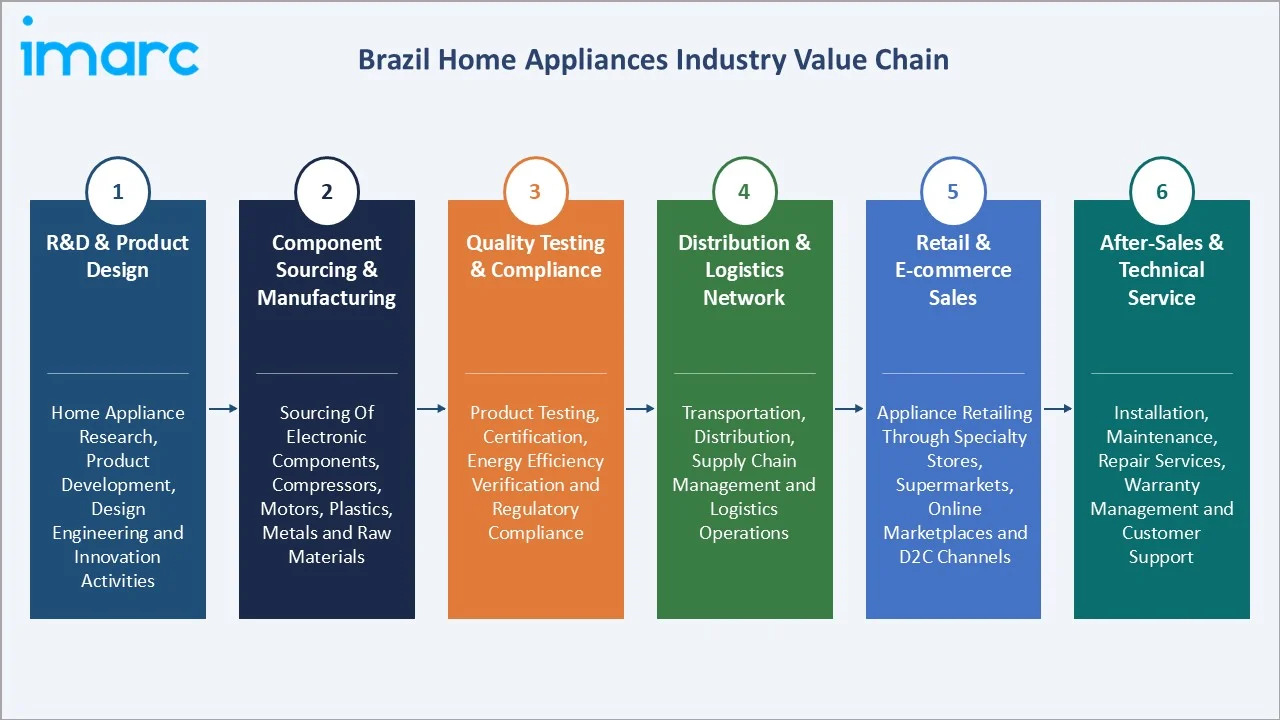

Industry Value Chain Analysis

Brazil's home appliance value chain integrates R&D and product design adapted for Brazilian conditions, component sourcing and manufacturing, quality testing and compliance, distribution and logistics, retail and e-commerce sales, and after-sales technical service.

|

Stage |

Key Participants |

|

R&D & Product Design |

Home appliance research, product development, design engineering and innovation activities |

|

Component Sourcing & Manufacturing |

Sourcing of electronic components, compressors, motors, plastics, metals and raw materials |

|

Quality Testing & Compliance |

Product testing, certification, energy efficiency verification and regulatory compliance |

|

Distribution & Logistics Network |

Transportation, distribution, supply chain management and logistics operations |

|

Retail & E-commerce Sales |

Appliance retailing through specialty stores, supermarkets, online marketplaces and D2C channels |

|

After-Sales & Technical Service |

Installation, maintenance, repair services, warranty management and customer support |

The manufacturing stage benefits from two structural Brazilian fiscal advantages: ZFM manufacturing and domestic manufacturing IPI reduction.

Technology Landscape in the Brazil Home Appliances Industry

Connected Appliances and Smart Home Integration

Connected appliances and smart home integration enable remote control, automation and real-time monitoring through mobile apps and voice assistants. These technologies improve convenience, energy management and appliance performance for consumers. They also allow manufacturers to offer predictive maintenance, personalized usage settings and connected service ecosystems. As adoption grows, smart appliances are driving premiumization and digital innovation across the industry.

Inverter Compressor Technology for Air Conditioners and Refrigerators

Inverter compressor technology improves energy efficiency and performance in air conditioners and refrigerators. Unlike conventional systems, inverter technology adjusts compressor speed based on cooling demand, reducing electricity consumption and operating noise. This supports consumer preference for energy-saving appliances and lower utility costs. As efficiency standards strengthen, manufacturers are increasingly integrating inverter technology into premium and mid-range product segments. In December 2025, Nidec ACIM opened a new production line for Embraco FMS compressors at its Joinville plant in Brazil. The facility will manufacture variable-speed inverter compressors for residential refrigeration, supporting energy efficiency and complies with new Brazilian energy efficiency regulations from INMETRO.

Air Fryer and Health Appliance Technology

Air fryer and health appliance technology are driving demand for healthier and convenience-focused cooking solutions. Manufacturers are introducing features such as digital controls, multifunction cooking modes, smart connectivity and energy-efficient heating systems. Health-oriented appliances, including air fryers, blenders and steam cookers, align with changing consumer lifestyles and wellness preferences. This trend is encouraging innovation and expanding the premium small appliance segment.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Major Appliances |

72.3% |

2025 |

|

Distribution Channel |

Specialty Stores |

34.8% |

2025 |

|

Region |

Southeast |

41.7% |

2025 |

By Product

Major appliances lead at 72.3% (2025). The major appliance category is anchored by refrigerators, washing machines, air conditioners, ranges and cooking appliances, dishwashers, dryers, and microwaves. The replacement cycle for major appliances creates a self-sustaining demand floor that provides recession resilience.

To access detailed market analysis, Request Sample

Small appliances at 27.7% encompass kitchen preparation appliances, personal care, climate and comfort, and cooking assistance. Small Appliances' faster growth (~3.2% CAGR) reflects premiumization.

By Distribution Channel

Specialty stores lead at 34.8% (2025), anchored by dominant specialty appliance chains. Supermarkets and hypermarkets at 27.6% serve the impulse-adjacent small appliance purchase occasion.

E-commerce at 23.9% is the fastest growing at ~4.5% CAGR. Others at 13.7% encompass direct sales, builder-supplied appliances, and corporate procurement.

Regional Market Insights

|

Region |

Share (2025) |

Key Home Appliance Market Drivers & Characteristics |

|

Southeast |

41.7% |

Driven by a large urban population, higher household incomes, strong retail presence and concentration of major metropolitan areas. |

|

South |

19.8% |

Benefits from higher consumer spending, strong manufacturing activity, organized retail networks and growing adoption of premium and energy-efficient appliances. |

|

Northeast |

16.5% |

Supported by urban expansion, rising middle-class households, improving retail access and increasing demand for essential and affordable home appliances. |

|

Central-West |

11.2% |

Driven by population growth, expanding residential developments, rising household incomes and demand linked to agribusiness-led economic activity. |

|

North |

10.8% |

Supported by improving e-commerce logistics, increasing appliance penetration and growing consumer access in previously underserved areas. |

Brazil’s home appliances market is led by the Southeast, supported by high urbanization, higher incomes, organized retail networks, and great metropolitan demand. The South benefits from higher consumer formality, premium appliance adoption, and established manufacturing activity.

The Northeast is expanding through rising household incomes, urban growth, and wider retail access, while the Central-West is supported by residential development and agribusiness-led income growth. The North offers long-term potential through improving e-commerce logistics and increasing appliance penetration in underserved areas.

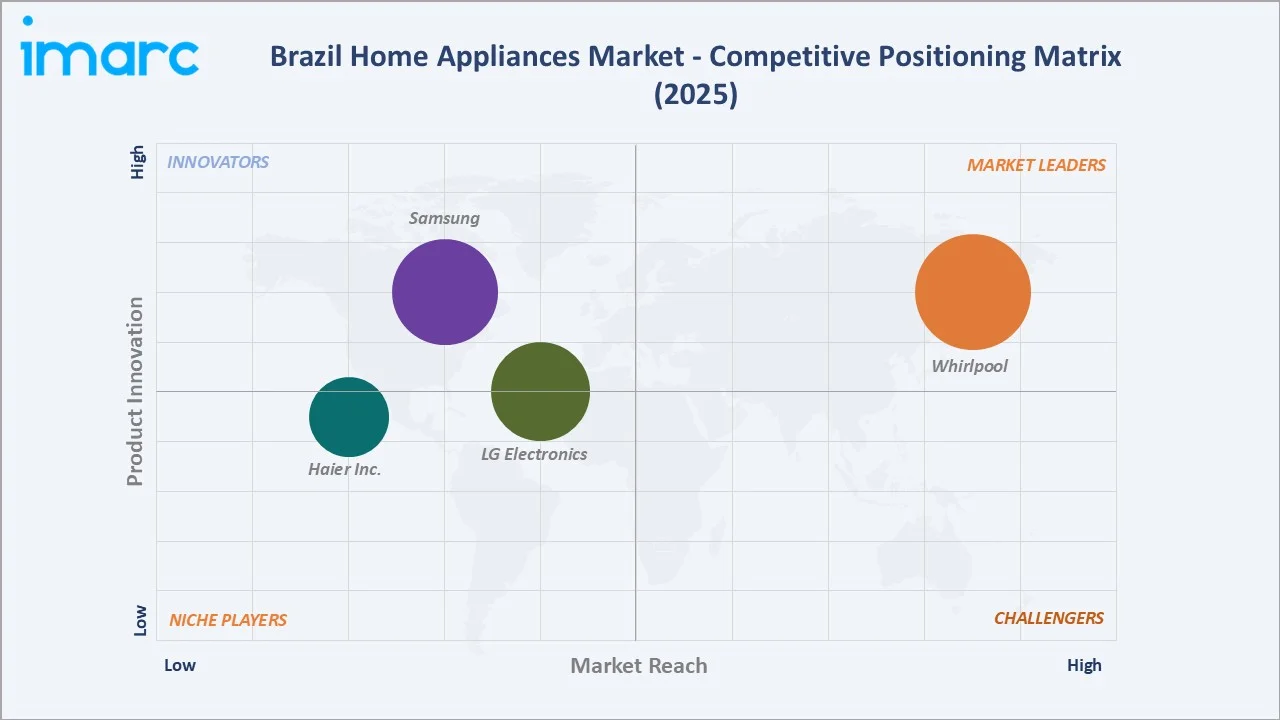

Competitive Landscape

Brazil's home appliance market competitive landscape is moderately concentrated at the major appliance tier. Small appliances are significantly more fragmented. The competitive dynamic is being reshaped by three forces: ZFM manufacturing-backed price aggression in air conditioners; the retail channel power in negotiating private label appliance and exclusive model arrangements; and the growing consumer preference for connected smart appliances, creating a technology differentiation tier above commodity major appliances.

|

Company Name |

Key Brands |

Market Position |

Core Strength |

|

Whirlpool |

Brastemp, Consul, KitchenAid, B.blend, Compra Certa, Compra Direta |

Market Leader |

Whirlpool is a dominant leader in the Brazilian home appliance market. It leads in kitchen and laundry, investing in local manufacturing, and focusing on innovation, sustainability, and high-tech manufacturing, often recognized as the top innovative company in the appliances sector. |

|

Samsung |

Samsung |

Innovator |

Samsung holds a major, premium-focused role in the Brazilian home appliances market, operating as a key competitor that drives innovation, smart technology adoption, and energy efficiency. |

|

LG Electronics |

LG |

Established Player |

LG Electronics holds a significant, premium position in the Brazilian home appliances market, focusing on high-end technology, local production, and smart, connected devices. |

|

Haier Inc. |

Haier |

Emerging Player |

Haier Inc. is rapidly expanding its footprint in Brazil's home appliances market, leveraging its global leadership in smart home technology to offer premium, IoT-enabled, and energy-efficient products. |

Brazil’s home appliances market is moderately concentrated, led by global brands, domestic manufacturers and large retail players competing across major and small appliance categories. Competition is driven by product innovation, energy efficiency, smart appliance technologies, local manufacturing capabilities and omnichannel distribution strategies. Companies are increasingly focusing on premiumization, connected appliances, e-commerce expansion and sustainable product development to strengthen market position.

Key Company Profiles

Whirlpool

Whirlpool is one of the leading players in Brazil’s home appliances market, operating through major brands such as Brastemp, Consul, KitchenAid, B.blend, Compra Certa, and Compra Direta, among others. The company has a strong presence across refrigerators, washing machines, cookers, dishwashers and small appliances, supported by local manufacturing operations and extensive distribution networks. Whirlpool focuses on innovation, energy-efficient products, smart appliance technologies and sustainability initiatives. Its strong brand portfolio and domestic production capabilities help maintain its leadership position in Brazil’s appliance industry.

- Key Brands: Brastemp, Consul, KitchenAid, B.blend, Compra Certa, and Compra Direta, among others.

- Strategic Focus: Strengthening its leadership in kitchen and laundry appliances through local manufacturing, energy-efficient product innovation and smart connected appliances.

Samsung

Samsung is a major player in Brazil’s home appliances market, offering a broad portfolio of refrigerators, washing machines, air conditioners, vacuum cleaners and smart home appliances. The company is recognized for integrating advanced technologies such as AI, IoT connectivity and SmartThings ecosystem features across its appliance range.

- Key Brands: Samsung

- Strategic Focus: Expanding premium and smart appliance adoption through AI-enabled products, IoT connectivity and integration with the SmartThings ecosystem.

Market Concentration Analysis

Brazil's home appliance market is moderately concentrated at the major appliance tier. The combined influence of refrigerators and washing machines creates a structural duopoly in these anchor categories, sustained by manufacturing scale advantages, brand equity depth, and authorized service network coverage that new entrants cannot replicate in short timeframes. The small appliance market is significantly more fragmented than the major appliances.

Investment & Growth Opportunities

Highest Growth Segments

E-commerce appliance channel (~4.5% CAGR), small appliances (~3.2% CAGR), connected smart appliances (~8% CAGR from small base), North and Northeast regional markets (~3.5-4.0% CAGR), air conditioner category (~5% CAGR from penetration growth), premium dishwasher (~4% CAGR from low penetration base), and first-time buyer appliance packages (~4% CAGR) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Emerging investment opportunities are centered on smart connected appliances, AI-enabled home ecosystems, and energy-efficient products driven by premiumization and sustainability trends. Additional opportunities are emerging in small appliances, e-commerce-led regional expansion, and localized manufacturing to reduce import dependence and improve supply-chain resilience.

Investment Themes

- Connected smart appliance ecosystem development: Investing in Brazilian Portuguese AI appliance integration and IoT ecosystem development creates a defensible premium that Chinese brands without local software engineering teams cannot easily match. Brands that achieve a connected appliance portfolio with Portuguese-language AI assistance by 2026-2027 position for the Brazilian smart home adoption wave that will follow as middle-class consumers upgrade conventional appliances.

- Northeast and North regional distribution expansion capturing underpenetrated growth markets through e-commerce logistics investment: The Northeast's 16.5% market share understates its relative consumer population, implying appliance underpenetration that e-commerce logistics improvement can progressively address. Brands and retailers investing in Northeast-specific logistics infrastructure capture above-national-average appliance demand growth as previously inaccessible consumers enter the formal appliance market through e-commerce.

Future Market Outlook (2026-2034)

Brazil's home appliances market is projected to grow from USD 13.00 Billion in 2025 to USD 16.82 Billion by 2034, delivering a 2.90% CAGR over the forecast period. The market's anchor value of USD 15.00 Billion in 2030 represents a Brazilian appliance industry at its most transformative commercial inflection since the democratization of the 1980s and 1990s, e-commerce has reached critical mass as a distribution channel, connected smart appliances have begun mainstream adoption beyond early adopters, and the delivery wave has fully seeded the Northeast and North regions with first-time appliance buyer households progressing to first replacement and upgrade cycles.

Three structural forces define Brazil's home appliance market growth through 2034 with confidence. The housing programme creates a structural demand floor that persists through economic cycles. The tightening cycle creates a regulatory-mandated replacement demand that is independent of economic growth. The digital commerce penetration of Brazil's appliance market is structural and irreversible.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025) including Brazilian country managers; commercial directors; retail operations executives; e-commerce category managers; consumer research from Brazil appliance consumer survey; appliance industry association data; and regional trade intelligence from regional appliance market experts in Northeast and North Brazil.

Secondary Research

Secondary research encompassed annual home appliance production and sales data; electronic goods statistics; energy efficiency market certification database; energy efficiency report; Brazil appliance market intelligence data; Brazil home appliances market report; company annual reports; household goods penetration data; consumer complaint data for home appliance category. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a category bottom-up model: (i) major appliances; (ii) small appliances, and e-commerce channel expansion enabling access to previously underserved geographic segments. Channel split modelled from the current trajectory with e-commerce share growth.

Brazil Home Appliances Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered |

|

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, E-commerce, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Whirlpool, Samsung, LG Electronics, Haier Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil home appliances market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Brazil home appliances market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the home appliances industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Home Appliances Market Report

Brazil's home appliances market reached USD 13.00 Billion in 2025, representing Latin America's largest national appliance market. The market is driven by major appliances at 72.3% (refrigerators, washing machines, and air conditioners as the primary categories), specialty stores leading distribution at 34.8% through Magazine Luiza installment credit infrastructure, Southeast regional dominance at 41.7% through Sao Paulo's consumer market concentration, and the housing programme creating structural new household formation appliance demand.

Brazil's home appliances market grows at 2.90% CAGR during 2026-2034, reaching USD 16.82 Billion by 2034. This growth reflects tightening driving replacement cycles for inefficient appliances, air conditioner penetration growth, small appliance premiumization through air fryer and premium coffee machine adoption, and e-commerce channel expansion extending market reach into secondary Brazilian cities previously underserved by specialty retail.

Major appliances lead at 72.3% through the essential household status of refrigerators and washing machines, creating sustained replacement-driven annual demand of 8-12 million units per category.

Specialty stores lead at 34.8% through Magazine Luiza, providing nationwide installment credit appliance retail.

The Southeast leads at 41.7% through Sao Paulo's metropolitan concentration, Rio de Janeiro's metro consumer market, and the region's superior e-commerce logistics infrastructure, enabling online appliance penetration.

Leading companies include Whirlpool, Samsung, LG Electronics, and Haier Inc., among others.

Brazil's appliance e-commerce market growth is the most significant distribution channel shift in Brazilian appliance retail in its history. Three forces drove this transformation: Pix expanded instant-payment options for online purchases and may support e-commerce adoption; BNPL fintech services; and e-commerce logistics investment, enabling reliable 2-person major appliance delivery.

Three priority opportunities: connected smart appliance ecosystem in Brazilian Portuguese; Northeast and North regional appliance market expansion through e-commerce logistics; and energy efficiency replacement cycle position.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade