Brazil Manufacturing Analytics Market Size, Share, Trends and Forecast by Component, Deployment Model, Application, Industry Vertical, and Region, 2026-2034

Brazil Manufacturing Analytics Market Summary:

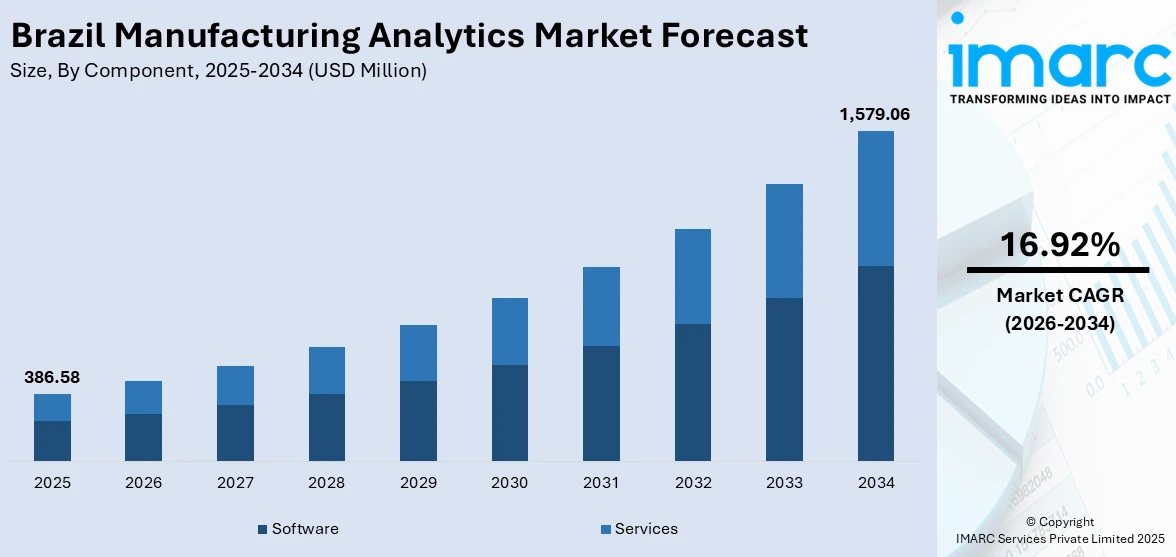

The Brazil manufacturing analytics market size was valued at USD 386.58 Million in 2025 and is projected to reach USD 1,579.06 Million by 2034, growing at a compound annual growth rate of 16.92% from 2026-2034.

The Brazil manufacturing analytics market is experiencing accelerated expansion as industrial enterprises increasingly embrace data-driven strategies to optimize production workflows and enhance operational visibility. Government-backed digital transformation programs, rising adoption of cloud computing infrastructure, and growing integration of artificial intelligence across factory floors are collectively strengthening demand. Advances in sensor technologies, expanding industrial internet of things ecosystems, and heightened emphasis on predictive operational capabilities are reshaping manufacturing practices, positioning Brazil as a key growth market for next-generation manufacturing analytics solutions and driving Brazil manufacturing analytics market share.

Key Takeaways and Insights:

- By Component: Software dominates the market with a share of 69.1% in 2025, driven by the growing demand for integrated analytics suites and real-time data visualization platforms across Brazilian manufacturing facilities.

- By Deployment Model: Cloud-based leads the market with a share of 63.5% in 2025, fueled by scalable infrastructure requirements and the flexibility of subscription-based analytics services for industrial applications.

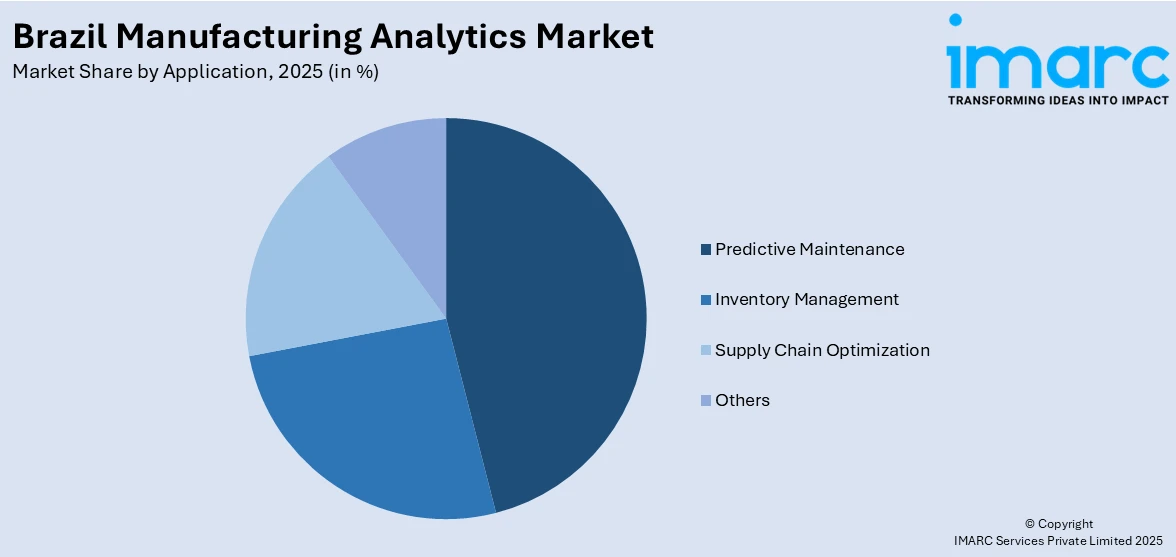

- By Application: Predictive maintenance represents the largest segment with a market share of 34.8% in 2025, owing to the critical need to minimize unplanned equipment downtime and extend machinery lifespan in capital-intensive manufacturing operations.

- By Industry Vertical: Automobile leads the market with a share of 22.6% in 2025, reflecting Brazil's position as Latin America's largest vehicle manufacturing hub with extensive automation and quality control requirements.

- By Region: Southeast dominated the market with approximately 46.9% revenue share in 2025, driven by the concentration of industrial infrastructure in São Paulo and Rio de Janeiro metropolitan areas and proximity to technology service providers.

- Key Players: The Brazil manufacturing analytics market exhibits a moderately competitive landscape, with established global technology providers expanding localized offerings alongside emerging domestic analytics firms. Market participants are increasingly focusing on cloud-native platforms, industry-specific solutions, and strategic partnerships to strengthen market positioning and capture growing industrial demand.

To get more information on this market Request Sample

The Brazil manufacturing analytics market is gaining momentum as the industrial sector accelerates digital modernization through coordinated public and private investment. Manufacturers across industries such as automotive, pharmaceuticals, electronics, and energy are increasingly adopting analytics solutions to enhance real-time production monitoring, optimize supply chains, and improve operational efficiency. Cloud-based analytics platforms are becoming more attractive due to their scalability, flexibility, and lower infrastructure requirements. At the same time, predictive maintenance and advanced process analytics are helping reduce unplanned downtime and improve asset utilization. The integration of artificial intelligence, industrial IoT, and edge computing is enabling more comprehensive, data-driven decision-making across factory operations. Together, these developments are strengthening analytical maturity within Brazilian manufacturing, improving competitiveness, and supporting the transition toward smarter, more resilient, and digitally connected industrial ecosystems.

Brazil Manufacturing Analytics Market Trends:

Rising Integration of Artificial Intelligence and Machine Learning in Production Analytics

Brazilian manufacturers are increasingly embedding artificial intelligence and machine learning capabilities into their analytics platforms to enhance decision-making accuracy and automate complex data interpretation processes. These technologies enable real-time pattern recognition, anomaly detection, and process optimization across production lines. For instance, in September 2024, Brazil’s Central Bank launched a Centre of Excellence in Data Science and AI, setting governance guidelines and evaluating generative AI applications[DA1] , signaling broader institutional commitment to AI-driven analytics that extends into industrial manufacturing domains and supports Brazil manufacturing analytics market growth.

Expansion of Edge Computing for Real-Time Manufacturing Insights

The deployment of edge computing infrastructure within Brazilian manufacturing facilities is accelerating, enabling data processing closer to production equipment and reducing latency for time-sensitive analytics workloads. This trend supports real-time quality monitoring, immediate fault detection, and faster operational responses without reliance on centralized cloud architectures. For instance, in September 2024, President Lula announced an investment of BRL 186.6 billion for developing IoT, AI, and big data infrastructure under Mission 4 of the Nova Indústria Brasil program[DA2] , directly supporting edge-enabled analytics deployment across the manufacturing sector.

Growing Adoption of Digital Twin Technology for Process Optimization

Digital twin adoption is accelerating among Brazilian manufacturers as companies seek virtual replicas of physical production systems to support simulation, monitoring, and predictive analysis. These models allow manufacturers to evaluate process changes, detect bottlenecks, and optimize resource use without interrupting ongoing operations. The growing availability of localized, cloud-based analytics platforms is further enabling advanced digital twin deployments by improving system responsiveness and data governance. As digital twins integrate with AI and industrial data streams, they are becoming valuable tools for enhancing operational efficiency, improving planning accuracy, and supporting more agile, data-driven manufacturing decision-making.

Market Outlook 2026-2034:

The Brazil manufacturing analytics market is set for strong growth over the coming years, driven by the rapid adoption of Industry 4.0 practices, expanding cloud availability, and wider use of artificial intelligence across factory operations. Public-sector digitalization initiatives, rising competitive pressure on local manufacturers, and increasing deployment of connected industrial equipment are collectively reinforcing the need for advanced analytics. As companies prioritize data-driven decision-making, operational transparency, and efficiency improvements, analytics platforms are becoming essential tools for optimizing production performance and strengthening long-term industrial competitiveness. The market generated a revenue of USD 386.58 Million in 2025 and is projected to reach a revenue of USD 1,579.06 Million by 2034, growing at a compound annual growth rate of 16.92% from 2026-2034.

Brazil Manufacturing Analytics Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Component |

Software |

69.1% |

|

Deployment Model |

Cloud-based |

63.5% |

|

Application |

Predictive Maintenance |

34.8% |

|

Industry Vertical |

Automobile |

22.6% |

|

Region |

Southeast |

46.9% |

Component Insights:

- Software

- Services

Software dominates with a market share of 69.1% of the total Brazil manufacturing analytics market in 2025.

The software segment’s commanding position reflects the strong enterprise preference for comprehensive analytics suites that integrate data collection, visualization, and advanced modeling capabilities within unified platforms. Brazilian manufacturers are prioritizing software investments to enable real-time production monitoring, quality assurance automation, and supply chain visibility. The growing availability of industry-specific software solutions tailored to automotive, pharmaceutical, and energy manufacturing workflows is further accelerating adoption rates across the industrial landscape.

Cloud-native software architectures are gaining strong momentum as they enable faster deployment, continuous updates, and flexible scalability without heavy upfront investment. Within Brazil’s evolving software landscape, application-focused platforms are seeing rising adoption, particularly in industrial environments. Manufacturing analytics vendors are increasingly embedding generative AI and natural language interfaces into their solutions, allowing plant operators and managers to interact with complex production data in a more intuitive way. This shift reduces reliance on specialized technical skills and supports wider, organization-wide use of analytics for operational decision-making and performance optimization.

Deployment Model Insights:

- Cloud-based

- On-premises

The Cloud-based segment leads with a share of 63.5% of the total Brazil manufacturing analytics market in 2025.

Cloud-based deployment has established clear market leadership as Brazilian manufacturers increasingly recognize the operational advantages of scalable, subscription-based analytics infrastructure. Cloud platforms eliminate the need for significant upfront hardware investments and enable manufacturers to access advanced computing resources on demand, which is particularly attractive for small and medium-sized enterprises with constrained capital budgets. The flexibility to scale analytics capabilities in response to fluctuating production demands and seasonal manufacturing cycles further reinforces cloud adoption.

The expansion of hyperscale data center infrastructure within Brazil is addressing previous concerns around data latency and sovereignty. For instance, in July 2025, Latin American data center firm Ascenty announced a new facility in São Paulo with a USD 55 million investment[DA3] , while ODATA announced a USD 450 million data center in Osasco, São Paulo, in March 2025.[DA4] These investments are reducing connectivity barriers and enabling Brazilian manufacturers to leverage cloud-based analytics with improved performance and full compliance with the country’s data protection regulations.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Predictive Maintenance

- Inventory Management

- Supply Chain Optimization

- Others

Predictive Maintenance represents the largest share at 34.8% of the total Brazil manufacturing analytics market in 2025.

Predictive maintenance has emerged as the foremost analytics application as Brazilian manufacturers increasingly deploy sensor-driven monitoring systems to anticipate equipment failures before they cause costly production interruptions. This application leverages machine learning algorithms and real-time equipment data to identify degradation patterns, optimize maintenance scheduling, and extend asset lifecycles. The economic imperative is compelling, as unplanned downtime in capital-intensive manufacturing environments can result in substantial financial losses and supply chain disruptions.

Brazilian manufacturers are increasingly shifting from reactive maintenance approaches to predictive strategies that rely on advanced analytics. Companies are adopting data-driven tools to anticipate equipment failures, optimize maintenance schedules, and improve overall operational reliability. The integration of analytics with industrial IoT systems is enhancing real-time equipment monitoring and fault detection, while AI-driven insights support better planning and asset utilization. This convergence of analytics, connected machinery, and operational expertise is transforming maintenance practices across manufacturing facilities, helping reduce downtime, extend equipment life, and strengthen productivity throughout Brazil’s industrial sector.

Industry Vertical Insights:

- Semiconductor and Electronics

- Energy and Power

- Pharmaceutical

- Automobile

- Heavy Metal and Machine Manufacturing

- Others

Automobile leads the highest revenue with a 22.6% share of the total Brazil manufacturing analytics market in 2025.

Brazil’s automotive sector is the largest adopter of manufacturing analytics, reflecting its position as Latin America’s principal vehicle manufacturing hub with extensive and complex production operations. Automotive manufacturers are deploying analytics across the entire production lifecycle, from body assembly and welding optimization to paint quality inspection and final assembly verification. The sector’s demanding quality standards, high production volumes, and competitive pressures necessitate continuous process monitoring and rapid defect identification.

Digital transformation within Brazil’s automotive industry is intensifying as manufacturers pursue efficiency improvements and adapt to evolving vehicle technologies. Major OEMs operating in Brazil, including operations in São Paulo and surrounding industrial regions, are implementing comprehensive analytics platforms that integrate production data with supply chain visibility. The government’s Mobilidade Verde e Inovação (Mover) program is further accelerating technological modernization within the automotive sector by providing tax incentives and research credits that encourage investment in advanced manufacturing technologies and analytics capabilities.

Regional Insights:

- Southeast

- South

- Northeast

- North

- Central-West

Southeast region exhibits a clear dominance with a 46.9% share of the total Brazil manufacturing analytics market in 2025.

The Southeast region’s commanding market position stems from its concentration of Brazil’s industrial infrastructure, technology ecosystems, and skilled workforce. São Paulo and Rio de Janeiro together command most of the manufacturing output and technology spending, supported by dense clusters of automotive, pharmaceutical, and electronics manufacturing operations. Proximity to hyperscale data centers, research universities, and technology service providers create a favorable ecosystem for analytics adoption that is difficult to replicate in other regions.

The region is further strengthening its analytics leadership through significant investments in digital infrastructure and innovation hubs. During the opening of Web Summit Rio 2025, the Rio de Janeiro city government launched the “Rio AI City” project, which aims to transform the city into the largest data center hub in Latin America and one of the ten largest globally. These infrastructure developments are creating additional capacity for cloud-based analytics workloads and attracting technology providers to expand their regional presence.

Market Dynamics:

Growth Drivers:

Why is the Brazil Manufacturing Analytics Market Growing?

Government-Led Industrial Digitalization and Policy Support

Brazil’s industrial modernization agenda is acting as a strong enabler for the adoption of manufacturing analytics across the country. Government-led programs focused on digital transformation are encouraging manufacturers to integrate advanced technologies such as analytics, artificial intelligence, and connected systems into their operations. Dedicated initiatives support both large industrial players and smaller manufacturers, helping them overcome cost, skill, and infrastructure barriers. Incentives that promote modernization of production assets further accelerate technology uptake. Together, these coordinated policy efforts are fostering a supportive ecosystem for digital manufacturing, driving sustained demand for analytics solutions that enhance productivity, efficiency, and global competitiveness.

Accelerating Industry 4.0 Technology Convergence

The convergence of multiple Industry 4.0 technologies is creating an increasingly compelling business case for manufacturing analytics deployment across Brazilian industries. The simultaneous maturation of industrial IoT sensors, cloud computing platforms, artificial intelligence algorithms, and edge processing capabilities enables manufacturers to implement comprehensive analytics ecosystems that deliver measurable operational improvements. Brazil’s industrial automation market reached USD 4,959.71 million in 2024, reflecting the expanding technological foundation upon which manufacturing analytics solutions are deployed. Manufacturers are increasingly combining connected sensors with cloud-based analytics platforms to gain comprehensive visibility across the entire production lifecycle, from input materials to final delivery. Analytics adoption is also expanding beyond efficiency and throughput optimization, supporting sustainability monitoring and regulatory compliance. By transforming operational data into environmental performance insights, these solutions enable industrial firms to track impacts more accurately, improve transparency, and embed sustainability considerations directly into day-to-day manufacturing decisions.

Rising Demand for Operational Efficiency and Competitive Resilience

Brazilian manufacturers are operating in an increasingly competitive environment that demands higher efficiency, tighter cost control, and consistent product quality across domestic and export markets. Volatile input prices, ongoing supply chain uncertainty, and rising expectations for customized products are pushing companies to rely more heavily on data-driven decision-making. Manufacturing analytics platforms help organizations uncover process inefficiencies, balance labor and material usage, and support structured continuous improvement initiatives grounded in real operational data. Beyond the factory floor, analytics adoption is expanding across the value chain, supporting smarter supply planning, procurement automation, and inventory optimization. The growing integration of advanced analytics and artificial intelligence reflects a strategic shift toward more agile, resilient, and responsive manufacturing operations nationwide.

Market Restraints:

What Challenges the Brazil Manufacturing Analytics Market is Facing?

Skilled Workforce Shortage and Digital Talent Gaps

The limited availability of professionals with combined expertise in data science, manufacturing operations, and analytics platform management presents a significant adoption barrier. Brazilian manufacturers often struggle to recruit and retain qualified personnel capable of deploying, configuring, and maintaining advanced analytics systems, particularly outside major metropolitan areas. This talent scarcity constrains implementation timelines and reduces the potential return on analytics investments.

Legacy System Integration Complexity

Many Brazilian manufacturing facilities operate with aging equipment and proprietary control systems that lack standardized data interfaces, creating substantial technical challenges for analytics platform integration. The heterogeneous nature of installed industrial infrastructure requires customized connectivity solutions and data harmonization efforts that increase deployment costs and extend implementation periods, discouraging adoption among resource-constrained manufacturers.

Data Security and Regulatory Compliance Concerns

Growing concerns around industrial data security and compliance with Brazil’s General Data Protection Law create hesitancy among manufacturers considering cloud-based analytics solutions. The sensitivity of production data, proprietary manufacturing processes, and supply chain information demands robust cybersecurity frameworks. Manufacturers in regulated sectors such as pharmaceuticals and defense face additional compliance requirements that complicate analytics deployment decisions.

Competitive Landscape:

The Brazil manufacturing analytics market features a moderately competitive environment characterized by the presence of established global technology providers alongside emerging domestic analytics firms and regional system integrators. Market participants are differentiating through industry-specific solution development, localized service delivery, and strategic technology partnerships. Competition is increasingly centered on cloud-native platform capabilities, artificial intelligence integration, and the ability to deliver rapid time-to-value for manufacturing clients. Companies are investing in local cloud infrastructure, Portuguese-language support, and region-specific compliance features to strengthen their competitive positioning. Strategic collaborations between analytics providers and industrial automation companies are creating integrated solution ecosystems that address the comprehensive digitalization needs of Brazilian manufacturers.

Recent Developments:

- In October 2025, Qlik launched its new cloud region in Brazil, hosted on Amazon Web Services, enabling Brazilian enterprises and public-sector organizations to deploy AI-driven analytics solutions locally with full compliance with the country’s General Data Protection Law and significantly reduced latency for data-intensive workloads.

- In September 2025, Rockwell Automation, Avvale, and ESGeo announced a collaboration to deliver operational technology-generated sustainability reporting solutions designed to help Brazilian industrial companies automate data collection, improve measurement accuracy, and enhance transparency in environmental performance tracking.

Brazil Manufacturing Analytics Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Components Covered |

Software, Services |

|

Deployment Models Covered |

Cloud-based, On-premises |

|

Applications Covered |

Predictive Maintenance, Inventory Management, Supply Chain Optimization, Others |

|

Industry Verticals Covered |

Semiconductor and Electronics, Energy and Power, Pharmaceutical, Automobile, Heavy Metal and Machine Manufacturing, Others |

|

Regions Covered |

Southeast, South, Northeast, North, Central-West |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The Brazil manufacturing analytics market size was valued at USD 386.58 Million in 2025.

The Brazil manufacturing analytics market is expected to grow at a compound annual growth rate of 16.92% from 2026-2034 to reach USD 1,579.06 Million by 2034.

Software, holding the largest revenue share of 69.1% in 2025, leads the Brazil manufacturing analytics market, driven by enterprise demand for integrated analytics suites that deliver real-time production monitoring, quality assurance automation, and comprehensive supply chain visibility.

Key factors driving the Brazil manufacturing analytics market include government-led industrial digitalization programs, accelerating Industry 4.0 technology convergence, rising demand for operational efficiency, expanding cloud infrastructure, and growing adoption of AI-driven predictive analytics.

Major challenges include skilled workforce shortages and digital talent gaps, legacy system integration complexity in aging manufacturing facilities, data security and regulatory compliance concerns, high initial implementation costs, and limited technology readiness among smaller manufacturers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)