Brazil Microinsurance Market Size, Share, Trends and Forecast by Product Type, Provider, Model Type, and Region, 2026-2034

Brazil Microinsurance Market Overview:

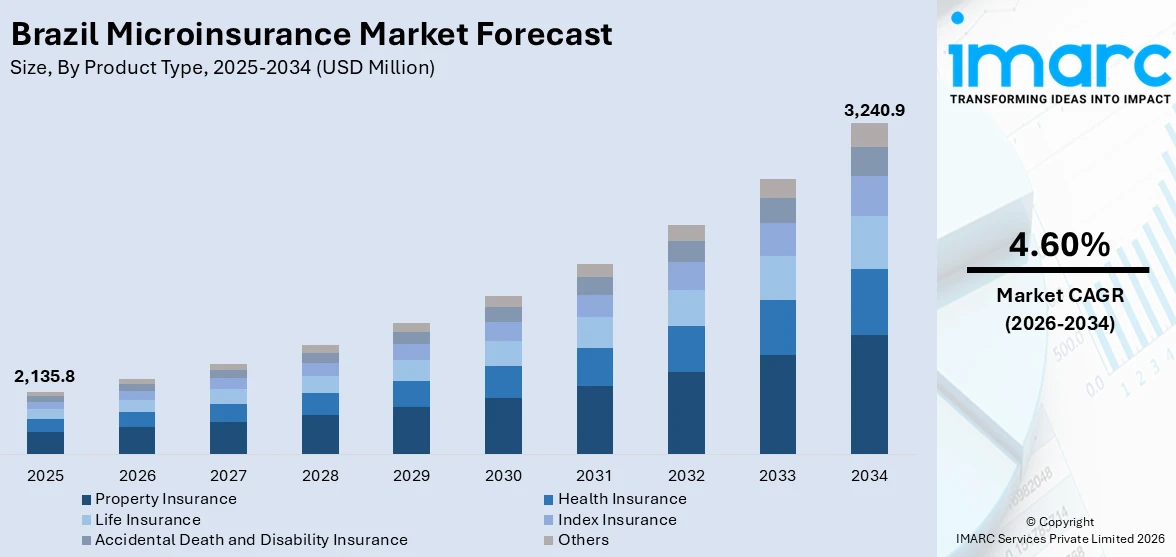

The Brazil microinsurance market size reached USD 2,135.8 Million in 2025. The market is projected to reach USD 3,240.9 Million by 2034, exhibiting a growth rate (CAGR) of 4.60% during 2026-2034. The market is expanding due to increasing awareness of affordable risk coverage among low-income populations and the growing penetration of digital platforms that simplify policy distribution. Rising exposure to climate risks, health emergencies, and natural disasters has further encouraged adoption. In combination, these trends continue to drive the Brazil microinsurance market share, strengthening the country’s inclusive financial protection ecosystem.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 2,135.8 Million |

| Market Forecast in 2034 | USD 3,240.9 Million |

| Market Growth Rate 2026-2034 | 4.60% |

Brazil Microinsurance Market Trends:

Regulatory Support Driving Market Expansion

Supportive regulatory frameworks have greatly fueled Brazil microinsurance market growth due to the encouragement of insurers with fintech innovators to develop coverage solutions that are affordable and low-risk. Regulatory initiatives aim for protecting policyholders, ensuring fair pricing, and easing broader access to microinsurance products. These projects matter much for fragile groups since they face weather, medical, and money dangers. Of late, policy reforms have come to allow insurers to then introduce flexible, pay-as-you-go, plus digital-first solutions, and these solutions align with global microinsurance best practices. More individuals are gaining access to microinsurance policies via collaborations. Government programs as well as social welfare initiatives happen to be expanding that reach. For example, when we integrate microinsurance alongside conditional cash transfers, health schemes, plus agricultural support programs, it ensures low-income households adopt it more widely with less risk. Regulators also simplify licensing requirements for microinsurance providers, they streamline reporting obligations, and they foster innovation by pilot programs and sandbox environments. Such steps allow surroundings for vendors trying technology-based answers while guarding customers. Brazil is positioned as a hub for insurance solutions, due to regulatory facilitation along with fintech innovation, which supports the Brazil microinsurance market's growth through improved coverage accessibility, affordability, and also operational efficiency.

To get more information on this market Request Sample

Climate and Health Risks Increasing Demand

Growing exposure to climate-related events along with health emergencies is what has driven the Brazil microinsurance market growth. Microinsurance protects from risk since low-income populations often lack financial buffers therefore these are disproportionately affected when extreme weather occurs when flooding happens when droughts arise as disease outbreaks emerge. Such vulnerabilities are becoming more known toward increasing demand for them. What is especially needed is coverage that is affordable and also tailored across both the urban and the rural areas. Now providers are responding using specialized products that do include crop insurance for small-scale farmers plus health microinsurance that then covers hospitalization plus outpatient care as well as weather-indexed protection for communities in flood-prone regions. Insurers are able to assess risk and also set premiums via leveraging of satellite data and also IoT devices along with analytics that are AI-powered. This guarantees financial sustainability while maintaining accessibility. Furthermore, collaborations among various NGOs, government agencies that exist, and private insurers can help to educate communities on risk management along with the benefits from microinsurance, which thus promotes higher enrollment rates. These schemes tackle climate with health-based weaknesses, so households gain better resilience then the complete microinsurance system grows too, building Brazil microinsurance sales and furthering broad fiscal safety.

Digital Platforms Enhancing Policy Accessibility

The Brazil microinsurance market growth has been strongly influenced by the rise of digital platforms and mobile technology, enabling insurers to reach underserved and remote populations efficiently. These platforms allow users to purchase, manage, and claim policies directly from smartphones, reducing the reliance on traditional agents and physical infrastructure. As financial inclusion increases, more individuals in rural and low-income urban areas are gaining access to microinsurance coverage tailored to their needs. Recent developments include partnerships between fintech companies and traditional insurers, creating integrated digital ecosystems that combine payment solutions, identity verification, and risk assessment. For instance, several mobile-first microinsurance platforms in Brazil now offer instant policy issuance, automated claims processing, and personalized coverage recommendations based on user behavior and data analytics. This integration not only increases the speed of service delivery but also reduces operational costs, allowing providers to offer lower premiums. The accessibility provided by digital channels has also improved transparency and trust in microinsurance products, which is critical for adoption among populations with limited prior exposure to formal insurance. By streamlining distribution and simplifying user experience, digital innovation is projected to remain a key driver for Brazil microinsurance market growth in the coming years.

.webp)

Brazil Microinsurance Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional level for 2026-2034. Our report has categorized the market based on product type, provider, and model type.

Product Type Insights:

- Property Insurance

- Health Insurance

- Life Insurance

- Index Insurance

- Accidental Death and Disability Insurance

- Others

The report has provided a detailed breakup and analysis of the market based on the product type. This includes property insurance, health insurance, life insurance, index insurance, accidental death and disability insurance, and others.

Provider Insights:

Access the comprehensive market breakdown Request Sample

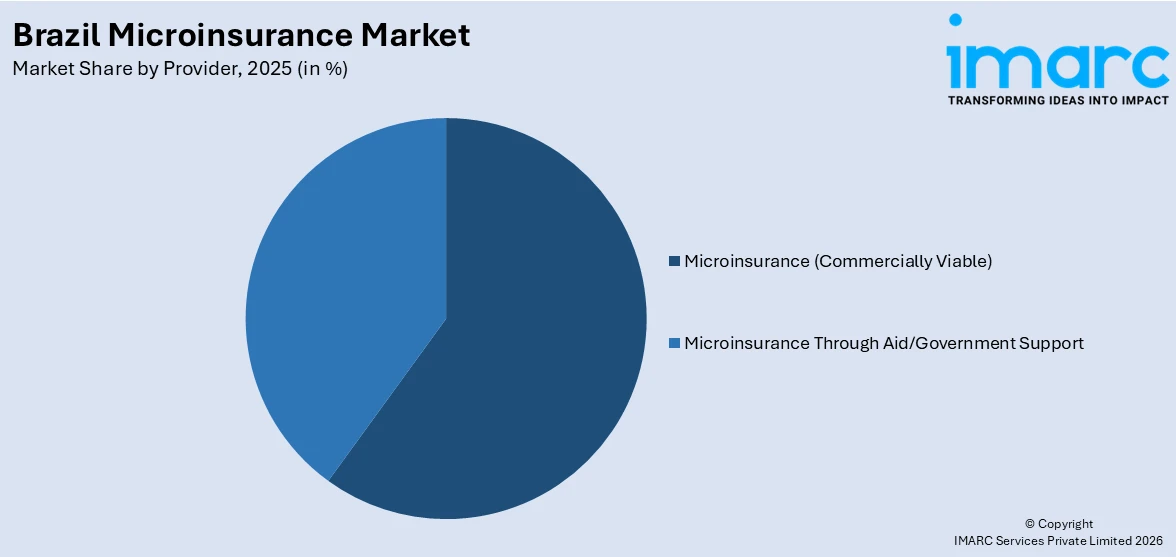

- Microinsurance (Commercially Viable)

- Microinsurance Through Aid/Government Support

A detailed breakup and analysis of the market based on the provider have also been provided in the report. This includes microinsurance (commercially viable) and microinsurance through aid/government support.

Model Type Insights:

- Partner Agent Model

- Full-Service Model

- Provider Driven Model

- Community-Based/Mutual Model

- Others

The report has provided a detailed breakup and analysis of the market based on the model type. This includes partner agent model, full-service model, provider driven model, community-based/mutual model, and others.

Regional Insights:

- Southeast

- South

- Northeast

- North

- Central-West

The report has also provided a comprehensive analysis of all the major regional markets, which include Southeast, South, Northeast, North, and Central-West.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Brazil Microinsurance Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Property Insurance, Health Insurance, Life Insurance, Index Insurance, Accidental Death and Disability Insurance, Others |

| Providers Covered | Microinsurance (Commercially Viable), Microinsurance Through Aid/Government Support |

| Model Types Covered | Partner Agent Model, Full-Service Model, Provider Driven Model, Community-Based/Mutual Model, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Brazil microinsurance market performed so far and how will it perform in the coming years?

- What is the breakup of the Brazil Microinsurance market on the basis of product type?

- What is the breakup of the Brazil Microinsurance market on the basis of provider?

- What is the breakup of the Brazil Microinsurance market on the basis of model type?

- What is the breakup of the Brazil microinsurance market on the basis of region?

- What are the various stages in the value chain of the Brazil microinsurance market?

- What are the key driving factors and challenges in the Brazil microinsurance market?

- What is the structure of the Brazil microinsurance market and who are the key players?

- What is the degree of competition in the Brazil microinsurance market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil microinsurance market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil microinsurance market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil microinsurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)