Brazil Oncology Drugs Market Size, Share, Trends and Forecast by Drug Class, Indication, Therapy Type, Distribution Channel, and Region, 2026-2034

Brazil Oncology Drugs Market Summary:

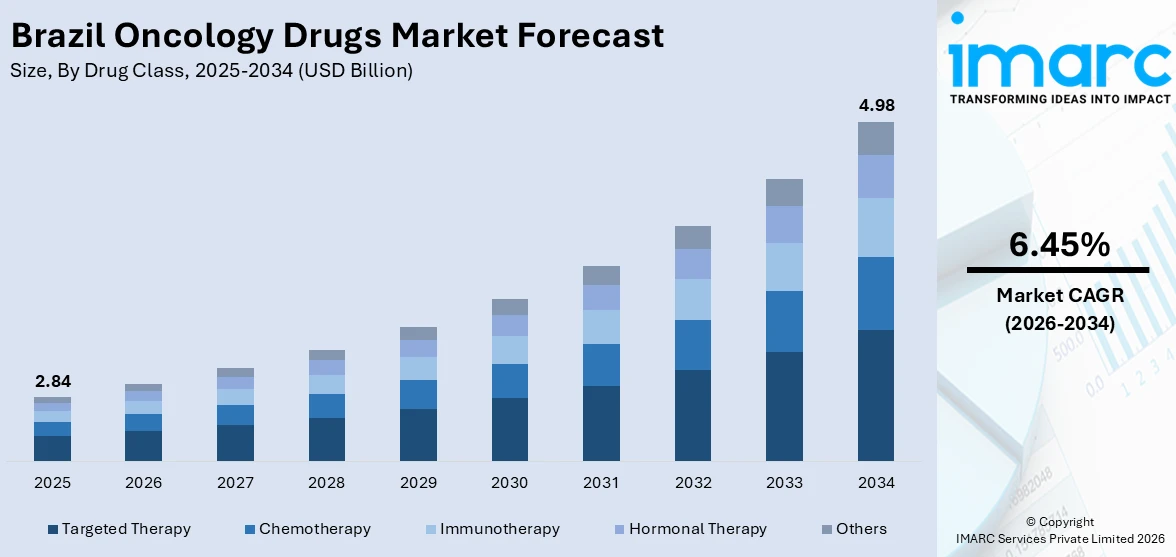

The Brazil oncology drugs market size was valued at USD 2.84 Billion in 2025 and is projected to reach USD 4.98 Billion by 2034, growing at a compound annual growth rate of 6.45% from 2026-2034.

The Brazil oncology drugs market is propelled by an escalating cancer burden across the country, expanding access to precision-based therapeutics, and strengthening regulatory infrastructure that accelerates the availability of novel treatment modalities. Rising healthcare expenditure in both public and private sectors, combined with growing adoption of targeted therapies and immunotherapies, continues to reshape the treatment landscape. The proliferation of biosimilar oncology agents and government-led technology incorporation processes further reinforce the Brazil oncology drugs market share.

Key Takeaways and Insights:

- By Drug Class: Targeted therapy dominates the market with a share of 38.7% in 2025, owing to its precision-based mechanism that selectively inhibits cancer cell growth while preserving healthy tissue, alongside increasing regulatory approvals and rising physician preference for molecularly guided treatment protocols.

- By Indication: Breast cancer leads the market with a share of 27.4% in 2025, driven by the high incidence of the disease among Brazilian women, expanding screening programs, and the growing utilization of advanced anti-HER2 agents and hormonal therapies.

- By Therapy Type: Combination therapy dominates the market with a share of 61.2% in 2025, reflecting the clinical superiority of multi-agent regimens in improving response rates and overall survival across diverse tumor types and disease stages.

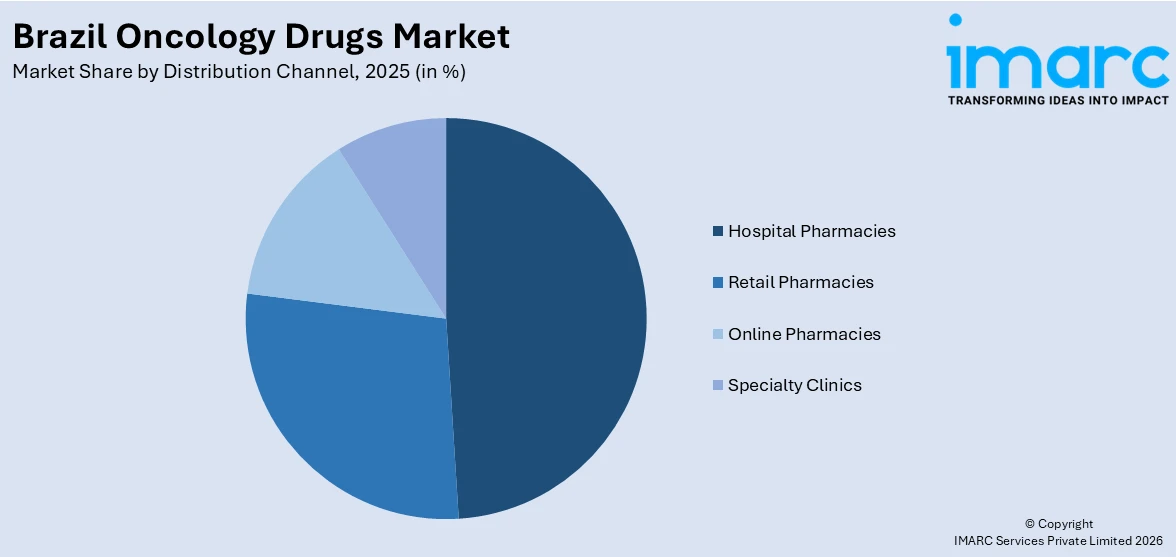

- By Distribution Channel: Hospital pharmacies lead the market with a share of 48.9% in 2025, supported by the concentration of oncology drug administration within hospital-based infusion centers and the specialized storage and handling requirements of parenteral cancer therapeutics.

- By Region: Southeast comprises the largest region with a share of 45.6% in 2025, driven by the concentration of premier oncology centers in São Paulo, Rio de Janeiro, and Minas Gerais, alongside higher diagnostic rates and superior healthcare infrastructure.

- Key Players: The market is highly competitive, driven by rising cancer incidence, expanding access through public and private healthcare systems, and increasing adoption of targeted therapies and immuno-oncology. Multinational pharmaceutical companies dominate innovative segments, while domestic manufacturers compete strongly in generics and biosimilars.

To get more information on this market Request Sample

The Brazil oncology drugs market is undergoing significant transformation as the country confronts a rising cancer burden estimated at 704,000 new cases annually during the 2023–2025, according to the National Cancer Institute. The South and Southeast regions together account for approximately 70% of all incident cases, reflecting concentrated diagnostic capacity and population density. Breast cancer remains the most prevalent malignancy among women, with an estimated 73,610 new cases per year, followed by prostate cancer with 71,730 cases and colorectal cancer with 45,000 cases annually. This epidemiological profile is driving robust demand for targeted therapies and combination treatment regimens. The regulatory framework, anchored by ANVISA for market authorization and CONITEC for public health system incorporation, continues to evolve with streamlined approval pathways for innovative oncology agents. The expansion of private healthcare coverage further catalyzes adoption of advanced treatment protocols across the country.

Brazil Oncology Drugs Market Trends:

Rising adoption of precision oncology and biomarker-driven treatments

The Brazil oncology drugs market is experiencing a pronounced shift toward precision medicine, with molecular profiling increasingly guiding therapeutic decisions. The growing availability of next-generation sequencing platforms in major cancer centers has expanded access to biomarker testing for mutations such as EGFR, ALK, and HER2. Between March 2022 and March 2024, ANVISA approved 15 new anticancer agents, constituting over 40.54% of all new drug registrations during that period, with a substantial proportion targeting specific molecular alterations. This trend reinforces the movement away from empirical chemotherapy toward individualized, genomically informed treatment strategies.

Expanding biosimilar penetration in oncology therapeutics

Oncology biosimilars are gaining significant traction in Brazil as a pathway to broaden patient access and reduce treatment costs. As such, in September 2025, ANVISA issued favorable opinions for four new biosimilars, including Bisintex, a trastuzumab biosimilar manufactured by Shanghai Henlius and marketed by Abbott Brazil for HER2-positive breast and gastric cancers. Brazil now ranks as the fourth-largest global market for approved biosimilars, with 66 follow-on biological products authorized as of late 2025. The availability of cost-effective biosimilar alternatives is enabling wider prescription of essential oncology biologics across both public and private healthcare channels.

Growing judicial demand for immunotherapy access

Patient litigation to access immunotherapy agents through the public health system has emerged as a defining feature of the Brazil oncology landscape. A 2025 cross-sectional study analyzing 1,288 technical notes issued by the Center for Technical Support of the Judiciary (NAT-Jus) revealed that pembrolizumab alone, which holds 36 ANVISA-approved indications by May 2025, accounted for a significant share of judicial drug requests. Approximately 66% of technical notes received favorable rulings, highlighting unmet demand for checkpoint inhibitors in the public system and pressuring policymakers to accelerate CONITEC incorporation timelines.

Market Outlook 2026-2034:

The Brazil oncology drugs market is positioned for sustained expansion as the country strengthens its pharmaceutical regulatory infrastructure and invests in broadening access to advanced cancer therapeutics. In accordance with this, increasing cancer incidence driven by population aging, expanding private insurance coverage, and the accelerating incorporation of targeted therapies and immunotherapies into clinical protocols are expected to reinforce growth momentum. An industry report indicates that currently around 11% of the population is aged 65 and above, and this proportion is projected to double by 2040, when older adults are expected to outnumber children in the country. The ongoing diversification of the biosimilar landscape, regulatory reforms enabling faster drug approvals, and rising investment by multinational pharmaceutical companies in clinical trial infrastructure across Brazil further underpin the favorable market trajectory throughout the forecast period. The market generated a revenue of USD 2.84 Billion in 2025 and is projected to reach a revenue of USD 4.98 Billion by 2034, growing at a compound annual growth rate of 6.45% from 2026-2034.

Brazil Oncology Drugs Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Drug Class |

Targeted Therapy |

38.7% |

|

Indication |

Breast Cancer |

27.4% |

|

Therapy Type |

Combination Therapy |

61.2% |

|

Distribution Channel |

Hospital Pharmacies |

48.9% |

|

Region |

Southeast |

45.6% |

Drug Class Insights:

- Chemotherapy

- Targeted Therapy

- Immunotherapy

- Hormonal Therapy

- Others

Targeted therapy dominates the market with a share of 38.7% of the total Brazil oncology drugs market in 2025.

The rise of targeted treatments in Brazil demonstrates how medical professionals worldwide now use molecular cancer testing to develop treatments that specifically target tumor signaling pathways while causing less harm to healthy body systems. Tyrosine kinase inhibitors and monoclonal antibodies and antibody-drug conjugates have established themselves as essential components in breast cancer and lung cancer and colorectal cancer treatment guidelines. The segment's dominance is reinforced by the expanding biomarker testing infrastructure in major cancer centers across São Paulo, Rio de Janeiro, and Porto Alegre, enabling clinicians to match patients with appropriate precision therapies based on genomic profiling results.

The continued growth of the targeted therapy segment is further supported by regulatory developments that facilitate faster access to innovative agents. Globally, the targeted therapy drugs category captured the largest oncology market share in 2024, driven by superior efficacy and favorable side-effect profiles compared to conventional chemotherapy. In Brazil, the private healthcare sector, which finances approximately 77% of total oncology expenditure, provides rapid access to ANVISA-approved targeted agents, while the public system gradually incorporates these treatments through the CONITEC evaluation framework, thereby expanding the addressable patient population for precision-based cancer therapeutics.

Indication Insights:

- Lung Cancer

- Breast Cancer

- Colorectal Cancer

- Prostate Cancer

- Leukemia & Lymphoma

- Melanoma

- Others

Breast cancer leads the market with a share of 27.4% of the total Brazil oncology drugs in 2025.

Breast cancer represents the highest-incidence malignancy among Brazilian women and the leading cause of cancer-related mortality in the female population across all geographic regions of the country. The substantial and growing disease burden drives significant pharmaceutical consumption underpin the segment's market-leading position in Brazil.

The therapeutic landscape for breast cancer in Brazil continues to evolve with the introduction of advanced treatment combinations. Approximately 15–25% of breast cancers are classified as HER2-positive, a subtype that responds to targeted agents including trastuzumab, pertuzumab, and newer antibody-drug conjugates. The availability of trastuzumab biosimilars in Brazil, has expanded access to this essential therapy across both public and private settings. The convergence of high disease prevalence, diversifying treatment options, and growing biosimilar availability collectively sustains breast cancer as the dominant indication segment.

Therapy Type Insights:

- Monotherapy

- Combination Therapy

Combination therapy accounts for the highest share of 61.2% of the total Brazil oncology drugs market in 2025.

Combination therapy's dominant position reflects the well-established clinical evidence demonstrating that multi-agent treatment regimens achieve superior tumor response rates, extended progression-free survival, and improved overall survival outcomes compared to single-agent approaches across most cancer types and disease stages. In Brazil, combination protocols pairing targeted agents with chemotherapy or immunotherapy have become the standard of care for breast, lung, and colorectal cancers. The approach effectively addresses tumor heterogeneity by simultaneously targeting multiple growth pathways, reducing the likelihood of therapeutic resistance and improving long-term patient outcomes across diverse populations.

The expanding adoption of combination therapy in Brazil is reinforced by evolving global treatment paradigms. In December 2025, the United States FDA approved trastuzumab deruxtecan plus pertuzumab as the first new first-line treatment in over a decade for HER2-positive metastatic breast cancer, based on DESTINY-Breast09 trial data demonstrating a 44% reduction in disease progression risk. Such landmark approvals signal the trajectory of future treatment standards that Brazilian oncologists and regulatory bodies are expected to follow, further consolidating the dominance of combination regimens in clinical practice.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Clinics

Hospital pharmacies hold the largest share of 48.9% of the total Brazil oncology drugs market in 2025.

Hospital pharmacies serve as the primary distribution point for oncology therapeutics in Brazil owing to the predominantly parenteral nature of cancer drug administration and the stringent requirements for specialized compounding, cold-chain storage, and clinical oversight during infusion-based treatments. The country's oncology care infrastructure is concentrated within hospital-based settings, where multidisciplinary teams comprising oncologists, pharmacists, and nursing staff manage complex treatment protocols. Brazil has 7,309 hospitals, with specialized oncology services concentrated primarily in the Southeast and South regions, where advanced treatment capabilities align with higher cancer diagnostic rates and patient volumes.

The sustained dominance of hospital pharmacies is further underpinned by the Brazilian regulatory framework, which mandates that high-cost oncology drugs administered through the SUS public health system be dispensed and supervised within accredited hospital environments. Total annual cancer treatment expenditure in Brazil is estimated at approximately BRL 20 Billion (USD 3.57 Billion) across public and private systems, with hospitalization costs representing a significant proportion of overall spending. The private healthcare sector, covering approximately 22% of the population through supplementary insurance, channels oncology treatments predominantly through hospital-based clinics, reinforcing the central role of hospital pharmacies in drug distribution.

Regional Insights:

- Southeast

- South

- Northeast

- North

- Central-West

The Southeast region exhibits clear dominance with a 45.6% share of the total Brazil oncology drugs market in 2025.

The Southeast region's leadership in the Brazil oncology drugs market reflects its unparalleled concentration of healthcare infrastructure, population density, and diagnostic capacity. Accordingly, São Paulo’s Rebouças Avenue emerged as a new healthcare hub, attracting major hospitals like Sabará, Albert Einstein, Santa Joana, and Hospital das Clínicas, driving BRL 1.5 Billion in investments and spurring outpatient and research facility development. Home to São Paulo, Rio de Janeiro, and Minas Gerais, the region hosts the country's most advanced cancer treatment centers and the largest pool of specialized oncologists.

In addition, the region benefits from stronger private health insurance penetration and higher healthcare spending per capita, enabling faster adoption of innovative oncology therapies, including targeted drugs and immunotherapies. Proximity to major research institutions and pharmaceutical company headquarters further supports clinical trial activity and early access programs, reinforcing the Southeast’s dominance in advanced cancer care and high-value oncology drug consumption across Brazil.

Market Dynamics:

Growth Drivers:

Why is the Brazil Oncology Drugs Market Growing?

Escalating cancer incidence driven by demographic transition and population aging

Brazil is undergoing a significant demographic shift characterized by rapid population aging and rising noncommunicable disease prevalence, which collectively amplify the demand for oncology therapeutics. IBGE reported that Brazil’s elderly population (60+) nearly doubled from 8.7% in 2000 to 15.6% in 2023 and is projected to reach 37.8% of the population by 2070. This aging trajectory directly increases the incidence of age-related malignancies including prostate, breast, colorectal, and lung cancers. The expanding patient pool creates sustained demand across all drug classes, from conventional chemotherapy to advanced immunotherapy and targeted treatments.

Expanding private healthcare coverage and oncology expenditure

The growth of private health insurance coverage in Brazil is creating a parallel pathway for accelerated access to innovative oncology drugs outside the constraints of the public health system. Private insurers are required to cover all ANVISA-approved oncology treatments, including oral medications and intravenous infusions, immediately upon registration. This regulatory mandate ensures that newly approved targeted therapies, immunotherapy agents, and combination protocols reach privately insured patients without the delays associated with CONITEC public system incorporation, thereby accelerating market adoption.

Regulatory modernization and biosimilar market expansion

Brazil's regulatory environment for oncology drugs is evolving to facilitate faster access to both innovative therapies and cost-effective biosimilar alternatives. In June 2024, ANVISA published Resolution RDC 875, amending existing regulations to streamline the biosimilar registration pathway through enhanced comparability development provisions. In the oncology space specifically, biosimilar versions of trastuzumab, rituximab, and bevacizumab are now commercially available, reducing treatment costs compared to reference products and expanding therapeutic access across both public and private healthcare channels.

Market Restraints:

What Challenges the Brazil Oncology Drugs Market is Facing?

Protracted timelines for public health system drug incorporation

The gap between ANVISA marketing approval and CONITEC-mediated incorporation into the SUS public health system creates substantial access delays for cancer patients. Even after regulatory clearance, additional evaluations and bureaucratic procedures prolong the timeline before new therapies become available to the majority of the population relying on public healthcare. As a result, many innovative oncology treatments, including advanced immunotherapies, remain inaccessible through the public system, limiting patient options and slowing adoption of cutting-edge therapies in Brazil.

Significant disparities in cancer care infrastructure across regions

Brazil’s vast geography produces marked regional inequalities in oncology care, constraining market reach outside major metropolitan areas. While urban centers in the South and Southeast host most specialized facilities, the North and Northeast face shortages of oncology specialists, diagnostic equipment, and accredited treatment centers. Smaller hospitals dominate the landscape, with few offering comprehensive cancer services. These disparities restrict the availability and utilization of advanced therapies in underserved areas, creating unequal access to quality cancer care across the country.

High treatment costs and currency-related pricing pressures

The high cost of innovative oncology drugs, coupled with currency volatility, creates persistent challenges for market expansion. The expense of advanced treatments often exceeds public healthcare budgets, limiting incorporation into SUS formularies and reducing patient access. Additionally, fluctuations in the Brazilian real increase the cost of imported medications, putting further pressure on healthcare providers and payers. This combination of elevated pricing and financial constraints hinders widespread adoption of targeted therapies and immunotherapies, particularly in public and resource-limited healthcare settings.

Competitive Landscape:

The Brazil oncology drugs market exhibits a moderately fragmented competitive structure dominated by multinational pharmaceutical companies with established portfolios in targeted therapy, immunotherapy, and chemotherapy. Key players leverage product differentiation, clinical trial investments, and regulatory engagement strategies to maintain market positioning. Strategic activities include biosimilar launches to capture price-sensitive segments, expansion of clinical trial sites across Brazilian institutions, and partnerships with local distributors to strengthen last-mile drug delivery. The competitive environment is further shaped by the growing presence of biosimilar manufacturers that challenge originator pricing and expand therapeutic access across both public and private healthcare channels.

Recent Developments:

- In October 2025, Brazil and China signed an agreement to jointly produce medicines for cancer, diabetes, obesity, and autoimmune diseases. The partnership includes domestic production of long-acting insulin, technology transfer, and aims to expand patient access while strengthening Brazil’s Unified Health System (SUS).

- In February 2026, Brazil and India established production agreements for oncology biosimilars which include nivolumab and pertuzumab through their Productive Development Partnerships (PDPs). The initial investment of USD 140 Million will achieve two goals which include cost reduction and establishment of a dependable supply chain. The companies involved in the project are Bionovis Dr. Reddy's Laboratories and Biocon Biologics do Brasil.

Brazil Oncology Drugs Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Drug Classes Covered |

Chemotherapy, Targeted Therapy, Immunotherapy, Hormonal Therapy, Others |

|

Indications Covered |

Lung Cancer, Breast Cancer, Colorectal Cancer, Prostate Cancer, Leukemia & Lymphoma, Melanoma, Others |

|

Therapy Types Covered |

Monotherapy, Combination Therapy |

|

Distribution Channels Covered |

Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Specialty Clinics |

|

Regions Covered |

Southeast, South, Northeast, North, Central-West |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Brazil Oncology Drugs Market Report

The Brazil oncology drugs market size was valued at USD 2.84 Billion in 2025.

The Brazil oncology drugs market is expected to grow at a compound annual growth rate of 6.45% from 2026-2034 to reach USD 4.98 Billion by 2034.

Targeted therapy dominated the market with a share of 38.7%, driven by expanding biomarker testing infrastructure, rising availability of tyrosine kinase inhibitors and monoclonal antibodies, and growing physician preference for precision-based treatment protocols.

Key factors driving the Brazil oncology drugs market include escalating cancer incidence linked to population aging, expanding private healthcare coverage enabling rapid access to innovative therapies, regulatory modernization accelerating drug approvals, and growing biosimilar availability.

Major challenges include protracted timelines for drug incorporation into the public health system, significant regional disparities in oncology care infrastructure, high treatment costs exacerbated by currency depreciation, limited CONITEC approvals for immunotherapy agents, and financing gaps between optimal and reimbursed treatment protocols.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)