Brazil Smart Meters Market Size, Share, Trends and Forecast by Product, Technology, End Use, and Region, 2026-2034

Brazil Smart Meters Market Summary:

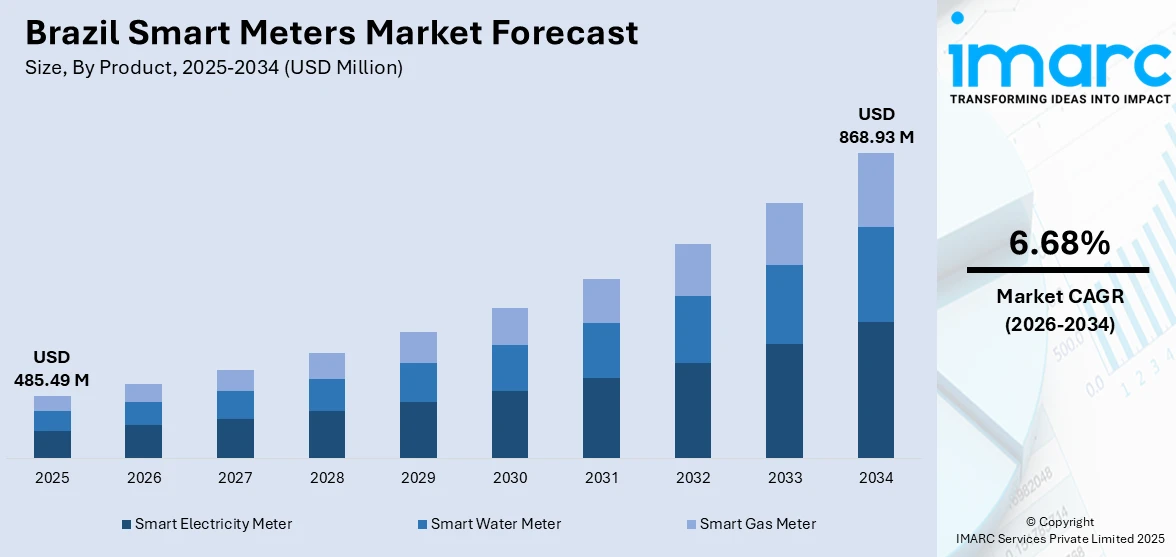

The Brazil smart meters market size was valued at USD 485.49 Million in 2025 and is projected to reach USD 868.93 Million by 2034, growing at a compound annual growth rate of 6.68% from 2026-2034.

The Brazil smart meters market is expanding steadily as utilities accelerate grid digitalization to address persistent energy losses and enhance operational efficiency. Regulatory initiatives from ANEEL and the Ministry of Mines and Energy are establishing clear deployment mandates, while growing distributed generation integration necessitates advanced metering solutions. Rising residential electricity consumption, expanding renewable energy capacity, and increasing consumer demand for real-time usage monitoring are reinforcing the transition from conventional meters to intelligent metering infrastructure across the country.

Key Takeaways and Insights:

- By Product: Smart electricity meter dominates the market with a share of 63.8% in 2025, owing to nationwide regulatory mandates for electricity grid modernization, significant utility-led rollouts, and the pressing need to reduce non-technical losses across distribution networks.

- By Technology: AMI (Advanced Metering Infrastructure) leads the market with a share of 71.2% in 2025, driven by its superior two-way communication capabilities, remote management functionalities, and alignment with national smart grid modernization strategies prioritizing real-time data exchange.

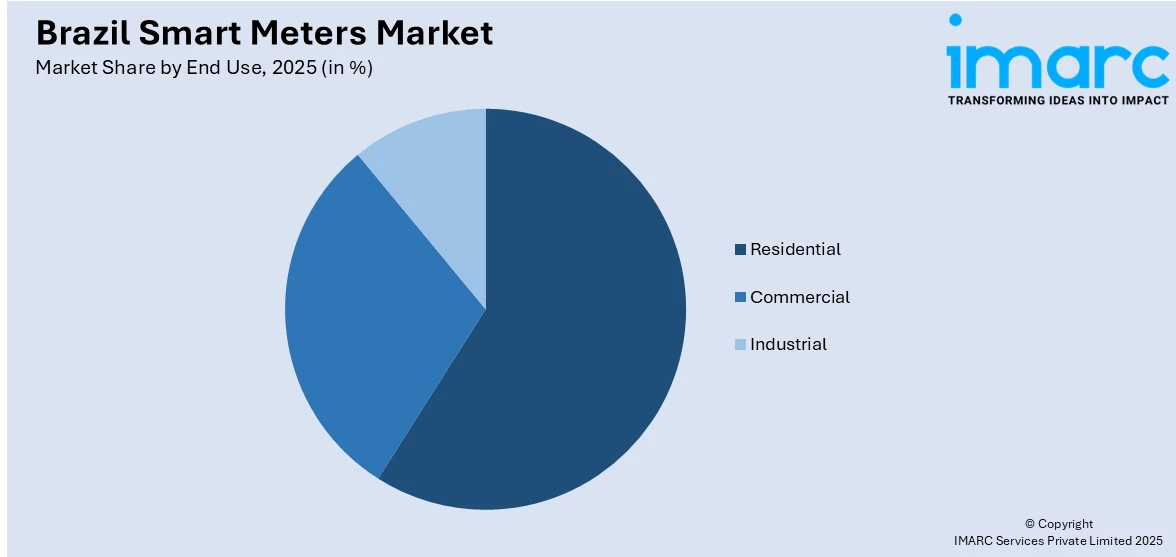

- By End Use: Residential represents the largest segment with a market share of 58.6% in 2025, reflecting government-driven programs targeting household energy monitoring, the expansion of distributed generation, and growing consumer interest in real-time consumption tracking.

- By Region: Southeast exhibits a clear dominance in the market with 44.9% share in 2025, driven by the concentration of major utilities including Enel São Paulo and CPFL Energia, higher urbanization rates, and significant infrastructure investment across São Paulo and Minas Gerais.

- Key Players: Key players are shaping the Brazil smart meters market by investing in locally manufactured metering solutions, expanding advanced metering infrastructure, forming strategic technology partnerships, and strengthening nationwide distribution to accelerate grid digitalization.

To get more information on this market Request Sample

The Brazil smart meters market is undergoing a transformative phase as utilities, regulatory bodies, and technology providers collaborate to modernize the nation’s aging electricity infrastructure. The country’s persistent challenge of high energy losses—particularly non-technical losses linked to meter tampering and illegal connections—has made smart metering a strategic priority for distribution companies seeking greater transparency and revenue protection. The growing integration of distributed solar generation across residential and commercial segments is further necessitating advanced metering solutions capable of managing bidirectional power flows and enabling time-of-use tariff structures. For instance, in October 2025, Brazil’s Ministry of Mines and Energy launched a public consultation on guidelines for nationwide smart meter deployment, proposing the installation of smart meters in at least four percent of consumer units in each concession area within twelve months. Policy encouragement, expanding digital infrastructure, and rising consumer awareness around energy management are fostering a supportive ecosystem for the sustained adoption of intelligent metering technologies across Brazil’s diverse regional markets.

Brazil Smart Meters Market Trends:

Government-Led Regulatory Push for Nationwide Smart Meter Deployment

Brazil is witnessing an accelerated regulatory push to formalize smart meter deployment across distribution concessions. The Ministry of Mines and Energy has initiated structured consultations aimed at establishing minimum installation benchmarks and interoperability standards for utility companies. These frameworks seek to reduce operational losses, improve billing transparency, and integrate digital platforms for enhanced grid management. Regulatory clarity is encouraging distribution companies to commit substantial capital toward metering infrastructure upgrades, positioning the country for a significant expansion in Brazil smart meters market growth.

Utility-Driven Large-Scale Smart Grid Modernization Programs

Major distribution utilities are spearheading ambitious smart grid programs that encompass meter replacement, network automation, and digital platform integration. For instance, in February 2025, Copel reported reaching one million smart meters installed across 119 municipalities in Paraná state as part of its Smart Electric Grid Program, the largest energy distribution modernization initiative in Brazil. These utility-led investments are transforming energy monitoring, enabling remote fault detection, and reducing vehicle-based operations, thereby lowering carbon emissions associated with manual meter reading processes.

Integration of Artificial Intelligence and Advanced Analytics in Grid Operations

The adoption of artificial intelligence and advanced data analytics is enhancing the intelligence layer of smart metering ecosystems across Brazil. Utilities are deploying AI-powered platforms capable of identifying grid faults in real time, optimizing load distribution, and predicting consumption anomalies. For example, in August 2025, Eletrobras expanded its partnership with C3 AI to deploy the Grid Intelligence platform across its entire national transmission network, building on a 2024 pilot at ten substations. These developments are strengthening grid resilience and enabling predictive maintenance capabilities.

Market Outlook 2026-2034:

The Brazil smart meters market is expected to grow at a significant rate due to the regulatory requirements, investment plans of the utilities, and the increasing adoption of smart energy management solutions among consumers. The current adoption of Advanced Metering Infrastructure in the residential, commercial, and industrial sectors is expected to contribute to the increased revenue streams. Collaborations between the local utilities and international technology companies, along with financing from development banks for the digitalization of the meters, are expected to further boost the growth trajectory of the market. With the increasing adoption of distributed generation and time-of-use pricing, the need for smart metering solutions is expected to increase in all regions. The market generated a revenue of USD 485.49 Million in 2025 and is projected to reach a revenue of USD 868.93 Million by 2034, growing at a compound annual growth rate of 6.68% from 2026-2034.

.webp)

Brazil Smart Meters Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Smart Electricity Meter |

63.8% |

|

Technology |

AMI (Advanced Metering Infrastructure) |

71.2% |

|

End Use |

Residential |

58.6% |

|

Region |

Southeast |

44.9% |

Product Insights:

- Smart Electricity Meter

- Smart Water Meter

- Smart Gas Meter

Smart electricity meter dominates with a market share of 63.8% of the total Brazil smart meters market in 2025.

Smart electricity meters constitute the backbone of Brazil’s metering modernization efforts, driven by regulatory directives from ANEEL and extensive utility-led deployment programs targeting loss reduction and grid transparency. The country’s electricity distribution sector—serving over 90 million consumer units—faces persistent challenges with non-technical losses, making intelligent electricity metering a strategic imperative. For instance, in December 2025, Enel Distribuição São Paulo reached the milestone of 2 million smart electricity meters installed across its concession area serving eight million customers in 24 municipalities.

The ongoing transition from electromechanical to digital electricity meters is being supported by substantial public and private investment. Distribution companies are leveraging smart electricity meters to enable remote meter reading, real-time consumption monitoring, and automated fault detection, significantly reducing operational costs and improving service reliability. Moreover, Brazil’s National Energy Plan 2050 identifies electricity metering digitalization as a cross-cutting priority, and development bank financing is accelerating procurement cycles.

Technology Insights:

- AMI (Advanced Metering Infrastructure)

- AMR (Automatic Meter Reading)

AMI (Advanced Metering Infrastructure) leads with a share of 71.2% of the total Brazil smart meters market in 2025.

Advanced Metering Infrastructure has emerged as the preferred technology platform for Brazil's smart meter deployments, offering bidirectional communication between meters and utility management systems. AMI enables real-time data exchange, remote connection and disconnection, fraud detection, and integration with digital billing platforms, which are critical functionalities for addressing Brazil's high non-technical loss rates. The technology supports granular interval consumption tracking and automated data transmission, eliminating the need for manual meter readings across vast concession areas. Distribution utilities are increasingly favoring AMI over legacy one-way systems due to its capacity to support demand response programs, power quality monitoring, and time-of-use tariff implementation, making it essential for managing the growing complexity of modern distribution networks.

The dominance of AMI over legacy AMR systems reflects the evolving demands of Brazil’s distribution sector, where one-way meter reading capabilities are insufficient for modern grid management requirements. AMI systems support advanced functionalities including power quality monitoring, demand response integration, and time-of-use tariff implementation, making them essential for utilities managing the growing penetration of distributed solar generation. The technology also facilitates predictive maintenance and outage management. In March 2025, Siemens partnered with CPFL Energia to deploy AMI-based smart metering solutions across São Paulo, targeting 1.6-million-meter replacements as part of one of the most ambitious metering digitalization initiatives in the country.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Industrial

The residential segment exhibits a clear dominance with a 58.6% share of the total Brazil smart meters market in 2025.

The residential sector represents the largest end-use segment for smart meters in Brazil, driven by the country’s household electricity connections and government programs targeting residential energy efficiency. Smart meters empower residential consumers with real-time consumption visibility through mobile applications, enabling behavioral adjustments that reduce electricity bills. The proliferation of rooftop solar installations under the net metering framework has further necessitated advanced residential metering capable of tracking bidirectional energy flows and crediting surplus generation accurately.

The focus of the utility companies is on the deployment of smart meters in residential areas to address non-technical losses, which are mainly found in the residential sector. The residential sector has an advantage in that there are regulatory measures that encourage the utility companies to install smart meters in the residential sector without charging the consumers. The distribution companies are investing heavily in the residential sector through smart metering initiatives that cover both urban and rural areas through the use of smart meters and mobile applications.

Regional Insights:

- Southeast

- South

- Northeast

- North

- Central-West

Southeast holds the largest share at 44.9% of the total Brazil smart meters market in 2025.

The Southeast holds the largest market share in Brazil’s smart metering industry, due to the presence of the country’s most populated states, such as São Paulo, Rio de Janeiro, and Minas Gerais, which together contribute a substantial share of the country’s total electricity consumption. The region is also home to the country’s largest distribution utilities, which have already committed to large-scale smart metering projects, thanks to the high population density of consumers, high non-technical loss concentrations in the suburbs, and government pressure to upgrade the country’s old distribution infrastructure in the metropolitan concession areas.

The region is also the most economically developed region in Brazil, with a strong digital infrastructure that provides a conducive environment for the widespread adoption of smart meters and their integration with utility management systems. The region’s distribution utilities have the advantage of higher revenue bases, which enable them to invest heavily in the digitalization of their metering infrastructure, communication networks, and data analytics systems. The region’s high population density of industrial, commercial, and residential consumers also provides an attractive business case for smart metering technologies that can improve billing accuracy, outage management, and distributed generation integration.

Market Dynamics:

Growth Drivers:

Why is the Brazil Smart Meters Market Growing?

Regulatory Mandates and Government-Led Grid Modernization Initiatives

Brazil’s regulatory framework is increasingly compelling utilities to adopt smart metering technologies as a core component of distribution network modernization. The National Electric Energy Agency has been establishing progressively stringent guidelines that require distribution concessionaires to deploy digital metering infrastructure for improved energy management, loss reduction, and billing accuracy. These regulatory interventions are creating a mandatory adoption pathway that ensures sustained demand for smart meters across all concession areas. The government’s strategic emphasis on energy sector digitalization is further reinforced through targeted financing mechanisms and innovation programs. For instance, in January 2025, Brazil’s National Bank for Economic and Social Development approved BRL 800 Million in financing for CPFL Energia to digitalize the metering infrastructure of three distribution subsidiaries, as part of a R$1.2 Billion investment planned between 2025 and 2029. Such initiatives demonstrate the alignment between public policy objectives and private sector investment in accelerating smart meter deployment across the country.

Persistent Energy Losses Driving Utility Investment in Smart Metering

Brazil’s electricity distribution sector contends with some of the highest energy loss rates in Latin America, with average distribution losses reaching approximately 19 percent, comprising both technical and non-technical components. Non-technical losses—resulting from energy theft, meter tampering, and illegal connections are particularly acute in northern and northeastern states. This persistent revenue leakage has made smart metering a critical tool for utilities seeking to protect revenue streams and improve operational transparency. Smart meters enable utilities to detect consumption irregularities, monitor tamper events in real time, and execute remote disconnections, thereby substantially reducing non-technical losses. The demonstrated success of early deployments has encouraged broader investment across the sector.

Expansion of Distributed Generation and Renewable Energy Integration

The rapid growth of distributed solar generation in Brazil is creating structural demand for advanced metering solutions capable of managing bidirectional power flows and supporting net metering compensation systems. The country’s installed distributed generation capacity has grown substantially, with rooftop solar installations proliferating across residential and commercial segments. This expansion requires meters that can accurately measure both consumption and generation, track surplus energy credits, and facilitate time-of-use tariff structures. The integration of intermittent renewable sources into distribution networks further necessitates smart meters with power quality monitoring and demand response capabilities.

Market Restraints:

What Challenges the Brazil Smart Meters Market is Facing?

High Upfront Deployment Costs and Infrastructure Investment Requirements

The deployment of smart metering infrastructure requires heavy capital outlay that encompasses the cost of purchasing meters, setting up communication infrastructure, as well as training personnel. For distribution companies that have to cover the large geographical area of Brazil, the capital expenditure required to replace millions of existing meters with smart meters is a major financial strain, especially for smaller concessionaires who have limited financial capacity. The issue of financing and economies of scale has remained a factor that slows down the deployment of smart meters.

Interoperability and Standardization Gaps Across Distribution Networks

The Brazilian electricity distribution market is characterized by a high degree of heterogeneity among the various regional concessionaries, each with their own set of legacy systems, communication protocols, and metering formats. The lack of a national interoperability standard makes it difficult to ensure compatibility among the various smart meter systems being integrated with the utility management systems in place. Such heterogeneity makes it more difficult to achieve the efficiencies of a fully integrated smart grid infrastructure.

Data Privacy Concerns and Cybersecurity Vulnerabilities

Smart meters generate granular consumption data transmitted through digital communication networks, raising concerns about consumer data privacy and cybersecurity risks. The two-way communication functionality inherent in advanced metering infrastructure creates potential attack vectors that could compromise grid operations or expose sensitive household consumption patterns. As Brazil strengthens its data protection regulations under the General Data Protection Law, utilities must invest in robust encryption, access controls, and compliance frameworks, adding complexity and cost to smart meter deployment initiatives.

Competitive Landscape:

The Brazil smart meters market has an increasingly dynamic competitive environment as local energy companies team up with international smart metering technology suppliers to drive the modernization of the power grid. The market is becoming more competitive in terms of the production of smart meters, communication technology, software, and system integration services. The players are adopting differentiation strategies that include locally produced smart meters, in-house data management systems, and comprehensive smart grid solutions. The formation of partnerships between Brazilian distribution companies and international technology companies is promoting shorter deployment times and technology transfer. The emergence of Chinese smart meter suppliers with competitive pricing is redefining the procurement environment, while financing from development banks is facilitating large-scale deployments that favor established players with strong supply chain capabilities.

Brazil Smart Meters Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products Covered |

Smart Electricity Meter, Smart Water Meter, Smart Gas Meter |

|

Technologies Covered |

AMI (Advanced Metering Infrastructure), AMR (Automatic Meter Reading) |

|

End Uses Covered |

Residential, Commercial, Industrial |

|

Regions Covered |

Southeast, South, Northeast, North, Central-West |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Brazil Smart Meters Market Report

The Brazil smart meters market size was valued at USD 485.49 Million in 2025.

The Brazil smart meters market is expected to grow at a compound annual growth rate of 6.68% from 2026-2034 to reach USD 868.93 Million by 2034.

Smart electricity meter dominated the market with a share of 63.8%, driven by regulatory mandates for distribution network modernization, extensive utility-led rollout programs, and the critical need to address persistent non-technical losses across Brazil’s electricity distribution sector.

Key factors driving the Brazil smart meters market include government regulatory mandates for grid digitalization, persistent energy loss reduction requirements, expanding distributed generation integration, utility-led modernization investments, and growing consumer demand for real-time energy monitoring capabilities.

Major challenges include high upfront deployment costs, interoperability gaps across heterogeneous distribution networks, cybersecurity and data privacy concerns, limited standardization frameworks, workforce training requirements, and the financial constraints of smaller regional concessionaires.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade