Brazil Solar Energy Market Size, Share, Trends and Forecast by Technology and Region, 2026-2034

Brazil Solar Energy Market Size, Share, Trends & Forecast (2026-2034)

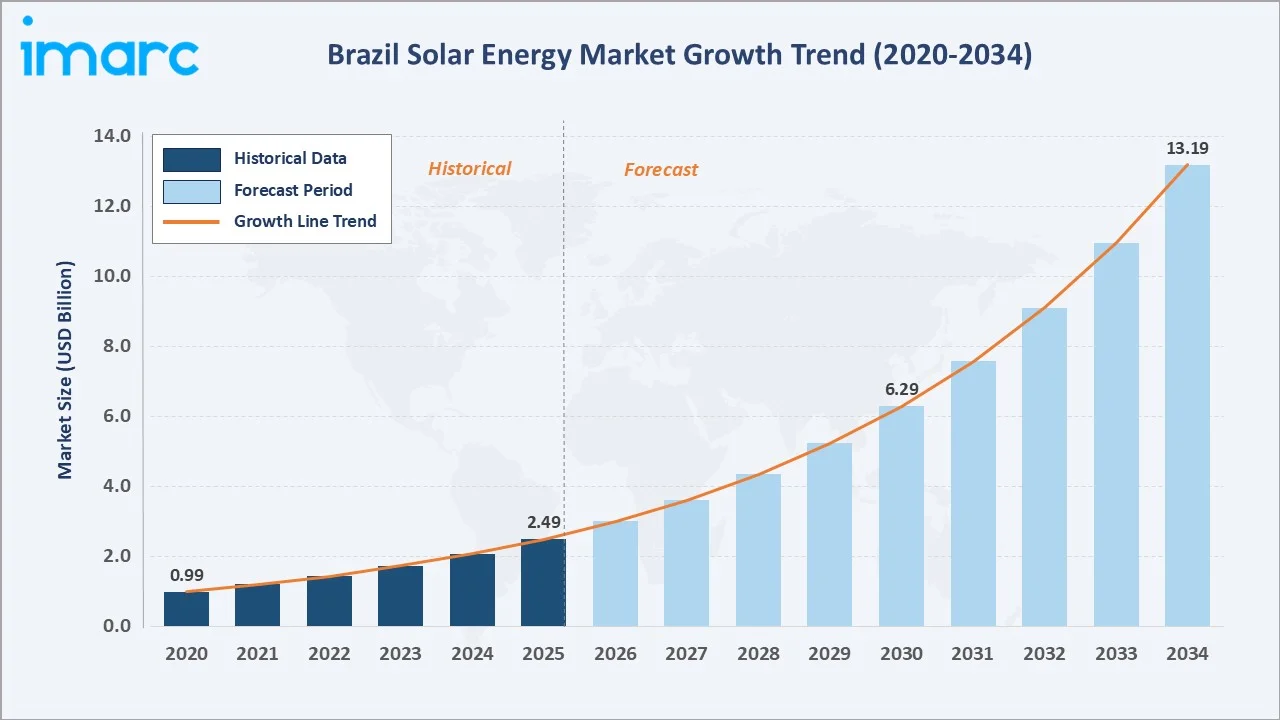

The Brazil solar energy market size reached USD 2.49 Billion in 2025 and is projected to reach USD 13.19 Billion by 2034, exhibiting a CAGR of 20.35% during 2026-2034. Brazil's strategic commitment to energy diversification, declining photovoltaic technology costs, and supportive net metering regulations under ANEEL frameworks are the primary forces driving market growth.

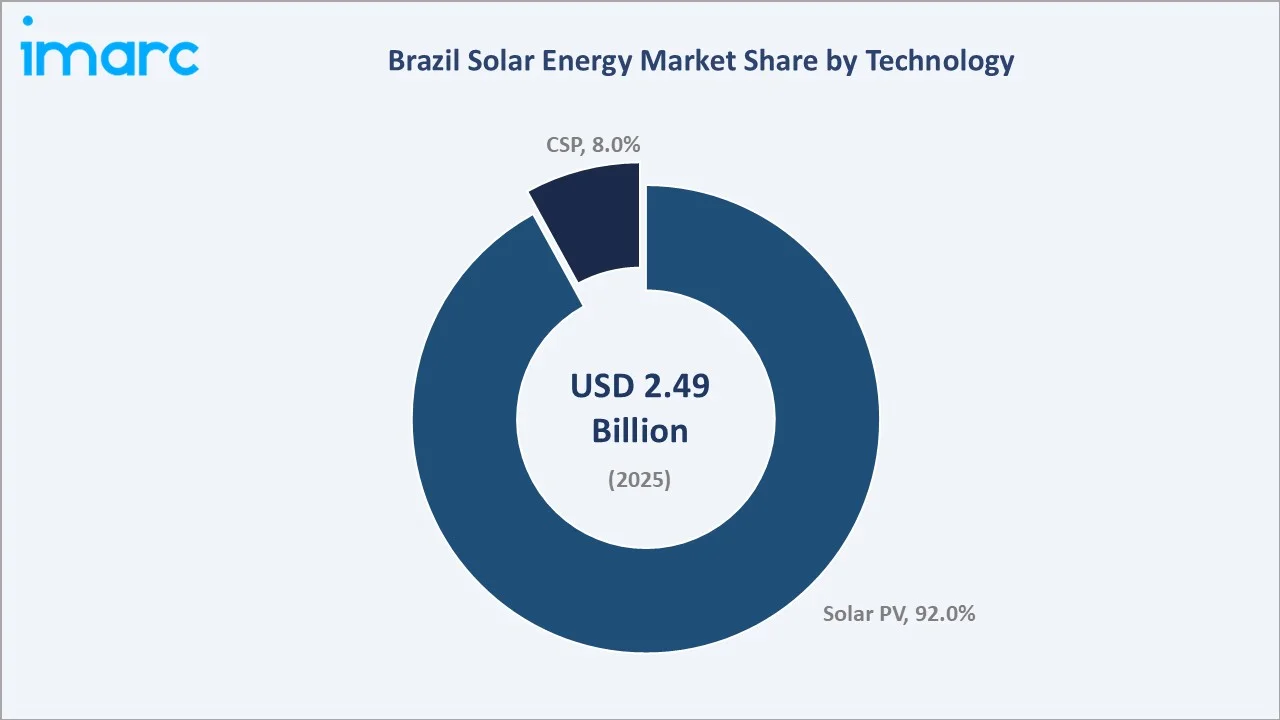

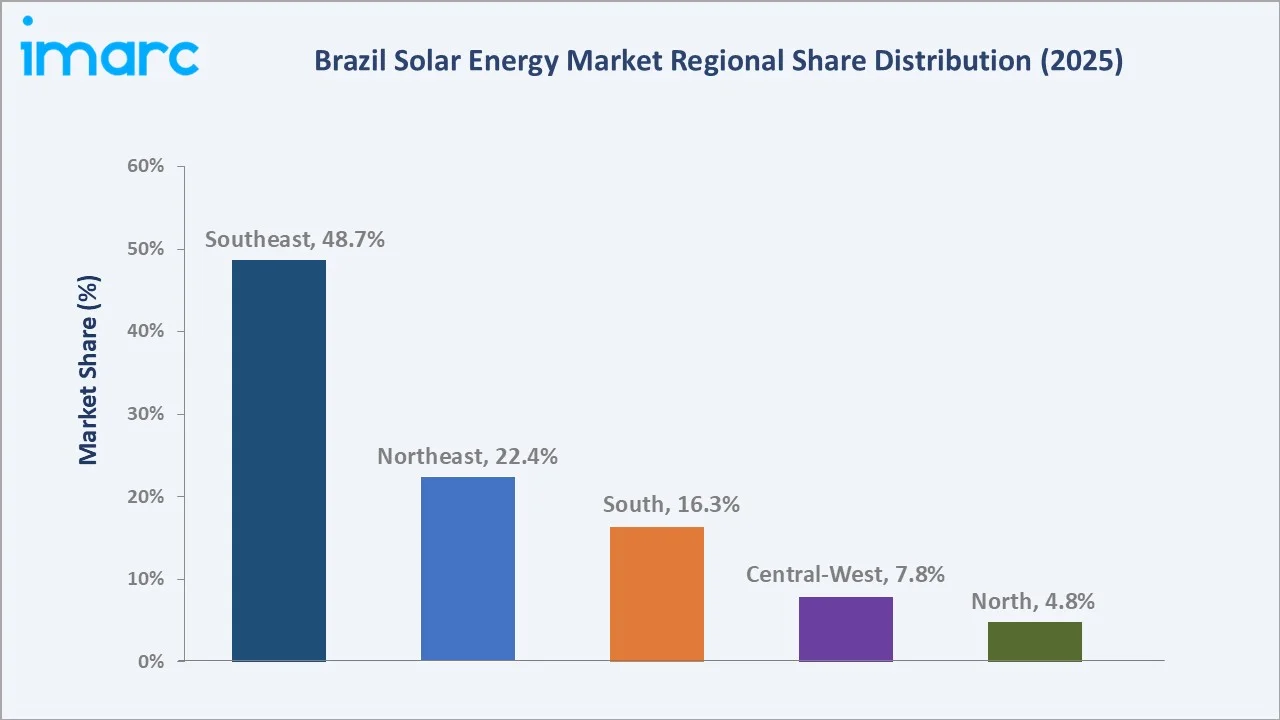

Solar PV dominates the technology mix at 92.0% in 2025, while the Southeast region commands a 48.7% share, reflecting concentrated economic activity and advanced grid infrastructure enabling rapid distributed generation adoption.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.49 Billion |

|

Forecast Market Size (2034) |

USD 13.19 Billion |

|

CAGR (2026-2034) |

20.35% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Southeast (48.7% share, 2025) |

|

Second Region |

Northeast (22.4% share, 2025) |

|

Leading Technology |

Solar PV (92.0%, 2025) |

|

Second Technology |

Concentrated Solar Power – CSP (8.0%, 2025) |

To get more information on this market, Request Sample

The Brazil solar energy market growth trajectory from 2020 through 2034, with historical expansion to USD 2.49 Billion in 2025 from USD 0.99 Billion in 2020, reflects consistent policy-driven demand acceleration, while the forecast to USD 13.19 Billion captures renewable energy transition momentum, electricity sector reform-driven adoption, and green hydrogen infrastructure development across residential, commercial, and utility-scale segments throughout Brazil.

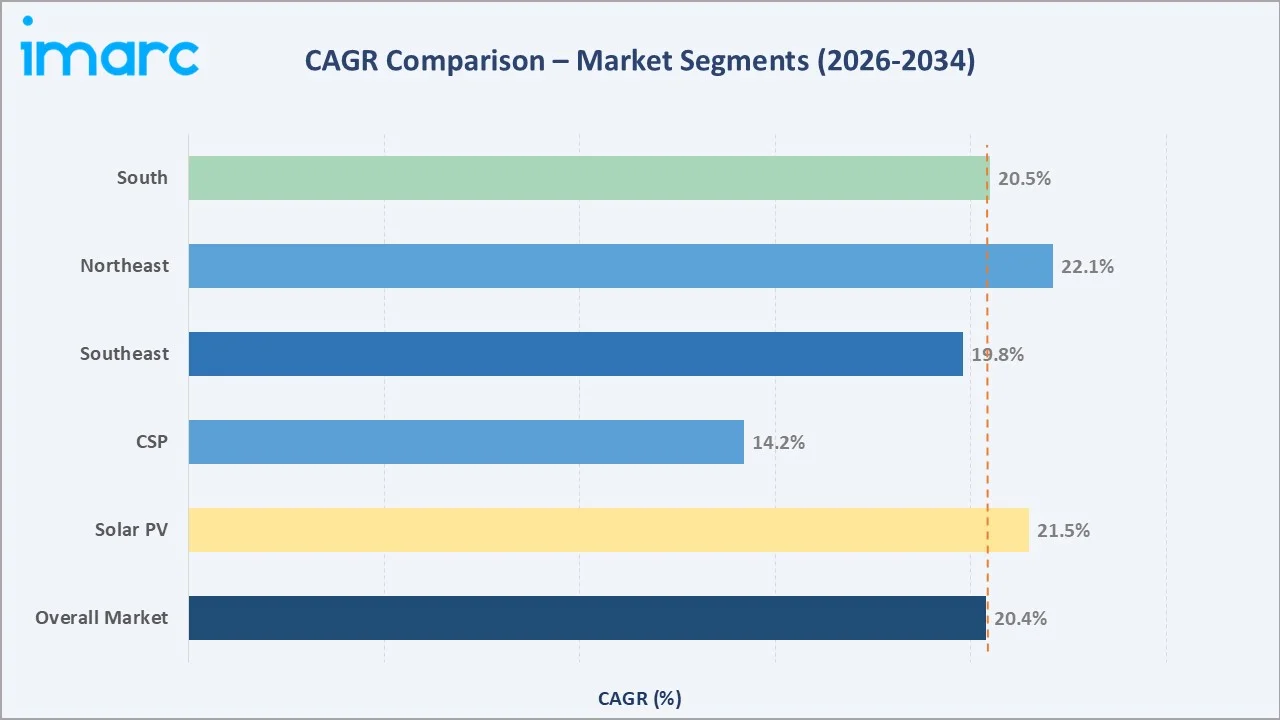

The CAGR trajectories across key technology and regional sub-segments, with the Northeast region at approximately 22.1% CAGR and Solar PV at approximately 21.5% CAGR, are the fastest-growing categories within the Brazil solar energy industry analysis through 2034, outpacing the overall market CAGR of 20.35%.

Executive Summary

The Brazil solar energy market is on a sustained high-growth trajectory, expanding from USD 2.49 Billion in 2025 to USD 13.19 Billion by 2034. Solar energy has emerged as the most dynamic component of Brazil's power matrix, supported by the country's exceptional solar irradiation resources, declining module costs, and evolving regulatory frameworks that incentivize distributed generation and large-scale utility development.

Solar PV dominates technology at 92.0% in 2025, owing to its proven scalability across residential rooftop, commercial ground-mount, floating solar, and utility-scale applications. Concentrated Solar Power accounts for 8.0%, serving utility projects requiring thermal storage in Brazil's semi-arid northeast where direct normal irradiance values exceed 2,000 kWh/m²/year.

Southeast Brazil leads regionally at 48.7% in 2025, driven by São Paulo and Minas Gerais economic concentration, high commercial electricity demand, and advanced grid infrastructure. The Northeast (22.4%) and South (16.3%) follow, with the Northeast growing fastest given its world-class solar irradiation and strong federal renewable energy auction pipeline.

Key Market Insights

|

Insight |

Data |

|

Leading Technology |

Solar PV – 92.0% share (2025) |

|

Second Technology |

Concentrated Solar Power (CSP) – 8.0% share (2025) |

|

Leading Region |

Southeast – 48.7% revenue share (2025) |

|

Second Region |

Northeast – 22.4% revenue share (2025) |

|

Top Companies |

Canadian Solar, Enel SpA, Engie SA, Atlas Renewable Energy, Scatec ASA, BYD Energy Storage |

Key Analytical Observations Supporting the Above Data:

- Solar PV, with 92.0% in 2025, dominates because declining module prices have made solar the most cost-competitive new electricity source in Brazil, enabling widespread deployment across rooftop, agrivoltaic, floating solar, and large-scale utility configurations throughout the country.

- Concentrated Solar Power (CSP), with 8.0% in 2025, serves utility-scale projects in Brazil's semi-arid northeast where thermal storage capabilities provide dispatchable clean power. States including Bahia, Piauí, and Ceará leverage the highest direct normal irradiance values in Latin America, exceeding 2,000 kWh/m²/year in significant portions of the region.

- Southeast's 48.7% dominance in 2025 reflects São Paulo state accounting for over 30% of Brazil's GDP, creating the strongest payback economics for solar distributed generation investment in Brazil, attracting both rooftop and commercial ground-mount system installations.

- Northeast, with 22.4% in 2025, benefits from the highest solar irradiation in Brazil, exceeding 2,000 kWh/m²/year in significant portions of the region. Federal renewable energy auctions have consistently awarded contracts to northeast solar projects at Brazil's lowest levelized cost of energy, driven by superior irradiation and competitive land costs.

Brazil Solar Energy Market Overview

Solar energy encompasses photovoltaic (PV) and Concentrated Solar Power (CSP) technologies that convert sunlight into electricity for residential, commercial, industrial, and utility-scale applications. Brazil represents Latin America's largest solar market by installed capacity and investment volume, underpinned by world-class irradiation resources and a rapidly maturing regulatory and financing ecosystem supporting continued accelerated growth.

The Brazilian solar ecosystem integrates silicon and glass raw material suppliers, module manufacturers, engineering procurement and construction (EPC) contractors, national grid operators, state distribution companies, financial institutions providing BNDES and international project financing, and diverse end-use segments spanning residential rooftops, agribusiness, mining, and utility-scale generation facilities across all five regions of the country.

Market Dynamics

To evaluate market opportunities, Request Sample

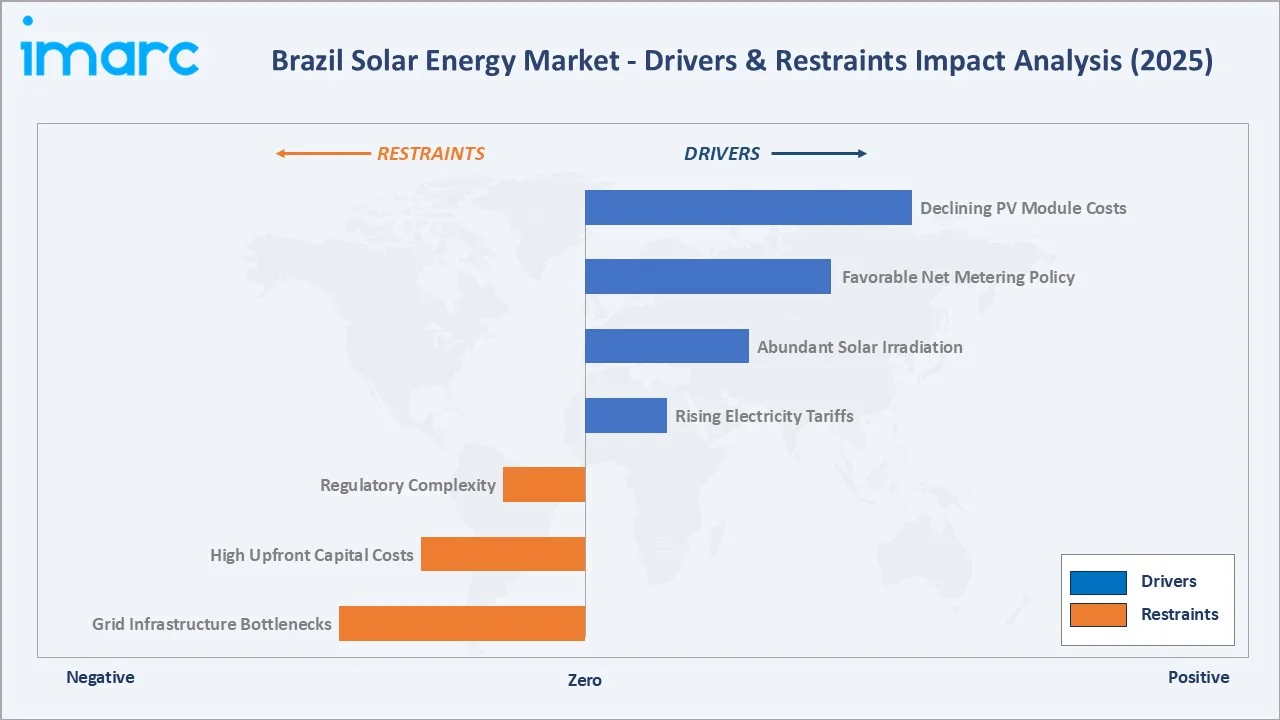

Market Drivers

- Declining Photovoltaic Technology Costs: Solar PV module prices declined over 90% between 2010 and 2025. This cost reduction has made solar the most economically competitive new electricity source in Brazil, with utility-scale solar achieving levelized costs below BRL 0.10/kWh in high-irradiation northeast regions, enabling competitive procurement in federal renewable energy auctions.

- Favorable Net Metering and Distributed Generation Regulation: ANEEL Resolution No. 482/2012 and the 2022 Marco Legal da Geração Distribuída established a robust net metering framework for Brazil. Over 4 million distributed generation systems were registered by 2025, spanning residential, commercial, rural, and community solar configurations, validating the regulatory framework's effectiveness in stimulating adoption across all consumer segments.

- Abundant Solar Irradiation Resources: Brazil receives global horizontal irradiation averaging 1,500–2,300 kWh/m²/year, with the northeast region representing the highest-irradiation territory in Latin America. This resource advantage translates directly to superior capacity factors and competitive LCOE versus other energy sources and versus solar in less-irradiated markets globally.

Market Restraints

- Grid Infrastructure Bottlenecks: Transmission and distribution infrastructure limitations, particularly in northeast and north regions where solar resources are most abundant, but load centers are distant, constrain connection timelines and create queue delays in ANEEL interconnection processes, extending project commissioning timelines and increasing financing costs for utility-scale developers.

- High Upfront Capital Costs for Distributed Generation: Despite declining module costs, total installed costs for rooftop and commercial solar in Brazil remain elevated relative to average income levels, limiting adoption in lower-income residential and small commercial segments without accessible and affordable financing programs from commercial banks or microfinance institutions.

Market Opportunities

- Green Hydrogen Production Infrastructure: Brazil's northeast is positioning as a global green hydrogen export hub, combining exceptional solar irradiation with offshore wind resources. Projects at the Pecém Industrial and Port Complex represent USD 5 billion-plus in announced investment, creating large-scale utility solar demand as the primary electrolysis power source for hydrogen production facilities.

- Agrivoltaics and Floating Solar Expansion: Brazil's vast agricultural sector and extensive hydroelectric reservoir network offer significant potential for agrivoltaic installations co-located with crops and floating solar on reservoirs that simultaneously reduce evaporation and generate clean electricity, representing a dual land-use strategy gaining regulatory and financing support from BNDES and state development agencies.

Market Challenges

- Regulatory Complexity and Permitting Delays: Environmental licensing for large solar projects in Brazil can extend 2–4 years due to overlapping federal, state, and municipal jurisdiction across IBAMA, state environmental agencies, and municipal authorities, creating delays that increase financing costs and extend payback periods for project developers and their investors.

- Foreign Exchange and Financing Risk: Brazil's historically volatile BRL/USD exchange rate creates hedging costs for projects importing PV equipment priced in USD or EUR while generating BRL-denominated PPA revenues, compressing equity returns for internationally financed project developers and increasing the effective cost of capital for projects relying on foreign equity.

Emerging Market Trends

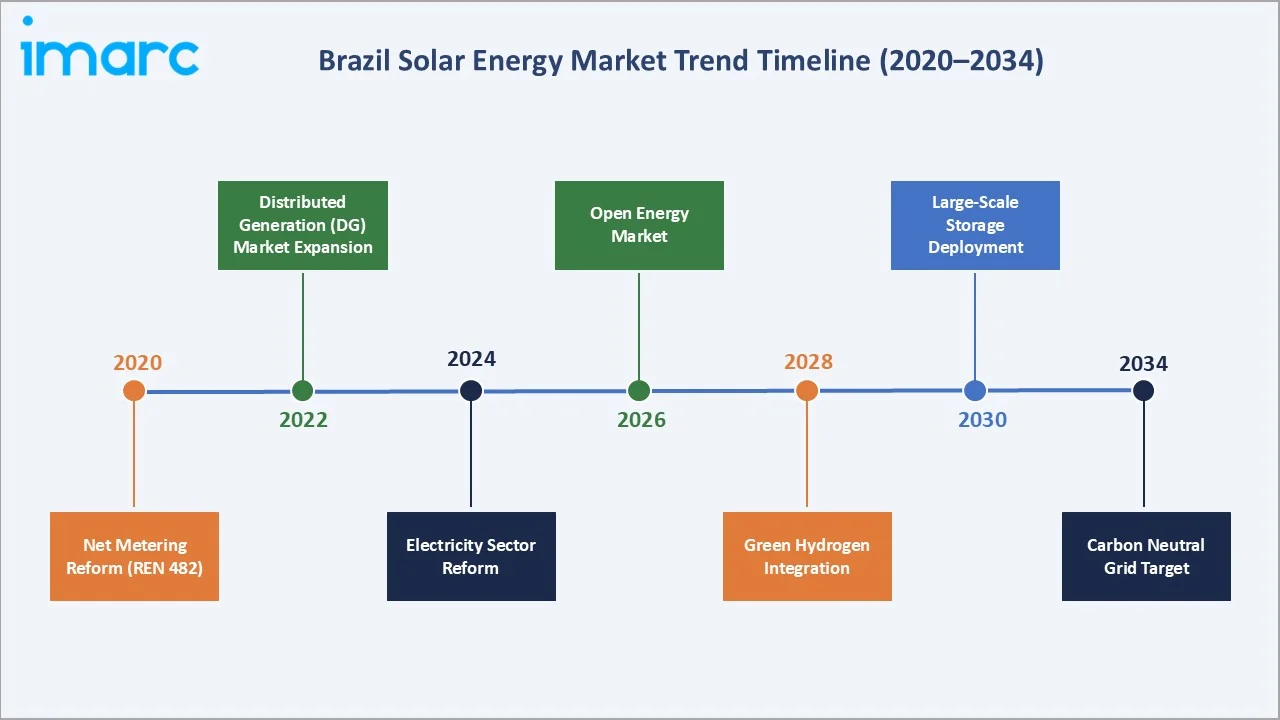

1. Electricity Sector Reform Accelerating Solar Adoption

Brazil's 2025 electricity sector reform, opening the energy market to all consumers by 2028, is creating new distributed generation monetization pathways and competitive market structures favoring low-cost solar generation. Self-production rule updates and revised energy tariff structures further incentivize commercial and industrial solar self-generation investment, expanding the addressable market for solar distributed generation across all consumer categories.

2. Integration of Storage and Solar Hybrid Systems

Declining lithium-ion battery prices are enabling solar-plus-storage configurations that address Brazil's grid intermittency challenges and time-of-use tariff arbitrage opportunities. BNDES financing programs are increasingly supporting hybrid solar-storage projects targeting industrial and utility customers requiring reliable clean power supply, while the combination addresses evening peak demand periods when solar generation alone is insufficient.

3. Corporate PPA Market Driving Utility-Scale Solar Development

Brazil's free energy market (ACL) has emerged as the primary channel for utility-scale solar procurement by corporate offtakers. Multinational consumer goods, manufacturing, and financial services companies with net-zero commitments are signing 15–20-year PPAs with Brazilian solar developers, financing a substantial pipeline of new greenfield utility solar farms and providing the revenue certainty needed to access competitive project financing from domestic and international lenders.

4. High-Efficiency Module Technology Penetration

TOPCon and bifacial module technologies are achieving commercial penetration in Brazil's utility-scale solar segment, delivering module efficiencies above 23% versus standard monocrystalline PERC at 20–21%. TCL Solar's 2025 launch of TOPCon modules in Brazil, offering 24.8% efficiency through SunPower technology lineage, exemplifies the advancement and competitive intensity at the technology frontier of Brazil's solar equipment market.

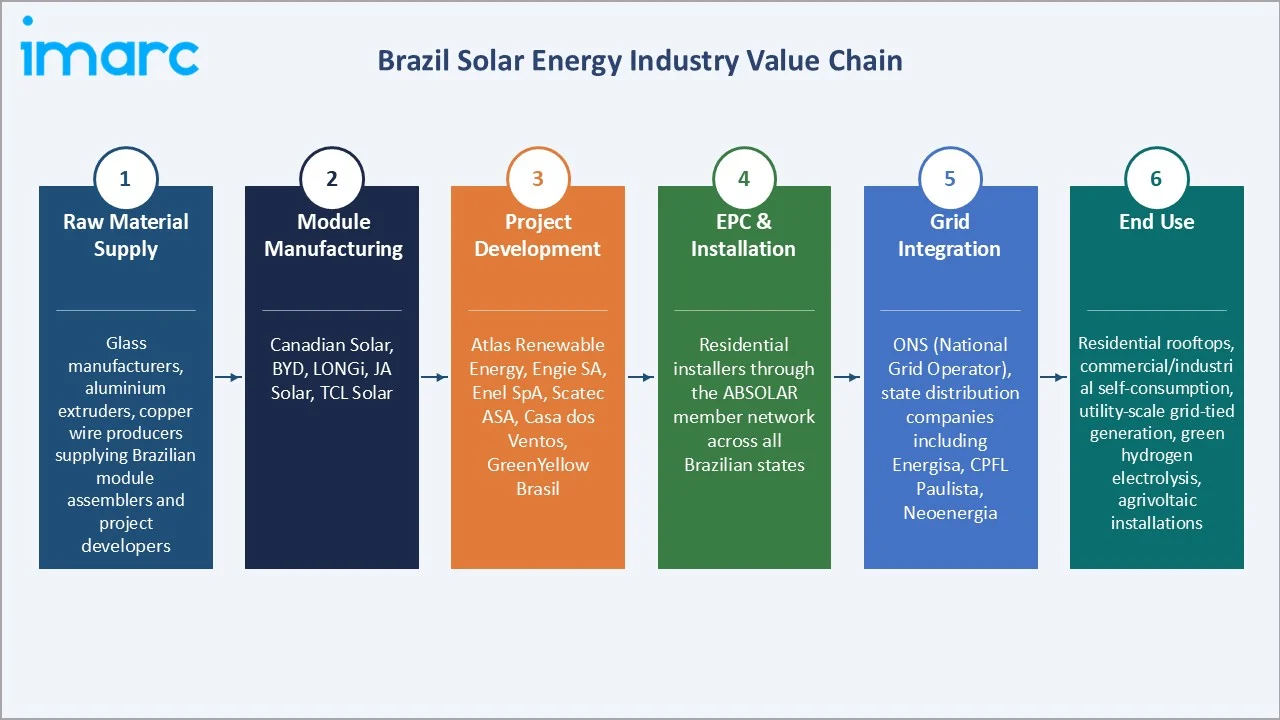

Industry Value Chain Analysis

The Brazil solar energy value chain spans six stages from raw material supply through end-use energy consumption. EPC and project development stages capture the highest domestic value-add margins, while O&M services generate stable long-term recurring revenue from Brazil's growing installed solar capacity base exceeding 40 GW by 2025, providing a resilient revenue stream for asset managers and independent O&M service providers throughout the country.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Glass manufacturers, aluminium extruders, copper wire producers supplying Brazilian module assemblers and project developers |

|

Module Manufacturing |

Canadian Solar, BYD, LONGi, JA Solar, TCL Solar |

|

Project Development |

Atlas Renewable Energy, Engie SA, Enel SpA, Scatec ASA, Casa dos Ventos, GreenYellow Brasil |

|

EPC & Installation |

Residential installers through the ABSOLAR member network across all Brazilian states |

|

Grid Integration |

ONS (National Grid Operator), state distribution companies including Energisa, CPFL Paulista, and Neoenergia |

|

End Use |

Residential rooftops, commercial/industrial self-consumption, utility-scale grid-tied generation, green hydrogen electrolysis, and agrivoltaic installations |

Integrated solar developers with direct module supply agreements, in-house engineering capabilities, and established BNDES financing relationships achieve lower total project cost bases than pure-play EPC contractors, representing a meaningful competitive advantage in Brazil's price-competitive auction and corporate PPA markets where LCOE differences of BRL 0.002/kWh can determine contract awards.

Technology Landscape in the Brazil Solar Energy Industry

Solar PV Technology: Monocrystalline PERC to TOPCon Innovation

Monocrystalline PERC technology dominates Brazil's installed solar base, progressively being displaced at the utility-scale segment by TOPCon and bifacial configurations delivering higher energy yields per installed watt-peak. Brazil's high ambient temperatures require temperature coefficient optimization, making advanced cell architectures particularly valuable for maximizing real-world energy generation across the country's diverse climatic zones.

Concentrated Solar Power: Parabolic Trough and Power Tower

CSP deployment in Brazil's northeast leverages parabolic trough and solar power tower configurations with molten salt thermal storage, enabling dispatchable clean generation complementing Brazil's hydro-dominated grid during low-water critical periods and providing a firm renewable capacity alternative to fossil gas peakers during the dry season peak demand periods across the northeast and southeast regions.

Digital Monitoring and Predictive Maintenance Technology

IoT-enabled performance monitoring platforms, AI-driven predictive maintenance algorithms, and drone-based panel inspection services are being adopted by large-scale solar operators to optimize operational performance of Brazil's growing utility solar asset base, maximizing energy yields and minimizing O&M costs per MWh generated across utility portfolios spanning multiple states and climatic conditions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

Solar PV |

92.0% |

2025 |

|

Region |

Southeast |

48.7% |

2025 |

By Technology

To access detailed market analysis, Request Sample

Solar PV commands a 92.0% majority share in 2025 owing to its fundamental cost-competitiveness and versatile scalability across residential rooftop distributed generation, floating solar on hydroelectric reservoirs, agrivoltaic dual-use installations, and large ground-mounted utility-scale solar farms throughout Brazil's diverse geographic and climatic regions from the semi-arid northeast to the subtropical south.

Concentrated Solar Power at 8.0% in 2025 serves specialized utility-scale projects requiring thermal storage capability for dispatchable generation. Brazil's semi-arid northeast states of Bahia, Piauí, and Ceará, with direct normal irradiance consistently exceeding 2,000 kWh/m²/year, represent the primary CSP deployment zone in the country and are attracting increasing project development interest from international CSP specialists.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Southeast |

48.7% |

High electricity tariffs; São Paulo/Minas Gerais industrial demand; advanced grid infrastructure enabling large-scale DG adoption |

|

Northeast |

22.4% |

Highest solar irradiation in Brazil; federal auction pipeline; BNDES project financing; green hydrogen development interest |

|

South |

16.3% |

State incentive programs in Paraná, SC, RS; agrivoltaic adoption; corporate PPA demand from agribusiness and manufacturing sectors |

|

Central-West |

7.8% |

Agribusiness self-generation in soy and sugarcane zones; Mato Grosso and Goiás solar expansion; rural grid extension programs |

|

North |

4.8% |

Off-grid solar replacing diesel in Amazon communities and island municipalities; BNDES rural electrification financing programs |

Southeast's 48.7% market dominance in 2025 is driven by São Paulo's position as Brazil's industrial and commercial hub. High electricity tariffs in ANEEL's Group A and B categories, reaching BRL 1.00/kWh for commercial users in 2025, create Brazil's most compelling return-on-investment case for solar installations, attracting both domestic and international distributed generation platform investment to the region.

The Northeast, at 22.4% in 2025, is experiencing a pronounced solar development acceleration driven by the lowest LCOE for utility solar in Brazil. ANEEL's competitive renewable energy auctions have consistently awarded contracts to northeast solar projects at prices that demonstrate the region's natural resource advantage.

Competitive Landscape

The Brazil solar energy market exhibits competitive intensity characterized by multinational energy corporations, Latin America-focused renewable developers, and emerging distributed generation platforms competing across residential, commercial, and utility-scale segments with differentiated financing, technology, and local market access capabilities that determine competitive positioning in Brazil's diverse procurement channels.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Canadian Solar |

High Power N-type TOPCon Bifacial Module |

Leader |

Global module manufacturer; Brazil utility developer; northeast solar pipeline expansion |

|

Enel SpA |

Utility-scale solar generation, distributed generation platform |

Leader |

Italy-based; Brazil largest renewable energy operator; full value chain presence across segments |

|

Engie SA |

Large-scale solar farms, hybrid solar-wind projects, corporate PPAs |

Leader |

France-based; diversified Brazil renewable portfolio; growing green hydrogen interest in northeast |

|

Atlas Renewable Energy |

Utility-scale solar, structured corporate PPA contracting, asset management |

Challenger |

Brazil/LATAM specialist; deep local expertise; BNDES and DFI financing relationships for utility projects |

|

Scatec ASA |

Solar project development |

Challenger |

Norway-based; 142 MW project under construction 2025; IFU financing and Statkraft PPA partnership |

|

BYD Energy Storage |

Solar modules, FS14, FP23, FP24, FP26, S48100, FS18, NSC1100 |

Emerging |

China-based; integrated solar+storage approach targeting Brazil commercial and industrial self-consumption |

Key players include Canadian Solar, Enel SpA, Engie SA, Atlas Renewable Energy, Scatec ASA, BYD Energy Storage, and others.

Key Company Profiles

Canadian Solar

Canadian Solar is a leading global solar energy company headquartered in Ontario, Canada. With vertically integrated manufacturing spanning polysilicon, wafers, cells, and modules, and project development operations through its Recurrent Energy subsidiary, Canadian Solar has established significant presence in the Brazilian solar market across both module supply and utility-scale project development activities in the northeast and southeast regions.

- Product Portfolio: Offers High Power N-type TOPCon Bifacial Module.

- Recent Developments: In February 2020, Canadian Solar Inc. announced that it has secured financing of 225.2 million Brazilian reais (approximately $55 million) from Banco do Nordeste do Brasil to support its Lavras solar power projects in Brazil. The funding is structured as non-recourse project financing and will be deployed over a 21-year period, covering both the construction and operational phases of the 152.4 MWp project.

- Strategic Focus: Canadian Solar's Brazil strategy combines global module manufacturing scale with local project development capabilities, targeting the utility-scale auction market and the growing corporate PPA segment through its Recurrent Energy project development subsidiary, with a focus on northeast Brazil's superior solar resource base.

Enel SpA

Enel SpA is Italy's largest utility and one of the world's leading renewable energy operators. Through its Brazilian subsidiary Enel Green Power Brasil, the company operates one of the largest renewable energy portfolios in the country, with significant solar capacity in the northeast region and a growing distributed generation platform serving commercial and industrial customers across Brazil's major metropolitan areas.

- Product Portfolio: Offers utility-scale solar generation, distributed generation platform.

- Recent Developments: In August 2024, Enel increased its investment focus in Brazil, raising allocated resources by about 45% as part of its strategic plan. The company aims to strengthen the country’s power distribution networks, expand renewable energy generation, and improve customer service. A major priority is enhancing the resilience of infrastructure so it can better withstand extreme weather events.

- Strategic Focus: Enel's Brazil strategy leverages its market-leading renewable portfolio to expand across the full solar value chain, from utility generation through residential distributed generation platforms, capitalizing on Brazil's electricity market liberalization trend and the growing demand for solar as a primary energy self-generation solution for commercial and industrial consumers.

Engie SA

Engie SA is a French multinational energy company with one of Brazil's most diversified renewable energy portfolios spanning solar, wind, and hydroelectric generation. The company, operating in Brazil as ENGIE Brasil Energia, has been active in country's solar market since the first utility-scale renewable energy auctions and has expanded through both greenfield development and strategic acquisitions, establishing strong positions in the northeast solar development zone and the corporate PPA market.

- Product Portfolio: Offers large-scale solar farms, hybrid solar-wind projects, corporate PPAs.

- Recent Developments: In February 2026, ENGIE successfully commissioned the Assú Sol photovoltaic complex in Brazil, marking it as the largest solar park in its global portfolio. The facility can generate enough clean electricity to supply approximately 850,000 people annually, highlighting its significant contribution to Brazil’s renewable energy capacity.

- Strategic Focus: Engie's Brazil strategy differentiates through hybrid renewable project structures that optimize capacity factors and serve corporate sustainability commitments requiring high-reliability clean power supply solutions, while building on the company's established position in Brazil's competitive federal renewable energy auction market where it has a proven track record of project delivery.

Market Concentration Analysis

The Brazil solar energy market is moderately fragmented at the project development level, with no single company holding more than 10–15% of total installed generation capacity. The utility-scale segment shows greater concentration, with Enel, Engie, and Atlas Renewable collectively operating a significant share of large-scale solar farms developed through federal renewable energy auctions since 2012 and through the corporate PPA free market since its expansion.

Consolidation is accelerating in the distributed generation segment as national platforms backed by private equity acquire regional solar installers and aggregators to build service coverage scale across Brazil's major metropolitan areas. The module supply segment is dominated by Chinese and Canadian manufacturers, with Canadian Solar, LONGi, JA Solar, and BYD collectively supplying the majority of Brazil's annual module demand by volume across residential, commercial, and utility-scale procurement channels.

Investment & Growth Opportunities

Fastest-Growing Segments

The Northeast region at approximately 22.1% CAGR through 2034 represents the highest-growth regional segment, driven by utility-scale solar auctions and the emerging green hydrogen project pipeline requiring large-scale solar electrolysis power. Solar PV technology at approximately 21.5% CAGR represents the broadest investment opportunity given its deployment versatility across all segments and regions of Brazil's diverse market.

Emerging Markets

North Brazil at approximately 18.5% CAGR through 2034 is the fastest-growing frontier market for solar, driven by off-grid electrification programs and Amazon community energy projects replacing diesel generation with solar-battery hybrid systems, supported by ANEEL rural electrification programs and federal energy access initiatives targeting the millions of remote connection points still reliant on costly and polluting diesel generation.

Venture & Investment Trends

The International Finance Corporation (IFC) announced USD 150 million in financing for Brazil solar projects in 2025, reflecting growing multilateral development bank commitment to Brazil's solar energy transition. BNDES's Finem program continues providing BRL-denominated long-term project financing at subsidized interest rates, reducing the cost of capital for domestic solar developers and improving project economics for utility-scale and distributed generation projects across all regions.

Future Market Outlook (2026-2034)

The Brazil solar energy market is forecast to expand from USD 2.49 Billion in 2025 to USD 13.19 Billion by 2034 at a CAGR of 20.35%, passing through the milestone forecast value of USD 6.29 Billion in 2030, adding USD 10.70 Billion in incremental annual market value over the forecast period. This high and sustained growth rate reflects the market's unique combination of exceptional natural resources, improving economics, and regulatory tailwinds.

Three transformative forces will most significantly shape Brazil's solar energy landscape through 2034. The 2028 electricity market opening will create new distributed generation monetization pathways for millions of connection points. Green hydrogen development will establish the northeast as a global clean fuel export hub. Continued PV cost reductions and storage integration will enable whole-day solar energy delivery at grid parity across all Brazilian consumer segments and geographic markets.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews in 2024–2025 with Brazil solar energy stakeholders, including senior managers from project developers, EPC contractors, ANEEL regulatory officials, BNDES project financing managers, and state distribution company procurement specialists. Primary data validated market sizing, technology segment shares, and regional demand estimates for the historical and base years of the study.

Secondary Research

Key secondary sources include ANEEL National Electric Energy Agency statistical databases, EPE Energy Research Office Ten-Year Energy Expansion Plan (PDE 2030), ABSOLAR Brazilian Solar Photovoltaic Association annual market reports, IEA World Energy Investment Report (2025), IRENA Renewable Capacity Statistics, ONS grid operator data publications, and BNDES annual project financing reports covering the 2020–2025 historical period.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models incorporating GDP growth rates, electricity tariff trajectories, installed capacity addition pipelines, and historical market evolution patterns. Scenario analysis across base, optimistic, and conservative cases was performed to account for regulatory uncertainty, exchange rate volatility, and global equipment supply chain variability.

Brazil Solar Energy Market Report:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Technologies Covered | Solar PV, Concentrated Solar Power (CSP) |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Canadian Solar, Enel SpA, Engie SA, Atlas Renewable Energy, Scatec ASA, BYD Energy Storage, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Brazil Solar Energy Market Report

The Brazil solar energy market reached USD 2.49 Billion in 2025, growing from USD 0.99 Billion in 2020 at a historical CAGR of approximately 20.2%, reflecting consistent acceleration from declining PV costs, favorable net metering regulation, and growing domestic and international investment in distributed and utility-scale solar generation.

The market is projected to reach USD 13.19 Billion by 2034, passing through USD 6.29 Billion in 2030, growing at a CAGR of 20.35% during 2026-2034, driven by electricity sector reform, green hydrogen infrastructure development, and continued distributed generation expansion under evolving net metering frameworks.

Solar PV leads with a 92.0% technology share in 2025, valued for its proven cost-effectiveness below USD 0.20/W in module costs, scalability across distributed and utility-scale applications, and mature global supply chain enabling rapid and cost-competitive deployment throughout Brazil's diverse geographic regions and solar resource conditions.

Concentrated Solar Power (CSP) holds 8.0% of the market in 2025, primarily serving utility-scale projects in Brazil's semi-arid northeast with thermal energy storage capabilities providing dispatchable clean power generation during evening peak demand periods and dry season hydro constraints in the national grid.

Southeast commands a dominant 48.7% market share in 2025, driven by São Paulo and Minas Gerais's concentrated economic activity, among the highest electricity tariffs in Brazil creating strong solar return on investment, and advanced grid infrastructure enabling distributed generation adoption at scale across millions of residential and commercial connection points.

The Northeast is the fastest-growing region at approximately 22.1% CAGR through 2034, leveraging the highest solar irradiation in Brazil exceeding 2,000 kWh/m²/year, a strong utility-scale project pipeline from competitive federal renewable energy auctions, and growing green hydrogen project development investment targeting the region's exceptional solar resources.

Leading companies include Canadian Solar, Enel SpA, Engie SA, Atlas Renewable Energy, Scatec ASA , BYD Energy Storage, and others.

Key drivers include declining PV module costs below USD 0.20/W, Brazil's abundant solar irradiation averaging 1,500–2,300 kWh/m²/year, favorable net metering regulation under the 2022 Marco Legal da Geração Distribuída, rising electricity tariffs improving solar investment returns, and growing corporate sustainability commitments driving long-term PPA demand.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)