Brazil Solar Panel Market Size, Share, Trends and Forecast by Type, End Use, and Region, 2026-2034

Brazil Solar Panel Market Size, Share, Trends & Forecast (2026-2034)

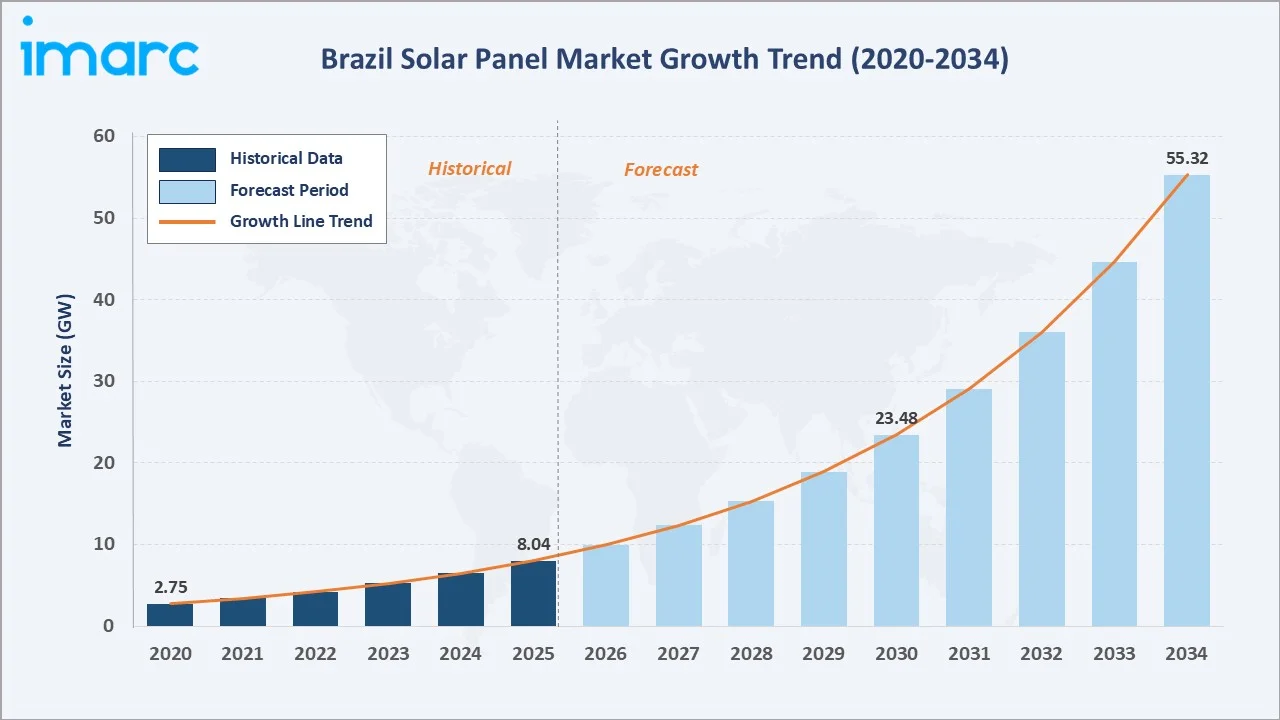

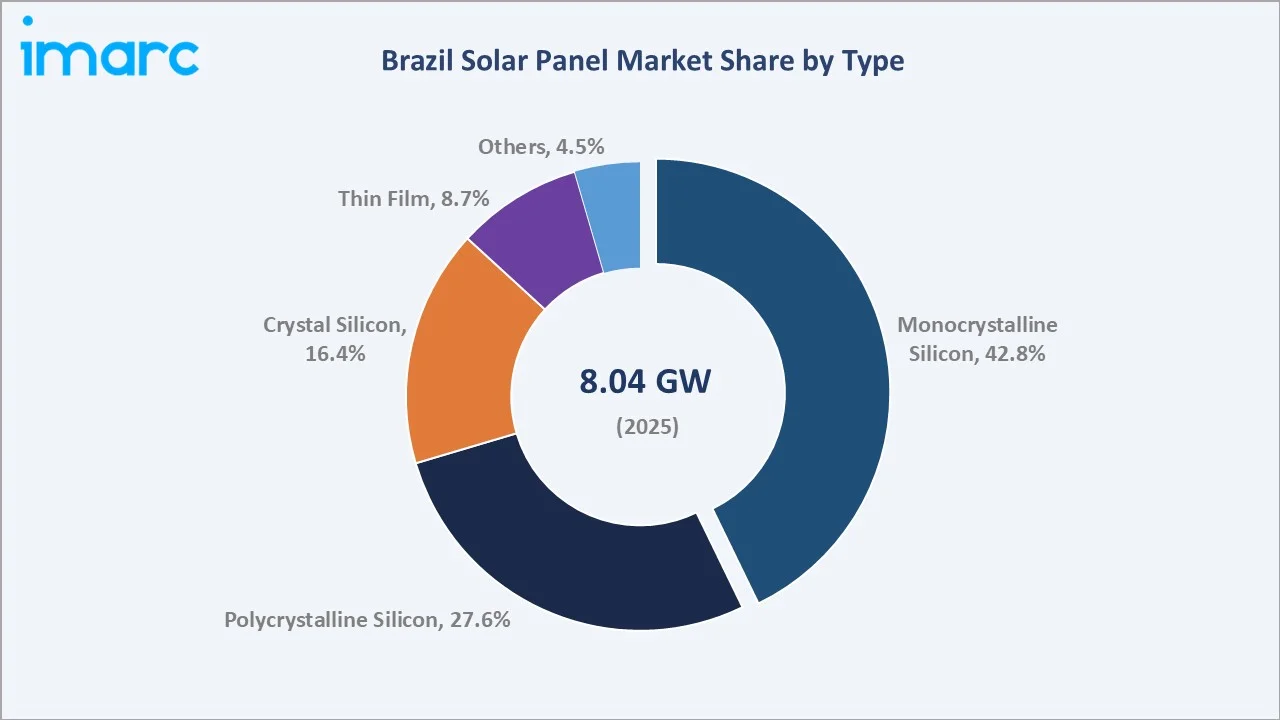

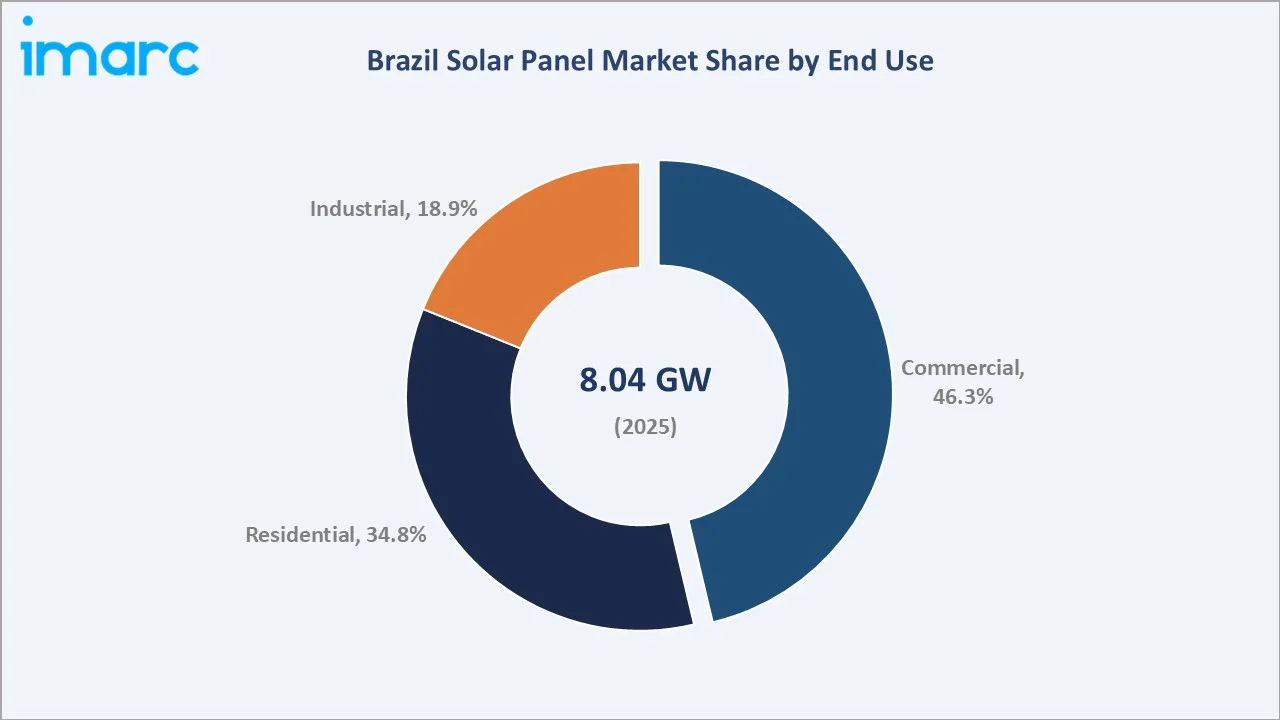

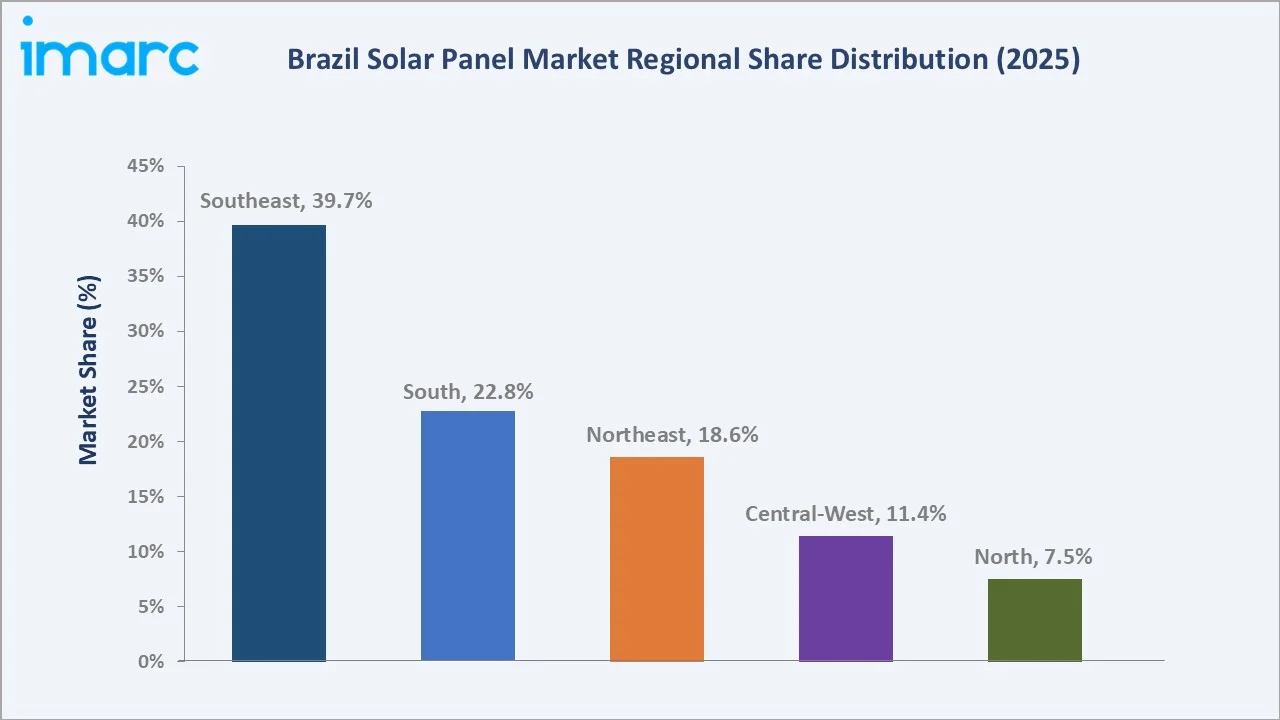

The Brazil solar panel market reached 8.04 GW in 2025 and is projected to reach 55.32 GW by 2034, growing at a CAGR of 23.90% during 2026-2034. The market is primarily driven by the country's expanding utility-scale and distributed solar installations, supported by abundant solar resources, favorable net metering policies, and increasing investments in renewable energy infrastructure. Brazil’s solar panel market is being driven by the rapid expansion of distributed solar PV adoption, with more than 2 million grid-connected systems serving over 1.5 million consumer units, according to the Brazilian Solar Association. This growing installed base, combined with solar PV’s global scale of over 1 TW by 2024, highlights rising consumer confidence, improving project economics, and strong demand for clean, decentralized electricity solutions. Monocrystalline silicon leads at 42.8%. Commercial leads end use at 46.3%. Southeast leads regionally at 39.7%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

8.04 GW |

|

Forecast Market Size (2034) |

55.32 GW |

|

CAGR (2026-2034) |

23.90% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Monocrystalline Silicon (42.8%, 2025) |

|

Dominant End Use |

Commercial (46.3%, 2025) |

|

Leading Region |

Southeast (39.7%, 2025) |

Brazil solar panel market expanded from 2.75 GW in 2020 to 8.04 GW in 2025, reflecting rapid adoption across utility-scale, commercial, and residential solar applications. The market is expected to accelerate further, reaching 23.48 GW by 2030, supported by favorable policies, rising distributed generation, and declining PV costs. By 2034, installed capacity is projected to reach 55.32 GW, highlighting Brazil’s strong transition toward renewable energy. This growth underscores increasing investments in solar infrastructure and the country’s rising dependence on clean, decentralized power generation.

To get more information on this market, Request Sample

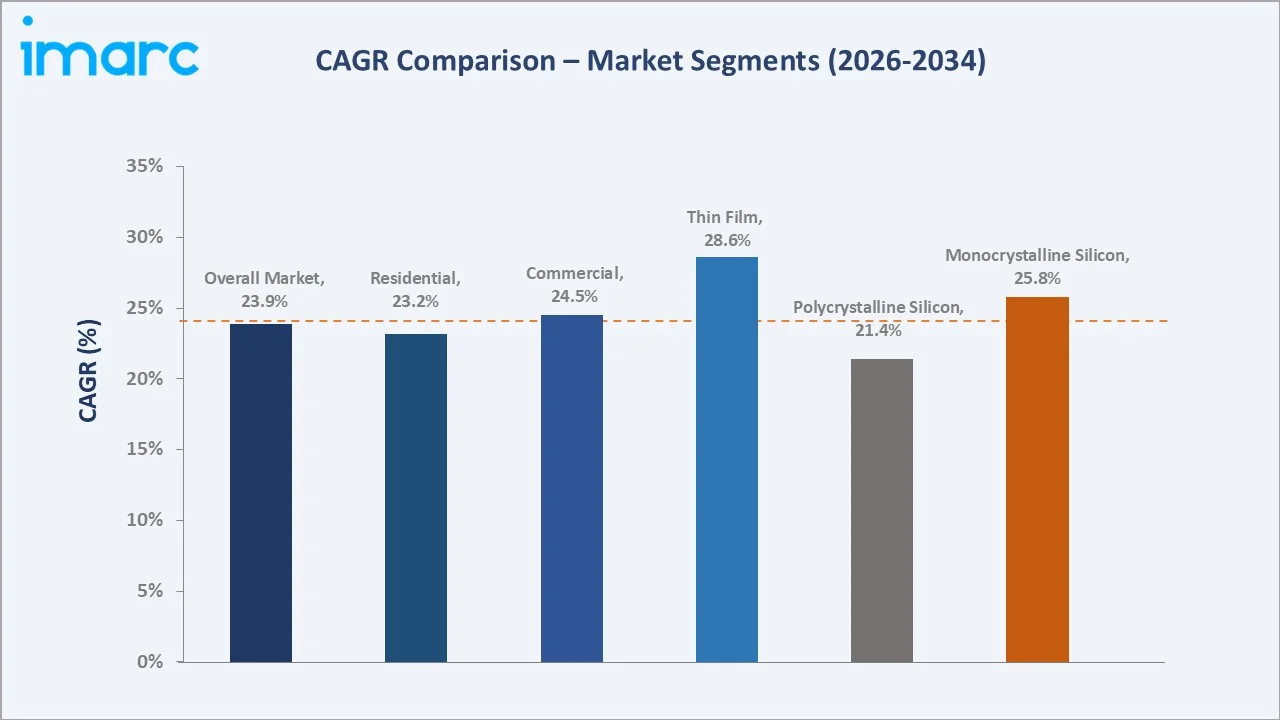

Thin film grows fastest at ~28.6% CAGR through floating solar and niche applications. Monocrystalline grows at ~25.8% CAGR through N-Type premium efficiency. Commercial end use grows fastest at ~24.5% CAGR through C&I distributed generation and ESG corporate mandate.

Executive Summary

Brazil solar panel market is witnessing strong momentum, supported by rapid growth in grid-connected solar PV systems and rising adoption across residential, commercial, and utility-scale segments. Abundant solar irradiation, declining module costs, and favorable distributed generation policies are strengthening project viability across the country. The market is also benefiting from increasing electricity demand, corporate decarbonization goals, and investments in clean energy infrastructure. With installed capacity projected to rise sharply through 2034, Brazil is emerging as one of Latin America’s most attractive solar power markets. Monocrystalline silicon at 42.8% leads through high-efficiency premium. Commercial at 46.3% leads through C&I distributed generation. Southeast leads regionally at 39.7%.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Monocrystalline Silicon - 42.8% share (2025) |

|

Dominant End Use |

Commercial - 46.3% market share (2025) |

|

Leading Region |

Southeast - 39.7% share (2025) |

|

Market Opportunity |

Agrivoltaics agribusiness; floating solar hydroelectric reservoir; N-Type TOPCon bifacial premium; rural electrification low-income; green hydrogen solar-powered; battery storage hybrid solar |

Key Analytical Observations Supporting the Above Data:

- Monocrystalline Silicon at 42.8%: Monocrystalline silicon dominates due to its higher efficiency, better space utilization, and superior performance in high-irradiation conditions. Its longer lifespan and suitability for residential rooftops, commercial projects, and utility-scale solar farms make it the preferred technology choice.

- Commercial at 46.3%: Commercial dominates as businesses increasingly adopt solar PV to reduce high electricity costs, improve energy security, and meet sustainability targets. Large rooftop spaces, tax benefits, and strong returns on captive solar installations further support commercial-sector adoption.

- Southeast at 39.7%: The Southeast region dominates due to its high electricity consumption, dense commercial and industrial base, and strong rooftop solar adoption across major urban centers. The region’s better financing access and grid infrastructure further support large-scale solar deployment.

Brazil Solar Panel Market Overview

Brazil solar panel market encompasses photovoltaic modules, cells, inverters, mounting structures, balance-of-system components, and related installation services. It covers residential rooftop systems, commercial and industrial solar projects, utility-scale solar farms, and distributed generation applications. The market includes monocrystalline, polycrystalline, and thin-film solar technologies used across grid-connected and off-grid power systems. It also involves engineering, procurement, construction, operations, maintenance, financing, and energy management solutions. Growing demand for clean power, cost savings, and decentralized electricity generation continues to broaden the market scope across Brazil. Macroeconomic factors include Brazil’s rising electricity demand, expanding commercial and industrial activity, and increasing investment in renewable energy infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

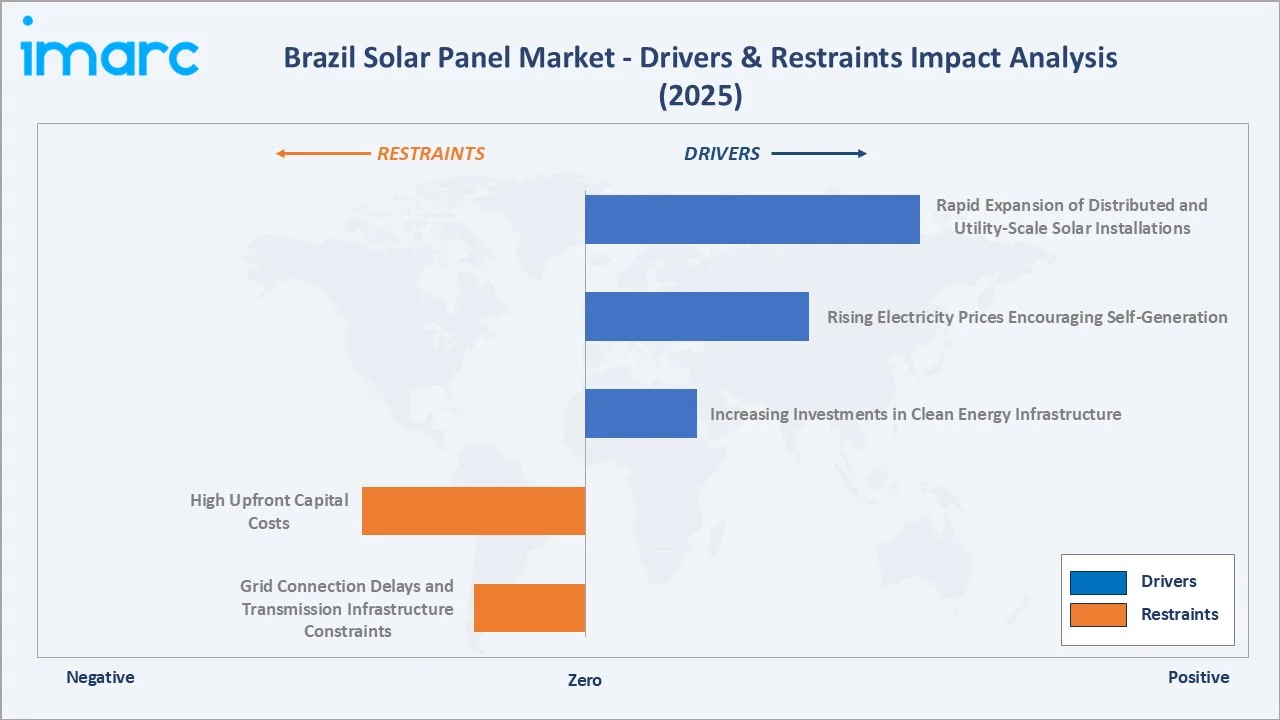

Market Drivers

- Rapid Expansion of Distributed and Utility-Scale Solar Installations: The rapid expansion of distributed and utility-scale solar installations is significantly increasing demand for photovoltaic modules across multiple end-use sectors. Brazil’s distributed solar generation capacity rose sharply from below 1 GW in 2018 to 40 GW by June 2025, representing 43% of total electricity capacity additions during the period. In comparison, utility-scale solar capacity stood at 17.9 GW at the end of June, as reported by ANEEL. By June 30, 2025, homeowners and building owners had installed over 3.7 million renewable distributed generation systems across Brazil. As Brazil diversifies its electricity mix beyond hydropower, both distributed and utility-scale projects continue to fuel sustained growth in solar panel demand.

- Rising Electricity Prices Encouraging Self-Generation: Rising electricity prices are driving the market as consumers and businesses increasingly turn to self-generation to reduce monthly power bills. Solar PV systems allow users to offset grid electricity consumption and gain better control over long-term energy costs. Commercial and industrial users are especially adopting rooftop and captive solar projects to improve cost predictability and operational efficiency. This shift toward energy independence is strengthening demand for solar panels across residential, commercial, and industrial applications.

- Increasing Investments in Clean Energy Infrastructure: Increasing investments in clean energy infrastructure is accelerating the development of solar parks, grid-connected PV projects, and distributed generation systems. To stay aligned with its net-zero pathway, Brazil will need to invest more than $1.3 trillion in low-carbon energy supply between 2024 and 2050. Of this, around $0.5 trillion is expected to be directed toward renewable energy development. These investments help expand solar access across commercial, industrial, and utility applications. As Brazil strengthens its low-carbon energy transition, rising infrastructure spending continues to boost demand for solar panels and related components.

Market Restraints

- Grid Connection Delays and Transmission Infrastructure Constraints: Grid connection delays and transmission infrastructure constraints hamper the Brazil solar panel market by slowing the commissioning of new solar projects. Limited grid capacity in high-potential solar regions can delay project approvals, increase curtailment risks, and reduce investor confidence. Utility-scale developers may face longer timelines for interconnection studies, substations, and transmission upgrades. These bottlenecks raise project costs and can postpone solar panel demand despite strong installation interest.

- High Upfront Capital Costs: High upfront capital costs hamper the Brazil solar panel market by making system installation less affordable for residential users and small businesses. Expenses for panels, inverters, mounting structures, batteries, and installation can delay purchase decisions despite long-term savings. Limited access to low-cost financing further restricts adoption among price-sensitive customers. As a result, some potential buyers postpone solar investments, slowing market penetration in certain end-use segments.

Market Opportunities

- Growth in Utility-Scale Solar Parks and Hybrid Renewable Projects: Growth in utility-scale solar parks and hybrid renewable projects is creating large-volume demand for PV modules and related components. In June 2026, CGN Brazil Energy (CGNBE) started commercial operations at its 165-MW Lagoinha Solar Park in Brazil after receiving approval from power sector regulator ANEEL. Located in Russas, Ceará, the project comprises four operational units and includes around 337,000 solar panels spread across 304 hectares. These projects also attract institutional investors, utilities, and corporate power buyers seeking long-term clean energy supply.

- Expansion of Commercial and Industrial Rooftop Solar Installations: Expansion of commercial and industrial rooftop solar installations is a strong opportunity as businesses seek to lower electricity expenses and improve energy independence. Large rooftops on factories, warehouses, malls, and office buildings offer scalable space for PV deployment without requiring additional land. These systems also help companies meet ESG targets and reduce exposure to grid tariff volatility. As financing models improve, C&I rooftop solar can significantly expand demand for high-efficiency panels and installation services.

Market Challenges

- Grid Congestion in High Solar Penetration Regions: Grid congestion in high solar penetration regions is challenging as it limits the ability to absorb new solar generation efficiently. Overloaded transmission and distribution networks can lead to curtailment, delayed interconnections, and lower project returns. This creates uncertainty for developers and slows new utility-scale and distributed solar approvals. Without timely grid upgrades, solar deployment may face bottlenecks despite strong demand.

- Supply Chain Disruptions and Module Price Fluctuations: Supply chain disruptions and module price fluctuations are creating uncertainty in project costs and delivery timelines. Heavy reliance on imported PV modules, inverters, and components exposes developers to shipping delays, currency volatility, and global price swings. Sudden increases in module prices can reduce project margins and delay investment decisions. This makes planning difficult for installers, developers, and commercial buyers, especially for large-scale projects with fixed budgets.

Emerging Market Trends

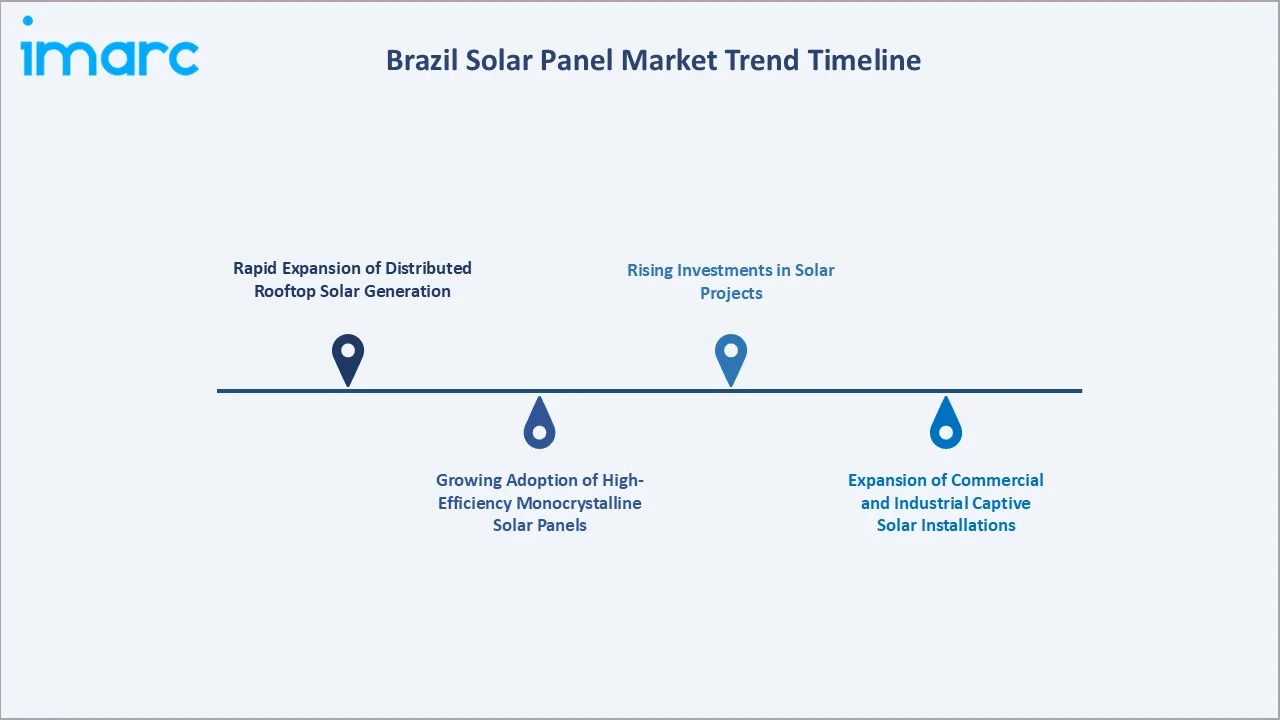

1. Rapid Expansion of Distributed Rooftop Solar Generation

The rapid expansion of distributed rooftop solar generation is emerging as households, commercial buildings, and industries increasingly install on-site PV systems to reduce electricity costs. Improvements in financing options, digital monitoring technologies, and net metering frameworks are making rooftop solar more accessible. Rising demand for energy independence and sustainability is further accelerating installations across urban areas. This trend is driving strong demand for high-efficiency solar panels, inverters, and related balance-of-system components.

2. Growing Adoption of High-Efficiency Monocrystalline Solar Panels

The growing adoption of high-efficiency monocrystalline solar panels is emerging as users seek greater power output from limited rooftop and project space. These panels offer better performance, longer durability, and higher conversion efficiency than conventional alternatives. Their suitability for residential, commercial, and utility-scale installations is increasing demand across Brazil. As system owners focus on maximizing returns, monocrystalline panels are becoming the preferred technology choice.

3. Expansion of Commercial and Industrial Captive Solar Installations

The expansion of commercial and industrial captive solar installations is emerging as businesses seek reliable, lower-cost power for their own operations. Factories, warehouses, malls, and office complexes are increasingly installing rooftop or on-site solar systems to reduce dependence on the grid. These projects support energy cost savings, sustainability targets, and long-term tariff protection. As corporate energy users prioritize self-generation, demand for efficient solar panels and installation services continues to rise.

4. Rising Investments in Solar Projects

Rising investments in solar projects are emerging as developers, utilities, and corporate buyers expand renewable power capacity. In November 2025, Iberdrola Chairman Ignacio Galán, alongside Brazilian energy officials and Neoenergia leadership, presented the Noronha Verde project for Fernando de Noronha. The initiative will combine a 22 MWp solar plant with over 30,000 panels and a 49 MWh battery storage system, supported by an investment of R$350 million (more than €50 million). The first phase begins operations in May 2026, followed by the second phase in 2027. As Brazil accelerates its clean energy transition, higher project investments are strengthening demand for solar panels and related components.

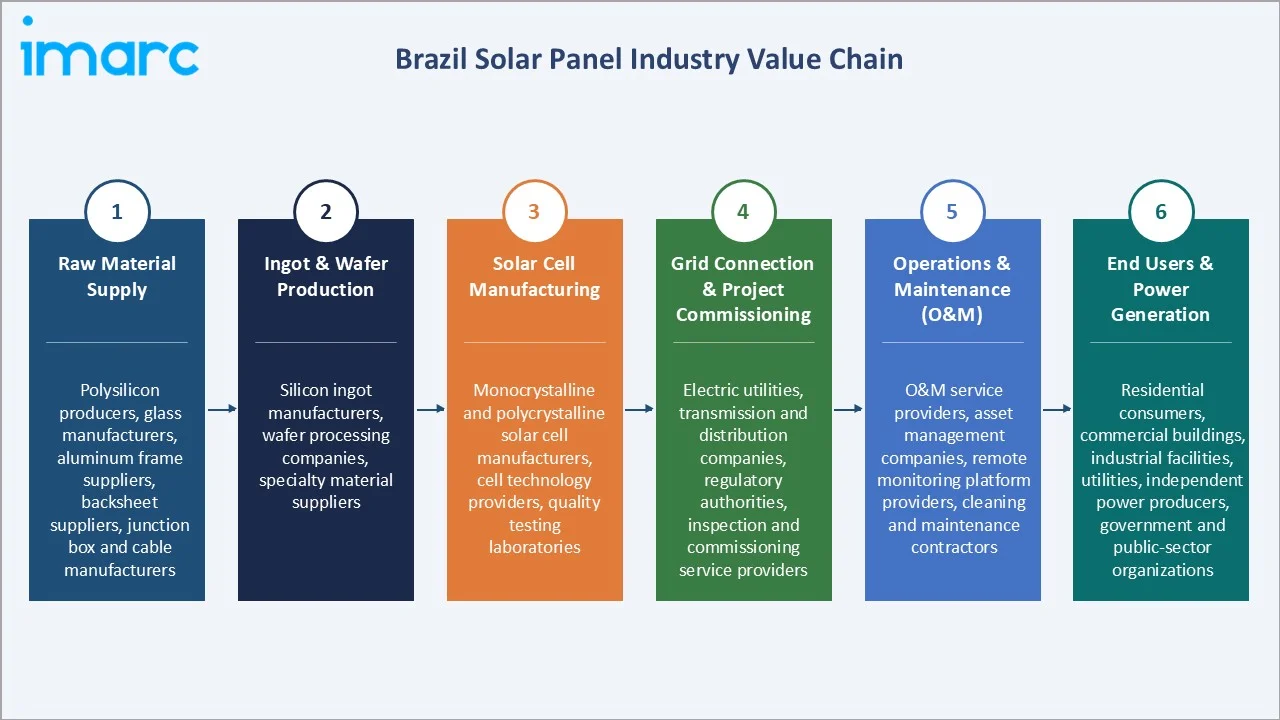

Industry Value Chain Analysis

Brazil solar panel value chain integrates raw material supply, ingot & wafer production, solar cell manufacturing, grid connection & project commissioning, operations & maintenance (O&M), and end users & power generation.

|

Stage |

Key Participants |

|

Raw Material Supply |

Polysilicon producers, glass manufacturers, aluminum frame suppliers, backsheet suppliers, junction box and cable manufacturers |

|

Ingot & Wafer Production |

Silicon ingot manufacturers, wafer processing companies, specialty material suppliers |

|

Solar Cell Manufacturing |

Monocrystalline and polycrystalline solar cell manufacturers, cell technology providers, and quality testing laboratories |

|

Grid Connection & Project Commissioning |

Electric utilities, transmission and distribution companies, regulatory authorities, and inspection and commissioning service providers |

|

Operations & Maintenance (O&M) |

O&M service providers, asset management companies, remote monitoring platform providers, and cleaning and maintenance contractors |

|

End Users & Power Generation |

Residential consumers, commercial buildings, industrial facilities, utilities, independent power producers, government and public-sector organizations |

Solar cell manufacturing is the most value-added stage. It involves converting processed wafers into high-efficiency solar cells, where technology, precision engineering, and quality control directly determine panel performance. This stage adds greater value than raw material or wafer supply because cell efficiency strongly influences module output, project economics, and end-user returns.

Technology Landscape in the Brazil Solar Panel Industry

Cell and Module Technology

Cell and module technology is shaping the technology landscape through the growing adoption of high-efficiency monocrystalline, TOPCon, and bifacial solar modules. Manufacturers are focusing on improving conversion efficiency, durability, and power output while reducing degradation and balance-of-system costs. Advanced technologies such as half-cut cells, multi-busbar designs, and anti-reflective coatings are further enhancing energy generation under Brazil's diverse climatic conditions. These innovations are increasing project performance and accelerating the deployment of utility-scale and distributed solar installations.

Inverter and BOS Technology

Inverter and BOS technology improve system efficiency, safety, and grid compatibility. Advanced string inverters, microinverters, optimizers, smart meters, mounting structures, and protection systems help maximize energy output and reduce operational losses. These technologies also support remote monitoring, fault detection, and better integration with distributed generation and utility-scale projects. As solar deployment expands, efficient inverter and balance-of-system solutions are becoming critical for reliable and cost-effective project performance.

Concentrated Solar Power Technology

Concentrated solar power (CSP) technology offers an alternative solar solution for large-scale power generation. CSP uses mirrors or lenses to concentrate sunlight and generate thermal energy, which can be stored and converted into electricity when needed. In May 2026, a partnership with the Government of Piauí was announced supporting the development of Brazil’s first concentrated solar power (CSP) initiative with thermal storage. The agreement with the Piauí Institute of Technology includes technical, economic, and regulatory feasibility studies for a proposed 100 MW tower CSP project. The project aims to increase dispatchable renewable power supply while addressing solar intermittency and grid evacuation challenges. Its potential is especially relevant for high-irradiation regions where hybrid solar and storage projects are being explored.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Monocrystalline Silicon |

42.8% |

2025 |

|

End Use |

Commercial |

46.3% |

2025 |

|

Region |

Southeast |

39.7% |

2025 |

By Type

Monocrystalline silicon leads at 42.8% (2025) due to its higher conversion efficiency, longer lifespan, and superior performance under high-temperature conditions. Its ability to generate more electricity from limited installation space makes it the preferred choice for residential, commercial, and utility-scale solar projects across the country.

To access detailed market analysis, Request Sample

Polycrystalline silicon at 27.6% reflects its lower manufacturing cost and cost-effective performance for large-scale installations. Crystal silicon at 16.4% reflects standard c-Si commercial modules. Thin film at 8.7% grows fastest at ~28.6% CAGR through floating solar hydroelectric reservoir and BIPV building-integrated facade applications. Others at 4.5% include emerging perovskite and tandem cell pilot technologies.

By End Use

Commercial leads at 46.3% (2025), through shopping mall and retail rooftop distributed generation, agribusiness self-consumption, ESG corporate mandate solar, and industrial self-generation.

Residential at 34.8% as households increasingly adopt rooftop solar systems to lower electricity bills and reduce dependence on the grid. Industrial at 18.9% reflects mining, manufacturing, and large industrial self-generation through factory rooftop and ground-mount solar.

Regional Market Insights

|

Region |

Share (2025) |

Key Brazil Solar Panel Market Drivers & Characteristics |

|

Southeast |

39.7% |

Supported by high electricity demand, strong commercial and industrial activity, widespread rooftop solar adoption, and well-developed grid infrastructure. |

|

South |

22.8% |

Driven by growing residential and commercial installations, supportive financing, and increasing investments in distributed solar generation. |

|

Northeast |

18.6% |

Benefiting from excellent solar irradiation, rapid expansion of utility-scale solar parks, and continued renewable energy investments. |

|

Central-West |

11.4% |

Supported by expanding agribusiness operations, large land availability, and rising adoption of captive solar systems for commercial and agricultural users. |

|

North |

7.5% |

Driven by increasing off-grid and distributed solar installations, rural electrification initiatives, and efforts to reduce dependence on diesel-based power generation. |

Southeast's 39.7% dominance reflects its high population density, strong industrial and commercial base, higher electricity consumption, and widespread adoption of distributed rooftop solar systems. South's 22.8% follows with growing residential and commercial installations supported by favorable financing and increasing renewable energy investments.

Northeast's 18.6% remains a key hub for utility-scale solar development because of its exceptional solar irradiation and availability of large land parcels. Central-West's 11.4% is witnessing rising solar adoption across agricultural and industrial operations. North's 7.5% is gradually expanding through off-grid and distributed solar projects aimed at improving energy access in remote areas.

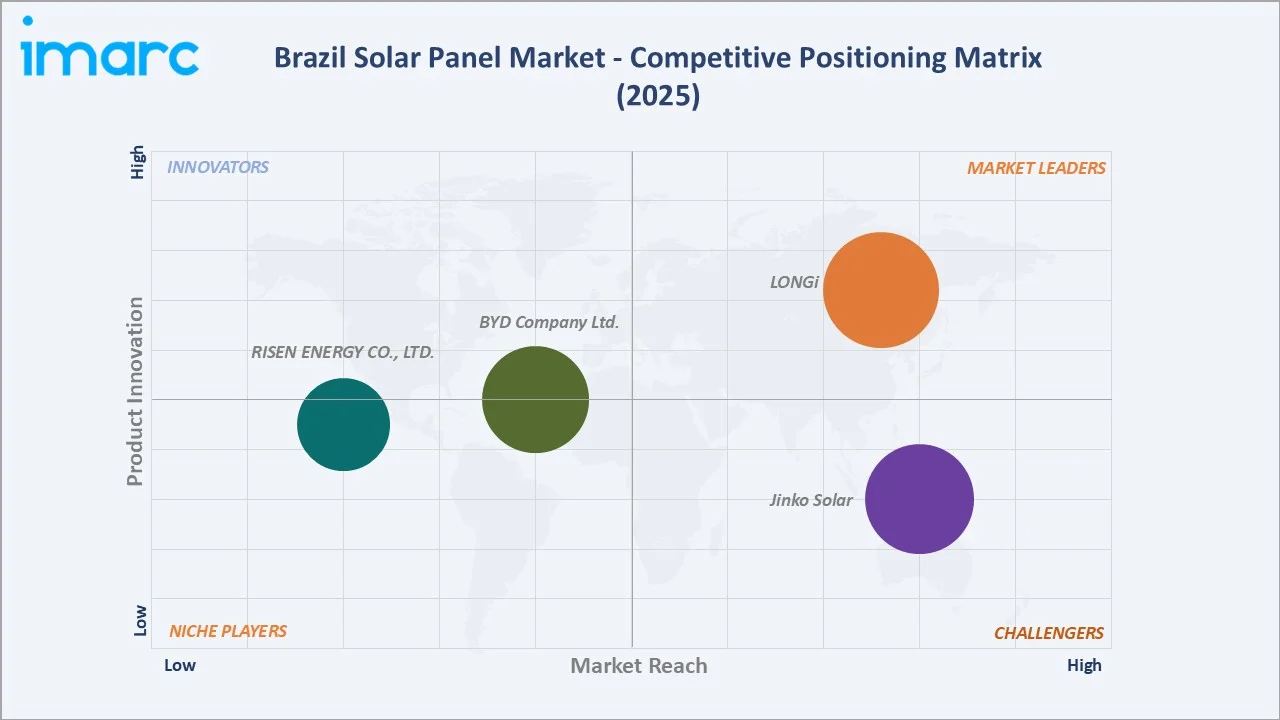

Competitive Landscape

The Brazil solar panel market is moderately competitive, with global module manufacturers, domestic distributors, EPC players, and project developers competing across utility-scale and distributed solar segments. Competition is shaped by panel efficiency, pricing, warranty terms, financing support, and installation capabilities. Leading companies focus on high-efficiency modules, rooftop solar solutions, and large solar park development.

|

Company |

Key Products |

Market Position |

Core Strength |

|

LONGi |

Hi-MO 9, Hi-MO 7, Hi-MO X6, Hi-MO 5m, Hi-MO 5 |

Market Leader |

LONGi is a primary supplier of high-efficiency photovoltaic modules and solar technology in Brazil. The company drives the nation's energy transition by supplying hundreds of megawatts for utility-scale power plants and distributed generation networks. |

|

BYD Company Ltd. |

HALO, AURO N series, AURO P series |

Established Player |

BYD Company Ltd. is a major player in Brazil's renewable energy sector, operating as a primary manufacturer of photovoltaic (PV) modules and a provider of utility-scale solar engineering, procurement, and construction. |

|

Jinko Solar |

Tiger Neo 72HC, Tiger Neo 72HC-BDV, Tiger Neo 60HC, Tiger Neo 78HC-BDV |

Challenger |

JinkoSolar is a dominant force in Brazil’s solar market, consistently ranking as the largest volume importer of photovoltaic modules in the country's distributed generation sector. The company drives Brazil's renewable energy transition by supplying high-efficiency N-type modules for massive utility-scale projects and everyday rooftop installations. |

|

RISEN ENERGY CO., LTD. |

Hyper-ion Pro 745Wp, Hyper-ion 715Wp |

Established Player |

RISEN ENERGY CO., LTD. is a leading tier-one supplier in Brazil's solar market, historically ranking among the top module importers in the country. The company plays a critical role in supplying advanced, utility-scale Heterojunction Technology (HJT) and energy storage solutions to major Brazilian developers. |

Partnerships with utilities, commercial users, and renewable energy investors are becoming important for market expansion. The market also sees growing competition from integrated players offering EPC, O&M, storage, and energy management services.

Key Company Profiles

LONGi

LONGi is one of the leading suppliers of high-efficiency solar PV modules in the Brazil solar panel market, serving utility-scale, commercial, industrial, and residential projects. LONGi has strengthened its presence in Brazil through partnerships with local distributors and participation in large-scale solar projects. The company is also expanding its sustainability initiatives in Brazil through photovoltaic module recycling and circular economy programs.

- Key Products: Hi-MO 9, Hi-MO 7, Hi-MO X6, Hi-MO 5m, Hi-MO 5.

- Recent Developments: In August 2025, LONGi officially introduced its HPBC 2.0 photovoltaic modules in Brazil, bringing advanced solar technology focused on higher performance, improved safety, and refined design. The Hybrid Passivated Back Contact technology is designed to deliver stronger output across multiple applications, including residential rooftops, distributed generation systems, centralized projects, and large ground-mounted solar plants.

- Strategic Focus: Centered on supplying high-efficiency monocrystalline and bifacial PV modules for utility-scale, commercial, and distributed generation projects. The company is strengthening partnerships with local developers, distributors, and integrators to expand its reach across Brazil’s fast-growing solar market.

Jinko Solar

Jinko Solar is a leading solar module manufacturer with a strong presence in the Brazil solar panel market, supplying high-efficiency PV modules for utility-scale, commercial, industrial, and distributed generation projects. The company offers advanced technologies such as N-type TOPCon, bifacial, and high-power modules that support Brazil’s growing demand for efficient solar systems.

- Key Products: Tiger Neo 72HC, Tiger Neo 72HC-BDV, Tiger Neo 60HC, Tiger Neo 78HC-BDV.

- Strategic Focus: Centered on expanding the supply of high-efficiency N-type TOPCon, bifacial, and high-power PV modules for utility-scale, commercial, and distributed generation projects. The company emphasizes product reliability, competitive pricing, and long-term performance to support Brazil’s rapidly growing solar installations.

Market Concentration Analysis

The Brazil solar panel market is moderately fragmented, with global module suppliers, regional distributors, EPC contractors, and project developers competing across distributed and utility-scale segments. Large international players hold strong positions through technology, scale, and pricing. However, the market also includes many local installers and integrators serving residential and commercial rooftop demand. Market concentration is higher in utility-scale projects due to large procurement volumes and bankability requirements, while distributed generation remains more fragmented. Competition is expected to intensify as high-efficiency modules, storage integration, and local partnerships become key differentiators.

Investment & Growth Opportunities

Highest Growth Segments

Thin film floating solar (~28.6% CAGR), monocrystalline N-type TOPCon (~25.8% CAGR), commercial C&I (~24.5% CAGR), Northeast utility-scale (~26% CAGR through irradiation advantage), agrivoltaics Central-West (~27% CAGR from growing base), and battery storage hybrid (~30% CAGR from emerging base) represent Brazil solar panel highest-growth investment vectors through 2034.

Investment Themes

- N-Type TOPCon premium module manufacturing: Investment in N-Type TOPCon modules offers strong potential as Brazil’s market shifts toward higher-efficiency, lower-degradation solar technologies for rooftops and utility-scale projects.

- Floating solar and agrivoltaics dual-land use: Floating solar and agrivoltaics create opportunities to expand solar capacity while optimizing water bodies and agricultural land, reducing land-use conflicts and supporting sustainable power generation.

Future Market Outlook (2026-2034)

Brazil solar panel market is projected to grow from 8.04 GW in 2025 to 55.32 GW by 2034, delivering a 23.90% CAGR over the forecast period through N-Type TOPCon premium efficiency mainstream, ESG agribusiness C&I scale, floating solar and agrivoltaics dual-land-use, and battery storage hybrid integration. The market's anchor value of 23.48 GW in 2030 represents Brazil solar at N-Type mainstream and transition inflection.

Three structural forces define Brazil's solar panel market growth through 2034. First, continued expansion of distributed generation and utility-scale solar parks will sustain strong demand for high-efficiency PV modules. Second, rising investments in grid modernization, battery energy storage, and transmission infrastructure will improve renewable energy integration and system reliability. Third, supportive decarbonization policies, growing corporate renewable energy procurement, and increasing adoption of advanced technologies such as TOPCon, bifacial modules, and hybrid solar-plus-storage systems will accelerate long-term market expansion.

Research Methodology

Primary Research

Primary research comprised interviews with solar module suppliers, EPC contractors, project developers, distributors, installers, and commercial end users across Brazil. It also included discussions with utility-scale solar operators, rooftop solar integrators, and industry experts to validate demand trends, technology adoption, pricing, and project pipeline assumptions.

Secondary Research

Secondary research encompassed company websites, annual reports, investor presentations, government energy databases, regulatory publications, and industry association reports. It also included solar project announcements, trade publications, policy documents, and market data sources to assess capacity additions, technology trends, competitive activity, and regional demand patterns.

Forecasting Models

Forecasting models combined historical solar installation trends, planned project pipelines, policy developments, electricity demand growth, and investment patterns to estimate future market expansion. The analysis incorporated technology adoption rates, module pricing trends, distributed generation growth, and utility-scale capacity additions. Macroeconomic indicators, regulatory changes, and renewable energy targets were also evaluated to generate reliable market forecasts through 2034.

Brazil Solar Panel Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | GW |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Crystal Silicon, Monocrystalline Silicon, Polycrystalline Silicon, Thin Film, Others |

| End Uses Covered | Commercial, Residential, Industrial |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | LONGi, BYD Company Ltd., Jinko Solar, RISEN ENERGY CO., LTD., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil solar panel market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil solar panel market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil solar panel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Solar Panel Market Report

The Brazil solar panel market reached 8.04 GW installed capacity in 2025, driven by rapid growth in distributed rooftop solar, utility-scale solar parks, and rising electricity costs that encourage self-generation. Supportive renewable energy policies, declining PV system costs, corporate decarbonization goals, and increasing investments in grid-connected solar projects are further accelerating market expansion.

The Brazil solar panel market grows at 23.90% CAGR during 2026-2034, reaching 55.32 GW by 2034. The CAGR reflects high grid tariff, abundant irradiation, and ESG agribusiness C&I demand.

Monocrystalline silicon leads at 42.8% due to its higher efficiency, better durability, and stronger energy output compared to other module types. Its suitability for rooftops, commercial systems, and utility-scale projects makes it the preferred technology across Brazil.

Commercial leads at 46.3% as businesses increasingly install rooftop and captive solar systems to reduce electricity costs and improve energy security. Large commercial buildings, malls, offices, and warehouses provide suitable rooftop space, making solar adoption scalable and cost-effective.

Southeast leads at 39.7% due to its dense population, strong commercial and industrial base, and high electricity consumption. The region’s advanced grid infrastructure and wider rooftop solar adoption further support strong demand for solar panel installations.

Leading companies include LONGi, BYD Company Ltd., Jinko Solar, and RISEN ENERGY CO., LTD., among others.

The market is projected to reach approximately 23.48 GW by 2030, driven by the rapid expansion of distributed rooftop systems and utility-scale solar parks. Declining PV costs, rising electricity prices, and clean energy investments are expected to sustain strong installation growth across Brazil.

Three priority investment opportunities in the Brazil solar panel market include expanding N-Type TOPCon and bifacial module manufacturing to meet demand for high-efficiency technologies, investing in utility-scale solar parks integrated with battery energy storage systems (BESS) to enhance grid stability, and developing commercial and industrial rooftop solar projects supported by distributed generation. Additional opportunities are emerging in floating solar and agrivoltaic projects, which optimize land and water use while supporting Brazil's long-term renewable energy transition.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)