Brazil Sports Nutrition Market Size, Share, Trends and Forecast by Product Type, Origin, Distribution Channel, and Region, 2026-2034

Brazil Sports Nutrition Market Size, Share, Trends & Forecast (2026-2034)

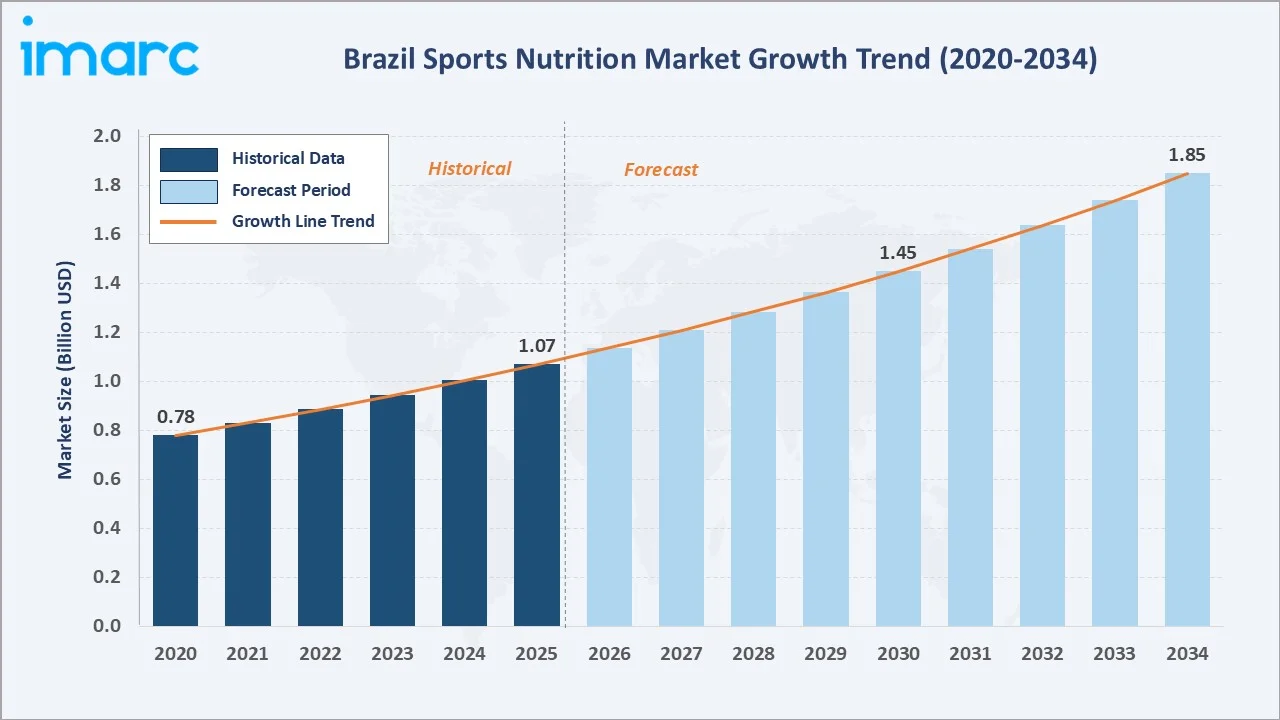

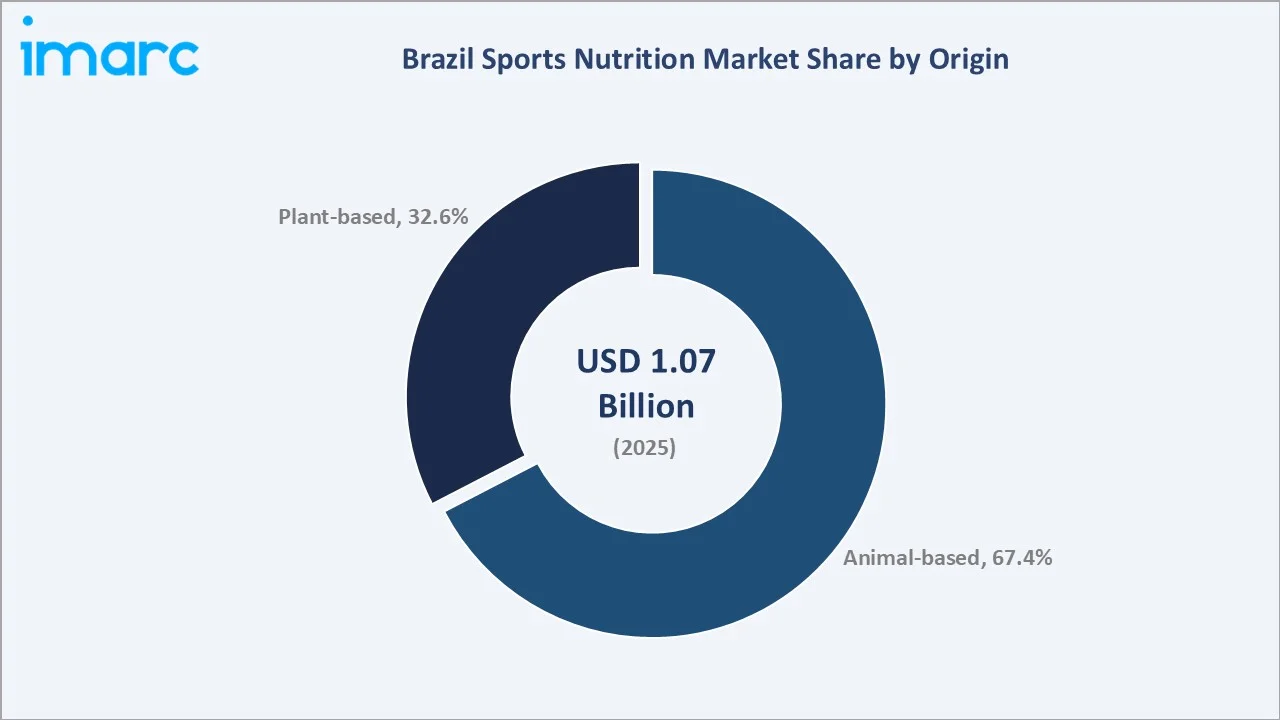

The Brazil sports nutrition market reached USD 1.07 Billion in 2025 and is projected to reach USD 1.85 Billion by 2034, growing at a CAGR of 6.34% during 2026-2034. The market is driven by an expanding fitness culture, rising gym memberships, and growing consumer preference for plant-based alternatives. Brazil's fitness sector counts more than 34,000 health clubs nationwide, yet gym penetration remains close to 4.6% in 2025, leaving substantial room for category growth. Sports supplements lead the product type segment at 52.8%, reflecting strong protein and amino-acid demand among gym-goers. Animal-based formulations dominate the origin segment at 67.4%, while plant-based options are gaining ground through clean-label trends. Southeast region leads regionally at 43.6%, anchored by São Paulo's dense fitness infrastructure and e-commerce penetration.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.07 Billion |

|

Forecast Market Size (2034) |

USD 1.85 Billion |

|

CAGR (2026-2034) |

6.34% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Sports Supplement (52.8%, 2025) |

|

Dominant Origin |

Animal-based (67.4%, 2025) |

|

Leading Region |

Southeast (43.6%, 2025) |

The Brazil sports nutrition market grew from USD 0.78 Billion in 2020 to USD 1.07 Billion in 2025, reflecting steady demand from gym-goers, athletes, and health-conscious consumers across the country's expanding fitness ecosystem. It is expected to reach USD 1.45 Billion by 2030, supported by rising protein consumption, e-commerce growth, and broader product accessibility. By 2034, the market is forecast to reach USD 1.85 Billion, driven by continued fitness club expansion, plant-based innovation, and digital direct-to-consumer adoption. Overall, the market reflects consistent long-term growth as Brazil strengthens its position as Latin America's largest fitness and wellness market.

To get more information on this market, Request Sample

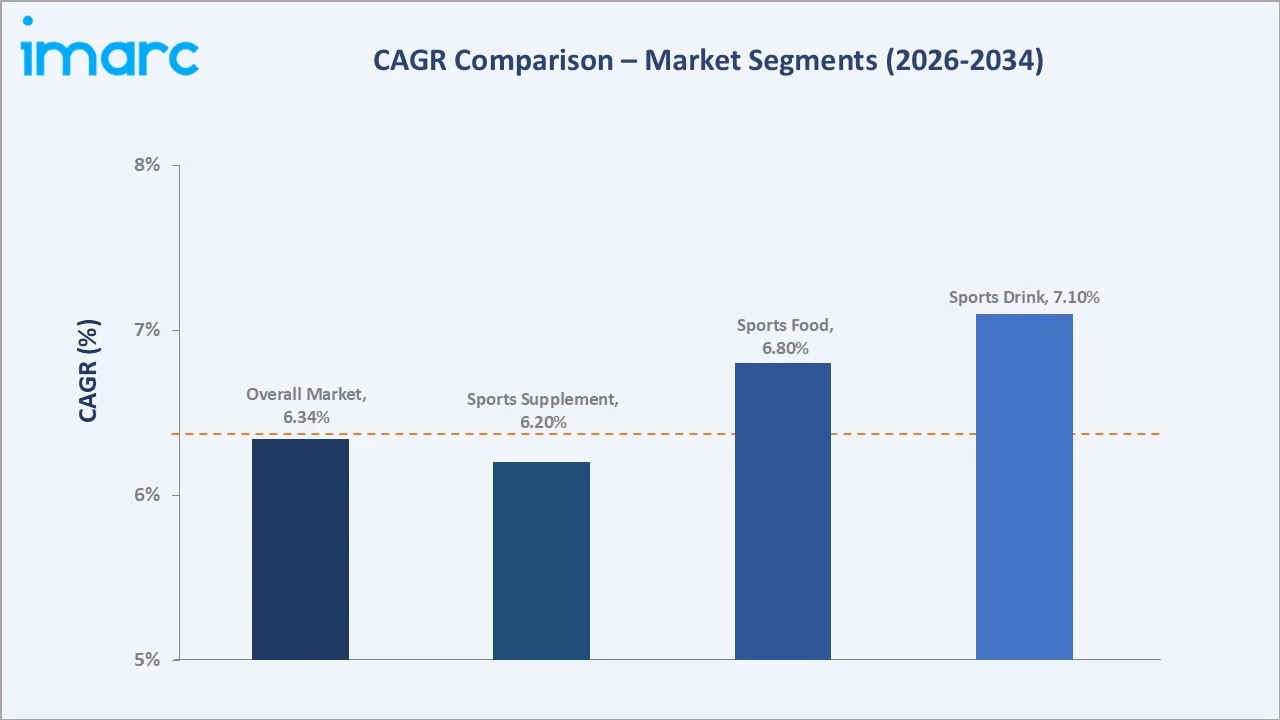

Sports Drink grows fastest at an estimated ~7.1% CAGR through 2034, supported by e-commerce expansion and hydration-focused product launches. Sports Supplement maintains steady growth near 6.2% CAGR as protein and amino-acid demand persists. Sports Food expands at roughly 6.8% CAGR, driven by convenient, on-the-go protein bar and snack formats.

Executive Summary

The Brazil sports nutrition market is expanding steadily, supported by the country's large and growing fitness infrastructure. Smart Fit alone operated around 1,000 gyms nationwide by late 2025, reflecting accelerating health club penetration across urban and secondary cities. Rising consumer focus on muscle recovery, performance, and weight management is increasing demand for protein powders, ready-to-drink beverages, and functional bars.

Market growth is also supported by digital retail expansion, with online stores forecast to outpace traditional brick-and-mortar channels through 2030. Manufacturers are investing in plant-based formulations, flavor innovation, and influencer-driven marketing to capture younger, digitally native consumers. Sports Supplement at 52.8% leads through whey protein and amino-acid demand. Animal-based products at 67.4% lead through established efficacy credentials. Southeast Brazil leads regionally at 43.6%.

Regulatory clarity from ANVISA's food supplement category, established in 2018, has further enabled product innovation while preserving safety standards. The market outlook remains positive, with consistent double-digit growth expected in plant-based and online distribution sub-segments through the forecast period.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Sports Supplement - 52.8% share (2025) |

|

Dominant Origin |

Animal-based - 67.4% market share (2025) |

|

Leading Region |

Southeast - 43.6% share (2025) |

|

Top Companies |

Supley Laboratório de Alimentos e Suplementos Nutricionais Ltda, Glanbia plc, Integralmédica Suplementos Nutricionais Ltda, and Merama |

|

Market Opportunities |

Plant-based protein innovation; e-commerce and D2C platform expansion; functional bar and RTD formats; corporate wellness partnerships; precision personalization through digital coaching |

Key Analytical Observations Supporting The Above Data:

- Sports Supplement at 52.8%: Sports supplements dominate due to strong whey protein and amino-acid demand among gym-goers and athletes. Their established efficacy, wide retail availability, and brand loyalty make them the preferred choice across Brazil's fitness community.

- Animal-based at 67.4%: Animal-based formulations lead due to their proven amino-acid profile and broad acceptance among performance-focused consumers. Whey protein concentrate remains the default choice for muscle recovery despite rising plant-based interest.

- Southeast at 43.6%: Southeast Brazil dominates regionally due to its dense concentration of gyms, fitness studios, and e-commerce logistics infrastructure centered around São Paulo and Rio de Janeiro. The region's high disposable income and fitness culture support sustained sports nutrition consumption.

Brazil Sports Nutrition Market Overview

Brazil sports nutrition market operates within the broader Latin American sports nutrition landscape as the region's dominant contributor, representing the highest regional revenue. The market's commercial uniqueness lies in its dense fitness club infrastructure, creating sports nutrition demand above pure retail grocery distribution.

The Brazil sports nutrition ecosystem integrates raw material suppliers, ingredient processors, manufacturers, distribution and retail networks, and the regulatory framework overseen by ANVISA. Macroeconomic factors include rising disposable incomes, expanding gym and fitness club penetration, and increasing demand for performance and recovery nutrition amid a growing, health-conscious middle class.

Market Dynamics

To evaluate market opportunities, Request Sample

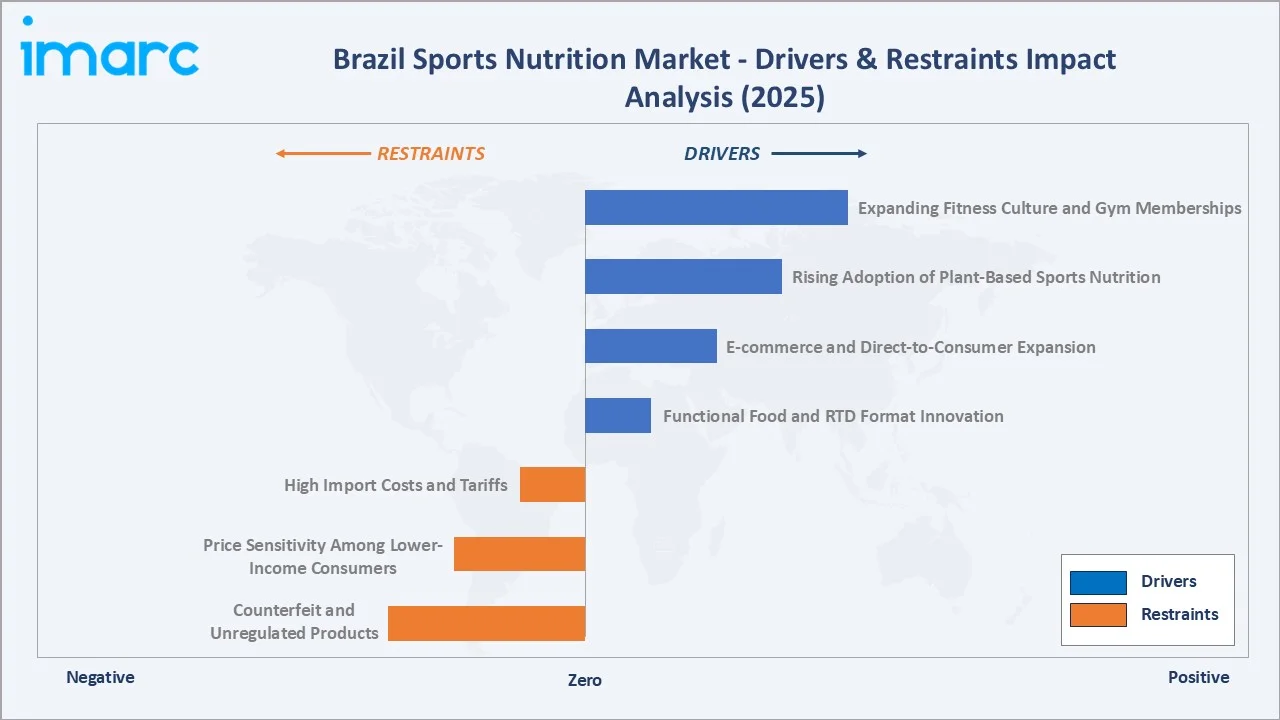

Market Drivers

- Expanding Fitness Culture and Gym Memberships: Brazil's fitness sector has witnessed remarkable growth in health club establishments, with Smart Fit alone operating around 1,000 gyms nationwide by the fourth quarter of 2025. This fitness boom is supported by technological integration, where connected equipment and wearable-compatible machines are becoming standard. Growing gym membership directly translates into rising demand for protein powders and performance-enhancing nutrition products.

- Rising Adoption of Plant-Based Sports Nutrition: Research indicates that 67% of Brazilian consumers express interest in plant protein alternatives, reflecting a broader shift in dietary patterns. Manufacturers are responding with pea protein, soy protein, and other plant-based formulations that match the amino-acid profile of conventional whey-based products. This trend extends beyond vegans to mainstream fitness enthusiasts seeking sustainable options.

- E-commerce and Direct-to-Consumer Expansion: Online retail stores are forecast to register a CAGR exceeding 10% between 2025-2030, significantly outpacing traditional channels. Mobile-first websites, subscription replenishment plans, and rapid last-mile delivery are enhancing convenience, particularly in secondary cities where specialist sports nutrition stores remain limited.

Market Restraints

- High Import Costs and Tariffs: Import taxes have historically added 30-35% to product costs for foreign brands entering Brazil, limiting affordability and slowing premium product penetration outside major metropolitan markets.

- Price Sensitivity Among Lower-Income Consumers: Brazil's income inequality means value-tier products often compete directly with premium offerings, creating margin pressure for manufacturers targeting broader consumer adoption.

Market Opportunities

- Functional Food and RTD Format Innovation: Growing demand for ready-to-drink protein shakes and single-serve sachets is creating opportunities for manufacturers to expand beyond traditional powder formats into mass retail and convenience channels.

- Corporate Wellness Partnerships: Platforms aggregating thousands of partner gyms are creating new institutional distribution channels for sports nutrition brands targeting corporate wellness programs.

Market Challenges

- Counterfeit and Unregulated Products: Counterfeit supplements weaken demand for legitimate branded products and create price pressure for authorized suppliers, while also raising consumer safety concerns.

- Regulatory Compliance Complexity: ANVISA's food supplement labeling and safety requirements demand continuous compliance investment, particularly for smaller domestic manufacturers competing against multinational players.

Emerging Market Trends

1. Connected Gym Equipment and Wearable Integration

Connected gym equipment and wearable integration are emerging as fitness operators invest in technology that tracks calories, heart rate, and performance progression. This trend is increasing consumer engagement with personalized nutrition recommendations linked to workout data, supporting demand for targeted sports nutrition products.

2. Plant-Based Protein Diversification

Plant-based protein diversification is emerging as manufacturers introduce pea, soy, and blended formulations with improved taste profiles. This trend is supported by sustainability-conscious consumers and is expanding the addressable market beyond traditional whey-based buyers.

3. Direct-to-Consumer Digital Platforms

Direct-to-consumer digital platforms are emerging as brands launch algorithm-driven personalized product recommendation engines. This trend enables companies to gather first-party data and offer tailored bundle offerings, strengthening customer retention and lifetime value.

4. Functional Food Formats at Sporting Events

Functional food formats are gaining visibility through sponsorships and product launches at major fitness and sporting events. This trend is increasing brand awareness and trial among performance-focused consumers seeking convenient, high-protein snacking options.

Industry Value Chain Analysis

The Brazil sports nutrition value chain integrates raw material sourcing, ingredient processing, product formulation and manufacturing, distribution and retail, and end-consumer engagement across fitness and wellness channels.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Dairy and whey suppliers, plant protein cultivators, ingredient importers |

|

Ingredient Processing |

Protein isolate and concentrate processors, flavor and additive suppliers |

|

Product Formulation & Manufacturing |

Sports nutrition manufacturers, contract formulators, packaging providers |

|

Quality and Regulatory Compliance |

ANVISA, testing laboratories, certification bodies |

|

Distribution & Retail |

Supermarkets, specialty stores, pharmacies, online platforms, gym retail counters |

|

End-Consumer Engagement |

Athletes, gym members, fitness enthusiasts, health-conscious consumers |

The product formulation and manufacturing stage is the most value-added stage in the Brazil sports nutrition value chain. This stage transforms raw protein and functional ingredients into differentiated products with specific taste, solubility, and nutritional characteristics. Innovation in plant-based formulations and flavor systems enables companies to command premium pricing and strengthen competitive positioning.

Technology Landscape in the Brazil Sports Nutrition Industry

Formulation and Flavor Technology

Advances in flavor masking and solubility technology are improving the taste, texture, and mixability of protein powders, particularly for plant-based formulations that historically faced grittiness and aftertaste challenges. Microencapsulation and enzymatic hydrolysis techniques are helping manufacturers mask bitter notes from pea and rice protein isolates while preserving amino-acid bioavailability. These innovations are narrowing the sensory gap between animal-based and plant-based products, encouraging trial among mainstream consumers who previously avoided plant-based options due to taste concerns.

Connected Fitness and Personalization

Wearable-compatible gym equipment and fitness apps are enabling personalized nutrition recommendations linked to individual performance data, creating new cross-selling opportunities for sports nutrition brands. Connected machines across major Brazilian gym chains now track calories, heart rate, and training load, generating data brands can use to recommend tailored protein dosages or recovery products. This convergence of fitness technology and nutrition is deepening consumer engagement and supporting premium positioning across digitally integrated retail and gym-based channels.

E-commerce and Digital Retail Infrastructure

Algorithm-driven recommendation engines and subscription replenishment systems are reshaping how consumers discover and repurchase sports nutrition products through direct-to-consumer digital channels. Brands are deploying machine-learning models that analyze purchase history and fitness goals to suggest personalized bundles, while automated replenishment reduces stockouts and strengthens retention. Mobile-first checkout flows, real-time inventory syncing, and last-mile delivery partnerships are further accelerating online category growth, particularly in secondary cities with limited specialty retail presence.

Sustainable Packaging Innovation

Manufacturers are increasingly adopting recyclable and reduced-plastic packaging formats in response to growing consumer environmental awareness, particularly within the plant-based product segment. Innovations include mono-material pouches that simplify recycling, paper-based tubs replacing rigid plastic containers, and concentrated formulations that cut packaging volume and shipping weight. These shifts are also helping brands meet tightening extended producer responsibility expectations while appealing to sustainability-conscious fitness consumers who increasingly factor packaging credentials into purchase decisions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Sports Supplement |

52.8% |

2025 |

|

Origin |

Animal-based |

67.4% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

Southeast |

43.6% |

2025 |

By Product Type

Sports Supplement leads at 52.8% (2025), driven by strong whey and plant-based protein powder demand, amino-acid formulations, and pre/post-workout products across gym retail and pharmacy channels.

To access detailed market analysis, Request Sample

Sports Drink follows at 28.6%, supported by hydration-focused and electrolyte-enhanced beverage formats gaining traction through e-commerce and convenience retail. Sports Food accounts for 18.6%, led by protein bars and functional snack formats favored by time-constrained, on-the-go consumers.

By Origin

Animal-based products lead at 67.4% (2025), through established whey protein concentrate and isolate formulations that remain the default choice among performance-focused consumers across Brazil's gym network.

Plant-based products account for 32.6%, growing through pea, soy, and rice protein innovations that appeal to sustainability-conscious and lactose-sensitive consumers. This segment benefits from improving taste profiles and expanding flavor portfolios introduced by both domestic and multinational manufacturers.

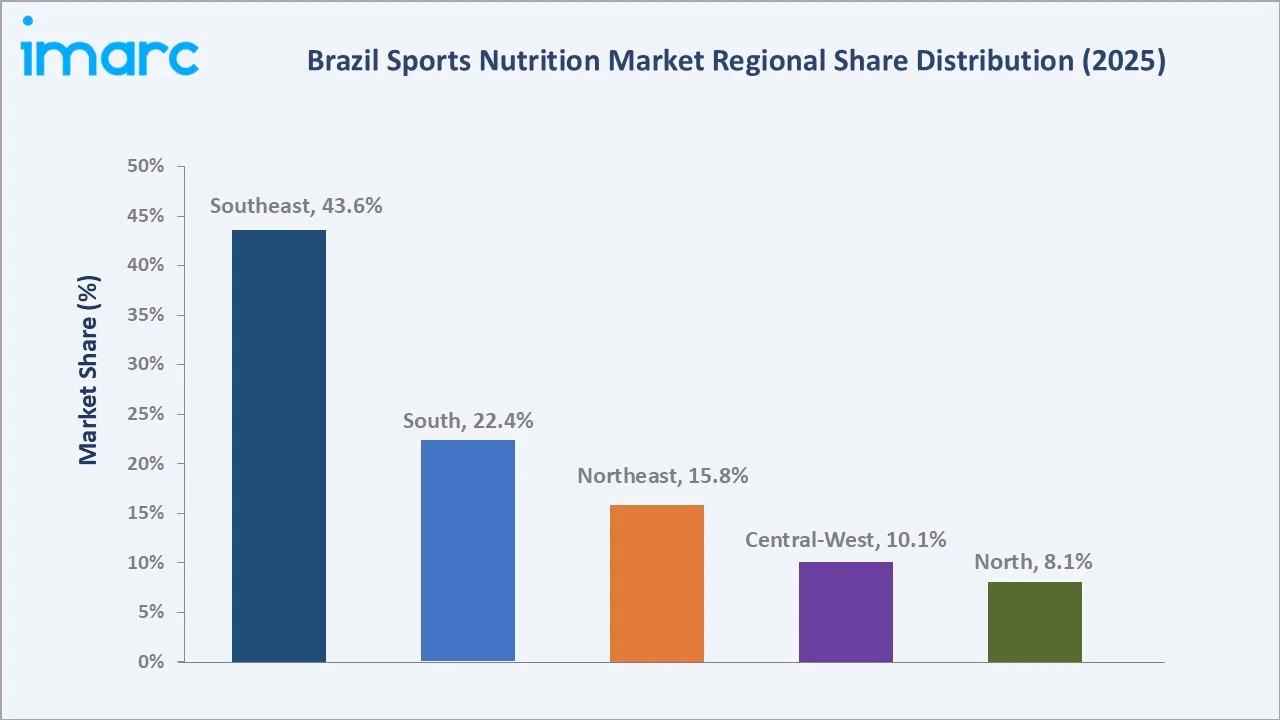

Regional Market Insights

|

Region |

Share (2025) |

Key Brazil Sports Nutrition Market Drivers & Characteristics |

|

Southeast |

43.6% |

Reflecting dense gym and fitness studio infrastructure across São Paulo and Rio de Janeiro, supported by high disposable income and strong e-commerce logistics. |

|

South |

22.4% |

Reflects established health club networks, strong outdoor and recreational sports culture, and steady demand for protein and recovery products. |

|

Northeast |

15.8% |

Supported by expanding budget gym chains, rising health awareness, and growing demand for accessible fitness and nutrition products in urban centers such as Salvador and Recife. |

|

Central-West |

10.1% |

Reflects moderate but steadily rising adoption of fitness services, supported by targeted gym chain expansion and growing digital fitness platform usage. |

|

North |

8.1% |

Supported by gradual fitness infrastructure development and increasing accessibility of sports nutrition products through online and pharmacy channels. |

Southeast Brazil's 43.6% dominance is supported by its concentration of commercial gyms, fitness studios, and established retail and pharmacy distribution networks. South Brazil's 22.4% follows with strong recreational sports culture and consistent demand from health club members.

Northeast Brazil's 15.8% reflects rising budget gym penetration and growing urban health awareness. Central-West at 10.1% and North at 8.1% show steady gains, supported by gradual fitness infrastructure expansion and increasing online retail accessibility across less densely populated regions.

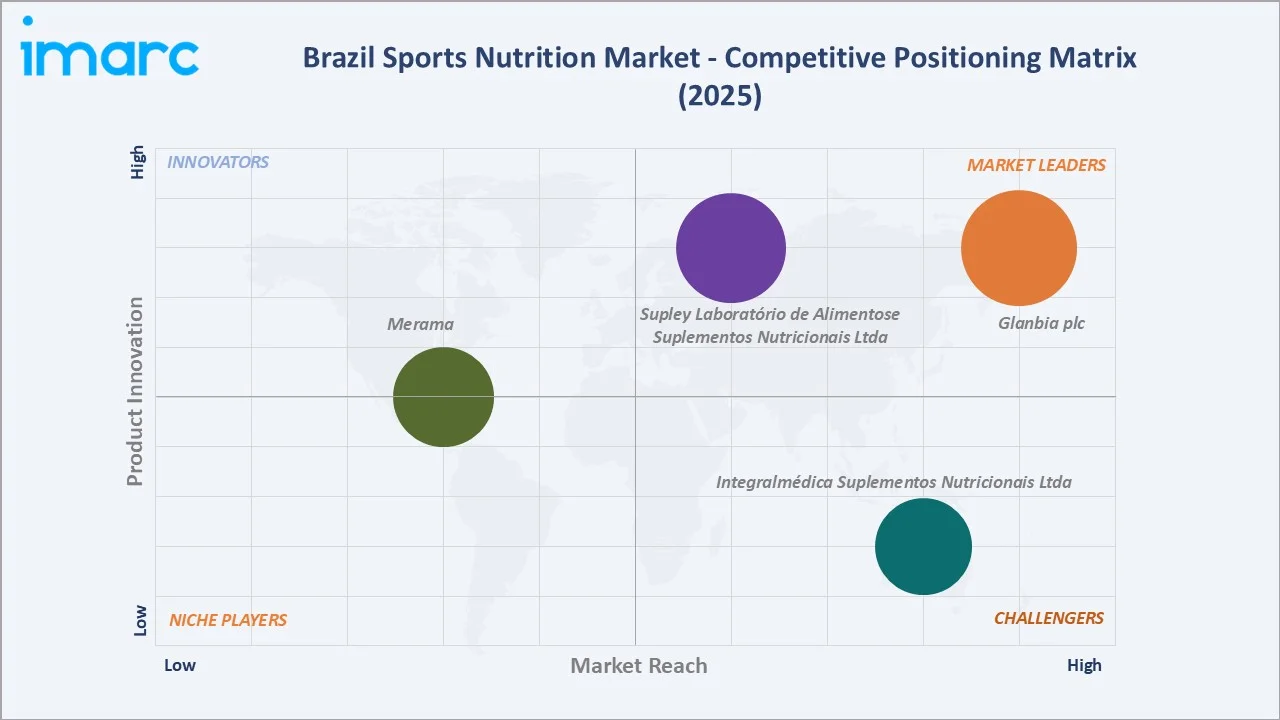

Competitive Landscape

The Brazil sports nutrition market is moderately competitive, with established domestic manufacturers competing alongside multinational brand owners. Key firms focus on protein powders, ready-to-drink beverages, and functional bars, with competition shaped by product efficacy, flavor innovation, distribution reach, and digital marketing capability.

|

Company |

Key Brands |

Market Position |

Core Strength |

|

Supley Laboratório de Alimentos e Suplementos Nutricionais Ltda |

Max Titanium / Probiótica / Dr. Peanut |

Market Leader |

Operating a highly advanced manufacturing plant in Matão, São Paulo, omnichannel distribution, high-value R&D |

|

Glanbia plc |

Optimum Nutrition / Isopure |

Market Leader |

Protein expertise & bioactives, operating locally through its dedicated entity, Glanbia Nutricional Solucoes Brasil Ltda |

|

Integralmédica Suplementos Nutricionais Ltda |

Integralmédica |

Strong Challenger |

Robust brand architecture, deep local penetration & supply chain, direct marketing and community engagement |

|

Merama |

Growth Supplements |

Established Player |

Operates Growth Supplements Produtos Alimentícios, direct-to-consumer model, offering high-quality, lab-tested sports nutrition at highly competitive prices |

Companies are increasingly investing in plant-based formulations, e-commerce platforms, and influencer-driven marketing to address shifting consumer preferences. The market is also seeing stronger participation from digital-native, direct-to-consumer brands as demand rises for personalized nutrition solutions.

Key Company Profiles

Supley Laboratório de Alimentos e Suplementos Nutricionais Ltda

Supley Laboratório de Alimentos e Suplementos Nutricionais Ltda, also known as Grupo Supley, is a prominent player in the Brazilian sports nutrition market. Based in Matão, São Paulo, it operates one of the largest dietary supplement manufacturing hubs in Latin America.

- Key Brands: Max Titanium / Probiótica / Dr. Peanut

- Strategic Focus: Omnichannel retail expansion, brand diversification, and scientific product development.

Glanbia plc

Glanbia operates in the Brazil sports nutrition market through its diverse portfolio, thereby holding a significant position in the Brazilian active lifestyle and fitness scenario. The company serves athletes and fitness enthusiasts with protein powders, meal replacements, and workout supplements.

- Key Brands: Optimum Nutrition / Isopure

- Strategic Focus: Expanding direct-to-consumer digital platforms with algorithm-driven personalized product recommendations to strengthen Brazilian market penetration.

Market Concentration Analysis

The Brazil sports nutrition market shows moderate concentration, with domestic manufacturers such as Supley and Integralmédica holding strong positions alongside multinational brand owners including Glanbia. Large players maintain stronger positions in branded protein powders and established retail distribution networks. However, the market remains fragmented at the specialty and online retail level due to numerous smaller domestic suppliers and emerging direct-to-consumer brands. Rising demand for plant-based and functional formats is also opening space for specialized challenger brands. Overall, competition is shifting from price-based selling toward differentiated formulations, flavor innovation, and digital engagement.

Investment & Growth Opportunities

Highest Growth Segments

Sports Drink (~7.1% CAGR), Sports Food (~6.8% CAGR), plant-based formulations (~8% CAGR), and the Northeast region (~7.5% CAGR) represent Brazil sports nutrition's highest-growth investment vectors through 2034.

Investment Themes

- Plant-based protein expansion: Growing consumer interest in sustainable and clean-label nutrition is creating opportunities for manufacturers investing in pea, soy, and blended plant-protein formulations with improved taste profiles.

- Digital direct-to-consumer platforms: The adoption of algorithm-driven personalization and subscription replenishment models is creating investment opportunities for brands seeking to deepen customer loyalty and capture first-party data.

Future Market Outlook (2026-2034)

The Brazil sports nutrition market is projected to grow from USD 1.07 Billion in 2025 to USD 1.85 Billion by 2034, delivering a 6.34% CAGR over the forecast period through continued fitness infrastructure expansion, plant-based product innovation, and e-commerce acceleration. The market's anchor value of USD 1.45 Billion in 2030 represents the midpoint of sustained category growth as digital retail and functional formats gain wider adoption.

Three structural forces define Brazil sports nutrition market growth through 2034. First, continued expansion of gym and fitness club networks is increasing the addressable consumer base for performance nutrition products. Second, rising consumer preference for plant-based and clean-label formulations is encouraging manufacturers to diversify beyond traditional whey-based offerings. Third, the modernization of retail through e-commerce and direct-to-consumer platforms is supporting higher product accessibility while improving personalization and customer retention.

Research Methodology

Primary Research

Primary research comprised interviews with sports nutrition manufacturers, distributors, gym operators, and fitness retailers across Brazil. Discussions also covered athletes and fitness enthusiasts to gather insights on product preference, pricing, and adoption of plant-based alternatives. Feedback from industry participants helped validate market size, regional trends, and competitive positioning.

Secondary Research

Secondary research encompassed regulatory data from ANVISA, trade publications, company reports, and industry databases. It also included reviews of fitness industry statistics, e-commerce trends, and consumer survey data. Public sources were assessed to map regional distribution patterns and validate market estimates.

Forecasting Models

Forecasting models combined historical market performance, fitness infrastructure growth trends, and macroeconomic indicators to project future demand. The analysis incorporated expected growth in gym membership, e-commerce penetration, and plant-based adoption. Scenario-based forecasting assessed the impact of regulatory and economic variables on long-term projections through 2034.

Brazil Sports Nutrition Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Sports Food, Sports Drink, Sports Supplement |

| Origins Covered | Animal-based, Plant-based |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Convenience Stores, Online Stores, Drug Stores and Pharmacies, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Supley Laboratório de Alimentos e Suplementos Nutricionais Ltda, Glanbia plc, Integralmédica Suplementos Nutricionais Ltda, Merama, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil sports nutrition market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil sports nutrition market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil sports nutrition industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Sports Nutrition Market Report

The Brazil sports nutrition market reached USD 1.07 Billion in 2025, driven by expanding gym infrastructure, rising fitness culture, and growing consumer demand for protein powders and functional nutrition products across urban centers.

The Brazil sports nutrition market grows at 6.34% CAGR during 2026-2034, reaching USD 1.85 Billion by 2034, supported by e-commerce expansion and plant-based product innovation.

Sports Supplement leads at 52.8% due to strong whey and plant-based protein demand among gym members and athletes seeking performance and recovery support across Brazil's fitness community.

Animal-based products lead at 67.4% due to established whey protein efficacy and broad consumer acceptance, though plant-based alternatives are gaining share through sustainability-driven demand.

Southeast Brazil leads at 43.6% due to its dense concentration of gyms and fitness studios across São Paulo and Rio de Janeiro, supported by strong e-commerce logistics and high disposable income.

Leading companies include Supley Laboratório de Alimentos e Suplementos Nutricionais Ltda, Glanbia plc, Integralmédica Suplementos Nutricionais Ltda, and Merama, among others.

The market is projected to reach approximately USD 1.45 Billion by 2030, supported by expanding fitness infrastructure and rising adoption of plant-based and online distribution channels.

Key investment opportunities include plant-based protein innovation, e-commerce and direct-to-consumer platform expansion, and functional ready-to-drink and bar formats targeting time-constrained, performance-focused consumers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)