Brazil Supply Chain Analytics Market Size, Share, Trends and Forecast by Component, Deployment Mode, Enterprise Size, Industry Vertical, and Region, 2026-2034

Brazil Supply Chain Analytics Market Size, Share, Trends & Forecast (2026-2034)

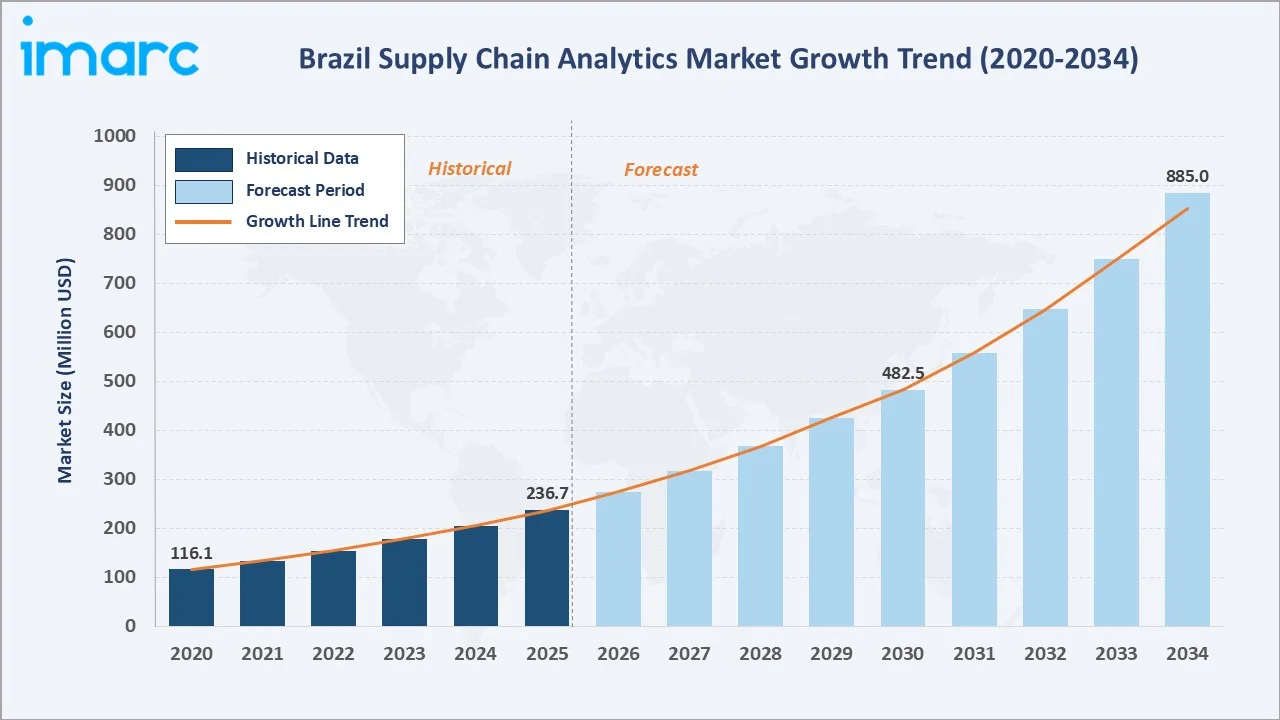

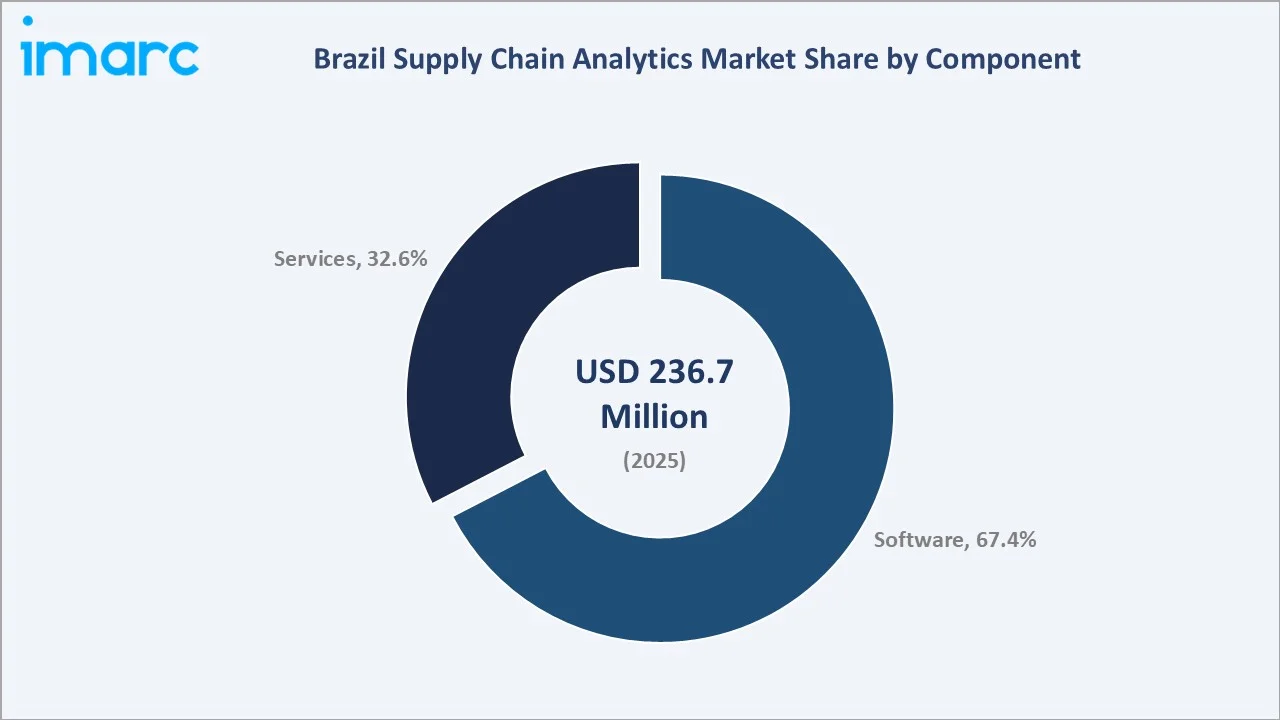

The Brazil supply chain analytics market reached USD 236.7 Million in 2025 and is projected to reach USD 885.0 Million by 2034, growing at a CAGR of 15.31% during 2026-2034. The e-commerce boom driving supply chain visibility demand, accelerating cloud analytics adoption, and Brazil’s growing regulatory compliance requirements for traceability across food and pharmaceutical supply chains are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 236.7 Million |

|

Forecast Market Size (2034) |

USD 885.0 Million |

|

CAGR (2026-2034) |

15.31% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

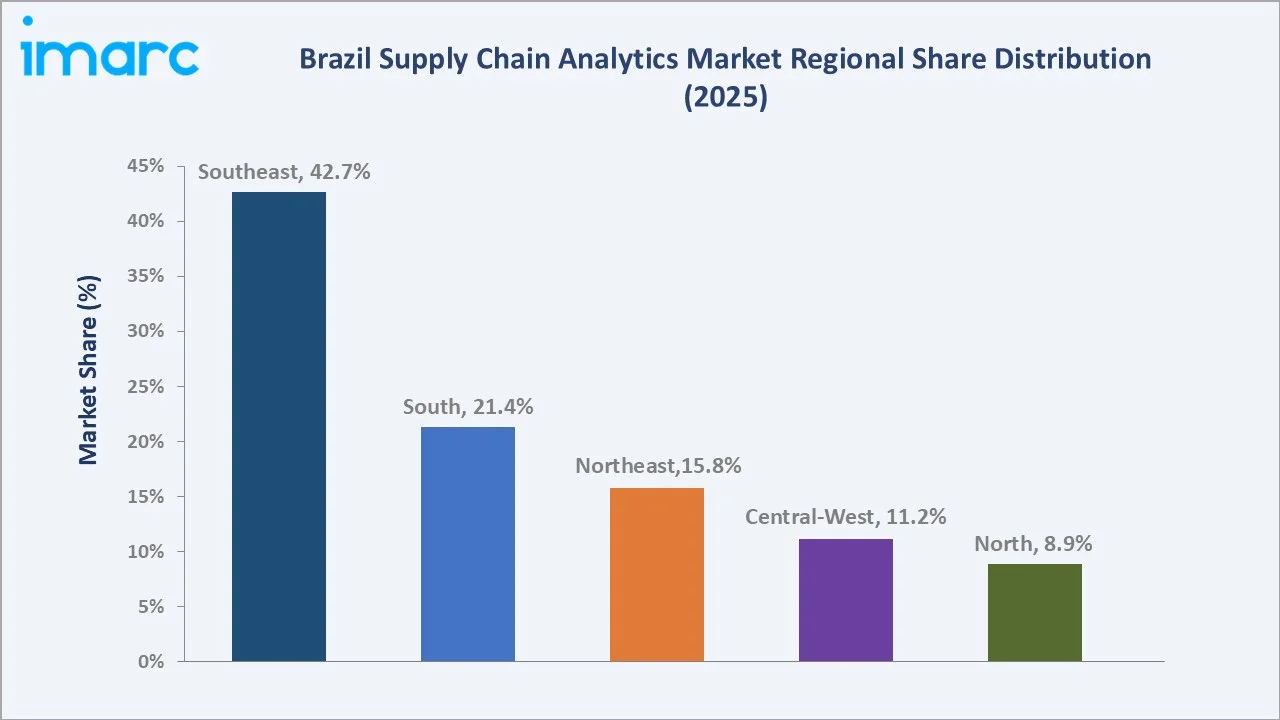

Southeast Brazil leads regionally with a 42.7% market share in 2025, driven by São Paulo state’s position as Latin America’s largest business and logistics hub, hosting the country’s most sophisticated supply chain operations across automotive, food processing, pharmaceutical, and retail sectors alongside the deepest concentration of certified supply chain analytics implementation partners and technology service providers.

To get more information on this market, Request Sample

Brazil’s supply chain analytics market is underpinned by three structural forces: the rapid growth of Brazilian e-commerce, which has quintupled in market size over the past five years and is generating unprecedented supply chain complexity and visibility requirements for retailers and logistics operators; the accelerating adoption of cloud-based analytics platforms that are democratizing sophisticated supply chain intelligence for mid-market enterprises beyond the traditional large multinational adopters; and Brazil’s evolving regulatory frameworks requiring traceability and compliance across food, pharmaceutical, and consumer goods supply chains.

Executive Summary

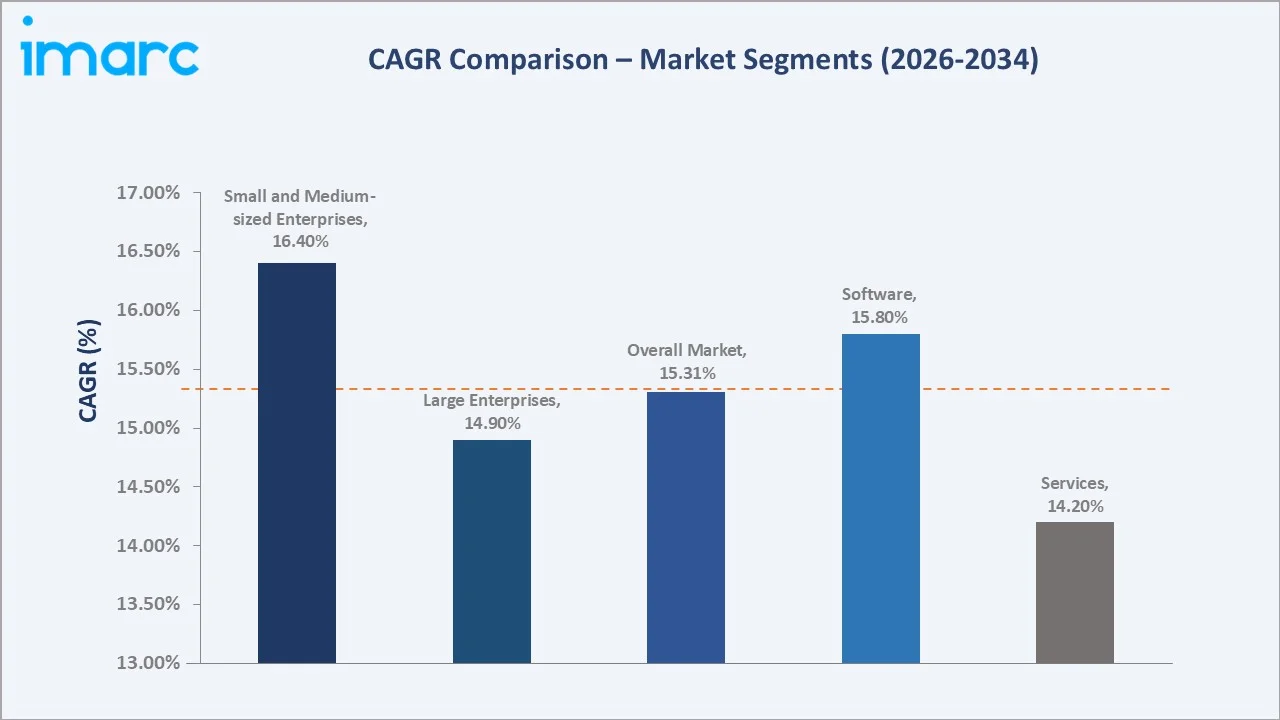

The Brazil supply chain analytics market is experiencing rapid expansion, driven by the convergence of e-commerce-driven supply chain complexity, digital transformation in manufacturing and logistics, and growing recognition among Brazilian enterprises that data-driven supply chain decision-making is essential for operational competitiveness. The market was valued at USD 236.7 Million in 2025 and is forecast to reach USD 885.0 Million by 2034, growing at a CAGR of 15.31%.

Software dominates the component segment with a 67.4% share in 2025, encompassing demand analysis and forecasting platforms, supplier performance analytics tools, spend and procurement analytics applications, inventory analytics solutions, and transportation and logistics analytics software. The software segment’s dominant share reflects the market’s maturation beyond point IoT sensor deployments toward integrated analytics platforms that aggregate data from multiple enterprise systems and external sources to provide comprehensive supply chain visibility and intelligence.

Large enterprises lead the organization-size segment with a 71.5% share in 2025, reflecting the higher analytical sophistication, larger data volumes, and greater financial capacity of Brazil’s multinational corporate subsidiaries and large domestic conglomerates that have historically been the primary adopters of enterprise supply chain analytics platforms. Key global technology vendors collectively define Brazil’s competitive supply chain analytics landscape through integrated software platforms that combine ERP data integration with advanced analytics and AI capabilities.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Software – 67.4% share (2025) |

|

Fastest Growing Component |

Software – ~15.8% CAGR (2026-2034) |

|

Largest Enterprise Size |

Large Enterprises – 71.5% share (2025) |

|

Fastest Growing Enterprise Size |

Small and Medium-sized Enterprises – ~16.4% CAGR (2026-2034) |

|

Leading Region |

Southeast – 42.7% share (2025) |

|

Top Companies |

SAP SE, Oracle Corporation, IBM Corporation, Microsoft, SAS Institute Inc. |

Key Analytical Observations Supporting The Above Data:

- Software at 67.4% share (2025) dominates the component segment, reflecting supply chain analytics’ fundamentally software-centric market structure where platform capabilities for multi-source data integration, predictive analytics, and real-time supply chain visibility represent the primary value creation layer.

- Large enterprises at 71.5% share (2025) lead the organization-size segment, reflecting the higher analytical maturity, larger data volumes generating greater analytics value, and stronger financial capacity of multinational corporate subsidiaries and major domestic conglomerates that form Brazil’s most sophisticated supply chain analytics buyer base.

- SMEs at 28.5% share (2025) are projected to be the fastest-growing segment at approximately 16.4% CAGR, driven by cloud-based SaaS supply chain analytics platforms that have dramatically reduced the upfront investment required for sophisticated analytics capabilities, making supply chain intelligence accessible to mid-market Brazilian companies across food distribution, retail, and manufacturing sectors.

- Southeast Brazil’s 42.7% share (2025) dominance reflects São Paulo’s unrivaled position as the center of Brazil’s e-commerce, manufacturing, logistics, and corporate technology investment, hosting the headquarters of the country’s most analytically sophisticated supply chain organizations and the deepest pool of supply chain analytics implementation talent and consulting capability.

Brazil Supply Chain Analytics Market Overview

Supply chain analytics encompasses the application of data analysis, statistical modeling, machine learning, and artificial intelligence to supply chain operational data for the purpose of improving demand forecasting accuracy, optimizing inventory levels, enhancing supplier performance, streamlining procurement spend, and improving transportation and logistics efficiency. Brazil’s supply chain analytics market serves organizations across manufacturing, retail, food and beverages, healthcare and pharmaceuticals, automotive, and transportation verticals, providing software platforms and professional services that transform operational supply chain data into actionable intelligence.

Brazil’s supply chain analytics market is experiencing structural acceleration driven by two simultaneous forces: the rapid expansion of e-commerce generating new supply chain data volumes and complexity requiring sophisticated analytics capabilities, and the progressive adoption of cloud-based analytics platforms that have fundamentally lowered the implementation cost and time required for supply chain analytics deployment. Brazil e-commerce market reached USD 513.25 Billion in 2025, compelling retailers and marketplace operators to invest in demand forecasting, inventory optimization, and last-mile delivery analytics capabilities that represent structurally new demand for supply chain analytics platforms.

Market Dynamics

To evaluate market opportunities, Request Sample

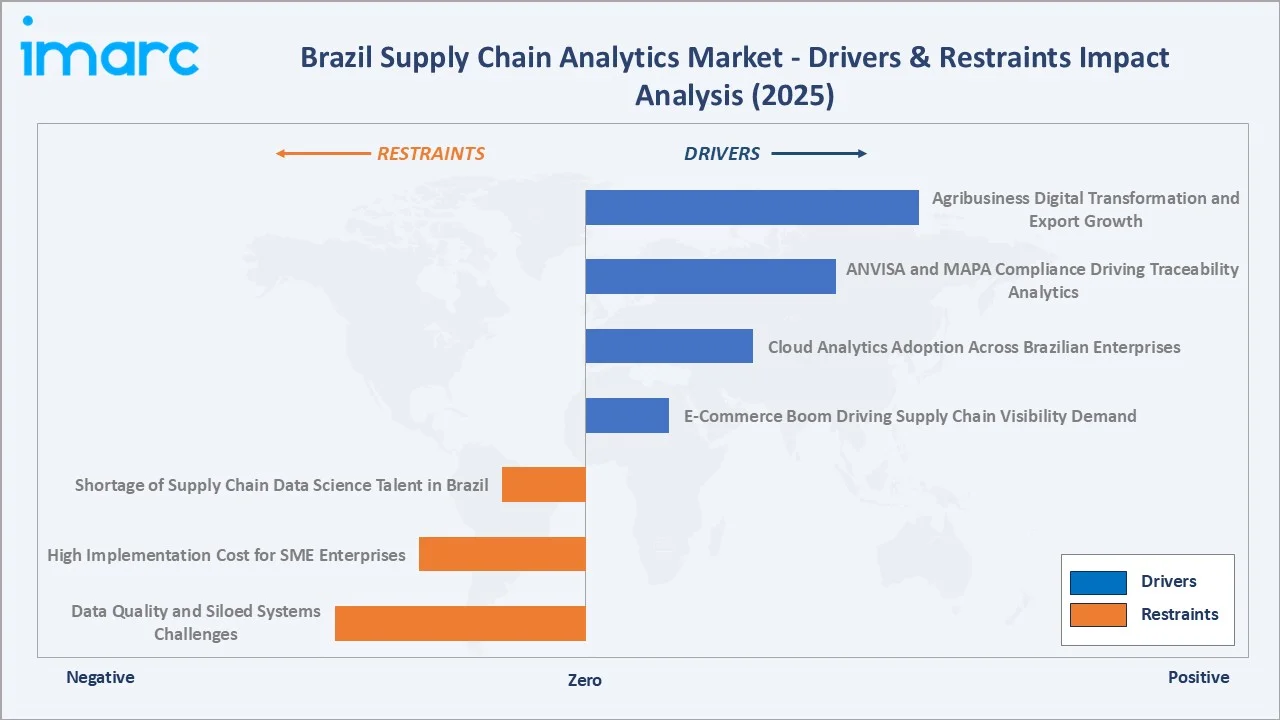

Market Drivers

- E-Commerce Boom Driving Supply Chain Visibility Demand: Brazil’s e-commerce growth is generating unprecedented supply chain complexity and data analytics requirements for both pure-play online retailers and traditional omnichannel retailers managing the integration of physical store and online fulfillment operations. E-commerce supply chains require sophisticated demand forecasting at the SKU and geography level and last-mile delivery analytics capabilities that are driving sustained investment in supply chain analytics platforms among Brazil’s rapidly growing digital commerce ecosystem.

- Cloud Analytics Adoption Across Brazilian Enterprises: The progressive migration of Brazilian enterprises to cloud-based ERP and supply chain management platforms is creating a structural demand expansion for cloud-native supply chain analytics capabilities. Moreover, cloud deployment eliminates the substantial on-premises infrastructure investment historically required for enterprise analytics platforms, enabling a broader range of Brazilian enterprises beyond the traditional large multinational base to justify supply chain analytics investment.

- ANVISA and MAPA Compliance Driving Traceability Analytics: Brazil’s regulatory frameworks for pharmaceutical supply chain traceability and food safety traceability are compelling pharmaceutical manufacturers, food producers, and their supply chain partners to invest in traceability analytics capabilities that can track product movement, validate compliance data, and respond to regulatory audit inquiries with comprehensive supply chain provenance documentation.

- Agribusiness Digital Transformation and Export Growth: Brazil’s position as the world’s largest exporter of soybeans, beef, sugar, and coffee is driving supply chain analytics adoption within the country’s vast agribusiness complex, where commodity price volatility, complex multi-tier supply chains spanning field production through export processing, and strict international food safety and phytosanitary compliance requirements are creating demand for sophisticated supply chain visibility, risk management, and compliance analytics capabilities.

Market Restraints

- Data Quality and Siloed Systems Challenges: Brazilian enterprises frequently operate heterogeneous IT landscapes combining multiple ERP instances, legacy warehouse management systems, transportation management platforms, and manual data collection processes that create data quality, consistency, and integration challenges that must be addressed before meaningful supply chain analytics value can be extracted.

- High Implementation Cost for SME Enterprises: Despite the democratizing effect of cloud-based SaaS analytics platforms, comprehensive supply chain analytics implementation, including data integration, user training, process redesign, and change management, remains a significant investment that constrains adoption among Brazil’s large population of small and medium enterprises with limited IT budgets and internal analytics expertise.

- Shortage of Supply Chain Data Science Talent in Brazil: The demand for professionals combining supply chain operational domain expertise with data science and analytics platform implementation skills significantly exceeds available talent supply in Brazil, creating implementation bottlenecks, elevated consulting costs, and dependency on international vendors for advanced analytics capabilities that constrain the speed of market adoption below its theoretical demand potential.

Market Opportunities

- AI and Generative AI Supply Chain Intelligence: The progressive integration of generative AI and large language model capabilities into supply chain analytics platforms is creating a new generation of natural language supply chain intelligence tools that enable non-technical supply chain practitioners to interrogate complex supply chain data through conversational interfaces, interpret analytics outputs without statistical expertise, and receive AI-generated scenario planning recommendations.

- Last-Mile and Urban Logistics Analytics: Brazil’s unique urban logistics challenges, including complex traffic environments in major cities, regulatory restrictions on freight vehicle circulation, and high last-mile delivery cost as a percentage of total logistics spend, are creating demand for specialized last-mile delivery analytics capabilities encompassing route optimization, delivery time prediction, returns management analytics, and urban distribution network design tools tailored to Brazilian logistics constraints.

Market Challenges

- Currency Volatility and USD-Denominated Software Pricing: International supply chain analytics software is predominantly priced in US dollars, creating real-price volatility for Brazilian enterprise buyers during periods of real depreciation that can disrupt multi-year software investment planning and increase total cost of ownership calculations relative to initial license estimates, sometimes causing procurement delays or scope reductions for planned analytics implementations.

- Change Management and User Adoption Barriers: Supply chain analytics implementations frequently deliver technical capabilities that exceed user adoption rates, as supply chain practitioners accustomed to intuition-based and spreadsheet-driven planning processes resist transitioning to data-driven platform workflows.

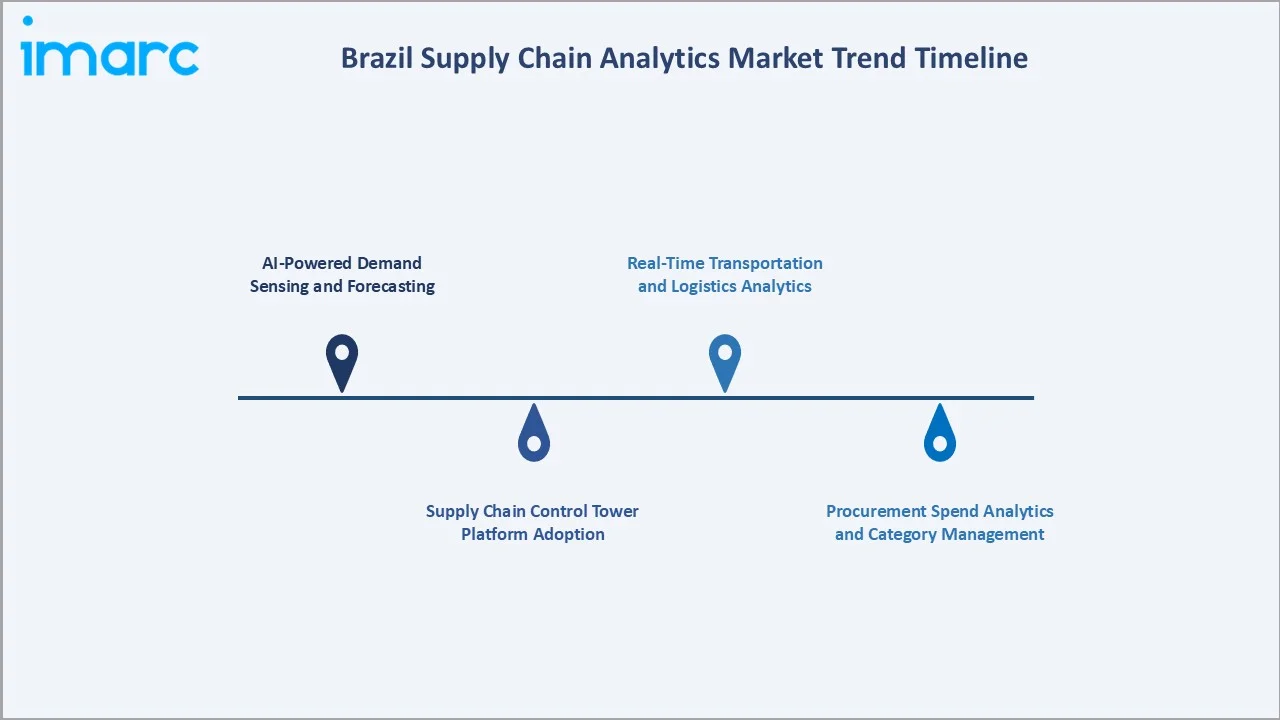

Emerging Market Trends

1. AI-Powered Demand Sensing and Forecasting

Brazilian enterprises are progressively adopting AI-driven demand sensing capabilities that use machine learning algorithms to incorporate near-real-time point-of-sale data, social media signals, weather data, and economic indicators into demand forecasting models that significantly outperform traditional statistical forecasting approaches. E-commerce platforms including Mercado Livre and Magazine Luiza are leading demand sensing technology adoption, using advanced forecasting to optimize dynamic inventory positioning across their fulfillment network operations.

2. Supply Chain Control Tower Platform Adoption

Supply chain control tower platforms, providing end-to-end supply chain visibility across supplier networks, manufacturing operations, distribution, and last-mile delivery through unified real-time dashboards and exception management capabilities, are gaining significant adoption momentum among Brazil’s larger manufacturing and retail enterprises. The COVID-19 pandemic supply disruptions demonstrated the critical importance of real-time supply chain visibility for rapid response to supply interruptions, accelerating control tower investment as organizations prioritize supply chain resilience alongside efficiency optimization.

3. Procurement Spend Analytics and Category Management

Procurement spend analytics and category management tools are experiencing strong adoption growth among Brazil’s large enterprises, driven by increasing CFO and CPO pressure to demonstrate procurement cost reduction and supplier consolidation value. Brazilian enterprises are investing in spend analysis platforms that can classify procurement expenditure by category and supplier, identify off-contract spending patterns, benchmark supplier pricing, and model procurement optimization scenarios.

4. Real-Time Transportation and Logistics Analytics

Real-time transportation and logistics analytics are becoming a priority investment area for Brazilian enterprises managing complex distribution networks across the country’s vast geographic extent, where transportation cost represents a disproportionately high share of total supply chain cost compared to more geographically compact markets. Fleet tracking integration, freight rate benchmarking, carrier performance analytics, and dynamic routing optimization capabilities are being actively deployed across Brazil’s major logistics operators and large enterprise shippers seeking to reduce transportation spend and improve on-time delivery performance across domestic distribution networks.

Industry Value Chain Analysis

Brazil’s supply chain analytics value chain spans enterprise data source systems through analytical insight delivery and decision support, with each stage involving specialized participants whose capabilities directly influence solution quality and enterprise analytics value realization.

|

Stage |

Key Players / Examples |

|

Data Source Providers |

ERP systems, warehouse management systems, transportation management platforms, and IoT and sensor networks |

|

Platform & Software Developers |

Supply chain analytics software vendors, AI and ML platform developers, and data visualization tool providers |

|

Cloud & Infrastructure |

Cloud infrastructure and data lake providers delivering compute, storage, and network resources |

|

System Integrators |

IT consulting firms, enterprise software implementation partners, and data integration specialists |

|

Channel Partners |

Value-added resellers, regional consulting firms, certified platform partners, and managed service providers |

|

Enterprise End Users |

Manufacturing, retail, food and beverages, pharmaceutical, logistics, and e-commerce companies |

Technology Landscape in the Brazil Supply Chain Analytics Industry

Demand Forecasting and Planning Analytics

Demand analysis and forecasting represent the highest-value and most broadly adopted supply chain analytics use case in Brazil, encompassing statistical time-series modeling, machine learning demand sensing, and AI-driven forecasting capabilities that improve inventory positioning and production planning accuracy. SAP Integrated Business Planning (IBP) and Oracle Supply Chain Management Cloud are leading enterprise demand planning platforms competing in Brazil’s market.

Supplier Performance and Procurement Analytics

Supplier performance analytics and procurement spend analysis tools are experiencing strong adoption growth among Brazil’s large enterprises, driven by CPO mandates to demonstrate procurement cost reduction and supplier consolidation value. SAP Ariba and Oracle Procurement Cloud provide comprehensive procure-to-pay analytics capabilities as extensions of their broader ERP ecosystems, while specialized procurement analytics vendors compete for enterprises seeking best-of-breed procurement intelligence.

Inventory and Network Optimization Analytics

Inventory analytics and supply chain network optimization tools are gaining adoption among Brazil’s larger manufacturers, distributors, and retailers seeking to reduce working capital tied up in excess inventory while maintaining target customer service levels. Given Brazil’s geographic complexity, high interest rates, and significant distribution infrastructure variation across regions, supply chain network optimization analytics that can model inventory positioning, warehouse location, and distribution routing trade-offs across the country’s diverse regional characteristics deliver substantial financial value for enterprises managing national distribution networks.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Software |

67.4% |

2025 |

|

Enterprise Size |

Large Enterprises |

71.5% |

2025 |

|

Industrial Vertical |

🔒 |

🔒 |

2025 |

|

Deployment Mode |

🔒 |

🔒 |

2025 |

|

Region |

Southeast |

42.7% |

2025 |

By Component

Software dominates with a 67.4% share in 2025. This segment encompasses the full spectrum of supply chain analytics software applications, including demand analysis and forecasting platforms, supplier performance analytics tools, and transportation and logistics analytics platforms. Supply chain analytics software’s dominant component share reflects the market’s maturation beyond data collection and basic reporting toward integrated analytics environments that combine multiple data sources and apply advanced modeling to generate actionable supply chain intelligence.

To access detailed market analysis, Request Sample

Services at 32.6% encompass professional services including consulting, implementation, customization, and managed analytics services, alongside support and maintenance services that sustain deployed analytics platform operations. The services component reflects the implementation complexity of enterprise supply chain analytics deployments, which typically require significant data integration, process redesign, and change management investment beyond software licensing to deliver realized analytics value.

By Enterprise Size

Large enterprises lead with a 71.5% share in 2025, encompassing Brazil’s multinational corporate subsidiaries, major domestic conglomerates, and large public and private sector organizations. Large enterprise supply chain analytics programs typically span multiple functional analytics modules, integrate with complex multi-system ERP landscapes, and require substantial professional services investment for implementation.

Small and medium-sized enterprises at 28.5% share (2025) represent the fastest-growing segment at approximately 16.4% CAGR, driven by cloud-based SaaS supply chain analytics platforms that have dramatically reduced implementation barriers and subscription pricing that aligns software cost with business scale.

Regional Market Insights

Southeast regional leadership (42.7%, 2025) reflects São Paulo’s position as the uncontested center of Brazil’s supply chain analytics ecosystem. São Paulo state hosts the headquarters of the country’s most analytically sophisticated supply chain organizations, the largest concentration of certified SAP, Oracle, and IBM implementation partners, and the deepest pool of supply chain analytics and data science talent in Latin America.

South at 21.4% share (2025) represents the country’s second-largest supply chain analytics market, with Paraná and Rio Grande do Sul states hosting Brazil’s most advanced agro-industrial processing operations in grain, meat, dairy, and wine production that are progressively adopting supply chain analytics for commodity procurement, cold chain management, and export logistics optimization.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Southeast |

42.7% |

São Paulo’s multinational headquarters concentration; deepest implementation partner ecosystem; e-commerce and retail analytics leadership |

|

South |

21.4% |

Agro-industrial and food processing supply chain analytics in Paraná and Rio Grande do Sul; growing automotive parts manufacturing analytics |

|

Northeast |

15.8% |

Petrochemical and textile supply chain analytics; expanding e-commerce logistics analytics in Fortaleza and Recife; growing retail distribution analytics investment |

|

Central-West |

11.2% |

Agribusiness supply chain analytics for grain, soy, and meat processing; commodity logistics and export analytics; cold chain management analytics for agricultural commodities |

|

North |

8.9% |

Manaus free trade zone manufacturing analytics; Amazon logistics and distribution analytics; growing regional e-commerce penetration driving fulfillment analytics investment |

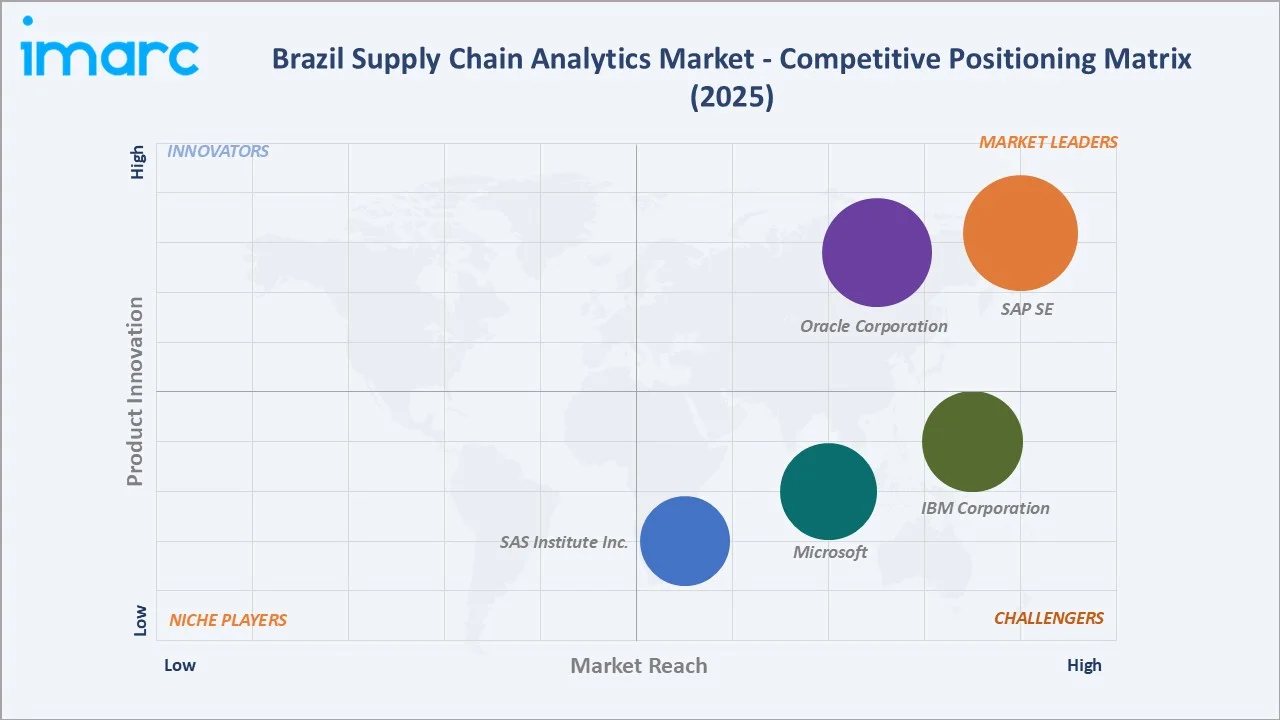

Competitive Landscape

Brazil’s supply chain analytics market features a competitive landscape dominated by global enterprise software companies that leverage their established ERP and enterprise application customer relationships to cross-sell analytics capabilities.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

SAP SE |

SAP Integrated Business Planning, SAP Ariba, SAP Analytics Cloud |

Market Leader |

One of Brazil's largest ERP installed bases providing natural SCA cross-sell; IBP demand planning leadership |

|

Oracle Corporation |

Oracle Supply Chain & Manufacturing, Oracle Demand Management Cloud |

Market Leader |

Integrated cloud SCM and analytics platform; strong manufacturing and retail vertical depth; leading AI demand sensing capabilities |

|

IBM Corporation |

IBM Sterling, IBM Planning Analytics |

Strong Challenger |

Sterling supply chain visibility platform; IBM Consulting implementation strength; AI-embedded supply chain intelligence |

|

Microsoft |

Dynamics 365 Supply Chain Management, Power BI |

Strong Challenger |

Power BI analytics democratization; Dynamics SCM integration; growing SME supply chain analytics footprint |

|

SAS Institute Inc. |

SAS Supply Chain Intelligence |

Challenger |

Demand sensing and forecasting sophistication; strong financial and government sector analytics relationships |

Global software vendors compete primarily through ERP integration depth and the ability to extend their core application customer relationships into supply chain analytics adjacent solutions. Microsoft Power BI’s broad adoption as an enterprise visualization tool is creating a competitive analytics democratization dynamic that is extending supply chain data insights to a wider range of users within enterprise organizations.

Key Company Profiles

SAP SE

SAP SE positions itself as Brazil’s largest ERP provider, with multiple Brazilian enterprise customers across manufacturing, retail, and services sectors, and provides a structural cross-sell advantage for supply chain analytics solutions that extend the analytical capabilities of existing SAP ERP investments.

- Product Portfolio: SAP Integrated Business Planning (demand sensing, inventory optimization, supply planning), SAP Ariba (procurement analytics and spend management), and SAP Analytics Cloud (enterprise BI and planning).

- Recent Developments: In October 2025, SAP SE launched AI-driven supply chain updates, including SAP Supply Chain Orchestration, designed to detect disruptions early and trigger intelligent actions. It also introduced new Joule Agents, SAP IBP enhancements, SAP Business Network upgrades, and SAP Logistics Management to improve planning, automation, and warehouse operations.

- Strategic Focus: Generative AI embedding across IBP and Analytics Cloud; RISE with SAP migration driving ERP and analytics cloud convergence; SAP Ariba procurement analytics expansion; Brazilian partner ecosystem certification for supply chain analytics specialization.

Oracle Corporation

Oracle Corporation holds a strong position in Brazil’s supply chain analytics market through its Oracle Supply Chain Management Cloud platform, which integrates inventory, procurement, order management, and logistics functionality with embedded analytics capabilities.

- Product Portfolio: Oracle Supply Chain & Manufacturing (integrated supply chain planning and execution analytics), Oracle Demand Management Cloud (demand sensing and forecasting), Oracle Fusion Analytics for Supply Chain (pre-built analytics for supply chain KPIs).

- Recent Developments: In June 2026, Oracle Corporation introduced new AI-powered agentic applications and inventory optimization capabilities within Oracle Fusion Cloud SCM to help enterprises automate planning, procurement, and manufacturing while improving supply chain resilience. The new tools leverage AI agents to optimize inventory, reduce operational risk, enhance decision-making, and strengthen end-to-end supply chain efficiency amid ongoing global disruptions.

- Strategic Focus: Integrated cloud application and analytics convergence; AI-embedded supply chain risk and disruption analytics; Fusion Analytics pre-built content for faster supply chain analytics time-to-value; Brazilian manufacturing and retail vertical expansion.

Market Concentration Analysis

Brazil’s supply chain analytics market exhibits moderate concentration, with global software leaders collectively holding the majority of large enterprise revenue through established ERP customer relationships and comprehensive analytics portfolio breadth. The market’s competitive structure is progressively becoming more dynamic as specialized supply chain analytics vendors and cloud-native platforms challenge the established ERP-centric analytics ecosystem, particularly in high-growth use cases including AI demand sensing, supply chain control tower visibility, and last-mile delivery analytics.

Microsoft Power BI’s broad adoption as a low-cost enterprise visualization tool is creating a structural competitive dynamic that democratizes basic supply chain analytics access while simultaneously expanding the market opportunity for more sophisticated analytics platforms that can serve as the data foundation for Power BI supply chain dashboards.

Investment & Growth Opportunities

Fastest Growing Segments

SME enterprise size (~16.4% CAGR) and software component (~15.8% CAGR) represent the highest-growth investment vectors through 2034. SME growth is driven by cloud SaaS platform accessibility, while software growth reflects the progressive deepening of analytics capabilities from basic reporting toward AI-powered predictive and prescriptive supply chain intelligence that commands higher platform pricing and generates greater switching costs.

Emerging Market Expansion

Central-West (11.2%) and North (8.9%) regions, representing Brazil’s agribusiness heartland and Amazon industrial zone respectively, offer significant underpenetrated growth potential as agribusiness supply chain digitalization, commodity export analytics, and expanding e-commerce distribution analytics drive supply chain technology investment beyond the Southeast and South’s established enterprise analytics ecosystems.

Venture and Institutional Investment Trends

- Growing venture capital investment in Brazilian supply chain technology startups developing AI-native demand forecasting, supplier risk monitoring, and last-mile delivery optimization tools is creating a domestic innovation ecosystem that complements global platform vendors with Brazilian market-specific supply chain intelligence capabilities.

- Brazilian government procurement modernization programs, including digitalization of public sector supply chain and procurement operations, represent an emerging institutional buyer segment for supply chain analytics platforms, with federal and state government entities progressively investing in procurement analytics to improve public expenditure efficiency and transparency.

Future Market Outlook (2026-2034)

Brazil’s supply chain analytics market is positioned for sustained, strong growth through 2034. From a base of USD 236.7 Million in 2025, the market is projected to reach USD 885.0 Million by 2034, representing total incremental value creation of USD 648.3 Million at a CAGR of 15.31%.

This growth reflects the compound effect of e-commerce complexity driving analytics demand, SME cloud adoption broadening the addressable buyer base, AI capabilities enhancing analytics platform value, and progressive penetration of supply chain analytics across Brazil’s diverse industrial verticals.

The market’s composition is expected to evolve meaningfully through 2034, with SMEs progressively increasing their share of total revenue from 28.5% toward approximately 35–38% as cloud SaaS platforms continue democratizing access. The software component’s leadership position is expected to strengthen further as AI and generative AI capabilities embedded within analytics platforms command premium pricing and accelerate platform differentiation from services-oriented analytics approaches.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 70 industry participants in 2024–2025, including supply chain analytics software vendor executives, systems integrators, supply chain and procurement directors at large Brazilian enterprises, industry association representatives, and technology analysts specializing in Brazil’s enterprise software market.

Secondary Research

Secondary research encompassed vendor annual reports, Brazilian enterprise software association publications, supply chain professional organization data, regulatory publications from ANVISA and MAPA, e-commerce market reports, and industry publications covering Brazil’s logistics, manufacturing, and retail technology sectors.

Forecasting Models

Market size estimations were derived from top-down and bottom-up forecasting incorporating enterprise software spending trends, supply chain analytics adoption penetration by enterprise size, cloud migration impact on addressable market expansion, and vendor revenue intelligence. A base-case CAGR of 15.31% reflects consensus estimates validated against enterprise software growth trends and IMARC market tracking from 2020 to 2025.

Brazil Supply Chain Analytics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Deployment Modes Covered | On-premises, Cloud-based |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium Enterprises |

| Industry Verticals Covered | Automotive, Food and Beverages, Healthcare and Pharmaceuticals, Manufacturing, Retail and Consumer Goods, Transportation and Logistics, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | SAP SE, Oracle Corporation, IBM Corporation, Microsoft, SAS Institute Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil supply chain analytics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil supply chain analytics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil supply chain analytics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Supply Chain Analytics Market Report

The Brazil supply chain analytics market reached USD 236.7 Million in 2025 and is projected to reach USD 885.0 Million by 2034, growing at a CAGR of 15.31% during 2026-2034.

Software leads with a 67.4% market share in 2025, reflecting supply chain analytics’ software-centric market structure where platform capabilities for demand forecasting, inventory optimization, supplier analytics, and logistics intelligence represent the primary value creation and commercial opportunity layer.

Large enterprises lead with a 71.5% market share in 2025, reflecting their higher analytical maturity, larger data volumes generating greater analytics value, and financial capacity to invest in comprehensive enterprise supply chain analytics platform implementations that typically span multiple functional modules.

Southeast Brazil leads with a 42.7% share in 2025, anchored by São Paulo’s position as Latin America’s largest business and logistics hub, hosting the country’s most analytically sophisticated supply chain organizations and the deepest concentration of certified supply chain analytics implementation talent.

Some of the leading companies include SAP SE, Oracle Corporation, IBM Corporation, Microsoft, and SAS Institute Inc. Global enterprise software vendors leverage established ERP customer relationships to cross-sell analytics capabilities, competing primarily on platform depth, AI capabilities, and local implementation ecosystem strength.

SMEs are growing fastest at approximately 16.4% CAGR as cloud-based SaaS supply chain analytics platforms have reduced implementation complexity and subscription pricing aligns software cost with SME scale.

AI is creating a new generation of supply chain intelligence capabilities, including generative AI conversational analytics, machine learning demand sensing, AI-driven supplier risk monitoring, and autonomous supply chain planning.

Key challenges include data quality and siloed systems creating implementation complexity, a supply chain data science talent shortage slowing implementation velocity, and change management barriers to realizing analytics adoption value within supply chain operations teams.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)