Brazil Third-Party Logistics Market Size, Share, Trends and Forecast by Transport, Service Type, End Use, and Region, 2026-2034

Brazil Third-Party Logistics Market Size, Share, Trends & Forecast (2026-2034)

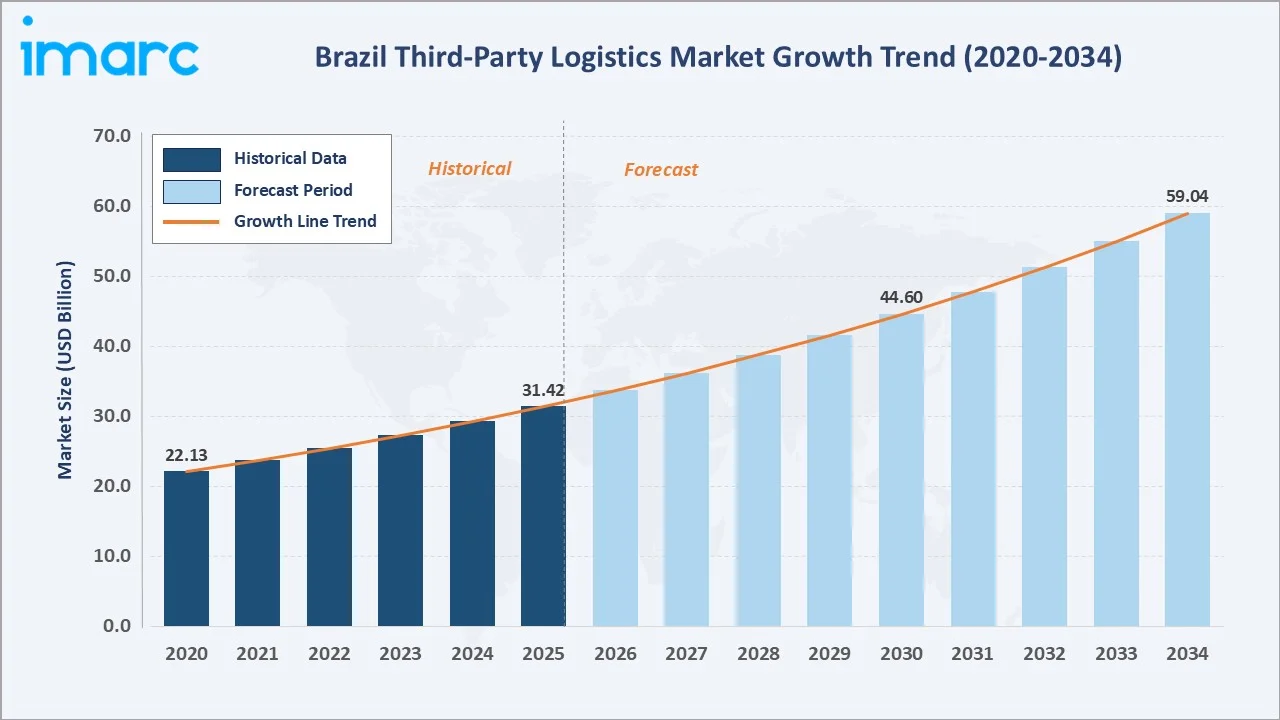

The Brazil third-party logistics (3PL) market reached USD 31.42 Billion in 2025 and is projected to reach USD 59.04 Billion by 2034, exhibiting a CAGR of 7.26% during 2026-2034. Growth is driven by robust e-commerce expansion, manufacturing sector recovery, and sustained government investment in transportation infrastructure.

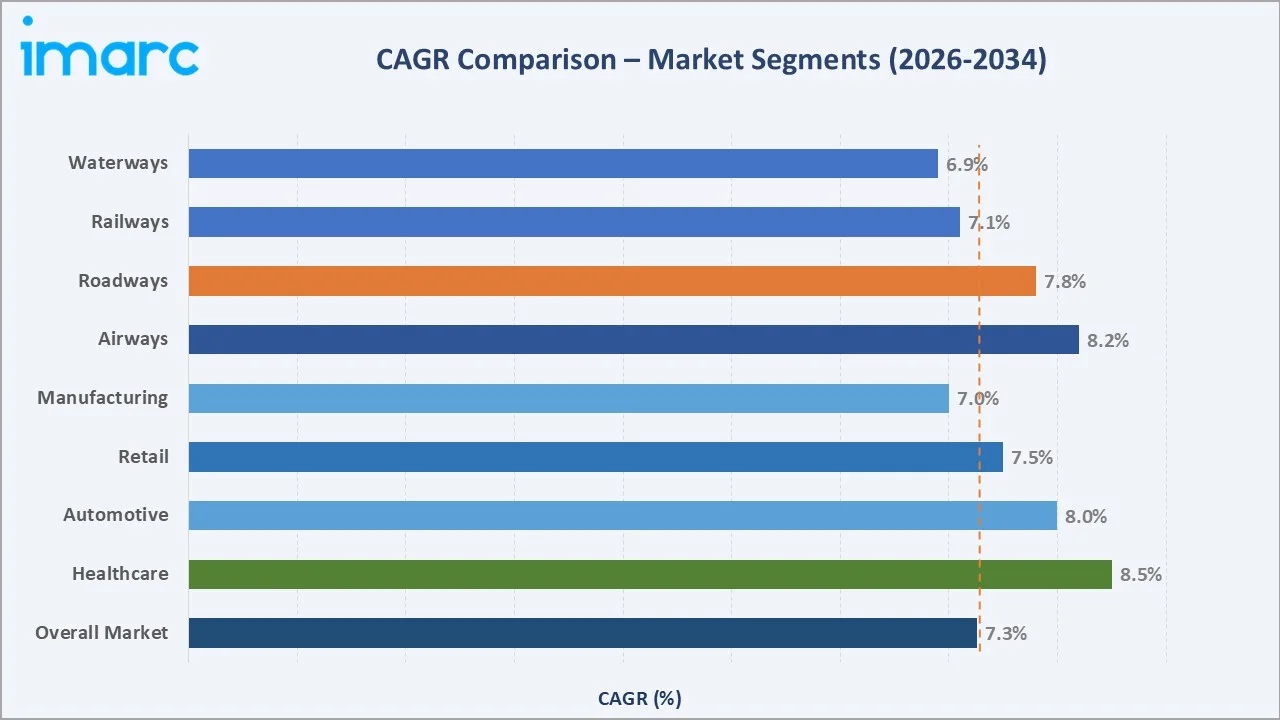

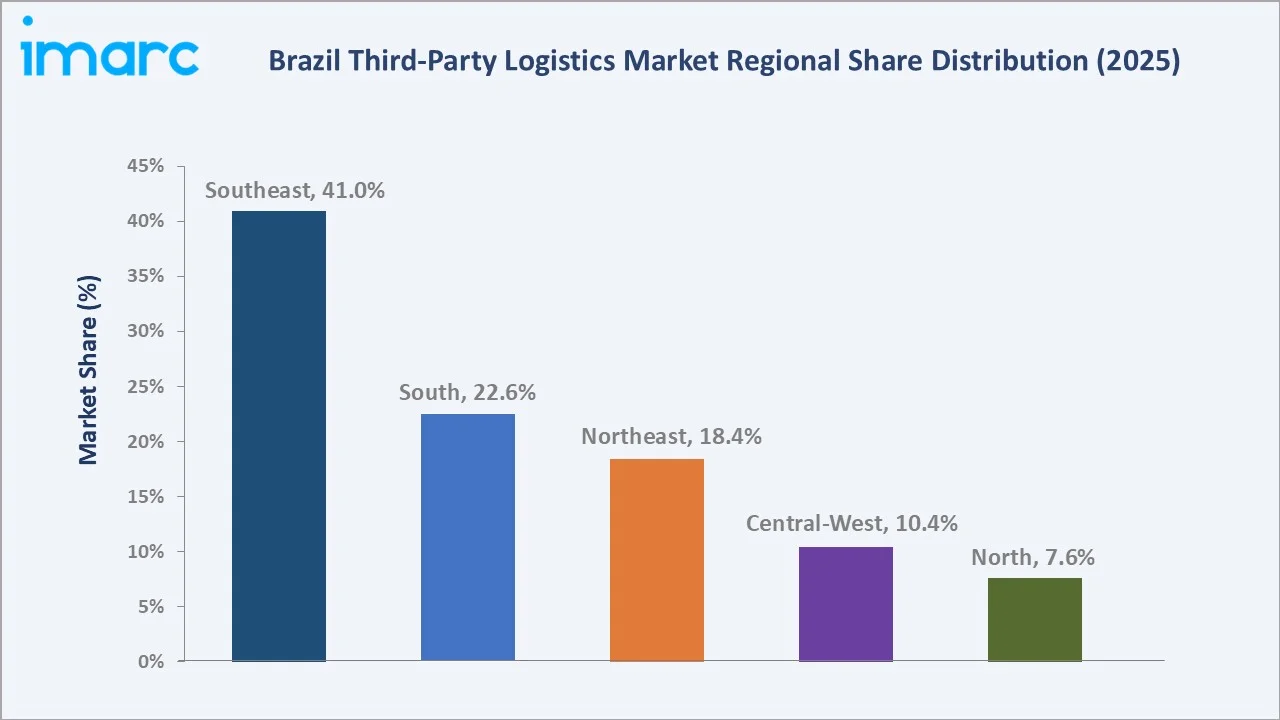

Southeast Brazil dominates with a 41.0% share in 2025, anchored by São Paulo and Rio de Janeiro industrial clusters. Roadways lead transport at 59.0%, while Manufacturing is the largest end-use sector at 25.0%. The market is projected to reach approximately USD 44.60 Billion by 2030.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 31.42 Billion |

|

Forecast Market Size (2034) |

USD 59.04 Billion |

|

CAGR (2026-2034) |

7.26% |

|

Largest Region |

Southeast (41.0%, 2025) |

|

Largest Transport |

Roadways (59.0%, 2026-2034) |

|

Leading End Use |

Manufacturing (25.0%, 2026-2034) |

|

Fastest Growing End Use |

Healthcare (8.5% CAGR) |

To get more information on this market, Request Sample

The market grew from approximately USD 22.13 Billion in 2020 to USD 31.42 Billion in 2025, reflecting resilience through economic disruptions. Digital transformation through AI-driven route optimization and warehouse automation is reshaping provider capabilities and accelerating market modernization.

The 7.26% CAGR through 2034 positions Brazil’s third-party logistics sector among Latin America’s fastest-growing logistics markets. Rising urbanization (87% urban population in 2024), e-commerce penetration, and agricultural export demand create self-reinforcing growth dynamics sustaining above-average category expansion.

Executive Summary

Brazil’s third-party logistics market stood at USD 31.42 Billion in 2025, propelled by accelerating e-commerce adoption, manufacturing expansion, and government infrastructure investment. The market is projected to reach USD 59.04 Billion by 2034 at a CAGR of 7.26%.

The Southeast region commands 41.0% revenue share (2025), anchored by São Paulo’s industrial base and the Santos port complex. By transport, Roadways lead at 59.0% (2025), leveraging Brazil’s 2 million km federal road network.

Key growth trends include e-commerce fulfillment network expansion, sustainability-focused green logistics initiatives, and multimodal transportation corridor development. Digital transformation through AI, IoT, and warehouse automation is fundamentally reshaping provider capabilities and competitive dynamics across Brazil’s logistics ecosystem.

Key Market Insights

|

Insight |

Data |

|

Largest Transport |

Roadways – 59.0% (2025) |

|

Largest End Use Segment |

Manufacturing – 25.0% (2025) |

|

Leading Region |

Southeast – 41.0% (2025) |

|

Fastest Growing End Use |

Healthcare |

|

Top Companies |

DHL Supply Chain, A.P. Moller – Maersk, JSL S.A., CEVA Logistics, BBM Logística |

|

Key Opportunity |

E-commerce fulfillment & cold chain |

Key Analytical Observations Supporting the Above Data:

- Roadways’ 59.0% share (2025) reflects Brazil’s 2 million km highway network, providing unmatched geographic flexibility for door-to-door deliveries across diverse industrial and agricultural supply chains.

- Manufacturing’s 25.0% lead (2025) is driven by automotive component sequencing, electronics distribution, and food processing logistics, as manufacturers outsource to focus on core production competencies.

- Southeast’s 41.0% share reflects industrial concentration in São Paulo and Rio de Janeiro, superior port connectivity through Santos, and higher economic activity supporting robust logistics infrastructure investment.

Brazil Third-Party Logistics Market Overview

Third-party logistics (3PL) refers to the outsourcing of logistics and supply chain management functions to specialized external service providers. In Brazil, third-party logistics encompasses transportation management, warehousing and distribution, dedicated contract carriage, value-added logistics services, and integrated supply chain solutions.

Brazil’s vast territory, complex geography, and diverse economic base create unique logistics challenges. The country’s position as Latin America’s largest economy, combined with its role as a global agricultural exporter and growing manufacturing hub, drives sustained demand for sophisticated logistics outsourcing.

Market Dynamics

To evaluate market opportunities, Request Sample

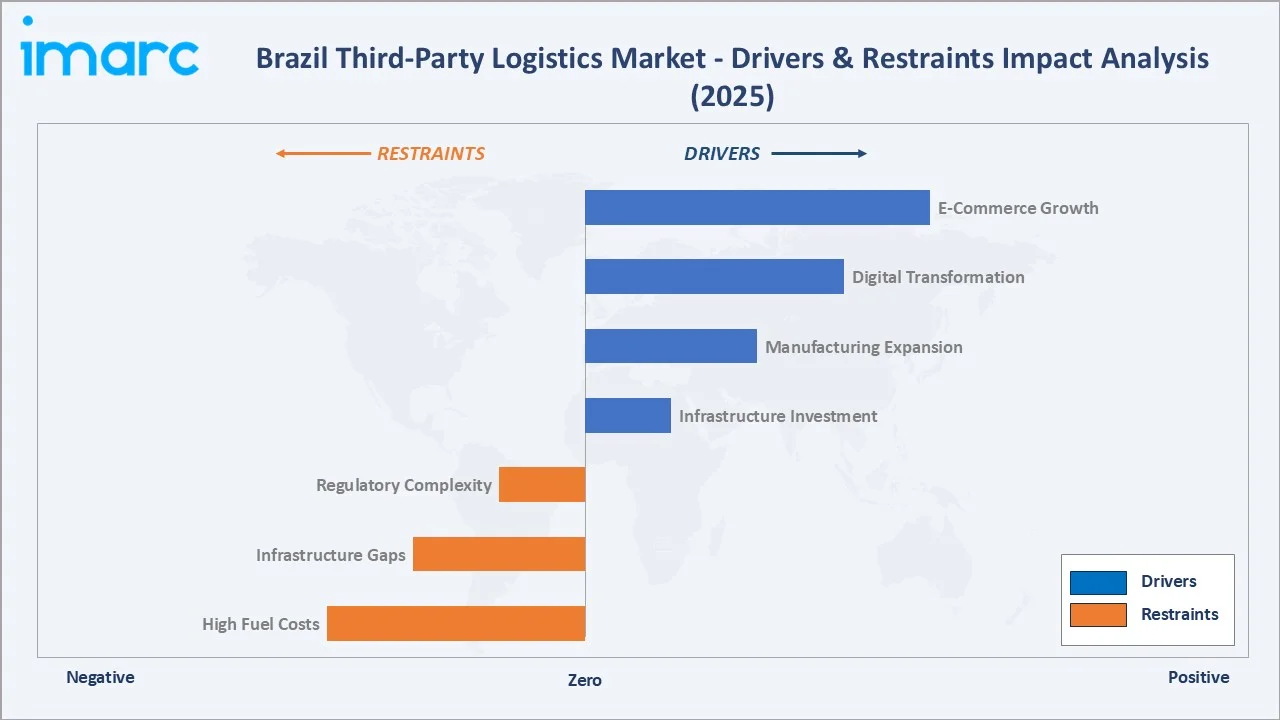

Market Drivers

- E-Commerce Growth and Fulfillment Demand: Brazil’s online retail grew 18.7% in H1 2024, reaching BRL 160.3 billion, creating intensive demand for last-mile delivery networks, urban fulfillment centers, and omnichannel logistics capabilities. Mercado Libre announced 11 additional distribution centers in Brazil by end of 2025.

- Government Infrastructure Investment: The federal government announced USD 12 Billion in February 2025 for grain harvest logistics infrastructure covering roads, railways, and ports. Brazil’s National Logistics Plan targets comprehensive transportation network improvements enabling faster, reliable goods movement.

- Manufacturing Sector Expansion: Brazil’s vehicle sales reached 2.6 million units in 2024, generating substantial demand for sequenced component delivery and finished vehicle logistics. Industrial growth across automotive, electronics, and food processing requires efficient inbound and outbound logistics.

- Digital Transformation via AI and IoT: Providers implementing AI-driven route optimization, real-time IoT tracking, and automated warehouse systems enhance operational efficiency.

Market Restraints

- Infrastructure Deficiencies and Regional Disparities: Inadequate Road conditions in North and Northeast regions increase vehicle maintenance costs and extend delivery times. Port congestion at Santos causes shipment delays, while limited rail development restricts multimodal transportation options.

- Complex Regulatory and Tax Environment: Brazil’s multi-state ICMS tax regimes and new Complementary Law 214/2025 implementing dual IBS-CBS consumption tax from January 2026 compel third-party logistics providers to overhaul tax-planning operations, increasing compliance costs significantly.

- High Fuel and Operational Costs: Fuel price volatility and high diesel costs directly impact road transport economics, compressing margins for third-party logistics providers reliant on trucking fleets for domestic cargo movement across Brazil’s vast territory.

Market Opportunities

- Healthcare and Pharmaceutical Logistics: Rising pharmaceutical production, medical device distribution, and cold chain demand create high-value specialty logistics opportunities for providers developing GMP-compliant warehousing and temperature-controlled transport capabilities across Brazil.

- Agricultural Export Logistics Integration: Brazil’s position as a leading agricultural exporter creates sustained demand for integrated bulk cargo, cold chain, and port logistics connecting interior agricultural regions to Santos, Paranáguá, and Itacoatiara export terminals.

- Green Logistics and Sustainability Services: Growing corporate sustainability requirements and environmental regulations create differentiation opportunities for providers investing in fleet electrification, renewable energy warehousing, and carbon tracking systems.

Market Challenges

- Last-Mile Complexity in Urban Areas: Brazil’s densely populated urban centers face significant last-mile challenges including traffic congestion, security concerns, and inadequate addressing systems, particularly in informal settlements surrounding major metropolitan areas.

- Talent Acquisition and Driver Shortage: Skilled logistics personnel shortages, including licensed truck drivers and warehouse management professionals, constrain provider capacity expansion and increase labor costs across Brazil’s competitive logistics market.

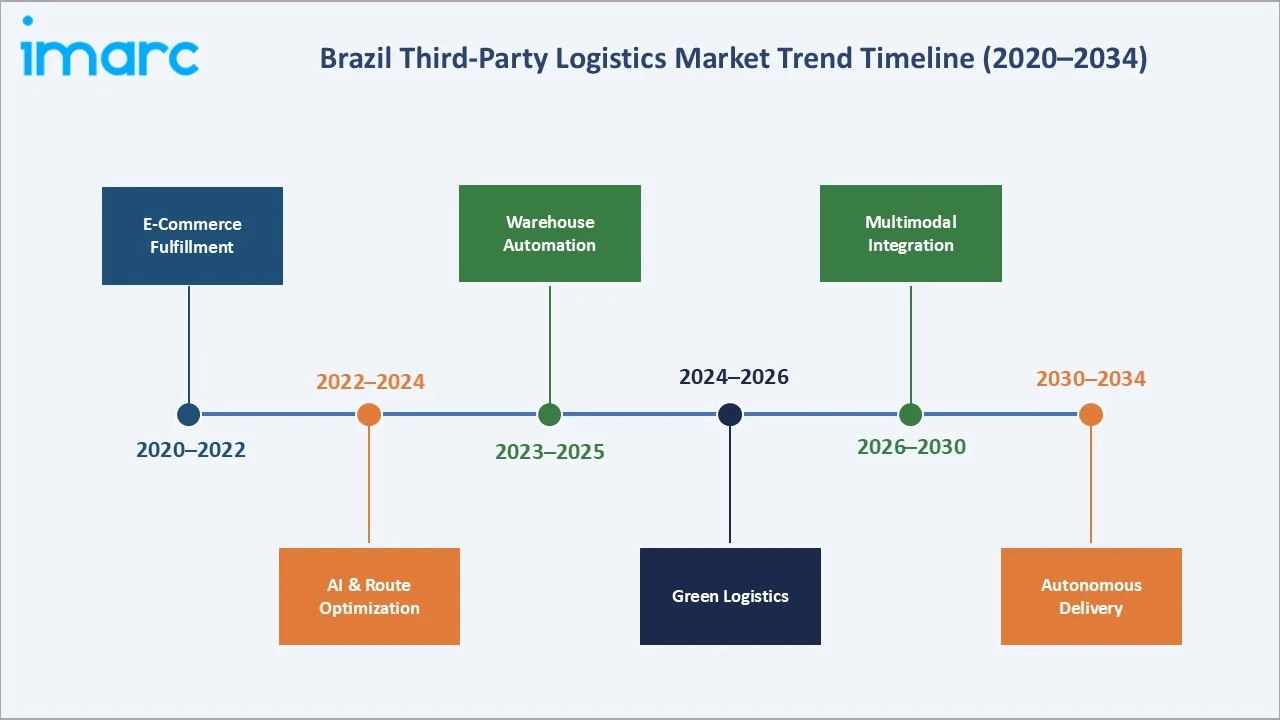

Emerging Market Trends

Brazil’s third-party logistics market is being reshaped by five converging trends redefining service delivery, technology adoption, and competitive dynamics across all regions through 2034.

1. E-Commerce Fulfillment Network Expansion

Third-party Logistics providers are establishing micro-fulfillment centers and dark stores in urban areas to support same-day and next-day delivery. Strategic warehouse positioning near population centers reduces last-mile distances. Omnichannel retail strategies are driving integrated fulfillment solutions managing inventory across physical and digital channels simultaneously.

2. Warehouse Automation and Robotics Adoption

Automated storage and retrieval systems (AS/RS), conveyor automation, and robotics are transforming warehouse operations. Labor cost pressures and throughput demand accelerate technology investment, particularly for high-velocity e-commerce fulfillment operations requiring rapid order processing and accurate inventory management capabilities.

3. Green Logistics and Sustainability Initiatives

Fleet electrification programs, sustainable packaging solutions, and renewable energy warehouse operations are becoming competitive differentiators. Providers implementing carbon tracking and reverse logistics capabilities for recycling attract sustainability-focused clients requiring verified emissions reduction commitments across supply chains.

Industry Value Chain Analysis

Brazil’s third-party logistics value chain encompasses interconnected stages from shipper engagement through end-consumer delivery. Specialized expertise at each stage is required to deliver reliable, cost-effective logistics services across Brazil’s complex geographic and regulatory environment.

|

Stage |

Key Activities |

Representative Players |

|

Shippers & Manufacturers |

Cargo preparation, documentation, compliance |

Industrial firms, agribusiness exporters |

|

Third-party Logistics Provider Selection |

RFQ, contract negotiation, SLA definition |

Procurement & supply chain teams |

|

Transportation Management |

Route optimization, carrier management, tracking |

DHL Supply Chain, JSL S.A. |

|

Warehousing & Distribution |

Inventory management, order fulfillment, cross-docking |

CEVA Logistics, FM Logistic, BBM Logística |

|

Last-Mile Delivery |

Urban distribution, delivery management, returns |

Sequoia Logística |

|

End Consumers |

Retail, B2B, institutional delivery receipt |

Manufacturers, retailers, healthcare institutions |

Transportation management is the primary value creation stage, where route optimization expertise, carrier relationships, and technology platforms generate the greatest competitive differentiation. Leading providers invest in proprietary TMS platforms and AI-driven tools to deliver measurable cost savings over self-managed logistics operations.

Technology Landscape in the Third-party Logistics Industry

AI and Route Optimization

AI-powered route optimization algorithms reduce transportation costs and improve delivery times for Brazil’s leading third-party logistics providers. Machine learning models incorporating real-time traffic, weather, and demand data enable dynamic routing decisions delivering 10–18% fuel efficiency improvements over traditional static planning approaches.

Warehouse Management Systems

Cloud-based warehouse management systems enable real-time inventory visibility, automated pick-and-pack workflows, and seamless e-commerce platform integration. Leading providers implement voice-directed picking, RFID tracking, and automated conveyor systems to increase throughput while reducing labor requirements in high-volume fulfillment operations.

Real-Time Tracking and IoT Integration

IoT-enabled asset tracking platforms provide end-to-end cargo visibility from origin to destination. Temperature monitoring for cold chain shipments, geofencing alerts, and predictive fleet maintenance analytics are becoming standard capabilities expected by major corporate logistics clients across Brazil.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Transport |

Roadways |

59.0% |

2025 |

|

Service |

Domestic Transportation Management |

52.0% |

2025 |

|

End Use |

Manufacturing |

25.0% |

2025 |

|

Region |

Southeast |

41.0% |

2025 |

By Transport

To access detailed market analysis, Request Sample

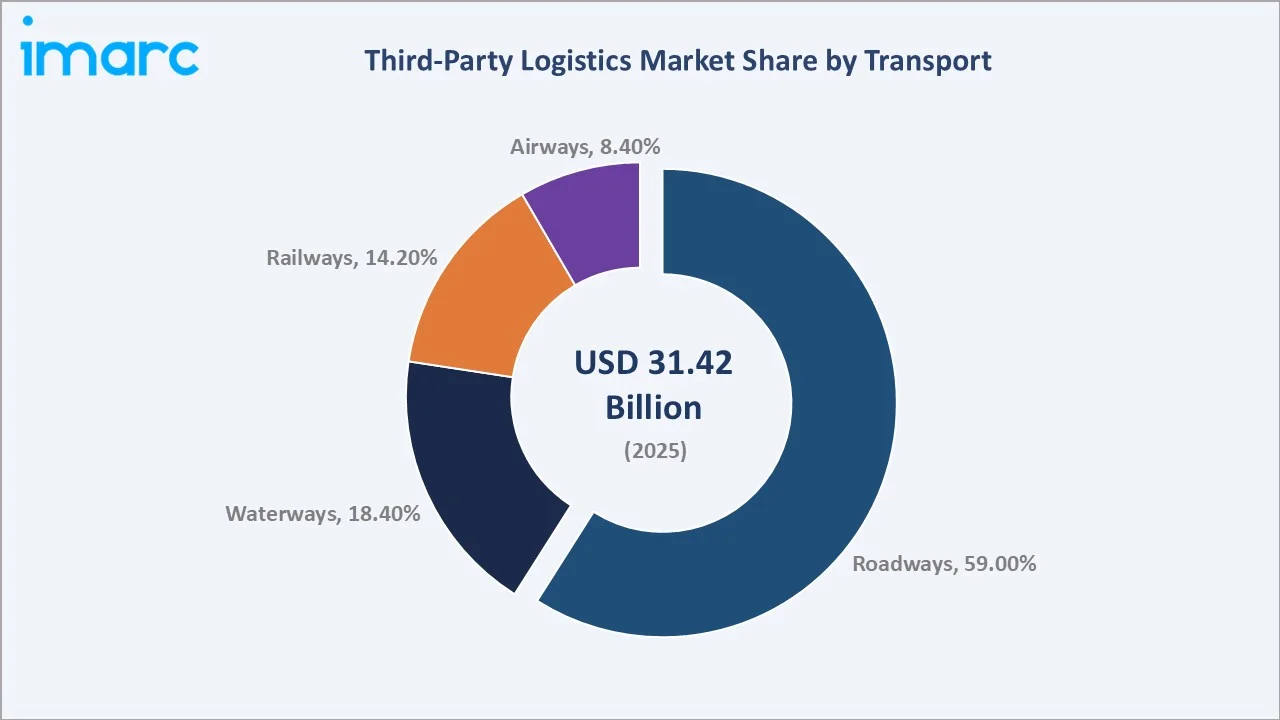

Roadways dominate with 59.0% share (2025), leveraging Brazil’s 2 million km federal highway network. Waterways hold 18.4% for bulk agricultural and industrial cargo. Railways (14.2%) serve mining and agricultural bulk corridors, while Airways (8.4%) support high-value express and pharmaceutical shipments.

Road freight handles most of the Brazil’s ton-mile cargo nationally, reflecting unparalleled flexibility for door-to-door deliveries. The flexibility of trucking allows logistics providers to customize routes, manage variable shipment sizes, and respond quickly to demand fluctuations across Brazil’s diverse industrial and agricultural supply chains.

By End Use

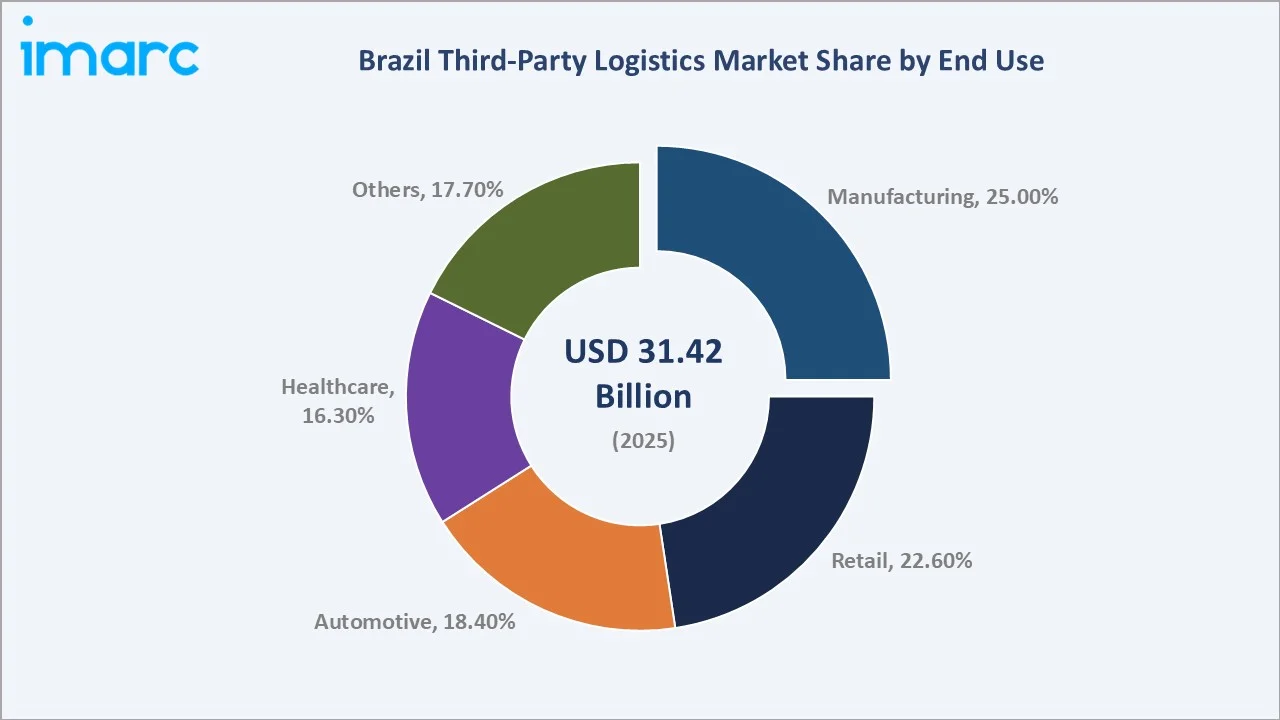

Manufacturing leads at 25.0% (2025), driven by automotive, electronics, and food processing logistics. Retail (22.6%) is second, propelled by e-commerce fulfillment growth. Automotive (18.4%) requires precise component sequencing logistics. Healthcare (16.3%) drives cold chain demand. Others account for 17.7%.

Manufacturing’s 25.0% dominance reflects Brazil’s expanding industrial base. Manufacturers outsource logistics to concentrate on core production competencies while leveraging specialized 3PL expertise in automotive sequencing, just-in-time delivery, and multi-modal supply chain coordination across national production networks.

Regional Market Insights

Brazil’s third-party logistics market exhibits distinct regional dynamics shaped by industrial concentration, infrastructure quality, geographic challenges, and economic development levels across five major regions with differing logistics maturity profiles.

Southeast Brazil (41.0%) is underpinned by São Paulo’s role as Latin America’s largest industrial hub. South (22.6%) reflects strong automotive manufacturing and agribusiness logistics demand anchored in Paraná and Santa Catarina states, supported by Paranáguá Port operations.

Competitive Landscape

Brazil’s third-party logistics competitive landscape combines large international providers with established domestic players. Leading providers invest in warehouse automation, digital platforms, and nationwide distribution networks. Strategic acquisitions and service portfolio expansion accelerate market consolidation across diverse industry verticals.

|

Company |

Market Position |

Primary Strategy |

|

DHL Supply Chain |

Global Leader |

Digital logistics, automation, sustainability |

|

A.P. Moller – Maersk |

Global Leader |

End-to-end integrated logistics solutions |

|

JSL S.A. |

National Leader |

Dedicated contract carriage, fleet expansion |

|

CEVA Logistics |

International Leader |

Contract logistics, air & ocean freight |

|

BBM Logística SA |

Established Player |

Industrial logistics, cold chain services |

|

Scan Global Logistics |

Challenger |

Airfreight, seafreight, customs clearance |

|

FM Logistic |

International Player |

Warehousing automation, e-commerce fulfillment |

|

Patrus Transportes |

Regional Leader |

Express road freight, B2B distribution |

|

Sequoia Logística |

Challenger |

Last-mile delivery, e-commerce logistics |

|

Tegma Gestão Logística S.A. |

Specialist Leader |

Automotive logistics specialization |

The companies covered in the report include DHL Supply Chain, A.P. Moller – Maersk, JSL S.A., CEVA Logistics, BBM Logística SA, Scan Global Logistics, FM Logistic, Patrus Transportes, Sequoia Logística, and Tegma Gestão Logística S.A.

Key Company Profiles

DHL Supply Chain

DHL Supply Chain is one of Brazil’s leading third-party logistics providers, offering integrated warehousing, transportation, and value-added logistics services across automotive, healthcare, retail, and technology verticals. DHL commands a significant Brazilian presence through its extensive São Paulo-based distribution network.

- Product Portfolio: Contract logistics, warehousing, transportation management, e-commerce fulfillment, cold chain, reverse logistics, and value-added services across Brazil’s major industrial regions.

- Recent Developments: Expanded automated distribution centers in São Paulo’s logistics corridor; launched AI-powered route optimization platform reducing delivery costs for major retail clients throughout 2024–2025.

- Strategic Focus: Digital logistics platform investment, warehouse automation, sustainability initiatives including fleet electrification, and expansion into underserved Northeast Brazilian markets.

A.P. Møller

A.P. Moller – Maersk offers comprehensive end-to-end supply chain solutions in Brazil, integrating ocean freight with warehousing, customs clearance, and distribution capabilities. Maersk’s Santos Port connectivity provides a strategic advantage for import and export logistics.

- Product Portfolio: Integrated logistics, warehousing and distribution, customs brokerage, cold chain logistics, and managed transportation services across Brazil’s major industrial and agricultural sectors.

- Recent Developments: Expanded Brazilian warehousing footprint in Southeast region; integrated digital TMS and WMS platforms enabling real-time supply chain visibility for manufacturing and retail clients.

- Strategic Focus: End-to-end supply chain integration, port-to-door delivery capabilities, digital platform development, and cold chain expansion for pharmaceutical and food sector clients.

JSL S.A.

JSL S.A. is one of Brazil’s largest domestic logistics providers, offering dedicated contract carriage, intermodal transportation management, and integrated supply chain solutions across industrial, mining, agricultural, and retail sectors nationwide.

- Product Portfolio: Dedicated fleet operations, intermodal transport management, warehousing, mining logistics, port logistics, and agricultural supply chain services across Brazil’s diverse geographic regions.

- Recent Developments: Strategic acquisitions of regional logistics companies expanded geographic coverage; implemented TMS platform upgrades enhancing real-time shipment visibility for manufacturing clients in 2024.

- Strategic Focus: Fleet expansion through strategic acquisitions, technology integration for operational efficiency, and market share growth across mining, agribusiness, and manufacturing logistics segments.

CEVA Logistics

CEVA Logistics is an international third-party logistics provider with significant Brazilian operations, specializing in contract logistics, freight management, and value-added services. CEVA serves major automotive, technology, and consumer goods clients across Brazil’s industrial regions.

- Product Portfolio: Contract logistics, air and ocean freight management, customs brokerage, warehousing, distribution, and specialized automotive sequencing services for global OEM clients in Brazil.

- Recent Developments: Expanded automotive logistics operations in Pouso Alegre, Minas Gerais; launched integrated digital freight platform improving multimodal coordination and real-time cargo visibility in 2025.

- Strategic Focus: Automotive logistics leadership, freight management integration, value-added warehousing services, and digital platform investment across Brazil’s competitive industrial logistics landscape.

Market Concentration Analysis

Brazil’s third-party logistics market is structurally fragmented at the operational level, with many independent regional carriers and small logistics operators. However, branded and technology-enabled providers are capturing disproportionate revenue growth in premium logistics segments.

In mature markets including Southeast Brazil, market concentration at the branded provider tier is higher, with international third-party logistics operators representing 40–50% of revenue in urban premium segments. In emerging markets including North and Northeast, regional operators and domestic providers dominate, creating significant white space for international expansion.

Consolidation at the branded provider tier is expected to accelerate through 2034, driven by private equity investment in logistics technology platforms and smaller regional operators seeking operational and brand support through acquisition or licensing partnerships. Significant brand acquisitions or strategic partnerships are expected annually through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

Healthcare logistics, e-commerce fulfillment infrastructure, and cold chain capabilities represent the highest-growth investment vectors through 2034.

Emerging Market Expansion

Northeast Brazil’s above-average growth, supported by manufacturing tax incentives and a 213.5 million population base, presents significant expansion opportunities for third-party logistics providers. The Manaus Free Trade Zone in North Brazil drives specialized electronics logistics demand requiring dedicated provider capabilities.

Technology and Innovation Investment Trends

- Warehouse automation investments in robotic AS/RS systems and conveyor automation are generating 25–40% throughput improvements for providers modernizing high-velocity e-commerce fulfillment operations across Southeast Brazil.

- Last-mile delivery technology platforms including dynamic routing, delivery lockers, and autonomous vehicle pilots are attracting logistics technology investment from both established providers and venture-backed startups.

- Cold chain infrastructure investment is accelerating to support pharmaceutical distribution, fresh food e-commerce, and agricultural export requirements across Brazil’s rapidly expanding organized retail network.

Future Market Outlook (2026-2034)

Brazil’s third-party logistics market is positioned for sustained above-average growth through 2034, anchored by e-commerce penetration expansion, manufacturing sector recovery, agricultural export growth, and continued infrastructure modernization. The 7.26% CAGR reflects structural demand drivers that transcend short-term economic cycles.

Digital transformation will be the primary competitive battleground. Providers successfully deploying AI, automation, and IoT at scale while maintaining cost competitiveness will capture the widest market share. Healthcare logistics and cold chain capabilities represent the highest premium service opportunity through 2034.

By 2034, Brazil’s third-party logistics sector is expected to reflect significantly higher market concentration, with digital-first international and domestic providers commanding larger revenue shares as technology investment creates sustainable barriers to entry for less-capitalized competitors.

Research Methodology

Primary Research

Primary research included structured interviews and surveys with over 120 industry participants in 2024–2025, comprising third-party logistics operators, shippers, freight forwarders, technology vendors, and logistics industry associations across Brazil’s major economic regions and diverse transport modes.

Secondary Research

Secondary research encompassed company reports, government transportation statistics (ANTT, ANTAQ, ANAC), trade publications, industry databases, and publicly available logistics industry data. Over 200 secondary sources were reviewed and triangulated across historical and forecast periods.

Forecasting Models

Market size estimations were derived using bottom-up revenue modeling by segment combined with top-down GDP-linked logistics expenditure analysis, incorporating infrastructure investment data, e-commerce penetration rates, and manufacturing output forecasts from official Brazilian statistical sources.

Brazil Third-Party Logistics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Transports Covered | Railways, Roadways, Waterways, Airways |

| Service Types Covered | Dedicated Contract Carriage, Domestic Transportation Management, International Transportation Management, Warehousing and Distribution, Value Added Logistics Services |

| End Uses Covered | Manufacturing, Retail, Healthcare, Automotive, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | DHL Supply Chain, A.P. Moller – Maersk, JSL S.A., CEVA Logistics, BBM Logística SA, Scan Global Logistics, FM Logistic, Patrus Transportes, Sequoia Logística, Tegma Gestão Logística S.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Brazil Third-Party Logistics Market Report

The Brazil third-party logistics market reached USD 31.42 Billion in 2025 and is projected to reach USD 59.04 Billion by 2034, growing at a CAGR of 7.26% from 2026-2034, driven by e-commerce expansion, manufacturing sector recovery, and government infrastructure investment.

Southeast Brazil leads with a 41.0% share in 2025, anchored by São Paulo’s industrial hub, Rio de Janeiro’s manufacturing clusters, and Latin America’s largest container terminal at Santos Port.

Roadways dominate with a 59.0% share in 2025, supported by Brazil’s 2 million km federal highway network enabling comprehensive national coverage for door-to-door freight delivery.

Key drivers include e-commerce expansion, government infrastructure investment, manufacturing sector growth, digital transformation via AI and IoT, and increasing agricultural export logistics requirements.

Manufacturing leads with a 25.0% share in 2025, driven by automotive, electronics, and food processing sector logistics outsourcing. Brazil’s vehicle sales reached 2.6 million units in 2024, generating substantial third-party logistics demand.

Healthcare logistics is the fastest growing segment at approximately 8.5% CAGR, driven by pharmaceutical distribution requirements, cold chain expansion, and medical device logistics demand across Brazil’s growing healthcare sector.

Leading companies include DHL Supply Chain, A.P. Moller – Maersk, JSL S.A., CEVA Logistics, BBM Logística SA, Scan Global Logistics, FM Logistic, Patrus Transportes, Sequoia Logística, and Tegma Gestão Logística S.A.

The Brazil third-party logistics market is projected to reach approximately USD 44.60 Billion by 2030, reflecting steady compound growth from the 2025 base at the market’s 7.26% CAGR across all transport and end-use segments.

High-growth opportunities include healthcare cold chain logistics, e-commerce fulfillment center development, warehouse automation, Northeast Brazil regional expansion, and last-mile delivery technology platforms targeting urban consumers.

Key challenges include infrastructure gaps in northern regions, Brazil’s complex multi-state tax system and new IBS-CBS regime from 2026, high fuel costs, last-mile complexity in urban areas, and logistics talent shortages.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)