Brazil Vegan Food Market Size, Share, Trends and Forecast by Product, Source, Distribution Channel, and Region, 2026-2034

Brazil Vegan Food Market Size, Share, Trends & Forecast (2026-2034)

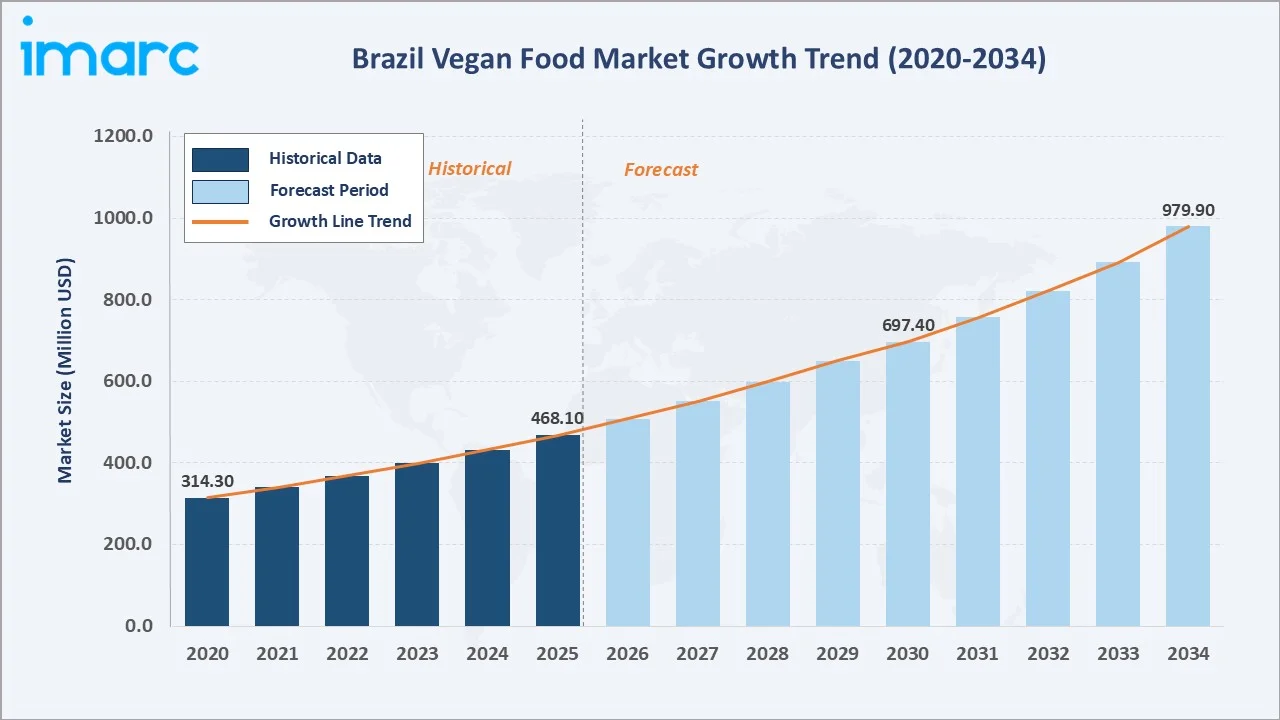

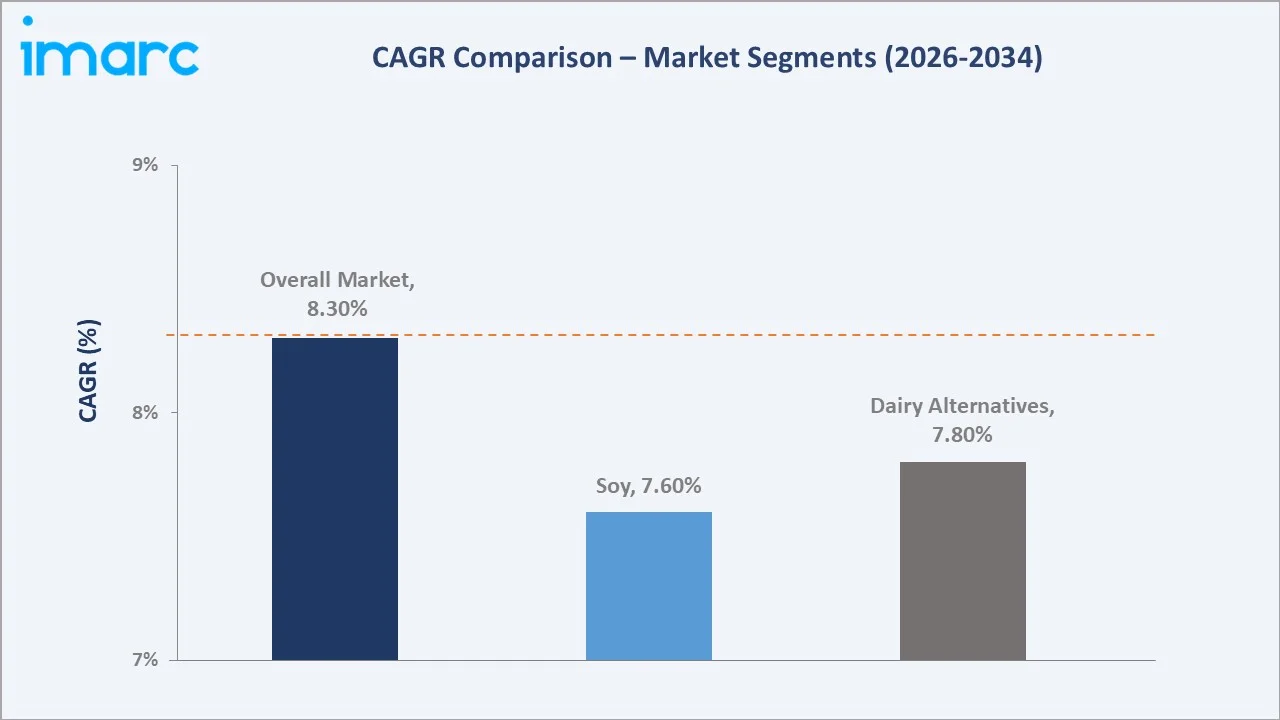

The Brazil vegan food market reached USD 468.1 Million in 2025 and is projected to reach USD 979.9 Million by 2034, growing at a CAGR of 8.30% during 2026-2034. Growth is driven by rising health consciousness, expanding retail availability, and increasing concern over the environmental footprint of animal agriculture. A 2025 survey commissioned by the Brazilian Vegetarian Society found that 74% of respondents would consider reducing or eliminating meat consumption for health reasons. Dairy alternatives lead the product segment at 48.7%. Soy dominates the source category at 39.5%. Southeast region commands 44.2% of the national market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 468.1 Million |

|

Forecast Market Size (2034) |

USD 979.9 Million |

|

CAGR (2026-2034) |

8.30% |

|

Dominant Product |

Dairy Alternatives (48.7%, 2025) |

|

Dominant Source |

Soy (39.5%, 2025) |

|

Leading Region |

Southeast Brazil (44.2%, 2025) |

Brazil vegan food market expanded from USD 314.3 Million in 2020 to USD 468.1 Million in 2025, anchored at USD 697.4 Million in 2030, and forecast to reach USD 979.9 Million by 2034. The COVID-19 pandemic accelerated home cooking and health-driven purchasing behavior, creating a lasting shift toward plant-based diets that has carried well beyond the pre-pandemic baseline.

To get more information on this market, Request Sample

Meat substitutes grow fastest at an estimated ~9.1% CAGR through 2034 as foodservice adoption widens. The soy-based source segment grows at ~7.6% CAGR, while the almond-based source segment expands faster at ~9.6% CAGR, supported by rising demand for nutrient-dense, allergen-friendly alternatives.

Executive Summary

Brazil vegan food market at USD 468.1 Million in 2025 represents one of Latin America's fastest-expanding plant-based food destinations, a market shaped by structural dietary shifts, an active retail innovation cycle, and a vegan and vegetarian population base estimated at around 29 million people. The market is projected to reach USD 979.9 Million by 2034, with an intermediate anchor of USD 697.4 Million expected by 2030.

Dairy alternatives lead the product segment at 48.7% share in 2025, supported by widespread availability of plant-based milks, cheeses, and yogurts across major retail chains. Soy leads the source segment at 39.5% due to its cost efficiency and established domestic supply chain, while almond-based products are growing fastest among sources. Southeast Brazil leads regionally with a 44.2% share, reflecting the concentration of population, retail infrastructure, and food manufacturing in the region.

Looking ahead, the market outlook remains positive as manufacturers expand product portfolios, foodservice operators introduce plant-based menu items, and government dietary guidelines increasingly emphasize reduced animal-protein consumption for public health and sustainability reasons.

Key Market Insights

|

Insight |

Data |

|

Dominant Product |

Dairy Alternatives - 48.7% share (2025) |

|

Dominant Source |

Soy - 39.5% market share (2025) |

|

Leading Region |

Southeast Brazil - 44.2% share (2025) |

|

Market Opportunity |

Foodservice plant-based menu expansion; clean-label dairy alternatives; almond and oat-based innovation; e-commerce distribution growth |

Key Analytical Observations Supporting The Above Data:

- Dairy Alternatives at 48.7%: The dairy alternatives segment leads due to widespread consumer familiarity with plant-based milk and yogurt, broad supermarket placement, and rising lactose-intolerance awareness among Brazilian consumers.

- Soy at 39.5%: Soy dominates the source category because of Brazil's position as one of the world's largest soybean producers, which keeps input costs low and supply chains short for domestic manufacturers.

- Southeast Brazil at 44.2%: Southeast Brazil dominates due to its concentration of supermarkets, specialty health food retailers, and food manufacturing hubs in São Paulo and Rio de Janeiro, alongside the region's higher average household income.

- Meat Substitutes Growth: Meat substitutes are expanding quickly as foodservice chains, including fast-food and casual dining operators, add plant-based burger and protein options to menus across urban centers.

- Retail Channel Shift: Online grocery and direct-to-consumer channels are capturing a growing share of vegan food purchases as urban consumers seek convenience and wider product variety than physical stores typically stock.

- Premiumization Trend: Brands are increasingly positioning vegan products as premium, clean-label offerings, supporting higher average selling prices and improved margins across the dairy alternatives and meat substitutes categories.

Brazil Vegan Food Market Overview

Brazil vegan food market operates within the broader Latin American plant-based food landscape as the region's largest contributor by population and retail scale. The market's distinguishing feature is its dual growth driver base, combining ethically motivated vegan consumers with a much larger flexitarian population reducing meat intake primarily for health reasons.

The Brazil vegan food ecosystem integrates raw material suppliers, ingredient processors, food manufacturers, retail and foodservice channels, and an evolving regulatory framework overseen by ANVISA, Brazil's health regulatory agency. Macroeconomic factors include rising urban disposable income, increasing health and wellness spending, and growing environmental awareness tied to Brazil's agricultural sector.

Market Dynamics

To evaluate market opportunities, Request Sample

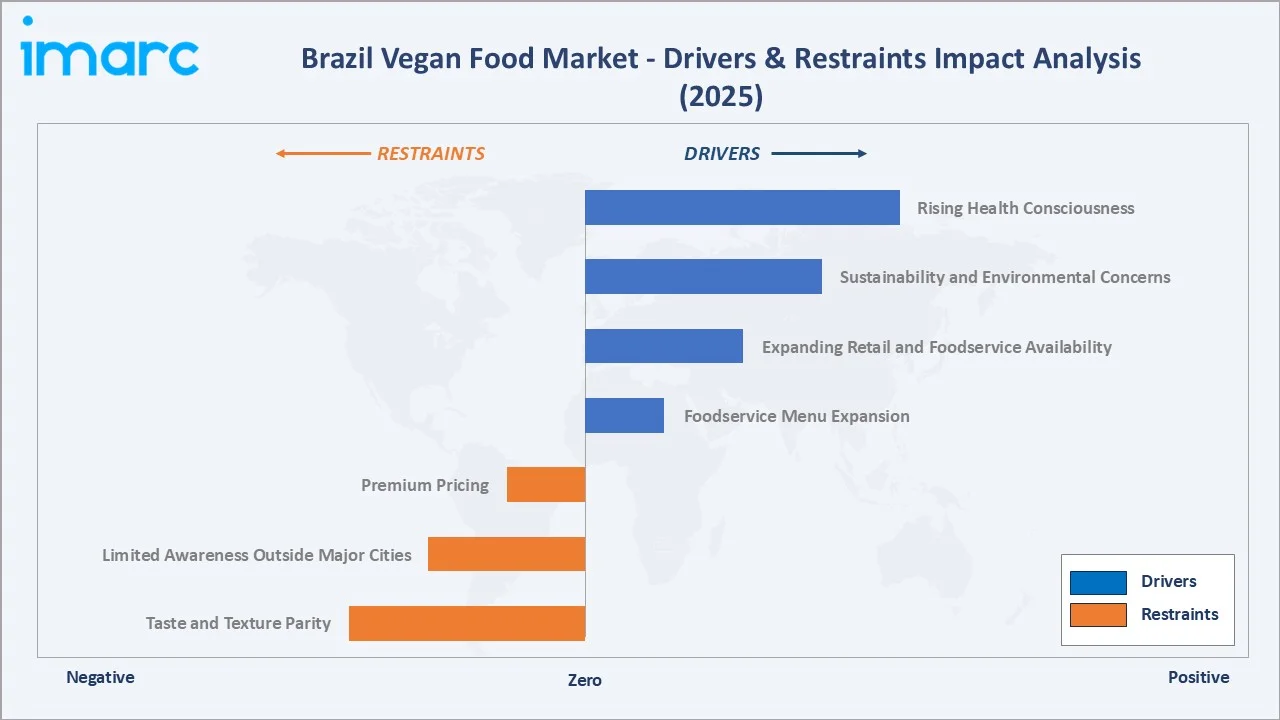

Market Drivers

- Rising Health Consciousness: Growing awareness of diet-related chronic diseases, including obesity and cardiovascular conditions, is encouraging Brazilian consumers to reduce animal-protein intake. This shift is supported by 74% of survey respondents in 2025 indicating openness to reducing or eliminating meat consumption for health reasons, according to the Brazilian Vegetarian Society. Rising health-driven purchasing is broadening demand beyond strict vegans toward flexitarian shoppers.

- Sustainability and Environmental Concerns: Brazilian consumers are increasingly factoring environmental impact into food choices, particularly given Brazil's prominent role in global animal agriculture and associated land-use debates. Plant-based products are positioned as a lower-footprint alternative, supporting adoption among environmentally conscious urban shoppers.

- Expanding Retail and Foodservice Availability: Major supermarket chains and foodservice operators are expanding plant-based product lines and menu items across Brazil's urban centers. Wider shelf placement and foodservice trial opportunities are lowering barriers to first-time purchase and supporting repeat consumption.

Market Restraints

- Premium Pricing: Vegan food products typically carry a price premium over conventional animal-based alternatives, limiting affordability for price-sensitive consumer segments and constraining broader mass-market adoption.

- Limited Awareness Outside Major Cities: Product availability and consumer awareness remain concentrated in large urban centers, with smaller cities and rural areas showing lower retail penetration and limited product variety.

Market Opportunities

- Foodservice Menu Expansion: Quick-service and casual dining chains introducing dedicated plant-based menu items represent a significant growth opportunity, exposing a broader consumer base to vegan products outside the retail channel.

- Clean-Label Product Innovation: Demand for simplified ingredient lists and recognizable plant sources is creating opportunities for manufacturers to differentiate through clean-label formulations in both dairy alternatives and meat substitutes categories.

Market Challenges

- Taste and Texture Parity: Achieving taste and texture comparable to animal-based products remains a technical challenge, particularly for meat substitutes, and continues to influence repeat-purchase rates among non-vegan consumers.

- Supply Chain and Cold Chain Limitations: Refrigerated distribution infrastructure outside major metropolitan areas can limit the shelf life and availability of fresh dairy alternative products in smaller markets.

Emerging Market Trends

1. Functional and Fortified Plant-Based Products

Manufacturers are increasingly fortifying plant-based products with vitamin B12, calcium, and protein to address nutritional gaps associated with plant-based diets. This trend is helping shift perception of vegan food from a niche dietary choice toward a mainstream functional nutrition category.

2. Foodservice and Quick-Service Restaurant Integration

Quick-service and casual dining chains are adding plant-based burgers, nuggets, and dairy-free options to permanent menus rather than limited-time offerings. This integration is normalizing vegan food consumption among occasional and flexitarian diners.

3. Clean-Label and Minimally Processed Formulations

Consumers are favoring products with shorter, recognizable ingredient lists over heavily processed alternatives. Brands are responding with whole-food-based formulations that emphasize transparency and simplicity in labeling.

4. E-Commerce and Direct-to-Consumer Growth

Online grocery platforms and direct-to-consumer subscription models are expanding access to specialty vegan products beyond traditional retail footprints, particularly benefiting smaller and newer brands seeking national reach without extensive physical distribution.

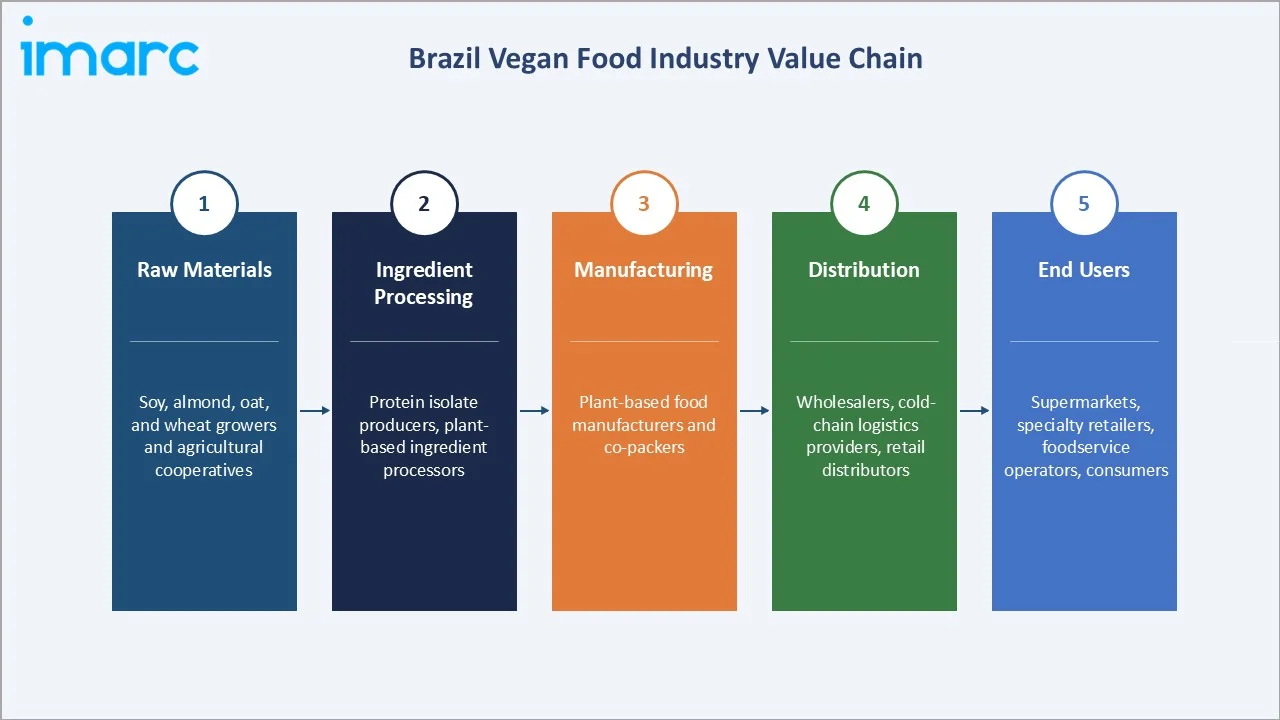

Industry Value Chain Analysis

Brazil vegan food value chain integrates raw material cultivation, ingredient processing, product formulation and manufacturing, packaging and quality control, distribution and logistics, and retail and foodservice delivery.

|

Stage |

Key Participants |

|

Raw Materials |

Soy, almond, oat, and wheat growers and agricultural cooperatives |

|

Ingredient Processing |

Protein isolate producers, plant-based ingredient processors |

|

Manufacturing |

Plant-based food manufacturers and co-packers |

|

Distribution |

Wholesalers, cold-chain logistics providers, retail distributors |

|

End Users |

Supermarkets, specialty retailers, foodservice operators, consumers |

Product formulation and manufacturing represents the most competitive stage in the Brazil vegan food value chain, as companies compete on taste, texture, and nutritional profile to differentiate offerings. Success at this stage directly shapes consumer repeat-purchase behavior and brand loyalty across both dairy alternatives and meat substitutes categories.

Technology Landscape in the Brazil Vegan Food Industry

Protein Extraction and Texturization Technology

Advances in protein extraction and texturization are improving the taste and mouthfeel of meat substitutes, helping close the sensory gap with animal-based products and broadening appeal among flexitarian consumers.

Plant-Based Fermentation Techniques

Fermentation-based processing is being applied to dairy alternatives to improve flavor complexity and nutritional profile, supporting premium product positioning within the dairy alternatives segment.

Cold Chain and Packaging Innovation

Improved packaging technology is extending shelf life for fresh plant-based products, helping manufacturers expand distribution beyond major metropolitan cold-chain networks into secondary cities.

Digital Retail and Traceability Platforms

E-commerce platforms and digital traceability tools are enabling brands to communicate sourcing transparency directly to consumers, supporting trust in clean-label and sustainably sourced product claims.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Dairy Alternatives |

48.7% |

2025 |

|

Source |

Soy |

39.5% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

Southeast |

44.2% |

2025 |

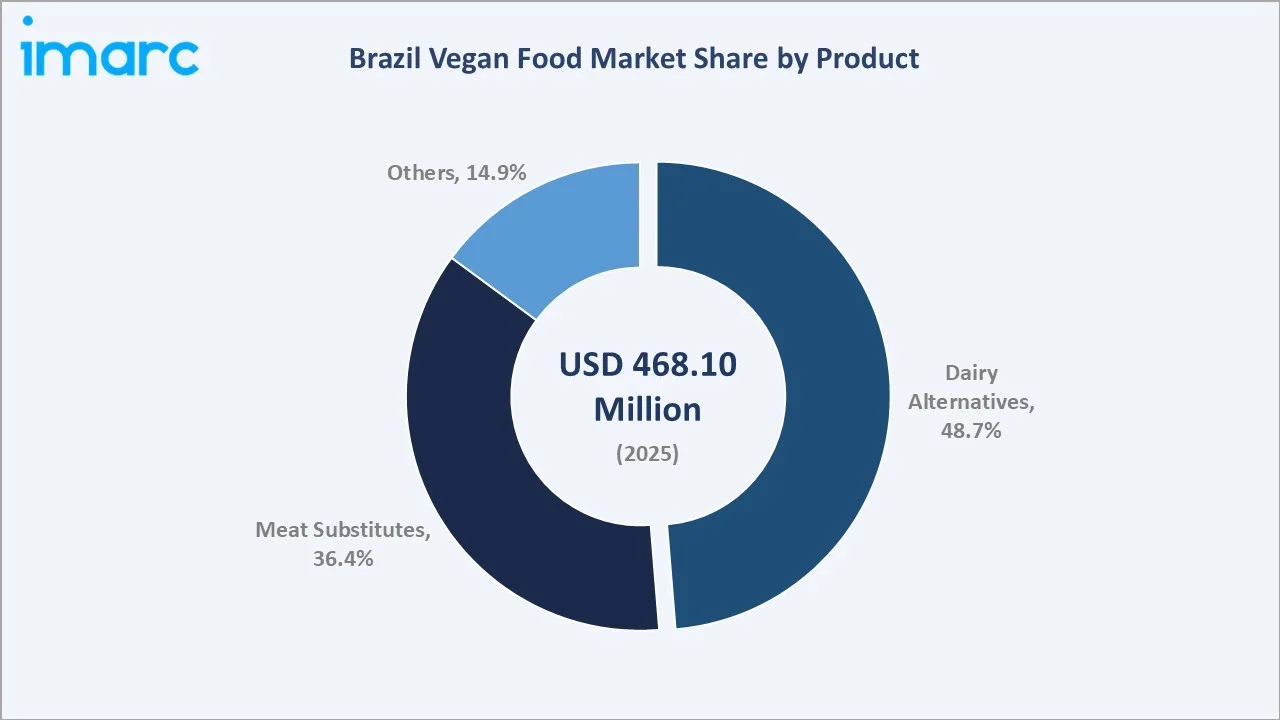

By Product

Dairy alternatives lead at 48.7% (2025), encompassing plant-based milk, cheese, yogurt, and dessert products, supported by broad retail distribution and high consumer familiarity built over more than a decade of category development.

To access detailed market analysis, Request Sample

Meat substitutes hold 36.4% share and are growing the fastest among product categories at an estimated 9.1% CAGR, driven by foodservice adoption and expanding retail variety. The others category, comprising plant-based eggs, spreads, and snacks, accounts for the remaining 14.9% of the product mix.

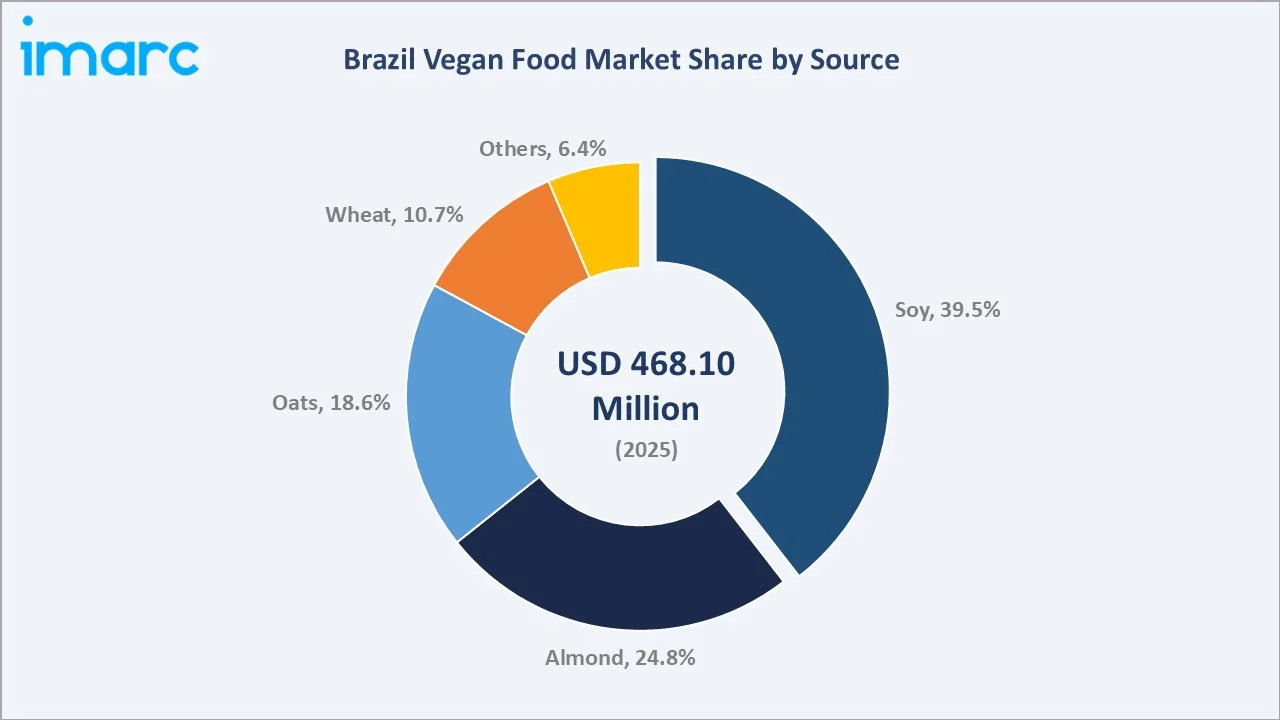

By Source

Soy leads the source segment at 39.5% (2025), reflecting Brazil's position as a major global soybean producer and the resulting cost advantage for domestic manufacturers sourcing soy protein locally.

Almond follows at 24.8% share and is the fastest-growing source category at an estimated 9.6% CAGR, supported by demand for nutrient-dense, allergen-friendly alternatives. Oats hold 18.6% share, wheat accounts for 10.7%, and other sources, including coconut and rice, make up the remaining 6.4%.

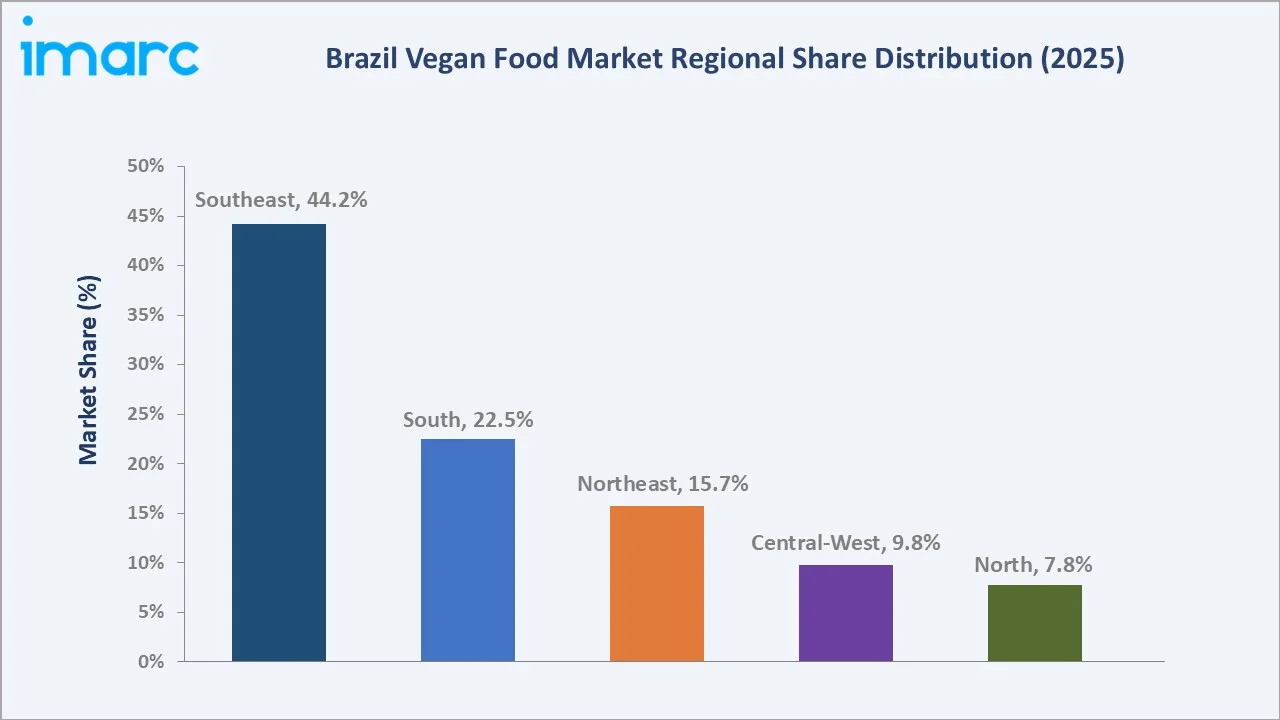

Regional Market Insights

Southeast Brazil's 44.2% market dominance reflects the region's concentration of population, retail infrastructure, and food manufacturing capacity centered around São Paulo and Rio de Janeiro. South Brazil follows at 22.5%, benefiting from strong agricultural ties and relatively high consumer purchasing power.

Northeast Brazil holds 15.7% share and is expanding as retail chains extend plant-based product distribution into the region's growing urban centers. Central-West Brazil accounts for 9.8% share, supported by its strong agricultural base, while North Brazil represents the smallest share at 7.8%, growing from a low base as awareness and retail access gradually improve.

|

Region |

Share (2025) |

Key Brazil Vegan Food Market Drivers & Characteristics |

|

Southeast |

44.2% |

Driven by high retail density, strong manufacturing presence, and higher average household income. |

|

South |

22.5% |

Benefits from strong agricultural ties to soy and grain production and rising health awareness among consumers. |

|

Northeast |

15.7% |

Witnessing growing retail penetration as supermarket chains expand plant-based product offerings in urban centers. |

|

Central-West |

9.8% |

Supported by proximity to raw material production and gradual expansion of modern retail formats. |

|

North |

7.8% |

Experiencing early-stage growth as awareness increases and retail and distribution infrastructure develop. |

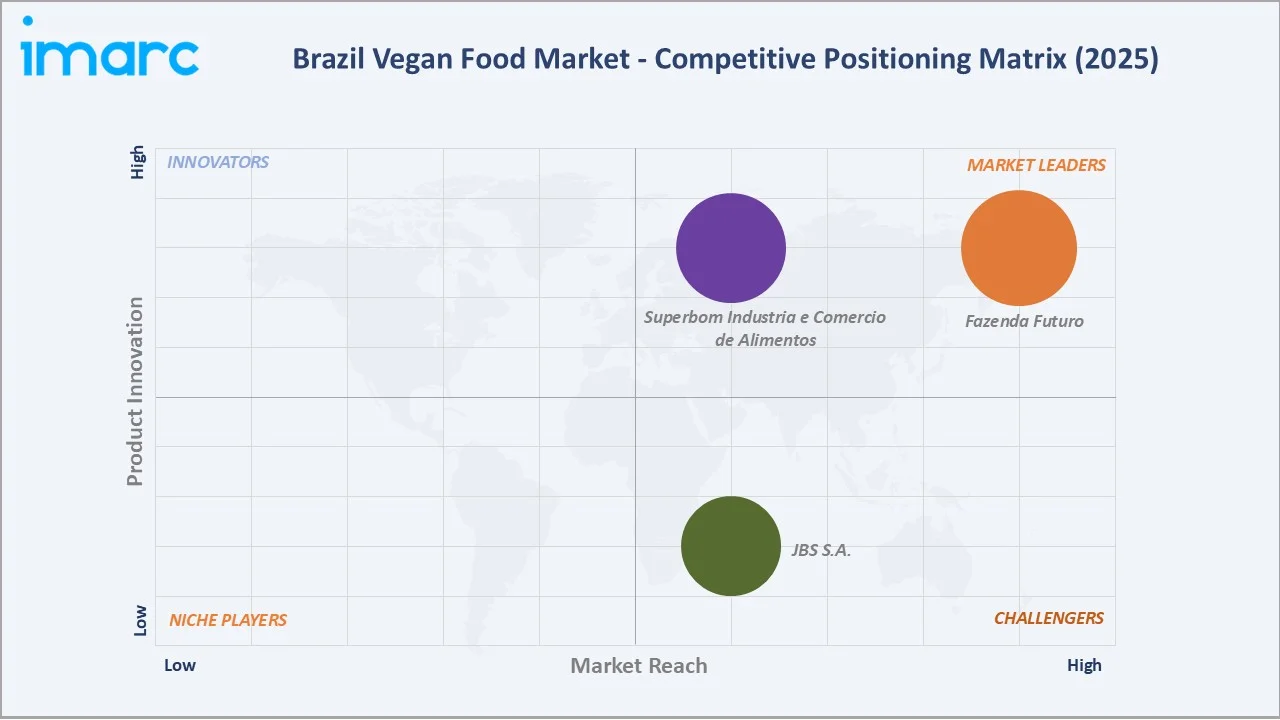

Competitive Landscape

Brazil vegan food competitive landscape is moderately fragmented, comprising established plant-based specialty brands, divisions of large traditional meat processors entering the category, and international entrants expanding into the Brazilian market. Large traditional meat companies entering the plant-based category through dedicated product lines represent a distinctive competitive dynamic in Brazil, leveraging existing distribution networks and brand recognition to accelerate plant-based product adoption among mainstream consumers.

|

Company |

Key Products |

Market Position |

Core Strength |

|

Fazenda Futuro |

Future Beef & Future Mince, Future Chicken, Future Pork & Sausages, Future Tuna |

Market Leader |

Hyper-realistic taste & texture, clean & healthy ingredients, strategic market placement, expanding portfolio, widespread accessibility |

|

Superbom Industria e Comercio de Alimentos |

Plant-Based Meats, Vegan Cheeses |

Market Leader |

Pioneering plant-based meats, dairy substitutes, clean label & nutrition |

|

JBS S.A. |

Incrível Burger, Incrível Frango, Incrível Salsicha, Incrível Carne Moída, Incrível Bacon |

Strong Challenger |

Operates Seara Incrível, massive supply chain & distribution, advanced "superprotein" innovation, specialized food technology hub |

Key Company Profiles

Fazenda Futuro

Fazenda Futuro, also known as Future Farm, is a Brazilian plant-based food company specializing in meat substitute products. The company produces a range of plant-based burgers, ground meat, meatballs, and sausages formulated primarily from pea and soy protein, with distribution across Brazilian retail and growing presence in international markets including the UK, Germany, and the Netherlands.

- Key Products: Future Beef & Future Mince, Future Chicken, Future Pork & Sausages, Future Tuna, and others.

- Strategic Focus: Expanding meat substitute product variety and scaling international distribution while strengthening domestic retail penetration in Brazil.

Superbom Industria e Comercio de Alimentos

Superbom Industria e Comercio de Alimentos is one of Brazil's longest-established plant-based food manufacturers, with a product range spanning vegan cheese, meat substitutes, and frozen plant-based seafood alternatives sold nationally in Brazilian supermarkets.

- Key Products: Plant-Based Meats, Vegan Cheeses, and others.

- Strategic Focus: Broadening category coverage across vegan cheese, meat, and seafood alternatives while maintaining its position as a long-established trusted Brazilian plant-based brand.

Market Concentration Analysis

Brazil vegan food market is moderately fragmented, with the top companies, such as Fazenda Futuro, Superbom Industria e Comercio de Alimentos, and JBS S.A., accounting for an estimated 45-55% combined market share as of 2025. The dairy alternatives segment shows relatively higher concentration due to established brand presence, while the meat substitutes segment remains more fragmented as new entrants, including divisions of traditional meat processors, continue to launch competing product lines.

Consolidation activity is increasing as larger traditional food companies acquire or build internal plant-based capabilities to compete with specialist vegan brands, a trend expected to gradually increase market concentration through the forecast period.

Investment & Growth Opportunities

Highest Growth Segments

Meat substitutes (~9.1% CAGR through 2034), almond-based products (~9.6% CAGR), foodservice plant-based menu items, and clean-label dairy alternatives represent Brazil's highest-growth vegan food investment vectors through the forecast period.

Investment Themes

- Foodservice partnership expansion: Investment in plant-based product lines developed specifically for quick-service and casual dining partnerships represents an opportunity to reach occasional and flexitarian consumers beyond the retail channel.

- Almond and oat-based ingredient innovation: Investment in domestic processing capacity for almond and oat-based ingredients could reduce reliance on imported inputs while capturing the fastest-growing source segment.

Future Market Outlook (2026-2034)

Brazil vegan food market is projected to grow from USD 468.1 Million in 2025 to USD 979.9 Million by 2034, delivering an 8.30% CAGR over the forecast period. The market's anchor value of USD 697.4 Million by 2030 represents a structural mid-point in the market's evolution from a niche dietary category toward broader mainstream adoption.

Three structural forces define Brazil's vegan food market through 2034: continued health-driven flexitarian adoption broadening the addressable consumer base beyond strict vegans, foodservice integration normalizing plant-based options in everyday dining occasions, and ingredient innovation improving taste and nutritional parity with animal-based products.

Research Methodology

Primary Research

Primary research comprised structured interviews with Brazil vegan food industry stakeholders, including company executives, product development leads, and retail category managers, alongside consumer surveys across the Southeast, South, and Northeast regions.

Secondary Research

Secondary research encompassed company annual reports, Brazil plant-based food investment data, government dietary and agricultural statistics, and industry association publications. Over 40 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a consumption-based model, combining Brazil's vegetarian and flexitarian population estimates with per-capita plant-based food spending trends, converted to USD using prevailing exchange rate forecasts.

Brazil Vegan Food Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Sources Covered | Almond, Soy, Oats, Wheat, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online Stores, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Fazenda Futuro, Superbom Industria e Comercio de Alimentos, JBS S.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil vegan food market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil vegan food market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil vegan food industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Vegan Food Market Report

The Brazil vegan food market reached USD 468.1 Million in 2025, driven by rising health consciousness, sustainability concerns, and expanding retail and foodservice availability of plant-based products across the country.

The Brazil vegan food market grows at an 8.30% CAGR during 2026-2034, reaching USD 979.9 Million by 2034, supported by foodservice integration, ingredient innovation, and broadening flexitarian consumer demand.

Dairy alternatives lead at 48.7% share in 2025, supported by wide retail availability and strong consumer familiarity built over more than a decade of category development in Brazil.

Soy leads at 39.5% share due to Brazil's position as a major global soybean producer, which provides domestic manufacturers with a cost-efficient and reliable local supply chain.

Southeast Brazil leads at 44.2% share, reflecting the region's concentration of population, retail infrastructure, and food manufacturing capacity around São Paulo and Rio de Janeiro.

Leading companies include Fazenda Futuro, Superbom Industria e Comercio de Alimentos, and JBS S.A., among others.

The Brazil vegan food market is projected to reach approximately USD 697.4 Million by 2030, as foodservice adoption and clean-label product innovation continue to broaden the addressable consumer base.

Priority opportunities include foodservice partnership expansion for plant-based menu items, almond and oat-based ingredient processing investment, and clean-label product innovation in dairy alternatives.

The Brazil vegan food market was valued at USD 314.3 Million in 2020, before expanding to USD 468.1 Million by 2025 amid rising health and sustainability-driven consumer demand.

Meat substitutes held 36.4% share in 2025 and represent the fastest-growing product category, supported by expanding foodservice adoption and continued improvements in taste and texture.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)