Brushless DC Motors Market Size, Share, Trends and Forecast by Product Type, Power Rating, End Use Industry, and Region 2026-2034

Global Brushless DC Motors Market Size, Share, Trends & Forecast (2026-2034)

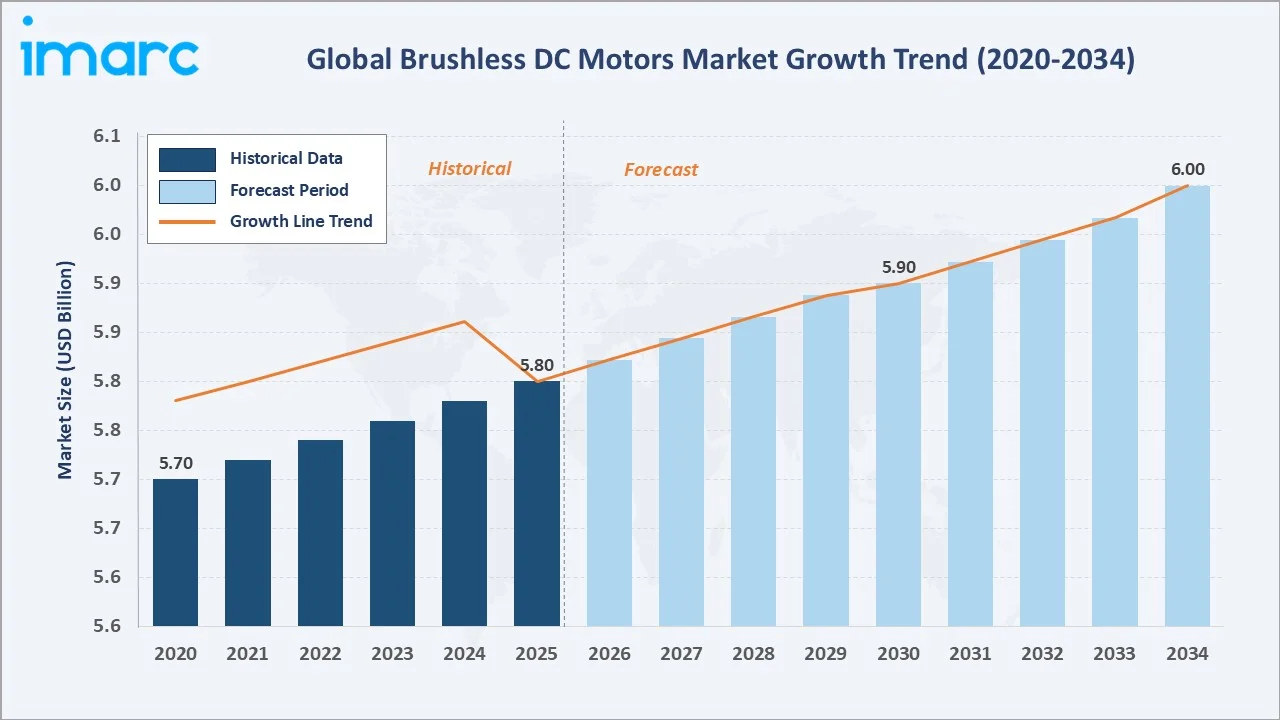

The global brushless DC motors market size was valued at USD 5.8 Billion in 2025 and is projected to reach USD 6.0 Billion by 2034. Rising industrial automation, growing electric vehicle (EV) adoption, and expanding consumer electronics applications sustain the brushless DC motors market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.8 Billion |

|

Forecast Market Size (2034) |

USD 6.0 Billion |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

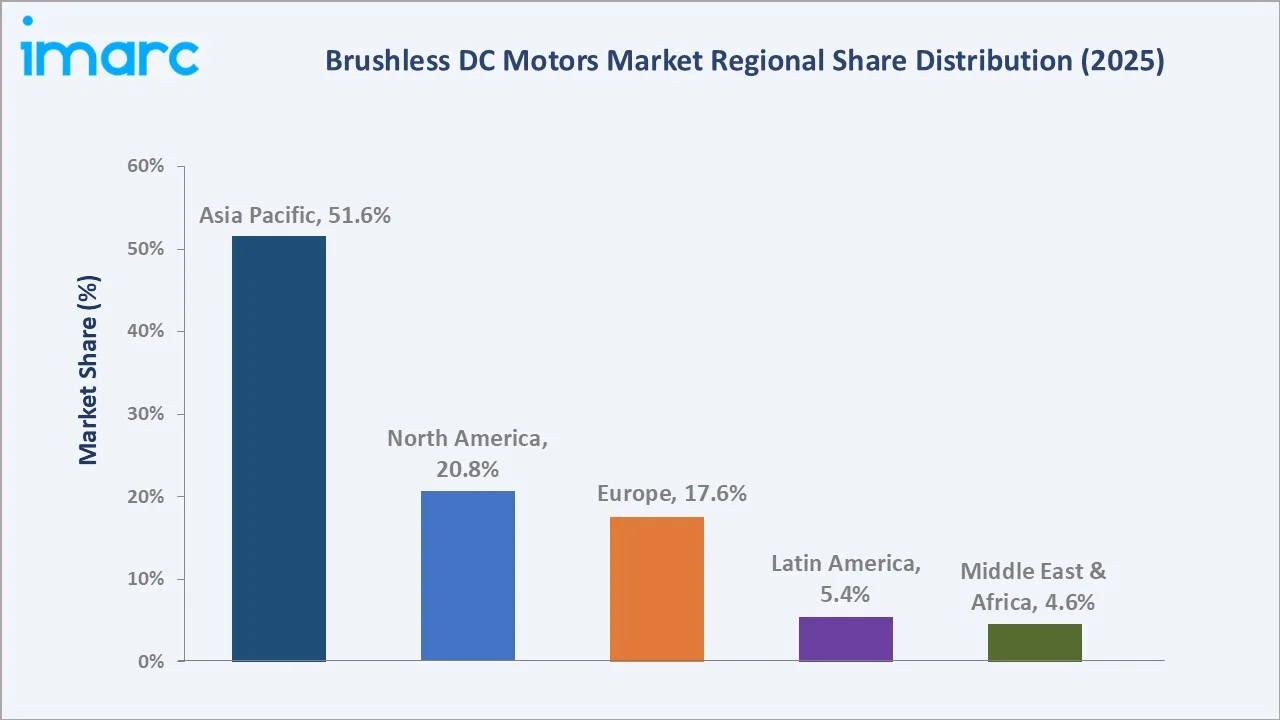

Asia Pacific (51.6% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Product Type |

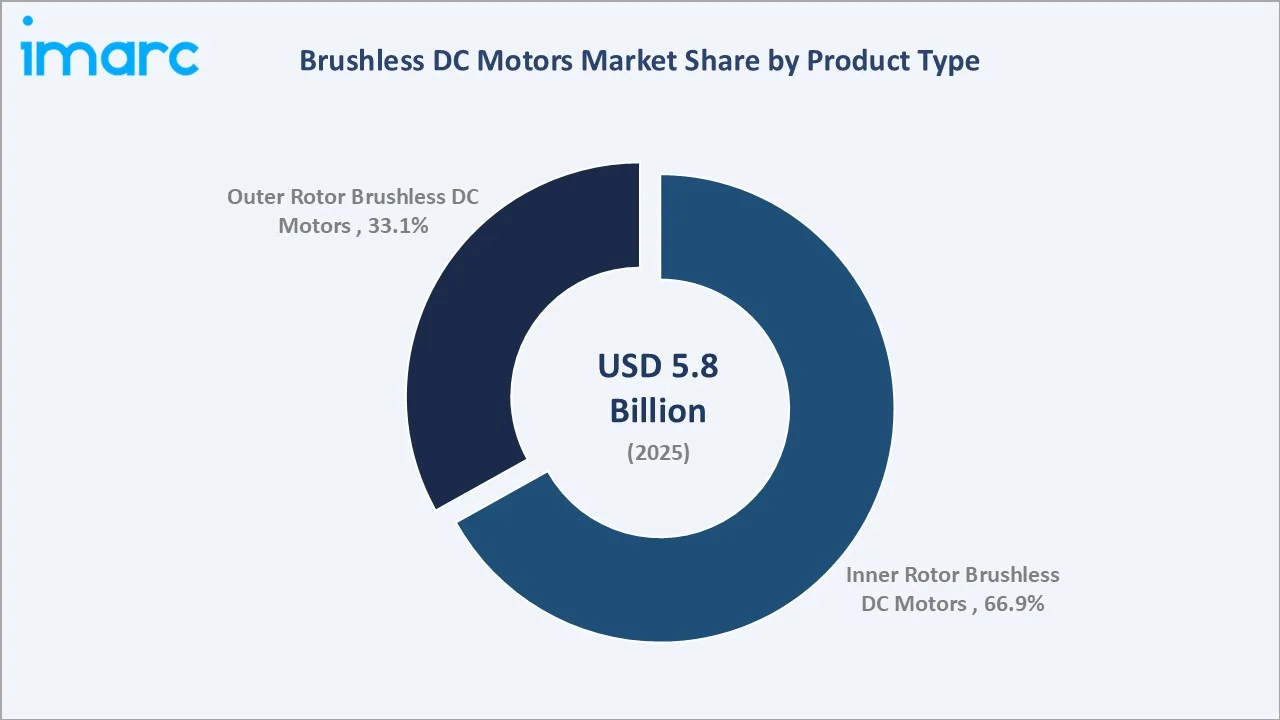

Inner Rotor BLDC Motors (66.9%, 2025) |

|

Leading Power Rating |

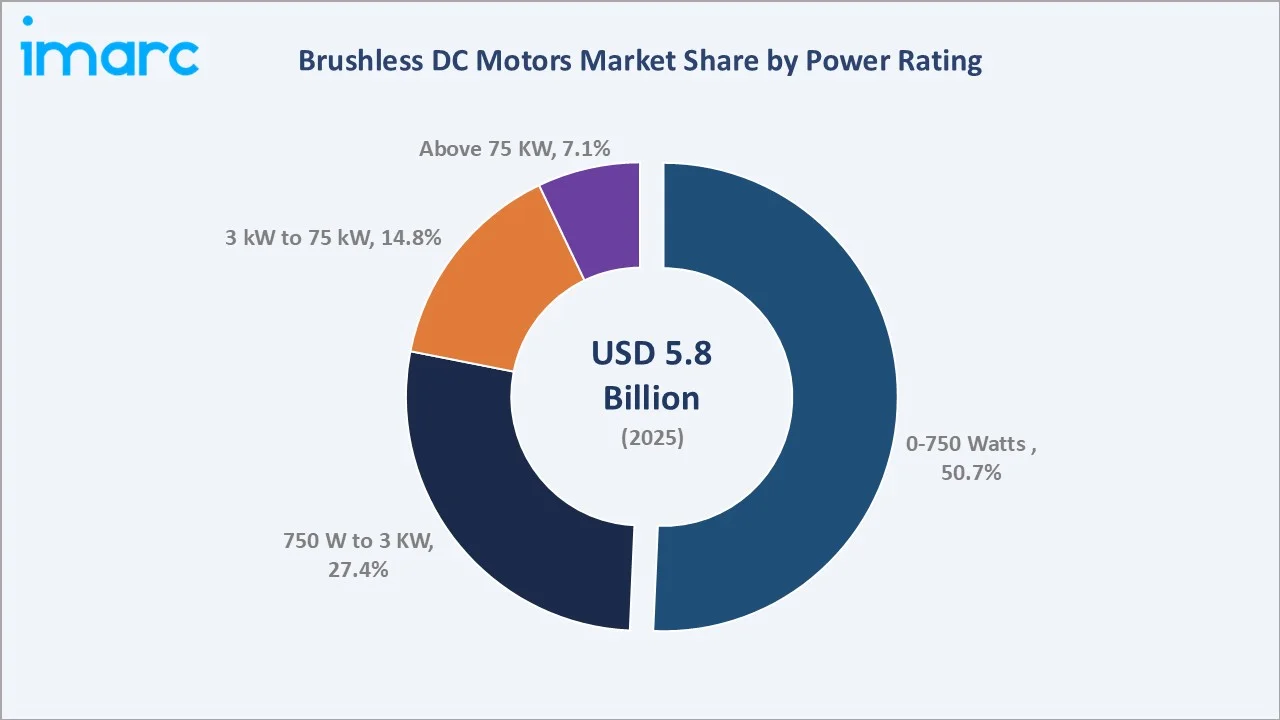

0-750 Watts (50.7%, 2025) |

The global brushless DC motors market growth trajectory from 2020 through 2034 contrasts stable historical expansion against a sustained forecast curve driven by automation adoption, energy-efficiency mandates, and smart motor integration across industrial and consumer applications.

To get more information on this market, Request Sample

Executive Summary

The global brushless DC motors market is sustaining stable growth. It is driven by accelerating industrial automation, the global electric vehicle (EV) transition, and expanding application in robotics, HVAC, and consumer electronics. Valued at USD 5.8 Billion in 2025, the market is forecast to reach USD 6.0 Billion by 2034, reflecting a mature but strategically critical market segment.

Inner rotor motors command 66.9% share in 2025, driven by compact design requirements, higher torque density, and superior thermal management in industrial servo systems.

Asia Pacific leads with 51.6% global revenue share in 2025, anchored by China's electronics manufacturing base and India's growing industrial automation sector

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Inner Rotor BLDC Motors – 66.9% share (2025) |

|

Second Product Type |

Outer Rotor BLDC Motors – 33.1% share (2025) |

|

Largest Power Rating |

0-750 Watts – 50.7% share (2025) |

|

Second Power Rating |

750W to 3 kW – 27.4% share (2025) |

|

Leading Region |

Asia Pacific – 51.6% revenue share (2025) |

|

Top Companies |

Nidec, Maxon, Allied Motion, Moog, Portescap, Oriental Motor |

|

Market Opportunity |

EV drivetrain electrification & industrial robotics expansion |

Key Analytical Observations Supporting The Above Data:

- Inner Rotor motors' Inner Rotor motors' 66.9% dominance in 2025 reflects their superior torque-to-inertia ratio and broad integration across CNC machines, servo drives, and precision automation equipment operating in industrial settings globally.

- Outer Rotor motors' Outer Rotor motors' 33.1% share is propelled by application versatility in drone propulsion, e-scooter wheels, HVAC fans, and washing machine drum drives, where high pole count and low-speed torque delivery are critical design requirements.

- 0-750W segment's 0-750W segment's 50.7% majority is underpinned by explosive growth in compact industrial robots, medical devices, and consumer electronics motors.

- Asia Pacific's Asia Pacific's 51.6% global dominance reflects China's role as the world's largest electronics manufacturing hub and India's government-backed Production Linked Incentive (PLI) scheme accelerating domestic motor manufacturing capacity.

- EV adoption EV adoption is a structural tailwind. Global EV registrations, a proxy for sales, rose by 6% to almost 2.1 million units in December, reaching 20.7 million vehicles in 2025, each requiring multiple brushless DC motors for traction, auxiliary pumps, cooling, and HVAC subsystems across the powertrain architecture.

Global Brushless DC Motors Market Overview

Brushless DC motors are electronically commutated electric motors offering high efficiency, low maintenance, and extended operational life compared to brushed alternatives. The global market encompasses a broad range of products spanning inner rotor, outer rotor, and axial flux configurations, rated from sub-watt medical micro-motors to multi-hundred-kilowatt industrial drive systems.

The industry operates at the intersection of power electronics innovation, electrification megatrends, and manufacturing automation. Growth is supported by macroeconomic drivers such as Industry 4.0 adoption, tightening energy-efficiency standards, and the global EV transition.

Market Dynamics

To evaluate market opportunities, Request Sample

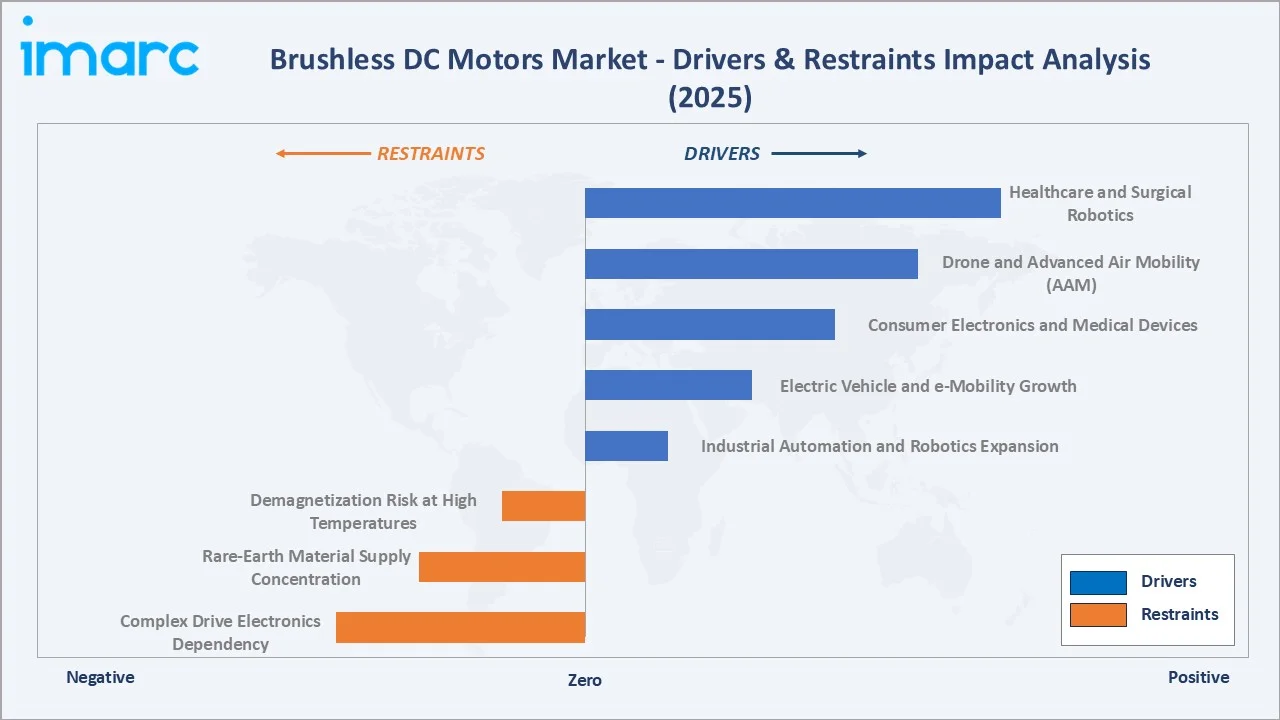

Market Drivers

- Industrial Automation and Robotics Expansion: The new World Robotics 2025 statistics on industrial robots showed 542,100 robots installed in 2024, more than double the number 10 years ago. Each collaborative robot (cobot) and industrial servo axis integrates a BLDC motor as its primary actuator, creating sustained, structurally demand across precision manufacturing globally.

- Electric Vehicle and e-Mobility Growth: Global EV registrations, a proxy for sales, rose by 6% to almost 2.1 million units in December, reaching 20.7 million vehicles in 2025. Each vehicle platform requires 4-16 BLDC motors for traction, power steering, thermal management, and auxiliary systems, creating multi-unit procurement demand per vehicle manufactured.

- Consumer Electronics and Medical Devices: Miniaturized BLDC motors power hard disk drives, cooling fans, surgical tools, ventilators, and insulin pumps. In 2024, wearable device shipments are expected to reach 560 million units, creating recurring replacement and new-unit demand for sub-100W precision motors.

Market Restraints

- Complex Drive Electronics Dependency: BLDC motors require dedicated electronic speed controllers (ESCs) or servo drives, adding system complexity, failure points, and engineering overhead. This constraint is particularly pronounced in retrofit applications where legacy brushed motor infrastructure requires full drive system replacement.

- Rare-Earth Material Supply Concentration: Permanent magnet BLDC motors depend on neodymium-iron-boron (NdFeB) magnets, with China controlling over 85% of global rare-earth production in 2024. Supply concentration and price volatility create raw-material risk for manufacturers globally.

Market Opportunities

- Drone and Advanced Air Mobility (AAM): Commercial drone deliveries and urban air mobility (UAM) platforms depend entirely on high-efficiency BLDC motors. 855,860 drones registered with the FAA in the United States (as of October 2026), each requiring 4-8 BLDC motors for propulsion, gimbal, and payload systems.

- Smart Motor and IoT Integration: Industry 4.0 platforms are driving demand for smart BLDC motor systems with integrated sensors, real-time diagnostics, and predictive maintenance capabilities. Embedding IoT connectivity enables condition-based maintenance.

- Healthcare and Surgical Robotics: The global surgical robotics market is expected to witness significant growth, driven by increasing adoption of advanced medical technologies. Minimally invasive surgical systems, rehabilitation robots, and diagnostic imaging platforms require miniaturized, ultra-quiet, and precisely controllable BLDC motor configurations.

Market Challenges

- Demagnetization Risk at High Temperatures: NdFeB permanent magnets are susceptible to demagnetization at sustained high operating temperatures above 80-150°C, limiting BLDC motor adoption in high-heat industrial environments without specialized magnet formulations or active thermal management systems.

- Skilled Engineering Shortage: Designing and calibrating BLDC motor drive systems requires specialized expertise in power electronics, field-oriented control (FOC), and embedded firmware. This skills gap creates project execution risk and extends design timelines in markets with limited engineering talent pipelines.

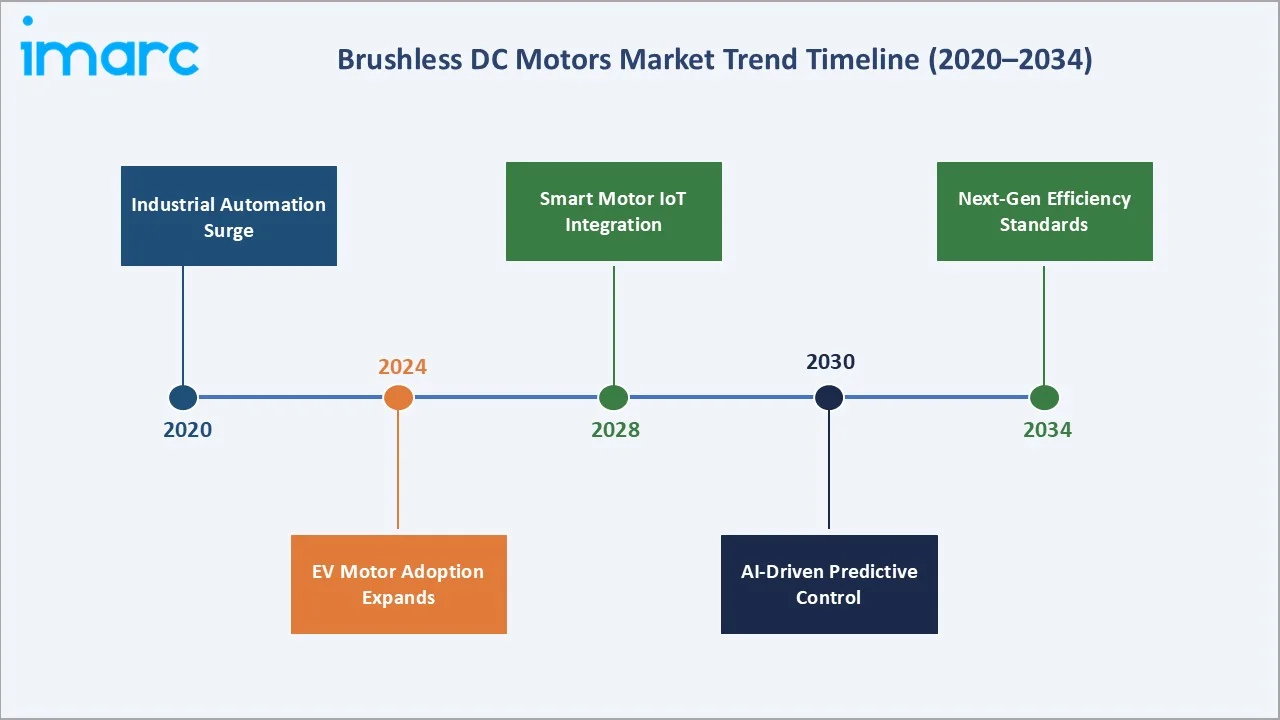

Emerging Market Trends

1. Accelerating Industrial Automation and Cobots Adoption

Collaborative robot deployments are expanding BLDC motor demand beyond traditional automotive and semiconductor manufacturing. BLDC motors are the preferred actuator due to their compactness, noise-free operation, and precise speed-torque control capabilities critical for human-robot collaboration.

2. EV and e-Mobility Platform Electrification

Every new EV platform displacing an internal combustion engine vehicle creates 6-14 new BLDC motor demand points across traction, HVAC, electric power steering, and braking systems. Major automakers including Toyota, Volkswagen, and GM are each committing multi-billion-dollar EV investment programs targeting volume ramp through 2030, sustaining a structurally growing procurement pipeline for BLDC motor suppliers.

3. Sensorless Control and FOC Algorithm Advancement

Sensorless field-oriented control (FOC) algorithms are eliminating the Hall-effect sensor requirement in many BLDC motor applications. This advancement is expanding BLDC motor adoption in cost-sensitive appliance and HVAC applications where traditional sensor-based systems were economically uncompetitive.

4. Smart Motor and Predictive Maintenance Integration

IoT-enabled BLDC motor systems with embedded vibration, temperature, and current sensors are enabling real-time health monitoring and predictive maintenance. Industry 4.0 adoption is driving procurement of smart motor solutions. Manufacturers such as Nidec and Siemens are embedding communication protocols like IO-Link and EtherCAT directly into motor drive packages.

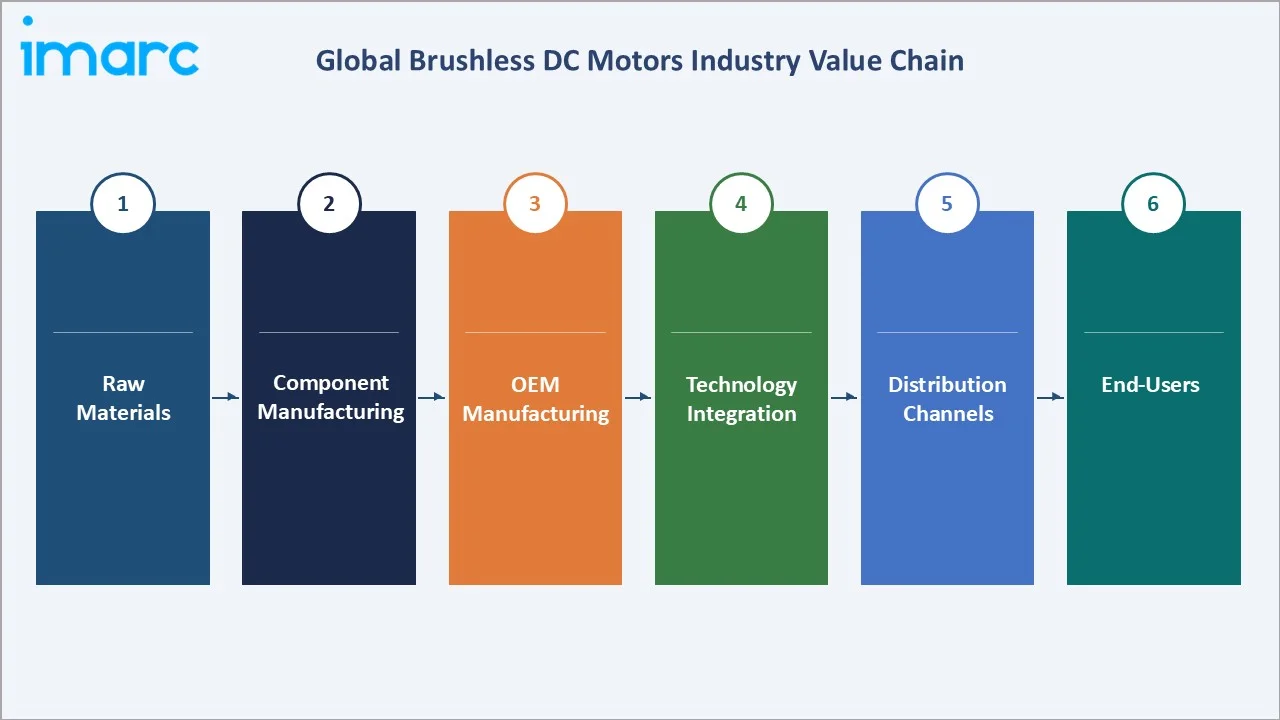

Industry Value Chain Analysis

The global brushless DC motors value chain comprises six interconnected stages, beginning with raw material sourcing and component manufacturing, followed by motor design, assembly, and system integration, each characterized by varying cost structures, competition, and supplier dependencies.

|

Stage |

Key Players / Activities |

|

Raw Materials |

NdFeB magnet suppliers, silicon steel lamination producers, copper wire manufacturers (China, Japan, Germany) |

|

Component Manufacturing |

Stator winding producers, rotor assembly specialists, encoder and Hall-effect sensor manufacturers |

|

OEM Manufacturing |

Nidec, Maxon, Allied Motion, Moog, Portescap, Oriental Motor, Siemens, ABB |

|

Technology Integration |

Drive controller suppliers (TI, Infineon), IoT platform integrators, servo system integrators |

|

Distribution Channels |

Industrial distributors (Grainger, RS Components), OEM-direct sales, e-commerce B2B platforms |

|

End Users |

Industrial automation, automotive/EV, aerospace, medical devices, consumer electronics, HVAC |

At later stages, distribution, customization, and end-user installation play critical roles, where application-specific requirements drive differentiation. These stages involve distinct margin profiles and ongoing technology investments, shaping competitive positioning and long-term growth within the brushless DC motors market.

Technology Landscape in the Brushless DC Motors Industry

Permanent Magnet Technology

Neodymium-iron-boron (NdFeB) magnets remain the dominant permanent magnet material, offering superior energy density enabling compact, high-power motor designs. Samarium-cobalt (SmCo) magnets are gaining traction in high-temperature aerospace and defense applications above 150°C operating environments, where NdFeB demagnetization risk is prohibitive.

Materials Innovation

Soft magnetic composite (SMC) materials are enabling 3D flux path stator designs not achievable with traditional laminated silicon steel. SMC adoption reduces eddy current losses at high frequencies. Amorphous and nanocrystalline core materials are further advancing efficiency in premium-tier industrial servo motors through 2034.

Smart Connectivity and IoT Integration

BLDC motor platforms are increasingly embedding IO-Link, EtherCAT, PROFINET, and CAN-bus communication interfaces, enabling real-time diagnostics and seamless integration into Industry 4.0 factory networks. Nidec's industrial motor platforms and Siemens SIMOTICS series exemplify this trend, offering integrated condition monitoring as a standard embedded feature from 2024 onward.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Inner Rotor Brushless DC Motors | 66.9% | 2025 |

| Power Rating | 0 -750 Watts | 50.7% | 2025 |

| End Use Industry | Industrial Machinery | 25.1% | 2025 |

| Region | Asia Pacific | 51.6% | 2025 |

By Product Type

Inner Rotor Brushless DC Motors dominate with a 66.9% revenue share in 2025. Inner rotor designs deliver superior torque density, higher maximum RPM, and better thermal management via direct stator-to-housing heat transfer paths. These characteristics make them the preferred platform for industrial servo drives, CNC machining centers, robotic joint actuators, and precision medical equipment worldwide.

To access detailed market analysis, Request Sample

By Power Rating

The 0-750 Watts segment holds the dominant 50.7% revenue share in 2025. This segment's primacy reflects the massive installed base of BLDC motors in consumer electronics cooling, computer peripherals, small home appliances, medical diagnostics, and warehouse robotics applications globally, where sub-750W ratings are the design requirement.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

51.6% |

China electronics manufacturing, India PLI scheme, ASEAN EV adoption, industrial automation |

|

North America |

20.8% |

U.S. defense & aerospace, reshoring manufacturing, EV adoption, EISA efficiency mandates |

|

Europe |

17.6% |

EU Ecodesign IE3/IE4 mandates, German industrial automation, EV powertrain production |

|

Latin America |

5.4% |

Brazil automotive sector, growing e-mobility, expanding industrial manufacturing base |

|

Middle East & Africa |

4.6% |

GCC industrial diversification, renewable energy systems, HVAC and building automation |

Asia Pacific commands 51.6% global revenue share in 2025. China is the single most important national market, combining the world's largest electronics manufacturing complex with aggressive EV production scaling. India's Production Linked Incentive (PLI) scheme for white goods and electric vehicles is creating structured procurement demand for domestically manufactured BLDC motor components. Asia Pacific is also forecast to maintain the fastest regional growth rate through 2034.

North America holds 20.8% of global revenue, anchored by U.S. defense, aerospace, and advanced manufacturing sectors. The CHIPS and Science Act's USD 52 billion semiconductor investment is spurring adjacent demand for precision BLDC-driven semiconductor equipment. EISA efficiency mandates are accelerating brushed-to-brushless motor replacement in industrial applications nationwide.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Nidec Corporation |

Nidec, Embraco, Leroy-Somer |

Leader |

Global scale, precision micro-motors |

|

Maxon Group |

Maxon, Escon |

Leader |

Swiss precision, medical & aerospace |

|

Allied Motion Technologies Inc. |

Heidrive, Tulsa, Megaflux |

Leader |

Custom servo solutions, diverse verticals |

|

Moog Inc. |

Moog, Animatics |

Leader |

Defense, aerospace, precision control |

|

Oriental Motor Co., Ltd. |

Oriental Motor, Vexta |

Leader |

Japan/Asia Pacific industrial motors |

|

Siemens AG |

SIMOTICS, Flender |

Challenger |

IIoT integration, industrial automation |

|

ABB Ltd. |

ABB Motors, Baldor |

Challenger |

High-efficiency industrial motors, global |

|

Portescap |

Portescap |

Challenger |

Medical & dental miniaturized motors |

|

Kollmorgen Corporation |

Kollmorgen, AKM |

Emerging |

Servo motor innovation, robotics focus |

The global brushless DC motors market's competitive landscape is moderately fragmented. Global technology leaders compete alongside regional specialists and high-volume Asian manufacturers. Leading players differentiate on precision engineering, IoT integration, distribution reach, and application specific engineering capabilities.

Key Company Profiles

Nidec Corporation

Nidec Corporation is the global leader in small precision motors, headquartered in Kyoto, Japan. Founded in 1973, it operates across automotive, appliance, industrial, and commercial sectors with subsidiaries in over 40 countries and annual motor production exceeding 1 billion units.

- Product & Platform Portfolio: Nidec's BLDC motor portfolio spans precision motors for HDD and data center cooling, traction motors for EV platforms, industrial servo motors via Leroy-Somer, and HVAC-grade EC motor platforms across residential and commercial applications globally.

- Recent Developments: In December 2022, Nidec Corporation developed a single-phase, low-vibration, and cost-efficient brushless DC motor designed for electric fans. The innovation aims to deliver improved durability and noise performance while addressing the higher cost limitations of traditional three-phase BLDC motors.

- Strategic Focus: Nidec's strategy centers on EV traction motor market share capture, precision micro-motor leadership in data center and consumer electronics, and vertical integration of motor drive and thermal management systems across its subsidiary network globally.

Maxon Group

Maxon Group is a Swiss precision motor and drive systems manufacturer headquartered in Sachseln, Switzerland. Founded in 1961, Maxon serves demanding applications across medical technology, robotics, aerospace, and industrial automation.

- Product & Platform Portfolio: Maxon's BLDC motor portfolio includes the EC series (electronically commutated), EC-i flat motors, and EC-4pole platform covering from 1.2mm to 90mm diameter configurations for surgical tools, robotic joints, dental equipment, and aerospace actuation systems.

- Recent Developments: In 2026, maxon Group expanded its ECX PRIME series with a new 22mm BLDC motor, offering higher torque and high-speed performance for compact, precision-driven applications. The enhanced series is designed to deliver stable speed control, improved dynamic response, and greater efficiency across a wide power range.

- Strategic Focus: Maxon focuses on ultra-premium precision motor platforms for life sciences, aerospace, and collaborative robotics markets where performance specifications prohibit commodity motor substitution, sustaining premium pricing and margins through deep application engineering partnerships.

Allied Motion Technologies Inc.

Allied Motion Technologies Inc. is a U.S.-based global designer and manufacturer of precision motors and motion systems, headquartered in Amherst, New York. The company operates 18 Technology Units. 20 Production Units, 16 Direct Sales Offices across North America, Europe, and Asia serving industrial, vehicle, and medical markets.

- Product & Platform Portfolio: Allied Motion's BLDC motor platforms include the Heidrive servo series, Megaflux direct-drive torque motors, Tulsa Winch electric drive systems, and compact DC motor platforms from the Globe Motors division serving automotive and medical device applications.

- Recent Developments: Allied Motion completed the acquisition of Ormec Systems in 2021 to strengthen its servo control and motion system integration capabilities, expanding its value-added solution offering for industrial automation and semiconductor equipment customers across North America.

- Strategic Focus: Allied Motion's strategy emphasizes custom-engineered motor and motion solutions for applications where standard catalogue products are inadequate, targeting industrial automation, medical robotics, and specialty vehicle electrification as core vertical growth platforms.

Market Concentration Analysis

The global brushless DC motors market exhibits moderate fragmentation. The top five players Nidec Corporation, Maxon Group, Allied Motion Technologies Inc., Moog Inc., Oriental Motor Co., Ltd., Siemens AG collectively account for an estimated 25-35% of global market revenue in 2025.

The market is experiencing a bifurcated competitive dynamic. At the premium OEM tier, consolidation is occurring around application engineering capability, IoT platform integration, and precision manufacturing certification (ISO 13485 for medical, AS9100 for aerospace). Simultaneously, Chinese manufacturers are reaching advanced quality benchmarks, intensifying price competition across mid-tier industrial automation and consumer electronics segments through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Higher power rating segments (3 kW-75 kW and above 75 kW) are the fastest-growing BLDC motor categories, driven by EV traction motor scaling and heavy industrial automation platform expansion. Outer rotor configurations in drone and e-mobility applications represent the highest-growth product type within the forecast period.

Emerging Market Expansion

India represents the highest-potential emerging market. The PLI scheme for electric vehicles and advanced chemistry cell batteries is driving domestic EV production and motor manufacturing investment. Southeast Asia's electronics manufacturing migration from China-plus-one strategies, GCC industrial diversification programs, and Sub-Saharan Africa's expanding manufacturing base collectively represent significant volume opportunities for BLDC motor suppliers with established regional distribution infrastructure.

Venture and Strategic Investment Trends

Strategic acquisitions are reshaping the competitive landscape. Investments in rare-earth magnet alternatives (ferrite and ferrite-composite compounds), sensorless motor control AI algorithms, and direct-drive integrated motor-controller platforms are the primary focus areas for corporate R&D and venture capital in the brushless DC motors industry through 2034. Axial flux motor architecture startups are attracting investment as a disruptive next-generation platform.

Future Market Outlook (2026-2034)

The global brushless DC motors market forecast projects steady value expansion from USD 5.8 Billion in 2025 to USD 6.0 Billion by 2034. This low but stable growth rate reflects a mature, essential technology market underpinned by structural electrification megatrends, partially offset by price deflation in high-volume consumer electronics segments and competitive market dynamics.

Three key shifts will reshape the brushless DC motors market through 2034. EV platform proliferation will embed BLDC motors as a standard drivetrain component across automotive, commercial vehicle, and two-wheeler segments globally. Smart motor-drive integration will become a procurement baseline as Industry 4.0 adoption advances, making IoT connectivity and predictive diagnostics standard embedded features rather than premium add-ons.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with brushless DC motors industry stakeholders, including engineering directors at OEM motor manufacturers, procurement managers at industrial automation integrators, purchasing leads at EV platform manufacturers, and institutional investors in electrification technology. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include International Federation of Robotics (IFR) World Robotics reports, IEA Global EV Outlook 2024, EU Ecodesign Regulation publications, IEC 60034 efficiency standard documentation, company annual reports, trade publications including Design News, Motion Control & Motor Association (MCMA) data, and regional industrial association databases from Japan, Germany, China, and the United States.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating industrial output indices, EV production volume forecasts, energy efficiency regulation implementation timelines, and historical motor market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for rare-earth supply chain volatility and macroeconomic uncertainty through 2034.

Brushless DC Motors Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Inner Rotor Brushless DC Motors, Outer Rotor Brushless DC Motors |

| Power Ratings Covered | 0-750 Watts, 750 Watts to 3 kW, 3 kW-75 kW, Above 75 kW |

| End Use Industries Covered | Industrial Machinery, Automotive, Consumer Electronics, Healthcare, Aerospace and Defense, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Nidec Corporation, Maxon Group, Allied Motion Technologies Inc., Moog Inc., Oriental Motor Co. Ltd., Siemens AG, ABB Ltd., Portescap, Kollmorgen Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the brushless DC motors market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global brushless DC motors market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the brushless DC motors industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brushless DC Motors Market Report Report

The global brushless DC motors market was valued at USD 5.8 Billion in 2025, driven by industrial automation growth, EV adoption, and expanding consumer electronics and medical device applications worldwide.

The market is projected to reach USD 6.0 Billion by 2034, supported by electrification megatrends, efficiency regulations, and smart motor platform integration globally.

Inner Rotor BLDC Motors lead with a 66.9% share in 2025, favored for superior torque density, high-speed capability, and thermal management advantages across industrial servo, robotics, and precision automation applications.

The 0-750 Watts segment holds the largest 50.7% share in 2025, reflecting dominant adoption in consumer electronics, medical devices, computer cooling, small appliances, and compact industrial automation globally.

Asia Pacific dominates with a 51.6% share in 2025. China's electronics manufacturing scale, India's PLI scheme, and ASEAN industrial growth underpin its commanding regional leadership through the forecast period.

Key drivers include industrial automation and robotics expansion, global EV production scaling, EU Ecodesign and EISA energy efficiency mandates, medical device miniaturization, and drone and advanced air mobility platform growth globally.

Major players include Nidec Corporation, Maxon Group, Allied Motion Technologies Inc., Moog Inc., Oriental Motor Co. Ltd., Siemens AG, ABB Ltd., Portescap, Kollmorgen Corporation.

Electric vehicle and e-mobility applications are the fastest-growing end-use category, as each EV platform requires multiple BLDC motors for traction, cooling, steering, and auxiliary subsystems across all vehicle classes manufactured.

Key opportunities include EV traction motor supply chain integration, smart IoT-enabled motor platforms, medical robotics miniaturized motor development, rare-earth alternative magnet R&D, and Asia Pacific manufacturing capacity expansion through 2034.

EU Ecodesign Regulation IE3 and IE4 mandates are accelerating brushed-to-brushless motor replacement across European industrial applications, creating structured replacement demand and premium product market expansion for high-efficiency BLDC motor suppliers.

The concentration of neodymium supply in China creates price volatility and supply chain risks, prompting increased R&D investment in alternative solutions such as ferrite composite magnets and rare-earth-free motor architectures globally.

Key trends include sensorless field-oriented control (FOC) algorithm advancement, IoT-embedded smart motor platforms, axial flux motor architecture scaling, and AI-driven predictive maintenance integration across industrial and automotive applications through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)