Building Information Modeling (BIM) Market Size, Share, Trends and Forecast by Offering Type, Deployment Mode, Application, End Use Sector, End User, and Region 2026-2034

Global Building Information Modeling (BIM) Market Size, Share, Trends & Forecast 2026-2034

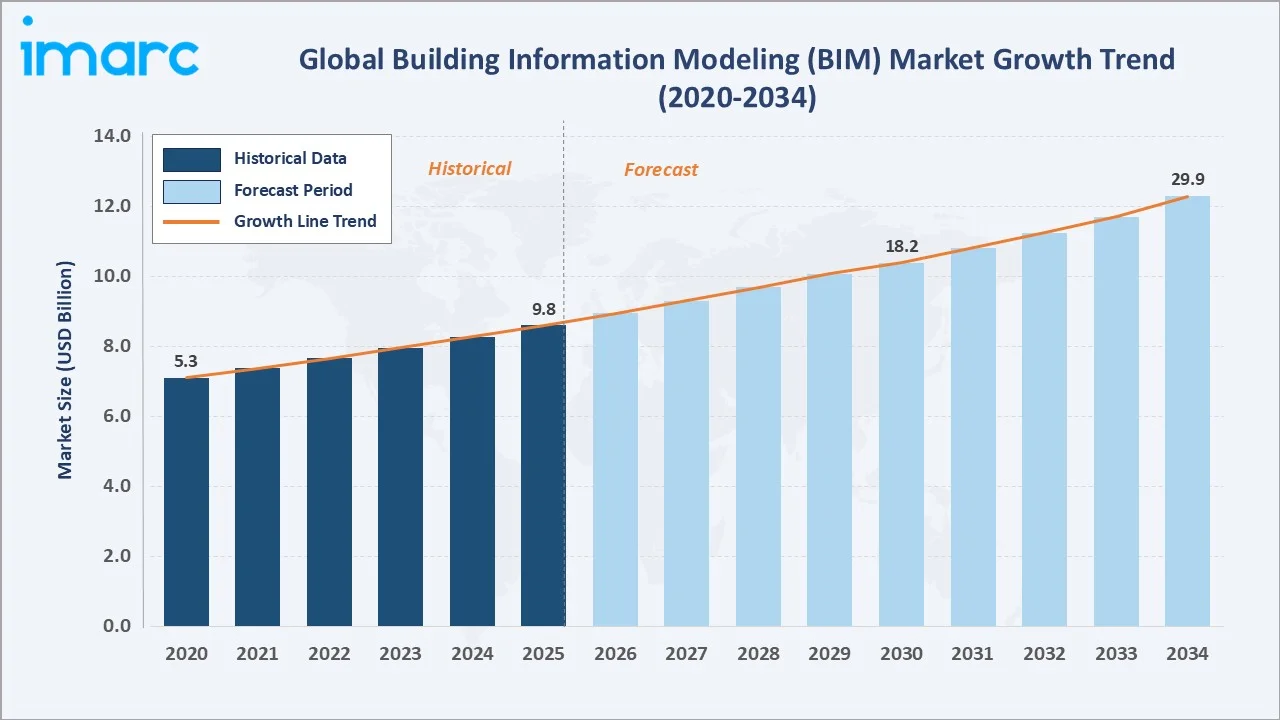

The global building information modeling (BIM) market was valued at USD 9.8 Billion in 2025 and is projected to reach USD 29.9 Billion by 2034, expanding at a CAGR of 13.20% during the forecast period 2026-2034. The BIM market growth is driven by government mandates for digital project delivery, rapid adoption of cloud-based and AI-integrated platforms, and growing emphasis on lifecycle cost efficiency across architecture, engineering, and construction (AEC) workflows.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.8 Billion |

|

Forecast Market Size (2034) |

USD 29.9 Billion |

|

CAGR (2026-2034) |

13.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region (2025) |

North America (36.4%) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~15.4%) |

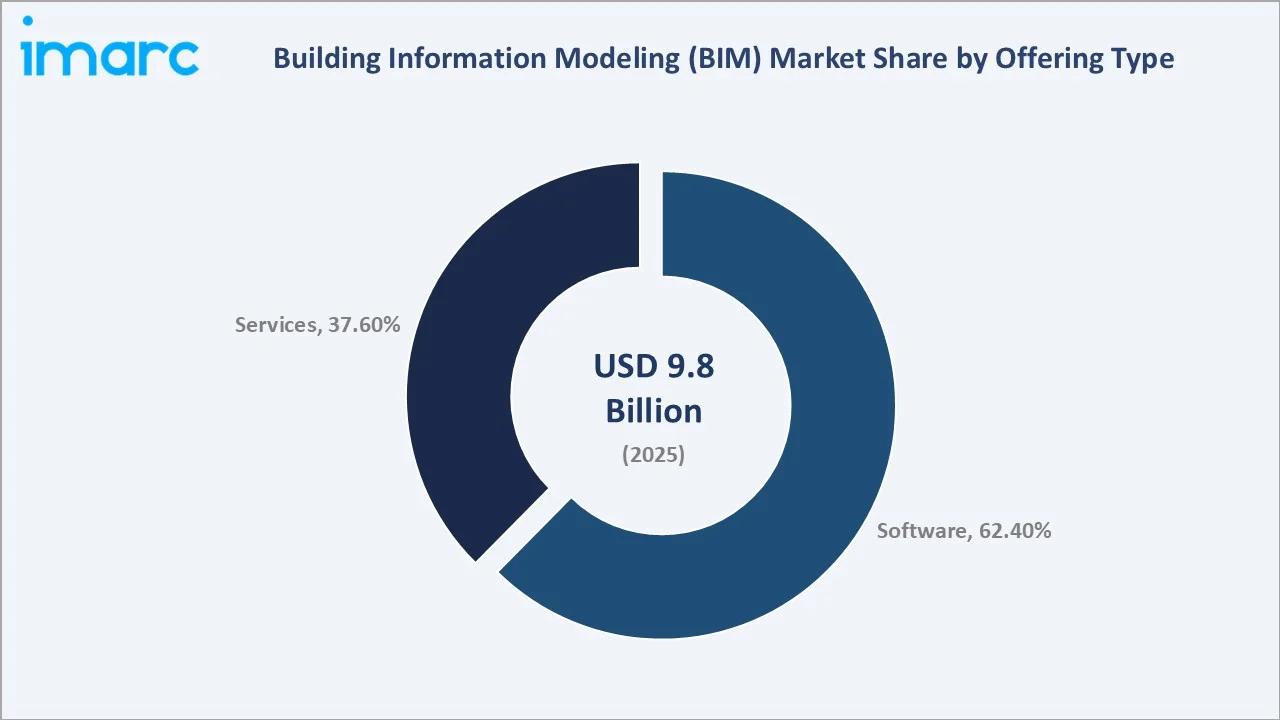

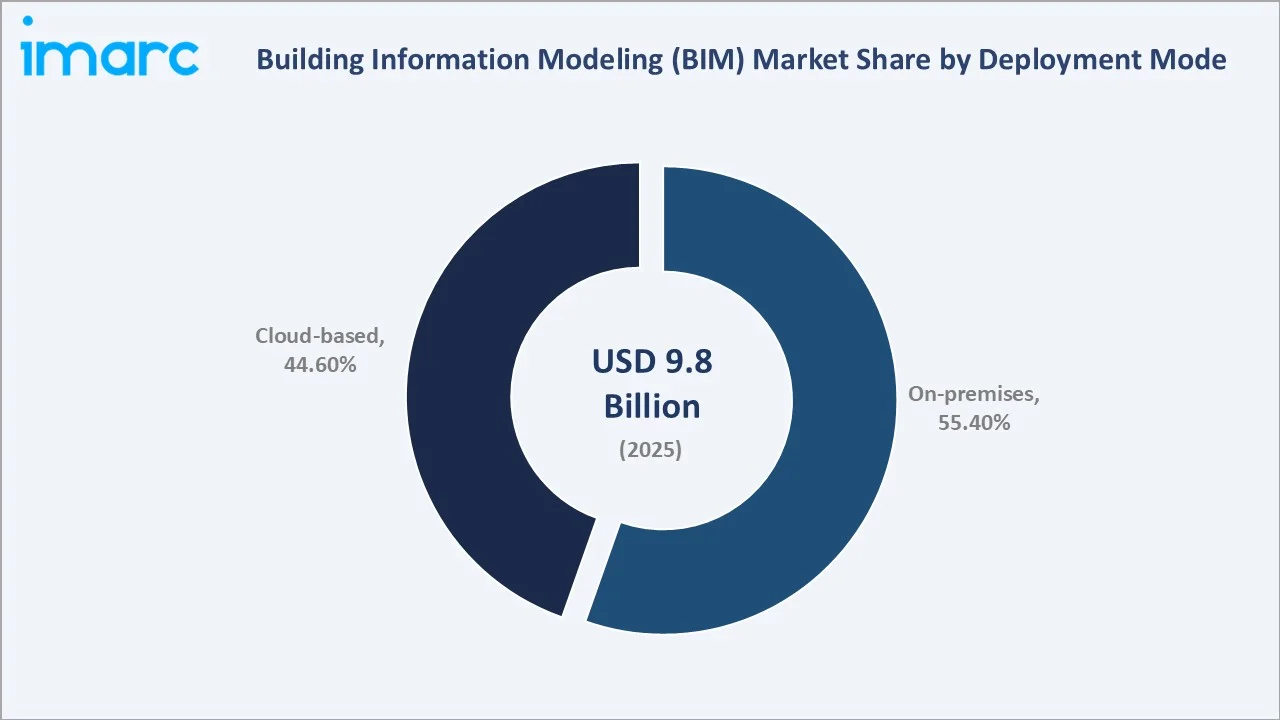

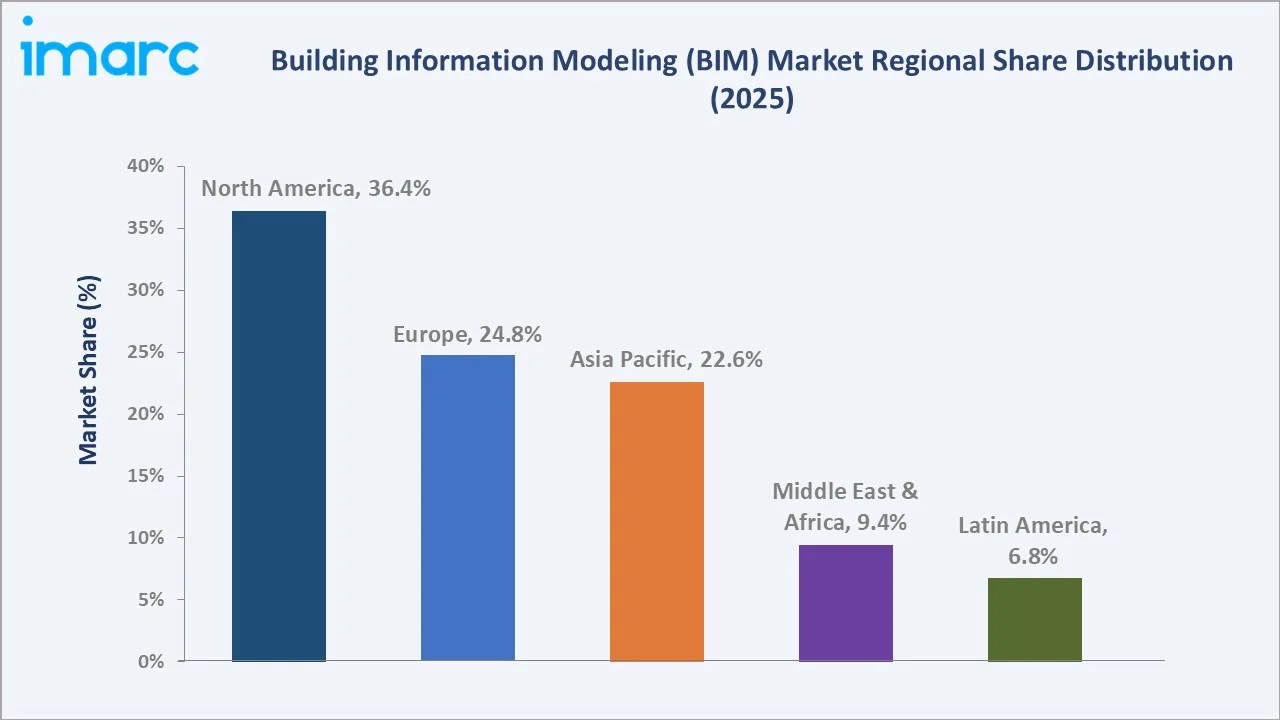

North America leads regional demand with a 36.4% share in 2025. Software dominates offerings at 62.4%, and on-premises deployment leads with a 55.4% share. Key industry participants include Autodesk Inc., Bentley Systems, Trimble Inc., Nemetschek SE, Dassault Systèmes SE, Hexagon AB, AVEVA Group Plc (Schneider Electric), AECOM, ABB Ltd., and Beck Technology Ltd.

To get more information on this market, Request Sample

The Building Information Modeling (BIM) market is witnessing strong growth as digital transformation reshapes the construction and infrastructure sectors. It enhances project visualization, coordination, and lifecycle management through intelligent 3D modeling and data integration.

Executive Summary

The global BIM market continues to demonstrate robust double-digit expansion, underpinned by the digital transformation of the AEC industry, mandatory government BIM policies, and the proliferation of cloud-native and AI-augmented modeling platforms. Valued at USD 9.8 Billion in 2025, the market is forecast to reach USD 29.9 Billion by 2034, at a CAGR of 13.20%.

Among key growth drivers, government mandates requiring BIM for public infrastructure projects in the U.S., UK, EU, Singapore, and emerging Asian markets remain the primary catalyst. In June 2025, Autodesk launched the BIM Package for Viksit Bharat, a specialized BIM suite for Indian public sector engineers and architects. Software accounted for 62.4% of the market in 2025, reflecting deep demand for design, clash detection, simulation, and lifecycle management tools.

North America retains market leadership with a 36.4% share (2025), while Asia Pacific is the fastest-growing region at a CAGR of ~15.4%, fueled by China's 14th Five-Year Plan, India's Smart Cities Mission, and Singapore's mandatory BIM submission policy for public projects above SGD 5 million. AI-enhanced automation, digital twin integration, and open-data interoperability are key themes reshaping the competitive landscape through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Offering Type) |

Software - 62.4% share (2025) |

|

Largest Segment (Deployment Mode) |

On-premises - 55.4% share (2025) |

|

Leading Region |

North America - 36.4% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific - CAGR ~15.4% (2026-2034) |

|

Top Companies |

Autodesk, Bentley Systems, Trimble, Nemetschek, Dassault Systèmes, Hexagon AB |

|

Market Opportunity |

Cloud-based BIM projected at ~USD 16.6 Billion by 2034 |

Key Analytical Observations Supporting The Above Data:

- Software dominates at 62.4% (2025), driven by demand for design, visualization, clash detection, and simulation tools. Autodesk Revit, Bentley MicroStation, and Nemetschek Archicad are widely deployed across commercial and infrastructure projects globally.

- On-premises deployment leads at 55.4% (2025), reflecting organizations’ preference for enhanced data security, control over sensitive project information, and integration with legacy systems in large-scale construction and infrastructure projects. Cloud-based deployment holds 44.6% and is rapidly expanding.

- North America generates 36.4% of global revenues (2025), bolstered by federal and state mandates, the presence of market leaders Autodesk, Bentley, and Trimble, and high awareness of lifecycle cost management practices among AEC stakeholders.

- Asia Pacific is the fastest-growing region (CAGR ~15.4%), driven by China's infrastructure investment programs, India's Viksit Bharat initiative, and Singapore's statutory BIM submission requirements on public projects.

Global BIM Market Overview

Building Information Modeling (BIM) is a digital representation process for the physical and functional characteristics of a facility, enabling coordinated, reliable information about a building project from design through construction and operations. Unlike traditional CAD drafting, BIM creates an intelligent 3D model linked to a live database of project properties, enabling real-time clash detection, cost estimation, scheduling, and lifecycle asset management.

The BIM market encompasses software platforms, implementation and consulting services, training programs, and cloud-based collaborative environments. According to 2023 survey data, BIM adoption in the U.S. is widespread, with 74% of contractors, 67% of engineers, and 70% of architects actively using the technology. Dodge Construction Network stated that the use of clash detection can reduce change orders by an average of 40%.

The BIM market outlook is increasingly shaped by four converging dynamics: regulatory mandates converting BIM from a voluntary practice into a statutory requirement; the migration of desktop tools to cloud-native SaaS platforms; integration with AI, digital twins, and IoT for real-time building performance analytics; and growing pressure from ESG-focused investors and green building certifications demanding energy simulation and lifecycle carbon modeling.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- Government BIM Mandates: Public infrastructure agencies in the U.S., UK, EU member states, Singapore, UAE, and Saudi Arabia (Vision 2030) now require BIM for publicly funded projects. The Singaporean government has mandated the use of Building Information Modeling (BIM) for construction projects with a gross floor area exceeding 5,000 m².

- Digital Twin & AI Integration: In June 2025, Autodesk launched an India-focused BIM suite integrated with AI and generative design to improve design efficiency, reduce rework, and ensure compliance with local construction standards.

- Smart City & Infrastructure Investment: China's 14th Five-Year Plan channels capital toward new urban clusters; India's Smart Cities Mission mandates BIM-ready documentation on tender packages; and the U.S. Bipartisan Infrastructure Law allocates over USD 1.2 trillion to roads, bridges, and transit.

- Sustainability & Green Building Certifications: LEED, BREEAM, and EDGE certifications increasingly require energy performance simulation and embodied-carbon analysis, capabilities natively supported by BIM platforms. The push for net-zero buildings is converting sustainability compliance into a structural demand driver for BIM software upgrades.

Market Restraints

- High Initial Implementation Costs: BIM tools such as Autodesk Revit and Bentley MicroStation carry significant licensing and ongoing subscription fees. For small and medium-sized AEC firms, the upfront investment in software, hardware, and training remains a substantial barrier to adoption.

- Interoperability Challenges: Fragmented file formats (RVT, IFC, DGN, DWG) across competing BIM platforms create friction in multi-disciplinary project teams. Despite the Autodesk-Nemetschek interoperability deal signed in April 2024 and Bentley Systems's iTwin open-source initiative, data translation errors remain a significant workflow pain point.

- Skills Gap & Training Barriers: A shortage of BIM-proficient professionals, especially in emerging markets, limits deployment velocity. Industry surveys indicate 87% of AEC firms cite skills gaps as a primary barrier to BIM adoption, while workforce training timelines extend project onboarding periods.

Market Opportunities

- Expansion into Emerging Markets: Asia Pacific, the Middle East, and Latin America collectively represent the highest-growth opportunity. India's BIM Package for Viksit Bharat (January 2025) and Saudi Arabia's Vision 2030 digital construction agenda are catalyzing rapid adoption in previously underserved markets with large construction pipelines.

- BIM for Facility Management (FM) & Operations: Post-construction BIM adoption for FM, predictive maintenance, and building performance monitoring is emerging as a major growth vector. Connecting BIM models to IoT sensor networks enables real-time occupancy analytics, energy optimization, and capital planning.

- Open-Data & Interoperability Ecosystems: The Autodesk-Nemetschek interoperability agreement and Bentley's iTwin open-source database are creating data-sharing ecosystems that expand total addressable BIM spend by removing user frustration with siloed platforms.

Market Challenges

- Cybersecurity of Cloud-Hosted Models: As BIM workflows migrate to cloud platforms hosting sensitive project data, intellectual property, and infrastructure schematics, cybersecurity risks are intensifying. High-profile breaches in construction data management are prompting stricter procurement security requirements, particularly for government contracts.

- Standardization Across Jurisdictions: Divergent national BIM standards (ISO 19650 vs. country-specific frameworks) create compliance complexity for multinational AEC firms. Harmonization efforts are ongoing but slow, increasing the cost of operating BIM workflows across multiple regulatory environments.

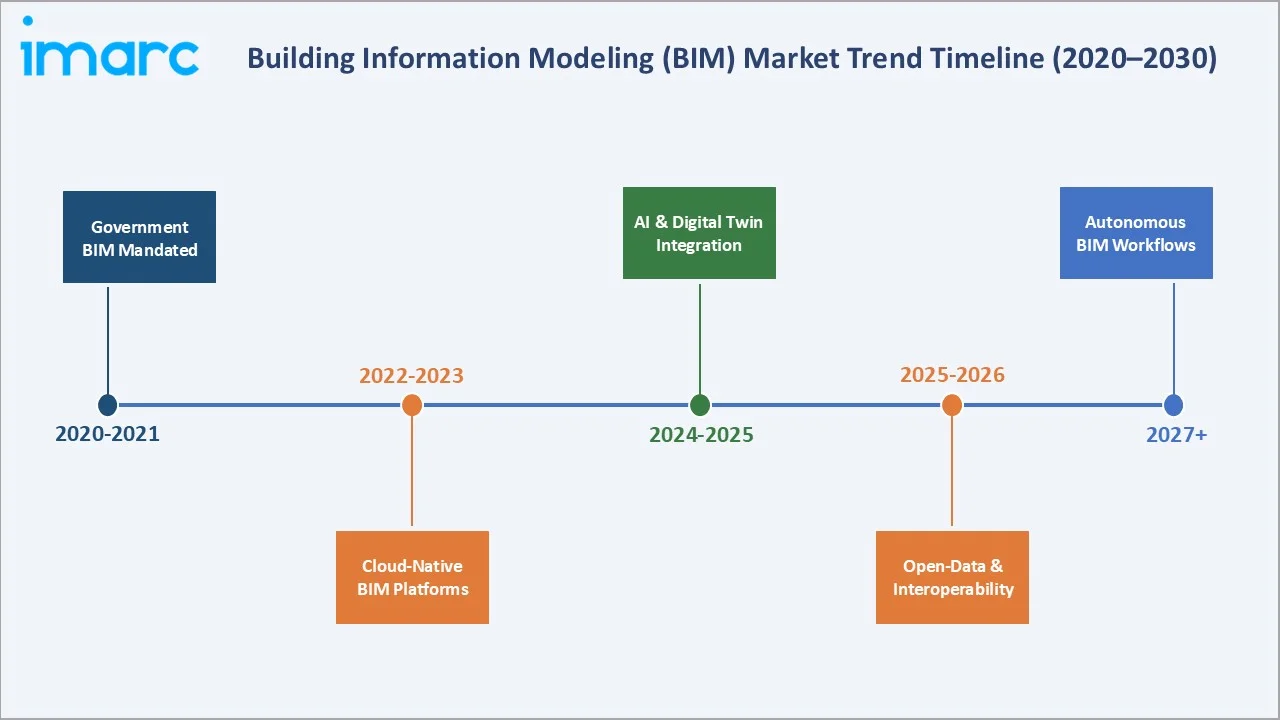

Emerging BIM Market Trends

1. AI-Augmented BIM and Generative Design

Autodesk rolled out Revit 2026 in April 2025, featuring reality-capture mesh imports and an accelerated graphics architecture for smoother model navigation. Trimble introduced Tekla Structures 2025 in June 2025 with AI-enhanced fabrication drawing automation and expanded Live Collaboration capabilities.

2. Cloud-Native BIM and Real-Time Collaboration

Cloud solutions held 44.6% of the BIM market in 2025 and are the fastest-growing deployment mode. The Autodesk-Nemetschek interoperability deal (April 2024) connected Nemetschek's dTwin, Bluebeam Cloud, BIMcloud, and BIMplus to Autodesk's Forma, Fusion, and Flow cloud platforms, enabling seamless data flow between the two largest AEC software ecosystems.

3. Digital Twins and IoT-Connected BIM

Intermodal Terminal Company (ITC) selected Hexagon’s HxGN EAM solution to support its Somerton Intermodal Terminal project in Melbourne, aimed at becoming Australia’s largest and first fully electric rail terminal. By 2034, digital twin-enabled BIM is projected to be standard practice on major commercial and infrastructure projects, significantly expanding the addressable market for FM and operations-phase BIM services.

4. Government Mandates Expanding to Emerging Markets

In June 2025, Autodesk launched the BIM Package for Viksit Bharat, tailored for Indian government engineers and architects. Nemetschek Group signed a Memorandum of Understanding with Nesma Infrastructure & Technology (NIT) in Saudi Arabia in June 2025, advancing Vision 2030’s construction digitalization agenda.

5. Open-Data Ecosystems and Interoperability Partnerships

Autodesk championed the Alliance for Open USD (AOUSD), joined by Apple, Siemens, Sony, Trimble, and Hexagon, to standardize data exchange across design and engineering workflows. These initiatives are reducing friction in multi-vendor BIM environments, expanding total addressable spend by making BIM adoption more accessible to smaller firms and enabling more seamless public-sector project delivery workflows globally.

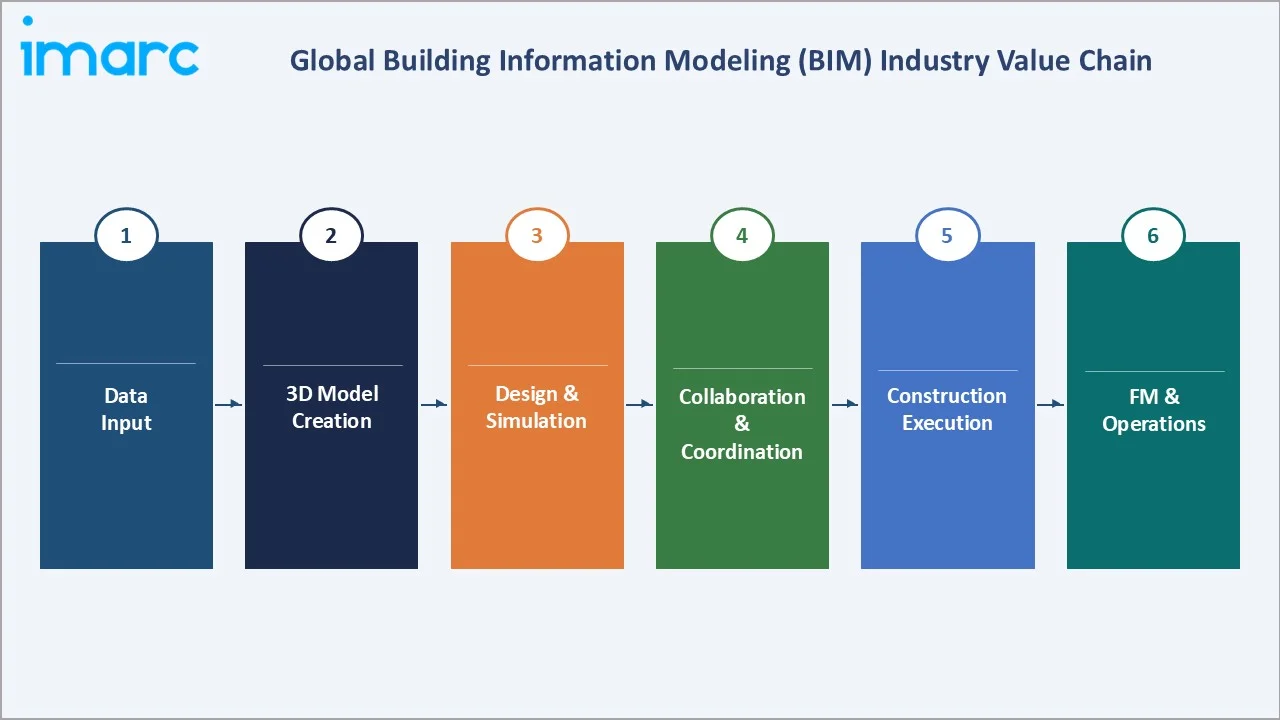

Industry Value Chain Analysis

The BIM industry value chain spans from raw data inputs and sensor feeds through model creation, simulation, collaboration, construction execution, and post-occupancy facility management. Each stage is served by specialized software, services, and hardware providers whose outputs directly influence project quality, cost efficiency, and compliance.

|

Stage |

Key Activities & Examples |

|

Data Input & Capture |

Survey data, point clouds, LiDAR scans, GIS data; laser-scan integration (Trimble, Hexagon) |

|

3D Model Creation |

Architectural, structural, MEP modeling; Autodesk Revit, Bentley MicroStation, Archicad, Allplan |

|

Design & Simulation |

Energy analysis, clash detection, cost estimation, Autodesk Forma, AVEVA, Autodesk Navisworks |

|

Collaboration & Coordination |

Common Data Environments (CDEs), BIM model sharing; Autodesk Construction Cloud (ACC), Bentley ProjectWise, Bluebeam Cloud |

|

Construction Execution |

Site coordination, prefabrication support, progress monitoring; Trimble, Autodesk Build/Procore/Trimble Connect, AVEVA |

|

FM & Operations |

Asset management, predictive maintenance, digital twins; Hexagon, ABB, AVEVA, Siemens, Autodesk Tandem, IBM Maximo |

|

End Users |

Architects/Engineers, Contractors/Developers, Government agencies, Facility managers |

Technology Landscape in the BIM Industry

AI and Generative Design

AI is embedded across BIM workflows, from parametric design optimization to automated code compliance checking. Autodesk's generative design tools evaluate thousands of design options against structural, cost, and sustainability constraints. A study by Autodesk indicates that digital material take-offs can reduce construction waste by up to 25% compared to traditional manual methods.

Cloud Computing and SaaS BIM

Cloud BIM enables new deployments via SaaS environments, supporting real-time multi-disciplinary collaboration across geographic boundaries. Subscription economics lower the initial barrier to adoption for small and mid-sized AEC firms. Cloud also enables continuous feature updates, AI service delivery, and integration with enterprise resource planning (ERP) and project management systems.

Digital Twins and IoT Integration

BIM models are evolving into living digital twins connected to IoT sensor networks. This enables real-time energy monitoring, predictive maintenance scheduling, and occupancy-based space optimization throughout asset lifecycles. Integration with IoT and digital twin frameworks supports 33% of smart building initiatives globally.

Reality Capture and Scan-to-BIM

Trimble's laser-scan integration module and Autodesk Revit 2026's reality-capture mesh imports reflect the mainstreaming of scan-to-BIM workflows. The scan-to-BIM market is growing rapidly as aging building stock across North America and Europe requires digital documentation for retrofit, energy efficiency upgrades, and compliance modeling.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Offering Type |

Software |

62.4% |

2025 |

|

Deployment Mode |

On-premises |

55.4% |

2025 |

|

Application |

Preconstruction |

🔒 |

2025 |

|

End Use Sector |

Commercial |

🔒 |

2025 |

| End User | Architects and Engineers | 🔒 | 2025 |

|

Region |

North America |

36.4% |

2025 |

By Offering Type

The software sub-segment dominates the BIM market with a 62.4% share (2025), driven by demand for design, visualization, clash detection, simulation, and lifecycle management tools. BIM software platforms, including Autodesk Revit, Bentley MicroStation, Nemetschek Archicad, Dassault CATIA, and Trimble Tekla, serve architects, structural engineers, MEP consultants, contractors, and facility managers.

To access detailed market analysis, Request Sample

The services segment (37.6%) encompasses implementation, consulting, training, support, and managed BIM services. Services are the fastest-growing sub-segment as government agencies and construction firms increasingly seek expert guidance to deploy BIM strategies at scale, develop BIM execution plans, train workforces, and ensure compliance with ISO 19650 standards and national BIM frameworks.

By Deployment Mode

The on-premises segment retains a 55.4% share among organizations with stringent data sovereignty, security, or compliance requirements, particularly in government agencies, defense contractors, and utilities managing sensitive infrastructure models

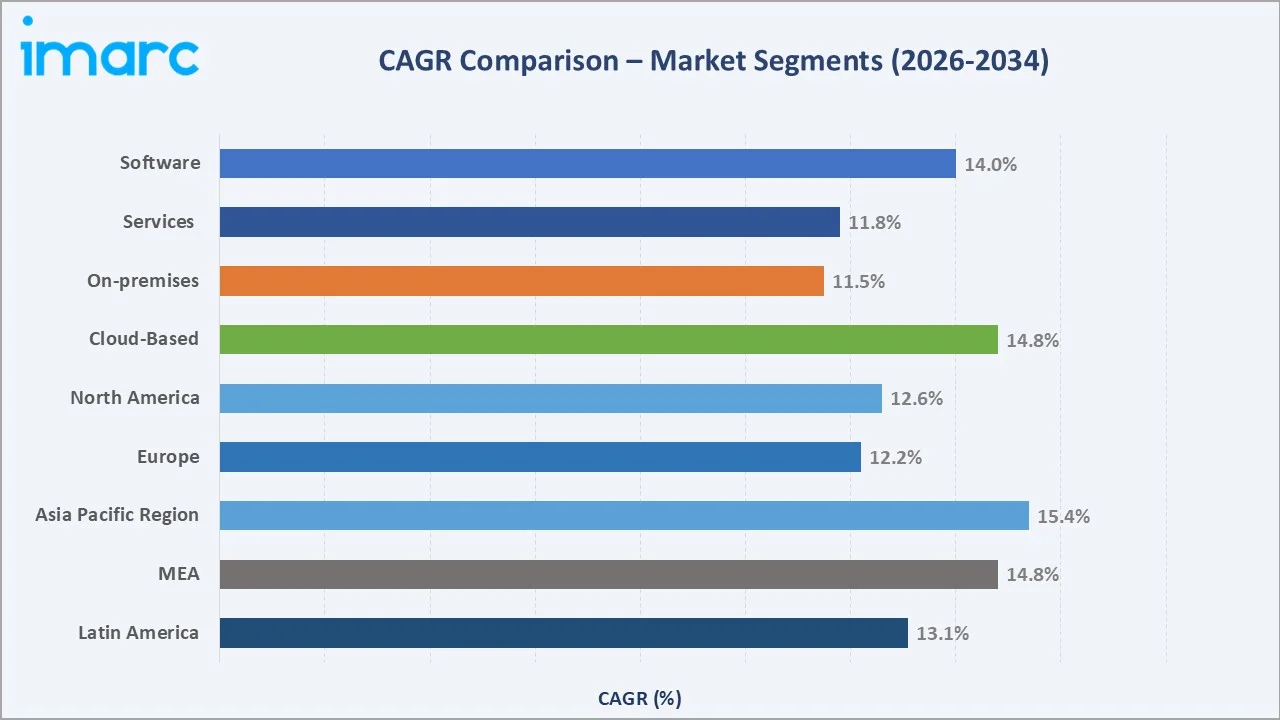

Cloud solutions are expanding at a CAGR of ~14.8% (2026-2034), reflecting growing AEC industry comfort with SaaS hosting and the productivity gains from always-current software. Hybrid deployment models, combining cloud collaboration layers with on-premises model authoring, are emerging as a transitional architecture for large enterprise clients.

Regional Market Insights

North America dominates with a 36.4% share (2025), supported by the federal Buy Clean and BIM mandates, GSA's long-standing BIM guidelines, and the infrastructure investment surge unlocked by the U.S. Bipartisan Infrastructure Law. The U.S. BIM market is valued at approximately USD 2.9 Billion in 2025, driven by commercial real estate, transportation infrastructure, and federal government projects.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Companies |

|

North America |

36.4% |

Federal BIM mandates; smart city investment; infrastructure modernization; digital twin adoption |

U.S. GSA BIM guidelines; state LEED mandates; federal infrastructure law; Canada BIM national strategy |

Autodesk, Bentley Systems, Trimble, Beck Technology |

|

Europe |

24.8% |

EU Green Deal digital construction; ISO 19650 adoption; UK BIM mandate Level 2+; sustainability certifications |

UK BIM Level 2 mandate; EU taxonomy for sustainable investment; Germany BIM roadmap 2025 |

Nemetschek, Hexagon AB, AVEVA, ABB |

|

Asia Pacific |

22.6% |

China 14th Five-Year Plan; India Smart Cities; Singapore mandatory BIM; Japan BIM guideline 2023 |

Singapore BCA mandate (SGD 5M+); Japan MLIT BIM guideline; India BIM adoption under Smart Cities Mission |

Trimble, Bentley, Autodesk APAC, local integrators |

|

Middle East & Africa |

9.4% |

Saudi Vision 2030; UAE smart infrastructure; NEOM project; large-scale urban development pipelines |

UAE Ministry of Infrastructure BIM policy; Saudi MOMRA digital requirements; Qatar QCS standards |

Nemetschek-NIT MoU (Jun 2025), Bentley, Autodesk |

|

Latin America |

6.8% |

Brazil urban housing programs; Mexico infrastructure investment; growing AEC digitalization |

Brazil BIM Action Plan (DecretoTO 10.306); Chile BIM roadmap; Argentina emerging mandates |

Autodesk, Bentley, Trimble, regional integrators |

Asia Pacific (22.6%) is the fastest-growing region, projected at a CAGR of ~15.4%. India's BIM adoption under the Smart Cities Mission provides government engineers and architects with ready-to-deploy BIM toolkits. China's 14th Five-Year Plan invests in new urban clusters requiring digital construction coordination. Japan's MLIT BIM guideline has driven structured adoption across the country's major construction companies.

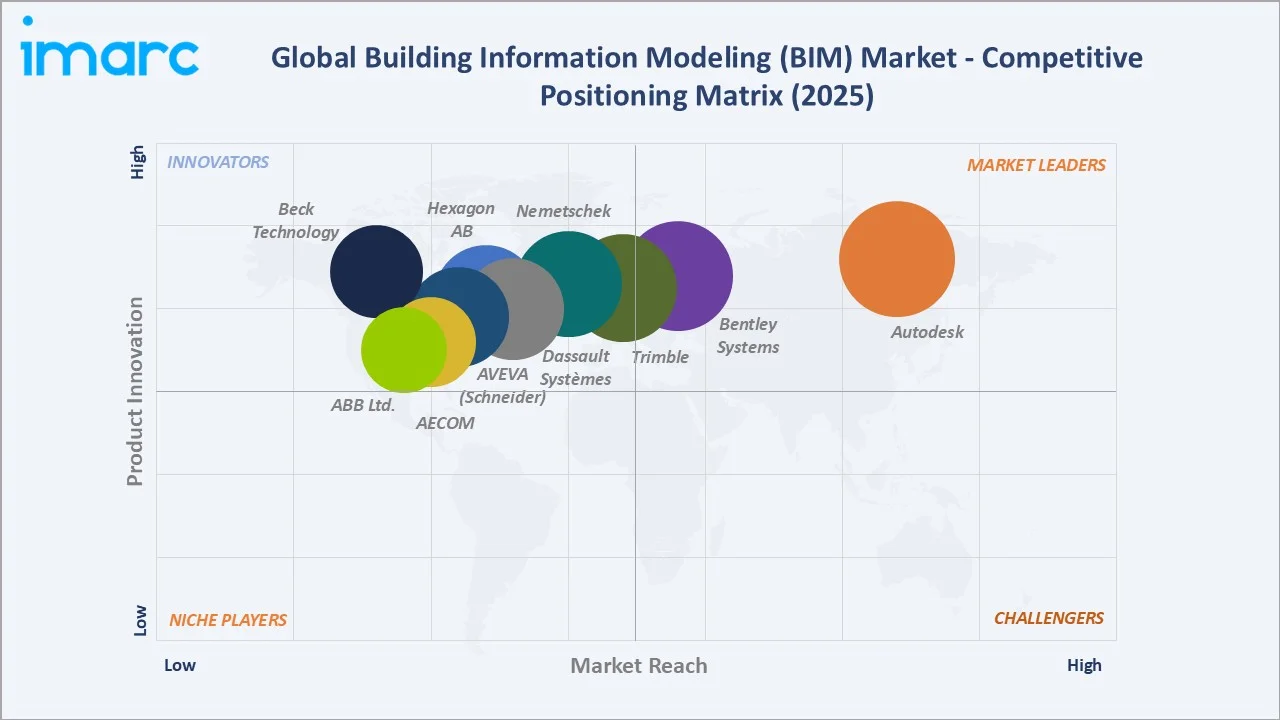

Competitive Landscape

The global BIM market is moderately consolidated, with Autodesk, Bentley Systems, Trimble, Nemetschek, and Dassault Systèmes collectively commanding approximately 67% of global revenues in 2025.

|

Company Name |

Key Product / Brand |

Market Position |

Core Strength |

|

Autodesk Inc. |

Revit/BIM 360/Forma |

Market Leader |

Largest global share ~22%; AI design assistants; cloud ecosystem |

|

Bentley Systems Inc. |

MicroStation/iTwin |

Market Leader |

Infrastructure BIM leadership; open-platform iTwin; Google Cloud alignment; linear infrastructure |

|

Trimble Inc. |

Tekla Structures/Trimble Connect |

Market Leader |

Structural steel BIM; laser-scan integration |

|

Nemetschek SE |

Archicad/Allplan/Bluebeam |

Strong Challenger |

5M+ users; 16 brands; Autodesk interoperability deal (Apr 2024) |

|

Dassault Systèmes SE |

CATIA/3DEXPERIENCE |

Strong Challenger |

Industrial & mixed-use BIM |

|

Hexagon AB |

BIM/GIS Analytics |

Regional Leader |

Geospatial BIM analytics; rail & port infrastructure |

|

AVEVA Group Plc (Schneider Electric) |

AVEVA Engineering |

Regional Leader |

Industrial & building lifecycle; digital twin integration; Schneider energy management synergies |

|

AECOM |

AECOM BIM Services |

Services Leader |

Full-lifecycle BIM consulting; global infrastructure delivery; design-build integration |

|

ABB Ltd. |

ABB Building Intelligence |

Emerging |

Building systems + OT integration; smart building automation; industrial facility management |

|

Beck Technology Ltd. |

DESTINI Estimator |

Innovator |

Preconstruction cost estimation BIM; design-cost integration; U.S. early-stage project market |

Autodesk maintains the largest share at ~22%, anchored by its Revit/BIM 360/Forma ecosystem and its dominant position in the U.S. Nemetschek's 5+ million users across 16 brands (Archicad, Vectorworks, Allplan, Bluebeam) make it the largest European competitor.

Key Company Profiles

Autodesk Inc.

Headquartered in San Francisco, California, Autodesk is the global leader in BIM software with approximately 22% market share. Autodesk Revit is the most widely deployed BIM authoring tool globally. Autodesk's AEC Collection provides a comprehensive suite spanning design, visualization, construction management, and field collaboration.

- Product Portfolio: Revit, Forma, AutoCAD, Autodesk Construction Cloud, Navisworks, Infraworks, Civil 3D, and the AEC Collection.

- Recent Developments: In May 2025, Revit 2026 was launched with reality-capture mesh imports and accelerated graphics architecture; in June 2025, the BIM Package for Viksit Bharat was launched for the Indian public sector.

- Strategic Focus: AI-augmented design workflows, cloud-first platform, open-data ecosystem via APS, and government sector expansion in India and the Middle East.

Bentley Systems Incorporated

Bentley Systems, headquartered in Exton, Pennsylvania, specializes in infrastructure engineering software. Its iTwin platform is a pioneering open platform with open-source components such as iTwin.js. used for managing complex infrastructure assets globally.

- Product Portfolio: MicroStation, OpenRoads, OpenBuildings, STAAD.Pro, ProjectWise, and the iTwin open-source digital twin platform.

- Recent Developments: Open-sourced iTwin database format on GitHub; aligned with Google Cloud for geospatial analytics in linear infrastructure; multiple deals with public infrastructure agencies across North America, Europe, and the Asia Pacific.

- Strategic Focus: Infrastructure digital twins, open-data interoperability, cloud-based engineering workflows, and lifecycle asset management for transportation, utilities, and public buildings.

Nemetschek SE

Munich-based Nemetschek SE is the largest Europe’s largest BIM software group, with a multi-brand portfolio and millions of users worldwide. Its portfolio spans architectural design, structural engineering, construction management, and document markup.

- Product Portfolio: Archicad, Allplan, Vectorworks, Bluebeam, dTwin, BIMcloud, and BIMplus industry clouds.

- Recent Developments: June 2025 – Signed MoU with Nesma Infrastructure & Technology (Saudi Arabia) supporting Vision 2030 digital construction; June 2025 – Partnered with Iowa State University's 3D Printing Housing Project; April 2024 – Interoperability agreement with Autodesk.

- Strategic Focus: Open BIM advocacy, cloud platform expansion, sustainability analytics integration, and emerging market growth in the Middle East and Asia.

Trimble Inc.

Trimble, headquartered in Westminster, Colorado, is a leading provider of BIM tools for structural engineering, steel fabrication, and field-to-office connectivity. Its Tekla suite is the industry standard for constructible structural BIM globally.

- Product Portfolio: Tekla Structures, Tekla Tedds, Tekla Structural Designer, Tekla PowerFab, Trimble Connect, and SketchUp.

- Recent Developments: In June 2025, Tekla Structures 2025 was launched with AI-enhanced fabrication drawing automation and Live Collaboration; joined AOUSD for open USD data exchange.

- Strategic Focus: AI-powered structural BIM, laser-scan integration, constructible model workflows, and global expansion of the Trimble Connect cloud collaboration platform.

Market Concentration Analysis

The global BIM market exhibits moderate concentration. The top five players, Autodesk, Bentley Systems, Trimble, Nemetschek, and Dassault Systèmes, collectively hold approximately 67% of total revenues in 2025. Autodesk alone commands ~22%, reflecting its dominant position across the U.S. and English-speaking AEC markets.

The software segment is more concentrated than services, where thousands of regional consulting, implementation, and training firms compete. In the cloud-based segment, Autodesk and Bentley account for over 60% of platform revenues combined. Asia Pacific is the least concentrated region, with strong local players in China (PKPM, CATIA China), Japan, and India supplementing global vendors.

Investment & Growth Opportunities

Fastest Growing Segments

Cloud-based BIM (CAGR ~14.8%), Asia Pacific regional market (CAGR ~15.4%), and the BIM services segment (CAGR ~11.8% but growing fastest within services) represent the highest-growth investment vectors through 2034. These segments collectively map to the trajectory from USD 9.8 Billion (2025) to USD 29.9 Billion (2034), representing over USD 20 Billion in incremental addressable market expansion.

Emerging Market Expansion

Saudi Arabia's Vision 2030 digital infrastructure pipeline, India's USD 1.4 trillion National Infrastructure Pipeline, and Southeast Asia's smart city programs represent the most compelling geographic investment opportunities. Entry via strategic partnerships, licensing of BIM execution frameworks, and cloud platform distribution agreements are the preferred market entry strategies.

Venture Investment Trends

AI-native BIM startups, digital twin analytics platforms, and open-data infrastructure tools are attracting significant venture capital. Key themes include AI-powered cost estimation, autonomous code compliance checking, and BIM-to-FM integration platforms.

- Key growth bets: AI generative design, scan-to-BIM automation, and BIM-integrated ESG reporting platforms for sustainable building certification.

- ESG-aligned institutional investors are requiring lifecycle BIM models as part of green building finance underwriting, creating a new class of financial-sector demand for BIM data.

- Development finance institutions are embedding BIM requirements into infrastructure loan covenants for emerging-market transport and housing projects, creating policy-driven market entry opportunities.

Future BIM Market Outlook (2026-2034)

The global BIM market is poised for sustained double-digit growth through 2034, anchored by regulatory expansion, AI platform maturation, and cloud-native architecture becoming the industry default. From a base of USD 9.8 Billion in 2025, the market is forecast to reach USD 29.9 Billion by 2034, representing incremental value addition of over USD 20 Billion across the decade.

Technological disruptions, including autonomous AI-drafted construction documents, BIM-native digital twins with real-time IoT feeds, and open-data platforms eliminating interoperability friction, will materially reshape how AEC projects are delivered. By 2028–2030, BIM is expected to be mandated in 60%+ of countries by GDP for public infrastructure projects, converting the global AEC industry's largest procurement channels into compliant BIM markets.

The next decade will also be defined by BIM's expansion beyond construction into circular economy workflows: tracking material carbon data through demolition, disassembly, and material recovery. Organizations that establish cloud BIM infrastructure, AI workflow integration, and lifecycle data governance today will hold a decisive competitive advantage in the AEC digital economy of 2034.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 180 industry participants in 2025, comprising AEC executives, BIM managers, government procurement officials, software vendors, and construction technology investors across North America, Europe, and the Asia Pacific.

Secondary Research

Secondary research encompassed company annual reports, regulatory filings, trade publications (AEC Magazine, BIM+, ENR, Construction Dive), government BIM strategy documents, and publicly available technology roadmaps. Over 220 secondary sources were reviewed and cross-validated.

Forecasting Models

Market size estimations were derived using top-down and bottom-up models incorporating GDP growth, construction output indices, BIM adoption rates by region and firm size, and regulatory mandate timelines. Scenario analysis covering base, optimistic, and conservative cases was applied to account for technology adoption uncertainty.

Building Information Modeling (BIM) Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Offering Types Covered | Software, Services |

| Deployment Modes Covered | On-premises, Cloud-based |

| Applications Covered | Preconstruction, Construction, Operations |

| End Use Sectors Covered | Commercial, Residential, Industrial |

| End Users Covered | Architects and Engineers, Contractors and Developers, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Autodesk Inc., Bentley Systems Inc., Trimble Inc., Nemetschek SE, Dassault Systèmes SE, Hexagon AB, AVEVA Group Plc (Schneider Electric), AECOM, ABB Ltd., Beck Technology Ltd., etc |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the building information modeling (BIM) market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global building information modeling (BIM) market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the building information modeling (BIM) industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Building Information Modeling Market Report

The global BIM market was valued at USD 9.8 Billion in 2025 and is projected to reach USD 29.9 Billion by 2034.

The BIM market is expected to grow at a CAGR of 13.20% during 2026-2034, reflecting strong demand from government mandates, cloud migration, AI integration, and expanding smart city infrastructure investments globally.

Software is the largest segment at 62.4% share 2025, driven by demand for design, clash detection, simulation, and facility management tools from Autodesk, Bentley, Nemetschek, Trimble, and Dassault Systèmes.

On-premises deployment is the leading mode at 55.4% 2025, reflecting organizations’ preference for enhanced data security, control over sensitive project information, and integration with legacy systems in large-scale construction and infrastructure projects.

North America dominates with approximately 36.4% of global BIM market revenues in 2025, driven by U.S. federal BIM guidelines, infrastructure investment programs, and the presence of Autodesk, Bentley Systems, and Trimble.

Asia Pacific is the fastest-growing region at a CAGR of ~15.4% 2026-2034, fueled by China's 14th Five-Year Plan, India's Viksit Bharat BIM package, and Singapore's mandatory BIM submission policy for public projects.

Key drivers include mandatory government BIM policies, cloud-native platform adoption, AI and digital twin integration, smart city infrastructure investment, and growing green building certification requirements demanding lifecycle energy modeling.

AI-augmented BIM and generative design, cloud-native BIM platforms, digital twin and IoT integration, government mandate expansion to emerging markets, and open-data interoperability ecosystems are the fastest-growing BIM market trends through 2034.

Leading companies include Autodesk Inc., Bentley Systems, Trimble Inc., Nemetschek SE, Dassault Systèmes SE, Hexagon AB, AVEVA Group Plc (Schneider Electric), AECOM, ABB Ltd., and Beck Technology Ltd.

Key challenges include high initial implementation costs (BIM software 20-30% premium for SMEs), interoperability fragmentation across file formats, skills gaps in emerging markets, and cybersecurity risks of cloud-hosted project data models.

High-growth opportunities exist in Asia Pacific infrastructure BIM, Middle East Vision 2030 digital construction mandates, AI-powered BIM analytics, scan-to-BIM automation, and BIM-integrated ESG lifecycle carbon reporting platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)