Cable Accessories Market Size, Share, Trends and Forecast by End-User, Voltage, Installation, and Region, 2026-2034

Cable Accessories Market Size, Share, Trends & Forecast (2026-2034)

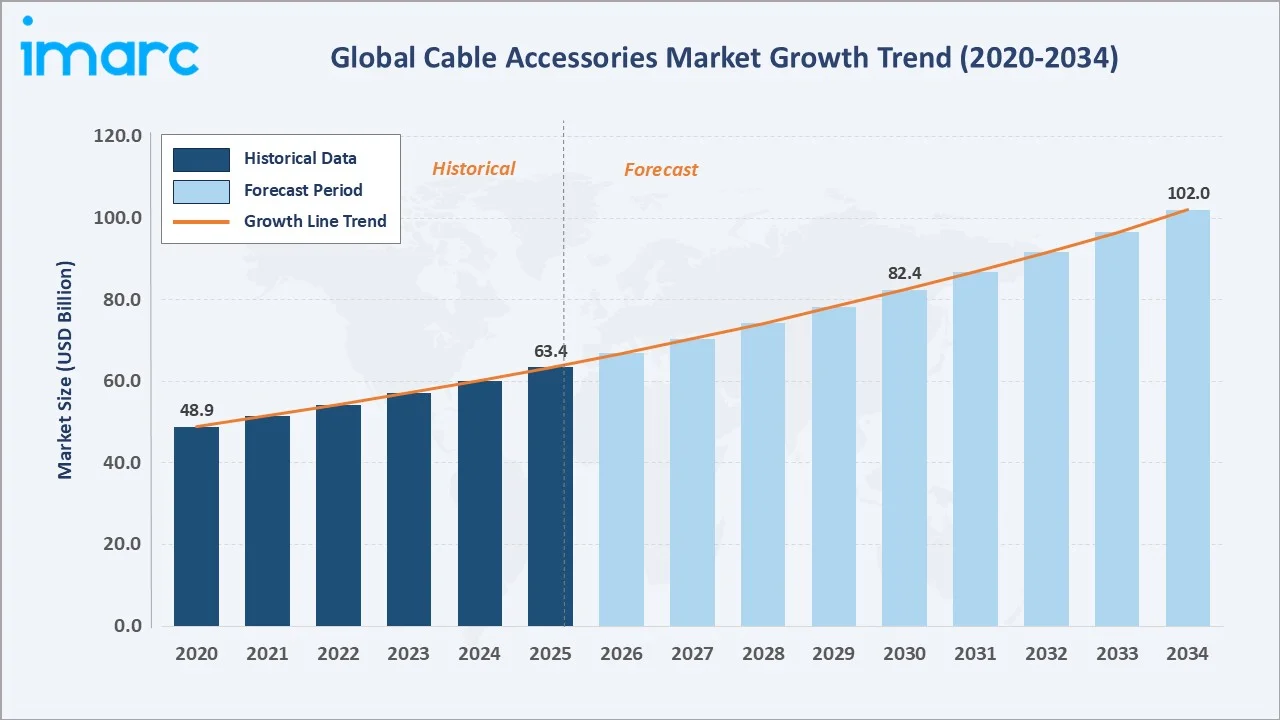

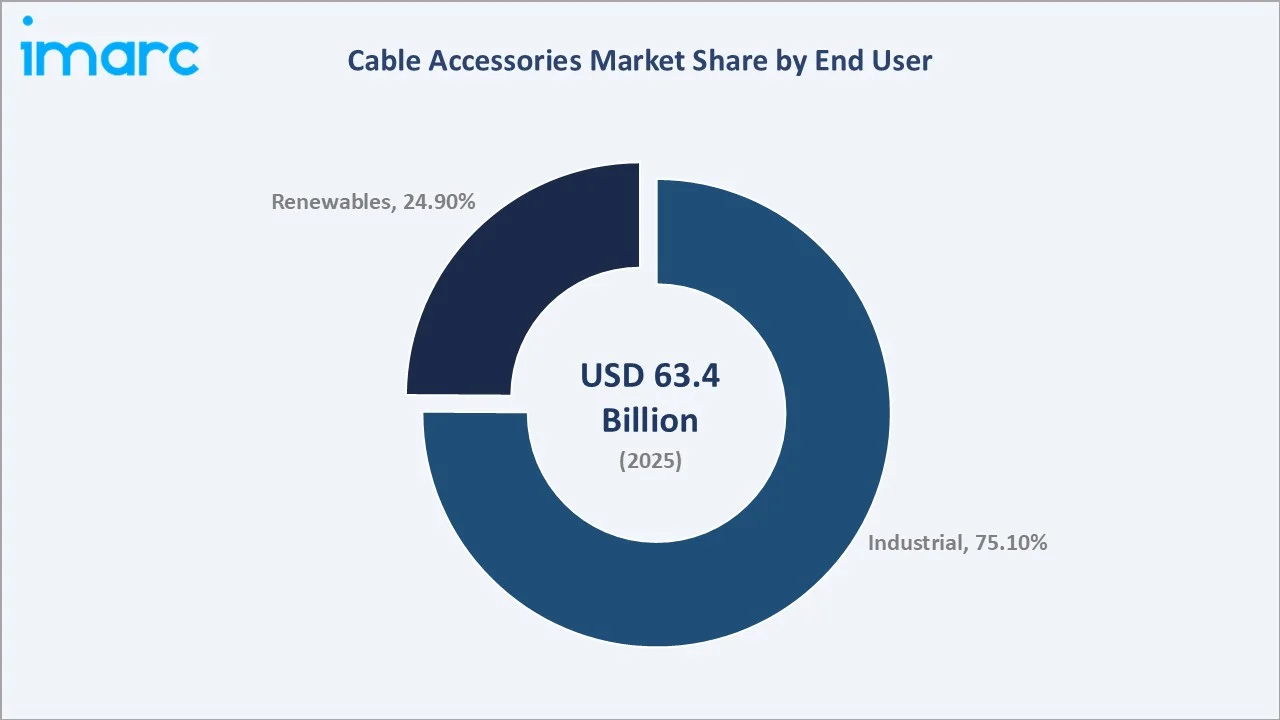

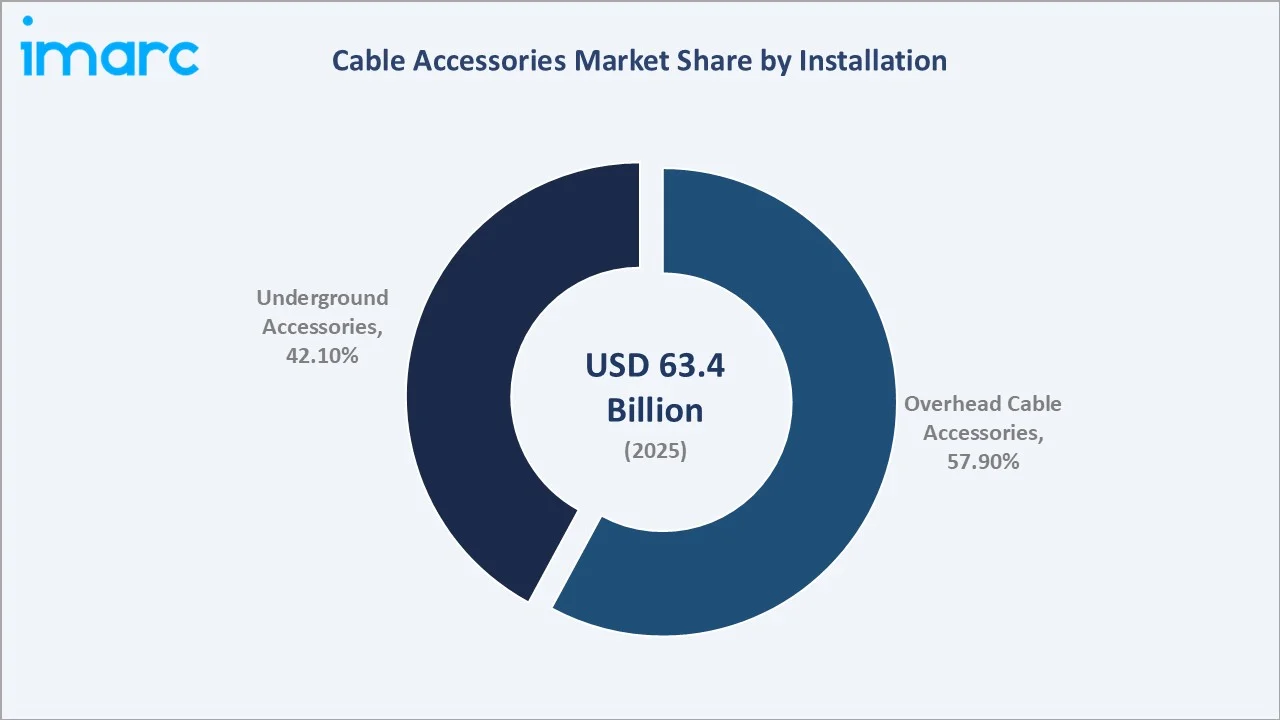

The global cable accessories market was valued at USD 63.4 Billion in 2025 and is projected to reach USD 102.0 Billion by 2034, expanding at a CAGR of 5.38% during 2026-2034. Growth is driven by rising investments in power transmission and distribution (T&D) infrastructure, rapid urbanization, the global shift toward renewable energy, and increasing adoption of smart grid technologies.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 63.4 Billion |

|

Forecast Market Size (2034) |

USD 102.0 Billion |

|

CAGR (2026-2034) |

5.38% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Fastest Growing Segment |

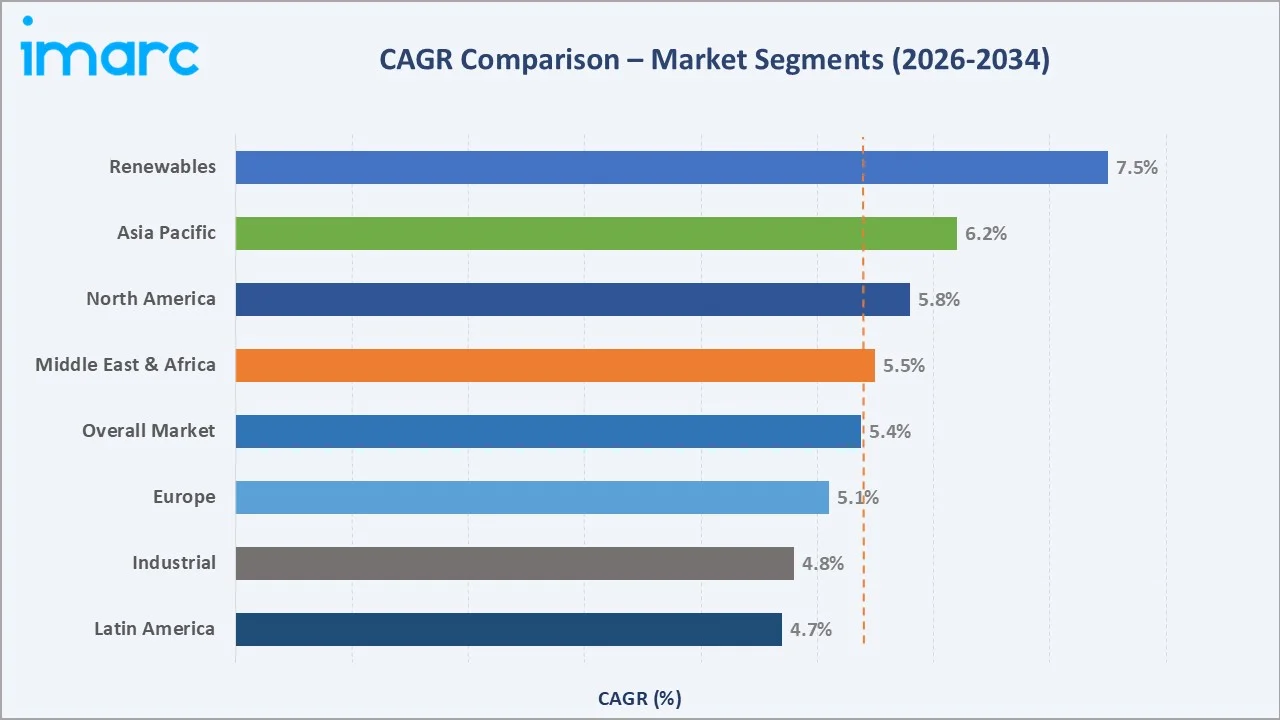

Renewables (CAGR ~7.5%) |

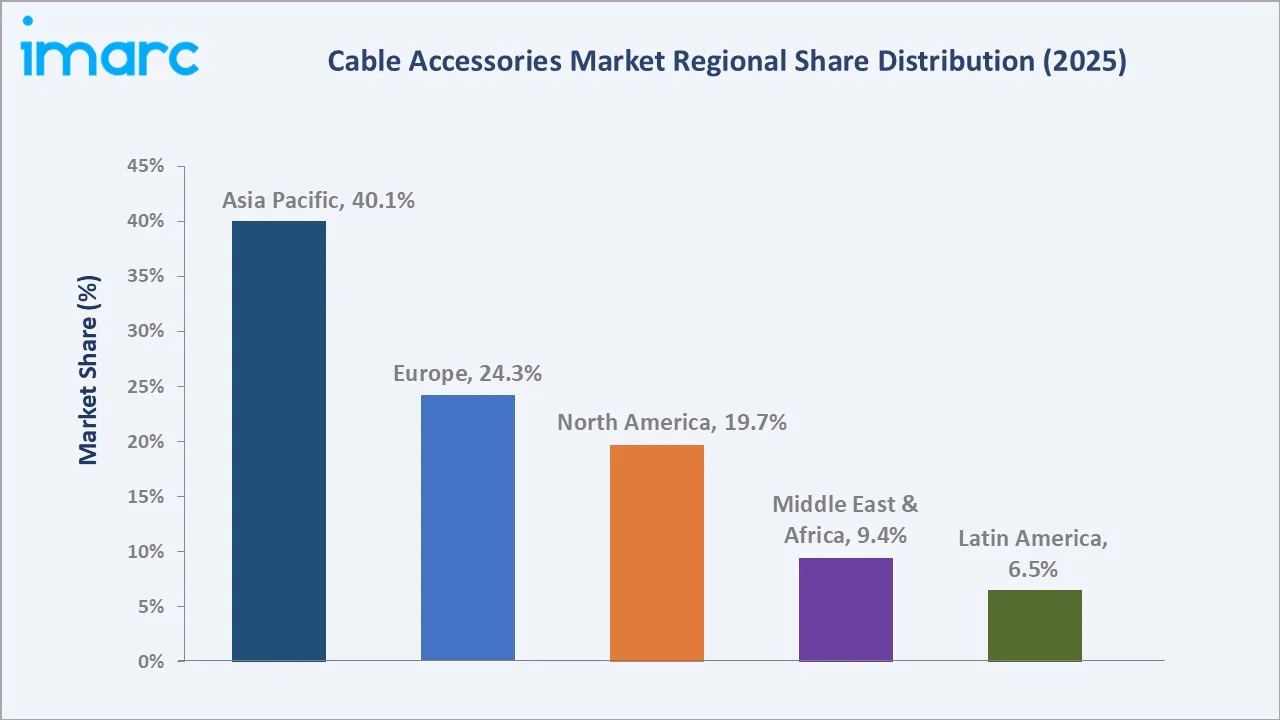

Asia Pacific dominates with a 40.1% market share (2025), supported by large-scale infrastructure projects in China and India. The industrial segment leads with a 75.1% share, while the overhead cable accessories segment accounts for 57.9% of the installation.

To get more information on this market, Request Sample

The cable accessories market plays a critical role in ensuring the reliability, safety, and efficiency of electrical transmission and distribution systems. It includes products such as cable joints, terminations, connectors, and insulation components used across power utilities, industrial facilities, and infrastructure projects.

Executive Summary

The global cable accessories market continues to exhibit robust expansion, underpinned by accelerating electrification efforts, renewable energy integration, and the widespread rollout of smart grid infrastructure. Valued at USD 63.4 Billion in 2025, the market is forecast to exceed USD 102.0 Billion by 2034, at a CAGR of 5.38%.

Among end users, the industrial segment commands 75.1% of the market, driven by complex machinery, automation adoption, and expanding manufacturing hubs globally. The renewables segment, however, is emerging as the fastest-growing end-use category, reflecting the surge in offshore wind and utility-scale solar projects.

Technological advancements in cross-linked polyethylene (XLPE) insulation, heat-shrink accessories, and AI-enabled predictive maintenance solutions are improving cable performance and reducing lifecycle costs. The cable accessories market trends point toward increasing adoption of smart accessories with real-time monitoring and self-diagnostic capabilities through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (End User) |

Industrial - 75.1% market share (2025) |

|

Largest Segment (Installation) |

Overhead Cable Accessories - 57.9% (2025) |

|

Fastest Growing Segment |

Renewables - CAGR ~7.5% (2026-2034) |

|

Leading Region |

Asia Pacific - 40.1% revenue share (2025) |

|

Top Companies |

Nexans SA, Prysmian Group, ABB Group, NKT A/S, Taihan Cable & Solution Co., Ltd. |

|

Key Market Opportunity |

Smart & IoT-enabled cable accessories adoption |

Key Analytical Observations:

- Industrial segment leads at 75.1% (2025), driven by extensive power distribution needs across manufacturing, oil & gas, and heavy industries that demand high-reliability cable accessories for uninterrupted operations.

- Overhead cable accessories hold 57.9% (2025) of the installation segment, primarily serving transmission networks and rural electrification projects with cost-effective, accessible overhead solutions.

- Renewables represent the fastest-growing end-use category, fueled by rapid wind and solar capacity additions globally, requiring specialized accessories for offshore and onshore integration with the grid.

- Asia Pacific commands 40.1% of global revenues (2025), supported by the Asian Development Bank (ADB), which estimates that Asia will need to invest around USD 1.7 trillion annually in infrastructure through 2030 to sustain economic growth, reduce poverty, and address climate risks.

- Smart and IoT-enabled cable accessories are opening new market opportunities, with integrated sensors enabling real-time fault detection, predictive maintenance, and remote diagnostics across utility networks.

Global Cable Accessories Market Overview

Cable accessories are essential components of power cable networks, designed to connect, terminate, and protect cables across electrical transmission and distribution (T&D) systems. The product ecosystem spans cable joints, terminations, connectors, heat-shrink tubing, cable lugs, end caps, and insulating accessories. They are deployed across overhead and underground configurations, serving utility-grade high-voltage networks as well as medium and low-voltage distribution systems for industrial, commercial, and residential end users.

The cable accessories market growth is reinforced by macro-level drivers, including urbanization, rising global energy consumption, and the accelerating transition to clean energy. Governments across Asia, Europe, and North America are allocating record budgets for grid modernization and underground power line projects, creating sustained demand. The expanding application of digital substations, 5G infrastructure cabling, and EV charging networks further extends the addressable market. The cable accessories market forecast through 2034 reflects positive momentum across all major regions and segments.

Market Dynamics

To evaluate market opportunities, Request Sample

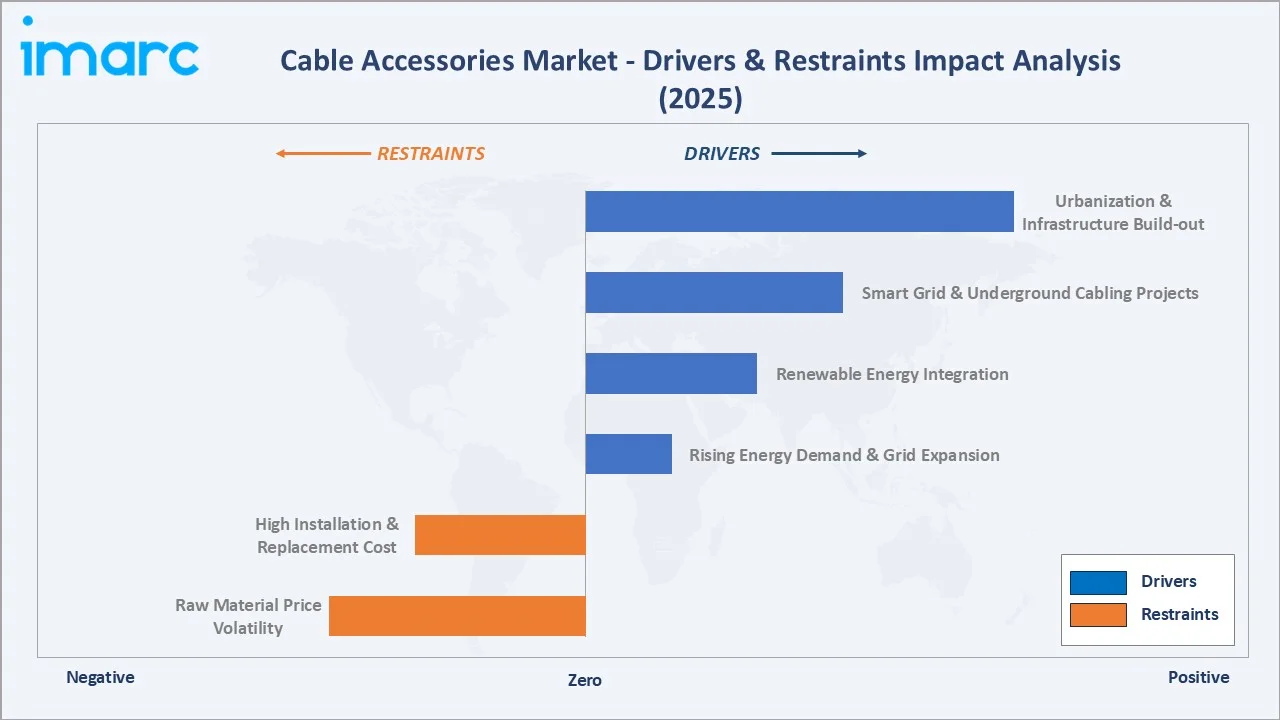

Market Drivers

- Rising Energy Demand and T&D Infrastructure Investments: Escalating electricity consumption globally is driving large-scale investments in power generation, transmission, and distribution networks. Urban and industrial expansion in emerging economies such as India, China, and Indonesia is necessitating robust cable systems and accessories.

- Renewable Energy Integration: The global shift toward solar and wind energy requires advanced cable accessories for connecting distributed generation sources to the grid. Investment in renewables in the US surged 60% in 2023 to reach USD 92.9 Billion, directly expanding the cable accessories market outlook.

- Smart Grid and Underground Cabling Projects: Governments across Europe and Asia-Pacific are funding extensive underground power line projects to improve grid resilience and urban aesthetics. France's RTE, for instance, committed nearly EUR 1 billion in 2024 to supply and install approximately 7,000 km of underground cables.

- Urbanization and Industrial Infrastructure: Rapid urbanization, supported by the UN projection that 68% of the global population will reside in urban areas by 2050, continues to drive demand for medium and low-voltage cable accessories in residential and commercial applications.

These drivers collectively underpin a sustained demand cycle — grid expansion requires higher-specification accessories, smart city initiatives accelerate underground adoption, and the energy transition creates premium specialty accessory verticals, all reinforcing long-run market expansion.

Market Restraints

- Raw Material Price Volatility: Fluctuating prices of copper, aluminum, and polymer-based insulation materials pose margin pressures for cable accessories manufacturers, complicating long-term contract pricing and product planning.

- High Initial Installation and Replacement Costs: Underground cabling, while preferred in dense urban areas, involves significantly higher installation costs compared to overhead infrastructure, limiting adoption in cost-sensitive emerging markets.

Market Opportunities

- Smart and IoT-Enabled Cable Accessories: The integration of fiber optic sensors and smart monitoring systems within cable accessories enables real-time fault detection and predictive maintenance, creating premium product categories and recurring revenue streams for manufacturers.

- Offshore Wind and HVDC Expansion: Offshore wind installations and HVDC transmission projects require highly specialized submarine cable accessories, presenting high-value growth opportunities for technically advanced players such as Nexans SA and NKT A/S.

Market Challenges

- Complex Regulatory Compliance: Cable accessories must comply with evolving IEC, IEEE, and regional safety standards, requiring significant R&D investment and certification processes that can delay product launches.

- Supply Chain Disruptions: Geopolitical tensions and raw material supply chain dependencies (particularly for copper and specialized polymers) expose manufacturers to procurement risks and production delays.

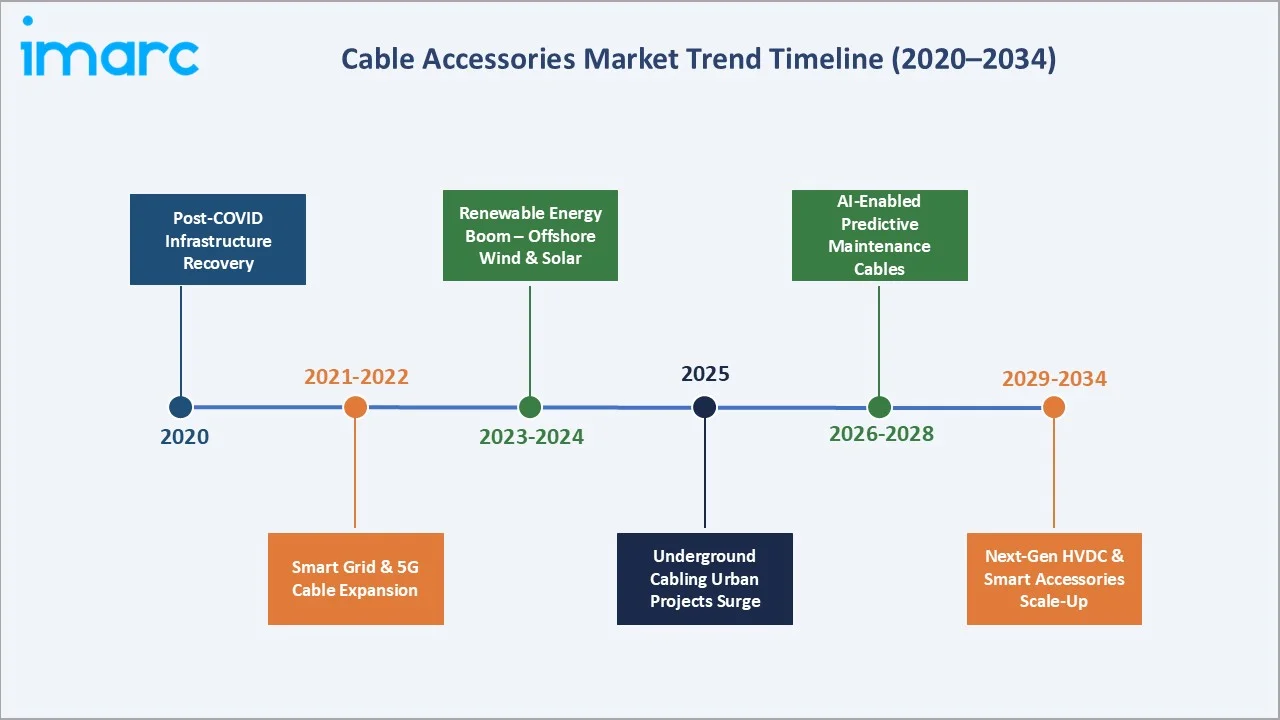

Emerging Market Trends

1. Rise of Smart and Self-Healing Cable Accessories

The integration of IoT connectivity and fiber optic monitoring within cable accessories is reshaping the industry's technological frontier. Smart accessories equipped with embedded sensors can transmit real-time data on temperature, load, and insulation integrity to grid control centers. Self-healing materials are now being developed that autonomously repair minor insulation damage, reducing maintenance downtime.

2. Surge in Underground Cable Accessories

Urbanization and regulatory mandates across Europe and the Asia-Pacific are accelerating the transition from overhead to underground cabling. Underground accessories are estimated to account for 42.1% of the cable accessories market in 2025, with a CAGR of approximately 6.5% forecast through 2034. Governments in Germany, France, and the Netherlands have mandated underground distribution in new urban developments since 2017, while Asian smart city initiatives further drive adoption.

3. Renewable Energy Driving Specialty Accessories Demand

Offshore applications require corrosion-resistant, water-blocking terminations and joints rated for saline, high-humidity environments. In Europe, investment in renewable energy grew 42.9% in 2023 to USD 134.4 Billion, directly expanding the addressable market for specialty cable accessories. This cable accessories market growth reflects the convergence of decarbonization policy and expanding grid interconnection requirements.

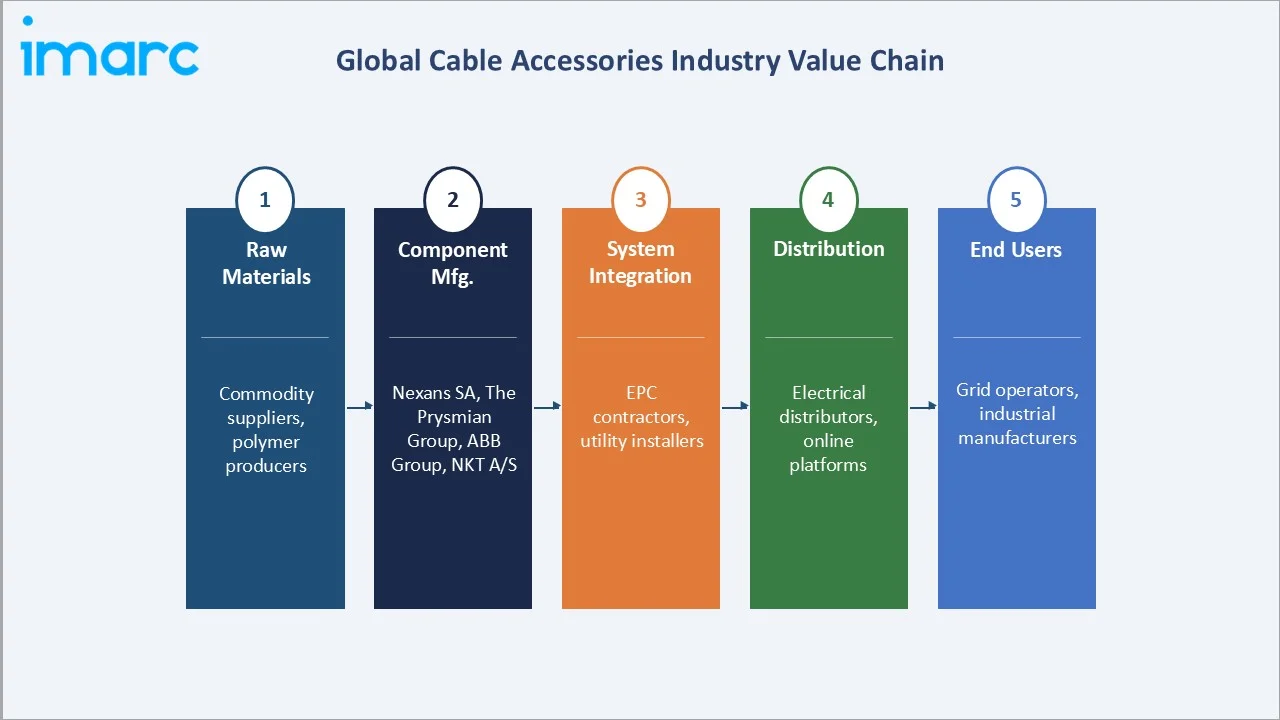

Industry Value Chain Analysis

The cable accessories value chain spans raw material suppliers, component manufacturers, systems integrators, and end-use utility operators. Each stage creates interdependencies that influence product quality, delivery timelines, and cost competitiveness.

|

Stage |

Description |

Key Examples |

|

Raw Materials |

Copper, aluminum, XLPE polymers, silicone rubber, heat-shrink materials |

Commodity suppliers, polymer producers |

|

Component Mfg. |

Production of joints, terminations, connectors, cable lugs, and end caps |

Nexans SA, The Prysmian Group, ABB Group, NKT A/S |

|

System Integration |

Installation, testing, and commissioning of cable accessories in T&D networks |

EPC contractors, utility installers |

|

Distribution |

Wholesale distribution to construction and infrastructure project channels |

Electrical distributors, online platforms |

|

End Users |

Power utilities, industrial facilities, and renewable energy project operators |

Grid operators, industrial manufacturers |

Technology Landscape

XLPE and Advanced Insulation Materials

Cross-linked polyethylene (XLPE) remains the dominant insulation material, with a projected 39% market share in 2025 and a CAGR of 6.4% through 2034, owing to its superior dielectric properties and thermal stability. Cold-shrink and heat-shrink technologies are gaining traction for their ease of installation, eliminating the need for open flames and specialized equipment.

Smart Monitoring and AI Integration

AI-powered cable monitoring systems are enabling predictive maintenance by analyzing performance data from embedded sensors. These digital solutions provide real-time diagnostics on temperature, load, and insulation integrity, transmitting alerts to grid control centers and enabling proactive fault management.

Pre-Molded Systems and Installation Innovation

Pre-molded joint systems are displacing traditional tape-wrapped solutions, reducing installation time by up to 40% while improving reliability and moisture-resistance. In high-voltage applications, 525 kV HVDC-rated accessories are being qualified by leading manufacturers, supporting the expansion of long-distance transmission corridors essential for large-scale renewable energy integration.

Sustainable and Eco-Friendly Technology

Cable accessories manufacturers are increasingly focused on sustainability, developing halogen-free, lead-free, and recyclable insulation materials in response to EU REACH regulations and customer ESG requirements. ABB's Kabeldon NXT low-voltage cable distribution cabinet, launched in May 2025, achieved a 29% reduced carbon footprint using 100% renewable energy in its manufacturing process — exemplifying the industry-wide shift toward green product innovation.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Voltage |

Low Voltage Cable Accessories |

52.0% |

2025 |

|

Installation |

Overhead Cable Accesories |

57.9% |

2025 |

|

End-User |

Industrial |

75.1% |

2025 |

|

Region |

Asia Pacific |

40.1% |

2025 |

By End-User

The industrial end-user segment dominates the cable accessories market, accounting for 75.1% of global revenue in 2025. Industrial operations ranging from manufacturing and petrochemicals to mining and data centers rely on extensive cable networks that require robust accessories to ensure operational continuity and electrical safety. The renewables segment, despite its current 24.9% share, is the most dynamic end-use category, projected to grow at approximately 7.5% CAGR through 2034, as utilities and independent power producers scale up clean energy capacity globally.

To access detailed market analysis, Request Sample

By Installation

Overhead cable accessories represent the larger installation segment at 57.9% in 2025, underpinned by the cost-efficiency and ease of maintenance associated with aerial infrastructure, particularly in rural and semi-urban electrification programs across Africa, Southeast Asia, and Latin America.

However, the underground accessories segment is growing faster, driven by urban utility corridor upgrades, aesthetic mandates, and the need for storm-resilient power supply. The cable accessories market outlook for underground systems remains strongly positive through 2034, with an estimated CAGR of approximately 6.5%.

Regional Market Insights

Asia Pacific dominates the global cable accessories market with a 40.1% share in 2025, reflecting massive and sustained investments in power infrastructure across the region. China is solidifying its position as the global leader in renewable energy development, with 180 GW of utility-scale solar and 159 GW of wind capacity currently under construction. Combined, this nearly doubles the capacity being built in the rest of the world and is sufficient to power all of South Korea, according to Global Energy Monitor (GEM).

|

Region |

Share (2025) |

CAGR (2026–34) |

Key Drivers |

Regulatory / Investment Context |

|

Asia Pacific |

40.1% |

~6.2% |

Urbanization, infrastructure investment, and renewable energy |

Power for All (India); USD 1.7T annual construction investment; ~293 GW of wind+solar (or ~301 GW including hydro) in China (2023) |

|

Europe |

24.3% |

~5.1% |

Grid modernization, underground cabling mandates, and offshore wind |

EUR 1B underground projects (France 2024); USD 134.4B renewable investment (2023); EU sustainability standards |

|

North America |

19.7% |

~5.8% |

Smart grid upgrades, renewable energy, EV charging infrastructure |

USD 92.9B US renewable investment (2023); Schneider Electric USD 700M US commitment through 2027 |

|

Middle East & Africa |

9.4% |

~5.5% |

Power for All initiatives, grid expansion, urban electrification |

GCC grid expansion programs; sub-Saharan electrification access projects |

|

Latin America |

6.5% |

~4.7% |

Infrastructure development, renewable energy projects |

Brazilian and Chilean renewable energy targets; urban infrastructure investment programs |

Europe represents the second-largest region at 24.3% (2025), driven by ambitious grid modernization programs, underground cabling mandates, and the rapid expansion of offshore wind infrastructure. NKT's EUR 100 Million investment in its Cologne production facility and Nexans's EUR 90 Million investment in offshore wind capacity expansion reflect the magnitude of European market activity.

Competitive Landscape

The global cable accessories market exhibits a moderately consolidated competitive structure, with a small number of multinational players commanding significant shares through deep product portfolios, vertical integration, and established relationships with utility operators and EPC contractors.

|

Company Name |

Core Products |

Market Position |

Key Strength |

|

Nexans SA |

HV/MV/LV cable accessories, offshore cable systems |

Market Leader |

Offshore wind & HVDC accessories; EUR 90M capacity expansion (Sep 2024) |

|

The Prysmian Group |

Cables and accessories for energy & telecom |

Market Leader |

Largest cable manufacturer; Encore Wire acquisition (Jul 2024); EUR 5B Amprion HVDC contracts (Q1 2024) |

|

ABB Group |

Cable distribution cabinets, tray systems, and connectors |

Strong Challenger |

Grid automation; Kabeldon NXT launch (May 2025); JV with Niedax Group (November 2024) |

|

NKT A/S |

HV/MV/LV cable systems and accessories |

Strong Challenger |

HVDC specialist; EUR 100M Cologne investment; record Q3 2024 EBITDA of EUR 93M |

|

Taihan Cable & Solution Co., Ltd. |

LV/MV/HV cable accessories for utility and industrial use |

Emerging Player |

Asia-Pacific growth, expanding medium and high-voltage cable accessories range |

Competitive intensity is shaped by technological differentiation, manufacturing capacity, and global distribution networks. Companies are increasingly investing in R&D to develop smart accessories, eco-friendly insulation materials, and HVDC-rated high-voltage systems to capture premium segments.

Key Company Profiles

Nexans SA

Nexans SA is a global leader in cable design, manufacturing, and distribution, covering power cables, cable accessories, and connectivity solutions across high, medium, and low voltage.

- Product Portfolio: High-voltage, medium-voltage, and low-voltage cable accessories; offshore cable systems and submarine accessories; connectivity solutions for energy and telecom.

- Recent Developments: EUR 90 Million facility investment for offshore wind capacity expansion (Sep 2024); three consecutive CDP 'A' climate ratings.

- Strategic Focus: Offshore wind and HVDC market leadership, sustainability-driven product development, and expanded European manufacturing capacity.

The Prysmian Group

The Prysmian Group is the world's largest cable manufacturer with 146 years of operational history, producing cables and accessories for energy transmission, telecom, and building applications across 50+ countries.

- Product Portfolio: Cables and accessories for transmission, distribution, renewables, and building; fiber optic and telecom cables; offshore and submarine systems.

- Recent Developments: Encore Wire acquisition (Jul 2024); EUR ~5B HVDC contracts from Amprion (Q1 2024); sustained expansion of North American manufacturing.

- Strategic Focus: HVDC market capture, North American scale-up, vertical integration, and technology-driven product premiumization.

ABB Group

ABB Group is a multinational industrial technology company offering a broad range of electrical and automation products, including cable distribution cabinets and accessories.

- Product Portfolio: Cable distribution cabinets (Kabeldon NXT), cable tray systems, grid automation solutions, and low-voltage accessories.

- Recent Developments: Kabeldon NXT launch with 29% lower carbon footprint (May 2025); Niedax Group JV for North American cable tray market (November 2024).

- Strategic Focus: Green product innovation, North American market development, and grid automation leadership through digital and sustainable solutions.

NKT A/S

NKT A/S is a focused high-voltage cable specialist, manufacturing and installing low, medium, and high-voltage cable systems for the energy sector.

- Product Portfolio: HV, MV, and LV cable systems; HVDC cable accessories; offshore and onshore cable installation services.

- Recent Developments: Record Q3 2024 EBITDA of EUR 93M; EUR 100M Cologne facility investment; RTE framework extended for 1,400 km of HV lines.

- Strategic Focus: HVDC specialization, European grid modernization, and capacity expansion to serve the growing offshore wind project pipeline.

Taihan Cable & Solution Co., Ltd.

Taihan Cable & Solution is a South Korea-based manufacturer of power cables and accessories with a growing presence across Asia-Pacific and the Middle East. The company offers a comprehensive product range covering low, medium, and high-voltage cable accessories for utility and industrial customers.

- Product Portfolio: LV, MV, and HV power cable accessories; utility-grade connectors, terminations, and joints for industrial and infrastructure applications.

- Recent Developments: Ongoing capacity expansion initiatives; increasing penetration in Asia-Pacific and Middle East utility procurement channels.

- Strategic Focus: Asia-Pacific market leadership, expanding high-voltage product range, and international growth through infrastructure-driven emerging markets.

Market Concentration Analysis

The global cable accessories market displays moderate to high concentration at the top, with the leading five players, Nexans SA, The Prysmian Group, ABB Group, NKT A/S, Taihan Cable & Solution Co., Ltd, collectively accounting for an estimated 40–50% of global revenues. Prysmian and Nexans hold the largest individual shares by virtue of their extensive manufacturing networks and product breadth.

Consolidation momentum is building, with recent M&A activity, including Prysmian's USD 4.2 Billion acquisition of Encore Wire, signaling intent by large players to capture market share and manufacturing scale. Entry barriers remain substantial, given the capital intensity of manufacturing, regulatory approvals required, and long-term utility procurement frameworks. Smaller players compete primarily on cost and local responsiveness in developing markets.

Investment & Growth Opportunities

- HVDC and Offshore Wind Infrastructure: Offshore wind capacity in Europe and Asia-Pacific is set to triple by 2034, requiring billions of dollars in submarine and onshore cable accessories. High barriers to entry and premium pricing make this a high-margin opportunity for vertically integrated players.

- Smart Grid and Digital Accessory Solutions: The pivot toward intelligent power networks is creating demand for sensor-enabled, IoT-compatible cable accessories. Manufacturers investing in embedded monitoring technologies can command higher ASPs and service-based revenue models.

- Emerging Market Electrification: Sub-Saharan Africa, Southeast Asia, and Latin America collectively represent an incremental addressable market opportunity tied to electrification access programs, rural grid expansion, and industrial zone development through 2034.

- EV Charging and Data Center Infrastructure: The expansion of electric vehicle charging networks and hyperscale data centers in North America and Europe is creating new demand verticals for medium-voltage cable accessories outside the traditional utility procurement channel.

Future Market Outlook (2026-2034)

The global cable accessories market is positioned for sustained growth through 2034, supported by structural tailwinds from the global energy transition, infrastructure modernization, and digital grid transformation. As HVDC transmission corridors expand across continents, demand for ultra-high-voltage accessories rated at 525 kV and above will become a premium growth vector.

Geographically, Asia Pacific will maintain its dominance, while North America is projected to grow at approximately 5.8% CAGR, driven by renewable energy investments and grid hardening programs. Europe's mandatory underground cabling transition and offshore wind ambitions will sustain robust demand. The market will increasingly bifurcate between commodity-grade accessories serving developing markets and premium smart accessories capturing value in mature economies.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with cable accessories manufacturers, utility operators, EPC contractors, and industry experts. This primary engagement captured direct market intelligence on procurement trends, technology adoption rates, product pricing dynamics, and competitive strategies across key geographies.

Secondary Research

Secondary research encompassed a comprehensive review of corporate filings, government energy reports, IEA data, regulatory frameworks (IEC, IEEE, EU directives), trade publications, and patent databases. Market sizing and trend analysis drew on publicly available financial data and official energy statistics across all covered regions.

Forecasting Models

Market size estimations and growth projections were derived using a bottom-up approach validated by a top-down review, with forecasts modeled using regression analysis, scenario planning, and expert triangulation. All figures are in USD Billion unless otherwise stated. The base year is 2025, and the forecast period covers 2026–2034.

Cable Accessories Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| End-Users Covered | Industrial, Renewables |

| Voltages Covered | Low Voltage Cable Accessories, Medium Voltage Cable Accessories, High Voltage Cable Accessories |

| Installations Covered | Overhead Cable Accessories, Underground Cable Accessories |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Nexans SA, The Prysmian Group, ABB Group, NKT A/S, Taihan Cable & Solution Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, cable accessories market forecast, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global cable accessories market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cable accessories industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cable Accessories Market Report

The global cable accessories market was valued at USD 63.4 Billion in 2025, reflecting strong demand from power infrastructure investments and industrial growth.

The market is projected to reach USD 102.0 Billion by 2034, exhibiting a CAGR of 5.38% during 2026-2034, driven by renewable energy expansion and grid modernization.

Key drivers include rising energy demand, renewable energy integration, urbanization, smart grid deployments, and growing underground cabling projects globally.

Asia Pacific dominates with a 40.1% share (2025), led by China and India's large-scale power infrastructure investments and rapid industrialization.

The industrial end-user segment leads with 75.1% share (2025), driven by power distribution needs across manufacturing, oil & gas, and heavy industries.

Overhead cable accessories hold 57.9%, and underground accessories account for 42.1% of the market in 2025, with underground growing faster.

Key players include Key players in the cable accessories market include Nexans SA, The Prysmian Group, ABB Group, NKT A/S, and Taihan Cable & Solution Co., Ltd.

Key trends include smart IoT-enabled accessories, HVDC-rated high-voltage solutions, rising underground cabling adoption, and sustainability-driven material innovation.

North America holds a 19.7% share (2025), with a projected CAGR of ~5.8% through 2034, supported by smart grid upgrades and renewable energy investments.

High-voltage cable accessories are the fastest-growing voltage segment, driven by HVDC expansion, offshore wind farms, and long-distance transmission projects.

Asia Pacific's cable accessories market exceeded USD 25.4 Billion in 2025, accounting for over 40% of global revenues, with a strong outlook through 2034.

Cable accessories are critical for connecting solar, wind, and storage systems to the grid, requiring specialized waterproof, corrosion-resistant, and high-voltage-rated solutions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)