Cables and Connectors Market Size, Share, Trends and Forecast by Product Type, Installation Type, Vertical, and Region, 2026-2034

Cables and Connectors Market Size, Share, Trends & Forecast (2026-2034)

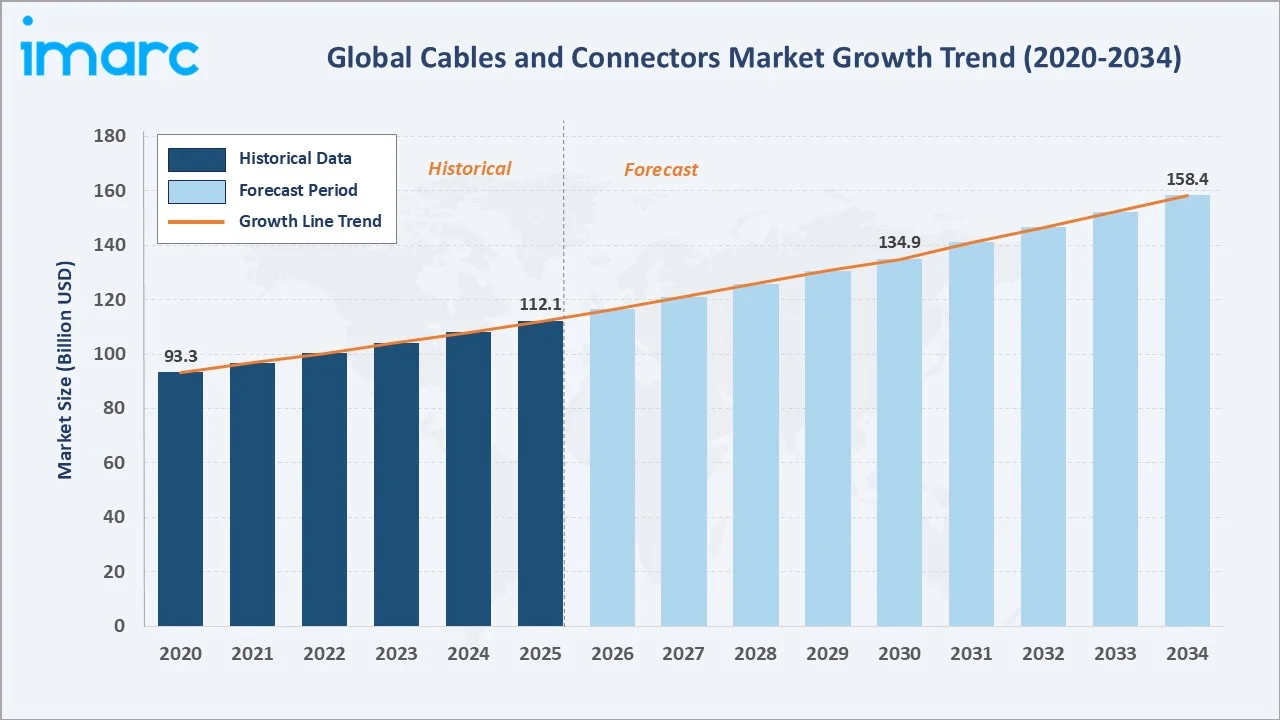

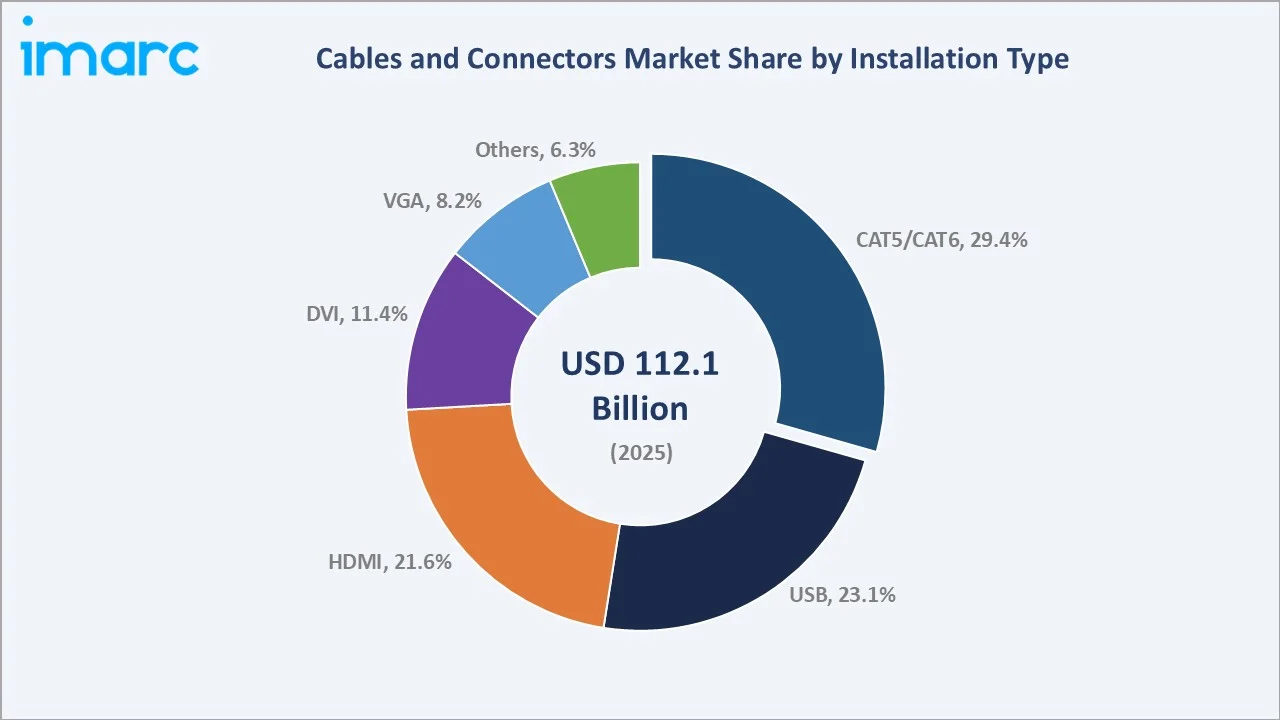

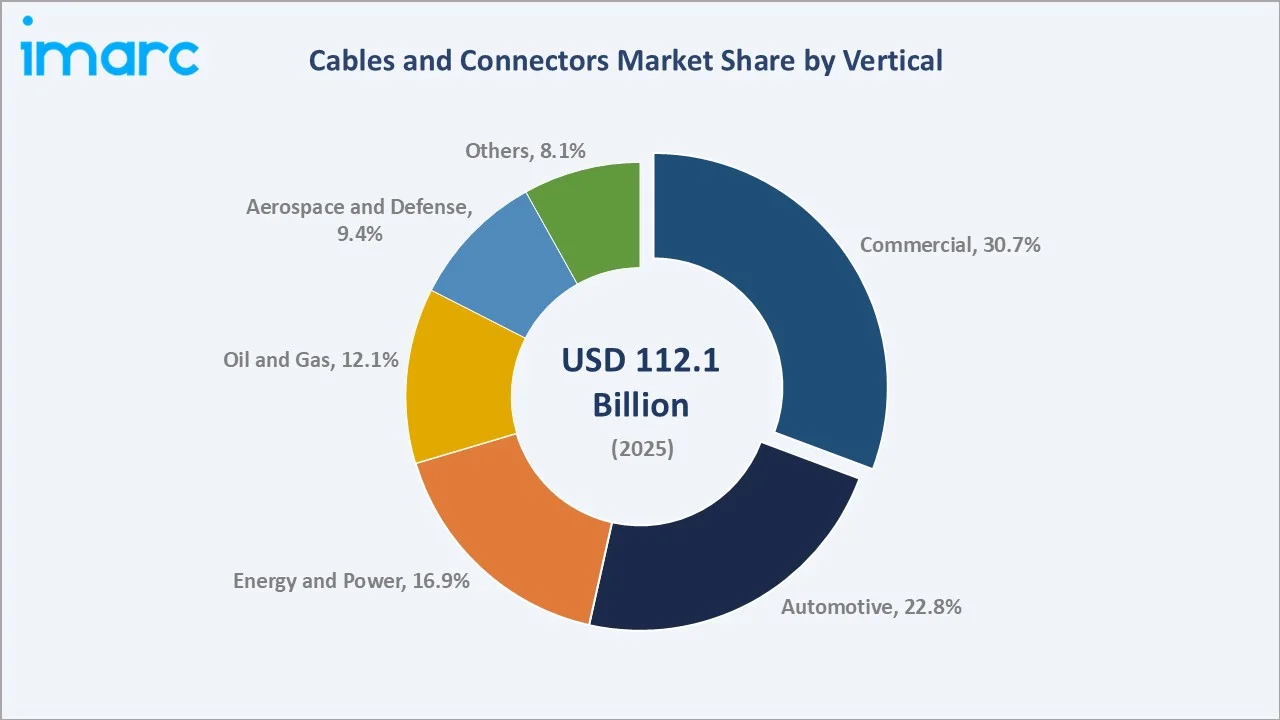

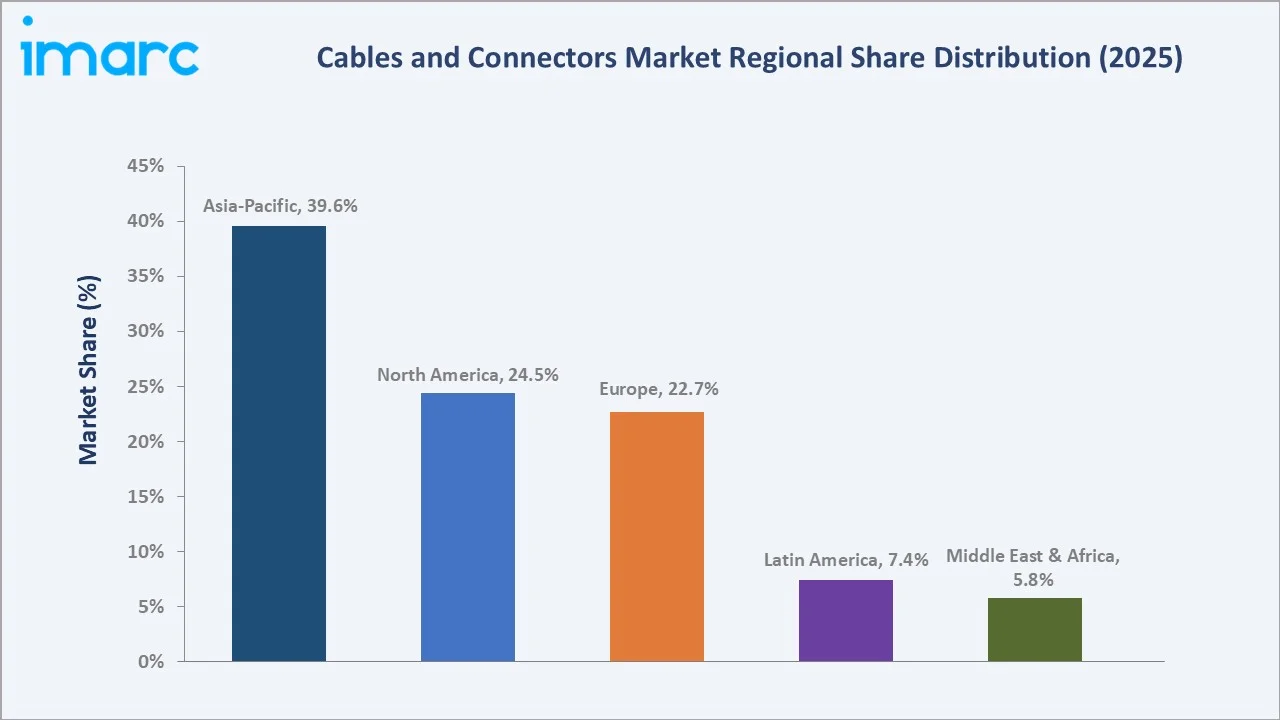

The global cables and connectors market reached USD 112.1 Billion in 2025 and is projected to reach USD 158.4 Billion by 2034, growing at a CAGR of 3.76% during 2026-2034. The market is driven by rising demand from telecom, data centers, consumer electronics, automotive, and industrial automation sectors. By the end of 2025, global 5G connections exceeded 2.7 billion, making 5G the fastest-growing mobile technology and positioning it to add nearly USD 1 Trillion to the global economy by 2030. This growth is driving the cables and connectors market by increasing demand for high-speed fiber, RF cables, antennas, backhaul connectors, and data transmission infrastructure. CAT5/CAT6 leads installation type at 29.4%. Commercial leads vertical at 30.7%. Asia-Pacific leads regionally at 39.6%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 112.1 Billion |

|

Forecast Market Size (2034) |

USD 158.4 Billion |

|

CAGR (2026-2034) |

3.76% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Installation Type |

CAT5/CAT6 (29.4%, 2025) |

|

Dominant Vertical |

Commercial (30.7%, 2025) |

|

Leading Region |

Asia-Pacific (39.6%, 2025) |

The global cables and connectors market grew from USD 93.3 Billion in 2020 to USD 112.1 Billion in 2025, supported by rising demand from telecom, data centers, automotive, and industrial sectors. It is projected to reach USD 134.9 Billion by 2030 as 5G rollout, cloud infrastructure, EVs, and automation increase the need for reliable connectivity solutions. By 2034, the market is forecast to reach USD 158.4 Billion, reflecting steady expansion across power, signal, and high-speed data transmission applications. Growth will be further supported by renewable energy projects, smart manufacturing, and increasing electronics penetration worldwide.

To get more information on this market, Request Sample

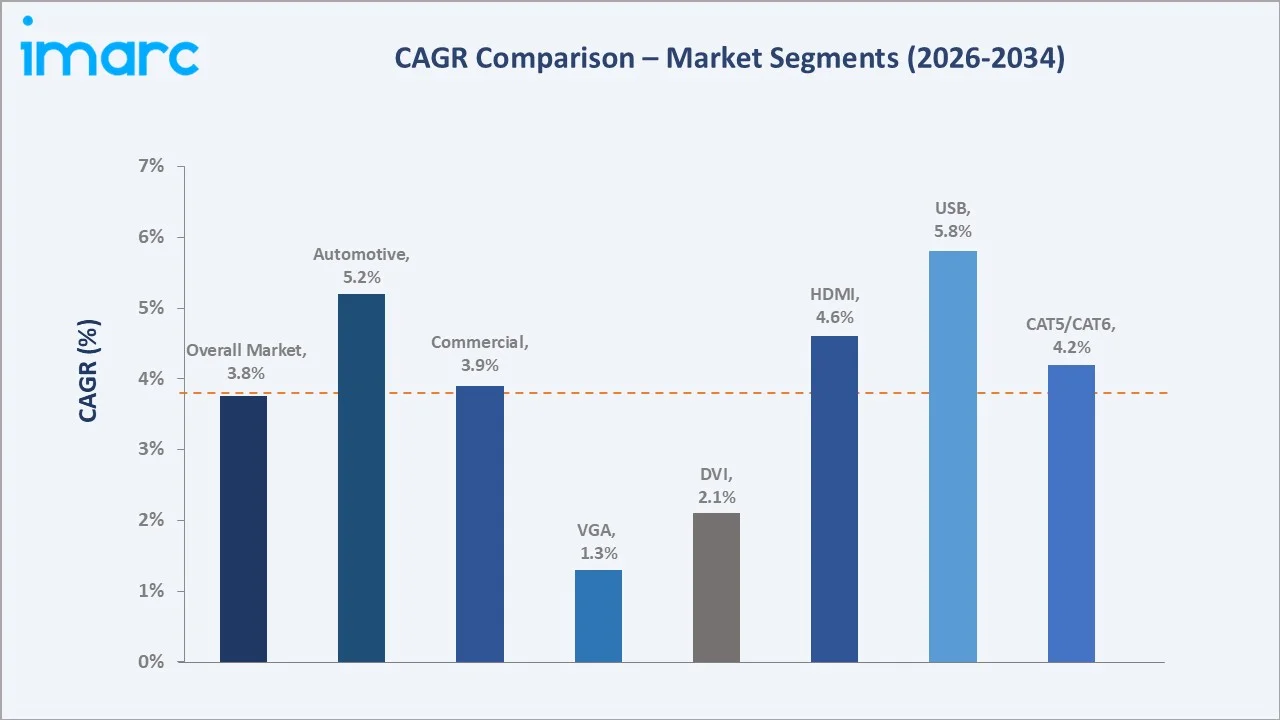

USB grows fastest at ~5.8% CAGR through USB-C universal standard adoption, USB4 version 2.0 / USB 80Gbps transition, and EV onboard USB-C charging integration. Automotive vertical grows at ~5.2% CAGR through EV 800V high-voltage harness, ADAS sensor cable proliferation, and OEM EV platform transition.

Executive Summary

The global cables and connectors market is growing steadily, driven by rising demand for high-speed data transmission, telecom networks, data centers, EVs, and industrial automation. The market expanded from USD 93.3 Billion in 2020 to USD 112.1 Billion in 2025 and is forecast to reach USD 158.4 Billion by 2034. Expanding 5G infrastructure, cloud computing, renewable energy projects, and smart manufacturing are increasing the need for reliable connectivity solutions. Automotive electrification and consumer electronics growth are further supporting demand. The market remains essential to digital infrastructure, power distribution, and connected industrial ecosystems.

CAT5/CAT6 at 29.4% leads through enterprise LAN and data center structured cabling volume. Commercial vertical at 30.7% leads through enterprise and data center cable demand. Asia-Pacific leads regionally at 39.6% through China's electronics manufacturing and Japan's automotive harness.

Key Market Insights

|

Insight |

Data |

|

Dominant Installation Type |

CAT5/CAT6 - 29.4% share (2025) |

|

Dominant Vertical |

Commercial - 30.7% market share (2025) |

|

Leading Region |

Asia-Pacific - 39.6% share (2025) |

|

Market Opportunity |

AI hyperscale data center 400G/800G optical cable; EV 800V high-voltage harness; offshore wind submarine cable; USB4 Gen 3 consumer cable; 5G fronthaul fiber-optic feeder cable |

Key Analytical Observations Supporting The Above Data:

- CAT5/CAT6 at 29.4%: CAT5/CAT6 cables dominate due to their widespread use in LAN networks, data centers, offices, and telecom infrastructure. Their cost-effectiveness, reliable performance, and ability to support high-speed data transmission make them preferred for enterprise and residential connectivity.

- Commercial at 30.7%: The commercial segment dominates due to extensive deployment across offices, data centers, telecom networks, retail facilities, and commercial buildings. Growing digitalization, cloud adoption, and demand for reliable power and data connectivity continue to drive strong commercial-sector demand.

- Asia-Pacific at 39.6%: Asia-Pacific dominates regionally due to large-scale electronics manufacturing, rapid 5G rollout, and strong infrastructure development across China, India, Japan, and South Korea.

Cables and Connectors Market Overview

The cables and connectors market operates as the infrastructure-enabling technology component market. The market spans power cables, signal cables, data cables, and specialized cables. The market is unique as it serves as a foundational enabler for both power delivery and high-speed data transmission across multiple industries. Its demand is closely linked to 5G rollout, data centers, EVs, renewable energy, industrial automation, and consumer electronics. The market also requires continuous product innovation in miniaturization, durability, bandwidth capacity, and heat resistance to support next-generation connected infrastructure.

The cables and connectors ecosystem integrates raw material suppliers, cable and connector manufacturers, contract manufacturing and EMS, distributors and system integrators, standards bodies, and commercial, automotive, energy, oil and gas, and aerospace end-user verticals. Macroeconomic factors include rising infrastructure investment, rapid urbanization, and expanding industrial production across major economies.

Market Dynamics

To evaluate market opportunities, Request Sample

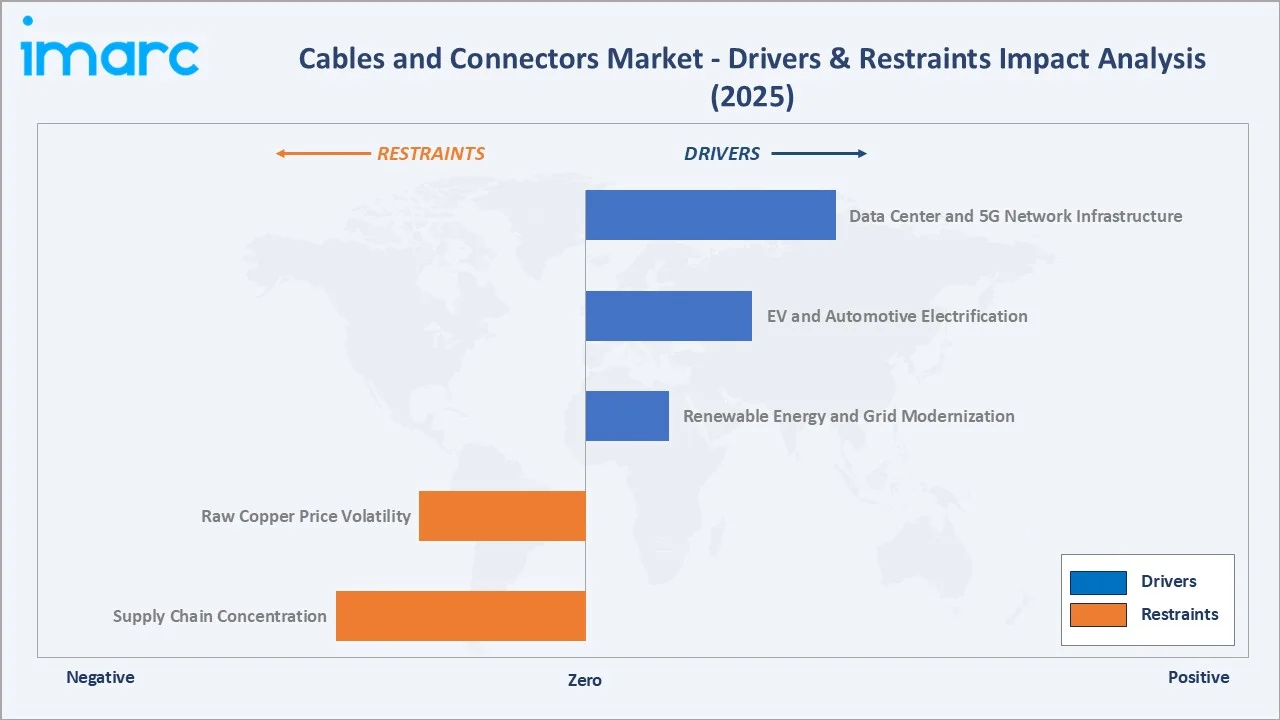

Market Drivers

- Data Center and 5G Network Infrastructure: There were approximately 11,800 data centers worldwide, as of March 2024. Government data indicates that India had 518,854 operational 5G base stations by the end of 2025. The rapid expansion of hyperscale data centers and 5G base stations is increasing demand for fiber optic cables, high-speed connectors, RF cables, and backhaul infrastructure. Growing cloud computing, edge computing, and AI workloads further amplify the need for robust connectivity systems. As telecom operators and enterprises invest in digital infrastructure, demand for advanced cables and connectors continues to rise.

- EV and Automotive Electrification: EV and automotive electrification are increasing the need for high-voltage power distribution, battery connectivity, charging systems, and electronic control units. Electric vehicles require a significantly higher number of specialized cables and connectors than conventional vehicles to support battery packs, inverters, motors, and onboard electronics. The expansion of EV charging infrastructure is also boosting demand for durable, high-performance connectivity solutions. As global EV adoption accelerates, manufacturers are investing in advanced cables and connectors capable of handling higher power loads, faster charging, and enhanced safety requirements.

- Renewable Energy and Grid Modernization: Renewable plants require durable cables and connectors for panels, inverters, turbines, substations, and grid connection systems. The U.S. electric grid is a major engineering achievement, comprising over 9,200 power generation units with more than 1 million megawatts of capacity, connected through over 600,000 miles of transmission lines. Grid upgrades also need advanced high-voltage, fiber optic, and control cables to support digital monitoring and efficient power distribution. As clean energy investment rises globally, demand for specialized connectivity solutions continues to expand.

Market Restraints

- Raw Copper Price Volatility: Raw copper price volatility hampers the market as copper is a key input material for power cables, wiring, and many connector components. Fluctuating copper prices increase production costs and make pricing less predictable for manufacturers. This can squeeze profit margins, delay procurement decisions, and raise final product prices for customers. High volatility also makes long-term contracts and project budgeting more challenging across telecom, power, construction, and industrial sectors.

- Supply Chain Concentration: Supply chain concentration hampers the market as production often depends on a limited number of suppliers for copper, aluminum, polymers, semiconductors, and precision connector components. Any disruption in key manufacturing hubs can lead to material shortages, longer lead times, and higher procurement costs. This affects project execution across telecom, data centers, EVs, renewables, and industrial sectors. High dependence on concentrated suppliers also limits flexibility and makes manufacturers more vulnerable to geopolitical risks, trade restrictions, and logistics delays.

Market Opportunities

- AI Hyperscale Data Center 400G and 800G Optical Cable: AI hyperscale data center 400G and 800G optical cable infrastructure presents a major opportunity as AI workloads require ultra-high-speed data transmission between servers, storage systems, and networking equipment. The deployment of hyperscale data centers is increasing demand for advanced fiber-optic cables, high-density connectors, and low-latency interconnect solutions capable of supporting 400G and 800G speeds. As cloud providers and AI companies expand computing capacity, investment in next-generation connectivity infrastructure is accelerating.

- EV 800V High-Voltage Harness and Charging Infrastructure: EV 800V high-voltage harness and charging infrastructure represent a significant opportunity as automakers transition to 800V vehicle architectures to enable faster charging and improved energy efficiency. These systems require advanced high-voltage cables, connectors, and wiring harnesses capable of handling greater power loads and thermal demands. The expansion of ultra-fast DC charging networks is further increasing demand for durable, high-performance connectivity solutions. Global EV sales reached 1.8 million units in May 2026. As EV adoption accelerates globally, investment in 800V platforms is expected to drive substantial growth in specialized cable and connector technologies.

Market Challenges

- Intense Price Competition Among Manufacturers: Intense price competition among manufacturers is putting constant pressure on selling prices and profit margins. Many manufacturers compete on cost, especially in standardized products such as LAN cables, wiring, and basic connectors. This can limit investment in product innovation, quality improvement, and advanced manufacturing capabilities. Price-led competition also increases the risk of low-quality or counterfeit products entering the market, affecting customer trust and long-term industry profitability.

- Counterfeit and Low-Quality Cable Products: Counterfeit and low-quality cable products undermine product reliability, safety, and performance. These products often fail to meet industry standards, increasing the risk of electrical faults, network failures, fire hazards, and equipment damage. Their lower prices create unfair competition for reputable manufacturers and pressure margins across the industry. Additionally, the presence of counterfeit products can erode customer trust and increase maintenance and replacement costs for end users.

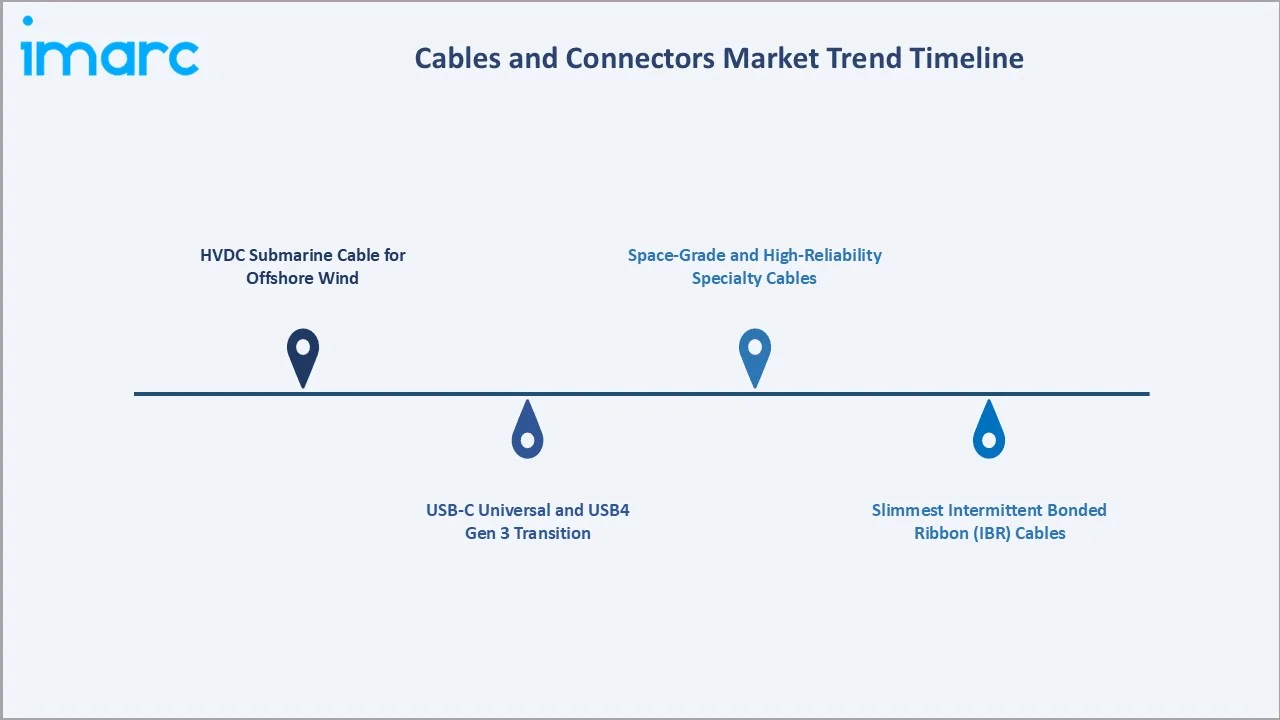

Emerging Market Trends

1. HVDC Submarine Cable for Offshore Wind

HVDC submarine cable for offshore wind is emerging as offshore wind farms are being developed farther from shore. HVDC submarine cables enable efficient long-distance power transmission with lower energy losses compared to conventional AC systems. These cables are critical for connecting offshore wind projects to onshore grids and supporting large-scale renewable integration. Rising investment in offshore wind and cross-border grid interconnections is increasing demand for advanced, high-capacity submarine cable solutions.

2. USB-C Universal and USB4 Gen 3 Transition

USB-C universal and USB4 Gen 3 transition is emerging as devices increasingly shift toward standardized, high-speed, multi-purpose connectivity. USB-C supports charging, data transfer, and video output through a single connector, increasing adoption across smartphones, laptops, tablets, and peripherals. USB4 Gen 3 further supports faster data transfer, higher bandwidth, and improved compatibility with advanced devices. This transition is driving demand for high-quality cables and connectors that can support faster charging, durability, and next-generation data performance.

3. Slimmest Intermittent Bonded Ribbon (IBR) Cables

Slimmest intermittent bonded ribbon (IBR) cables are emerging as telecom operators and data centers require higher fiber density in limited duct and rack space. IBR designs allow more fibers to be packed into compact cables while maintaining flexibility and easier installation. They support faster network expansion for 5G, FTTH, cloud, and hyperscale data center applications. In September 2025, Sterlite Technologies Inc., STL’s U.S. subsidiary, developed one of the world’s slimmest optical fiber cables for data center operators, hyperscalers, and telecom providers in the United States. Its Celesta IBR Cable packs 864 fibers into an 11.7 mm cable diameter and is designed for efficient jetting in 14 mm ducts. The cable can be installed over around 4,700 ft in under 20 minutes and uses bend-insensitive 200-micron fiber to improve installation performance. As demand for high-capacity optical networks rises, slim IBR cables are gaining traction for efficient, space-saving fiber deployment.

4. Space-Grade and High-Reliability Specialty Cables

Space-grade and high-reliability specialty cable is emerging as satellites, launch vehicles, defense systems, and aerospace electronics require cables that perform under extreme conditions. These cables must withstand radiation, vibration, temperature variation, vacuum exposure, and strict safety standards. Rising satellite launches, space exploration programs, and defense modernization are increasing demand for lightweight, durable, and high-performance specialty cables. This creates opportunities for manufacturers offering certified, mission-critical cable and connector solutions.

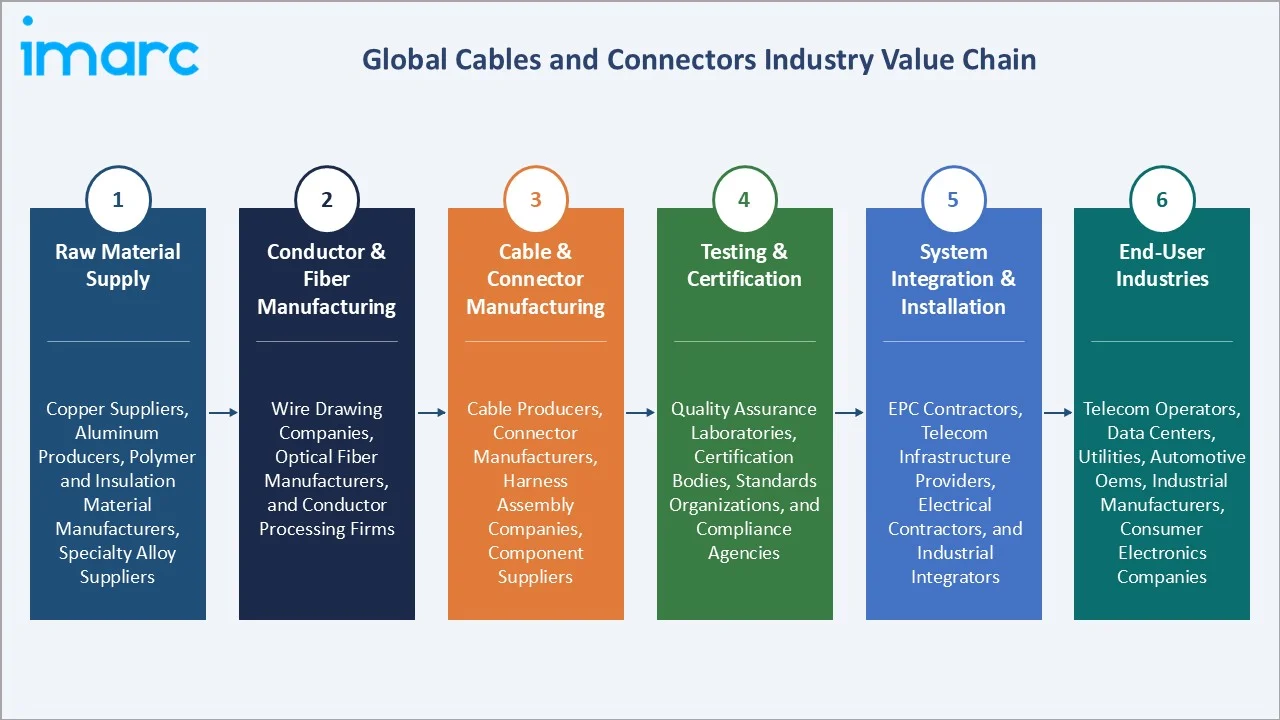

Industry Value Chain Analysis

The cables and connectors value chain integrates raw material supply, conductor & fiber manufacturing, cable & connector manufacturing, testing & certification, system integration & installation, and end-user industries.

|

Stage |

Key Participants |

|

Raw Material Supply |

Copper suppliers, aluminum producers, polymer and insulation material manufacturers, specialty alloy suppliers |

|

Conductor & Fiber Manufacturing |

Wire drawing companies, optical fiber manufacturers, and conductor processing firms |

|

Cable & Connector Manufacturing |

Cable producers, connector manufacturers, harness assembly companies, component suppliers |

|

Testing & Certification |

Quality assurance laboratories, certification bodies, standards organizations, and compliance agencies |

|

System Integration & Installation |

EPC contractors, telecom infrastructure providers, electrical contractors, and industrial integrators |

|

End-User Industries |

Telecom operators, data centers, utilities, automotive OEMs, industrial manufacturers, consumer electronics companies |

Cable & connector manufacturing is the most value-added stage in the value chain because it transforms raw conductors, fibers, and materials into specialized products designed for specific performance requirements. Product differentiation is driven by innovation in bandwidth capacity, durability, miniaturization, thermal management, and safety. Manufacturers create significant value through engineering expertise, quality control, and application-specific customization for telecom, EV, renewable energy, and industrial markets.

Technology Landscape in the Cables and Connectors Industry

High-Speed Data Cable Technology

High-speed data cable technology enables faster and more reliable data transmission for data centers, cloud computing, AI workloads, and 5G networks. Advances in fiber-optic cables, high-density connectors, and low-loss transmission materials support growing bandwidth requirements and reduced latency. These technologies are essential for 400G, 800G, and next-generation networking applications. As digital infrastructure expands globally, demand for high-performance data connectivity solutions continues to accelerate.

Fast-Charging Connector Technology

Fast-charging connector technology enables higher power delivery, improved thermal management, and faster energy transfer for EVs, consumer electronics, and industrial systems. Advanced connector designs support high-current applications while maintaining safety, durability, and efficiency. Innovations in materials, cooling mechanisms, and compact form factors are helping meet the requirements of ultra-fast charging infrastructure. As EV adoption and high-power electronic devices continue to grow, demand for next-generation fast-charging connectors is increasing rapidly.

Rural Broadband Fiber Network Expansion

Rural broadband fiber network expansion is increasing demand for high-performance fiber-optic cables, connectors, and last-mile connectivity solutions. Governments and telecom operators are investing heavily in fiber deployment to extend high-speed internet access to underserved and remote areas. This is driving innovation in compact, easy-to-install, and cost-efficient fiber cable designs that reduce deployment time and infrastructure costs. In November 2024, Prysmian introduced EcoSpan cables with FlexRibbon technology, a new fiber and connectivity solution aimed at improving rural broadband deployment. The low fiber-count cable is designed for easy splicing as either ribbons or individual fibers, installs like a drop cable using P-Clamps, and is available in 24F to 72F configurations. As digital inclusion initiatives accelerate globally, advanced fiber connectivity technologies are becoming a key focus area for the industry.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

External Cables and Connectors |

🔒 |

2025 |

|

Installation Type |

CAT5/CAT6 |

29.4% |

2025 |

|

Vertical |

Commercial |

30.7% |

2025 |

|

Region |

Asia-Pacific |

39.6% |

2025 |

By Installation Type

CAT5/CAT6 leads at 29.4% (2025), through enterprise LAN structured cabling, data center top-of-rack copper, and CAT6A 10GBASE-T.

To access detailed market analysis, Request Sample

USB at 23.1% grows fastest at ~5.8% CAGR through USB-C universal standard, USB4 version 2.0 / USB 80Gbps transition, and EU USB-C mandate. HDMI at 21.6% reflects HDMI 2.1 48Gbps premium display. DVI at 11.4% and VGA at 8.2% reflect legacy-display transitioning installed base. Others at 6.3% include Thunderbolt 4, DisplayPort 2.1, and coaxial.

By Vertical

Commercial leads at 30.7% (2025), through enterprise LAN, data center, commercial building structured cabling, and retail AV installation.

Automotive at 22.8% grows fastest at ~5.2% CAGR through EV 800V HV harness, ADAS sensor cable, and OEM EV platform transition. Energy and power at 16.9% reflect offshore wind HVDC submarine, grid modernization, and solar farm cable. Oil and gas at 12.1% reflects subsea umbilical, topsides, and refinery cable. Aerospace and defense at 9.4% reflect MIL-SPEC connector and space-grade cable. Others at 8.1% include healthcare, marine, and rail.

Regional Market Insights

|

Region |

Share (2025) |

Key Cables and Connectors Market Drivers & Characteristics |

|

Asia-Pacific |

39.6% |

Driven by large-scale electronics manufacturing, rapid 5G deployment, expanding data center capacity, and strong investments in EVs, renewable energy, and industrial automation. |

|

North America |

24.5% |

Benefits from robust demand from hyperscale data centers, cloud computing, AI infrastructure, EV charging networks, and grid modernization projects. |

|

Europe |

22.7% |

Supported by renewable energy expansion, offshore wind developments, EV production, and smart grid deployment. |

|

Latin America |

7.4% |

Witnessing growing demand from telecom network expansion, infrastructure modernization, renewable energy projects, and increasing digital connectivity. |

|

Middle East and Africa |

5.8% |

Driven by smart city initiatives, power transmission projects, data center investments, and expanding telecom infrastructure. |

Asia-Pacific leads the global cables and connectors market with a 39.6% share in 2025, supported by strong electronics manufacturing, 5G rollout, EV production, and industrial automation. North America follows with 24.5%, driven by hyperscale data centers, AI infrastructure, cloud computing, and grid modernization. Europe holds 22.7%, backed by renewable energy expansion, offshore wind projects, EV adoption, and strict safety standards.

Latin America accounts for 7.4%, with growth supported by telecom expansion and infrastructure upgrades. The Middle East and Africa represent 5.8%, driven by smart cities, power transmission projects, and rising data center investments.

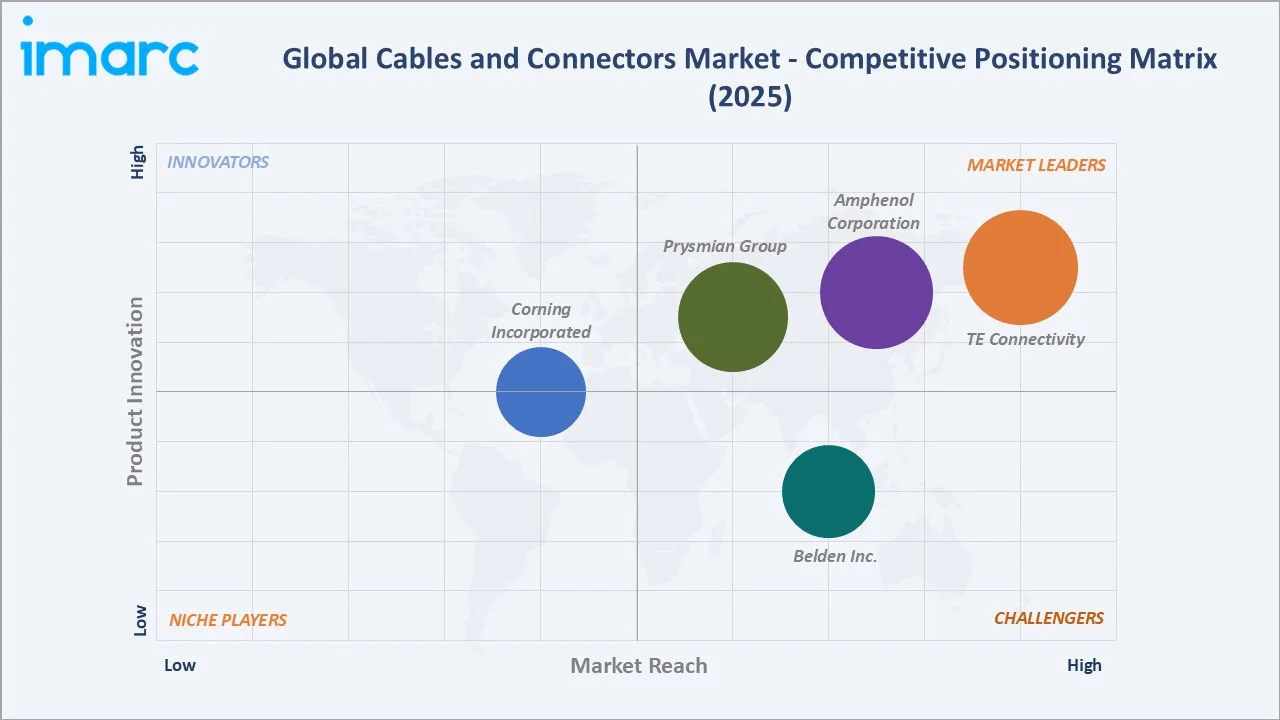

Competitive Landscape

The global cables and connectors market is moderately fragmented, with competition driven by product quality, technological innovation, manufacturing scale, and global distribution capabilities. Leading companies focus on expanding their portfolios in fiber-optic cables, high-speed data connectivity, EV charging systems, renewable energy applications, and industrial automation solutions.

|

Company |

Key Products |

Market Position |

Core Strength |

|

TE Connectivity |

Automotive Connectors, Circular Connectors, Docking Connectors, Fiber Optic Connectors, PCB Connectors, RF Connectors, Socket Connectors |

Market Leader |

TE Connectivity is a global industrial technology leader that designs and manufactures highly engineered electrical power connectors and wire and cable products. |

|

Amphenol Corporation |

0.21mm Super Low Profile FPC connector, 0.30mm FPC Connectors, 0.50mm FFC/FPC Connectors, 0.50mm Pitch FFC/FPC Autolock Connectors, 0.80mm Board-to-Board Connectors |

Market Leader |

Amphenol Corporation is a global leader in the design, manufacturing, and marketing of electrical, electronic, and fiber optic connectors. Their role involves enabling the seamless transmission of power, data, and signals across diverse industries. |

|

Prysmian Group |

Railway Cables, HV cables for Pipelines & LNG, Power Link Submarine Cable Solutions |

Market Leader |

Prysmian Group is a leading global player in the cable systems industry. The company provides the critical infrastructure required for both global power transmission and digital telecommunications. |

|

Belden Inc. |

Multi-Pair Cable, Flat Ribbon Cable, Multi-Conductor Cable, RS-485 Cable, RS-232 & RS-423 Cable, RS-422 Cable, Power Connectors, Sensor Actuator Connectors, Data Connectors, Valve Connectors, Single Pair Ethernet (SPE) Connectors |

Strong Challenger |

Belden Inc. designs, manufactures, and distributes end-to-end networking, security, and connectivity products. Their role revolves around supplying high-performance cables, connectors, and networking devices for demanding industries. |

|

Corning Incorporated |

Indoor Simplex Cable Assemblies, Indoor Duplex Cable Assemblies, Indoor Multifiber Cable Assemblies, Outdoor Simplex Cable Assemblies, Outdoor Duplex Cable Assemblies, Outdoor Multifiber Cable Assemblies |

Established Player |

Corning Incorporated is widely recognized for igniting the global communications revolution by inventing the first low-loss optical fiber. The company serves as the foundational manufacturer for the high-speed internet, data center, and AI computing infrastructure. |

Market participants are investing in advanced materials, high-density connectivity, and next-generation transmission technologies to address growing demand from data centers, telecom networks, and electrification projects. Strategic acquisitions, capacity expansions, and long-term supply agreements are common competitive strategies. As digital infrastructure, 5G, AI data centers, and EV adoption accelerate, companies are increasingly competing on performance, reliability, and application-specific customization.

Key Company Profiles

TE Connectivity

TE Connectivity Ltd. is a global leader in connectivity and sensor solutions, serving the automotive, industrial, telecommunications, aerospace, defense, energy, and consumer electronics sectors. The company designs and manufactures a broad portfolio of connectors, cable assemblies, terminals, relays, antennas, and high-speed interconnect solutions used in mission-critical applications.

- Key Products: Automotive Connectors, Circular Connectors, Docking Connectors, Fiber Optic Connectors, PCB Connectors, RF Connectors, Socket Connectors.

- Recent Developments: In March 2026, TE Connectivity introduced its 56G MezzaWave connectors and cable assemblies, designed to support high-performance applications such as edge AI, data centers, industrial automation, robotics, and aerospace and defense systems.

- Strategic Focus: Expanding its leadership in the cables and connectors market through the development of high-speed connectivity, power distribution, and miniaturized interconnect solutions.

Amphenol Corporation

Amphenol Corporation is one of the largest manufacturers of electronic and fiber-optic connectors, interconnect systems, cable assemblies, and related connectivity products. The company serves a diverse range of industries, including telecommunications, data communications, automotive, aerospace, defense, industrial automation, mobile devices, and renewable energy.

- Key Products: 0.21mm Super Low Profile FPC connector, 0.30mm FPC Connectors, 0.50mm FFC/FPC Connectors, 0.50mm Pitch FFC/FPC Autolock Connectors, 0.80mm Board-to-Board Connectors.

- Recent Developments: In February 2026, Amphenol RF introduced single-crimp N-Type connectors to its expanding interconnect portfolio. These connectors simplify field installation by allowing cable attachment with a single ferrule crimp, removing the need for separate contact crimping. The connectors are suitable for antennas, base stations, radar systems, and other applications requiring quick installation with minimal tools.

- Strategic Focus: Strengthening its position in the cables and connectors market through continuous innovation in high-speed interconnects, fiber-optic connectivity, power distribution systems, and advanced cable assemblies.

Market Concentration Analysis

The global cables and connectors market is moderately fragmented, with a mix of large multinational manufacturers and numerous regional suppliers competing across end-use industries. Leading companies such as TE Connectivity, Amphenol Corporation, Prysmian Group, Belden Inc., and Corning Incorporated hold strong positions through extensive product portfolios, global manufacturing networks, and long-term customer relationships. Market leadership is driven by technological innovation in fiber optics, high-speed data connectivity, EV charging systems, and industrial automation solutions. While standard cable products face intense price competition, specialized segments such as data center connectivity, renewable energy cables, aerospace interconnects, and high-voltage applications remain more concentrated. Strategic acquisitions, capacity expansions, and R&D investments continue to shape competitive dynamics across the industry.

Investment & Growth Opportunities

Highest Growth Segments

USB (~5.8% CAGR), automotive (~5.2% CAGR), AI data center 400G/800G optical cable (~12-15% CAGR from premium segment), HVDC submarine cable (~8-10% CAGR through offshore wind), aerospace and defense specialty (~4.5% CAGR), and 5G antenna feeder (~6-8% CAGR through 5G base station) represent cables and connectors highest-growth investment vectors through 2034.

Investment Themes

- EV 800V high-voltage harness and DC fast charging cables: The transition to 800V EV architectures is creating strong investment opportunities in high-voltage wiring harnesses, connectors, and DC fast-charging cables. As automakers seek faster charging times and improved vehicle efficiency, demand for advanced power transmission and thermal-management cable solutions is rising rapidly.

- HVDC submarine cables: HVDC submarine cables represent a major investment theme driven by offshore wind expansion, cross-border power interconnections, and grid modernization projects. These high-capacity cables enable efficient long-distance electricity transmission with lower losses, creating significant opportunities for manufacturers specializing in advanced power cable technologies and installation services.

Future Market Outlook (2026-2034)

The global cables and connectors market is projected to grow from USD 112.1 Billion in 2025 to USD 158.4 Billion by 2034, growing at a 3.76% CAGR over the forecast period. This reflects steady demand from 5G networks, data centers, EVs, renewable energy, and industrial automation. The 2030 anchor value of USD 134.9 Billion indicates a product-upgrade inflection point, where demand shifts toward high-speed, high-voltage, compact, and application-specific connectivity solutions. Growth will be supported by fiber optics, 400G/800G data cables, EV charging connectors, HVDC submarine cables, and smart grid applications. As digital and electrification infrastructure expands, cables and connectors will remain critical enabling components across industries.

Three structural forces define the cables and connectors market growth through 2034. First, the rapid expansion of 5G networks, cloud computing, AI infrastructure, and hyperscale data centers is driving demand for high-speed fiber-optic cables and advanced connectivity solutions. Second, the global shift toward electrification, including electric vehicles, EV charging infrastructure, renewable energy projects, and smart grids, is increasing demand for high-voltage cables and power connectors. Third, growing investments in industrial automation, smart manufacturing, and digital infrastructure modernization are accelerating the adoption of specialized, high-performance cable and connector technologies.

Research Methodology

Primary Research

Primary research comprised detailed interviews with cable manufacturers, connector suppliers, telecom operators, data center operators, automotive OEMs, renewable energy developers, distributors, and industry experts. Discussions focused on demand trends, technology adoption, raw material dynamics, pricing strategies, and end-use industry requirements. Insights were gathered on fiber-optic deployment, EV connectivity, industrial automation, and high-speed data transmission applications.

Secondary Research

Secondary research encompassed company annual reports, investor presentations, industry publications, trade databases, government infrastructure reports, and regulatory documents. It included analysis of telecom rollout, data center expansion, EV charging infrastructure, renewable energy projects, and grid modernization trends. Company press releases, product launches, and technology updates were reviewed to assess competitive developments.

Forecasting Models

Forecasting models used top-down and bottom-up approaches based on historical demand, end-use industry growth, and regional infrastructure investment trends. The projections incorporated 5G rollout, data center expansion, EV adoption, renewable energy deployment, and industrial automation growth. CAGR modeling, scenario analysis, and expert validation were applied to estimate market performance through 2034.

Cables and Connectors Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Internal Cables and Connectors, External Cables and Connectors |

| Installation Types Covered | HDMI, USB, VGA, DVI, CAT5/CAT6, Others |

| Verticals Covered | Automotive, Commercial, Oil and Gas, Energy and Power, Aerospace and Defense, Others |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | TE Connectivity, Amphenol Corporation, Prysmian Group, Belden Inc., Corning Incorporated, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cables and connectors market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global cables and connectors market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cables and connectors industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cables and Connectors Market Report

The global cables and connectors market reached USD 112.1 Billion in 2025, driven by rising demand for high-speed data transmission, 5G network expansion, and hyperscale data center growth. Increasing EV adoption, renewable energy projects, and grid modernization are boosting demand for high-voltage cables and power connectors. Industrial automation, smart manufacturing, and expanding consumer electronics usage further support steady market growth.

The global cables and connectors market grows at 3.76% CAGR during 2026-2034, reaching USD 158.4 Billion by 2034. The CAGR reflects AI hyperscale data center premium cable, EV automotive harness electrification, HVDC submarine offshore wind cable, USB-C universal adoption, and 5G antenna cable.

CAT5/CAT6 leads at 29.4% due to its widespread use in offices, commercial buildings, LAN networks, and data communication systems. Its affordability, easy installation, and reliable high-speed performance make it a preferred choice for enterprise and residential connectivity.

Commercial leads at 30.7% due to high demand from offices, data centers, telecom facilities, retail spaces, and commercial buildings. Growing digital infrastructure, reliable power distribution needs, and high-speed network connectivity requirements continue to support strong adoption in this segment.

Asia-Pacific leads at 39.6% due to large-scale electronics manufacturing, rapid 5G deployment, and strong infrastructure development across China, India, Japan, and South Korea. Expanding EV production, data center capacity, renewable energy projects, and industrial automation further support regional dominance.

Leading companies include TE Connectivity, Amphenol Corporation, Prysmian Group, Belden Inc., and Corning Incorporated, among others.

The market is projected to reach USD 134.9 Billion by 2030, reflecting steady demand from digital infrastructure, EVs, renewables, and industrial automation. This milestone indicates a product-upgrade phase, with stronger adoption of high-speed data cables, fiber optics, high-voltage connectors, and application-specific connectivity solutions.

Three priority investment opportunities are emerging in the cables and connectors market. First, EV 800V high-voltage harnesses and DC fast-charging cables are benefiting from rapid vehicle electrification and charging infrastructure expansion. Second, HVDC submarine cables are seeing strong demand from offshore wind projects and cross-border power transmission networks. Third, AI hyperscale data centers and 400G/800G optical connectivity solutions are creating significant opportunities in high-speed fiber-optic cables and advanced interconnect technologies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)