Calcined Anthracite Market Size, Share, Trends and Forecast by Technology, Application, End Use Industry, and Region, 2026-2034

Calcined Anthracite Market Size and Trends:

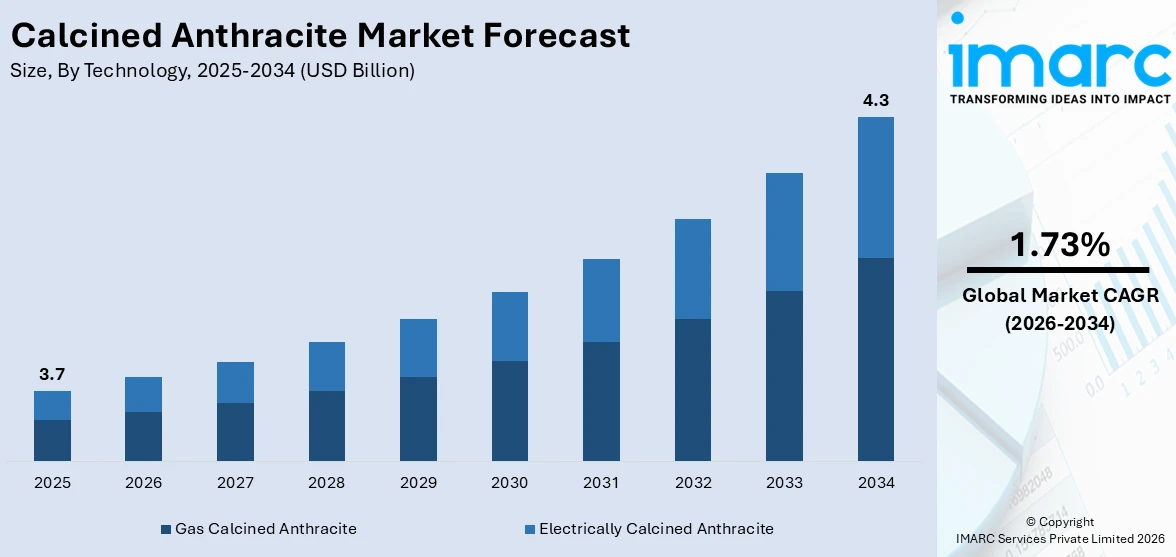

The global calcined anthracite market size reached USD 3.7 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 4.3 Billion by 2034, exhibiting a growth rate CAGR of 1.73% during 2026-2034. Asia Pacific currently dominates the market, holding a market share of over 37.8% in 2025. The market is experiencing significant growth mainly driven by the rising demand in steel manufacturing, aluminum smelting and other industrial applications. Rising focus on cleaner energy sources and technological advancements further bolster its market expansion globally.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 3.7 Billion |

|

Market Forecast in 2034

|

USD 4.3 Billion |

| Market Growth Rate (2026-2034) | 1.73% |

The global calcined anthracite market is mainly driven by its growing use in steelmaking and aluminum production due to high carbon content and thermal efficiency. According to industry reports, in October 2024, global steel production reached 151.2 million tons marking a 0.4% increase as compared to the same month in previous year. Additionally, production rose by 5.3% compared to September 2024. The rising demand for cleaner energy sources has amplified its application in filtration and water treatment. Expanding industrial activities particularly in emerging economies and advancements in manufacturing technologies further drive market growth. Additionally, stringent environmental regulations encourage industries to adopt low-ash and eco-friendly materials like calcined anthracite, thereby boosting its demand across diverse applications.

To get more information on this market Request Sample

The United States calcined anthracite market is mainly driven by the increasing demand from steel and aluminum industries where its high carbon purity and thermal efficiency enhance production processes. The widespread adoption of eco-friendly materials aligns with stringent environmental regulations boosting its use in filtration and water treatment systems. Expanding infrastructure projects and industrial development further fuel the demand for calcined anthracite in refractory applications. In line with this, in October 2024, The Biden-Harris Administration announced over $4.2 billion in funding for 44 infrastructure projects, with key allocations including $472.3 million for Boston's North Station renovations and $217.2 million for Philadelphia's SouthPort terminal expansion. These infrastructural expansion projects are expected to facilitate the demand for calcined anthracite, thereby driving the market further toward growth. Additionally, advancements in technology and a focus on reducing greenhouse gas emissions contribute to its popularity as a cleaner energy source. Rising investments in sustainable manufacturing practices also support the market's growth trajectory in the United States.

Calcined Anthracite Market Trends:

Rising Demand from the Steel Manufacturing Sector

Calcined anthracite is widely used as a carbon additive in steel production due to its high carbon content and low impurities. The global steel market reached USD 942.3 Billion in 2023, with global steel projected to grow at a CAGR of 3.3% from 2024 to 2032 driven by construction and infrastructure projects demand for calcined anthracite is steadily increasing. The ten largest steel producers in the world are China, India, Japan, the United States, Russia, South Korea, Turkey, Germany, Brazil, and Iran. These countries are also one of the largest consumers of Calcium Anthracite owing to the huge steel industry. The steel industry consumed over 50% of calcined anthracite and this share is expected to grow further as manufacturers prioritize high-quality raw materials for efficiency and sustainability.

Growth in the Aluminum Smelting Industry

The aluminum industry relies on calcined anthracite as a key material in cathode blocks and electrodes. The global aluminium market size is expected to exhibit a growth rate (CAGR) of 4.71% during 2024-2032 fueled by increasing demand from the automotive and packaging sectors. According to the data by International Aluminium Organization, total production of aluminum stood at 131,188 thousand metric tonnes with China producing the highest amount of production at 77,700 thousand metric tonnes. The need for lightweight and corrosion-resistant aluminum is growing thus major producers like China and India are increasing their smelting facilities. The industry's transition to sustainable practices and improvements in smelting technologies are also propelling the use of calcined anthracite because of its effectiveness and reduced environmental impact.

Increasing Energy Efficiency and Low-Carbon Initiatives

One major factor propelling the calcined anthracite market is the demand for greater energy efficiency and adherence to low carbon policies. Because of its high purity and energy efficient qualities which lower emissions and improve process efficiency calcined anthracite is being used by industries all over the world. Governments and businesses are encouraging the use of ecofriendly materials in industrial processes to meet global carbon reduction targets like the Paris Agreement. For example, the use of calcined anthracite in water filtration systems and electric arc furnaces supports environmentally friendly industrial methods.

Calcined Anthracite Industry Segmentation:

IMARC Group provides an analysis of the key trends in each sub-segment of the global calcined anthracite market report, along with forecasts at the global, regional, and country level from 2026-2034. Our report has categorized the market based on technology, application, and end use industry.

Analysis by Technology:

- Gas Calcined Anthracite

- Electrically Calcined Anthracite

Gas Calcined Anthracite leads the market with around 69.8% of market share in 2025. Gas calcined anthracite leads the calcined anthracite market due to its superior carbon content, consistent quality and reduced impurities as compared to electrically calcined variants. Produced using gas fired furnaces it offers high thermal efficiency and better control over the calcination process ensuring uniformity in product characteristics. Its widespread application in steelmaking, aluminum smelting and other industrial processes underscores its dominance. The material's ability to improve furnace efficiency and reduce emissions aligns with the industry's focus on sustainability and cost-effectiveness. Additionally, growing industrialization and infrastructure development globally further bolster the demand for gas calcined anthracite solidifying its market leadership.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Pulverized Coal Injection (PCI)

- Basic Oxygen Steelmaking

- Electric Arc Furnaces

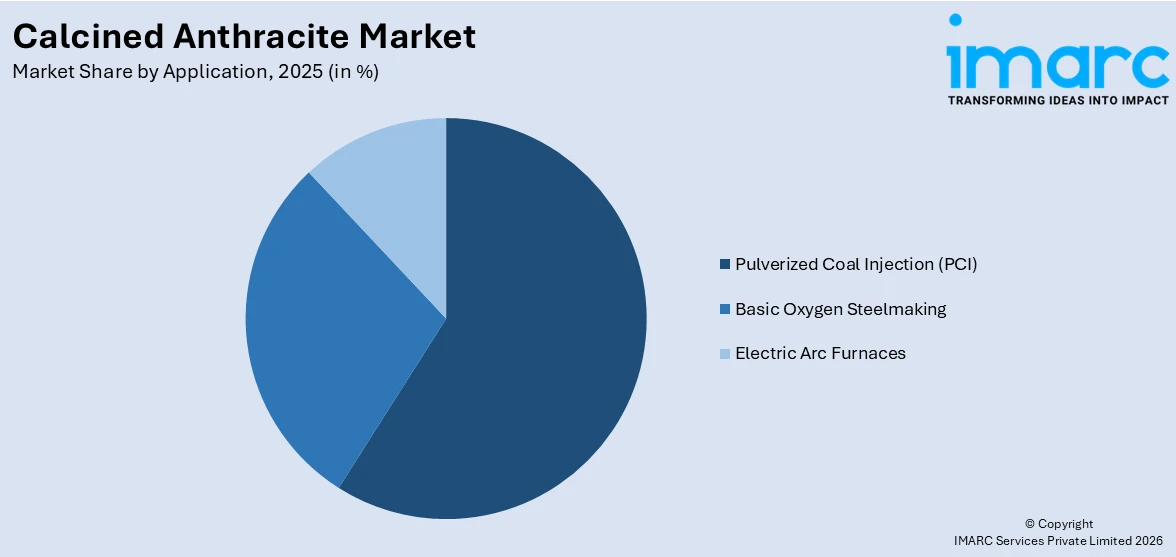

Pulverized Coal Injection (PCI) leads the market with around 58.6% of market share in 2025. Pulverized coal injection (PCI) dominates the calcined anthracite market by application due to its extensive use in the steelmaking industry. PCI involves injecting fine coal particles into blast furnaces as a cost effective and efficient fuel source replacing coke partially. Calcined anthracite with its high carbon content and low ash levels enhances combustion efficiency and reduces impurities making it an ideal choice for PCI. The growing demand for steel in construction, automotive and infrastructure projects further propel the adoption of PCI techniques. Additionally, PCI's ability to lower carbon footprints aligns with environmental regulations reinforcing its leadership in the calcined anthracite market.

Analysis by End Use Industry:

- Iron and Steel

- Aluminum

- Pulp and Paper

- Power Generation

- Water Filtration

- Others

Iron and steel lead the market with around 48.4% of market share in 2025. The iron and steel industry is the leading end-user of calcined anthracite due to its critical role in enhancing production efficiency and product quality. With its high carbon content and low impurities calcined anthracite is extensively used as a carbon raiser in steelmaking and a reducing agent in iron production. It improves the thermal performance of blast furnaces, reduces slag formation, and minimizes energy consumption. The increasing demand for steel in construction, automotive, and infrastructure projects globally drives the market. Furthermore, the industry's focus on sustainability and cost optimization reinforces the adoption of calcined anthracite as a preferred material.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

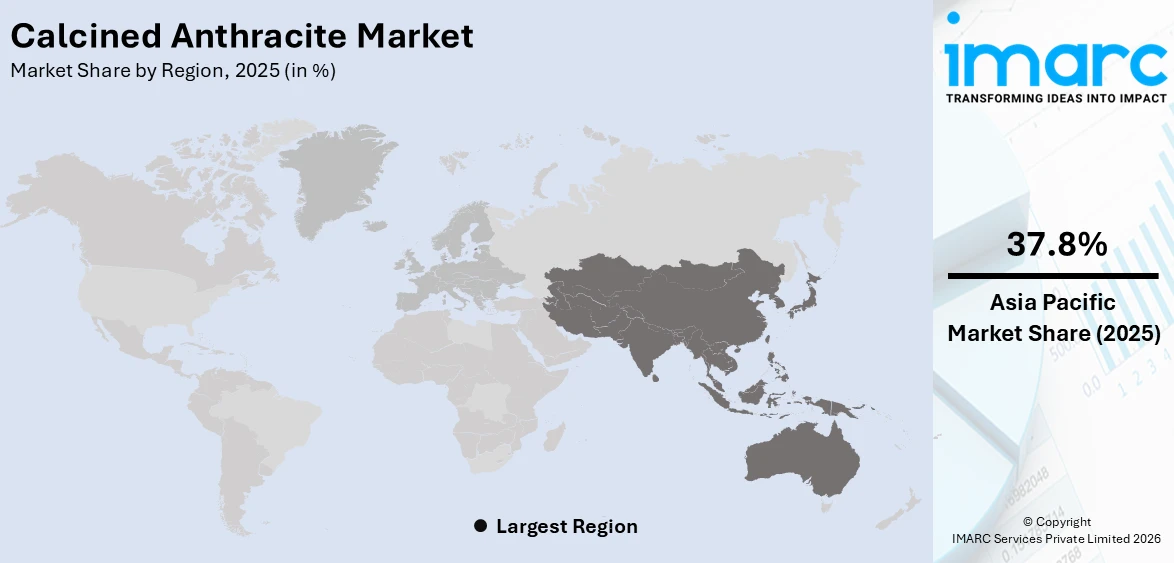

In 2025, Asia Pacific accounted for the largest market share of over 37.8%. In 2025, Asia Pacific dominated the calcined anthracite market accounting for the largest share due to the region's expanding industrial and manufacturing sectors. Rapid urbanization and infrastructure development in countries like China and India drive significant demand for steel and aluminum key industries utilizing calcined anthracite. For instance, in December 2023, China's National Development and Reform Commission announced the first batch of nearly 2,900 infrastructure projects funded by special government bonds. Focused on post-flood recovery in the Beijing-Tianjin-Hebei region it includes projects for public asset restoration and disaster prevention supported by one trillion yuan in bonds. The presence of abundant raw materials and cost-effective production capabilities further bolster the region's leadership. Additionally, increasing investments in transportation, construction, and energy projects contribute to market growth. Supportive government policies promoting industrialization and sustainable practices enhance calcined anthracite adoption solidifying Asia Pacific's position as the largest market for this material globally.

Key Regional Takeaways:

North America Calcined Anthracite Market Analysis

The North American calcined anthracite market is propelled by the robust steel and aluminum industries particularly in the United States and Canada. With increasing adoption of electric arc furnaces (EAFs) for sustainable steel production calcined anthracite serves as a crucial recarburizer supporting efforts to reduce carbon emissions. The region’s emphasis on renewable energy projects drives demand for aluminum where calcined anthracite is integral in the smelting process. Infrastructure initiatives such as Canada’s Investing in Canada Plan and the U.S. Bipartisan Infrastructure Law further boost steel and aluminum consumption. Advanced manufacturing capabilities and a well-developed supply chain enhance production efficiency while policies encouraging domestic raw material sourcing reduce import dependency. Additionally, the region’s focus on lightweight materials for automotive and aerospace industries strengthens market growth.

United States Calcined Anthracite Market Analysis

In 2025, United States accounted for a share of 89.20% of the North America market. The steel and aluminium industries which depend on calcined anthracite for its high carbon content, low sulphur and better thermal and electrical conductivity are the main drivers of the market for this material in the United States. One of the main drivers is the increasing use of electric arc furnaces (EAFs) which use calcined anthracite as a recarburizer in the manufacturing of steel. Demand for calcined anthracite as a cleaner carbon additive has increased because of the United States steel market's transition to sustainable production methods where the full-year 2023 net earnings from steel stood at USD 895 Million. Additionally, the aluminum industry, which uses calcined anthracite in the smelting process has grown because of the increased emphasis on renewable energy projects.

The market for calcined anthracite is being driven by government infrastructure programs such as the Bipartisan Infrastructure Law which allots USD 1.2 Trillion for construction and maintenance projects. These initiatives are also increasing demand for steel and aluminum. The market has grown because of the existence of sophisticated production facilities and an emphasis on lowering carbon emissions. To lessen reliance on imports the United States is also placing a strong emphasis on domestic raw material procurement which will support domestic calcined anthracite manufacturing.

Europe Calcined Anthracite Market Analysis

The demand for decarbonization in industrial processes and strict environmental requirements are driving the calcined anthracite industry in Europe. To reach net zero carbon emissions by 2050 the European Union's Green Deal encourages businesses to switch to low emission substitutes like calcined anthracite. Europe produces 152 Million tons of steel annually on average with a turnover of about €130 Billion (USD 137 Billion) according to data from the European Steel Association. Millions more European residents are employed directly or indirectly by more than 500 steel producing facilities spread throughout 22 EU Member States.

Aluminum production where calcined anthracite is essential to the smelting process has increased due to the growing need for lightweight materials in the automotive and aerospace industries. The demand for aluminum is rising because of significant investments made in the production of electric vehicles (EVs) by nations like Germany, France, and Italy. Calcined anthracite now has more uses in secondary steelmaking processes thanks to Europe's emphasis on circular economy principles which include metal recycling. Additionally, region benefits from a strong supply chain network and cutting-edge technology skills.

Latin America Calcined Anthracite Market Analysis

The expanding need for steel and aluminum in the energy, automotive and construction industries is driving the calcined anthracite market in Latin America. With a steel industry that produces more than 36,000 thousand tons a year. Brazil the largest country in the region is a major player. The use of calcined anthracite as a carbon ingredient in steel production has expanded because of infrastructure building projects in nations including Argentina, Brazil and Mexico. Investments in renewable energy and lightweight materials to produce automobiles have contributed to the steady growth of the aluminum sector especially in Brazil. Additionally, calcination facilities have a local supply base because to the region's mining activity and natural anthracite reserves. However, obstacles including volatile energy prices and unstable economies in some nations could hinder industry expansion.

Middle East and Africa Calcined Anthracite Market Analysis

Infrastructure development is the primary driver of the calcined anthracite market in the Middle East and Africa (MEA) region especially in the Gulf Cooperation Council (GCC) nations where massive construction projects like NEOM City in Saudi Arabia are currently under way. Calcined anthracite is being used more often in manufacturing operations as the steel and aluminum industries grow to satisfy the demands of these projects. The mining and metallurgical sectors in Africa which use calcined anthracite for smelting and refining are expanding in nations like South Africa and Nigeria. The market is expanding due to the growing need for lightweight materials in the aerospace and automotive industries.

Competitive Landscape:

The calcined anthracite market is characterized by intense competition among manufacturers, driven by the growing demand in steelmaking, aluminum smelting, and filtration applications. Key players emphasize technological advancements to enhance product quality and reduce emissions, aligning with sustainability trends. Companies compete on cost efficiency, supply chain optimization, and product customization to cater to diverse industrial needs. Regional manufacturers benefit from access to abundant raw materials, while global entities leverage advanced production techniques and extensive distribution networks. The market also witnesses strategic investments in capacity expansion and partnerships to address rising demand, particularly in emerging economies with infrastructure and industrial growth.

The report has also provided a comprehensive analysis of the competitive landscape in the global calcined anthracite market. Detailed profiles of all major companies have also been provided. Some of the companies covered include:

- Asbury Carbon

- Black Diamond (Clarus Corporation)

- Dev Technofab Ltd.

- Elkem ASA (Orkla ASA)

- Headwin Exim Private Limited

- Henan Star Metallurgy Material Co.Ltd

- Jh Carbon Pty Ltd

- Kingstone Group

- Resorbent s.r.o.

- Rheinfelden Carbon Products GmbH

- Sojitz JECT Corporation

- Voltcon International PTE Limited

Recent Developments:

- November 2024: India's Ministry of Steel has detected the import of steel products that fail to meet mandatory quality standards, raising concerns over non-compliance with Bureau of Indian Standards (BIS) certifications. This issue highlights risks to domestic industries and public safety. The ministry is enhancing monitoring mechanisms and enforcement to ensure adherence to quality regulations. Such measures aim to prevent the influx of substandard imports and protect local manufacturers.

- November 2024: Japan's Kobe Steel has announced plans to begin in-house production of corrosion-resistant steel sheets with a new investment. This initiative aims to meet growing demand in sectors like construction and infrastructure by enhancing product durability and reducing reliance on external suppliers. The investment will involve upgrading existing facilities to ensure efficient production while maintaining high-quality standards.

- March 2024: The U.S. government is exploring a reboot of its aluminum industry with plans for a new aluminum smelter, aiming to reduce reliance on imports and bolster domestic production. This initiative is driven by the critical role of aluminum in defense, automotive, and renewable energy sectors. The project seeks to address supply chain vulnerabilities while promoting eco-friendly and energy-efficient technologies in smelting processes.

Calcined Anthracite Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Gas Calcined Anthracite and Electrically Calcined Anthracite |

| Applications Covered | Pulverized Coal Injection (PCI), Basic Oxygen Steelmaking and Electric Arc Furnaces |

| End Use Industries Covered | Iron and Steel, Aluminum, Pulp and Paper, Power Generation, Water Filtration and Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Asbury Carbon, Black Diamond (Clarus Corporation), Dev Technofab Ltd., Elkem ASA (Orkla ASA), Headwin Exim Private Limited, Henan Star Metallurgy Material Co.Ltd, Jh Carbon Pty Ltd, Kingstone Group, Resorbent s.r.o., Rheinfelden Carbon Products GmbH, Sojitz JECT Corporation, and Voltcon International PTE Limited |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, Calcined Anthracite market forecast, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global Calcined Anthracite market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Calcined Anthracite industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Calcined Anthracite Market Report

Calcined anthracite is a high-grade, heat-treated form of anthracite coal characterized by its elevated carbon content and minimal impurities. Primarily utilized as a carbon additive in steelmaking and aluminum smelting, it offers superior thermal efficiency and enhances various industrial processes through its consistent quality and reduced emission potential.

The calcined anthracite market was valued at USD 3.7 Billion in 2025.

IMARC estimates the global calcined anthracite market to exhibit a CAGR of 1.73% during 2026-2034.

Key factors include increasing demand in steel and aluminum production due to high carbon content and thermal efficiency, a rising focus on cleaner energy sources, technological advancements, expanding industrial activities in emerging economies, and stringent environmental regulations promoting eco-friendly materials.

In 2025, Gas Calcined Anthracite represented the largest segment by technology, driven by its superior carbon content, consistent quality, and reduced impurities.

Pulverized Coal Injection (PCI) leads the market by application owing to its extensive use in the steelmaking industry as a cost-effective and efficient fuel source.

The Iron and Steel segment is the leading segment by end-use industry, driven by its critical role in enhancing production efficiency and product quality in steel manufacturing.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, wherein Asia Pacific currently dominates the global market.

Some of the major players in the global calcined anthracite market include Asbury Carbon, Black Diamond (Clarus Corporation), Dev Technofab Ltd., Elkem ASA (Orkla ASA), Headwin Exim Private Limited, Henan Star Metallurgy Material Co.Ltd, Jh Carbon Pty Ltd, Kingstone Group, Resorbent s.r.o., Rheinfelden Carbon Products GmbH, Sojitz JECT Corporation, and Voltcon International PTE Limited etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)