Calcium Chloride Market Size, Share, Trends and Forecast by Product Type, Application, Raw Material, Grade, and Region 2026-2034

Global Calcium Chloride Market Size, Share, Trends & Forecast (2026-2034)

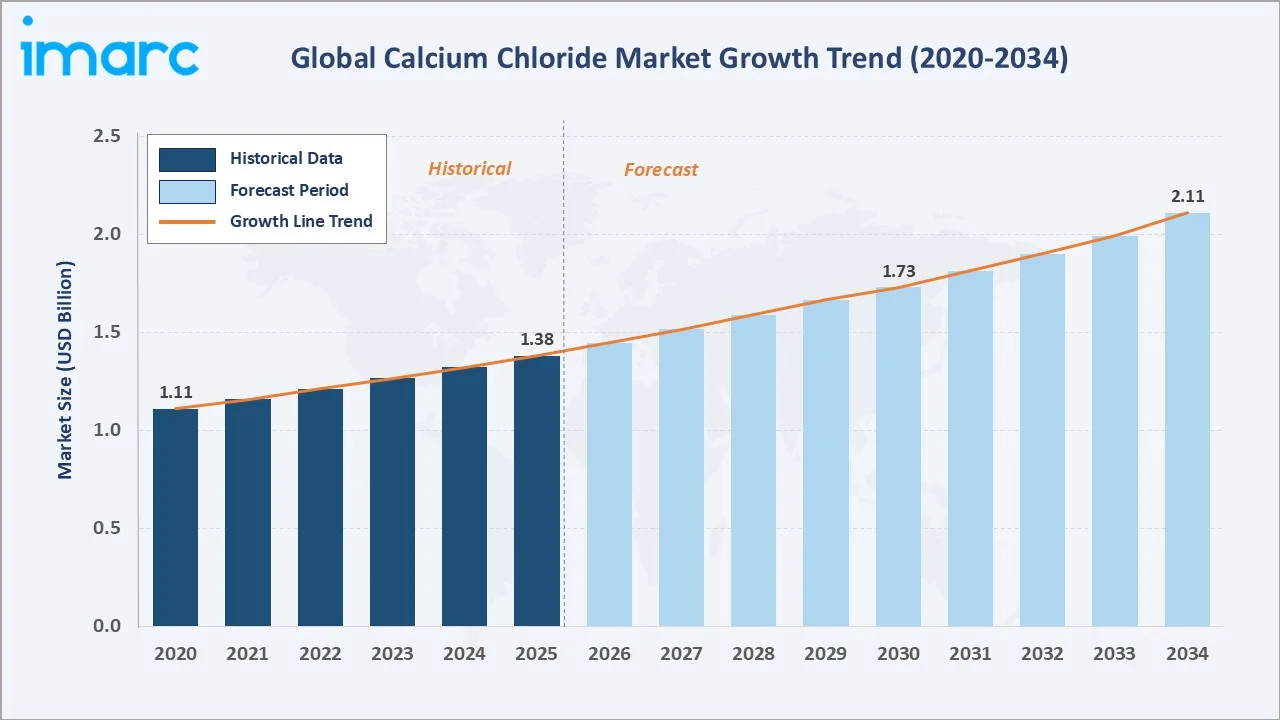

The global calcium chloride market reached USD 1.38 Billion in 2025 and is projected to reach USD 2.11 Billion by 2034, exhibiting a CAGR of 4.53% during 2026-2034. Growth is driven by broadening de-icing applications, rising dust control and road stabilization activity, growing oilfield drilling demand, and increasing adoption in food and pharmaceutical processing.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.38 Billion |

|

Forecast Market Size (2034) |

USD 2.11 Billion |

|

CAGR (2026-2034) |

4.53% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.4% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

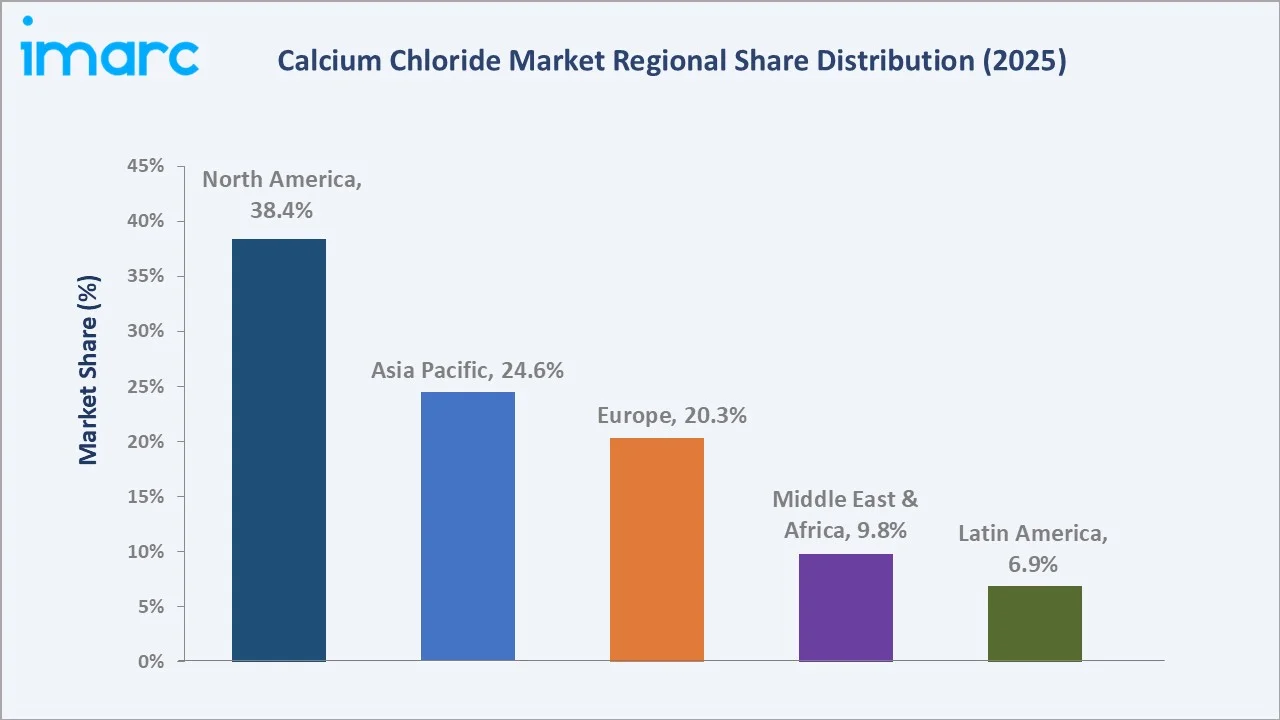

North America leads with 38.4% revenue share in 2025, supported by harsh winters and well-established industrial infrastructure. The global calcium chloride market is experiencing steady growth, driven by its widespread use in various industries such as construction, chemical processing, road maintenance, and de-icing applications. As a versatile compound,

To get more information on this market, Request Sample

With the growing focus on infrastructure development and the need for sustainable solutions, the Calcium Chloride market is poised for continued expansion, especially in regions with harsh winter conditions or expanding construction activities.

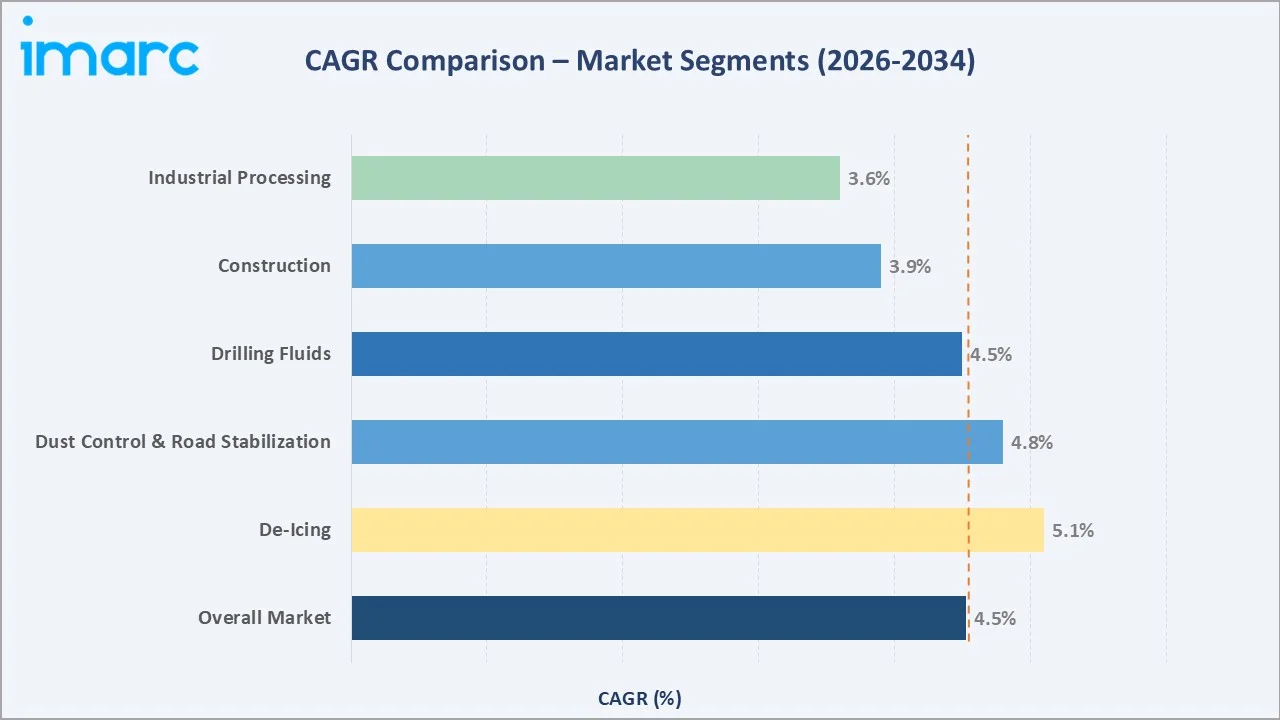

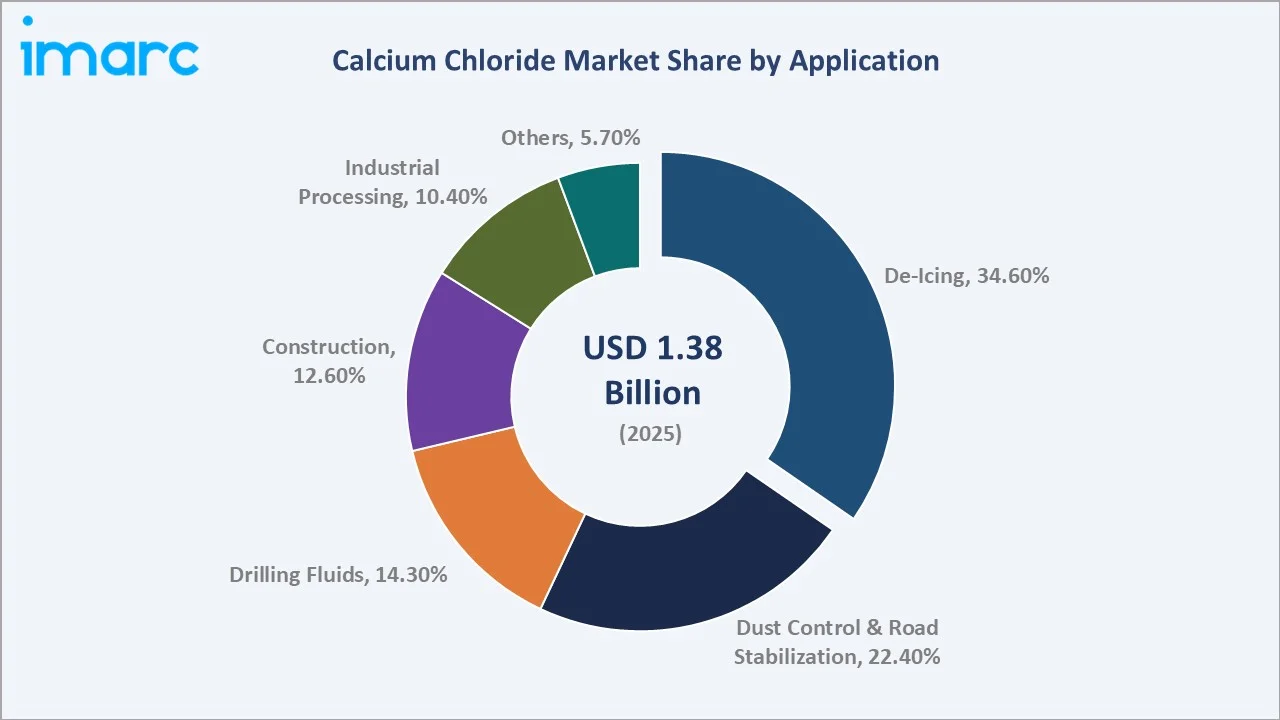

De-Icing leads all application segments with a projected CAGR of 5.1% (2026–2034), driven by expanding municipal road safety budgets. Dust control and road stabilization follow at 4.8% CAGR, while drilling fluids and construction segments register 4.5% and 3.9%, respectively, through the forecast period.

Executive Summary

The global calcium chloride market is on a sustained growth trajectory, underpinned by diverse industrial demand, expanding infrastructure activity, and the compound's exceptional chemical versatility. Valued at USD 1.38 Billion in 2025, the market is forecast to reach USD 2.11 Billion by 2034 at a CAGR of 4.53%.

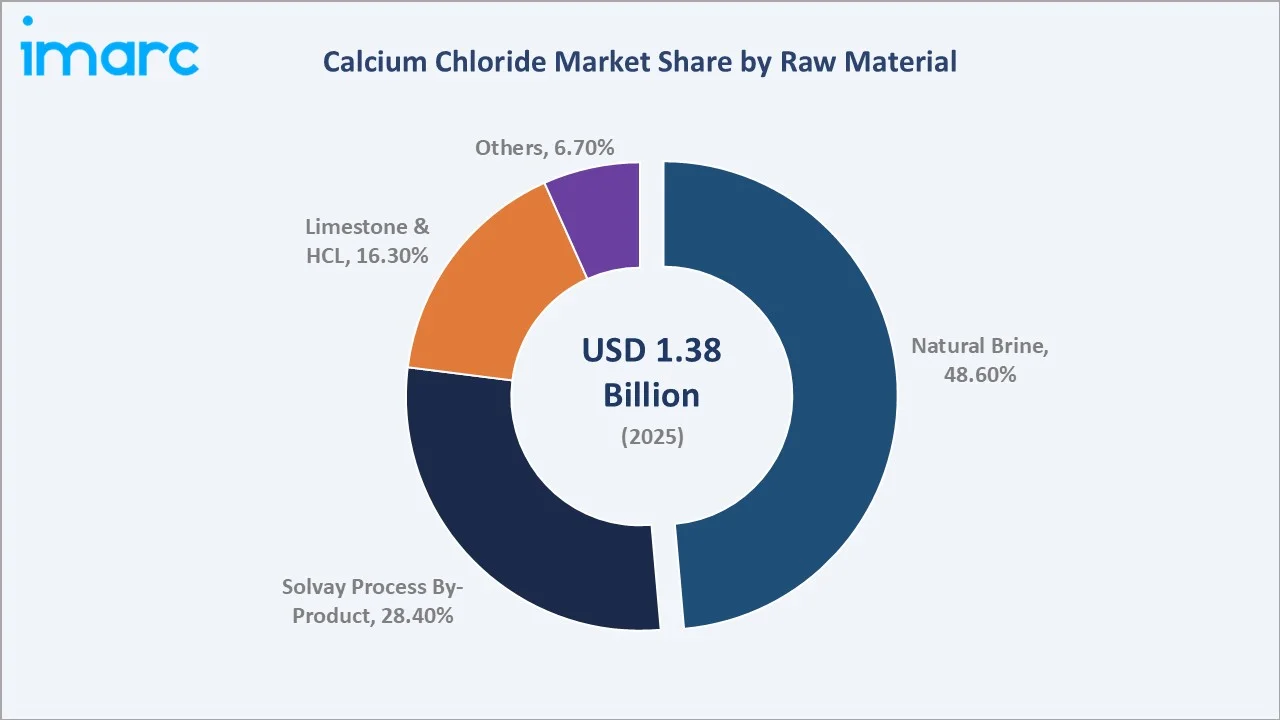

De-icing commands the largest application share at 34.6% in 2025, driven by government road safety mandates across North America and Northern Europe. Dust control and road stabilization follow at 22.4%, gaining momentum from expanding mining and unpaved road networks. Natural brine commands 48.6% as the most cost-efficient raw material production pathway for industry.

North America dominates with 38.4% share in 2025, anchored by production at TETRA Technologies Inc.. Asia Pacific is the fastest-growing region, with China, India, and Southeast Asian markets driving accelerated demand through rapid urbanization and oilfield activity. The top five producers hold approximately 55-60% of global capacity, reflecting moderate market concentration.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Application) |

De-Icing – 34.6% share (2025) |

|

Largest Segment (Raw Material) |

Natural Brine – 48.6% share (2025) |

|

Leading Region |

North America – 38.4% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (rapid industrialization & construction) |

|

Top Companies |

TETRA Technologies, Inc., Solvay, Tangshan Sanyou Group, Ward Chemical Inc. |

|

Market Opportunity |

Food & pharma-grade premium segments growing at 5%+ CAGR through 2034 |

Key Analytical Observations Supporting The Above Data:

- De-Icing dominates application demand at 34.6% share (2025). Government road safety mandates across North America and Europe require calcium chloride procurement for seasonal ice and snow management operations annually.

- Natural brine is the leading raw material at 48.6% (2025), favored for cost-efficiency at established operations in Michigan, Ohio, and China's Sichuan province.

- North America generates 38.4% of global revenues (2025), anchored by TETRA Technologies Inc.'s vertically integrated oilfield supply chain.

- Asia Pacific is the fastest-growing region, with China's construction boom, India's infrastructure drive, and expanding oilfield exploration accelerating calcium chloride demand through 2034.

- Drilling fluids represent 14.3% of application demand (2025), reflecting calcium chloride's critical role as a high-density, low-corrosivity brine base for oil and gas completion and workover operations.

- Food and pharma-grade premium segments are growing at 5%+ CAGR through 2034, driven by tightening food safety standards, dairy industry adoption, and pharmaceutical processing requirements.

Global Calcium Chloride Market Overview

Calcium chloride (CaCl₂) is an inorganic salt with exceptional hygroscopic and exothermic dissolution properties, making it commercially indispensable across industrial, municipal, and food processing applications globally. The market spans raw material extraction from natural brine wells, limestone-HCl reactions, and soda ash by-product streams through large-scale chemical processing plants into diversified end-use sectors.

The compound's functional versatility positions it as an irreplaceable material across road de-icing, dust suppression, oilfield drilling fluid formulation, concrete acceleration, food preservation, and pharmaceutical manufacturing. Macroeconomic drivers, including urbanization, infrastructure investment cycles, energy sector capital expenditure, and climate-driven winter weather variability, reinforce structural demand globally.

By 2034, calcium chloride is expected to be a critical procurement category across multiple countries. The market's resilience to economic cycles reflects its essential role in public infrastructure maintenance and irreplaceable function in oilfield operations, both facing limited substitution risk from alternative chemical compounds.

Market Dynamics

To evaluate market opportunities, Request Sample

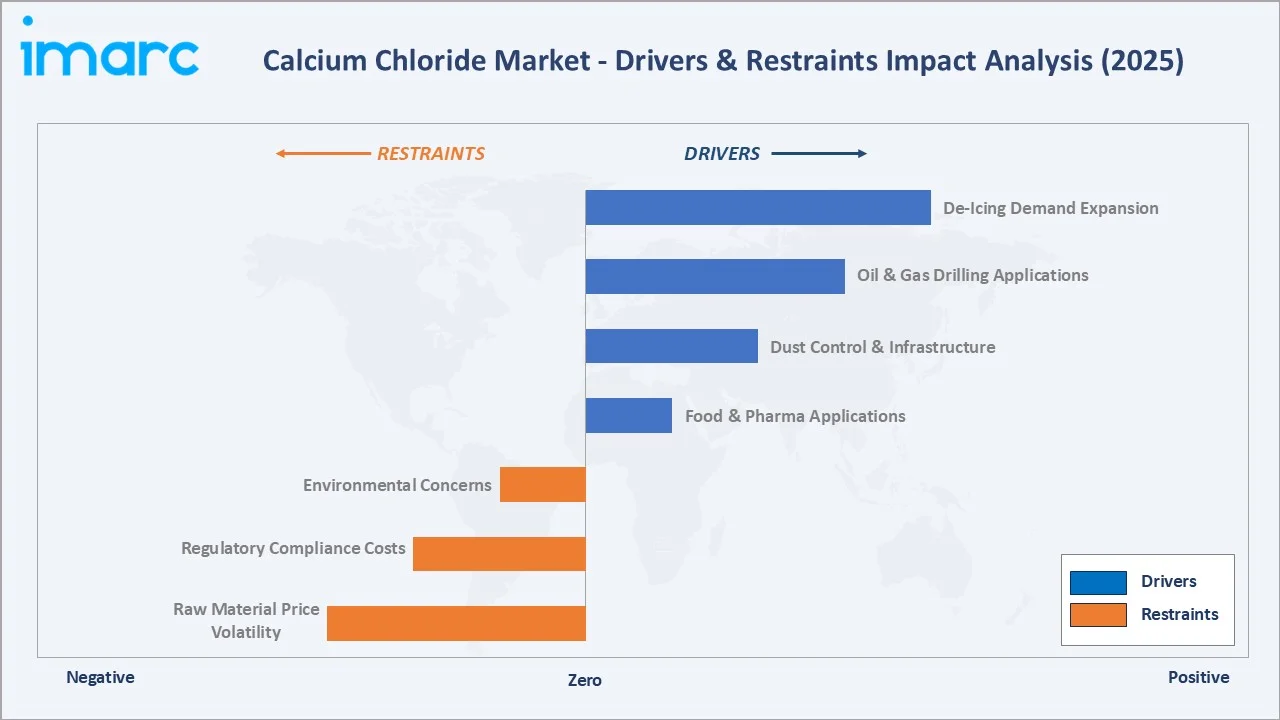

Market Drivers

- Increasing De-Icing Demand: Calcium chloride's effectiveness at -30°C, versus -10°C for rock salt, drives preference in severe winter climates. Government road safety mandates sustain high-volume institutional procurement, with the de-icing segment registering 5.1% CAGR through 2034.

- Growing Dust Control and Soil Stabilization: Mining and construction industries rely on calcium chloride's hygroscopic properties to suppress road dust. Environmental regulations on airborne particulates are accelerating adoption, with dust control applications registering 4.8% CAGR through 2034.

- Expanding Oil and Gas Drilling Applications: Rising global oilfield activity, particularly in North American shale plays and Middle Eastern fields, sustains steady demand for technical and oilfield-grade CaCl₂ used as high-density completion brines.

- Growing Food and Pharmaceutical Adoption: Food-grade CaCl₂ is widely used as a firming agent in dairy processing. Pharmaceutical-grade applications are expanding with growing demand for intravenous calcium solutions and drug formulation excipients.

These drivers collectively create a resilient demand base. Seasonal de-icing requirements provide volume certainty, while food, pharma, and oilfield segments provide margin enhancement, supporting the market's steady 4.53% CAGR through 2034.

Market Restraints

- Environmental Concerns from De-Icing Use: Heavy CaCl₂ application raises concerns regarding soil salinization, groundwater contamination, and corrosion of road infrastructure. Stricter environmental controls in Europe and Canada may constrain per-unit application volumes.

- Raw Material and Energy Price Volatility: Energy-intensive chemical processing makes production sensitive to natural gas and electricity price fluctuations, periodically compressing producer margins during commodity price spikes.

- Regulatory Compliance Costs for Premium Grades: Meeting food-grade, pharmaceutical-grade, and environmental discharge standards requires significant investment in quality systems and third-party certification, creating barriers for smaller regional producers.

Market Opportunities

- Expansion into Emerging Markets: Asia Pacific, Latin America, and the Middle East represent significant untapped growth potential, driven by industrialization, road network expansion, and growing mining activity, with per-capita CaCl₂ consumption well below developed-market levels.

- Eco-Friendly Formulation Development: Regulatory pressure is creating market space for reduced-environmental-impact products. The application rate of NaCl brine ranges from 10 to 90 gallons per lane-mile, depending on the weather conditions, with the most common rate being between 30 and 40 gallons per lane-mile.

- Food and Pharmaceutical Grade Specialization: Premium specialty grades command 15-25% price premiums over industrial grades, attracting producer investment in food safety certification and traceability systems for high-margin market segments.

Market Challenges

- Competition from Lower-Cost Alternative De-Icers: Calcium chloride (CaCl2) is environmentally safer but costs three times more than NaCl, which limits market penetration in price-sensitive municipal markets despite CaCl₂'s performance superiority at low temperatures.

- Logistics and Storage Complexity: CaCl₂'s hygroscopic nature requires specialized packaging and warehouse conditions, increasing supply chain operational costs and demanding bulk tank infrastructure investment from distributors.

- Quality and Import Risks: Non-certified calcium chloride imports, particularly from unregulated producers, create pricing pressure and quality perception risks that complicate specification-based sales in premium segments.

Emerging Market Trends

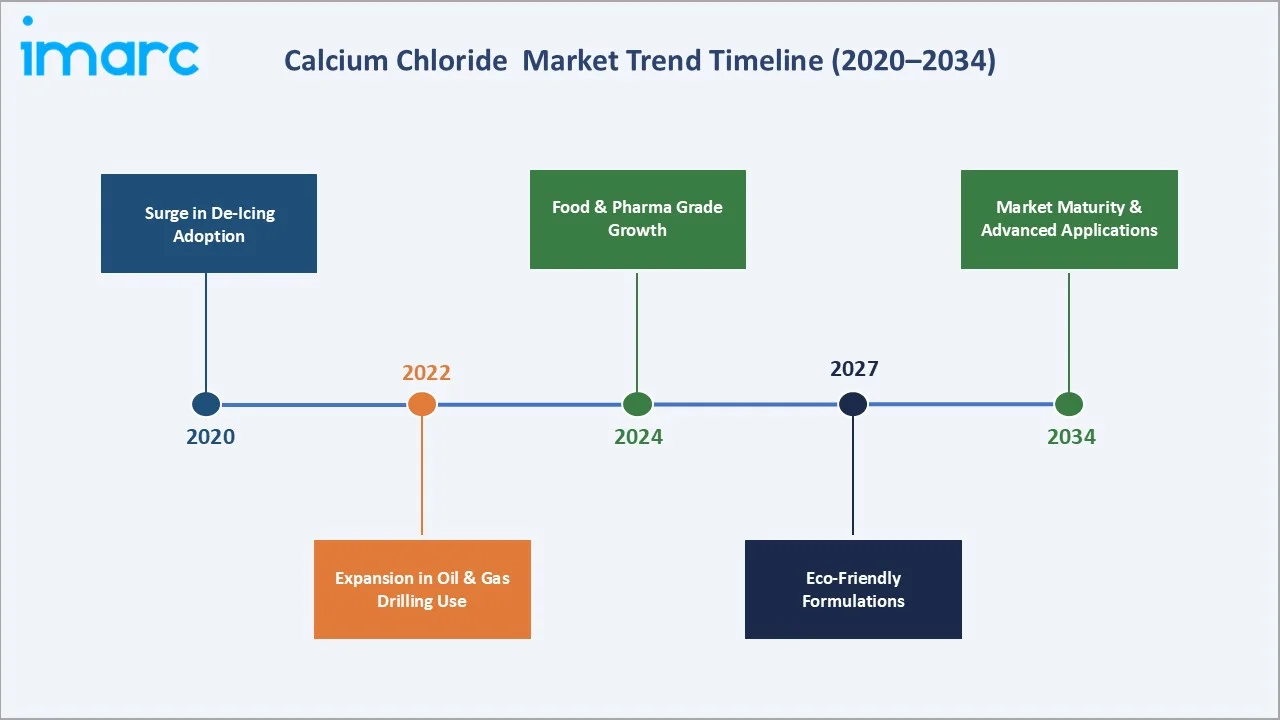

1. Surge in De-Icing Adoption Driven by Extreme Winter Weather

Increasingly severe winter weather events are expanding the geographic scope and intensity of de-icing chemical demand. Municipal and highway authority budgets for winter maintenance have grown above-market rates in North America, with CaCl₂ gaining preference over rock salt. The de-icing segment grew at 5.1% CAGR between 2020 and 2025, the fastest among all application categories.

2. Technology-Driven Production Efficiency Improvements

In November 2025, Nuberg EPC has secured an EPC contract to build a 120 TPD chlor-alkali expansion and an 80 TPD calcium chloride plant for Al Ghaith Chemical Industries in Oman, marking the second phase of its integrated chemical complex. This reflects industry-wide capacity modernization. Advanced membrane electrolysis and process optimization technologies are reducing energy consumption in chlor-alkali co-production facilities globally.

3. Food and Pharmaceutical Grade Market Development

Amphastar Pharmaceuticals received U.S. FDA approval for its Calcium Chloride injection, a product used to treat conditions such as hypocalcaemia and as an adjunct in certain cardiac resuscitation situations, marking a significant regulatory milestone for the company’s cardiovascular portfolio.

4. Precision Application and Digital Integration

Automated liquid CaCl₂ spreader systems with GPS mapping and real-time weather data integration are enabling highway authorities to reduce per-application volumes by 15-25%. This digital integration trend is accelerating adoption among environmentally conscious municipal procurement departments, creating competitive differentiation for suppliers offering turnkey digital service solutions.

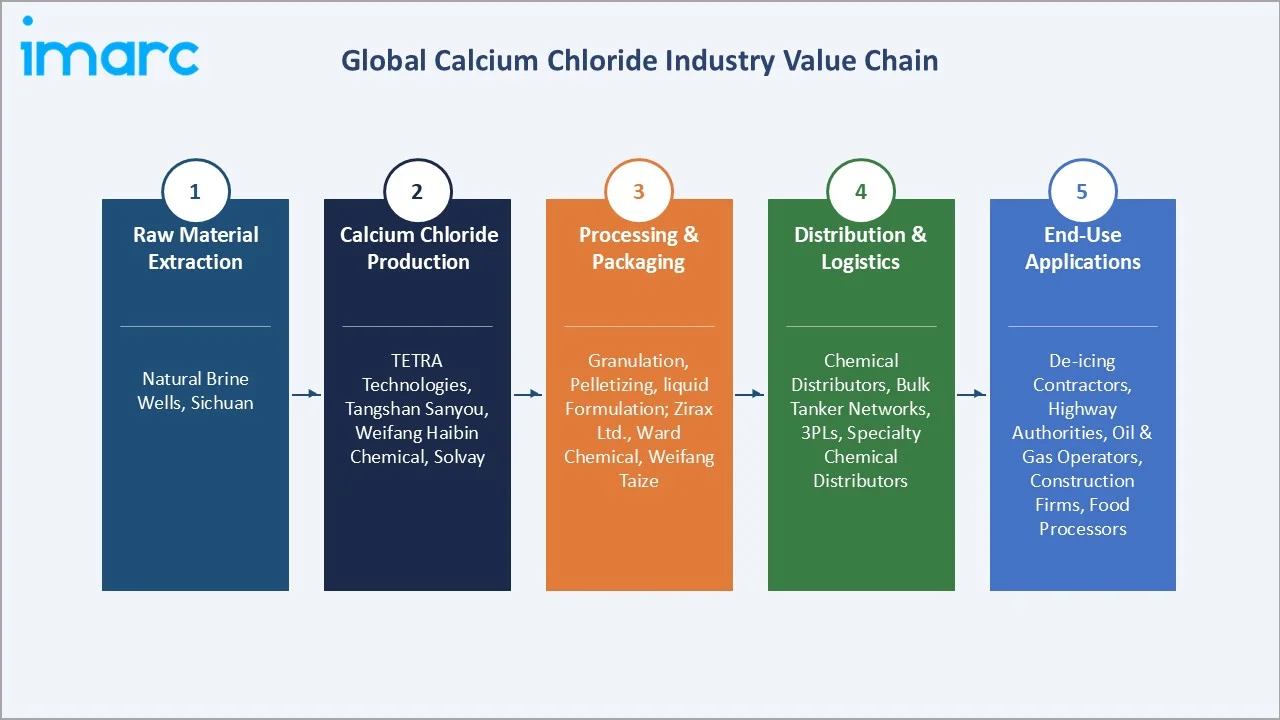

Industry Value Chain Analysis

The calcium chloride value chain spans five distinct, specialized stages from raw material extraction through to industrial, municipal, and commercial end-use applications. Each stage is populated by dedicated operators with distinct technical capabilities and market access requirements.

|

Stage |

Key Players / Examples |

|

Raw Material Extraction |

Natural brine wells, Sichuan |

|

Calcium Chloride Production |

Chemical processing plants: TETRA Technologies, Tangshan Sanyou, Weifang Haibin Chemical, Solvay |

|

Processing & Packaging |

Granulation, pelletizing, liquid formulation; Zirax Ltd., Ward Chemical, Weifang Taize |

|

Distribution & Logistics |

Chemical distributors, bulk tanker networks, 3PLs; specialty chemical distributors globally |

|

End-Use Applications |

De-icing contractors, highway authorities, oil & gas operators, construction firms, food processors |

Technology Landscape in the Calcium Chloride Industry

Production Process Innovation

Advanced membrane electrolysis technologies reduce energy consumption in chlor-alkali co-production. In February 2026, Solvay announced plans to optimize its soda ash production at the Torrelavega, Spain, plant by reducing capacity from 600 kt to 420 kt in response to global oversupply and high energy costs, aiming to boost competitiveness.

Precision Application Technology

Automated liquid CaCl₂ spreader systems equipped with GPS mapping, real-time weather data integration, and IoT sensors enable highway authorities to reduce per-application volumes by 15-25% while improving coverage consistency. These systems deliver measurable environmental and cost benefits, driving municipal procurement preference for certified precision application equipment and trained service contractors.

Specialty Grade Formulation Technology

Advanced purification and crystallization technologies enable producers to achieve pharmaceutical and food-grade CaCl₂ specifications with tighter impurity controls. Zirax started supplying its high‑purity Fudix food‑grade calcium chloride prills to a new customer in Croatia, expanding its market presence there.

Sustainable Production and Environmental Technology

Brine-water treatment systems, closed-loop process water recycling, and low-emission pelletizing technology are being adopted to meet tightening discharge standards. Producers with Environmental Product Declarations (EPDs) are gaining preference in European and North American municipal and food processing procurement processes.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Application | De-Icing | 34.6% | 2025 |

| Product Type | Hydrated Solid | 🔒 | 2025 |

| Raw Material | Natural Brine | 48.6% | 2025 |

| Grade | Industrial Grade | 🔒 | 2025 |

| Region | North America | 38.4% | 2025 |

By Raw Material

Natural Brine dominates raw material sourcing at 48.6% market share in 2025. Natural brine extraction offers cost-competitive production economics, with major U.S. operations in Michigan and Ohio and significant Chinese capacity in Sichuan province. These operations benefit from integrated brine-to-product supply chains with low incremental extraction costs per ton of finished product.

To access detailed market analysis, Request Sample

The Solvay process by-product segment (28.4% share, 2025) benefits from supply chain integration at soda ash manufacturing facilities, with Solvay representing the leading global producer. Limestone and HCl-based production accounts for 16.3%, providing a technically flexible route accessible to a broader range of producers.

By Application

De-Icing leads application demand at 34.6% in 2025, reflecting structural demand from winter-affected markets. Municipal and state highway authorities are the primary institutional buyers, with calcium chloride's -30°C effectiveness threshold providing a decisive performance advantage over alternatives in severe winter conditions.

Dust control and road stabilization follow at 22.4% (2025), supported by growth in mining, quarrying, and unpaved road maintenance activity. Drilling fluids at 14.3% reflects oilfield demand for high-density completion brines. Construction (12.6%) covers concrete acceleration and on-site dust suppression. Industrial processing at 10.4% encompasses food, refrigeration, and water treatment uses.

Regional Market Insights

North America's 38.4% market share reflects the region's position as both the world's largest producer and consumer of calcium chloride. Extensive highway infrastructure requiring annual de-icing maintenance, a highly active oil and gas sector, and major integrated production at TETRA Technologies facilities anchor the region's market leadership.

In absolute USD terms, North America accounted for approximately USD 0.53 Billion of global revenues in 2025, followed by Asia Pacific at USD 0.34 Billion and Europe at USD 0.28 Billion. The Middle East & Africa (USD 0.14 Billion) and Latin America (USD 0.10 Billion) represent the highest incremental growth opportunities through the forecast period ending 2034.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Companies |

|

North America |

38.4% |

Harsh winters; de-icing mandates; active oil & gas sector |

FHWA guidelines |

TETRA Technologies Inc. |

|

Asia Pacific |

24.6% |

Rapid industrialization; infrastructure build-out; oilfield expansion |

GB chemical standards (China) |

Tangshan Sanyou Group, Weifang Haibin Chemical |

|

Europe |

20.3% |

Food & pharma-grade demand; infrastructure maintenance |

EU REACH chemical regulations |

Solvay, Zirax Ltd. |

|

Middle East & Africa |

9.8% |

Oil & gas drilling activity; construction growth |

Local chemical safety standards |

NAMA Chemicals and regional distributors |

|

Latin America |

6.9% |

Mining expansion; road stabilization projects |

Country-specific regulations |

TETRA Technologies, Inc., regional distributors |

Asia Pacific represents the most compelling growth region at 24.6% share (2025). China accounts for a significant portion of regional production capacity, with Tangshan Sanyou Group and Weifang Haibin Chemical investing in capacity expansions. Europe's 20.3% share reflects a mature base with strong food-grade demand. The Middle East & Africa (9.8%) is driven by active oilfield operations, while Latin America (6.9%) shows emerging demand from mining and infrastructure development.

Competitive Landscape

The global calcium chloride market exhibits moderate-to-high concentration in premium industrial and specialty segments. The top five producers - TETRA Technologies, Inc., Solvay, Tangshan Sanyou Group, Ward Chemical Inc. - collectively hold approximately 55-60% of global production capacity in 2025. Significant fragmentation exists in regional distribution markets, with numerous smaller Chinese producers competing aggressively on volume and pricing.

|

Company Name |

Brand Name/Products |

Market Position |

Core Strength |

|

TETRA Technologies, Inc. |

CC tech, CC food, CC farm, and CC road |

Market Leader |

Oilfield-focused; vertically integrated US and European production & supply |

|

Solvay |

CASO |

Strong Challenger |

Soda-ash by-product CaCl₂; food & pharma specialty grades |

|

Tangshan Sanyou Group |

Calcium Chloride derivatives |

Strong Challenger |

Leading Chinese producer; broad Asia-Pacific distribution reach |

|

Ward Chemical Inc. |

Heavy Brine Plus, Soil-Cal, MG-30 |

Challenger |

Canadian specialist; dust control & de-icing focus |

|

Zirax Ltd. |

Fudix and Icemelt |

Challenger |

Specialty-grade producer; food, pharma & oilfield |

|

Weifang Haibin Chemical |

Industrial-grade Calcium Chloride |

Niche Player |

High-volume pelleted CaCl₂; 2023 capacity expansion |

|

Tiger Calcium Services Inc. (subsidiary of Morton Salt) |

Formula 35 Plus, Road Guard Plus, Clear Guard Advanced, Road Guard Eco-Plus |

Niche Player |

North American dust-control & de-icing service provider |

Key Company Profiles

TETRA Technologies, Inc.

TETRA Technologies is a vertically integrated calcium chloride producer with operations spanning manufacturing, bulk storage, and distribution across North America, European, and international oilfield markets.

- Product Portfolio: Industrial CaCl₂ liquids and dry solids; oilfield completion and workover brines; calcium bromide specialty brines; water treatment mineral solutions.

- Recent Developments: December 2024 launched TETRA Oasis TDS, an end-to-end produced water desalination solution for beneficial re-use and mineral extraction from oil and gas produced water.

- Strategic Focus: Oilfield chemical market leadership; water management solutions; geographic expansion in North American shale and unconventional resource plays.

Solvay

Solvay is a global specialty chemicals leader producing calcium chloride as a by-product of soda ash manufacturing at facilities across Europe and North America.

- Product Portfolio: Food-grade and pharmaceutical-grade CaCl₂; industrial liquids and solids; soda ash by-product calcium chloride in multiple purity grades for diverse markets.

- Recent Developments: The e.Solvay electrochemical process was piloted in Europe (Dombasle-sur-Meurthe, France).

- Strategic Focus: Premium specialty grade development; sustainability leadership; food and pharmaceutical market penetration; European distribution optimization.

Tangshan Sanyou Group Co., Ltd.

Tangshan Sanyou Group is one of China's leading calcium chloride producers with large-scale integrated chemical operations in Hebei Province. The company benefits from proximity to major Chinese industrial markets and competitive brine extraction economics.

- Product Portfolio: Calcium chloride dihydrate; anhydrous calcium chloride; dry and liquid grades for industrial, de-icing, and construction applications across domestic and export markets.

- Recent Developments: Ongoing capacity expansion at Tangshan facilities to serve growing domestic construction and industrial demand in China and neighboring Asian markets.

- Strategic Focus: Asia Pacific market leadership; cost-competitive volume production; domestic industrial and municipal customer base development and export market penetration.

Market Concentration Analysis

The global calcium chloride market exhibits moderate-to-high concentration in the high-performance industrial and specialty tier. The top five global producers account for approximately 55-60% of total production capacity in 2025, while the remaining 40-45% is distributed among regional formulators, private-label blenders, and lower-grade commodity importers, particularly from China.

Consolidation pressure is building among mid-tier producers. Leading companies are investing in capacity expansions and product quality improvements to defend market positions against lower-cost Chinese competition.

The specialty-grade segment is notably more concentrated than the commodity industrial segment. In food-grade and pharmaceutical-grade calcium chloride, the top three certified producers like Solvay and Zirax Ltd., collectively hold the majority of specification-approved supply globally. PE interest in mid-tier specialty chemical distributors with established calcium chloride portfolios remains elevated through 2025.

Investment & Growth Opportunities

Fastest Growing Segments

Food-grade calcium chloride (CAGR 5.2%), de-icing premium formulations (CAGR 5.1%), and oilfield specialty brines (CAGR 4.9%) represent the three highest-growth investment vectors through 2034. These segments collectively address a total addressable market of approximately USD 0.8 Billion by 2034 and offer margin premiums of 15-25% above commodity industrial grades.

Emerging Market Expansion

Asia Pacific and Latin America present the most compelling geographic investment opportunities. India's calcium chloride market is expected to grow at 6.5% CAGR (2026–2034), driven by construction expansion and growing food processing demand. Southeast Asian markets represent an incremental USD 0.15 Billion opportunity by 2034, while Brazil's mining and infrastructure sector is forecast to drive 5.8% CAGR regional growth.

Venture Investment Trends

Strategic investment is increasingly targeting precision application technology, environmental compliance solutions, and specialty-grade manufacturing capacity. In March 2025, TETRA Technologies Inc. partnered with EOG Resources to launch a pilot project using its Oasis TDS technology to treat and desalinate produced water from the Permian Basin for reuse and potential industrial applications. Companies integrating CaCl₂ supply with digital precision application systems are attracting ESG-aligned investment capital and preferred municipal procurement status.

Future Market Outlook (2026-2034)

The global calcium chloride market is positioned for sustained, broad-based growth through 2034, anchored by stable industrial demand, premium segment expansion, and geographic diversification into the Asia Pacific and Latin America. From USD 1.38 Billion in 2025, the market is forecast to reach USD 2.11 Billion by 2034, representing absolute incremental value addition of USD 0.73 Billion over the nine years.

Technological disruptions, including digital precision application systems, sustainable production processes, and specialty-grade formulation innovation, are expected to reshape competitive dynamics. Producers achieving cost efficiency gains through process modernization while maintaining premium-grade certification capabilities will capture disproportionate market share in high-margin application segments through 2030-2034.

Environmental compliance credentials, product traceability, and application efficiency documentation will transition from differentiating factors to baseline requirements in regulated markets. Companies embedding sustainability metrics and digital service capabilities into their value propositions are expected to secure preferred supplier status with municipal, food processing, and pharmaceutical customers.

Research Methodology

Primary Research

Primary research comprised structured interviews and surveys with over 150 industry participants in 2024–2025, including calcium chloride producers, procurement managers, municipal road maintenance authorities, oilfield services companies, food processing buyers, and specialty chemical distribution specialists across North America, Europe, and the Asia Pacific.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, regulatory filings, USGS mineral commodity data, trade publications including Chemical Week and ICIS, industry databases including Euromonitor and IHS Markit, and publicly available financial disclosures. Over 200 secondary sources were reviewed and triangulated to validate market estimates.

Forecasting Models

Market size estimations were derived using bottom-up and top-down forecasting models, incorporating GDP growth indices, industrial production data, winter severity indicators, oil and gas capital expenditure trends, and historical calcium chloride consumption patterns. A base-case CAGR of 4.53% reflects consensus estimates validated against regional production capacity expansion data.

Calcium Chloride Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Million Tons |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Liquid, Hydrated Solid, Anhydrous Solid |

| Applications Covered | De-Icing, Dust Control and Road Stabilization, Drilling Fluids, Construction, Industrial Processing, Others |

| Raw Materials Covered | Natural Brine, Solvay Process (By-Product), Limestone and HCL, Others |

| Grades Covered | Food Grade, Industrial Grade |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | TETRA Technologies, Inc., Solvay, Tangshan Sanyou Group, Ward Chemical Inc., Zirax Ltd., Weifang Haibin Chemical, Tiger Calcium Services Inc. (subsidiary of Morton Salt), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the calcium chloride market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global calcium chloride market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the calcium chloride industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Calcium Chloride Market Report

The global calcium chloride market reached USD 1.38 Billion in 2025 and is projected to reach USD 2.11 Billion by 2034, growing at a CAGR of 4.53% during 2026-2034.

The market is expected to grow at a CAGR of 4.53% during 2026-2034, reflecting steady structural demand across de-icing, dust control, oilfield, and food processing application segments.

North America leads with 38.4% of global revenues in 2025, driven by harsh winter conditions, extensive highway infrastructure, and major integrated production by TETRA Technologies, Inc.

Asia Pacific is the fastest-growing region, driven by rapid industrialization, construction expansion, and growing oilfield exploration in China, India, and Southeast Asia through 2034.

Key drivers include expanding de-icing demand, growing dust control activity in mining and construction, rising oil and gas drilling brine requirements, and increasing food and pharmaceutical-grade adoption globally.

De-Icing leads with a 34.6% share in 2025, supported by government road safety mandates and calcium chloride's superior performance at very low temperatures compared to alternative de-icing chemicals.

Natural Brine accounts for 48.6% of raw material sourcing in 2025, favored for cost-competitive extraction economics at established brine well operations in the United States and China.

Leading companies include TETRA Technologies, Inc., Solvay, Tangshan Sanyou Group, Ward Chemical Inc., Zirax Ltd., Weifang Haibin Chemical, and Tiger Calcium Services Inc.

Key challenges include environmental concerns from heavy de-icing application, competition from lower-cost rock salt alternatives, energy cost volatility in chemical production, and quality risks from non-certified imports.

High-growth opportunities exist in food and pharmaceutical-grade specialty capacity, precision de-icing application technology, oilfield specialty brine formulations, and emerging market distribution infrastructure in Asia and Latin America.

Key trends include food-grade specialty segment expansion, precision liquid application systems for de-icing, eco-friendly production process adoption, and digital supply chain management integration through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade