Canada Diabetes Market Size, Share, Trends and Forecast by Segment and Distribution Channel, 2026-2034

Canada Diabetes Market Size, Share, Trends & Forecast (2026-2034)

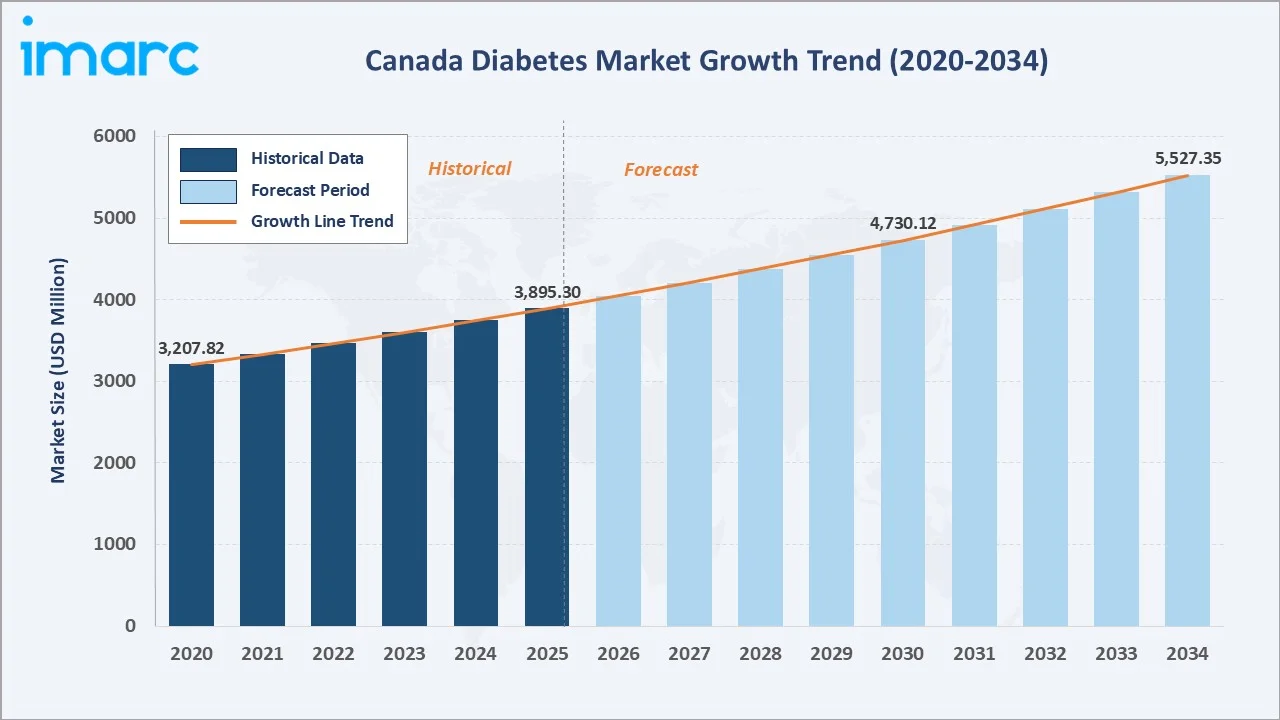

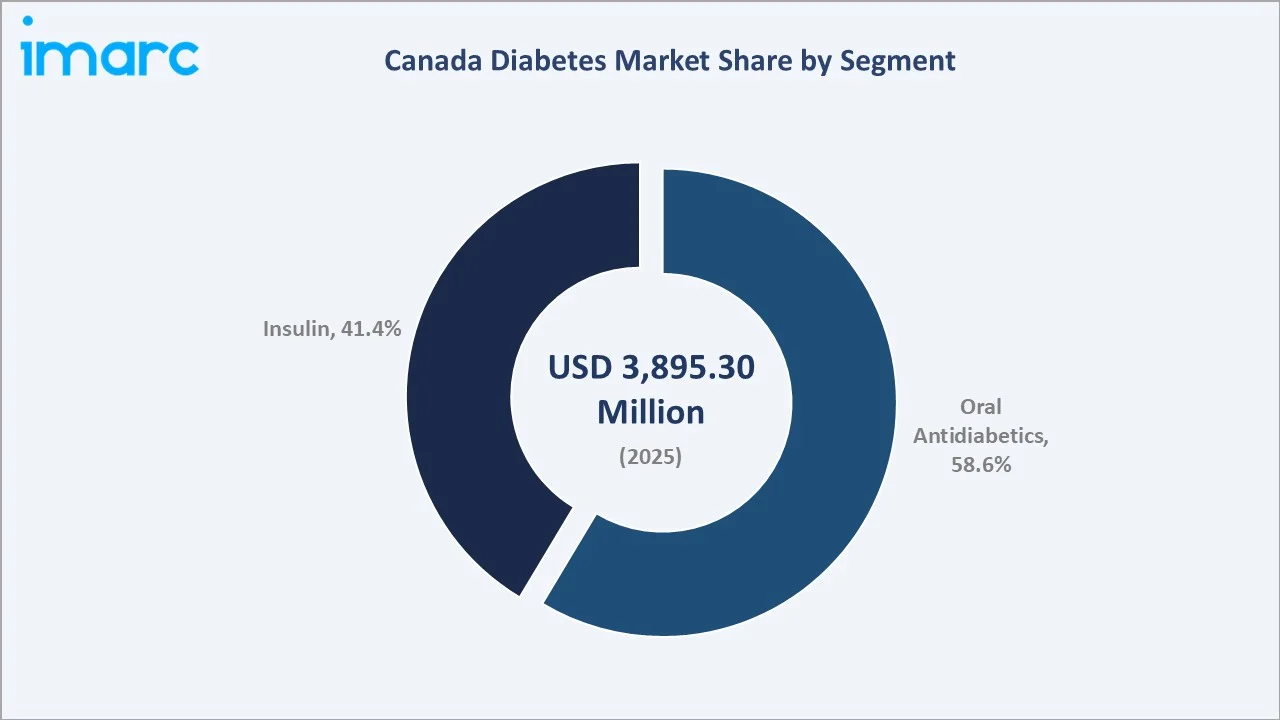

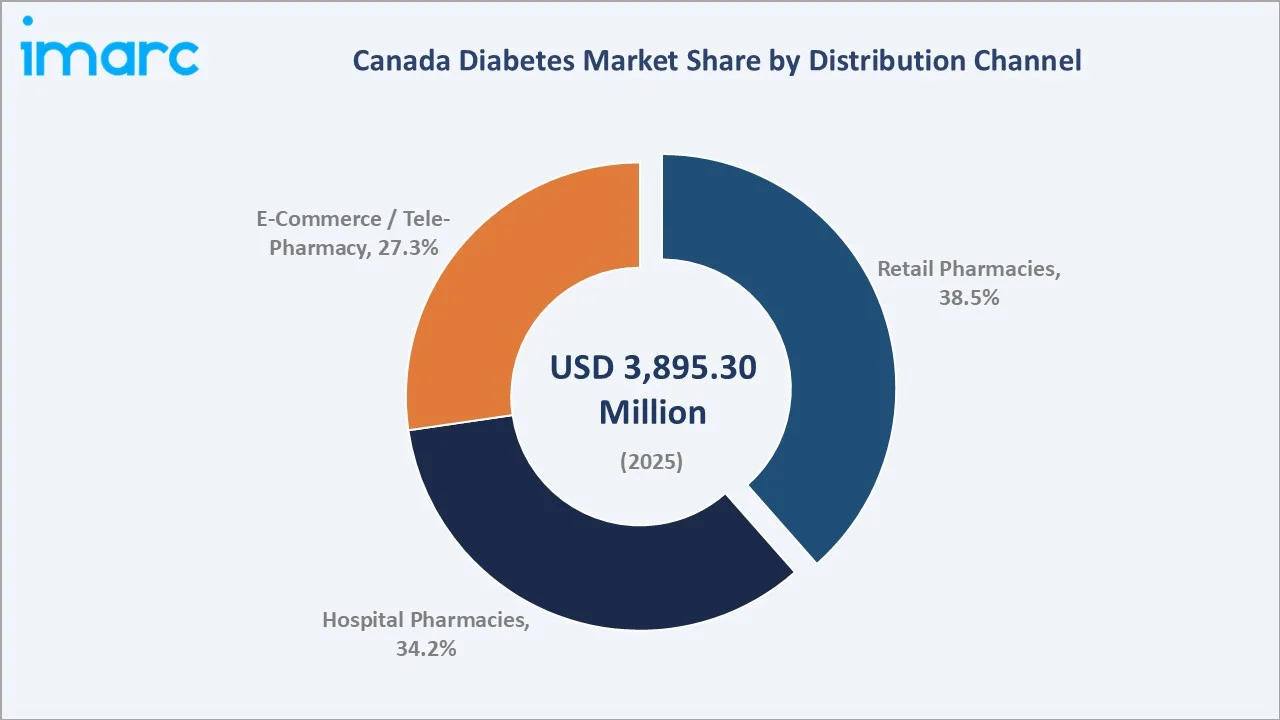

The Canada diabetes market reached USD 3,895.30 Million in 2025 and is projected to reach USD 5,527.40 Million by 2034, growing at a CAGR of 3.96% during 2026-2034. Rising diabetes prevalence driven by an ageing population, sedentary lifestyles, and escalating obesity rates are the primary market catalysts. Canada has one of the highest diabetes prevalence rates among G7 nations, creating sustained demand for both oral antidiabetics and insulin therapies across its provincially administered healthcare system.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3,895.30 Million |

|

Forecast Market Size (2034) |

USD 5,527.40 Million |

|

CAGR (2026-2034) |

3.96% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Segment |

Oral Antidiabetics – 58.6% share (2025) |

|

Leading Distribution Channel |

Retail Pharmacies – 38.5% share (2025) |

The Canada diabetes market demonstrated a steady historical CAGR of approximately 3.96% during 2020–2025, driven by persistently rising Type-2 diabetes incidence, progressive expansion of provincial drug benefit formularies to include newer therapeutic classes, and an accelerating shift toward tele-pharmacy and digital prescription platforms following the COVID-19 pandemic.

To get more information on this market, Request Sample

Looking forward, the forecast period 2026–2034, the sustained momentum will be anchored by three structural forces: the rapid commercialization of GLP-1 receptor agonists generating premium revenue in the private and employer-sponsored insurance segments; the progressive listing of biosimilar insulins on provincial formularies reducing per-unit costs while expanding patient volumes; and the proliferation of digital health and tele-pharmacy platforms broadening reach into rural and remote communities across Northern Ontario.

Executive Summary

The Canada diabetes market is on a sustained upward trajectory, underpinned by a rising burden of Type-2 diabetes, expanding provincial drug benefit coverage, and the increasing adoption of digital health tools and tele-pharmacy platforms across Canada vast geography. The market reached USD 3,895.30 Million in 2025 and is forecast to surpass USD 5,527.40 Million by 2034, reflecting a CAGR of 3.96% across the forecast period.

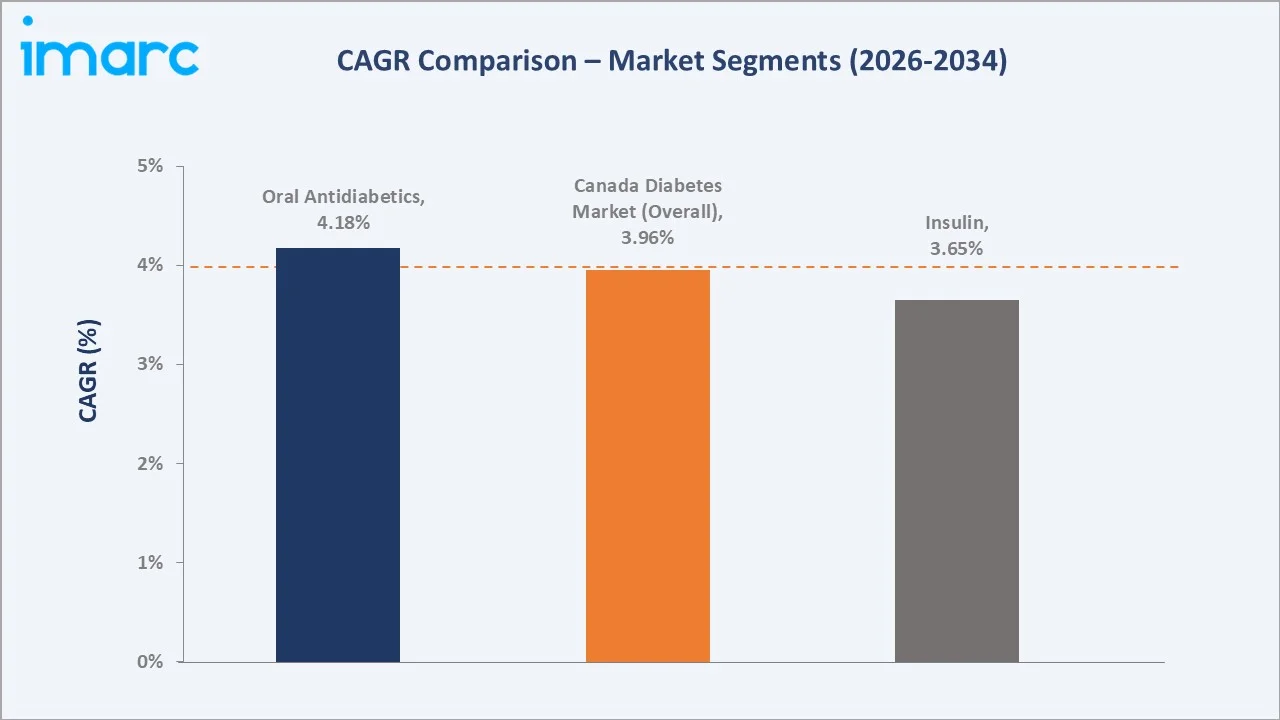

Oral antidiabetics command the largest segment share at 58.6% in 2025, driven by widespread prescription of metformin as first-line therapy and the rapidly growing SGLT-2 inhibitor and GLP-1 receptor agonist classes, which have gained significant traction following landmark cardiovascular and renal outcome trial results recognized in Canadian Diabetes Association clinical practice guidelines.

The insulin segment accounts for 41.4% and is growing steadily as biosimilar insulin products gain provincial formulary listings, improving affordability for patients and expanding volume-driven revenues for distributors. Key players include Novo Nordisk A/S, Sanofi, Lilly USA, LLC, AstraZeneca, and Merck & Co., Inc., alongside domestic generic and biosimilar manufacturers Apotex and Teva Canada.

Key Market Insights

|

Insight |

Data |

|

Largest Segment |

Oral Antidiabetics – 58.6% share (2025) |

|

2nd Largest Segment |

Insulin – 41.4% share (2025) |

|

Leading Channel |

Retail Pharmacies – 38.5% share (2025) |

|

Fastest Growing Channel |

E-Commerce/Tele-Pharmacy – 27.3% share (2025) |

|

Dominant Region |

Ontario – ~38% revenue share (2025) |

|

Top Companies |

Novo Nordisk A/S, Sanofi, Lilly USA, LLC, AstraZeneca, and Merck & Co., Inc. |

|

Market Opportunity |

GLP-1 & biosimilar insulin segment projected at USD 1.1 Billion by 2034 |

Key Analytical Observations Supporting the Above Data:

- Oral antidiabetics account for 58.6% of the Canada diabetes market in 2025, anchored by metformin as the universal first-line Type-2 treatment and the rapidly growing SGLT-2 and GLP-1 classes driven by cardiovascular and renal co-benefit data recognized in CDA/Diabetes Canada clinical guidelines.

- Insulin holds a 41.4% share in 2025; growth is fueled by biosimilar glargine listings on provincial formularies in Ontario and Quebec, rising Type-1 patient volumes, and expanded coverage under the Non-Insured Health Benefits (NIHB) program for Indigenous Canadians.

- Retail pharmacies remain the leading distribution channel at 38.5% in 2025, supported by the Shoppers Drug Mart and Rexall networks spanning over 1,700 outlets nationally and provincial dispensing fee subsidy programs.

- E-commerce and tele-pharmacy channels have reached 27.3% of the market in 2025, growing rapidly as post-pandemic regulatory changes permanently enabled virtual pharmacy services across all provinces and the Yukon, Northwest Territories, and Nunavut territories.

- Ontario leads with 38% share in 2025, driven by the Ontario Drug Benefit program, which covers the majority of the cost for over 5,900 medications listed on the ODB Formulary, along with nearly 1,500 additional drug products that qualify under the Exceptional Access Program (EAP).

Canada Diabetes Market Overview

Diabetes mellitus is the most prevalent chronic metabolic condition in Canada, with approximately 3.9 million Canadians living with diagnosed diabetes in 2025. According to Diabetes Canada, the condition accounts for approximately 30% of strokes, 40% of heart attacks, and 50% of kidney disease cases requiring dialysis in the country. The market encompasses two principal therapeutic classes – oral antidiabetics (OADs) and insulin – distributed through retail pharmacies, hospital pharmacies, and rapidly expanding tele-pharmacy and e-commerce platforms.

Canada's healthcare structure is governed by the Canada Health Act, with each province and territory operating its own drug benefit plan. This creates a multi-tier market: publicly funded provincial formularies (ODB in Ontario, RAMQ in Quebec, BC PharmaCare, Alberta Drug Benefit) provide coverage to eligible populations, including seniors, social assistance recipients, and chronic disease patients; employer-sponsored private insurance covers the majority of working-age Canadians; and a residual out-of-pocket segment encompasses newer drug classes not yet formulary-listed.

Market Dynamics

To evaluate market opportunities, Request Sample

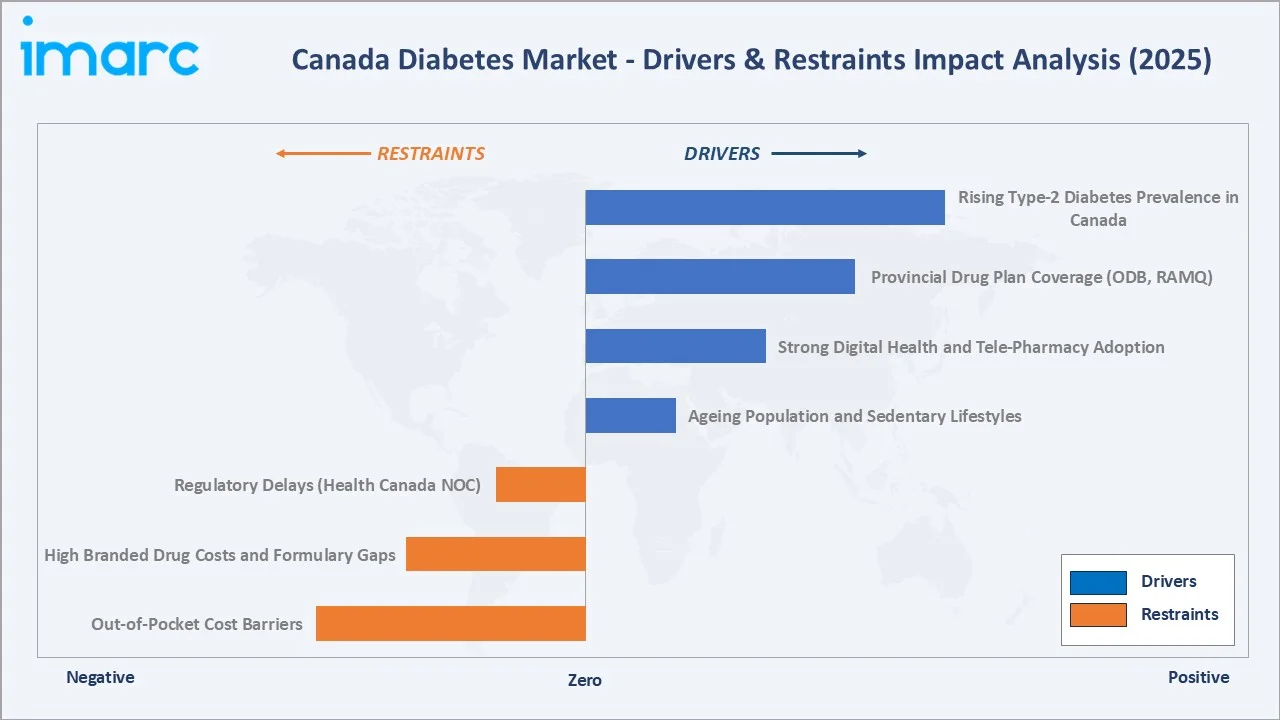

Market Drivers

- Rising Type-2 Diabetes Prevalence in Canada: Approximately 3.9 million Canadians aged one and older are living with diagnosed diabetes, accounting for 9.7% of the population, with Type-2 diabetes representing about 90-95% of cases. Rising obesity rates (68% of Canadian adults aged 18 to 79 had a BMI classified as overweight or having obesity), sedentary urban lifestyles, and an ageing baby-boomer cohort are the structural engines of this growth, creating sustained therapy demand across all segments.

- Provincial Drug Plan Coverage (ODB, RAMQ): Provincial drug benefit plans covering seniors, social assistance recipients, and registered chronic disease patients provide substantial prescription drug coverage. The Ontario Drug Benefit program alone covered over 9 million eligible Ontarians in 2025, while Quebec's RAMQ provides near-universal drug coverage to all Quebec residents, creating stable formulary-driven volume in both the OAD and insulin segments.

- Strong Digital Health & Tele-Pharmacy Adoption: Tele-pharmacy legislation was permanently extended post-pandemic across all provinces by 2023, enabling virtual prescription, consultation, and home delivery. Digital diabetes management platforms integrating CGM, mobile apps, and AI-powered coaching are reshaping patient adherence patterns and expanding the addressable market.

- Ageing Population & Sedentary Lifestyles: By 2030, seniors are projected to make up between 21.4% and 23.4% of the total population, representing the highest-risk cohort for Type-2 diabetes onset and insulin progression. Population-weighted diabetes prevalence will rise significantly in Atlantic Canada and Quebec, where the population median age is highest, driving structural demand growth through the forecast period.

Market Restraints

- Out-of-Pocket Cost Barriers: A total of 20% of Canadians report being uninsured or underinsured, with the majority of their prescription drug costs paid out-of-pocket for newer therapeutic classes, including SGLT-2 inhibitors and GLP-1 receptor agonists, which are not universally listed on provincial formularies.

- High Branded Drug Costs & Formulary Gaps: Branded SGLT-2 inhibitors and GLP-1 receptor agonists carry average annual therapy costs of CAD 2,400–3,600 per patient in Canada, placing a significant burden on patients without employer-sponsored insurance and limiting provincial formulary listing timelines due to health technology assessment (HTA) cost-effectiveness thresholds.

- Regulatory Delays (Health Canada NOC): Health Canada's Notice of Compliance (NOC) review timelines for new molecular entities average 18–22 months from submission, creating access delays relative to the United States FDA. The Canadian Drug Review (CDR) process through CADTH adds a further 12–18 months before provincial formulary listing, collectively delaying commercial market access for innovative therapies.

Market Opportunities

- Biosimilar Insulin Expansion & Provincial Substitution: Health Canada approved its biosimilar guidance in 2020, and provinces, including British Columbia and Ontario, mandated biosimilar substitution for insulin in 2021–2022, with other provinces following. This is reducing insulin costs by 30–45% and expanding formulary access to a broader patient base.

- GLP-1 Receptor Agonist Premium Growth: Semaglutide (Ozempic, Wegovy) and dulaglutide (Trulicity) are experiencing outstanding uptake in Canada's employer-sponsored insurance market. Ozempic became the most prescribed brand-name drug in Canada in 2023–2024.

- National Pharmacare Policy Momentum: A national pharmacare strategy has been a priority policy for successive Canadian federal governments. Full implementation would significantly expand universal drug coverage for diabetes medications, potentially creating a substantial volume uplift for both OAD and insulin segments.

Market Challenges

- Rural & Remote Access Inequities: A significant portion of Canada's 1.7 million Indigenous Canadians face elevated diabetes prevalence rates combined with limited pharmacy infrastructure in remote First Nations, Metis, and Inuit communities.

- PMPRB Pricing Reform Uncertainty: Canada's drug pricing is governed by the Patented Medicine Prices Review Board (PMPRB), which has implemented new pricing regulations to align branded drug prices with international benchmarks.

Emerging Market Trends

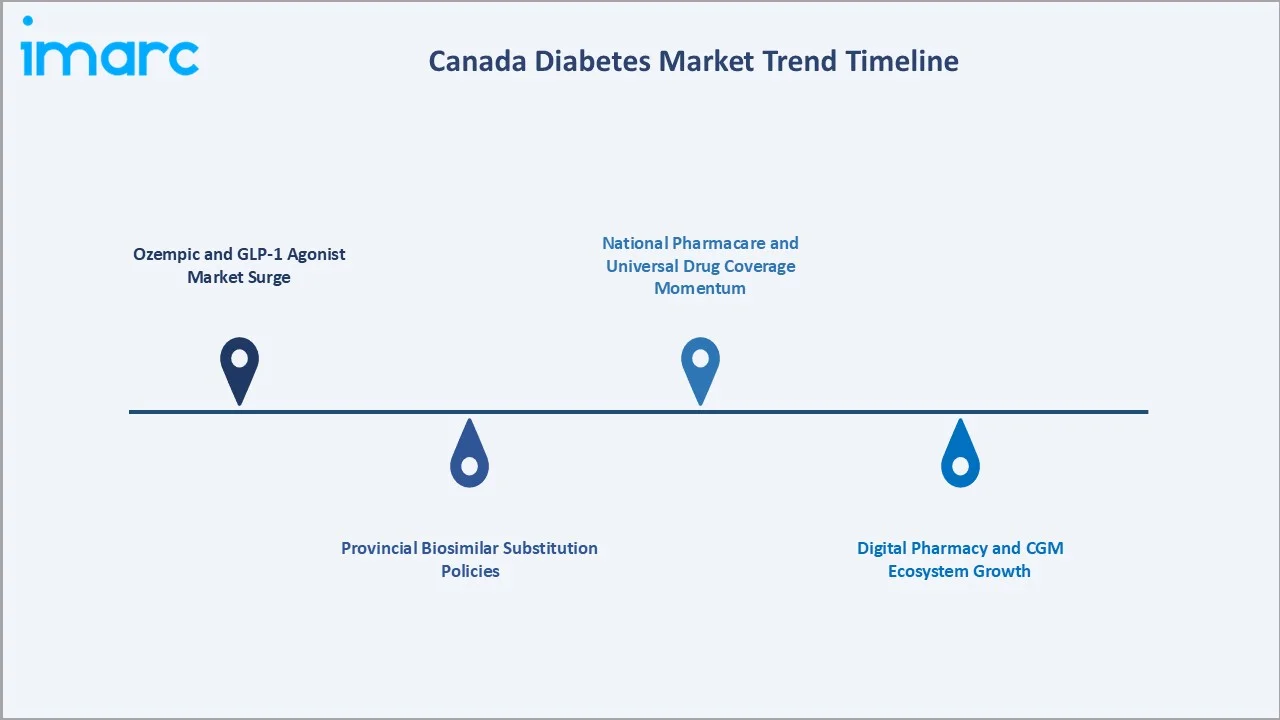

1. Ozempic and GLP-1 Agonist Market Surge

Ozempic (semaglutide) was approved by Health Canada for Type-2 diabetes and became the most prescribed branded drug in Canada by 2024, driven by its dual diabetes and weight management benefits. Prescription volume for GLP-1 agents in Canada grew at approximately 38% annually between 2022 and 2025, reshaping the premium OAD segment and driving significant revenue concentration toward Novo Nordisk.

2. Provincial Biosimilar Substitution Policies

Between 2021 and 2024, British Columbia, Ontario, Alberta, and Quebec implemented mandatory biosimilar insulin substitution policies for new provincial drug benefit plan claimants. Biosimilar glargine now accounts for an estimated 22% of the Canadian insulin market in 2025, up from 8% in 2020, with this share projected to reach 40% by 2034 as existing patient cohorts transition on formulary renewal cycles.

3. Digital Pharmacy and CGM Ecosystem Growth

Digital pharmacy platforms, including PharmaClik, Pharmx, and emerging direct-to-consumer services, grew their combined annual prescription volume in diabetes medications by 31% in 2024. Simultaneously, CGM adoption among Canadian Type-1 and Type-2 patients expanded 42% in 2024 as provincial governments in Ontario and British Columbia introduced CGM reimbursement for Type-1 patients under their drug benefit programs.

4. National Pharmacare and Universal Drug Coverage Momentum

The Canadian government's Pharmacare Act, tabled in 2024, represents the most significant potential structural change to Canada's pharmaceutical market in decades. If fully implemented, a national pharmacare program covering diabetes medications would materially expand the publicly funded patient pool for both insulins and key OADs, creating volume-driven growth while compressing average selling prices and restructuring the competitive dynamics between branded and generic manufacturers.

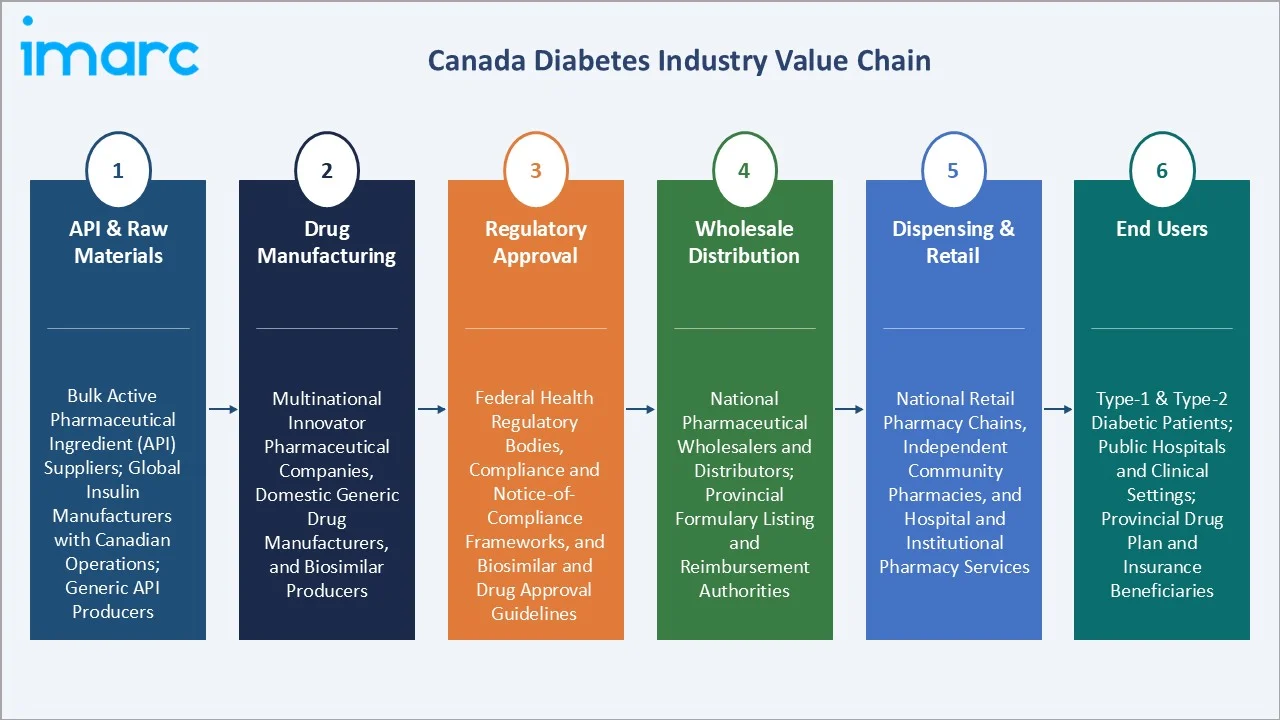

Industry Value Chain Analysis

The Canadian diabetes drug market value chain spans active pharmaceutical ingredient (API) production through to end-patient dispensing, with each stage shaped by Canada's unique provincial health system structure, Health Canada regulatory framework, and the parallel operation of public formulary and private insurance reimbursement channels.

|

Stage |

Key Players / Examples |

|

API & Raw Materials |

Bulk active pharmaceutical ingredient (API) suppliers; global insulin manufacturers with Canadian operations; generic API producers |

|

Drug Manufacturing |

Multinational innovator pharmaceutical companies, domestic generic drug manufacturers, and biosimilar producers |

|

Regulatory Approval |

Federal health regulatory bodies, compliance and notice-of-compliance frameworks, and biosimilar and drug approval guidelines |

|

Wholesale Distribution |

National pharmaceutical wholesalers and distributors; provincial formulary listing and reimbursement authorities |

|

Dispensing & Retail |

National retail pharmacy chains, independent community pharmacies, and hospital and institutional pharmacy services |

|

End Users |

Type-1 & Type-2 diabetic patients; public hospitals and clinical settings; provincial drug plan and insurance beneficiaries |

Technology Landscape in the Canada Diabetes Market

Smart Insulin Delivery and Digital Pen Ecosystem

Novo Nordisk and Sanofi have introduced Bluetooth-enabled smart insulin pens (NovoPen 6, SoloSmart connected) to the Canadian private market, enabling automated dose logging, app integration, and remote sharing of adherence data with endocrinologists. These devices are particularly impactful in Canada vast geography, where rural patients may have only quarterly specialist access and require high-quality remote monitoring tools.

AI-Powered Diabetes Management Platforms

Canadian digital health companies, including various healthcare platforms and tools, including Google’s DeepMind Health, and mobile apps like BlueLoop and OneDrop, are aiding in the early detection of diabetes. These platforms are being adopted by employer-sponsored group benefit plans as a workplace wellness and chronic disease management investment, creating a new B2B revenue stream alongside the traditional B2C pharmacy channel.

Biosimilar Manufacturing Technology

Apotex Inc. and Teva Canada are investing in enhanced biosimilar insulin manufacturing capabilities, accelerating their pipeline of Health Canada NOC submissions. Apotex's biosimilar glargine candidate, leveraging its existing recombinant protein manufacturing infrastructure, is positioned to capture a significant share of provincial formulary volume as substitution policies expand across remaining provinces through 2026–2028.

Remote Prescribing and Tele-Pharmacy Infrastructure

Health Canada's 2022 permanent regulatory framework for virtual care and the provincial licensure of tele-pharmacy across all provinces have created a robust infrastructure for remote diabetes consultations and electronic prescribing. This is directly driving the e-commerce and tele-pharmacy channel's share growth from 11% in 2020 to 27.3% in 2025.

Market Segmentation Analysis

By Segment

Oral antidiabetics dominate the Canada diabetes market with a 58.6% share in 2025, reflecting the entrenched role of metformin as the universal first-line Type-2 therapy, supplemented by the growing penetration of premium OAD classes including SGLT-2 inhibitors and GLP-1 receptor agonists.

To access detailed market analysis, Request Sample

Insulin accounts for 41.4% of the market. The segment is anchored by a large insulin-dependent Type-1 patient cohort, complemented by a growing Type-2 population transitioning to basal insulin therapy as disease progresses. Provincial biosimilar substitution mandates are reshaping the competitive landscape within the insulin segment, driving biosimilar glargine market share from approximately 8% in 2020 toward an estimated 22% in 2025.

By Distribution Channel

Retail pharmacies represent the leading channel at 38.5% share in 2025, anchored by the Shoppers Drug Mart network (1,300+ locations), Rexall (400+ locations), and a dense ecosystem of independent and banner pharmacies serving both urban and rural Canadian communities. Hospital pharmacies follow at 34.2%, driven by inpatient insulin management, post-surgical diabetes care, and specialist hospital clinic dispensing.

E-commerce and tele-pharmacy platforms have reached 27.3% of the market in 2025 – among the highest tele-pharmacy market shares in the G7 – reflecting Canada's post-pandemic regulatory embrace of virtual pharmacy services and the country's tech-forward healthcare consumer demographics.

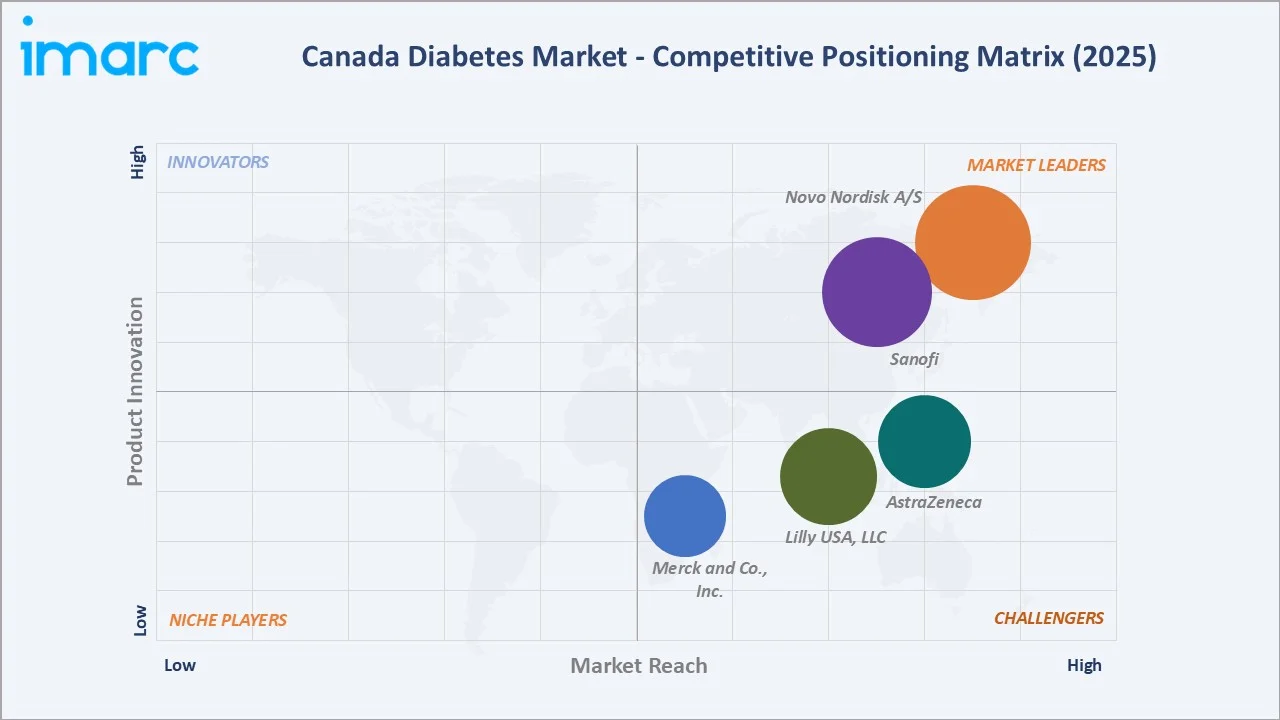

Competitive Landscape

The Canada diabetes market exhibits a moderately concentrated structure at the innovative pharmaceutical level. The top five companies, Novo Nordisk A/S, Sanofi, Lilly USA, LLC, AstraZeneca, and Merck & Co., Inc., collectively account for approximately 58–62% of market revenue in 2025.

|

Company Name |

Market Position |

Core Segment |

Core Strength |

|

Novo Nordisk A/S |

Market Leader |

Insulin & GLP-1 |

Global insulin leader; Ozempic leads GLP-1 segment in Canada |

|

Sanofi |

Market Leader |

Insulin |

Lantus is dominant in basal insulin; Toujeo Premium analogue positioning |

|

Lilly USA, LLC |

Strong Challenger |

Insulin & OAD |

Operating as Eli Lilly Canada Inc. in Canada; Humalog portfolio; Jardiance co-promotion with Boehringer |

|

AstraZeneca |

Strong Challenger |

Oral Antidiabetics |

Forxiga (dapagliflozin) leading the SGLT-2 segment; cardio-renal labelling |

|

Merck & Co., Inc. |

Challenger |

Oral Antidiabetics |

Operating as Merck Canada Inc. in Canada; Januvia/Janumet DPP-4 franchise; provincial formulary presence |

Domestic manufacturers Apotex Inc. and Teva Canada compete strongly in the generic and biosimilar segments, with biosimilar insulin products gaining increasing provincial formulary traction following mandatory substitution policies in Ontario and British Columbia.

Key Company Profiles

Novo Nordisk A/S

Novo Nordisk A/S, headquartered in Bagsvaerd, Denmark, holds the largest single-company revenue share in the Canada diabetes market. Its Canadian operations are anchored by the dominant Ozempic (semaglutide) franchise, which became the most prescribed branded drug in Canada by 2024.

- Product Portfolio: Tresiba (degludec), Ozempic (semaglutide), Victoza (liraglutide), NovoRapid (aspart), NovoMix 30; Rybelsus (oral semaglutide).

- Recent Developments: In March 2026, Health Canada approved Ozempic (semaglutide injection) to reduce the risk of major adverse cardiovascular events (MACE), including cardiovascular death, non‑fatal heart attack, or non‑fatal stroke, in adults with type 2 diabetes and established cardiovascular disease and/or chronic kidney disease.

- Strategic Focus: GLP-1 market dominance in Canada's premium private and employer-sponsored insurance segments; defense of insulin portfolio against biosimilar substitution via Tresiba long-acting differentiation.

Sanofi

Sanofi, headquartered in Paris, France, maintains a leading position in Canada's basal insulin market through Lantus (insulin glargine), the country's most commonly prescribed basal insulin by historical volume.

- Product Portfolio: Lantus (glargine), Toujeo (glargine U300), Apidra (glulisine), Amaryl (glimepiride); Admelog (lispro biosimilar).

- Recent Developments: In February 2024, JDRF Canada and Sanofi Canada partnered to raise awareness of autoimmune type 1 diabetes and highlight the importance of screening for early detection of the disease. The initiative focuses on educating patients, families, and healthcare providers on early-stage identification to improve long-term health outcomes.

- Strategic Focus: Premium insulin analogue positioning via Toujeo differentiation; OAD portfolio maintenance; strategic engagement with provincial formulary committees to secure Toujeo preferential listing over biosimilar glargine.

AstraZeneca

AstraZeneca, headquartered in Cambridge, UK, is one of the most commercially successful OAD players in Canada through Forxiga (dapagliflozin), which benefits from landmark DAPA-HF and DAPA-CKD trial results that expanded its prescriber base well beyond endocrinology into cardiology and nephrology.

- Product Portfolio: Forxiga (dapagliflozin)

- Recent Developments: In August 2021, Health Canada approved Forxiga (dapagliflozin), an oral SGLT2 inhibitor, to treat adults with chronic kidney disease (CKD) by reducing the risk of kidney function decline, end‑stage kidney disease, and cardiovascular/renal death.

- Strategic Focus: SGLT-2 leadership in Canada's OAD segment; multi-specialty prescriber expansion across cardiology, nephrology, and endocrinology; physician education programs tied to the updated 2024 CDA clinical practice guidelines.

Market Concentration Analysis

The Canada diabetes market displays moderate-to-high concentration at the innovative pharmaceutical level, with the top five originator companies collectively holding approximately 58–62% of total market revenue in 2025. However, domestic generic and biosimilar manufacturers, including Apotex Inc. and Teva Canada, account for a growing share of provincial formulary dispensing volume, particularly for metformin, glibenclamide, and biosimilar glargine, ensuring overall market accessibility from a public health perspective.

Market concentration dynamics are actively shifting as provincial biosimilar substitution mandates and PMPRB pricing reforms create structural pressures on branded manufacturers while creating market-opening opportunities for domestic generics producers. The top-five branded players' combined revenue share is expected to decline modestly from 60% in 2025 to approximately 52–55% by 2034 as genericization of SGLT-2 and DPP-4 molecules accelerates.

Investment & Growth Opportunities

Fastest Growing Segments

GLP-1 receptor agonists (estimated CAGR ~9.2%), biosimilar insulin (volume CAGR ~8.0%), and digital/tele-pharmacy distribution platforms (CAGR ~12%) represent the three highest-growth investment vectors in Canada through 2034. Together, these niches address an incremental addressable market of approximately USD 1.1 Billion by 2034 within the broader Canada diabetes market, with GLP-1 agonists alone expected to exceed USD 650 Million in annual Canadian sales by 2030.

Emerging Market Expansion

Canada's remote and Indigenous communities represent the most underserved high-growth opportunity, with diabetes prevalence rates 3–5x the national average among First Nations, Metis, and Inuit populations, but a pharmaceutical distribution infrastructure that is among the most limited in the developed world. Investment in cold-chain drone-assisted last-mile delivery, tele-pharmacy infrastructure, and culturally competent chronic disease management programs can unlock significant incremental revenue while advancing health equity objectives aligned with Canada's Truth and Reconciliation commitments.

Venture and Institutional Investment Trends

- Key investment themes in Canada include biosimilar insulin manufacturing scale-up (Apotex, Teva pipelines), CGM-integrated digital health platforms targeting employer-sponsored wellness programmes, and tele-pharmacy infrastructure expanding into Northern and rural communities.

- Canada's venture capital ecosystem has seen a surge in digital health investment, with diabetes management platforms attracting CAD 280 Million in disclosed funding between 2022 and 2025, signalling strong institutional appetite for technology-enabled diabetes management tools.

- International pharmaceutical companies are accelerating Health Canada NOC submissions for next-generation GLP-1 and dual GIP/GLP-1 receptor agonists (e.g., tirzepatide, retatrutide) targeting Canada's premium private and employer-sponsored insurance market, the highest-growth sub-segment.

Future Market Outlook (2026-2034)

The Canada diabetes market is positioned for sustained, broad-based growth through 2034. From a base of USD 3,895.30 Million in 2025, the market is projected to reach USD 5,527.4 Million by 2034, representing total incremental value creation of approximately USD 1,632.1 Million over the forecast decade at a CAGR of 3.96%.

Regulatory evolution, particularly Health Canada's advancing biosimilar substitution guidance, the federal Pharmacare Act implementation, and PMPRB pricing reform outcomes, will simultaneously create volume growth opportunities and pricing pressures across segments. Companies that align their portfolio strategies with provincial formulary requirements while building premium private-market franchises in the GLP-1 and connected insulin delivery spaces will capture a disproportionate share of Canada's structurally growing diabetes market.

Long-term, Canada's market trajectory will be shaped by three structural forces: the demographic dividend of an ageing population generating sustained Type-2 diabetes incidence growth; the regulatory and political momentum behind national pharmacare creating a potential step-change in publicly funded coverage; and the maturation of Canada's digital health infrastructure enabling broader therapy access across the country's vast and geographically diverse population.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 130 industry participants in 2024–2025, including pharmaceutical company representatives, hospital pharmacists, retail pharmacy managers, endocrinologists, provincial drug formulary officers, and patient advocacy groups across Canada's major provinces and territories.

Secondary Research

Secondary research encompassed a systematic review of Health Canada regulatory filings, IQVIA Canada pharmaceutical intelligence data, Diabetes Canada epidemiological surveillance reports, provincial drug benefit program formulary publications, company annual reports, PMPRB pricing registry data, and clinical trial registries. Over 220 secondary sources were reviewed and triangulated to ensure data consistency.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating Canadian diabetes epidemiological data, provincial drug plan reimbursement trends, private insurance drug spend data, and biosimilar substitution adoption modelling. A base-case CAGR of 3.96% reflects consensus analyst estimates validated against reported pharmaceutical company Canada segment revenues and provincial formulary expenditure trend data.

Canada Diabetes Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered | Oral Antidiabetics, Insulin |

| Distribution Channels Covered | E-commerce and Tele-pharmacy, Hospital Pharmacies, Retail Pharmacies |

| Companies Covered | Novo Nordisk A/S, Sanofi, Lilly USA, LLC, AstraZeneca, Merck & Co., Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Canada Diabetes Market Report

The Canada diabetes market reached USD 3,895.30 Million in 2025, making it the second-largest diabetes pharmaceutical market in North America and one of the largest per-capita diabetes drug markets among G7 nations.

The market is projected to reach USD 5,527.4 Million by 2034, growing at a CAGR of 3.96% during 2026-2034, driven by rising diabetes prevalence, biosimilar insulin expansion, GLP-1 agonist uptake, and national pharmacare momentum.

Oral antidiabetics lead with a 58.6% market share in 2025 (approximately USD 2,282.6 Million). The segment is anchored by metformin as first-line therapy and driven by rapid GLP-1 receptor agonist and SGLT-2 inhibitor adoption, with Ozempic becoming the most prescribed branded drug in Canada by 2024.

Insulin accounts for 41.4% of the market in 2025 (approximately USD 1,612.7 Million). Biosimilar glargine holds ~22% of the insulin segment in 2025, a share expected to reach 40% by 2034 as provincial substitution mandates expand. This is driving volume growth while moderating average selling prices.

Retail pharmacies lead with 38.5% share in 2025, anchored by Shoppers Drug Mart and Rexall networks. E-commerce and tele-pharmacy represent 27.3% share in 2025 and are the fastest-growing channel, reflecting post-pandemic tele-pharmacy legislation and Canada's high digital health adoption rate.

Ontario leads with approximately 38% market share in 2025, driven by the Ontario Drug Benefit program and the Greater Toronto Area's pharmaceutical infrastructure. Quebec follows with 23%, sustained by the RAMQ universal drug plan. British Columbia (14%), Alberta (12%), and the rest of Canada (13%) complete the regional picture.

Leading companies include Novo Nordisk A/S, Sanofi, Lilly USA, LLC, AstraZeneca, and Merck & Co., Inc., collectively holding approximately 58–62% of market revenue in 2025.

The Ontario Drug Benefit (ODB), Quebec RAMQ, BC PharmaCare, and Alberta Drug Benefit collectively determine formulary access, biosimilar substitution policies, and pricing for a substantial share of Canadian diabetic patients, making provincial listing strategies critical for pharmaceutical manufacturers.

Key growth drivers include rising Type-2 diabetes prevalence, strong digital health and tele-pharmacy adoption, provincial drug plan coverage expansion, the GLP-1 receptor agonist commercial surge led by Ozempic, and biosimilar insulin volume growth through provincial substitution mandates.

Key challenges include out-of-pocket cost barriers for patients without drug insurance (approximately 2.5 million uninsured working-age Canadians), high branded drug costs limiting formulary listing of premium OADs, and rural/remote access inequities, particularly affecting Indigenous communities.

The federal Pharmacare Act, tabled in 2024, has significant potential to reshape the Canada diabetes market by expanding universal public coverage for diabetes medications. Full implementation could materially increase the publicly insured patient population for both OADs and insulins, driving volume growth while applying pricing pressure on branded manufacturers and potentially accelerating generic/biosimilar adoption across all provinces.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)