Canada E-Commerce Market Size, Share, Trends and Forecast by Business Model, Mode of Payment, Service Type, Product Type, and Region, 2026-2034

Canada E-Commerce Market Size, Share, Trends & Forecast (2026-2034)

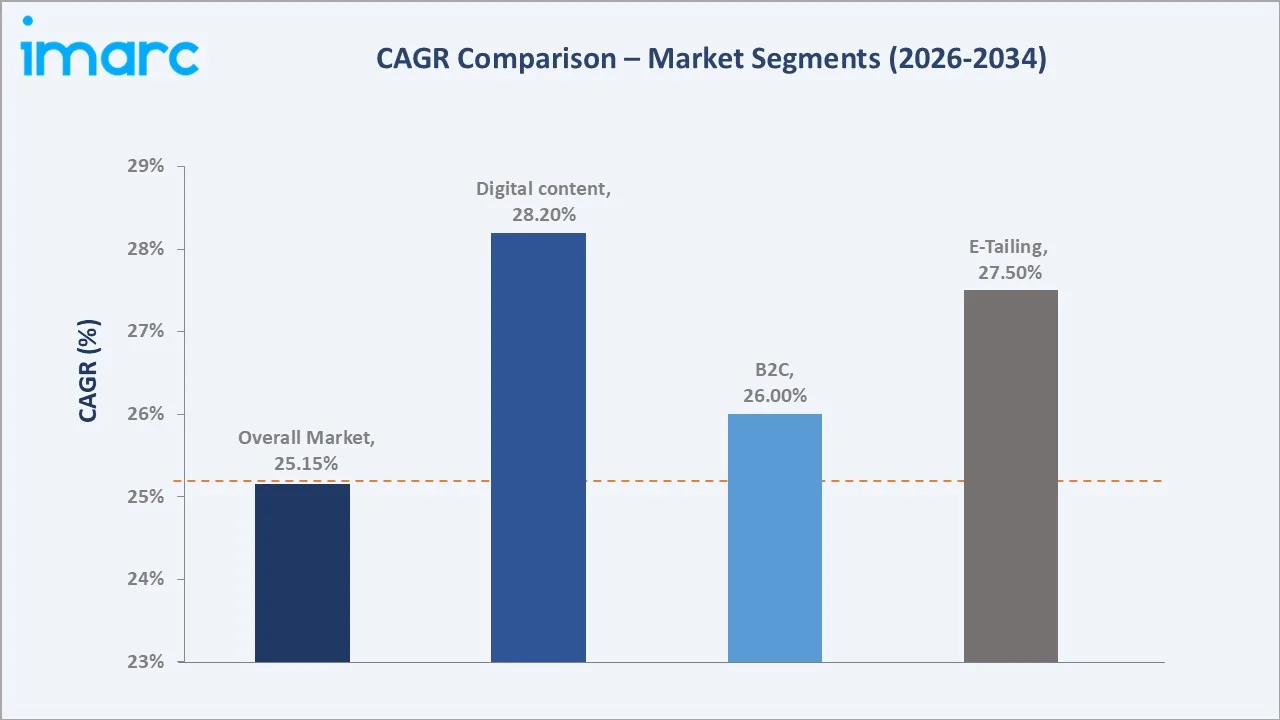

The Canada e-commerce market reached USD 672.3 Billion in 2025 and is projected to reach USD 5,353.6 Billion by 2034, growing at a CAGR of 25.15% during 2026-2034. The market is driven by rapid digital adoption, rising mobile commerce penetration, expanding broadband infrastructure, and evolving consumer preference for online retail. Canada's high internet penetration rate of 95% (2025) provides a strong foundation for sustained e-commerce growth. B2C leads the business model segment at 68.4% in 2025. E-Tailing dominates the service type at 52.6%. Ontario leads regionally at 39.4%, supported by its large population base and advanced digital infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 672.3 Billion |

|

Forecast Market Size (2034) |

USD 5,353.6 Billion |

|

CAGR (2026-2034) |

25.15% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Business Model |

B2C (68.4%, 2025) |

|

Dominant Service Type |

E-Tailing (52.6%, 2025) |

|

Leading Region |

Ontario (39.4%, 2025) |

The Canada e-commerce market grew from USD 219.0 Billion in 2020 to USD 672.3 Billion in 2025, reflecting strong demand expansion driven by pandemic-accelerated digital adoption and sustained post-pandemic growth. The market is expected to reach USD 2,064.0 Billion by 2030, supported by mobile commerce, AI-powered personalization, and expanding rural connectivity. By 2034, the market is projected to attain USD 5,353.6 Billion, driven by omnichannel integration, social commerce, and digital payments modernization.

To get more information on this market, Request Sample

B2B e-commerce grows at approximately 24.8% CAGR through 2034 via enterprise procurement digitalization and supply chain integration. Digital content grows fastest at approximately 28.2% CAGR through streaming platforms, SaaS, and digital subscriptions expansion.

Executive Summary

The Canada e-commerce market is expected to grow at an exceptional pace, rising from USD 672.3 Billion in 2025 to USD 5,353.6 Billion by 2034. Growth is supported by rising internet penetration, accelerating smartphone adoption, expanding digital payment options, and shifting consumer behavior toward online retail. Canada's digital-first economy, led by Amazon Canada and Walmart Canada, provides a competitive and innovation-driven marketplace. Federal broadband investments targeting rural connectivity and the emergence of Canada's Real-Time Rail (RTR) payment infrastructure will continue catalyzing market expansion.

B2C leads at 68.4% (2025) through direct-to-consumer platforms, marketplace retail, and subscription commerce. E-Tailing at 52.6% dominates via apparel, electronics, and home goods. Ontario at 39.4% drives national volumes through its concentrated urban population. However, challenges include cybersecurity threats, high last-mile logistics costs, and cross-border duty complexities. Overall, the market presents exceptional opportunities for merchants, platform providers, and logistics companies.

Key Market Insights

|

Insight |

Data |

|

Dominant Business Model |

B2C - 68.4% share (2025) |

|

Dominant Service Type |

E-Tailing - 52.6% market share (2025) |

|

Leading Region |

Ontario - 39.4% share (2025) |

|

Market Opportunity |

Mobile commerce expansion; AI-driven personalization; cross-border e-commerce growth; rural broadband rollout; social commerce integration |

Key Analytical Observations Supporting The Above Data:

- B2C at 68.4%: B2C dominates due to consumer preference for direct online shopping, convenience, competitive pricing, and broad product availability across marketplaces. Mobile-optimized interfaces and loyalty programs further reinforce B2C leadership.

- E-Tailing at 52.6%: E-Tailing leads through fashion, electronics, and home goods, benefiting from product variety, competitive discounting, and improved logistics. Same-day and next-day delivery investments by Amazon and Walmart have accelerated e-tailing adoption.

- Ontario at 39.4%: Ontario dominates due to its dense urban population, high household income, advanced digital infrastructure, and concentration of major distribution centers and technology companies.

Canada E-Commerce Market Overview

The Canada e-commerce market encompasses the buying and selling of goods and services over digital platforms, including B2C retail, B2B procurement, C2C marketplaces, digital content, financial services, and travel and leisure segments. The market is supported by high internet penetration (95% in 2025), widespread smartphone adoption, and a diverse range of digital payment solutions. Canada's bilingual market environment, with English and French as official languages, adds complexity for platform operators, driving investment in localization technologies.

Key market participants include global marketplace giants, domestic retailers, and fintech disruptors. Macroeconomic factors influencing the market include consumer spending levels, Bank of Canada interest rate policies, retail inflation trends, government digital infrastructure investments, and cross-border trade agreements. The market is further shaped by evolving privacy regulations under PIPEDA and provincial data protection frameworks.

Market Dynamics

To evaluate market opportunities, Request Sample

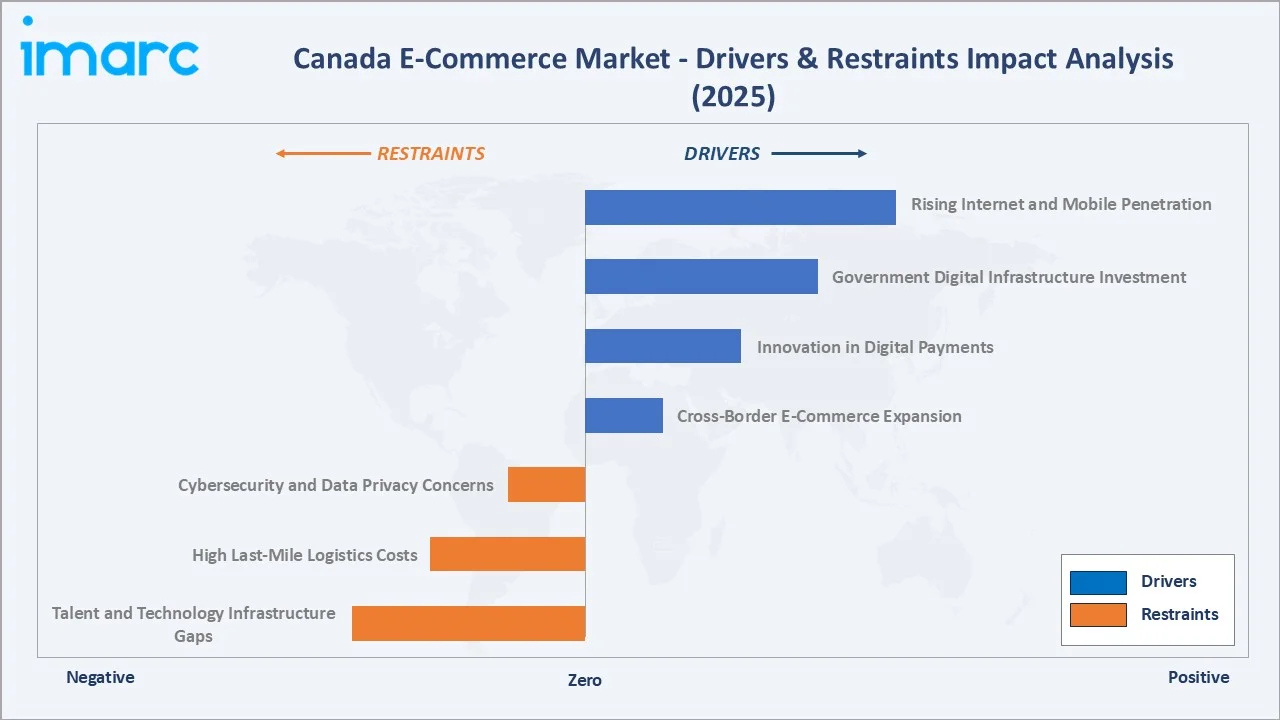

Market Drivers

- Rising Internet and Mobile Penetration: Canada's internet penetration reached 95% in 2025, according to Statistics Canada, providing a vast addressable digital consumer base. Mobile commerce is projected to account for over 50% of all e-commerce transactions in Canada by 2025, with smartphone users reaching 35 million. As consumers increasingly rely on mobile apps for shopping, platforms investing in mobile-first experiences capture higher conversion rates and stronger customer retention.

- Government Digital Infrastructure Investment: Federal and provincial broadband initiatives, including the Universal Broadband Fund (UBF) targeting USD 2.35 billion in investment, are expanding internet access in underserved rural and remote communities. Increased connectivity directly expands the e-commerce addressable market, unlocking new consumer segments outside major metropolitan areas such as Toronto, Vancouver, and Montreal.

Market Restraints

- Cybersecurity and Data Privacy Concerns: Cybersecurity risks remain a primary challenge, with data breaches, payment fraud, and phishing attacks exposing consumers and merchants to financial losses. Canada's PIPEDA regulations impose strict data protection obligations, increasing compliance costs for e-commerce operators. Consumer distrust of data handling practices limits conversion rates, particularly among older demographic segments.

- High Last-Mile Logistics Costs: Canada's vast geography creates significant logistical challenges, with last-mile delivery costs substantially higher in suburban and rural regions than in dense urban centers. Retailers report 15-20% higher per-unit delivery costs in regions outside Toronto, Vancouver, and Montreal. These elevated costs constrain margin expansion and limit the affordability of free or low-cost shipping offers that drive consumer purchase decisions.

Market Opportunities

- Innovation in Digital Payments: Canada's Real-Time Rail (RTR) system under Payments Canada's modernization program, set to launch in Q4 2026, will introduce instant account-to-account payment rails. By 2025, digital payments account for approximately 86% of total payment volume. Digital wallets including Apple Pay, Google Pay, and Interac e-Transfer reduce transaction friction, increase checkout conversion, and attract mobile-native consumers.

- Cross-Border E-Commerce Expansion: Canada's support for the WTO customs duty moratorium and bilateral trade agreements facilitate cross-border digital trade. Approximately 68% of Canadian consumers (2025) prefer Canadian products, yet cross-border platforms such as Temu and Shein are scaling logistics partnerships to improve delivery speeds. Domestic merchants can capitalize on this preference through "buy Canadian" positioning and enhanced fulfillment capabilities.

- AI-Driven Personalization and Social Commerce: Artificial intelligence is transforming product discovery, recommendation engines, and customer experience management. Social commerce integration, particularly through platforms adopted by Canadian youth demographics, is creating new direct purchase pathways. Brands leveraging influencer coalitions and shoppable social media content can bypass traditional advertising costs and achieve high conversion rates.

Market Challenges

- Talent and Technology Infrastructure Gaps: E-commerce growth requires continuous investment in software development, data science, cybersecurity, and logistics technology. Canada faces skilled talent shortages in AI, machine learning, and supply chain engineering, constraining innovation velocity. Platform operators and retailers competing with global technology companies for talent face elevated hiring costs.

- Regulatory and Compliance Complexity: Quebec's Bill 96 mandates French-language parity across all digital touchpoints, affecting approximately 250,000 businesses. Compliance with multilingual requirements, combined with evolving privacy laws and cross-border duty thresholds, creates an increasingly complex regulatory environment. These complexities raise operational costs and slow market entry for smaller merchants.

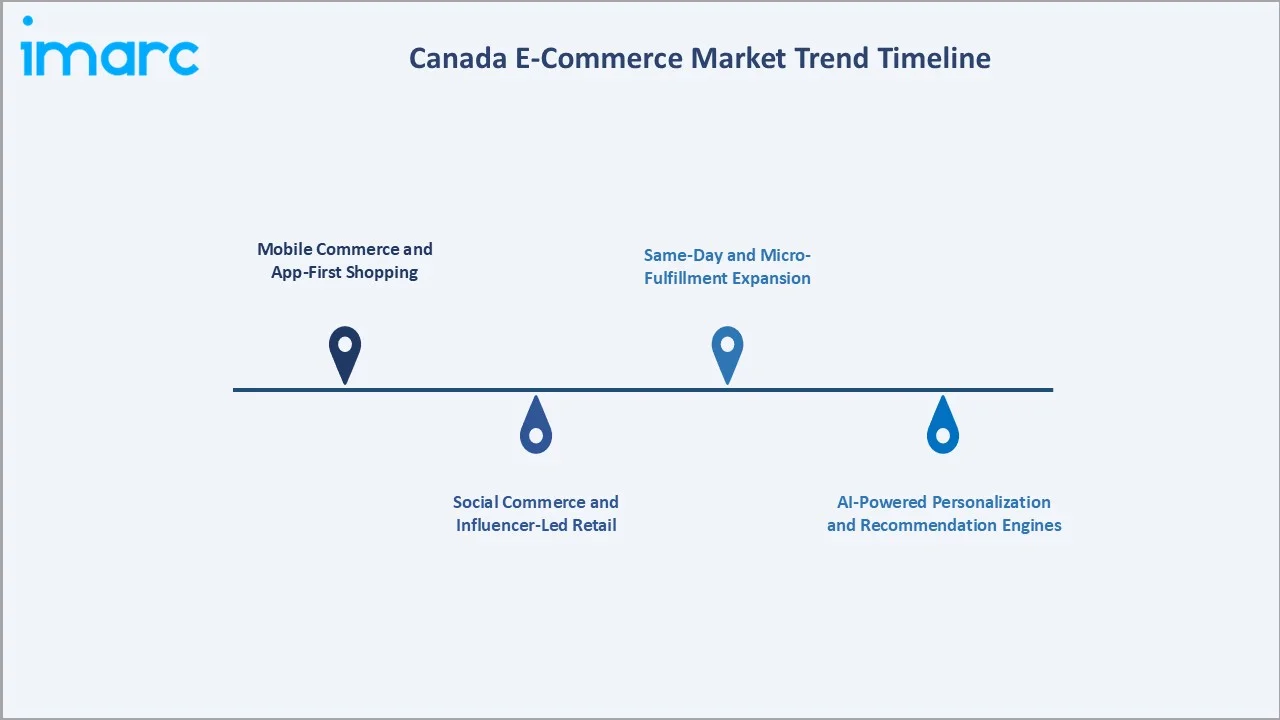

Emerging Market Trends

1. Mobile Commerce and App-First Shopping

Mobile commerce is emerging as the dominant e-commerce channel, with smartphone-based transactions projected to exceed 50% of total online purchases in Canada by 2025. Retailers are accelerating investments in native mobile apps, one-click checkout, and push notification-driven re-engagement campaigns. Platforms delivering sub-3-second mobile load times report 20-30% conversion uplifts, making mobile UX optimization a core competitive differentiator.

2. Social Commerce and Influencer-Led Retail

Social commerce is reshaping product discovery and purchase pathways. Canadian brands are leveraging Instagram, TikTok, and Pinterest shopping integrations to enable direct in-feed purchases. Influencer-led product launches on social platforms generate rapid brand awareness and drive impulse purchasing, particularly in fashion, beauty, and consumer electronics categories. Social commerce adoption is projected to accelerate through 2030 as platform shopping features mature.

3. Same-Day and Micro-Fulfillment Expansion

Same-day delivery has shifted from a premium service to a baseline expectation in Toronto, Ottawa, and Montreal. Retailers adopting same-day delivery report revenue lifts of approximately 10% and customer satisfaction gains of 80%. Micro-fulfillment centers embedded in mixed-use urban properties are reducing last-mile delivery windows.

4. AI-Powered Personalization and Recommendation Engines

Artificial intelligence is transforming the e-commerce experience through hyper-personalized product recommendations, dynamic pricing engines, and predictive inventory management. Shopify's AI improvements and machine learning integration across Canadian retailer platforms are improving conversion rates and average order values. One in five Canadian consumers (2025) is willing to pay a 20% premium for personalized products, driving AI investment across the market.

5. Sustainable and Ethical E-Commerce

Canadian consumers, particularly younger demographics, are prioritizing sustainability in their online purchasing decisions. E-commerce platforms are adapting by highlighting eco-friendly product certifications, carbon-neutral shipping options, and ethical sourcing credentials. Brands that transparently communicate environmental commitments are gaining preference among the 18-35 age cohort, creating a measurable premium market segment.

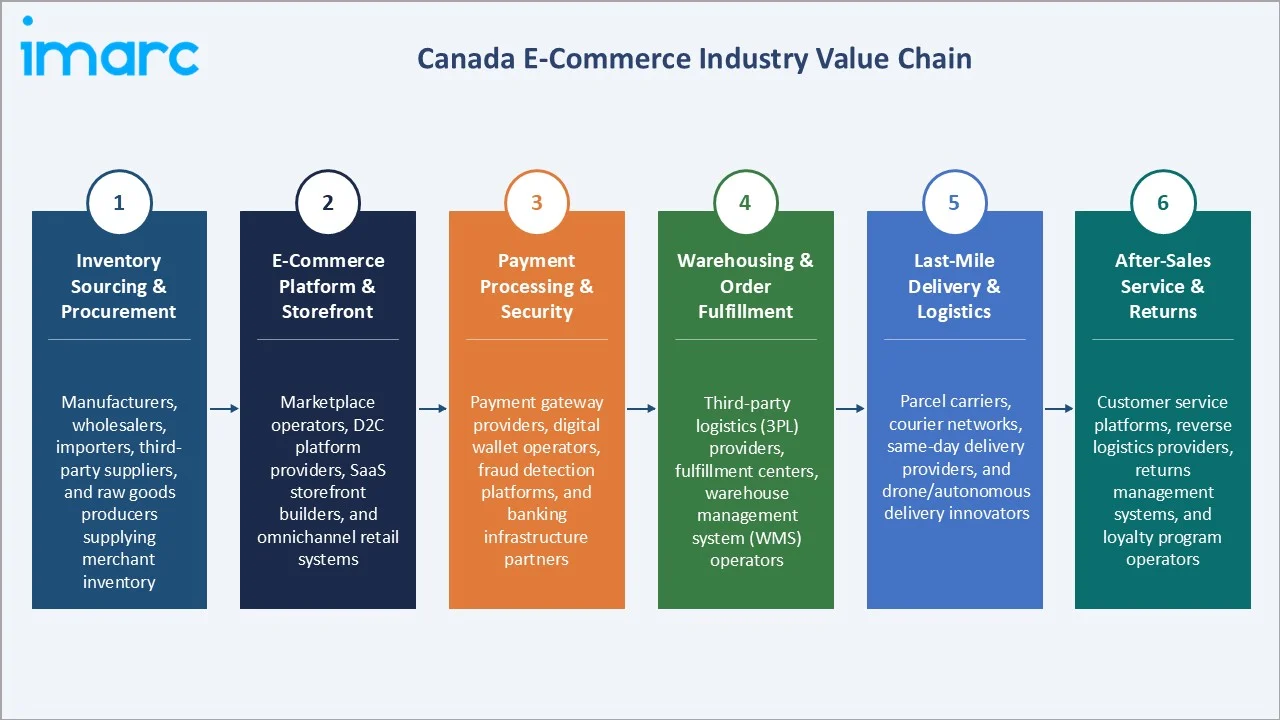

Industry Value Chain Analysis

The Canada e-commerce value chain integrates inventory sourcing and procurement, platform and storefront operations, payment processing, warehousing and fulfillment, last-mile delivery, and after-sales service. Each stage adds value through specialization, technology integration, and operational efficiency. The most value-added stages are platform and payment processing, where technology differentiation drives consumer loyalty and conversion rates.

|

Stage |

Key Participants |

|

Inventory Sourcing & Procurement |

Manufacturers, wholesalers, importers, third-party suppliers, and raw goods producers supplying merchant inventory |

|

E-Commerce Platform & Storefront |

Marketplace operators, D2C platform providers, SaaS storefront builders, and omnichannel retail systems |

|

Payment Processing & Security |

Payment gateway providers, digital wallet operators, fraud detection platforms, and banking infrastructure partners |

|

Warehousing & Order Fulfillment |

Third-party logistics (3PL) providers, fulfillment centers, warehouse management system (WMS) operators |

|

Last-Mile Delivery & Logistics |

Parcel carriers, courier networks, same-day delivery providers, and drone/autonomous delivery innovators |

|

After-Sales Service & Returns |

Customer service platforms, reverse logistics providers, returns management systems, and loyalty program operators |

The platform and payment stages represent the highest value concentration, as technology-driven personalization, seamless checkout, and fraud prevention directly determine conversion rates and repeat purchase behavior. Logistics and last-mile delivery are emerging as critical competitive differentiators, with major players investing heavily in fulfillment speed and coverage to meet rising consumer expectations.

Technology Landscape in the Canada E-Commerce Industry

Artificial Intelligence and Machine Learning

AI and machine learning are transforming personalization, demand forecasting, and customer service across Canada's e-commerce landscape. Recommendation engines powered by deep learning algorithms now drive significant portions of product discovery revenue for major platforms. Natural language processing enables conversational commerce through chatbots and voice assistants, while computer vision supports visual search and augmented reality try-on features in fashion and beauty categories.

Mobile Commerce and Progressive Web Apps

Progressive web app (PWA) technology is enabling retailers to deliver app-quality experiences through mobile browsers, reducing friction in the customer acquisition journey. Native iOS and Android apps with biometric authentication, one-tap checkout, and push notifications are accelerating mobile conversion rates. Canada's leading e-commerce platforms are investing in cross-device synchronization to support consumers who research on mobile and purchase on desktop.

Logistics Technology and Automation

Warehouse automation through robotics, conveyor systems, and AI-driven picking optimization is improving fulfillment speed and accuracy. Route optimization algorithms and predictive delivery windows are reducing last-mile costs by 15-20% for high-density urban markets. Autonomous delivery pilot programs in select Canadian cities point toward future cost reduction opportunities.

Payments and Fintech Integration

Canada's Real-Time Rail (RTR) system is set to enable instant account-to-account payments, reducing card processing fees for merchants. Buy Now Pay Later (BNPL) solutions are growing at an 18.82% CAGR through 2031, expanding purchasing power for mid-income consumers. Cryptocurrency payment integration and stablecoin-based commerce remain nascent but are being explored by digital-native platforms targeting tech-savvy demographics.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Business Model |

B2C |

68.4% |

2025 |

|

Service Type |

E-Tailing |

52.6% |

2025 |

|

Mode of Payment |

🔒 |

🔒 |

2025 |

|

Product Type |

🔒 |

🔒 |

2025 |

|

Region |

Ontario |

39.4% |

2025 |

By Business Model

B2C leads at 68.4% (2025), driven by marketplace platforms like Amazon.ca and Walmart.ca-powered direct-to-consumer storefronts. Consumer preference for convenience, competitive pricing, and broad product assortments underpins B2C dominance. Mobile-optimized shopping apps and loyalty programs reinforce consumer retention within B2C channels.

To access detailed market analysis, Request Sample

B2B at 21.7% is growing rapidly as enterprise procurement digitalization accelerates. Companies are shifting to online sourcing platforms for office supplies, industrial equipment, and business services. C2C at 6.3% operates through platforms like eBay Canada, Facebook Marketplace, and Kijiji. Others at 3.6% include government e-procurement, nonprofit digital fundraising, and hybrid models.

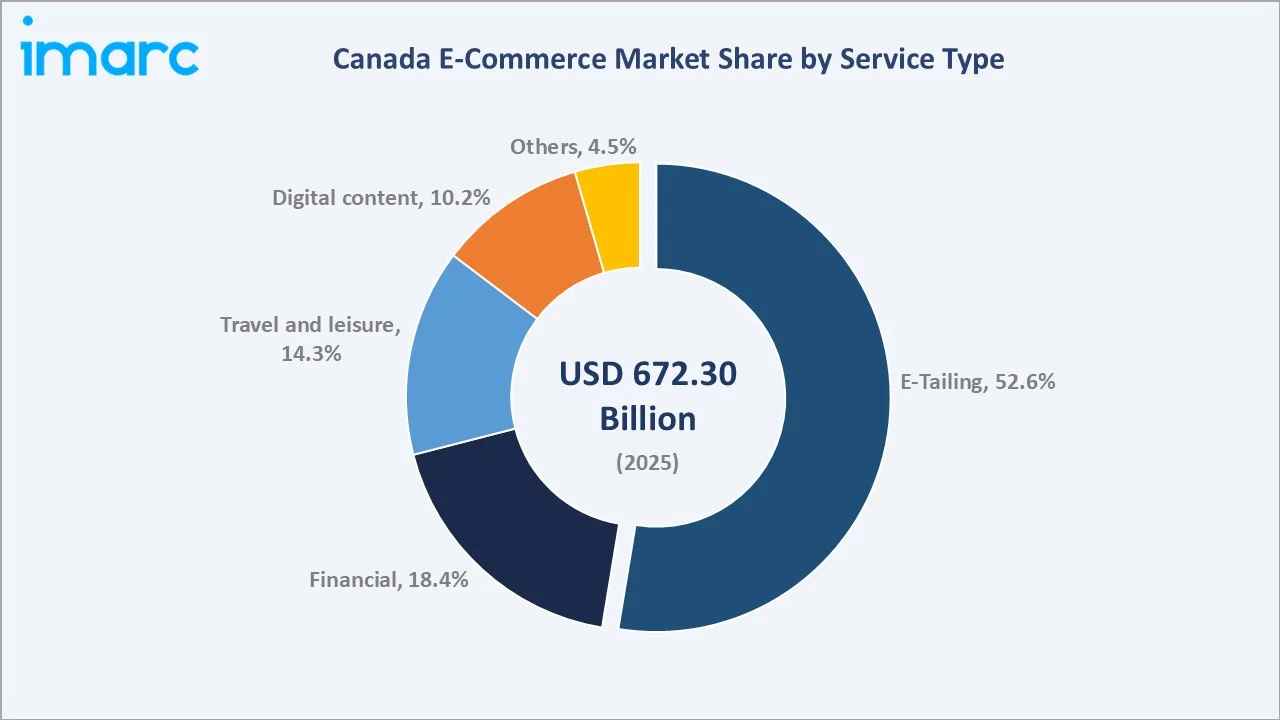

By Service Type

E-Tailing leads at 52.6% (2025) through fashion, electronics, home goods, and grocery categories. Amazon Canada's projection of 98% of Canadian sales through e-commerce channels by 2027 highlights the e-tailing trajectory. Consumer demand for product variety, competitive pricing, and next-day delivery continues to expand e-tailing's market share.

Financial services at 18.4% include digital banking, insurance, and investment platforms. Travel and leisure at 14.3% benefits from growing online booking adoption across airlines, hotels, and experience providers. Digital content at 10.2% grows at approximately 28.2% CAGR through streaming, gaming, e-learning, and SaaS subscriptions. Others at 4.5% include government services, healthcare telemedicine, and niche digital platforms.

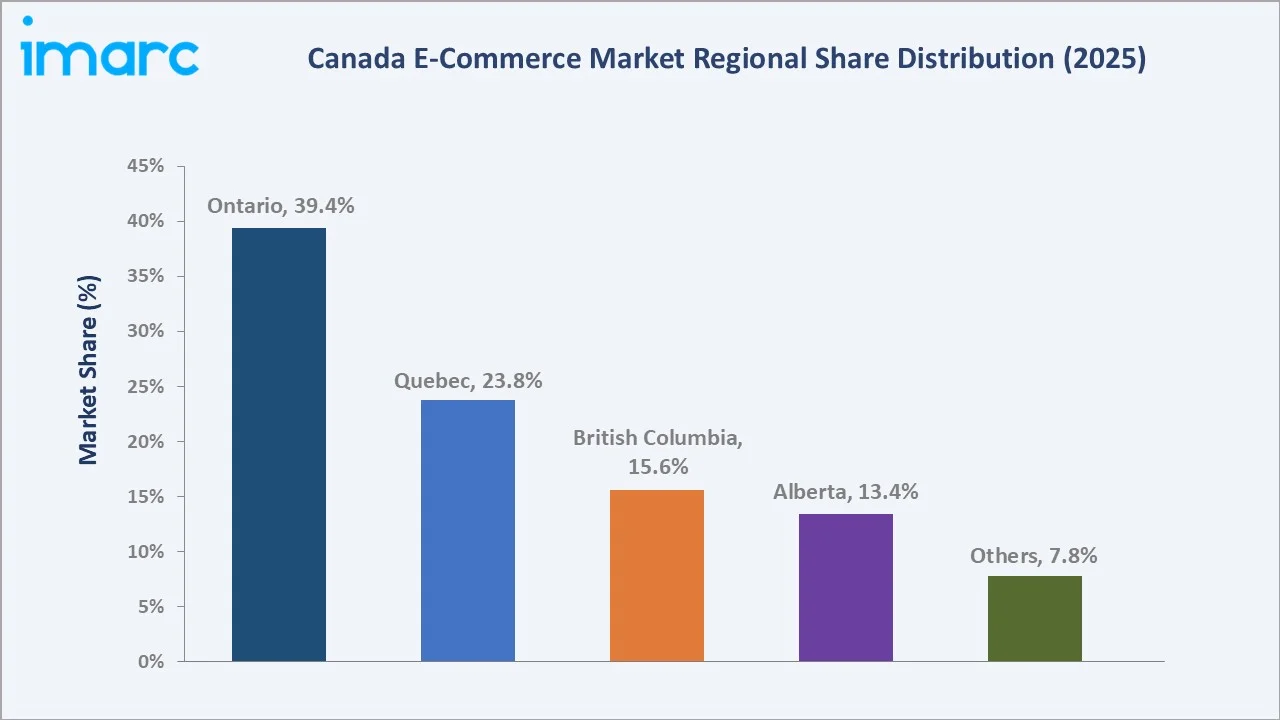

Regional Market Insights

|

Region |

Share (2025) |

Key E-Commerce Market Drivers & Characteristics |

|

Ontario |

39.4% |

Benefits from dense urban population, high household incomes, advanced logistics infrastructure, and strong technology company concentration driving B2C and B2B adoption. |

|

Quebec |

23.8% |

Supported by French-language platform investments, growing mobile commerce, transportation digitalization, and provincial e-commerce support programs. |

|

British Columbia |

15.6% |

Driven by tech-forward consumer demographics in Vancouver, expanding cross-border trade with Asia-Pacific markets, and strong LNG and tourism digital booking activity. |

|

Alberta |

13.4% |

Supported by high per-capita income from oil and gas employment, growing agricultural e-procurement, and strong enterprise B2B platform adoption. |

|

Others |

7.8% |

Includes Saskatchewan, Manitoba, Nova Scotia, New Brunswick, and Northern Territories contributing through rural e-commerce, agricultural supply procurement, and government digital services. |

Ontario's 39.4% dominance reflects its status as Canada's largest provincial economy, highest population density, and home to major distribution centers for Amazon, Walmart, and Costco fulfillment networks. Quebec's 23.8% is driven by sustained government investment in French-language digital commerce and growing mobile commerce adoption in Montreal's tech ecosystem.

British Columbia's 15.6% benefits from cross-Pacific trade linkages, high consumer technology adoption in Metro Vancouver, and growing online booking in the province's substantial tourism sector. Alberta's 13.4% is underpinned by high disposable income levels, expanding agricultural e-procurement platforms, and enterprise digital transformation in Calgary's energy sector. Others at 7.8% contribute through expanding rural broadband coverage, agricultural supply e-procurement, and targeted government digital service investments across Atlantic Canada and the Northern territories.

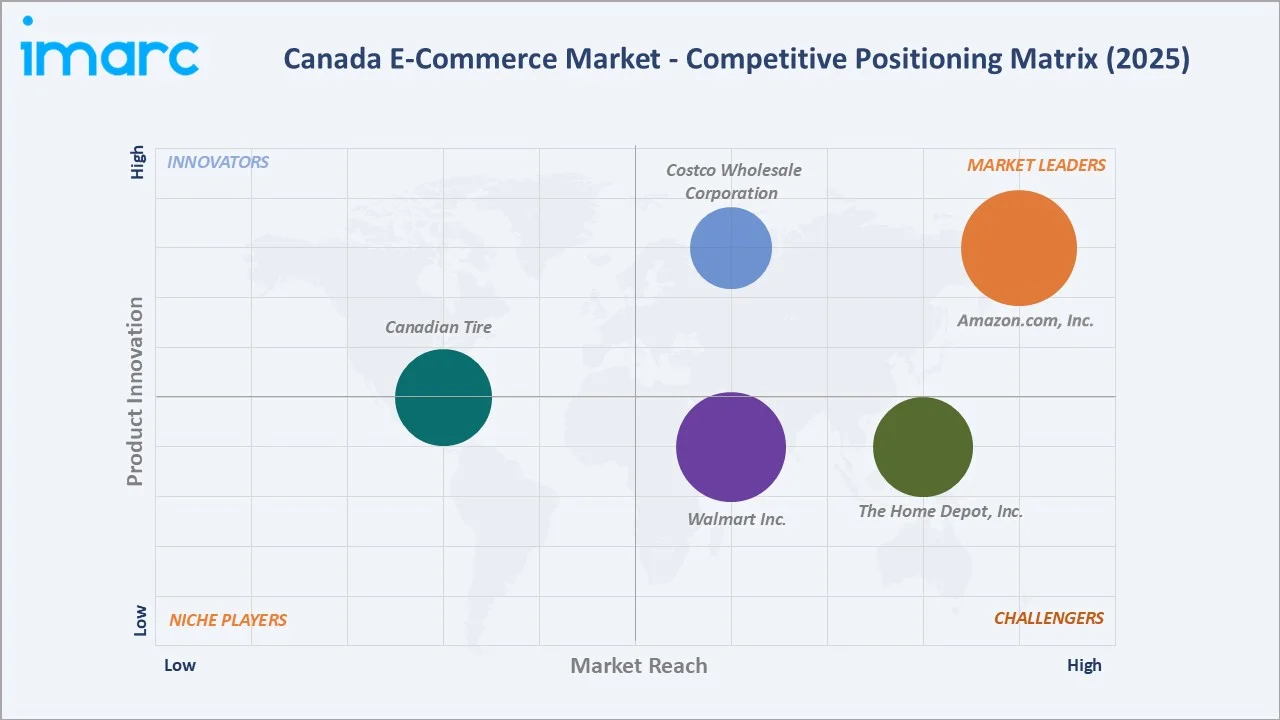

Competitive Landscape

The Canada e-commerce market is moderately concentrated, with the top players holding approximately 40% market share. Competition is led by global marketplace platforms, domestic technology companies, and omnichannel retail giants. Market participants compete on fulfillment speed, platform breadth, payment convenience, AI-powered personalization, and customer loyalty programs.

|

Company |

E-commerce Platform |

Market Position |

Core Strength |

|

Amazon.com, Inc. |

Amazon.ca |

Market Leader |

Amazon Canada leads through Prime membership loyalty, fastest fulfillment via robotics DCs, and comprehensive marketplace enabling third-party sellers |

|

Costco Wholesale Corporation |

Costco.ca |

Market Leader |

Loyalty-driven membership model, online-exclusive categories, Kirkland signature brand, express delivery |

|

Walmart Inc. |

Walmart.ca |

Strong Challenger |

Walmart Canada leverages its extensive physical store network as forward-inventory nodes, reducing last-mile costs and enabling same-day pickup |

|

The Home Depot, Inc. |

Homedepot.ca |

Strong Challenger |

"Magic Apron" AI integration, pro-centric digital tools, user-generated content, omnichannel fulfillment |

|

Canadian Tire |

canadiantire.ca |

Established Player |

Triangle rewards integration, unified digital platform, advanced AI and retail intelligence, supply chain and logistics scale |

Strategic investments in logistics automation, retail media networks, and AI-driven personalization are defining competitive advantage. The growing focus on social commerce, buy-now-pay-later financial tools, and omnichannel integration is further driving product innovation and market differentiation.

Key Company Profiles

Amazon.com, Inc.

Amazon.com, Inc., which operates Amazon.com.ca ULC, is the dominant e-commerce marketplace in Canada, offering tens of millions of products across electronics, fashion, home goods, grocery, and digital services. Operating through Amazon.ca, Prime Video, and Amazon Fresh, the company serves millions of Canadian Prime members with fast, reliable delivery and exclusive digital content.

- Key Platform: Amazon.ca

- Strategic Focus: Deepening Prime ecosystem loyalty, scaling same-day and next-day delivery infrastructure, expanding AWS enterprise cloud services, and growing Amazon Ads retail media revenue in Canada.

Costco Wholesale Corporation

Costco Wholesale Corporation, which operates Costco Wholesale Canada Ltd., is one of the largest grocery retailers in Canada. Operating a network of membership-only warehouse clubs, Costco Wholesale Canada serves more than 10 million members across Canada, offering discount prices on approximately 4,000 products, many in bulk packaging, including appliances, food, furniture, office products, and software.

- Key Platform: Costco.ca

- Strategic Focus: Costco's recent expansion has been driven by a relocation and conversion strategy that allows the company to grow efficiently, including opening new, larger consumer warehouses and converting former locations into business centers.

Walmart Inc.

Walmart Inc., which operates Walmart Canada, is a prominent omnichannel retail network, with approximately 400+ stores and a growing digital commerce platform at Walmart.ca. The company integrates its store footprint as a fulfillment asset, offering ship-from-store, curbside pickup, and same-day delivery options.

- Key Platform: Walmart.ca

- Strategic Focus: Deepening store-based fulfillment integration, expanding Walmart Marketplace seller volumes, growing grocery e-commerce penetration, and competing with Amazon Prime through Walmart+ loyalty programs.

Market Concentration Analysis

The Canada e-commerce market is moderately concentrated, with the top five players - Amazon.com, Inc., Costco Wholesale Corporation, Walmart Inc., The Home Depot, Inc., and Canadian Tire - holding approximately 40% combined market share in 2025. The remaining 60% is distributed across thousands of mid-market merchants, vertical specialists, and D2C brands operating on third-party platforms.

Market concentration is increasing as major platforms invest in fulfillment infrastructure, retail media networks, and AI personalization tools that create structural advantages over smaller competitors. Amazon's Prime loyalty ecosystem, Walmart's merchant platform scale, and large retailers’ omnichannel integration position them as dominant forces. However, the 60% unconcentrated share reflects a highly dynamic mid-market with ongoing opportunities for vertical specialists and niche platform operators.

Investment & Growth Opportunities

Highest Growth Segments

Digital content grows at approximately 28.2% CAGR through streaming subscriptions, SaaS platforms, and gaming. E-Tailing grows at 27.5% CAGR through fashion and electronics. Mobile commerce investment across app development and PWA optimization generates strong conversion returns. Rural e-commerce expansion enabled by federal broadband investment unlocks previously underserved consumer segments.

Investment Themes

- Mobile Commerce Infrastructure: Investments in native mobile app development, progressive web apps, and mobile payment integration target Canada's rapidly growing smartphone-first consumer base. Platform operators achieving sub-3-second mobile load times report 20-30% higher conversion rates.

- Logistics and Last-Mile Technology: Micro-fulfillment centers, route optimization AI, and same-day delivery networks represent high-return investment opportunities as consumer delivery expectations intensify. Property developers and logistics operators partnering to embed fulfillment infrastructure in urban mixed-use properties are capturing premium occupancy and fee revenues.

- AI and Personalization Platforms: AI-powered recommendation engines, dynamic pricing tools, and predictive inventory management platforms are generating measurable revenue lifts for merchants. With one in five Canadian consumers willing to pay 20% more for personalized products, AI-driven commerce solutions offer strong monetization potential.

- Cross-Border E-Commerce Enablement: Technology platforms simplifying cross-border checkout, duty calculation, and international returns management address a growing opportunity as Canadian merchants expand globally and global brands scale their Canadian presence.

Future Market Outlook (2026-2034)

The Canada e-commerce market is projected to grow from USD 672.3 Billion in 2025 to USD 5,353.6 Billion by 2034, delivering a 25.15% CAGR over the forecast period. The anchor market value of USD 2,064.0 Billion in 2030 represents the market's digital commerce maturation inflection point, where mobile-first consumer behavior, AI-driven personalization, and autonomous fulfillment converge to redefine the online retail experience.

Three structural forces are expected to define Canada's e-commerce growth trajectory through 2034. First, continued expansion of mobile commerce and social commerce channels will deepen consumer engagement and drive incremental transaction volumes across B2C and C2C segments. Second, sustained government investment in broadband connectivity will unlock rural and remote consumer markets, broadening the addressable digital economy.

Third, logistics technology innovation - including AI-powered fulfillment, drone delivery pilots, and autonomous last-mile solutions - will compress delivery timelines and reduce operational costs, enabling both margin improvement and competitive price positioning. Together, these forces point to a Canada e-commerce market entering a transformative scale phase where platform breadth, logistics excellence, and AI capability will determine long-term competitive outcomes.

Research Methodology

Primary Research

Primary research comprised structured interviews and consultations with e-commerce platform operators, logistics providers, digital payment companies, retail merchants, and consumer behavior specialists across Canada. Insights were gathered on market trends, platform adoption drivers, fulfillment economics, payment preferences, and regulatory impacts. Industry expert consultations validated market size estimates, segment share assumptions, and competitive positioning assessments.

Secondary Research

Secondary research encompassed company annual reports, Statistics Canada e-commerce sales data, International Trade Administration country commercial guides, government digital infrastructure announcements, industry association publications, and financial analyst reports. Sources included data from the Bank of Canada, Innovation, Science and Economic Development Canada (ISED), and Payments Canada. Platform-specific disclosures from Amazon, Costco, and Walmart Canada supplemented market sizing and trend analysis.

Forecasting Models

Forecasting models combined historical e-commerce sales performance from 2020-2025, demographic and internet penetration trends, mobile commerce adoption curves, government broadband investment timelines, and competitive landscape dynamics to project market growth through 2034. The analysis incorporated CAGR-based projections, segment-level demand modeling, and scenario analysis evaluating accelerated digital adoption versus baseline growth trajectories.

Canada E-Commerce Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Busines Models Covered | B2C, B2B, C2C, Others |

| Modes Of Payments Covered | Payment Cards, Online Banking, E-Wallets, Cash-On-Delivery, Others |

| Service Types Covered | Financial, Digital Content, Travel and Leisure, E-Tailing, Others |

| Product Types Covered | Groceries, Clothing and Accessories, Mobiles and Electronics, Health and Personal Care, Others |

| Regions Covered | Ontario, Quebec, Alberta, British Columbia, Others |

| Companies Covered | Amazon.com Inc., Costco Wholesale Corporation, Walmart Inc., The Home Depot Inc., Canadian Tire, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Canada e-commerce market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Canada e-commerce market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Canada e-commerce industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Canada E-Commerce Market Report

The Canada e-commerce market reached USD 672.3 Billion in 2025, driven by high internet penetration, mobile commerce growth, digital payment adoption, and accelerating consumer preference for online retail.

The market grows at a 25.15% CAGR during 2026-2034, reaching USD 5,353.6 Billion by 2034, reflecting sustained digital adoption and platform innovation.

B2C leads at 68.4% (2025) due to marketplace scale, mobile app convenience, and direct-to-consumer brand growth on platforms like Amazon.ca and Walmart.ca storefronts.

E-Tailing dominates at 52.6% (2025), driven by fashion, electronics, and home goods demand, along with competitive pricing and improving fulfillment speed.

Ontario leads at 39.4% (2025) due to its dense urban population, high incomes, advanced logistics infrastructure, and concentration of major e-commerce distribution centers.

Leading companies include Amazon.com, Inc., Costco Wholesale Corporation, Walmart Inc., The Home Depot, Inc., and Canadian Tire, among others.

The market is projected to reach approximately USD 2,064.0 Billion by 2030, supported by mobile commerce expansion, social commerce growth, and rural broadband deployment.

Mobile commerce is driven by 44% smartphone internet usage (2023), mobile-optimized app experiences, one-click checkout, and digital wallet adoption through Apple Pay and Interac e-Transfer.

B2C leads at 68.4% through consumer marketplace retail. B2B at 21.7% is growing rapidly as enterprise procurement platforms digitalize purchasing workflows.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)