Canada Geotechnical Services Market Size, Share, Trends and Forecast by Type, End-User, and Region, 2026-2034

Canada Geotechnical Services Market Size, Share, Trends & Forecast (2026-2034)

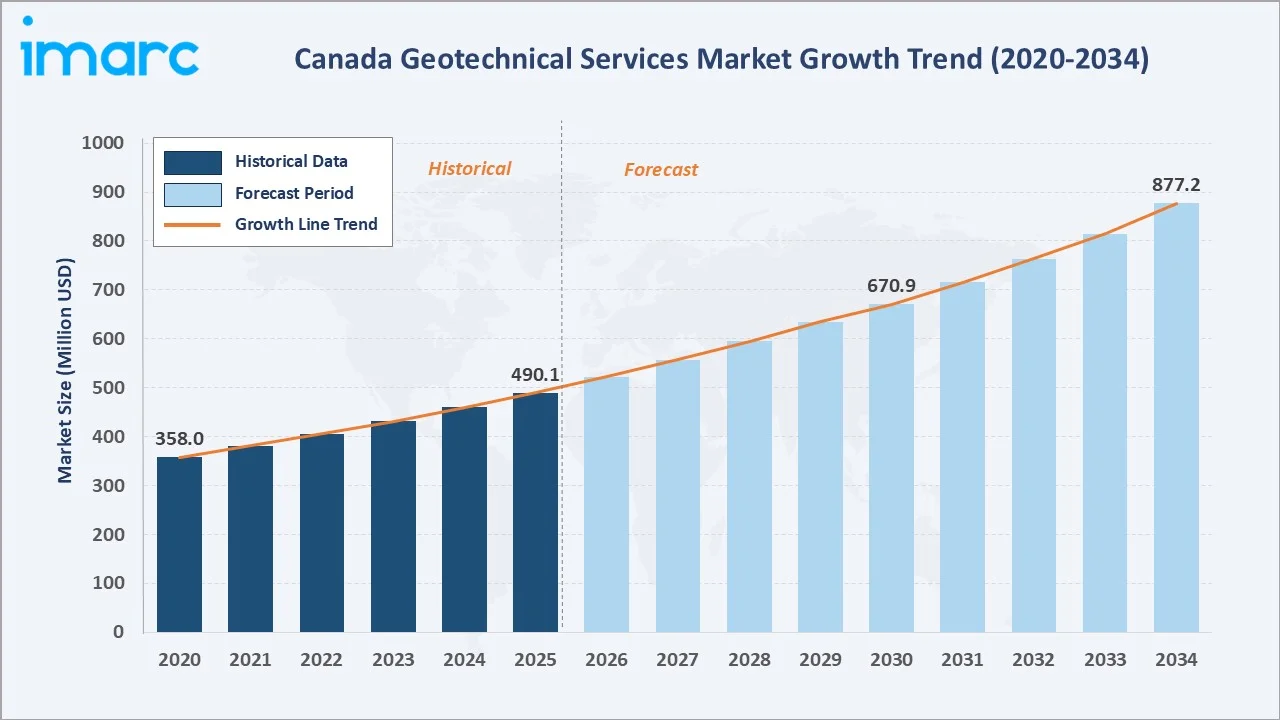

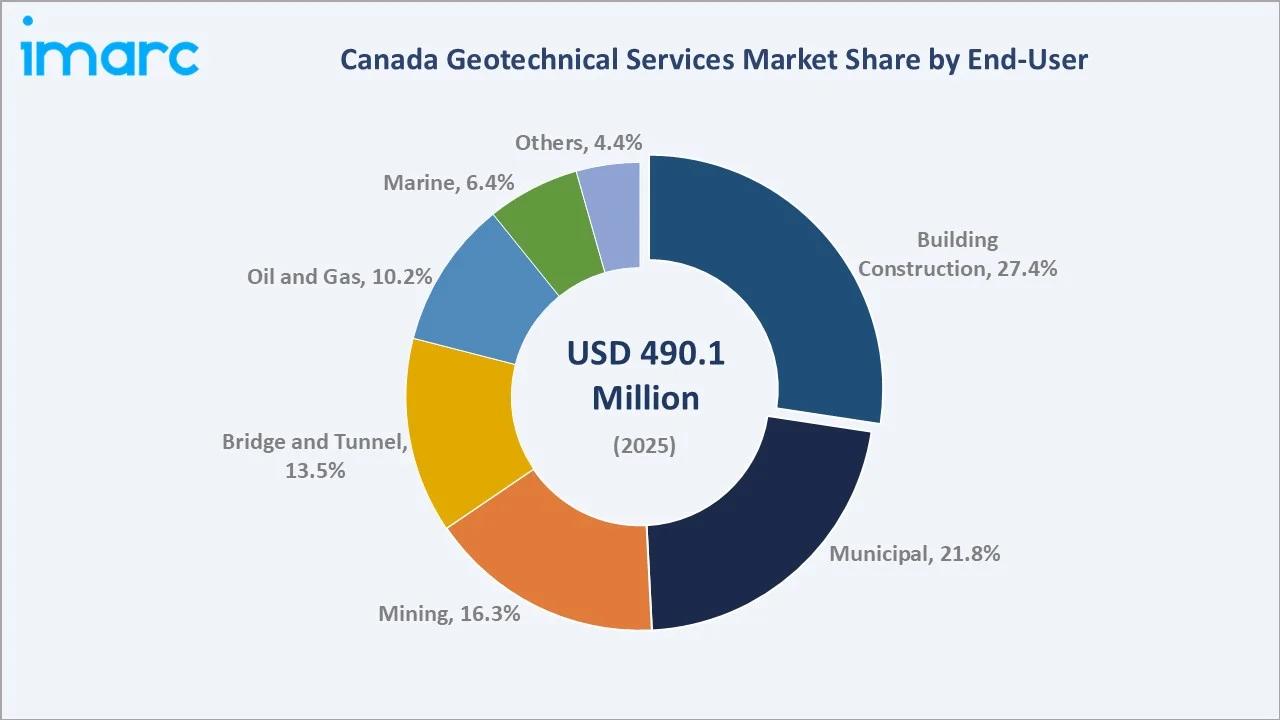

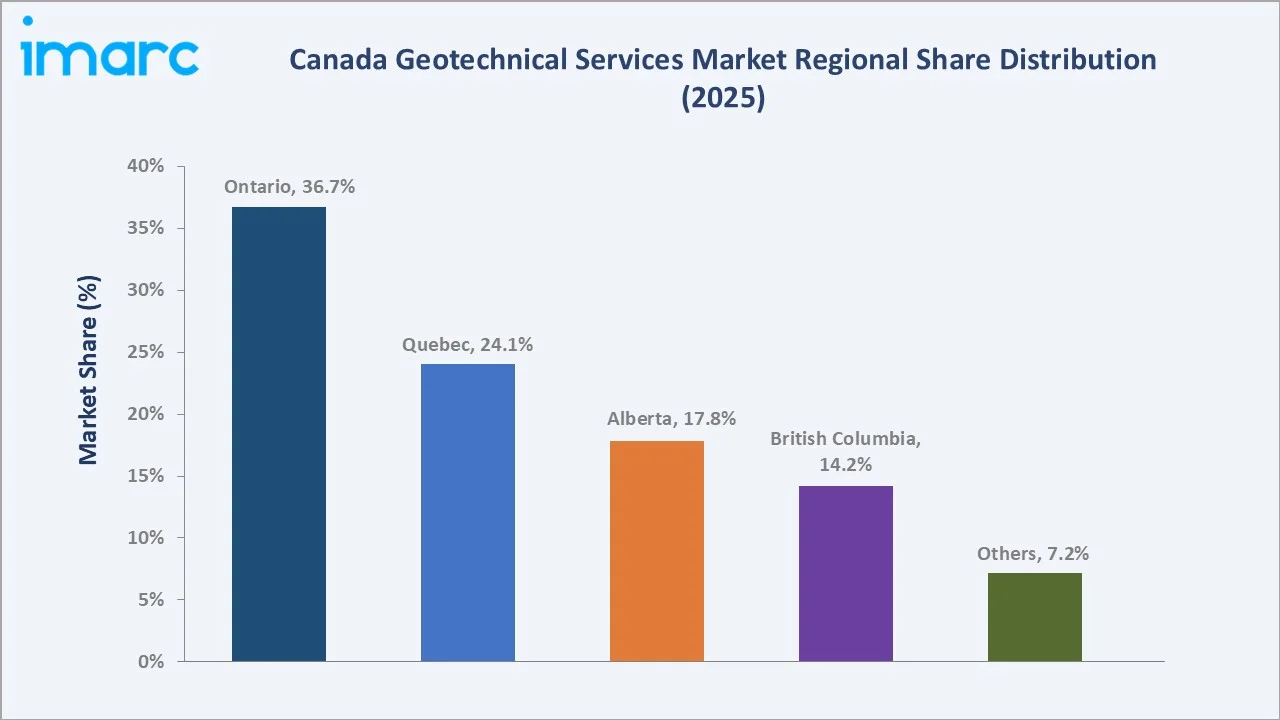

The Canada geotechnical services market reached USD 490.1 Million in 2025 and is projected to reach USD 877.2 Million by 2034, growing at a CAGR of 6.48% during 2026-2034. The market is driven by rising investments in transportation, energy, mining, commercial construction, and public infrastructure projects across the country. The Canadian government is encouraging infrastructure development through the C$15 Billion Canada Growth Fund and tax incentives for clean energy projects. Under its broader C$60 Billion investment plan through 2035, the government allocated C$10 Billion for clean power and another C$10 Billion for green infrastructure. This is driving the Canada geotechnical services market by increasing demand for site investigation, soil testing, foundation analysis, slope stability assessment, and ground improvement studies. Ground and foundation lead type at 42.8%. Building construction leads the end-user at 27.4%. Ontario leads regionally at 36.7%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 490.1 Million |

|

Forecast Market Size (2034) |

USD 877.2 Million |

|

CAGR (2026-2034) |

6.48% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Ground and Foundation (42.8%, 2025) |

|

Dominant End-User |

Building Construction (27.4%, 2025) |

|

Leading Region |

Ontario (36.7%, 2025) |

The Canada geotechnical services market expanded from USD 358.0 Million in 2020 to USD 490.1 Million in 2025, reflecting steady demand from infrastructure, mining, energy, and construction projects. The market is anchored at USD 670.9 Million by 2030, supported by rising investments in transport corridors, clean power, green infrastructure, and urban development. By 2034, the market is forecast to reach USD 877.2 Million, driven by stronger demand for site investigation, soil testing, foundation design, and slope stability assessment. Climate-resilient infrastructure planning and stricter engineering standards will further support long-term market growth.

To get more information on this market, Request Sample

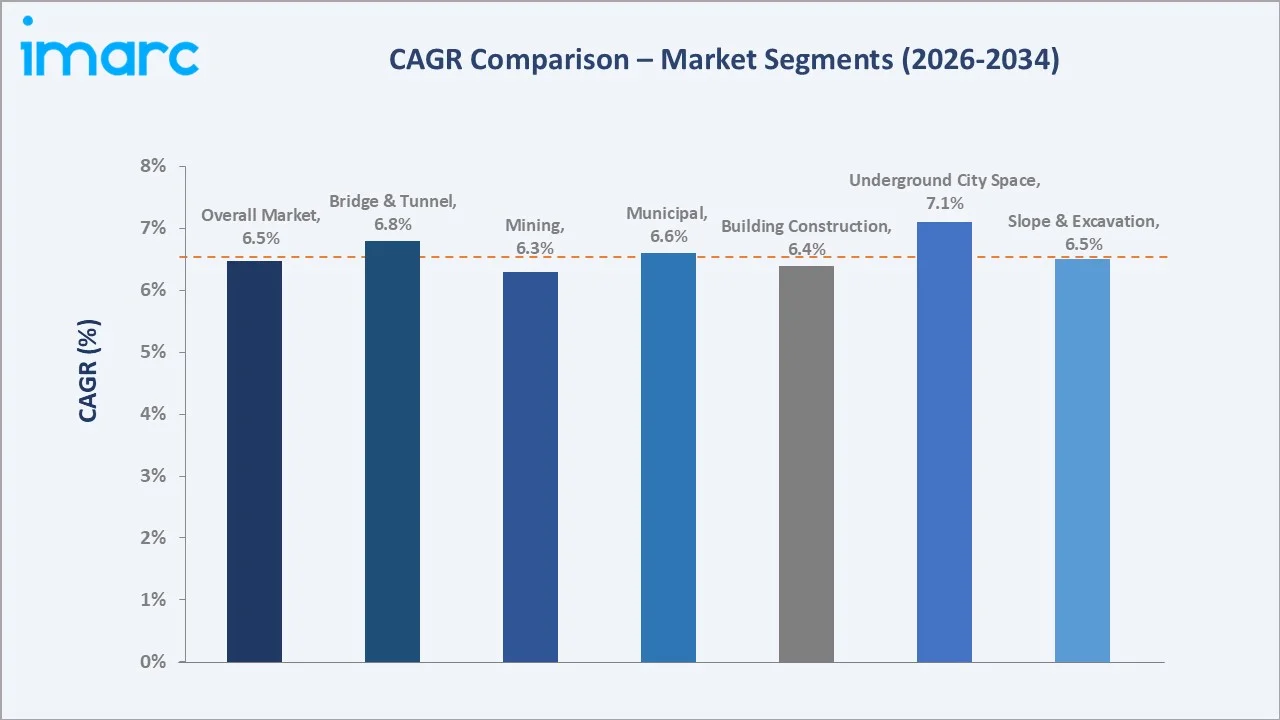

Underground city space grows fastest at ~7.1% CAGR through Ontario Line subway tunnelling, Montreal REM underground, and deep excavation projects. Bridge and tunnel end-user grows at ~6.8% CAGR through federal transit infrastructure investment and highway bridge rehabilitation programs.

Executive Summary

Canada geotechnical services market is gaining momentum as infrastructure, clean energy, mining, and urban construction projects require deeper ground-risk assessment. Demand is shifting from basic soil testing toward integrated services covering site investigation, foundation design, slope stability, seismic assessment, and climate-resilience planning. Public infrastructure funding and green project investment are creating steady opportunities for engineering consultants and testing providers. With the market forecast to reach USD 877.2 Million by 2034, advanced geotechnical analysis will remain critical to safe, durable, and sustainable project development. Ground and foundation at 42.8% leads through pile and deep foundation. Building construction at 27.4% leads through Toronto high-rise and housing. Ontario leads regionally at 36.7%.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Ground & Foundation - 42.8% share (2025) |

|

Dominant End-User |

Building Construction - 27.4% market share (2025) |

|

Leading Region |

Ontario - 36.7% share (2025) |

|

Market Opportunity |

Critical minerals mining geotechnical; permafrost engineering northern Canada; digital BIM-geotechnical integration; Ontario Line and transit geotechnical; Indigenous northern infrastructure; climate-resilient ground engineering |

Key Analytical Observations Supporting the Above Data:

- Ground and Foundation at 42.8%: Ground and foundation services lead the market as they are essential for almost every construction, infrastructure, energy, and industrial project. Soil bearing capacity, settlement risk, and foundation stability assessments are required before safe project design and execution.

- Building Construction at 27.4%: Building construction leads the market as residential, commercial, and institutional projects require soil testing, foundation design, and settlement assessment before development. Rapid urban expansion, redevelopment, and high-rise construction further support strong demand for geotechnical services.

- Ontario at 36.7%: Ontario leads regionally due to its high concentration of building construction, transportation infrastructure, and urban redevelopment projects. Strong activity across the Greater Toronto Area, highways, transit, and commercial developments drives consistent demand for soil testing, foundation design, and site investigation services.

Canada Geotechnical Services Market Overview

Canada geotechnical services market encompasses soil and rock investigation, laboratory and in-situ testing, foundation engineering, slope stability, underground excavation, ground improvement, and geoenvironmental assessment. The Canada geotechnical services market is unique because it combines strong demand from dense urban construction with complex ground conditions across mining, energy, coastal, northern, and infrastructure projects. Its growth is closely linked to climate-resilient design, clean energy development, and public infrastructure modernization. The market also requires highly specialized expertise in soil behavior, permafrost, slope stability, seismic risk, and foundation safety. Macroeconomic factors include government infrastructure spending, construction activity, mining and energy sector investments, urbanization trends, interest rates, and economic growth.

Market Dynamics

To evaluate market opportunities, Request Sample

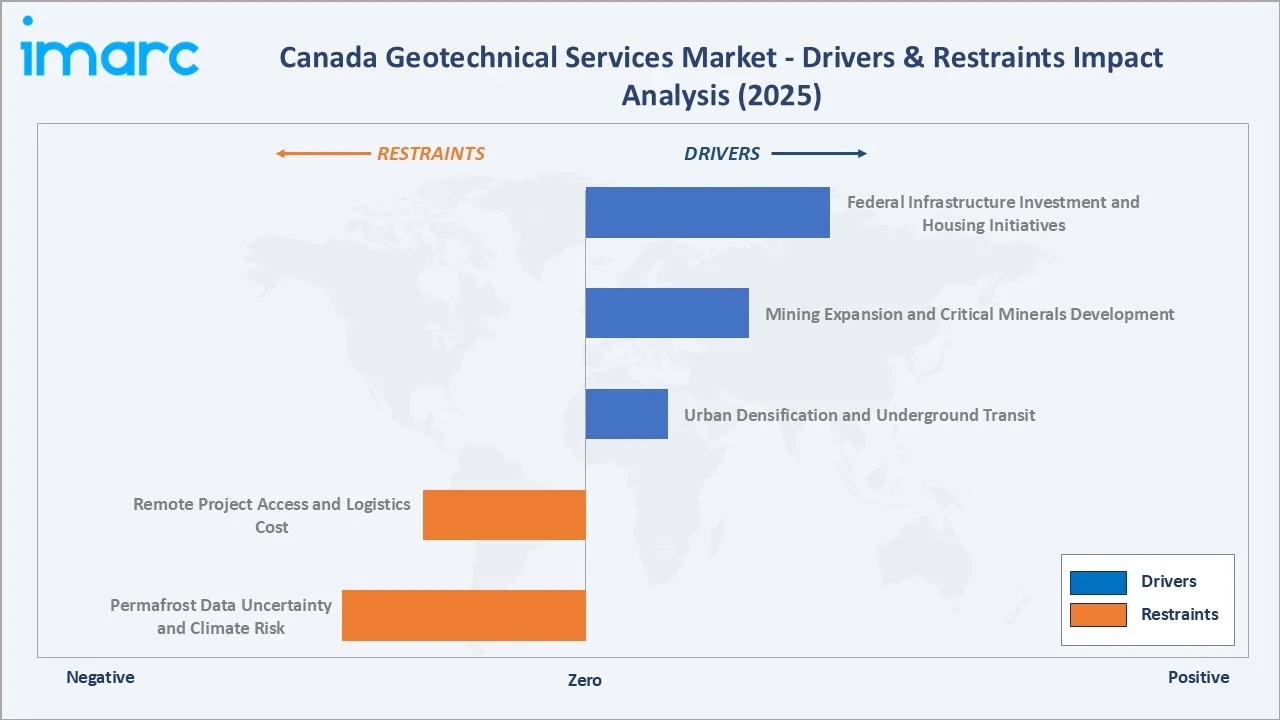

Market Drivers

- Federal Infrastructure Investment and Housing Initiatives: Federal infrastructure investment and housing initiatives are accelerating the development of transportation networks, utilities, public facilities, and residential projects. Large-scale government funding programs require extensive site investigations, soil characterization, foundation design, and geotechnical risk assessments before construction begins. The push to increase housing supply is further expanding demand for ground engineering and subsurface analysis services. In 2026–27, Build Canada Homes (BCH), a special operating agency under HICC, will continue investing, forming partnerships, and supporting housing innovation while preparing to transition into an arm’s length organization. Its initial investments will include building 4,000 homes on federal lands in Ottawa, Toronto, Winnipeg, Edmonton, Longueuil, and Dartmouth, allocating $1 billion for supportive and transitional housing, and advancing new housing partnerships, including an agreement with Nunavut for 750 homes. As infrastructure projects become larger and more complex, geotechnical expertise is becoming increasingly critical to ensure safety, regulatory compliance, and long-term asset performance.

- Mining Expansion and Critical Minerals Development: Canada produced 60 minerals and metals across nearly 200 mines and about 6,500 sand, gravel, and stone quarries. In 2024, the country’s total mineral production value reached C$64.3 Billion. This mining expansion and critical minerals development are increasing exploration and mine development activities across provinces rich in lithium, nickel, copper, cobalt, and rare earth elements. Geotechnical investigations are essential for mine site selection, tailings storage facilities, slope stability analysis, underground excavation design, and infrastructure construction. As mining projects move into remote and geologically complex regions, the need for advanced geotechnical assessment and risk management continues to rise.

- Urban Densification and Underground Transit: Urban densification and underground transit development are increasing the complexity of construction in densely populated cities. Projects such as subway extensions, underground stations, tunnels, utility corridors, and high-rise developments require extensive geotechnical investigations to assess soil conditions, groundwater behavior, and excavation risks. As major urban centers like Toronto, Vancouver, and Montréal expand their transit networks, demand for foundation engineering, tunnel geotechnics, and ground stabilization services continues to grow. These projects rely heavily on geotechnical expertise to ensure safety, minimize settlement impacts, and support long-term infrastructure performance.

Market Restraints

- Remote Project Access and Logistics Cost: Remote project access and logistics costs hamper the market because many mining, energy, and infrastructure projects are located in remote northern and resource-rich regions. Transporting drilling rigs, testing equipment, materials, and specialized personnel to these sites increases project costs and extends mobilization timelines. Harsh weather conditions, limited road networks, and seasonal access constraints can further delay field investigations and data collection. These logistical complexities reduce operational efficiency and place pressure on project budgets, particularly for smaller-scale developments.

- Permafrost Data Uncertainty and Climate Risk: Permafrost data uncertainty and climate risk make subsurface conditions harder to predict in northern and cold-region projects. Thawing permafrost can alter soil strength, settlement behavior, groundwater movement, and slope stability, increasing design complexity. Limited long-term ground temperature and permafrost monitoring data can create uncertainty during feasibility and foundation planning. As climate change accelerates freeze-thaw cycles and ground instability, geotechnical firms face higher investigation costs, longer study timelines, and greater liability risks.

Market Opportunities

- Advanced Geotechnical Data Analytics and AI-Based Modeling: Advanced geotechnical data analytics and AI-based modeling improve the accuracy and efficiency of subsurface investigations. AI-driven models can analyze large volumes of geological, geophysical, and historical site data to predict soil behavior, settlement risks, and slope stability more effectively. These technologies help reduce project uncertainty, optimize foundation designs, and accelerate decision-making for infrastructure, mining, and energy projects. As Canada undertakes increasingly complex developments in urban and remote regions, demand for data-driven geotechnical solutions is expected to grow significantly.

- Building Information Modeling (BIM) Integration in Geotechnical Engineering: Building Information Modeling (BIM) integration in geotechnical engineering enables better coordination between subsurface investigations and project design teams. BIM platforms allow geotechnical data, soil models, foundation designs, and geological risks to be incorporated into a unified digital project environment. This improves design accuracy, reduces construction conflicts, and supports more efficient project planning and cost management. As Canada increases investment in large-scale infrastructure, transit, and building projects, demand for BIM-enabled geotechnical services is expected to grow rapidly.

Market Challenges

- Liability and Risk Exposure from Ground Failure Events: Liability and risk exposure from ground failure events is a major challenge, as errors in subsurface investigation, soil interpretation, or foundation recommendations can lead to costly structural damage, delays, or safety incidents. Ground failures such as settlement, slope collapse, landslides, or retaining wall failures can create legal claims and reputational risks for consultants. This increases the need for detailed testing, conservative design, documentation, and professional insurance coverage. As projects become larger and more complex, liability exposure raises operating costs and risk management pressure for geotechnical firms.

- Weather-Related Disruptions to Field Investigation Activities: Weather-related disruptions to field investigation activities are challenging as drilling, sampling, in-situ testing, and site inspections are highly dependent on safe field conditions. Heavy snowfall, extreme cold, flooding, storms, and freeze-thaw cycles can delay equipment mobilization and restrict site access. These interruptions extend project timelines, raise labor and equipment costs, and create scheduling uncertainty for construction and infrastructure projects. In remote and northern regions, short seasonal work windows further intensify the impact of weather-related delays.

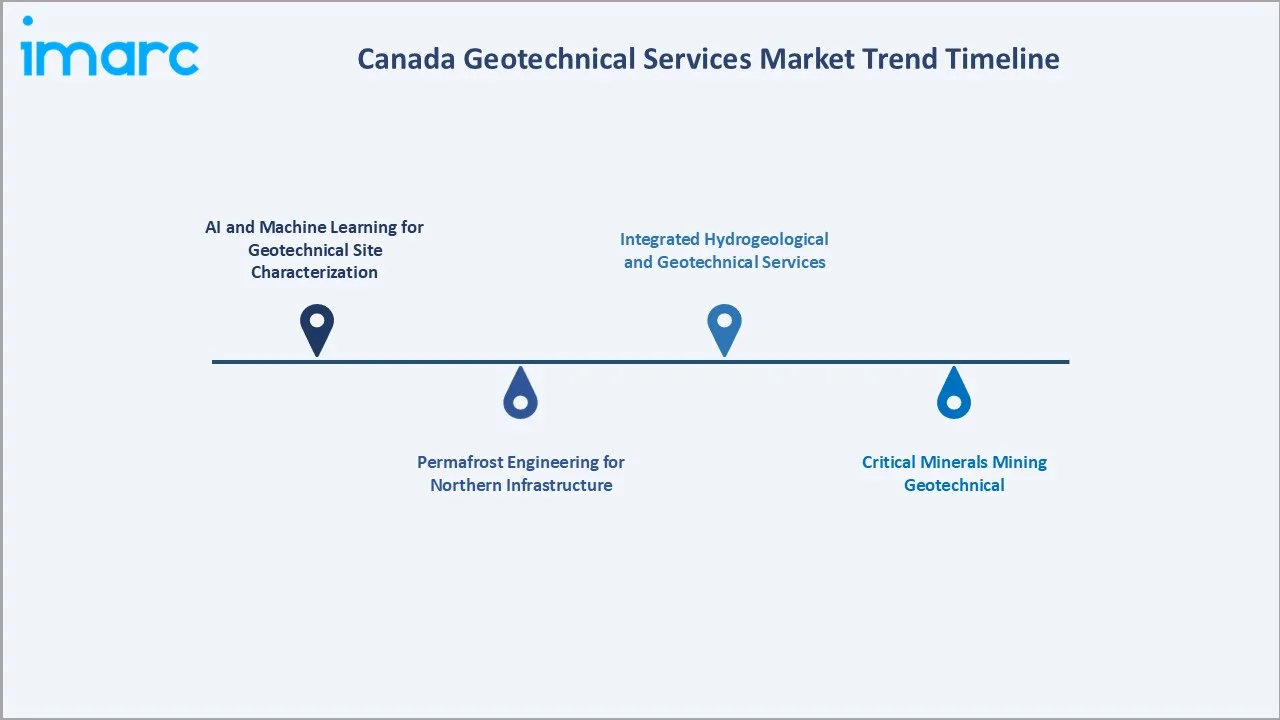

Emerging Market Trends

1. AI and Machine Learning for Geotechnical Site Characterization

AI and machine learning for geotechnical site characterization are emerging as firms use data-driven tools to interpret borehole logs, lab results, geophysical data, and historical ground records more efficiently. These technologies help predict soil behavior, groundwater conditions, settlement risks, and slope instability with greater accuracy. AI-based models can reduce uncertainty in complex projects such as tunnels, high-rise foundations, mines, and northern infrastructure. This trend supports faster decision-making, better risk management, and more cost-effective geotechnical design.

2. Permafrost Engineering for Northern Infrastructure

Permafrost engineering for northern infrastructure is emerging as warming temperatures increase ground instability in Arctic and sub-Arctic regions. Roads, airports, pipelines, mines, housing, and community infrastructure in northern areas require specialized assessment of frozen soil behavior, thaw settlement, and foundation performance. This is creating demand for thermal modeling, ground temperature monitoring, insulated foundation systems, and climate-adaptive design solutions. As northern development and critical mineral projects expand, permafrost-focused geotechnical expertise is becoming increasingly important.

3. Critical Minerals Mining Geotechnical

Critical minerals mining geotechnical is emerging as lithium, nickel, copper, cobalt, graphite, and rare earth projects expand to support clean energy and battery supply chains. These projects require specialized geotechnical work for open pits, underground workings, tailings facilities, haul roads, processing plants, and mine infrastructure. Complex geology, remote locations, and strict safety requirements are increasing the demand for advanced slope stability, rock mechanics, and ground-control studies. As Canada prioritizes critical minerals development, mining-focused geotechnical services are becoming a high-growth specialization.

4. Integrated Hydrogeological and Geotechnical Services

Integrated hydrogeological and geotechnical services are emerging as infrastructure, mining, and urban projects increasingly require a combined assessment of soil, rock, and groundwater conditions. In January 2026, Vista Clara Inc. launched Vista Clara Geotech Ltd., a new Canadian company based in Surrey, British Columbia. The company will manufacture NMR instruments for geoscience applications and offer sales, rentals, and customer support in Canada and international markets. Vista Clara focuses exclusively on NMR technology, developing and manufacturing advanced magnetic resonance tools that measure key hydrogeological properties controlling where groundwater is located and how it moves through the subsurface. By integrating hydrogeology with geotechnical engineering, firms can provide more accurate risk assessments and cost-effective design solutions. This trend is especially important for tunnels, mines, dams, landfills, coastal projects, and climate-resilient infrastructure development.

Industry Value Chain Analysis

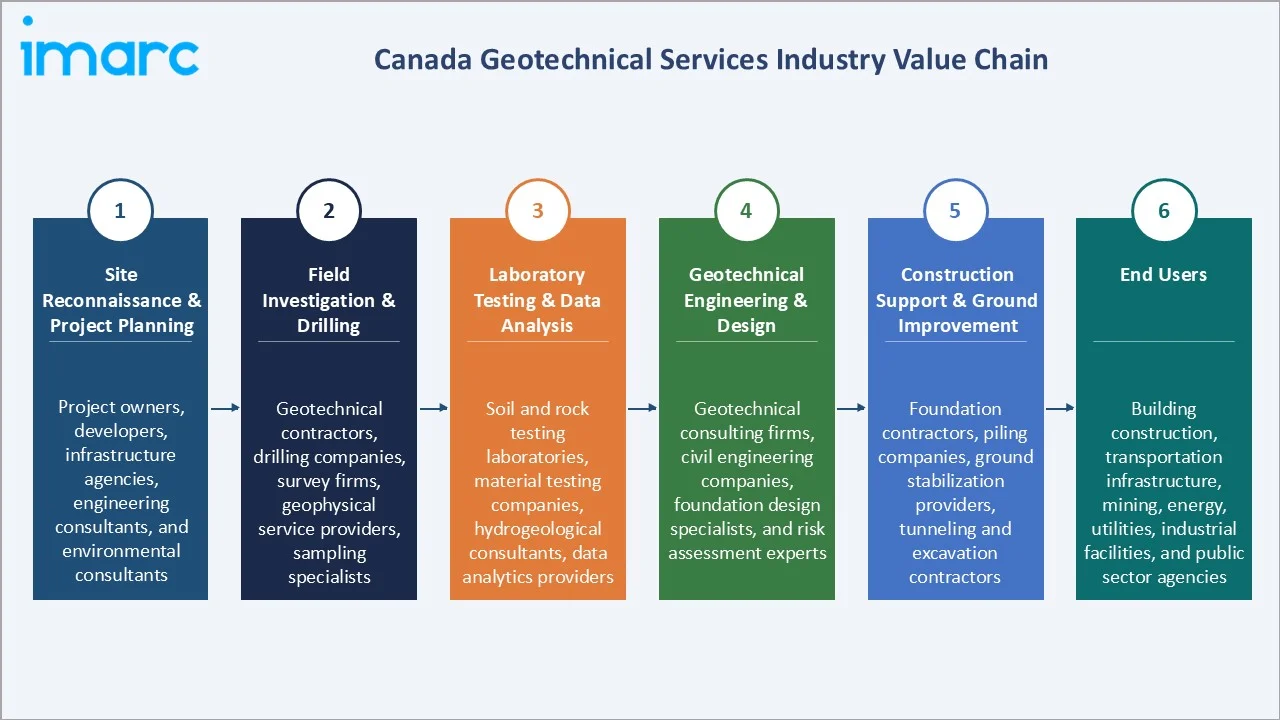

Canada geotechnical services value chain integrates site reconnaissance & project planning, field investigation & drilling, laboratory testing & data analysis, geotechnical engineering & design, construction support & ground improvement, and end-users.

|

Stage |

Key Participants |

|

Site Reconnaissance & Project Planning |

Project owners, developers, infrastructure agencies, engineering consultants, and environmental consultants |

|

Field Investigation & Drilling |

Geotechnical contractors, drilling companies, survey firms, geophysical service providers, sampling specialists |

|

Laboratory Testing & Data Analysis |

Soil and rock testing laboratories, material testing companies, hydrogeological consultants, data analytics providers |

|

Geotechnical Engineering & Design |

Geotechnical consulting firms, civil engineering companies, foundation design specialists, and risk assessment experts |

|

Construction Support & Ground Improvement |

Foundation contractors, piling companies, ground stabilization providers, tunneling and excavation contractors |

|

End-Users |

Building construction, transportation infrastructure, mining, energy, utilities, industrial facilities, and public sector agencies |

The geotechnical engineering & design stage is the most value-added segment in the Canada geotechnical services value chain. This stage transforms raw field and laboratory data into actionable engineering recommendations, including foundation design, slope stability analysis, excavation support systems, and geotechnical risk assessments. It requires highly specialized expertise, advanced modeling tools, and regulatory compliance capabilities, enabling firms to command premium margins.

Technology Landscape in the Canada Geotechnical Services Industry

Remote Sensing, LiDAR, and Drone Survey Technologies

Remote sensing, LiDAR, and drone survey technologies are enabling faster, safer, and more detailed site investigations. These tools generate high-resolution topographic maps, terrain models, and surface condition data across large or difficult-to-access areas, including mines, forests, mountains, and northern regions. They improve the identification of geohazards such as landslides, erosion, and slope instability while reducing field survey time and costs. As infrastructure, mining, and environmental projects become more complex, geotechnical firms are increasingly integrating drone and LiDAR data into 3D modeling, risk assessment, and project planning workflows.

Permafrost Monitoring and Thermal Modeling Technologies

Permafrost monitoring and thermal modeling technologies enable more accurate assessment of frozen ground conditions in northern regions. Advanced sensors, remote monitoring systems, and thermal simulation software help engineers track ground temperature changes, predict thaw settlement, and evaluate long-term foundation performance. These technologies are becoming essential for roads, airports, pipelines, mining facilities, and community infrastructure located in Arctic and sub-Arctic environments. As climate change accelerates permafrost degradation, demand for data-driven thermal modeling and continuous monitoring solutions is increasing across geotechnical projects.

Tunnel and Underground Construction Monitoring Technologies

Advanced instrumentation, such as inclinometers, extensometers, settlement sensors, fiber-optic monitoring systems, and real-time data platforms, enables continuous tracking of ground movement, tunnel deformation, and structural performance. These technologies help reduce construction risks, improve worker safety, and detect potential failures before they become critical. As subway expansions, underground utilities, and tunneling projects grow across Canadian cities, demand for sophisticated monitoring and predictive geotechnical solutions is rising rapidly.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Ground and Foundation |

42.8% |

2025 |

|

End-User |

Building Construction |

27.4% |

2025 |

|

Region |

Ontario |

36.7% |

2025 |

By Type

Ground and foundation leads at 42.8% (2025), through pile foundation design, deep caisson design, soil investigation for building construction, and ground improvement.

To access detailed market analysis, Request Sample

Slope and excavation at 33.6% reflects tieback and soldier pile shoring for deep excavation, slope stability analysis for river valley and mining, and retaining wall design. Underground city space at 23.6% grows fastest at ~7.1% CAGR.

By End-User

Building construction leads at 27.4% (2025), through Toronto high-rise pile foundation, Canada Housing Plan site investigation, and commercial and institutional building geotechnical services. Municipal at 21.8% reflects water main and sewer renewal, road and pavement subgrade investigation, and municipal bridge geotechnical.

Mining at 16.3% reflects open-pit slope stability, tailings dam safety review, and underground mine geotechnical for critical minerals. The bridge and tunnel at 13.5% grows at ~6.8% CAGR through federal transit tunnel and highway bridge rehabilitation. Oil and gas at 10.2% reflects the oil sands tailings dam and wellpad geotechnical. Marine at 6.4% reflects port expansion and offshore foundation geotechnical.

Regional Market Insights

|

Region |

Share (2025) |

Key Canada Geotechnical Services Market Drivers & Characteristics |

|

Ontario |

36.7% |

Reflects its concentration of residential and commercial construction, major transit expansions, highway upgrades, and urban redevelopment projects. |

|

Quebec |

24.1% |

Supported by public infrastructure investments, hydroelectric developments, transportation projects, and extensive underground construction activities. |

|

Alberta |

17.8% |

Reflects strong activity in energy, industrial, mining, and transportation sectors. |

|

British Columbia |

14.2% |

Driven by urban construction, port infrastructure, transportation corridors, and geohazard management requirements. |

|

Others |

7.2% |

Other provinces and territories contribute through mining projects, northern infrastructure development, municipal construction, environmental remediation, and resource-sector investments. |

Ontario's 36.7% supported by dense building construction, major transit programs, highway upgrades, and redevelopment activity across the Greater Toronto Area. Quebec's 24.1% with strong demand from public infrastructure, hydroelectric projects, underground works, and urban mobility investments.

Alberta's 17.8% driven by energy, mining, industrial facilities, pipelines, and renewable infrastructure projects. British Columbia's 14.2% benefits from port development, seismic design requirements, mountainous terrain, and geohazard management needs. Others at 7.2% contribute through critical minerals projects, northern infrastructure, municipal works, environmental remediation, and resource-sector developments.

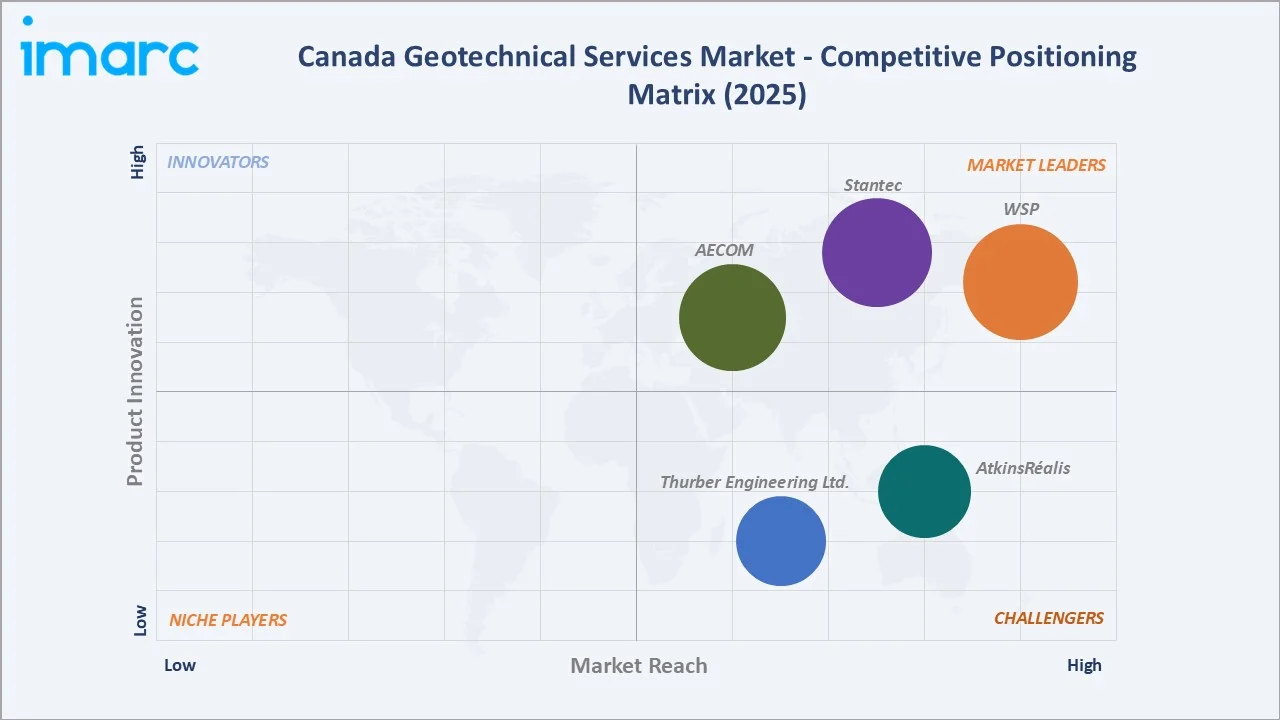

Competitive Landscape

The Canada geotechnical services market is moderately concentrated, with a mix of large multidisciplinary engineering firms and specialized geotechnical consultancies competing across infrastructure, mining, energy, and construction projects. Leading participants focus on expanding their capabilities in digital ground monitoring, geotechnical modeling, hydrogeology, and environmental services to differentiate their offerings. Competition is driven by technical expertise, project experience, regulatory compliance, and the ability to deliver integrated engineering solutions.

|

Company |

Key Services |

Market Position |

Core Strength |

|

WSP |

Geotechnical and Ground Engineering |

Market Leader |

In Canada, WSP provides end-to-end Geotechnical and Ground Engineering services. Its role spans from initial site investigations and subsurface characterization to foundation design, construction support, and rehabilitation. |

|

Stantec |

Geotechnical Engineering & Materials Testing |

Market Leader |

Stantec plays a critical role in Canada’s geotechnical sector by providing multidisciplinary engineering, design, and materials testing for infrastructure, mining, water, and energy projects. |

|

AECOM |

Geotechnical Services |

Market Leader |

AECOM delivers comprehensive Geotechnical Services across Canada, encompassing site investigations, numerical modeling, and construction oversight for major civil, industrial, and infrastructure projects. |

|

AtkinsRéalis |

Geotechnical Engineering |

Strong Challenger |

AtkinsRéalis plays a vital role in Canadian Geotechnical engineering by delivering complex site investigations, numerical modeling, and foundation designs for major infrastructure, transit, and energy projects across the country. |

|

Thurber Engineering Ltd. |

Geotechnical Site Investigations, Soft Ground Engineering, Retaining Structures, Foundation Engineering, Horizontal Directional Drilling Design, Tunnelling and Trenchless Technology |

Strong Challenger |

Thurber Engineering Ltd. is a Canadian-owned consulting firm that plays a critical role in geotechnical engineering. It provides specialist advice where infrastructure meets the ground, mitigating geohazards and supporting sustainable development across the country |

Firms are increasingly investing in AI-enabled data analytics, remote sensing, BIM integration, and real-time monitoring technologies to improve project outcomes. Strategic acquisitions, regional expansion, and partnerships with infrastructure and mining developers remain common approaches to strengthen market presence and secure long-term contracts.

Key Company Profiles

WSP

WSP is one of Canada's largest engineering and professional services firms, providing comprehensive geotechnical, geological, hydrogeological, environmental, and infrastructure consulting services across the country. The company supports major transportation, building construction, mining, energy, water, and urban development projects through site investigation, foundation engineering, ground improvement, slope stability, and geohazard assessment services.

- Key Services: Geotechnical and Ground Engineering.

- Strategic Focus: Centers on providing integrated geotechnical, hydrogeological, environmental, and infrastructure solutions for large-scale transportation, building, mining, energy, and water projects.

Stantec

Stantec is one of the leading Canadian engineering, consulting, and design firms with extensive capabilities in geotechnical engineering, hydrogeology, environmental services, and infrastructure development. The company provides site investigation, foundation engineering, slope stability analysis, earthworks design, geohazard assessment, and construction-phase geotechnical support for projects across transportation, buildings, water, energy, and mining sectors.

- Key Services: Geotechnical Engineering & Materials Testing.

- Recent Developments: In March 2026, Stantec secured a contract to deliver engineering and design services for Canada’s Arctic Over-the-Horizon Radar project. Defence Construction Canada selected Stantec and its consortium partners for the long-range early-warning radar system in northern Canada, with Stantec handling multidisciplinary project management and design, while Aecon and Pomerleau will jointly provide construction services.

- Strategic Focus: Centered on delivering integrated geotechnical, hydrogeological, environmental, and infrastructure consulting solutions for transportation, buildings, water, energy, and mining projects.

Market Concentration Analysis

The Canada geotechnical services market is moderately concentrated, with a group of large engineering and consulting firms such as WSP, Stantec, AECOM, AtkinsRéalis, and Thurber Engineering Ltd. holding significant market shares through their nationwide presence and multidisciplinary capabilities. These firms compete alongside regional geotechnical specialists that focus on local infrastructure, mining, and environmental projects. Market competition is driven by technical expertise, project execution capabilities, regulatory compliance, and access to advanced investigation and monitoring technologies. Larger players benefit from integrated service offerings covering geotechnical, environmental, hydrogeological, and structural engineering disciplines. Ongoing investments in digital modeling, AI-based analytics, remote sensing, and real-time monitoring technologies are further strengthening the competitive positions of leading firms.

Investment & Growth Opportunities

Highest Growth Segments

Underground city space (~7.1% CAGR), bridge and tunnel (~6.8% CAGR), municipal (~6.6% CAGR), critical minerals mining (~7-8% CAGR), permafrost geotechnical (~8-10% CAGR Northern Canada), and digital BIM-geotechnical (~10-12% CAGR from emerging segment) represent Canada geotechnical highest-growth investment vectors through 2034.

Investment Themes

- Digital BIM-geotechnical Integration: Digital BIM-geotechnical integration is an attractive investment theme as infrastructure owners increasingly require geotechnical data to be incorporated into unified digital project models. Investments in BIM-enabled subsurface modeling, digital twins, and geotechnical data platforms can improve design coordination, reduce construction risks, and enhance lifecycle asset management, creating strong demand for advanced engineering solutions.

- Critical Minerals Mining Geotechnical Services: Critical minerals mining geotechnical services represent a high-growth investment opportunity driven by Canada's expanding lithium, nickel, copper, cobalt, graphite, and rare earth development projects. Rising exploration and mine construction activity is increasing demand for specialized geotechnical investigations, slope stability analysis, tailings facility design, and ground-control engineering, supporting long-term growth in mining-focused consulting services.

Future Market Outlook (2026-2034)

Canada geotechnical services market is projected to grow from USD 490.1 Million in 2025 to USD 877.2 Million by 2034, delivering a 6.48% CAGR over the forecast period through federal infrastructure investment, urban transit tunnelling expansion, critical minerals mining boom, climate-driven permafrost geotechnical demand, and digital BIM-geotechnical transformation. The market's anchor value of USD 670.9 Million in 2030 represents Canada's geotechnical infrastructure and digital inflection.

Three structural forces define Canada geotechnical services market growth through 2034. First, sustained federal and provincial investments in transportation networks, housing, utilities, and public infrastructure are generating long-term demand for site investigation, foundation engineering, and geotechnical consulting services. Second, the expansion of critical minerals mining and energy-transition projects is increasing the requirements for specialized geotechnical, hydrogeological, and ground stability assessments. Third, climate resilience priorities, including permafrost degradation, flooding risks, landslide hazards, and extreme weather adaptation, are driving greater adoption of advanced geotechnical analysis, monitoring technologies, and risk-management solutions across infrastructure and resource developments.

Research Methodology

Primary Research

Primary research comprised in-depth interviews and discussions with geotechnical consultants, engineering firms, drilling contractors, laboratory testing providers, infrastructure developers, mining companies, and government agencies across Canada. Insights gathered from industry participants were used to validate market sizing, technology adoption trends, project activity levels, competitive dynamics, and future demand outlook.

Secondary Research

Secondary research encompassed company reports, government infrastructure plans, mining and construction databases, industry publications, regulatory documents, and trade association sources. It also included a review of public project pipelines, procurement updates, technology trends, and competitive information across Canada’s geotechnical services industry.

Forecasting Models

Forecasting models combined historical market trends, infrastructure investment pipelines, mining project developments, construction activity indicators, and engineering services demand patterns to estimate future market growth. A blended approach incorporating time-series analysis, bottom-up project assessment, and macroeconomic forecasting was used to develop market projections. Forecast assumptions were validated through primary industry consultations and cross-referenced with government spending plans, critical minerals investments, and regional construction outlooks.

Canada Geotechnical Services Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Underground City Space, Slope and Excavation, Ground and Foundation |

| End-Users Covered | Municipal, Bridge and Tunnel, Oil and Gas, Mining, Marine, Building Construction, Others |

| Regions Covered | Ontario, Quebec, Alberta, British Columbia, Others |

| Companies Covered | WSP, Stantec, AECOM, AtkinsRéalis, Thurber Engineering Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Canada geotechnical services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Canada geotechnical services market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Canada geotechnical services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Canada Geotechnical Services Market Report

The Canada geotechnical services market reached USD 490.1 Million in 2025, driven by strong investment in transportation, housing, utilities, mining, clean energy, and public infrastructure projects. Rising critical minerals development, urban densification, underground transit expansion, and climate-resilient infrastructure planning are increasing demand for site investigation, soil testing, foundation design, slope stability, and geohazard assessment.

The Canada geotechnical services market grows at 6.48% CAGR during 2026-2034, reaching USD 877.2 Million by 2034. The CAGR reflects investing in the Canada Housing Plan, critical minerals mining, permafrost geotechnical, and digital BIM-geotechnical.

Ground and foundation leads at 42.8% as they are essential for almost every building, infrastructure, mining, and energy project. Foundation design, soil bearing analysis, settlement assessment, and ground stability checks are required before construction can safely begin.

Building construction leads at 27.4% due to sustained demand for residential, commercial, institutional, and mixed-use developments across major urban centers. Every construction project requires geotechnical investigations, foundation design, excavation support, and ground stability assessments to ensure safe and compliant development.

Ontario leads at 36.7% due to strong activity in building construction, transit expansion, highways, utilities, and urban redevelopment. The Greater Toronto Area’s large project pipeline drives steady demand for site investigation, foundation design, and geotechnical consulting.

Leading companies include WSP, Stantec, AECOM, AtkinsRéalis, and Thurber Engineering Ltd., among others.

The market is projected to reach approximately USD 670.9 Million by 2030, supported by infrastructure expansion, housing development, and critical minerals projects. Growth will also be driven by demand for foundation engineering, site investigation, climate resilience, and advanced geotechnical monitoring solutions.

Three priority investment opportunities stand out in the Canada geotechnical services market. First, digital BIM-geotechnical integration and digital twin platforms offer strong growth potential as infrastructure projects increasingly require connected subsurface data and lifecycle asset management. Second, critical minerals mining geotechnical services present significant opportunities due to expanding lithium, nickel, copper, and rare earth developments across Canada. Third, climate-resilience and permafrost engineering solutions are attracting investment as governments and project developers seek to mitigate risks associated with thawing permafrost, flooding, landslides, and extreme weather events.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)