Cancer Diagnostics Market Report by Product (Consumables, Instruments), Technology (IVD Testing, Imaging, Biopsy Technique), Application (Breast Cancer, Lung Cancer, Colorectal Cancer, Melanoma, and Others), End User (Hospitals and Clinics, Diagnostic Laboratories, and Others), and Region 2026-2034

Market Overview:

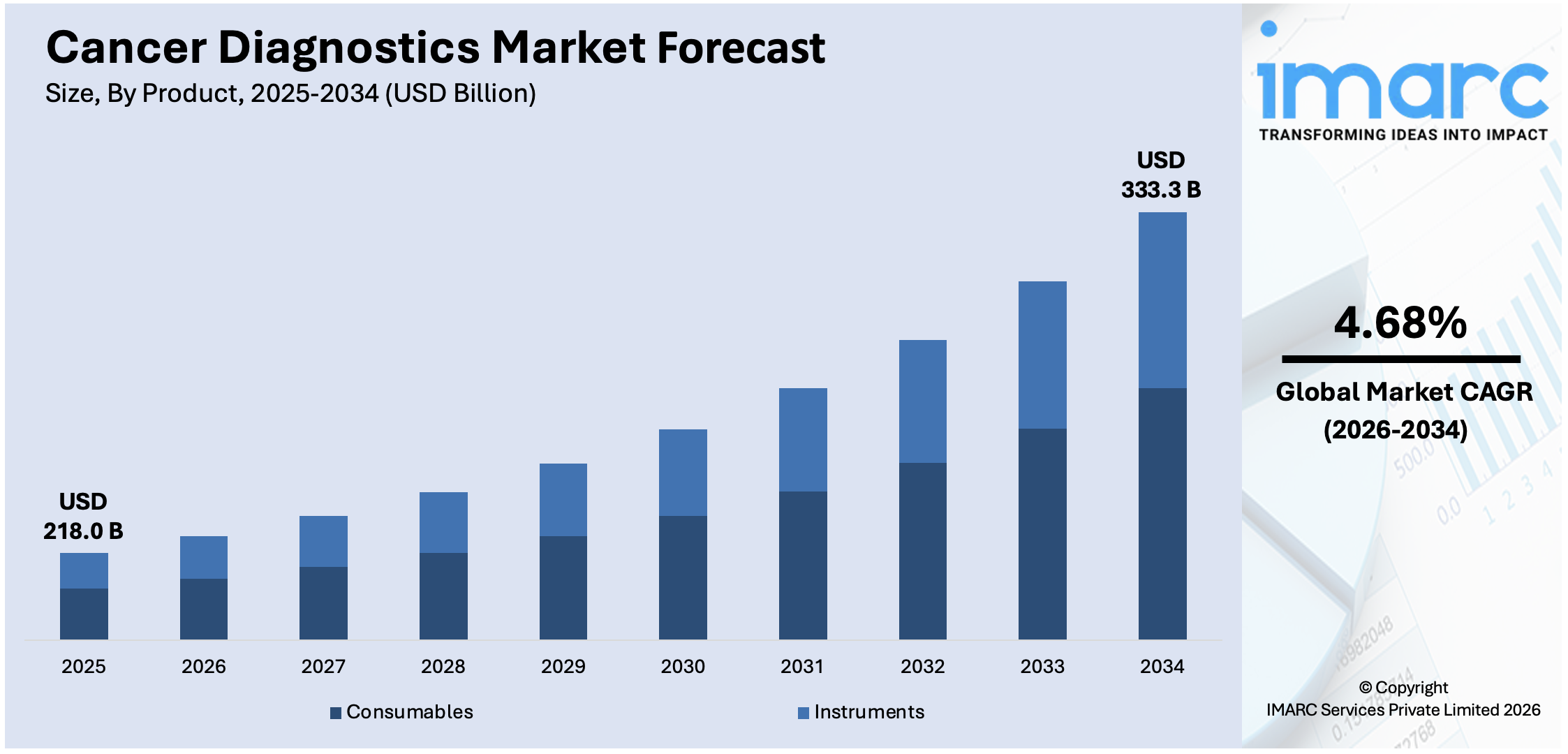

The global cancer diagnostics market size reached USD 218.0 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 333.3 Billion by 2034, exhibiting a growth rate (CAGR) of 4.68% during 2026-2034. North America leads the cancer diagnostics market owing to advanced healthcare infrastructure, high research investment, widespread technology adoption, and strong regulatory support. The growing awareness about early detection of disease, rising prevalence of cancer due to lifestyle changes and genetic predisposition, and advancements in diagnostics techniques to enhance patient care are some of the major factors propelling the market.

Market Size & Forecasts:

- Cancer diagnostics market was valued at USD 218.0 Billion in 2025.

- The market is projected to reach USD 333.3 Billion by 2034, at a CAGR of 4.68% from 2026-2034.

Dominant Segments:

- Products: Consumables (antibodies, kits and reagents, probes, and others) are essential elements that aid in performing cancer diagnostic tests. They guarantee the precision and uniformity of outcomes via their unique chemical and biological characteristics. Instruments (pathology-based instruments, imaging instruments, and biopsy instruments) are advanced tools that allow for the identification and examination of cancer at different stages. They offer exact and comprehensive insights essential for correct diagnosis and treatment strategy.

- Technology: Imaging [magnetic resonance imaging {MRI}, computed tomography {CT}, positron emission tomography {PET}, mammography, and ultrasound] leads the cancer diagnostics market, as it offers detailed, non-invasive views of tumors. It enables early identification, correct diagnosis, and careful tracking of disease advancement, improving clinical decision-making and enhancing patient care, thus promoting extensive adoption and market expansion.

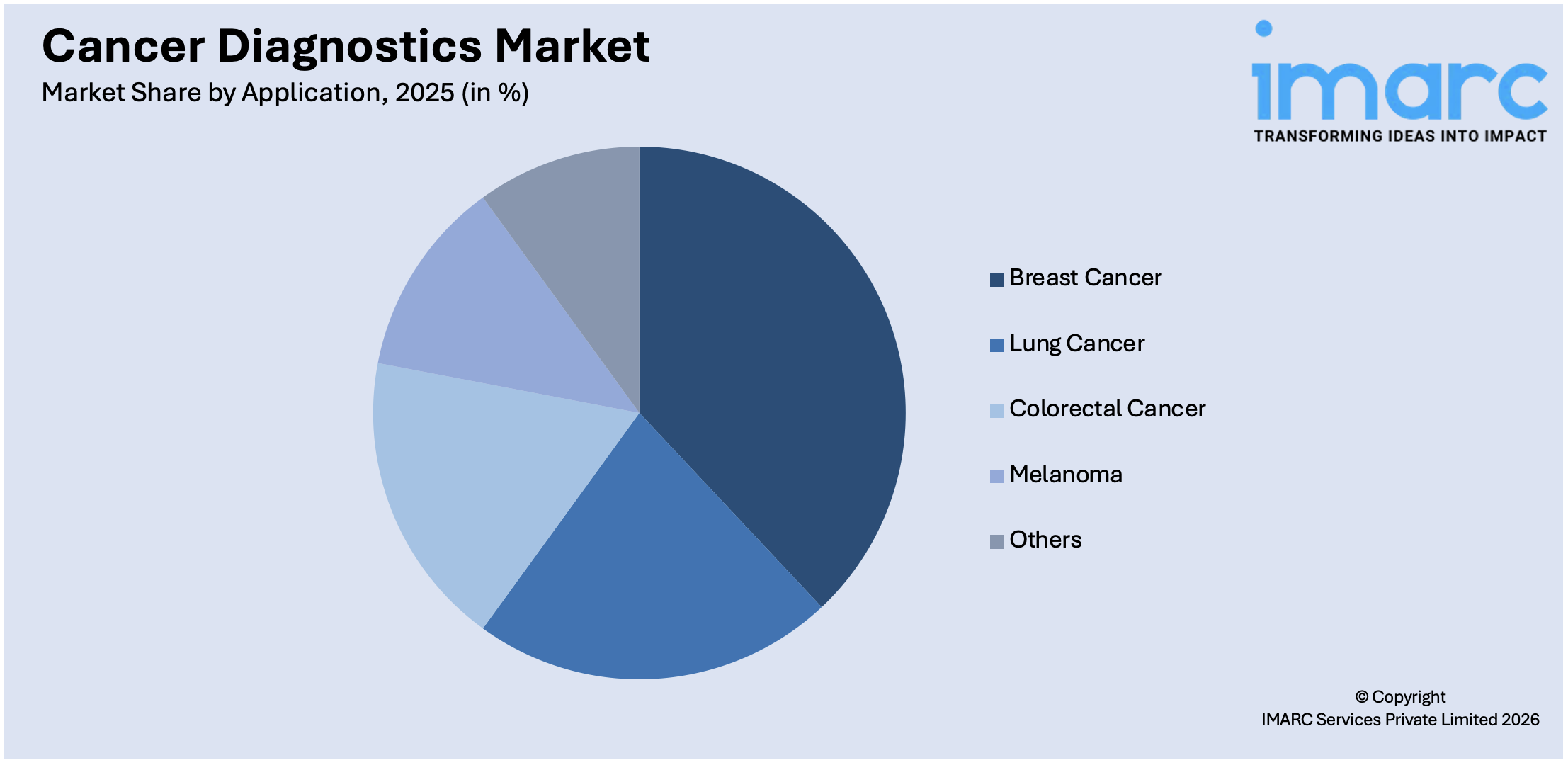

- Application: Breast cancer accounts for the largest market share because of its widespread occurrence and the essential requirement for early identification. Sophisticated diagnostic techniques facilitate precise detection and observation, aiding in efficient treatment approaches. This emphasis improves patient results and stimulates significant investment in diagnostic technologies for this purpose.

- End User: Hospitals and clinics represent the largest segment owing to their wide patient access, sophisticated diagnostic technologies, and capacity to deliver all-encompassing care. Their developed healthcare systems and ongoing investment in advanced technologies facilitate prompt and effective cancer identification, fostering considerable market demand.

- Region: North America leads the cancer diagnostics market attributed to its sophisticated healthcare system, robust research and development (R&D) resources, significant healthcare spending, and widespread use of cutting-edge diagnostic technologies. The area also gains from favorable regulatory structures and a well-established network of healthcare providers and facilities.

Key Players:

- The leading companies in cancer diagnostics market include Abbott Laboratories, Agilent Technologies, Inc., Becton, Dickinson and Company, bioMérieux, Bio-Rad Laboratories, Inc., F. Hoffmann-La Roche Ltd, GE HealthCare, Hologic, Inc., Illumina, Inc., Koninklijke Philips N.V., Qiagen N.V., Quest Diagnostics, Siemens Healthineers AG (Siemens AG), and Thermo Fisher Scientific Inc.

Key Drivers of Market Growth:

- Integration of Artificial intelligence (AI): The integration of artificial intelligence (AI) and digital platforms is revolutionizing cancer diagnostics through enhanced precision, faster analysis, and facilitating real-time monitoring. These technologies simplify data analysis, minimize human mistakes, and aid in clinical decision-making, greatly improving diagnostic efficiency and patient care results.

- Demand for Minimally Invasive Diagnostic Procedures: The increasing preference for minimally invasive techniques is bolstering the market growth by providing benefits like decreased patient discomfort, lower risk of complications, and faster recovery times. These methods improve diagnostic accuracy and patient satisfaction, speeding up the creation of specialized instruments that facilitate safer, more effective cancer detection.

- Rise of Mobile Diagnostic Services: Mobile diagnostic services are increasing availability of cancer screening in isolated and underserved regions. These mobile units lessen geographical obstacles, facilitating early detection and prompt care. By enhancing healthcare equality and access, they play a crucial role in localized cancer management initiatives.

- Growing Geriatric Population: Elderly people need consistent evaluations and tracking, leading healthcare systems to allocate resources for easy-to-use, accessible diagnostic solutions. This demographic shift fosters ongoing market demand and promotes innovations specifically designed for elderly care.

- Advancements in Diagnostic Tools: Ongoing advancements in diagnostic technologies, such as imaging, molecular techniques, and biomarker evaluation, are providing quicker, more precise detection and tailored treatment insights. These improvements are promoting higher utilization within healthcare systems and enhancing the diagnostic abilities crucial for effectively managing intricate cancer cases.

- Expanding Healthcare Infrastructure: Enhanced healthcare systems worldwide, particularly in developing nations, broaden access to cancer diagnostics. Increased access to advanced facilities, public health initiatives, and heightened awareness about early detection results in wider adoption of diagnostic technologies.

Future Outlook:

- Strong Growth Outlook: The cancer diagnostics market demonstrates a strong growth outlook because of continuous advancements in technology, rising need for early detection, expanding healthcare infrastructure, and increasing awareness among patients and providers. These factors collectively contribute to sustained market expansion and innovation in diagnostic solutions.

- Market Evolution: The cancer diagnostics market is evolving rapidly with the integration of advanced technologies and personalized medicine approaches. Continuous improvements in accuracy, efficiency, and accessibility are enhancing diagnostic capabilities, thereby enabling better patient outcomes and driving ongoing growth and transformation within the healthcare sector.

To get more information on this market Request Sample

With aging populations and increasing lifestyle-related risks, early identification is crucial for successful treatment, leading to investments in cutting-edge screening technologies and resources to address the growing disease burden. Moreover, advances in molecular diagnostics, imaging technologies, and biomarker identification are improving precision and rapidity in cancer detection. These advancements facilitate earlier detection, improved disease tracking, and tailored treatment strategies, enhancing the efficiency and reliability of diagnostic processes, thereby contributing to the market growth. Besides this, public health efforts and government-funded screening programs are raising awareness regarding the early detection of cancer. With an increasing number of people getting routine examinations, the need for diagnostic equipment grows. These initiatives greatly aid in early diagnosis and enhance patient survival rates, supporting the market growth.

Cancer Diagnostics Market Trends:

Integration of AI and Digital Technologies

The incorporation of AI and digital technologies into cancer diagnostics to improve functionality is bolstering the market growth. AI algorithms improve image analysis, pattern detection, and data interpretation, resulting in quicker and more precise diagnoses. Digital platforms enhance data management, enable remote diagnostics, and allow real-time monitoring, boosting efficiency and accessibility. These technologies also facilitate the integration of various data sources, including imaging and genomic data, to produce thorough diagnostic insights. The use of AI-driven tools minimizes human mistakes and assists clinicians in their decision-making, thereby enhancing the overall standard of cancer treatment. With healthcare systems progressively adopting digital transformation, the need for AI-enhanced diagnostic solutions rises, fostering additional innovation and growth in the cancer diagnostics sector. For example, in 2025 Montréal-based Avitia launched its AI-powered cancer diagnostics platform and secured a $5 million seed round backed by PacBridge Capital Partners. Built on assets from the defunct Imagia Canexia, the platform uses machine learning (ML) and next-generation sequencing for faster, cost-effective cancer detection.

Growing Demand for Minimally Invasive Diagnostic Procedures

There is an increase in shift towards minimally invasive diagnostic techniques in cancer treatment, which provide several benefits compared to conventional invasive approaches, such as minimized patient discomfort, decreased complication risks, shorter recovery times, and reduced hospital admissions. These advantages are especially crucial in oncology, where patient safety, comfort, and prompt diagnosis are vital. Minimally invasive methods usually employ sophisticated tools and imaging technologies that allow for exact localization, identification, and characterization of tumors with enhanced precision. The increasing acceptance of these procedures is backed by both healthcare professionals, who desire more effective and efficient diagnostic options, and patients, who prefer safer and less invasive approaches. This trend is speeding up the creation and market introduction of novel diagnostic tools tailored for minimally invasive uses, thus improving patient outcomes, broadening market opportunities, and strengthening the shift towards more patient-focused cancer diagnostic methods.

Rise of Mobile Diagnostic Services in Rural Areas

The growing deployment of mobile diagnostic units in rural and underserved regions is a key factor impelling the cancer diagnostics market growth. These mobile services bridge the accessibility gap by bringing essential screening tools directly to populations with limited access to fixed healthcare facilities. Equipped with latest diagnostic tools and trained medical personnel, mobile units enable early detection of various cancers, facilitating timely intervention and reducing disease burden. Their mobility allows for widespread coverage, including remote or geographically isolated areas where traditional healthcare infrastructure is often lacking. For example, in February 2025, Dhule MP Shobha Bachhav flagged off a cancer diagnostic van in Nashik to offer oral, breast, and uterine cancer screenings in rural areas. The van is equipped with medical tools, private exam areas, and staffed by a dentist and gynecologist.

Cancer Diagnostics Market Growth Drivers:

Increasing Geriatric Population

The increasing elderly population globally is a key factor bolstering the cancer diagnostics market growth. Aging is a well-established risk factor for many types of cancer, resulting in higher demand for regular diagnostic screenings and ongoing monitoring among older adults. With increasing life expectancy, more people need regular cancer screenings to guarantee early diagnosis and efficient disease control. The World Health Organization (WHO) states that by 2030, one out of every six individuals worldwide will be 60 years or older, and this figure is expected to climb to 2.1 billion by 2050. This change in demographics requires healthcare systems to allocate resources for accessible, advanced diagnostic technologies tailored to the needs of older adults. The rising focus on geriatric care support market growth by encouraging more use of diagnostic services and the creation of less invasive, easier-to-use diagnostic tools designed for this demographic.

Advancements in Diagnostic Tools

The market for cancer diagnostics is propelled by ongoing technological innovations that enhance the accuracy, speed, and dependability of diagnostic procedures. Advancements in molecular diagnostics, imaging methods, and biomarker identification facilitate more precise detection and characterization of various cancer types. These advancements improve the precision of diagnoses and enable tailored treatments by uncovering intricate genetic and molecular characteristics of tumors. Moreover, the incorporation of digital technologies and automation enhances the efficiency and availability of diagnostic services. In 2024, Roche expanded its Digital Pathology Open Environment by integrating over 20 advanced AI algorithms from eight collaborators to enhance cancer diagnosis and personalized treatment. This AI-driven platform supported pathologists with precise insights for various cancers, improving patient outcomes. Roche’s initiative aimed to advance digital pathology and bring innovative AI tools into routine clinical practice. Such innovative initiatives encourage healthcare professionals to embrace advanced diagnostic technologies, contributing to the market expansion and broadening the scope of cancer diagnostics globally.

Expanding Healthcare Infrastructure

The global expansion of healthcare infrastructure, especially in emerging economies, plays a pivotal role in strengthening the growth of the market. Enhanced access to healthcare facilities equipped with state-of-the-art diagnostic technologies allows a significantly larger patient population to benefit from timely cancer screening and accurate diagnosis. Moreover, increasing awareness regarding cancer prevention and the critical importance of early detection among the general public encourages more individuals to proactively seek diagnostic testing. This growing consciousness is further supported by extensive public health initiatives and educational campaigns aimed at promoting routine screenings and consistent follow-up care. Collectively, these developments establish a favorable environment for the widespread acceptance and integration of advanced cancer diagnostic tools. This environment not only sustains ongoing demand but also facilitates consistent market expansion, ensuring improved healthcare outcomes across various geographic regions and diverse healthcare delivery systems.

Cancer Diagnostics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global cancer diagnostics market report, along with forecasts at the global, regional and country levels from 2026-2034. Our report has categorized the market based on product, technology, application and end user.

Breakup by Product:

- Consumables

- Antibodies

- Kits and Reagents

- Probes

- Others

- Instruments

- Pathology-based Instruments

- Imaging Instruments

- Biopsy Instruments

The report has provided a detailed breakup and analysis of the market based on the product. This includes consumables (antibodies, kits and reagents, probes, and others) and instruments (pathology-based instruments, imaging instruments, and biopsy instruments).

Consumables comprise a wide range of products used in the process of cancer diagnostics. These include reagents, test kits, stains, and antibodies that are utilized in various diagnostic procedures, such as immunohistochemistry, molecular testing, and blood-based assays. In addition, consumables play a crucial role in facilitating accurate sample processing, analysis, and interpretation. The rising adoption of consumables due to the increasing demand for diagnostic testing in cancer care is bolstering the growth of the market.

Instruments refer to the equipment and devices employed to perform diagnostic tests and procedures. This category encompasses a diverse range of technologies, such as imaging equipment, laboratory equipment, and diagnostic platforms. Apart from this, there is a rise in the innovation of diagnostic instruments to improve the accuracy, speed, and efficiency of cancer diagnostics.

Breakup by Technology:

- IVD Testing

- Polymerase Chain Reaction (PCR)

- In Situ Hybridization (ISH)

- Immunohistochemistry (IHC)

- Next-generation Sequencing (NGS)

- Microarrays

- Flow Cytometry

- Immunoassays

- Others

- Imaging

- Magnetic Resonance Imaging (MRI)

- Computed Tomography (CT)

- Positron Emission Tomography (PET)

- Mammography

- Ultrasound

- Biopsy Technique

Imaging accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the technology. This includes IVD testing (polymerase chain reaction (PCR), in situ hybridization (ISH), immunohistochemistry (IHC), next-generation sequencing (NGS), microarrays, flow cytometry, immunoassays, and others), imaging (magnetic resonance imaging (MRI), computed tomography (CT), positron emission tomography (PET), mammography, and ultrasound), and biopsy technique. According to the report, imaging represented the largest segment.

Imaging technologies involve the usage of advanced medical equipment to visualize internal structures and detect abnormalities within the body. Imaging techniques, such as magnetic resonance imaging (MRI), computed tomography (CT) scans, positron emission tomography (PET) scans, and ultrasound, provide detailed images of tumors and their size, location, and potential metastases. These technologies aid in tumor detection, staging, and treatment monitoring. In line with this, they play a vital role in guiding medical decisions, enabling precise surgical interventions, and evaluating treatment responses.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Breast Cancer

- Lung Cancer

- Colorectal Cancer

- Melanoma

- Others

Breast cancer represents the largest market share

The report has provided a detailed breakup and analysis of the market based on the application. This includes breast cancer, lung cancer, colorectal cancer, melanoma, and others. According to the report, breast cancer represented the largest segment.

Breast cancer diagnostics comprise a wide range of methods for the early detection, diagnosis, and monitoring of breast tumors. Mammography is a widely used imaging technique that aids in detecting abnormalities, such as masses or microcalcifications. Besides this, biopsy procedures, such as core needle and fine-needle biopsies, provide tissue samples for pathological analysis that determine the nature and stage of the tumor. Molecular tests assess specific biomarkers like HER2/neu and estrogen receptor status. In addition, advanced imaging methods, such as breast MRI and molecular breast imaging, offer enhanced visualization and characterization of lesions.

Breakup by End User:

- Hospitals and Clinics

- Diagnostic Laboratories

- Others

Hospitals and clinics hold the biggest market share

The report has provided a detailed breakup and analysis of the market based on the end user. This includes hospitals and clinics, diagnostic laboratories, and others. According to the report, hospitals and clinics represented the largest segment.

Hospitals serve as comprehensive healthcare institutions that are equipped with advanced diagnostic equipment and expert medical personnel. They offer a wide range of cancer diagnostic services and provide comprehensive treatment planning based on diagnostic findings. On the other hand, clinics involve specialized cancer centers that cater to outpatient needs and often focus exclusively on cancer care. They offer diagnostics, such as mammograms and consultations, which makes it convenient for patients to receive timely evaluations. Both hospitals and clinics play pivotal roles in delivering accurate and efficient diagnostics for cancer patients.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America exhibits a clear dominance, accounting for the largest cancer diagnostics market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America held the biggest market share due to the improved healthcare infrastructure. Apart from this, the rising focus on early detection of diseases among individuals is contributing to the growth of the market in the region. In line with this, the increasing awareness about cancer, along with favorable reimbursement policies, is propelling the cancer diagnostics market growth. Besides this, the presence of key diagnostic technology manufacturers, research institutions, and a strong network of healthcare facilities is bolstering the growth of the market in the North America region. The cancer diagnostics market revenue is increasing in the region, reflecting the high demand due to advancements in medical technology, increasing cancer prevalence, and the imperative for early and accurate diagnostic procedures

Competitive Landscape:

Major players are investing in research and development (R&D) activities to develop innovative diagnostic technologies. This involves exploring new biomarkers, improving imaging modalities, and enhancing the accuracy of molecular and genetic testing methods. In addition, diagnostic companies are continuously updating their existing technologies and platforms and incorporating artificial intelligence (AI) and machine learning (ML) algorithms for more accurate interpretation of diagnostic results. Apart from this, many companies are engaging in collaboration with research institutions, universities, and healthcare providers to gain expert knowledge and can access patient data for validation and improvement of diagnostic tools. Furthermore, key players are introducing new diagnostic products and services that focus on improved sensitivity, specificity, and ease of use.

The report has provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Abbott Laboratories

- Agilent Technologies, Inc.

- Becton, Dickinson and Company

- bioMérieux

- Bio-Rad Laboratories, Inc.

- F. Hoffmann-La Roche Ltd

- GE HealthCare

- Hologic, Inc.

- Illumina, Inc.

- Koninklijke Philips N.V.

- Qiagen N.V.

- Quest Diagnostics

- Siemens Healthineers AG (Siemens AG)

- Thermo Fisher Scientific Inc.

Recent Developments:

- In July 2025, Bern-based medtech company Compremium launched a human clinical study for its non-invasive thyroid cancer diagnostic device that measures tissue compressibility to better distinguish between benign and malignant nodules. The 18-month trial at Bern University Hospital targets patients with Bethesda IV nodules to help reduce unnecessary thyroid surgeries.

- In July 2025, Fred Hutch Cancer Center launched the Vanguard Study, the first trial under the Cancer Screening Research Network (CSRN), to assess the effectiveness of multi-cancer detection (MCD) blood tests in adults aged 45–75. The study will compare two MCD tests—Avantect® and Shield™—to determine their potential for early cancer detection. Results aim to guide future national cancer screening strategies.

- In June 2025, UK-based Dxcover launched its US headquarters in Nashville, aiming to commercialize its AI-powered multiomic PANAROMIC™ cancer detection test. The platform uses infrared spectroscopy and AI to analyze blood samples for early cancer detection, targeting hard-to-diagnose cancers.

- In May 2025, Metropolis Healthcare launched TruHealth Cancer Screen 360, a comprehensive, gender-specific cancer screening panel aimed at improving early cancer detection in India. It includes tumor markers, hereditary risk analysis across 25+ cancer types, and organ-specific assessments. The initiative targets both urban and rural areas to boost preventive oncology access and affordability.

- In April 2025, India launched indigenously developed HPV test kits for cervical cancer screening, created under the Department of Biotechnology’s Grand Challenges India program. These RT-PCR-based kits target the most common cancer-causing HPV types, aiming for cost-effective, accurate screening suited for national deployment.

- In February 2025, the NHS announced the world’s largest trial of AI for breast cancer diagnosis, involving 700,000 mammograms to test if AI can match radiologists in accuracy. If successful, it could replace the current “second reader” system, cutting radiologists’ workload in half and speeding up diagnosis. The £11 million trial begins later this year across 30 screening centers.

- In 2020, GE Healthcare, the leading global provider of advanced medical imaging, partnered with GenesisCare, a leading provider of integrated cancer care globally and cardiovascular care in Australia, that aimed at improving patient outcomes for the two biggest health burdens, such as cancer and heart disease.

- In November 2021, Siemens Healthineers launched NAEOTOM Alpha, the world’s first photon-counting CT Scanner with improved resolution and reduction in radiation dose by up to 45% for ultra-high resolution (UHR) scans.

- In October 2021, Agilent Technologies Inc. announced that its PD-L1 IHC 22C3 pharmDx assay can now be used as an aid in identifying triple-negative breast cancer (TNBC) in the European Union.

Cancer Diagnostics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered |

|

| Technologies Covered |

|

| Applications Covered | Breast Cancer, Lung Cancer, Colorectal Cancer, Melanoma, Others |

| End Users Covered | Hospitals and Clinics, Diagnostic Laboratories, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott Laboratories, Agilent Technologies, Inc., Becton, Dickinson and Company, bioMérieux, Bio-Rad Laboratories, Inc., F. Hoffmann-La Roche Ltd, GE HealthCare, Hologic, Inc., Illumina, Inc., Koninklijke Philips N.V., Qiagen N.V., Quest Diagnostics, Siemens Healthineers AG (Siemens AG), Thermo Fisher Scientific Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cancer diagnostics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global cancer diagnostics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cancer diagnostics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cancer Diagnostics Market Report

The global cancer diagnostics market was valued at USD 218.0 Billion in 2025.

We expect the global cancer diagnostics market to exhibit a CAGR of 4.68% during 2026-2034.

The rising adoption of cancer diagnostics by healthcare practitioners to develop a personalized treatment plan, evaluate specific antigens in a sample tissue, provide enhanced clinical outcomes through early care, etc., is primarily driving the global cancer diagnostics market.

The sudden outbreak of the COVID-19 pandemic had led to the postponement of elective cancer diagnostics procedures to reduce the risk of coronavirus infection upon hospital visits or interaction with healthcare professionals and medical equipment.

Based on the technology, the global cancer diagnostics market can be divided into IVD testing, imaging, and biopsy technique. Currently, imaging accounts for the largest market share.

Based on the application, the global cancer diagnostics market has been segregated into breast cancer, lung cancer, colorectal cancer, melanoma, and others. Among these, breast cancer currently exhibits a clear dominance in the market.

Based on the end user, the global cancer diagnostics market can be bifurcated into hospitals and clinics, diagnostic laboratories, and others. Currently, hospitals and clinics hold the majority of the total market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global cancer diagnostics market include Abbott Laboratories, Agilent Technologies, Inc., Becton, Dickinson and Company, bioMérieux, Bio-Rad Laboratories, Inc., F. Hoffmann-La Roche Ltd, GE HealthCare, Hologic, Inc., Illumina, Inc., Koninklijke Philips N.V., Qiagen N.V., Quest Diagnostics, Siemens Healthineers AG (Siemens AG), and Thermo Fisher Scientific Inc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)