Cancer Monoclonal Antibodies Market Size, Share, Trends and Forecast by Antibody Type, Medication Type, Application, End User, and Region, 2026-2034

Cancer Monoclonal Antibodies Market Size and Share:

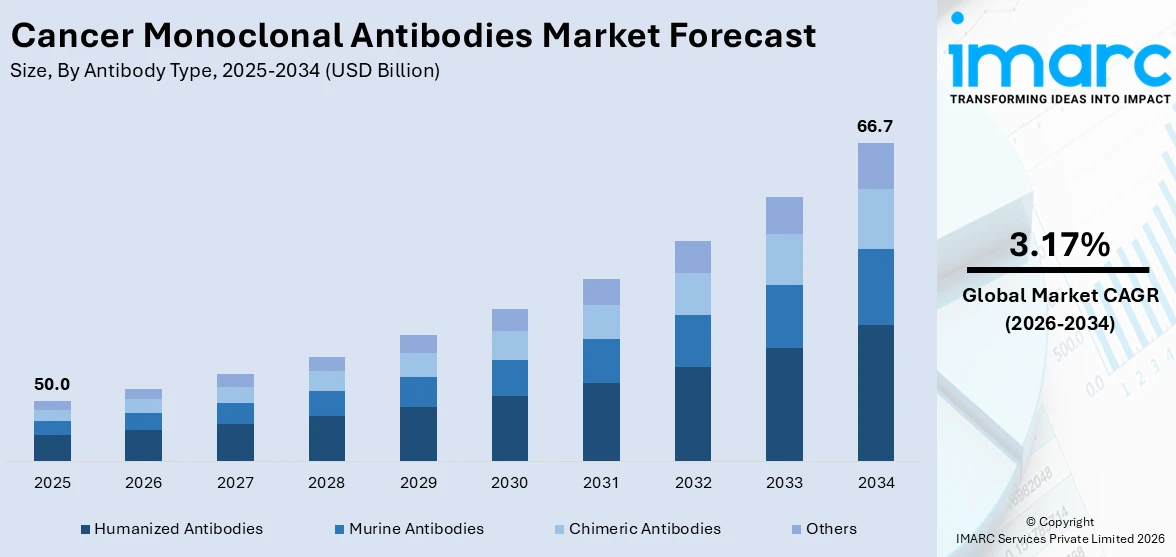

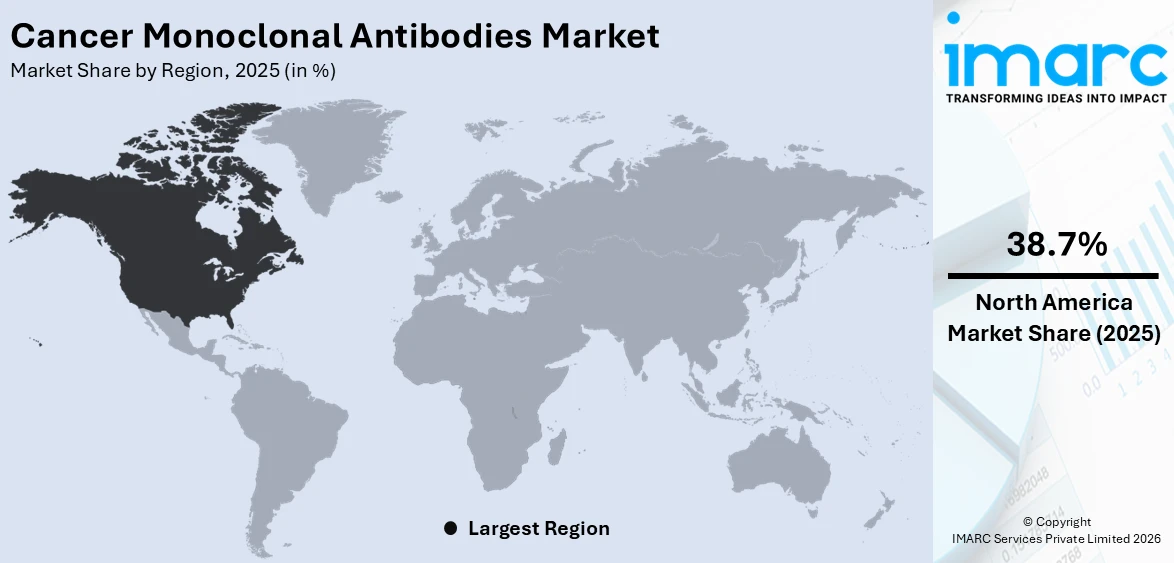

The global cancer monoclonal antibodies market size was valued at USD 50.0 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 66.7 Billion by 2034, exhibiting a CAGR of 3.17% during 2026-2034. North America currently dominates the market, holding a significant market share of 38.7% in 2025. This is attributed to its advanced healthcare infrastructure, early adoption of innovative therapies, and strong presence of leading biopharmaceutical companies. High cancer incidence rates and favorable reimbursement policies further support market growth. These factors collectively contribute to North America's leading cancer monoclonal antibodies market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 50.0 Billion |

|

Market Forecast in 2034

|

USD 66.7 Billion |

| Market Growth Rate 2026-2034 | 3.17% |

The market is primarily driven by the growing prevalence of complex and refractory tumor types, necessitating more precise and biologically targeted treatment modalities. Increased emphasis on immunotherapy as a frontline approach in oncology has accelerated clinical trials and regulatory pathways for monoclonal antibody-based drugs. Moreover, the rise of biosimilars has expanded access to these therapies in emerging markets, fostering broader adoption. Continuous innovation in antibody-drug conjugates and bispecific antibodies is also enhancing treatment efficacy and specificity. Expanding academic-industry collaborations are contributing to faster therapeutic development, while supportive reimbursement frameworks in high-income countries are further creating a positive cancer monoclonal antibodies market outlook. For instance, in May 2025, researchers from Ludwig Cancer Research (Lausanne, Switzerland) and Taipei Medical University (Taiwan) developed PLT012, a novel monoclonal antibody targeting CD36, a lipid transporter exploited by tumors to suppress immune responses in fat-rich microenvironments. PLT012 blocks CD36, restoring immune function and showing strong anti-tumor effects in liver cancer models, including immunotherapy-resistant cases. It works alone or with checkpoint inhibitors and rewires the tumor immune landscape. With FDA orphan drug status, PLT012 offers a promising new metabolic immunotherapy approach for difficult-to-treat cancers.

To get more information on this market Request Sample

In the United States, the cancer monoclonal antibodies market growth is propelled by a strong biopharmaceutical innovation ecosystem supported by robust federal funding and private sector investment. The presence of advanced clinical infrastructure enables rapid progression from discovery to commercial availability, accelerating market momentum. High patient awareness and access to precision diagnostics promote early adoption of novel therapies. Additionally, the increasing integration of real-world evidence and artificial intelligence in drug development and patient stratification supports more personalized treatment regimens. The U.S. FDA’s expedited approval pathways, including Breakthrough Therapy and Priority Review designations, further streamline product launches. Strategic partnerships and licensing agreements among domestic biotech firms also sustain competitive advancement in monoclonal antibody therapeutics.

Cancer Monoclonal Antibodies Market Trends:

Rising Cancer Incidence Driving Demand for Monoclonal Antibodies

The steadily increasing prevalence of cancer globally is significantly contributing to the growth of the monoclonal antibodies market. According to the World Health Organization (WHO), over 35 million new cancer cases are projected by 2050, underscoring an urgent demand for safer and more effective therapies. Unlike traditional treatments such as chemotherapy, monoclonal antibodies offer targeted therapy with fewer side effects. This patient-centric approach enhances treatment outcomes while minimizing systemic harm. As oncologists seek more personalized and precise therapies, monoclonal antibodies have become an integral part of modern oncology treatment regimens. This trend reflects a shift toward biologics that can address complex diseases with higher specificity and safety, supporting their increasing adoption in cancer treatment strategies.

Growing Adoption of Cost-Effective Biosimilar Monoclonal Antibodies

A key cancer monoclonal antibodies market trend is the increasing use of biosimilars. These cost-effective alternatives to original biologic therapies are gaining popularity among healthcare professionals due to their comparable efficacy and reduced costs. An analysis by Avalere Health for the Biosimilars Council estimates that biosimilar access could enable 1.2 million U.S. patients to obtain biologic treatments by 2025. This affordability plays a pivotal role in market expansion, especially in regions with limited healthcare funding. Additionally, advancements in biotechnology have enabled the production of biosimilars that closely match the reference drugs in terms of structure and performance. As cost-efficiency becomes a critical consideration for healthcare systems globally, biosimilar monoclonal antibodies are expected to play an increasingly important role in expanding treatment access.

Technological Advancements Supporting Personalized Medicine

Technological progress in gene sequencing and target gene selection is fostering a significant shift toward personalized medicine in the monoclonal antibodies market. With these advancements, monoclonal antibodies can be engineered to target specific genetic markers, enhancing their effectiveness in treating not only cancers but also autoimmune and inflammatory diseases. The ability to tailor treatments based on individual genetic profiles improves patient outcomes and reduces adverse effects. This precision medicine approach is supported by increased R&D investments and improved healthcare infrastructure worldwide. Moreover, these innovations allow monoclonal antibodies to mimic the therapeutic properties of original biologics while being produced at lower costs. As the healthcare industry continues to prioritize individualized treatment protocols, personalized monoclonal antibody therapies are becoming a central trend in global healthcare delivery. For instance, BioNTech’s Phase 2 trial of BNT111 combined with cemiplimab showed a significant response in patients with advanced, anti-PD-(L)1 refractory melanoma. The treatment improved overall response rates versus historical data and was well tolerated. BNT111 uses uridine mRNA and targets four melanoma antigens. The program holds FDA Fast Track and Orphan Drug designations.

Cancer Monoclonal Antibodies Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global cancer monoclonal antibodies market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on antibody type, medication type, application, and end user.

Analysis by Antibody Type:

- Murine Antibodies

- Chimeric Antibodies

- Humanized Antibodies

- Others

Humanized antibodies stand as the largest antibody type in 2025, holding around 40.7% of the market. The humanized antibodies segment dominates the cancer monoclonal antibodies market due to its superior efficacy, reduced immunogenicity, and enhanced safety profile. By replacing most of the mouse antibody components with human sequences, humanized antibodies minimize the risk of adverse immune responses in patients, making them more suitable for repeated administration. These antibodies offer targeted treatment by binding specifically to cancer cell antigens, thereby improving therapeutic outcomes while limiting damage to healthy tissues. Additionally, their compatibility with human immune systems enhances pharmacokinetics and therapeutic effectiveness. The growing adoption of personalized medicine and advancements in genetic engineering further support the dominance of humanized antibodies in cancer treatment.

Analysis by Medication Type:

- Bevacizumab (Avastin)

- Rituximab (Rituxan)

- Trastuzumab (Herceptin)

- Cetuximab (Erbitux)

- Panitumumab (Vectibix)

- Others

Trastuzumab (Herceptin) leads the market in 2025. The Trastuzumab (Herceptin) segment dominates the cancer monoclonal antibodies market due to its established efficacy in treating HER2-positive breast and gastric cancers. As one of the first targeted therapies approved for oncology, Herceptin has significantly improved survival rates in patients with aggressive tumors overexpressing the HER2 protein. Its widespread clinical adoption, proven long-term safety profile, and inclusion in standard cancer treatment protocols have cemented its leading position. Additionally, ongoing research has expanded its applications through combination therapies and biosimilar developments, enhancing its accessibility and affordability. The sustained clinical success of Trastuzumab continues to drive its dominance in the cancer monoclonal antibodies market.

Analysis by Application:

- Breast Cancer

- Blood Cancer

- Liver Cancer

- Brain Cancer

- Colorectal Cancer

- Others

Blood cancer leads the market with around 23.8% of market share in 2025. The blood cancer segment dominates the cancer monoclonal antibodies market due to the high effectiveness of monoclonal antibody therapies in treating hematologic malignancies such as leukemia, lymphoma, and multiple myeloma. These cancers often exhibit specific surface antigens, making them ideal targets for antibody-based treatments like Rituximab and Daratumumab. Moreover, blood cancers generally have a more accessible cellular environment compared to solid tumors, enhancing therapeutic delivery and response rates. The increasing incidence of blood cancers globally, coupled with advancements in targeted therapy and the development of biosimilars, has further expanded patient access. As a result, the blood cancer segment continues to lead in terms of treatment demand and market share.

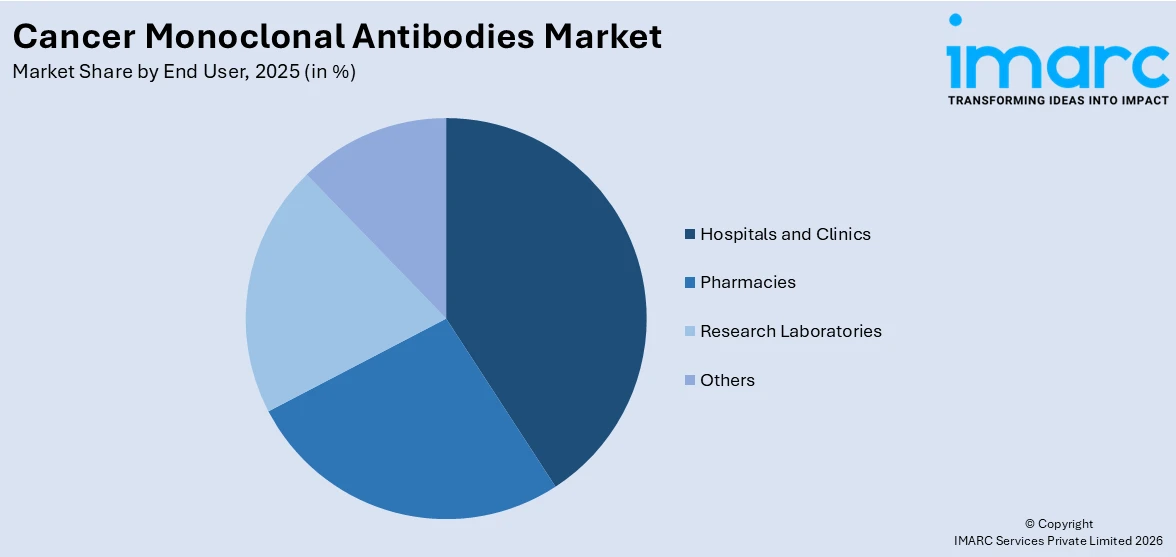

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Hospitals and Clinics

- Pharmacies

- Research Laboratories

- Others

Hospitals and clinics lead the market with around 40.3% of market share in 2025. The hospitals and clinics segment dominates the cancer monoclonal antibodies market due to their central role in administering advanced oncology treatments and managing complex care protocols. These facilities are equipped with the necessary infrastructure, specialized staff, and diagnostic capabilities required for safe and effective monoclonal antibody therapy. Additionally, most monoclonal antibody treatments are administered intravenously, necessitating a clinical setting for proper dosage, monitoring, and management of potential adverse effects. The growing number of hospital-based cancer centers, increased patient footfall, and favorable reimbursement policies further reinforce the dominance of this segment. As a result, hospitals and clinics remain the primary channel for delivering cancer monoclonal antibody therapies.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 38.7%. North America dominates the cancer monoclonal antibodies market due to its advanced healthcare infrastructure, high adoption of innovative therapies, and strong presence of major pharmaceutical companies. The region benefits from significant investments in oncology research and favorable regulatory support for fast-track drug approvals. Additionally, rising cancer incidence, increased awareness about targeted therapies, and widespread availability of health insurance contribute to higher treatment uptake. Robust clinical trial activity and strategic collaborations between biotech firms and research institutions also fuel innovation and market expansion. These factors collectively position North America as the leading region in the global cancer monoclonal antibodies market. For instance, in March 2024, the FDA approved BeiGene’s TEVIMBRA (tislelizumab) for adults with unresectable or metastatic esophageal squamous cell carcinoma after prior chemotherapy. The Phase 3 RATIONALE 302 trial showed TEVIMBRA significantly improved overall survival over chemotherapy. This is BeiGene’s first U.S. approval for TEVIMBRA. The PD-1 monoclonal antibody has also been approved in the EU and is under review for first-line use in ESCC and gastric cancers. Over 900,000 patients worldwide have received the drug to date.

Key Regional Takeaways:

United States Cancer Monoclonal Antibodies Market Analysis

In 2025, the United States held a market share of around 84.30% in North America. The United States cancer monoclonal antibodies market is expanding steadily, driven by a high burden of chronic diseases and advanced research capabilities in immunotherapy. The region benefits from significant investments in precision medicine and cutting-edge biotechnological tools, enabling the development of particular antibody-based cancer treatments. According to the American Cancer Society, over 2 Million new cancer cases are expected to be diagnosed in the US in 2025, with more than 618,000 deaths projected, further intensifying the demand for innovative monoclonal antibody therapies. Strong regulatory support for fast-tracking breakthrough therapies also contributes to the market’s dynamism. Moreover, the presence of specialized academic institutions and translational research centers fosters innovation in monoclonal antibody development. Growing awareness of personalized treatment options is prompting patients and healthcare providers to favor biologics over conventional chemotherapy. The integration of real-world data into clinical trial design is enhancing therapy success rates and market penetration. Additionally, strategic collaborations between research entities and manufacturers are accelerating product pipelines. Increasing uptake of outpatient care and ambulatory infusion centers has further supported therapy accessibility, enhancing treatment continuity. Furthermore, the adoption of artificial intelligence in clinical oncology is optimizing patient stratification, thereby improving monoclonal antibody efficacy.

Europe Cancer Monoclonal Antibodies Market Analysis

The cancer monoclonal antibodies market in Europe is driven by strong public health infrastructure and proactive government policies that emphasize immuno-oncology innovation. Research funding through national and regional programs has strengthened the pipeline of monoclonal antibodies targeting solid tumors and hematological malignancies. In this context, the European Commission reports partnerships with nearly 630 organizations and a funding commitment of approximately USD 425 Million toward cancer prevention, detection, diagnosis, and treatment, strengthening Europe’s immuno-oncology ecosystem. Clinical trial harmonization across countries is supporting faster regulatory assessments and multi-center study enrollments, facilitating product approval timelines. Additionally, a shift toward value-based healthcare is encouraging the adoption of therapies that offer high clinical benefits and long-term survival outcomes. Europe's focus on reducing hospitalizations through targeted outpatient biologic therapies has improved treatment adherence. Technological advances in biomanufacturing, continuous bioprocessing, and better post-marketing surveillance in integrated healthcare systems are enhancing production efficiency and cost reduction. Rising geriatric populations with complex cancer profiles demand tailored therapies.

Asia Pacific Cancer Monoclonal Antibodies Market Analysis

The cancer monoclonal antibodies market in Asia Pacific is witnessing notable expansion, propelled by increased healthcare spending and rapid improvements in diagnostic capabilities. Public-private partnerships along with rising government expenditure on healthcare in the region are playing a vital role in establishing regional biopharmaceutical hubs, facilitating the local development and distribution of antibody-based cancer treatments. The Ministry of Health and Family Welfare in India, for instance, has been allocated approximately USD 11.98 Billion in the 2024–2025 budget, with USD 11.51 Billion designated for healthcare services and USD 467 Million for health research, signaling a substantial national commitment to advanced cancer care. An expanding middle class and growing healthcare literacy are driving demand for advanced, targeted therapies that minimize side effects. The integration of genomic profiling in oncology care is promoting personalized monoclonal antibody applications, while medical tourism and investments in cold chain infrastructure support market growth. Digital health platforms are improving treatment monitoring and adherence to monoclonal antibody regimens.

Latin America Cancer Monoclonal Antibodies Market Analysis

The Latin American market for cancer monoclonal antibodies is gaining momentum, fueled by improving oncology care infrastructure and expanding access to specialty treatment. It has been estimated that, in Brazil, an estimated 23.8% of men and 18.3% of women will develop cancer before the age of 75. Government initiatives aimed at modernizing cancer care protocols are driving the adoption of biologics in clinical settings. The region’s rising cancer prevalence, especially among working-age populations, is boosting interest in therapies that improve quality of life and reduce hospital stays. Strategic international collaborations with academic and research institutions are enhancing local capacity for clinical trials and biological development.

Middle East and Africa Cancer Monoclonal Antibodies Market Analysis

In the Middle East and Africa, the cancer monoclonal antibodies market is expanding due to growing investments in oncology centers and enhanced access to specialty care. A recent report highlights that Saudi Arabia has committed USD 65 Billion to healthcare privatization, aiming to transform the country’s entire healthcare landscape, an initiative that is expected to enhance cancer treatment infrastructure and access to advanced biologics. The region is witnessing an increase in public awareness campaigns that promote early cancer detection, creating demand for advanced biological treatments. Infrastructure development, including infusion clinics and diagnostic labs, is improving treatment accessibility. Educational initiatives targeting healthcare professionals are increasing familiarity with immunotherapy protocols, and facilitating clinical adoption.

Competitive Landscape:

The cancer monoclonal antibodies market is marked by fast-paced innovation, active pipeline expansion, and partnerships between biotech firms and research institutions. In January 2024, Johnson & Johnson acquired Ambrx Biopharma for $2 Billion to boost its oncology pipeline, particularly with advanced antibody-drug conjugates like ARX517 for prostate cancer and additional candidates for HER2+ breast and renal cancers. Companies are focusing on antibody engineering to improve targeting and reduce side effects. Market competition is influenced by IP protection, regulatory pathways, biosimilar pressure, licensing deals, and geographic growth strategies. Strategic licensing agreements and regional expansions are also shaping the market dynamics. The cancer monoclonal antibodies market forecast projects sustained growth over the coming years, driven by rising cancer incidence, expanding therapeutic applications, and continued research in next-generation antibody therapies.

The report provides a comprehensive analysis of the competitive landscape in the cancer monoclonal antibodies market with detailed profiles of all major companies, including:

- Amgen Inc.

- AbbVie Inc. (Abbott Laboratories)

- AstraZeneca plc

- Biocon Limited

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- F. Hoffmann-La Roche Ltd. (Roche Holding AG)

- Genmab A/S

- Merck & Co., Inc.

- Pfizer Inc.

Latest News and Developments:

- June 2025: The MHRA approved serplulimab (Hetronifly) as the first anti-PD-1 monoclonal antibody in the UK for extensive-stage small-cell lung cancer. In clinical trials, it extended survival by 4.5 months over placebo. Administered with chemotherapy, serplulimab improved the immune targeting of tumors by inhibiting PD-1 signaling.

- June 2025: Hummingbird Bioscience, a pioneering biotherapeutics company dedicated to developing transformative medicines for hard-to-treat diseases, has announced a significant licensing deal with Percheron Therapeutics. Under the agreement, Percheron has obtained exclusive worldwide rights to Hummingbird's anti-VISTA monoclonal antibody, HMBD-002, for further clinical development. The deal allows Percheron Therapeutics to advance HMBD-002 through clinical trials, with a focus on commencing Phase II development in 2026. Hummingbird Bioscience stands to receive up to USD 290 million in upfront and milestone payments, in addition to royalties on net sales.

- March 2025: Infinity Bio launched its MuSIGHT™ platform for mouse antibody reactome profiling. Using MIPSA technology, enabled detailed mapping of immune responses and autoimmunity in cancer models. The innovation supported translational research by clarifying differences between murine and human immune behavior in oncology studies.

- January 2025: Roche received FDA approval to expand its PATHWAY HER2 (4B5) test to identify HER2-ultralow breast cancer patients eligible for ENHERTU. Based on DESTINY-Breast06 trial results, the test enabled targeted therapy access for a previously untreated segment, offering improved progression-free survival with HER2-directed monoclonal antibody therapy.

Cancer Monoclonal Antibodies Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Antibody Types Covered | Murine Antibodies, Chimeric Antibodies, Humanized Antibodies, Others |

| Medication Types Covered | Bevacizumab (Avastin), Rituximab (Rituxan), Trastuzumab (Herceptin), Cetuximab (Erbitux), Panitumumab (Vectibix), Others |

| Applications Covered | Breast Cancer, Blood Cancer, Liver Cancer, Brain Cancer, Colorectal Cancer, Others |

| End Users Covered | Hospitals and Clinics, Pharmacies, Research Laboratories, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Brazil, Mexico |

| Companies Covered | Amgen Inc., AbbVie Inc. (Abbott Laboratories), AstraZeneca plc, Biocon Limited, Bristol-Myers Squibb Company, Eli Lilly and Company, F. Hoffmann-La Roche Ltd. (Roche Holding AG), Genmab A/S, Merck & Co., Inc., Pfizer Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cancer monoclonal antibodies market from 2020-2034.

- The cancer monoclonal antibodies market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cancer monoclonal antibodies industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cancer Monoclonal Antibodies Market Report

The cancer monoclonal antibodies market was valued at USD 50.0 Billion in 2025.

The cancer monoclonal antibodies market is projected to exhibit a CAGR of 3.17% during 2026-2034, reaching a value of USD 66.7 Billion by 2034.

Key factors driving the cancer monoclonal antibodies market include rising global cancer incidence, advancements in antibody engineering, increasing approvals of targeted therapies, and growing investment in oncology research. Additionally, improved diagnostic technologies, personalized medicine trends, and expanding applications of monoclonal antibodies in combination therapies are propelling market growth and innovation.

North America currently dominates the cancer monoclonal antibodies market, accounting for a share of 38.7%, driven by advanced healthcare infrastructure, high cancer prevalence, significant R&D investments, and strong presence of leading pharmaceutical companies. Favorable regulatory support and rapid adoption of novel therapies further bolster the region’s market leadership.

Some of the major players in the cancer monoclonal antibodies market include Amgen Inc., AbbVie Inc. (Abbott Laboratories), AstraZeneca plc, Biocon Limited, Bristol-Myers Squibb Company, Eli Lilly and Company, F. Hoffmann-La Roche Ltd. (Roche Holding AG), Genmab A/S, Merck & Co., Inc., Pfizer Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade