Caprolactam Prices, Trend, Chart, Demand, Market Analysis, News, Historical and Forecast Data Report 2026 Edition

Caprolactam Price Trend, Index and Forecast

Track real-time and historical caprolactam prices across global regions. Updated monthly with market insights, drivers, and forecasts.

Caprolactam Prices July 2026

| Region | Price (USD/KG) | Latest Movement |

|---|---|---|

| Northeast Asia | 1.8 | 1.7% ↑ Up |

| Europe | 2.17 | -9.2% ↓ Down |

| North America | 1.93 | -9.8% ↓ Down |

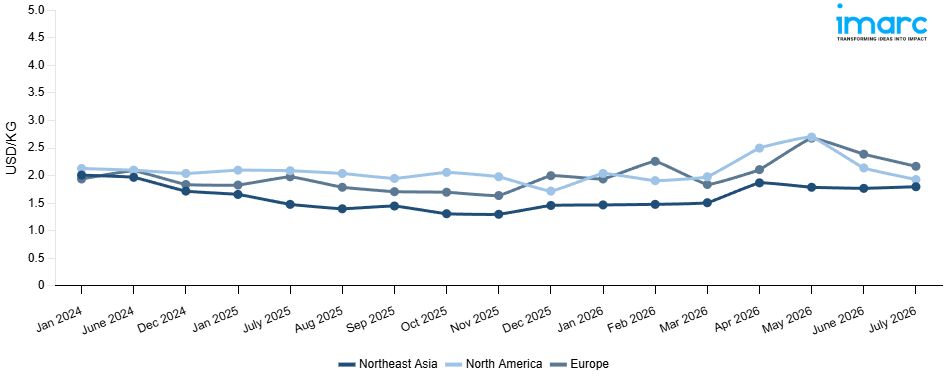

Caprolactam Price Index (USD/KG):

The chart below highlights monthly caprolactam prices across different regions.

Get Access to Monthly/Quarterly/Yearly Prices, Request Sample

Market Overview Q1 Ending March 2026

Northeast Asia: The caprolactam prices in Northeast Asia reached 1.51 USD/KG in March 2026. The upward pricing movement registered between December and March 2026 was 3.4%. The rate of price appreciation was mainly driven by the sustained upstream costs of benzene and cyclohexane feedstocks, thereby influencing the production costs of regional manufacturers. Sustained consumption from Nylon 6 fiber, engineering plastics, and industrial filaments segments continued to underpin firm procurement activity. Balanced production output from key polymerization plants was maintained to ensure controlled market availability. Additionally, sustained consumption from carpet fiber and packaging film segments continued to underpin firm offtake fundamentals.

Europe: The caprolactam prices in Europe reached 1.84 USD/KG in March 2026. The downward pricing movement registered between December and March 2026 was 8.0%. The notable price correction was primarily attributed to weakened demand from the Nylon 6 fiber, engineering resin, and textile filament manufacturing sectors amid broader contraction in regional automotive production schedules and industrial output. Softening upstream valuations for benzene and cyclohexane feedstock reduced production cost benchmarks for domestic producers, diminishing baseline pricing support across the supply chain. Surplus availability from established manufacturing facilities exerted additional downward pressure on prevailing market rates, while elevated stockpile positions among key distributors prompted competitive pricing concessions to stimulate buyer interest.

North America: The caprolactam prices in North America reached 1.98 USD/KG in March 2026. The upward pricing movement registered between December and March 2026 was 15.1%. The significant price appreciation was driven by supply side factors stemming from unscheduled operational stoppages and scheduled maintenance turnarounds at important production facilities, which significantly curtailed domestic supply. Strong demand out of the Nylon 6 fiber, engineering plastics, and industrial filament manufacturing sectors fueled procurement competition, given the constrained available spot supply. Soaring upstream costs for benzene and cyclohexane based feedstocks continued to drive up producer costs, thereby continuing the price appreciation trend. Further, robust end use demand out of the automotive components and carpet fibers fueled strong off take fundamentals.

Market Overview Q4 Ending December 2025

Northeast Asia: The caprolactam prices in Northeast Asia reached 1.46 USD/KG in December 2025. The upward pricing movement registered between September and December 2025 was 0.7%. The marginal price increase reflected a largely balanced market environment, with steady demand from the Nylon 6 manufacturing sector sustaining baseline consumption levels. Firm upstream benzene and cyclohexane feedstock costs provided incremental pricing support, while controlled production output by regional suppliers prevented market oversaturation and maintained relatively stable pricing dynamics throughout the quarter.

Europe: The caprolactam prices in Europe reached 2.00 USD/KG in December 2025. The upward pricing movement registered between September and December 2025 was 17.0%. The substantial price appreciation was primarily driven by tightened supply conditions resulting from scheduled and unscheduled plant maintenance shutdowns at key European production facilities, significantly constraining regional availability. The textile filament and engineering plastics industries' strong demand further heightened downstream consumers' competitiveness for procurement. The upward pricing pressure was exacerbated by high upstream benzene feedstock prices, and purchasers' ability to obtain competitively priced spot cargoes throughout the quarter was hampered by limited import options due to logistical constraints and strict international pricing.

North America: The caprolactam prices in North America reached 1.72 USD/KG in December 2025. The downward pricing movement registered between September and December 2025 was 11.9%. The notable price decline was attributed to weakened demand from the Nylon 6 fiber and engineering resins sectors amid softening end-market conditions in the automotive and textiles industries. Bearish market sentiment persisted throughout the quarter due to increased import availability from competitively priced Asian cargoes, which further pushed domestic pricing down, and lower feedstock costs, which further undermined production cost support.

Market Overview Q3 Ending September 2025

Northeast Asia: The rise was primarily driven by strong downstream demand from the polyamide and nylon sectors in China, Japan, and South Korea. Supply-side factors, including limited domestic production capacity and higher raw material costs, contributed to the price increase. International shipping rates and port handling charges also added to cost pressures, particularly for imported cyclohexanone and adipic acid, key feedstocks. Currency fluctuations, especially the relative strength of the Japanese yen against the US dollar, further influenced import costs. Domestic logistics, including inland transportation and storage for industrial-grade Caprolactam, experienced marginal cost increases due to higher energy and labor expenses. Additionally, compliance costs for environmental regulations and safety standards in production facilities modestly affected overall pricing dynamics in the region. The combination of constrained supply, elevated raw material costs, and consistent industrial demand sustained the observed upward movement in caprolactam prices across Northeast Asia.

Europe: The downward movement was largely due to softer demand from automotive and textile manufacturing sectors across Germany, France, and Italy, reflecting slower economic activity in key downstream industries. On the supply side, European producers maintained stable output levels, and some import volumes of raw materials increased, which eased pressure on local inventories. Additional factors impacting pricing included reductions in international freight costs and moderate fluctuations in port handling fees. Currency movements, particularly the euro against the US dollar, also played a role in moderating costs for imported feedstocks. Domestic logistics and transportation within Europe remained relatively stable, and compliance costs for environmental and safety standards did not exhibit major changes in this quarter.

North America: Reduced demand from nylon and polymer industries in the United States and Canada contributed to softer pricing trends. Supply-side factors, including consistent production volumes from domestic manufacturers, prevented further upward price pressures. Raw material costs, including cyclohexanone and ammonia, remained relatively stable, while international shipping costs experienced slight moderation, influencing overall pricing. Port handling charges and domestic logistics, including warehousing and inland transportation, were stable in this quarter. Currency fluctuations between the US dollar and other major currencies had minimal impact on domestic production costs. Compliance expenses related to environmental and safety regulations maintained a steady baseline and did not significantly affect pricing. Collectively, these factors led to a moderate decline in North American prices during the third quarter.

Caprolactam Price Trend, Market Analysis, and News

IMARC's latest publication, “Caprolactam Prices, Trend, Chart, Demand, Market Analysis, News, Historical and Forecast Data Report 2026 Edition,” presents a detailed examination of the caprolactam market, providing insights into both global and regional trends that are shaping prices. This report delves into the spot price of caprolactam at major ports and analyzes the composition of prices, including FOB and CIF terms. It also presents detailed caprolactam prices trend analysis by region, covering North America, Europe, Asia Pacific, Latin America, and Middle East and Africa. The factors affecting caprolactam pricing, such as the dynamics of supply and demand, geopolitical influences, and sector-specific developments, are thoroughly explored. This comprehensive report helps stakeholders stay informed with the latest market news, regulatory updates, and technological progress, facilitating informed strategic decision-making and forecasting.

Caprolactam Industry Analysis

The global caprolactam industry size reached USD 18.14 Billion in 2025. By 2034, IMARC Group expects the market to reach USD 25.29 Billion, at a projected CAGR of 3.76% during 2026-2034. The market is driven by the increasing demand for nylon in automotive and textile industries, expansion of polyamide manufacturing, rising consumption in engineering plastics, investment in sustainable production processes, and continued industrial demand from consumer goods and packaging sectors.

Latest developments in the Caprolactam Industry:

- August 2025: Hengyi Petrochemical confirmed the underway commencement of its new caprolactam plant in Qinzhou, Guangxi, China. This facility is part of a comprehensive caprolactam-polyamide integrated industrial project with an annual capacity of 1.2 million tons.

- November 2024: HighChem Co., Ltd. acquired Sumitomo Chemical's vapor-phase Beckmann rearrangement process for caprolactam production, a method that produces high-quality caprolactam without generating ammonium sulfate as a byproduct. This acquisition positions HighChem to globally license this technology and supply catalysts from its own facilities, potentially influencing the caprolactam market by offering a more sustainable and efficient production method.

- October 2024: BASF introduced Ultramid® LowPCF and Ultramid® ZeroPCF, offering caprolactam with reduced and net-zero CO₂ footprints, aiming to offer more sustainable options for caprolactam users.

- March 2022: DOMO Chemicals achieved a milestone by delivering its 5 millionth metric tons of caprolactam at its Leuna site. The production capacity had been progressively increased throughout this time to reach the current level of 176,000 metric tons annually.

- October 2022: Xuyang Group's caprolactam expansion project in Cangzhou Park increased its production capacity to 750,000 tons/year. The second phase of the expansion project achieved stable operation after reaching full load in 24 days, consolidating Xuyang Group's position as a vital player in the coastal polyamide industry.

Product Description

Caprolactam is a colorless crystalline organic compound and a key chemical intermediate used primarily in the production of nylon-6 fibers and resins. Recognized for its high purity and reactivity, caprolactam occupies a central position in global polymer and textile manufacturing. Its unique property of polymerizing into high-strength nylon makes it indispensable in producing industrial fibers, automotive components, engineering plastics, and packaging materials. Caprolactam enhances product durability, heat resistance, and mechanical performance, making it critical for industries such as automotive, textiles, electronics, and consumer goods. Its widespread industrial application and pivotal role in nylon production position it as a core chemical in global manufacturing supply chains.

Report Coverage

| Key Attributes | Details |

|---|---|

| Product Name | Caprolactam |

| Report Features | Exploration of Historical Trends and Market Outlook, Industry Demand, Industry Supply, Gap Analysis, Challenges, Caprolactam Price Analysis, and Segment-Wise Assessment. |

| Currency/Units | US$ (Data can also be provided in local currency) or Metric Tons |

| Region/Countries Covered | The current coverage includes analysis at the global and regional levels only. Based on your requirements, we can also customize the report and provide specific information for the following countries: Asia Pacific: China, India, Indonesia, Pakistan, Bangladesh, Japan, Philippines, Vietnam, Thailand, South Korea, Malaysia, Nepal, Taiwan, Sri Lanka, Hongkong, Singapore, Australia, and New Zealand Europe: Germany, France, United Kingdom, Italy, Spain, Russia, Turkey, Netherlands, Poland, Sweden, Belgium, Austria, Ireland, Switzerland, Norway, Denmark, Romania, Finland, Czech Republic, Portugal and Greece North America: United States and Canada Latin America: Brazil, Mexico, Argentina, Columbia, Chile, Ecuador, and Peru Middle East & Africa: Saudi Arabia, UAE, Israel, Iran, South Africa, Nigeria, Oman, Kuwait, Qatar, Iraq, Egypt, Algeria, and Morocco The list of countries presented is not exhaustive. Information on additional countries can be provided if required by the client. |

| Information Covered for Key Suppliers |

|

| Customization Scope | The report can be customized as per the requirements of the customer |

| Report Price and Purchase Option |

Plan A: Monthly Updates - Annual Subscription

Plan B: Quarterly Updates - Annual Subscription

Plan C: Biannually Updates - Annual Subscription

|

| Post-Sale Analyst Support | 360-degree analyst support after report delivery |

| Delivery Format | PDF and Excel through email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report presents a detailed analysis of caprolactam pricing, covering global and regional trends, spot prices at key ports, and a breakdown of FOB and CIF prices.

- The study examines factors affecting caprolactam price trend, including input costs, supply-demand shifts, and geopolitical impacts, offering insights for informed decision-making.

- The competitive landscape review equips stakeholders with crucial insights into the latest market news, regulatory changes, and technological advancements, ensuring a well-rounded, strategic overview for forecasting and planning.

- IMARC offers various subscription options, including monthly, quarterly, and biannual updates, allowing clients to stay informed with the latest market trends, ongoing developments, and comprehensive market insights. The caprolactam price charts ensure our clients remain at the forefront of the industry.

Frequently Asked Questions About the Caprolactam Price Index Report

The caprolactam prices in July 2026 were 1.8 USD/Kg in Northeast Asia, 2.17 USD/Kg in Europe, and 1.93 USD/Kg in North America.

The caprolactam pricing data is updated on a monthly basis.

We provide the pricing data primarily in the form of an Excel sheet and a PDF.

Yes, our report includes a forecast for caprolactam prices.

The regions covered include North America, Europe, Asia Pacific, Middle East, and Latin America. Countries can be customized based on the request (additional charges may be applicable).

Yes, we provide both FOB and CIF prices in our report.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Inquire Before Buying

Inquire Before Buying

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Why Choose Us

IMARC offers trustworthy, data-centric insights into commodity pricing and evolving market trends, enabling businesses to make well-informed decisions in areas such as procurement, strategic planning, and investments. With in-depth knowledge spanning more than 1000 commodities and a vast global presence in over 150 countries, we provide tailored, actionable intelligence designed to meet the specific needs of diverse industries and markets.

1000

+Commodities

150

+Countries Covered

3000

+Clients

20

+Industry

Robust Methodologies & Extensive Resources

IMARC delivers precise commodity pricing insights using proven methodologies and a wealth of data to support strategic decision-making.

Subscription-Based Databases

Our extensive databases provide detailed commodity pricing, import-export trade statistics, and shipment-level tracking for comprehensive market analysis.

Primary Research-Driven Insights

Through direct supplier surveys and expert interviews, we gather real-time market data to enhance pricing accuracy and trend forecasting.

Extensive Secondary Research

We analyze industry reports, trade publications, and market studies to offer tailored intelligence and actionable commodity market insights.

Trusted by 3000+ industry leaders worldwide to drive data-backed decisions. From global manufacturers to government agencies, our clients rely on us for accurate pricing, deep market intelligence, and forward-looking insights.