Carbon Black Market Size, Share, Trends and Forecast by Type, Grade, Application, and Region, 2026-2034

Global Carbon Black Market Size, Share, Trends & Forecast (2026-2034)

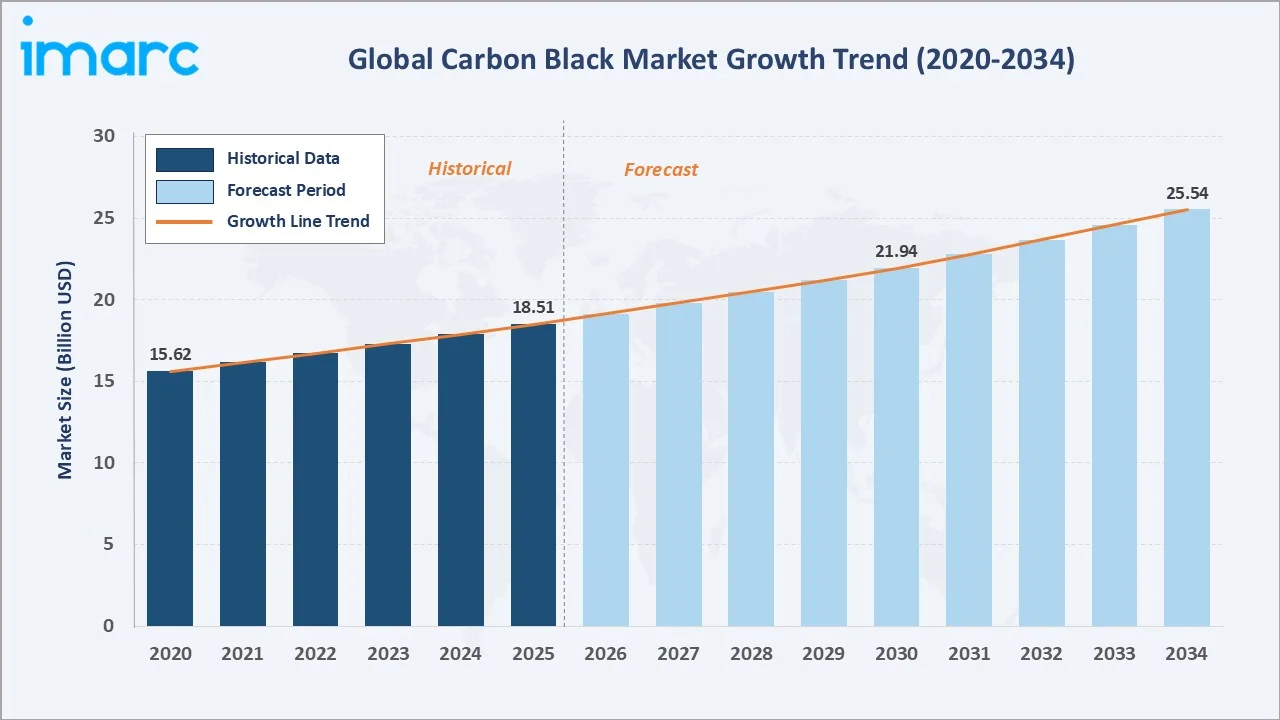

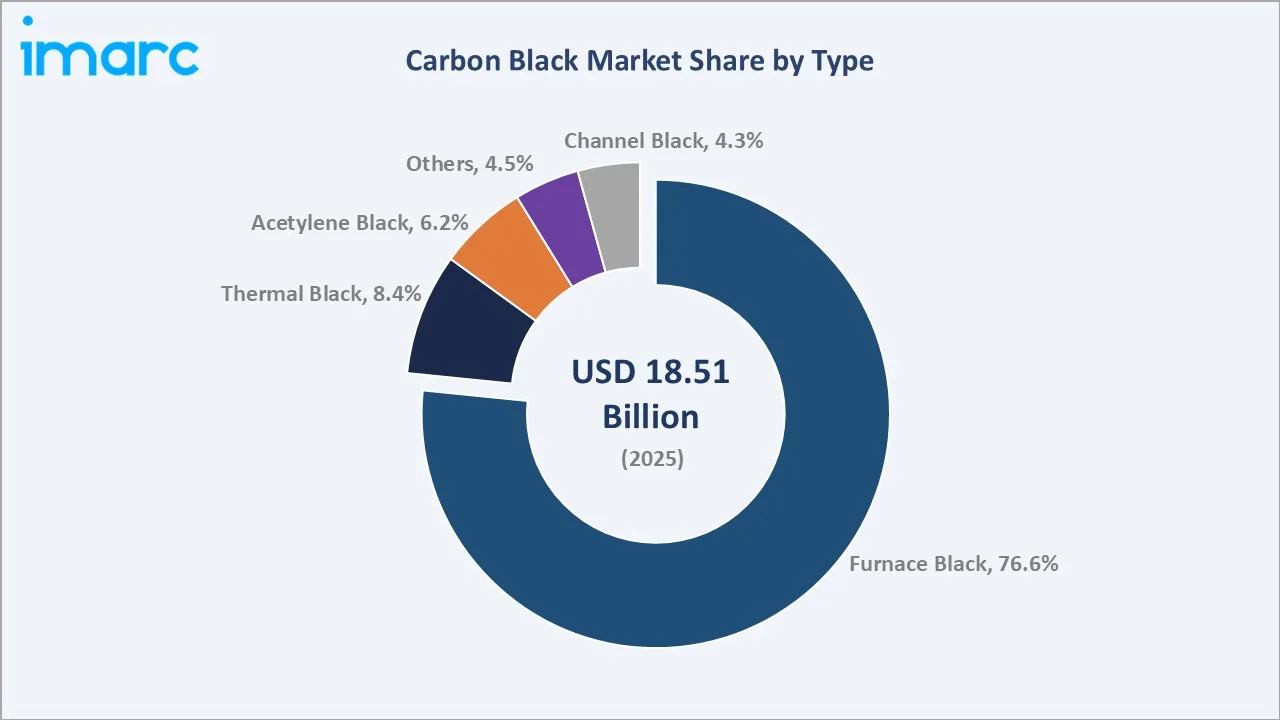

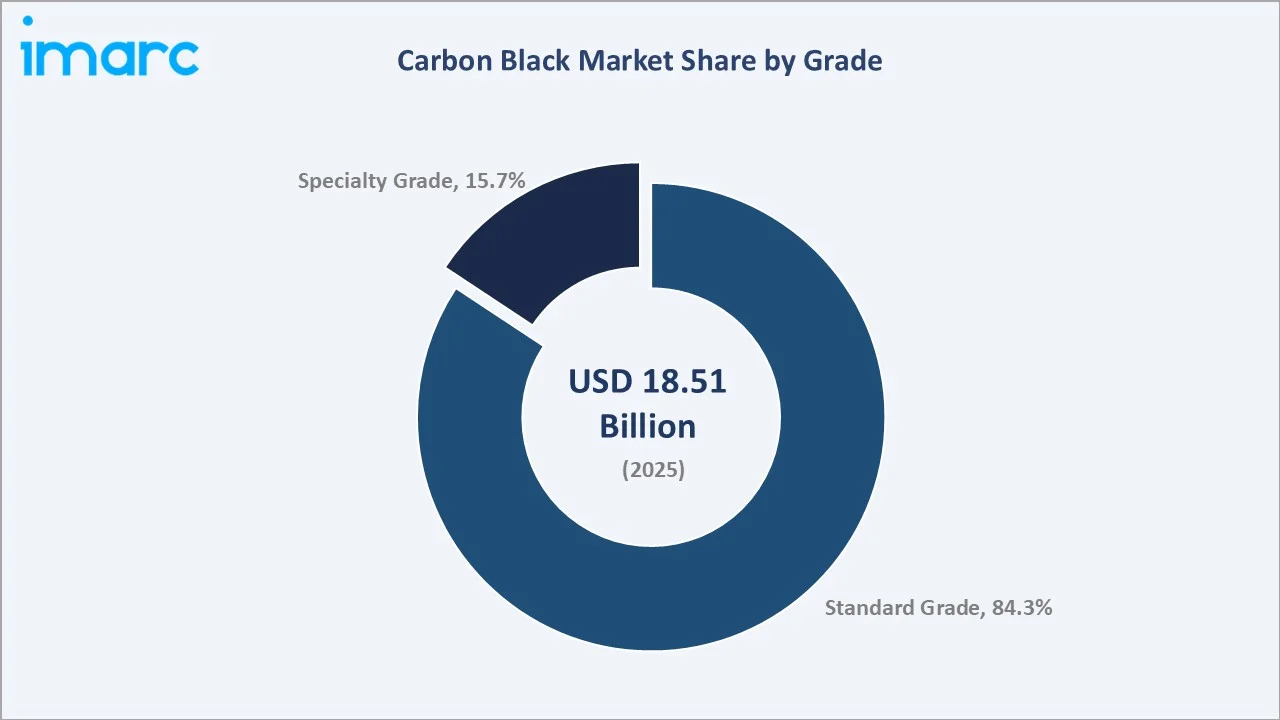

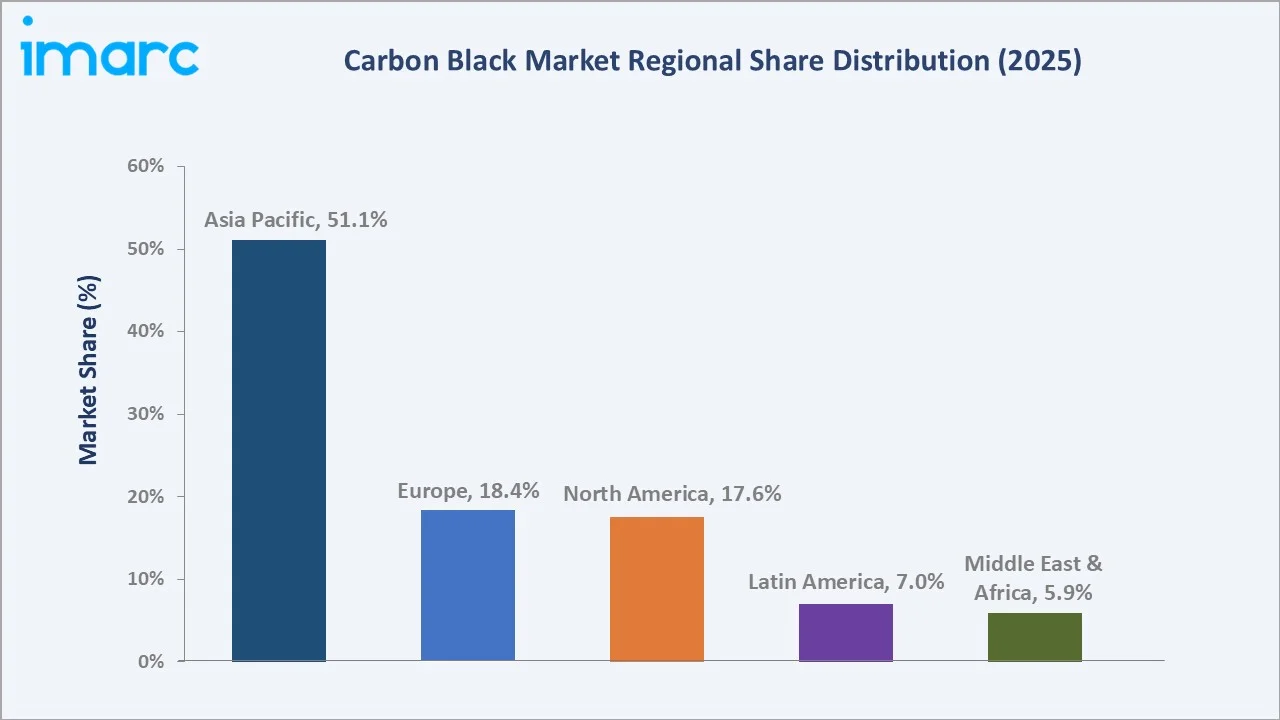

The global carbon black market size was valued at USD 18.51 Billion in 2025 and is projected to reach USD 25.54 Billion by 2034, exhibiting a CAGR of 3.46% during the forecast period 2026-2034. Rising demand from the tire and automotive industry, expanding use across plastics and specialty coatings, rapid scale-up of recovered carbon black (rCB) capacity, and strong industrial growth across the Asia Pacific are driving the carbon black market growth. Furnace Black leads the type segment at 76.6% in 2025, while Standard Grade dominates the grade segment at 84.3%. Asia Pacific accounts for 51.1% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 18.51 Billion |

|

Forecast Market Size (2034) |

USD 25.54 Billion |

|

CAGR (2026-2034) |

3.46% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (51.1% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~4.3%) |

|

Leading Type |

Furnace Black (76.6%, 2025) |

|

Leading Grade |

Standard Grade (84.3%, 2025) |

The global carbon black market growth trajectory from 2020 through 2034 contrasts a steady historical expansion base against a moderated forecast curve anchored by tire demand, specialty grade acceleration, and circular carbon black capacity build-out across the Asia Pacific and Europe.

To get more information on this market, Request Sample

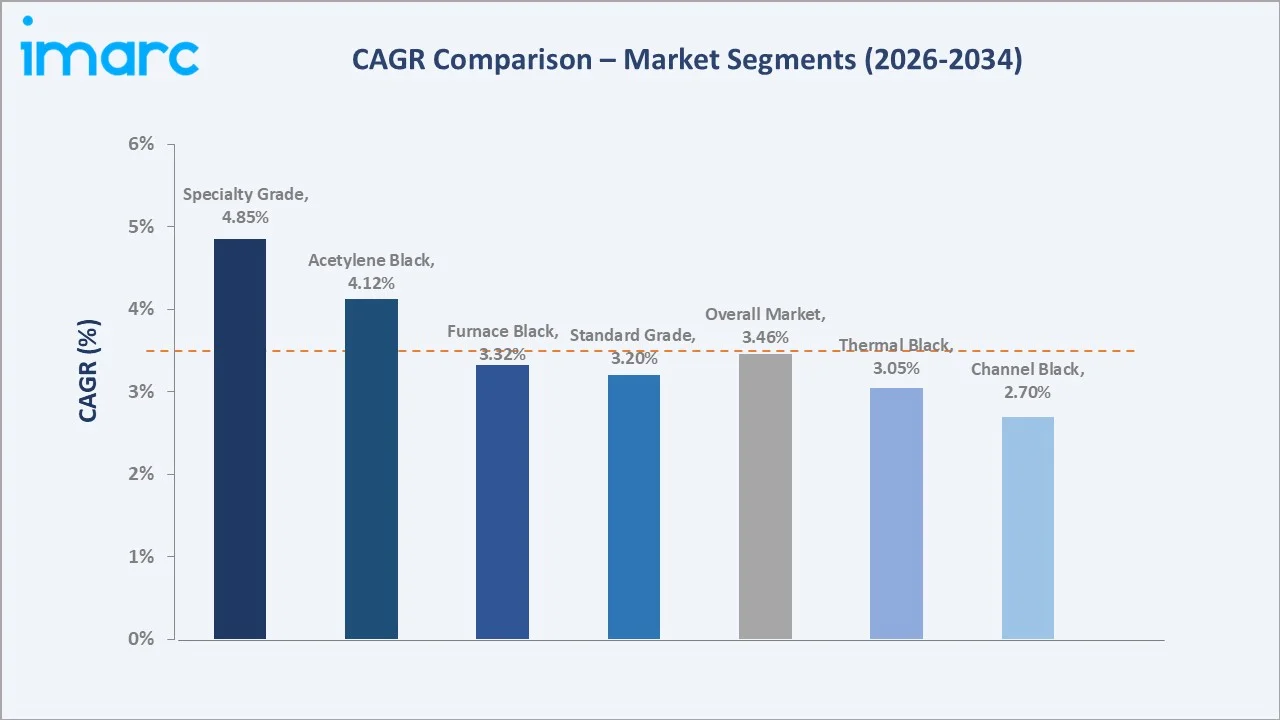

Segment-level CAGR comparison highlights Specialty Grade and Acetylene Black as the two fastest-growing sub-categories within the global carbon black industry analysis through 2034, driven by battery-grade conductive demand and premium coatings applications.

Executive Summary

The global carbon black market is entering a structurally moderate but resilient growth phase, shaped by a mature tire industry, rising specialty grade penetration, and the emergence of circular production pathways. Valued at USD 18.51 Billion in 2025, the market is forecast to reach USD 25.54 Billion by 2034 at a CAGR of 3.46%.

Furnace Black commands the dominant share at 76.6% in 2025, owing to its cost-competitive yield and scalability in high-volume tire and rubber manufacturing. Acetylene Black, though smaller at 6.2%, is the fastest-growing type at ~4.12% CAGR through 2034, fuelled by rising use as a conductive additive in lithium-ion batteries. Standard Grade leads at 84.3%, while Specialty Grade at 15.7% is the faster-growing category, supported by premium pricing in coatings, inks, and battery materials.

Asia Pacific dominates with a 51.1% global revenue share in 2025, led by China's annual output, India's expanding tire cluster, and ASEAN's auto manufacturing base. Europe holds 18.4% and North America 17.6%, with both regions advancing sustainability-led investments in recovered carbon black (rCB).

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Furnace Black – 76.6% share (2025) |

|

Largest Grade |

Standard Grade – 84.3% share (2025) |

|

Leading Region |

Asia Pacific – 51.1% revenue share (2025) |

|

Second Region |

Europe – 18.4% revenue share (2025) |

|

Fastest Growing Type |

Acetylene Black – ~4.12% CAGR (2026-2034) |

|

Top Companies |

Cabot Corporation, Birla Carbon, Orion S.A., RP-Sanjiv Goenka Group, Tokai Carbon Co., Ltd. |

Key Analytical Observations Supporting The Above Data:

- Furnace Black's 76.6% dominance in 2025 reflects process efficiency, scalability, and tight particle-size control in tire-grade production.

- Standard Grade at 84.3% in 2025 is driven by broad applicability across tires, rubber, plastics, and coatings, along with cost advantages and deep supply chain availability.

- Asia Pacific's 51.1% global dominance in 2025 reflects China's 5+ million tonne annual output and India's 28.43 Million vehicle production between April 2023 and March 2024 (Invest India).

- Specialty Grade (15.7%, 2025) is scaling faster due to premium pricing in paints, coatings, inks, and lithium-ion battery conductive additives.

- Recovered carbon black is the defining structural opportunity, with multiple 30,000–50,000 tonne per annum facilities announced across India, Malaysia, and North America in 2024–2026.

Global Carbon Black Market Overview

Carbon black is a fine, powdered form of elemental carbon produced through controlled partial combustion or thermal decomposition of hydrocarbon feedstocks. It is used as a reinforcing filler in rubber goods, a pigment in inks and coatings, a UV stabiliser in plastics, and a conductive additive in batteries and cables.

Applications span tires, non-tire rubber, plastics, inks, coatings, and specialty materials across automotive, construction, and electronics sectors, with tires accounting for the largest end-use share.

Macroeconomic enablers include global vehicle production and rising demand for high-performance materials across the Asia Pacific's expanding industrial base.

Market Dynamics

To evaluate market opportunities, Request Sample

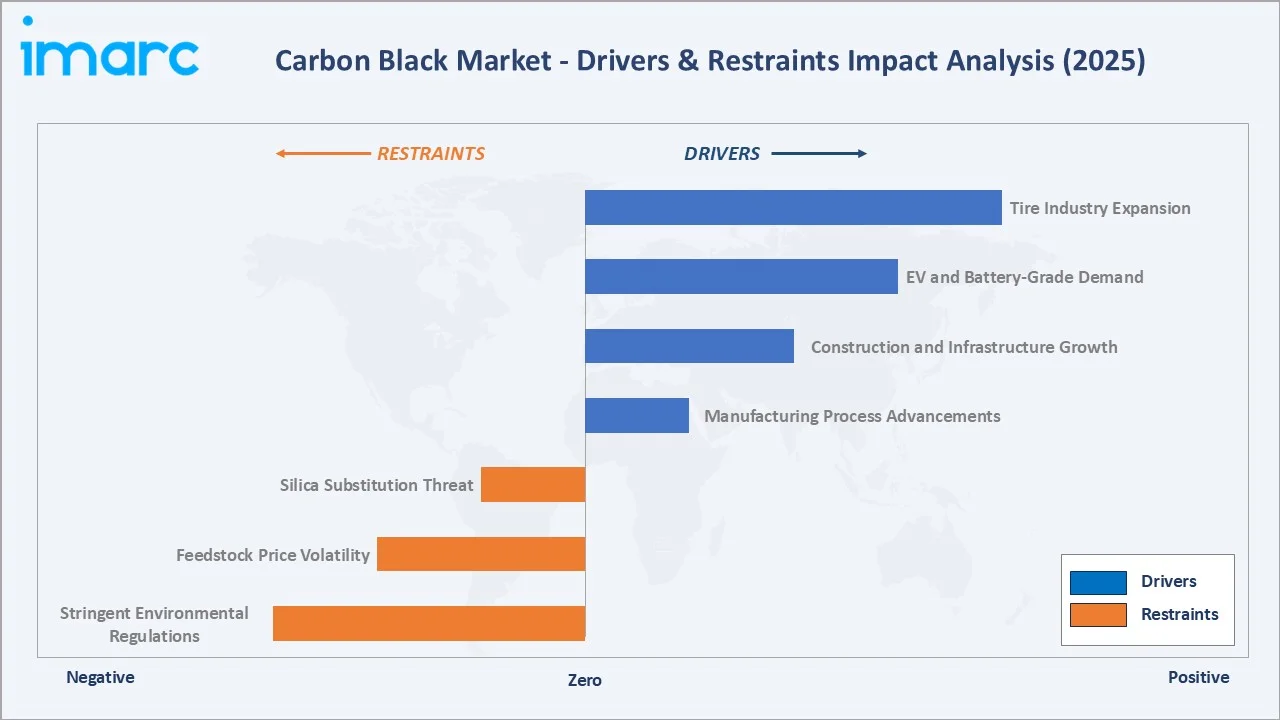

Market Drivers

- Tire Industry Expansion: Carbon black forms roughly 30% of a tire's weight, and global tire output crossed 2.3 Billion units in 2024. Rising personal and commercial vehicle ownership in emerging economies is the single largest volume driver for the carbon black market growth.

- Construction and Infrastructure Growth: Global construction spending is expanding over the next 15 years. Carbon black is used in concrete pigments, roofing membranes, sealants, and cable sheathing, all of which scale with infrastructure investment.

- Manufacturing Process Advancements: Automated process control, improved yield management, and tighter particle-size engineering are lifting production efficiency. Balkrishna Industries expects carbon black to contribute 8–9% of the company's revenue after its new production line ramps up.

- EV and Battery-Grade Demand: Acetylene black and specialty conductive grades are being adopted as conductive additives in lithium-ion cathode and anode formulations, creating incremental demand linked to 17 Million electric car sales in 2024, as reported by the IEA.

Market Restraints

- Stringent Environmental Regulations: Carbon black manufacturing is energy-intensive, emitting CO2 and SOx. The EU Green Deal and tightening US EPA air-quality rules are raising compliance costs and pressuring margins for legacy furnace black producers.

- Feedstock Price Volatility: Furnace black production depends on heavy aromatic oils and coal tar, tracking crude oil prices. Energy price swings in 2022–2024 disrupted producer margins across Europe and North America.

- Silica Substitution Threat: In premium 'green tire' formulations, precipitated silica is increasingly paired with or replaces carbon black for better fuel efficiency, which could moderate carbon black volume growth in passenger car radial tires.

Market Opportunities

- Recovered Carbon Black (rCB) Scaling: In June 2024, CSRC Group and Eco Infinic announced a 30,000 tonne per year rCB facility in North America. Klean Industries separately signed an LOI for four rCB plants across India and Malaysia with a combined 50,000 tonnes per year capacity.

- Battery-Grade Specialty Demand: Acetylene and conductive specialty blacks are emerging as strategic inputs for EV battery cell manufacturers, with premium pricing per tonne versus tire grade and double-digit demand CAGR projected through 2030.

- Capacity Expansion in India: Phillips Carbon Black is building its sixth plant in Naidupeta with up to 450,000 tonnes per year capacity, positioning India as a rising net exporter across the Asia Pacific and Africa.

Market Challenges

- Capital Intensity and Long Payback: New carbon black plants require USD 150–300 Million per line with 6–8 year payback, limiting the pace of capacity additions and favouring incumbents with integrated feedstock access.

- Trade Policy and Tariff Risk: Anti-dumping duties imposed by the EU, US, and India on imports from China and Russia have reshaped global trade flows and created pricing asymmetry across regions.

- Health and Worker Safety Compliance: Carbon black is classified as a Group 2B possible carcinogen by IARC, and evolving occupational exposure limits require continued investment in dust containment and worker monitoring programmes.

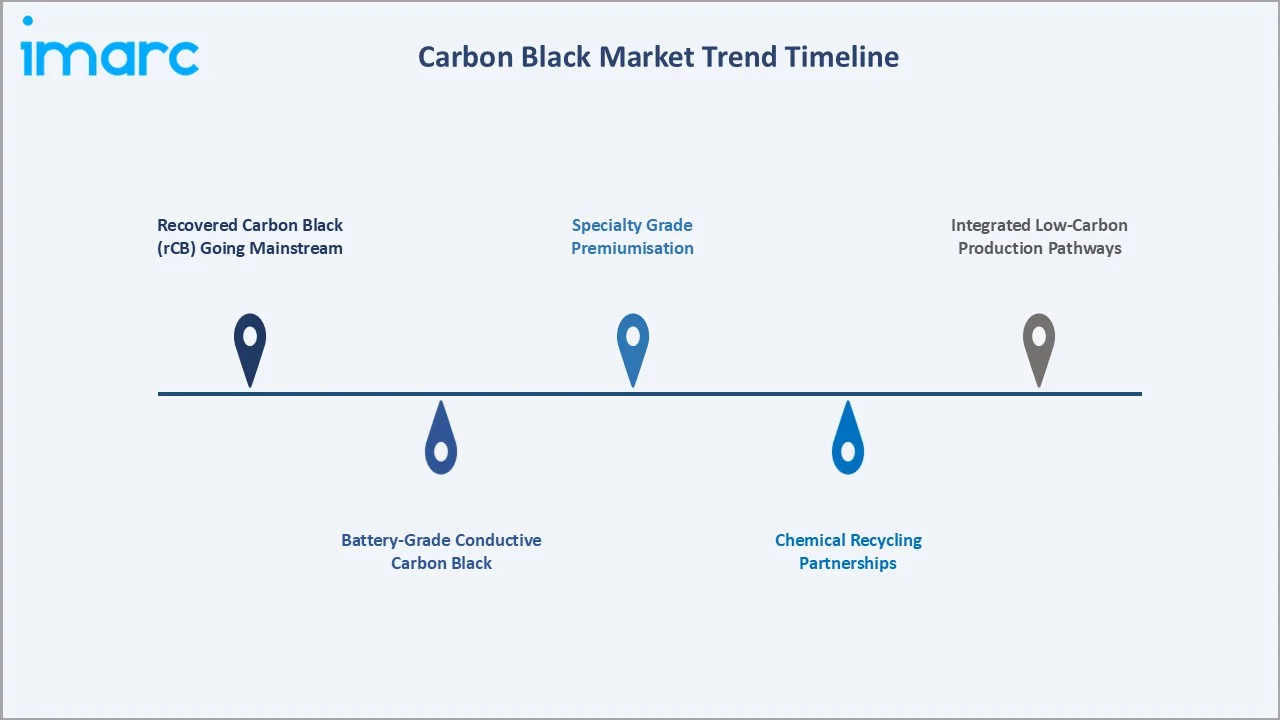

Emerging Market Trends

1. Recovered Carbon Black (rCB) Going Mainstream

rCB produced from end-of-life tire pyrolysis is transitioning from pilot scale to commercial tonnage. Epsilon Carbon launched Terrablack in January 2025 with up to 50% lower Global Warming Potential, positioning rCB for tire and non-tire rubber applications.

2. Battery-Grade Conductive Carbon Black

Acetylene and conductive specialty grades are being reformulated specifically for lithium-ion cell chemistries. Orion S.A. and Cabot have both expanded conductive carbon product lines to target EV battery OEMs in China, South Korea, and the United States.

3. Chemical Recycling Partnerships

In January 2025, Sumitomo Rubber Industries and Mitsubishi Chemical launched the world's first commercial project to recycle carbon black from tire waste via chemical recycling in coke ovens, with the recycled output used in race-car and passenger tires.

4. Specialty Grade Premiumisation

Specialty carbon black, at 15.7% of the market in 2025, commands rising unit economics across printing inks, high-jet coatings, and polymer masterbatches. Epsilon Carbon's N134 hard carbon black, launched in June 2025, illustrates the push into high-abrasion premium tire grades.

5. Integrated Low-Carbon Production Pathways

Producers are investing in waste heat recovery, cogeneration, and green hydrogen pilots to reduce the carbon intensity of furnace black production. Birla Carbon's BC1060 grade, launched in September 2025, was developed alongside sustainability upgrades across its manufacturing base.

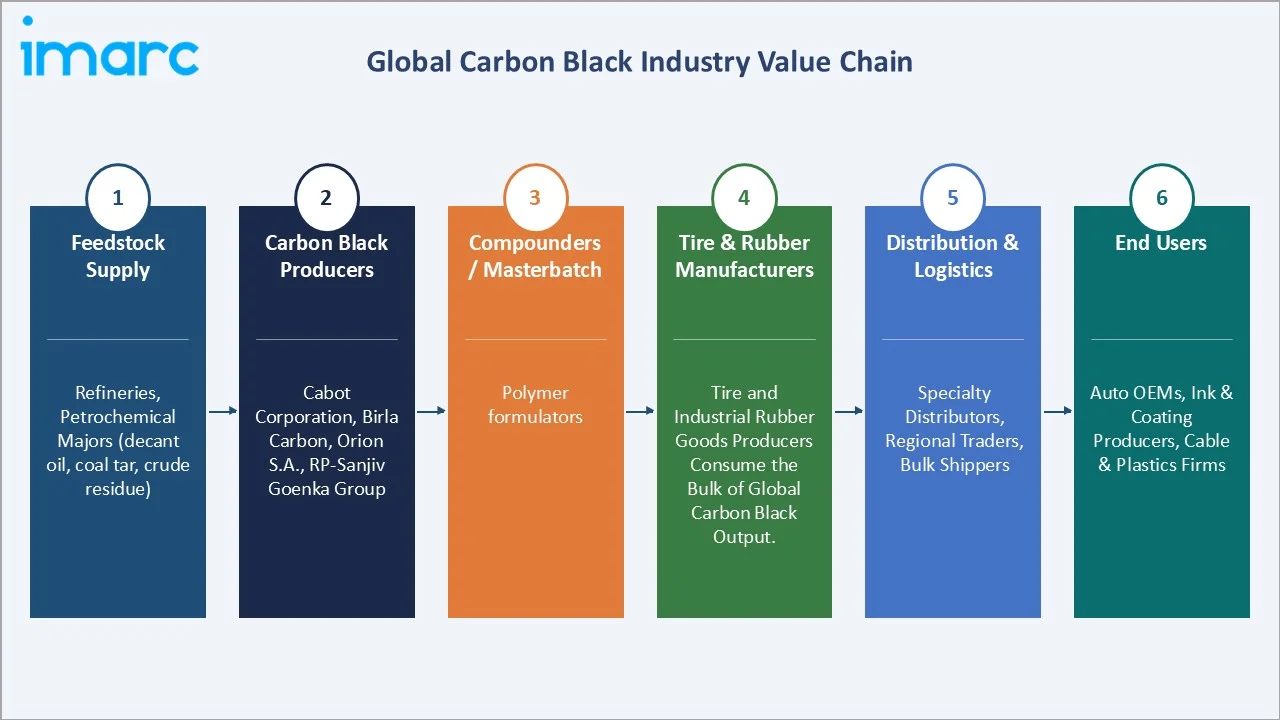

Industry Value Chain Analysis

The carbon black value chain spans six integrated stages from hydrocarbon feedstock supply through end-use integration in tires, rubber, plastics, and coatings. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Feedstock Supply |

Refineries and petrochemical majors supply heavy aromatic residues (decant oil, coal tar, crude residue) that serve as the primary hydrocarbon input for carbon black production. |

|

Carbon Black Producers |

Specialty chemical manufacturers convert feedstock into various grades of carbon black through furnace, thermal, or channel processes, forming the highest-margin tier of the chain. |

|

Compounders / Masterbatch |

Formulators disperse carbon black into polymer carriers and rubber compounds, delivering ready-to-use blends tailored to downstream processing needs. |

|

Tire & Rubber Manufacturers |

Tire and industrial rubber goods producers consume the bulk of global carbon black output, using it as the primary reinforcing filler for strength, wear resistance, and UV protection. |

|

Distribution & Logistics |

Specialty distributors, regional traders, and bulk shippers manage storage, packaging, and last-mile delivery, bridging producers and fragmented end-use buyers. |

|

End Users |

Auto OEMs, packaging converters, ink producers, cable and coatings firms |

Tier-1 producers such as Cabot, Birla Carbon, and Orion S.A. capture the highest margin pools by controlling feedstock contracts, specialty grade portfolios, and downstream OEM relationships. Integrated producers in the Asia Pacific are increasingly capturing additional value by aligning refinery feedstock contracts with carbon black capacity, reducing exposure to feedstock price swings.

Technology Landscape in the Carbon Black Industry

Production Technology and Yield Optimisation

The furnace black process remains the workhorse technology, accounting for over three-quarters of global capacity. Modern units use staged combustion, improved heat recovery, and digital process control to deliver particle-size distributions calibrated for each application tier.

Recovered and Circular Carbon Black

Pyrolysis of end-of-life tires, followed by upgrading of crude char, is producing rCB grades approaching virgin specification quality. Commercial capacity is projected to exceed 500,000 tonnes globally by 2028, up from under 100,000 tonnes in 2024.

Specialty Grade Engineering

Surface treatment, oxidised and pelletised formats, and narrow particle-size control are enabling new specialty use cases in conductive plastics, high-performance coatings, and battery electrodes, where pricing per tonne is 2–4x that of standard tire grade.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Furnace Black |

76.6% |

2025 |

|

Grade |

Standard Grade |

84.3% |

2025 |

|

Application |

Tire |

70.2% |

2025 |

|

Region |

Asia Pacific |

51.1% |

2025 |

By Type

Furnace Black commands a 76.6% majority share in 2025, reflecting its dominance across reinforcing applications in tires, belts, hoses, and industrial rubber goods. The furnace process offers the best combination of yield, particle-size control, and cost per tonne, making it the default choice for high-volume tire manufacturing.

To access detailed market analysis, Request Sample

Thermal Black at 8.4% in 2025 serves specialty rubber goods, mechanical goods, and wire and cable applications requiring a larger particle size and cleanliness. Acetylene Black (6.2%) is the fastest-growing sub-category at ~4.12% CAGR through 2034, supported by its high purity and conductivity, essential for lithium-ion battery electrodes and conductive plastics.

Channel Black (4.3%) retains a niche position in high-jet pigment applications, while the Others category (4.5%) includes lamp black, plasma black, and emerging recovered carbon black, which is scaling rapidly from a small base.

By Grade

Standard Grade dominates at 84.3% in 2025, driven by its broad use in tires, general-purpose rubber, and commodity plastics. Cost-effectiveness, consistent supply, and compatibility with a wide polymer matrix make standard grade the default across tier-1 tire producers globally.

Specialty Grade, at 15.7% in 2025, is the fastest-growing segment at ~4.85% CAGR through 2034. Its expansion is anchored by rising demand in printing inks, high-performance coatings, UV-stable plastics, fibres, and battery-grade conductive additives. Specialty grades command 1.8–3.0x the realised price of standard grades, making them disproportionately important to producer profitability.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

51.1% |

China 5M+ tonne output, India tire cluster, ASEAN auto growth |

|

Europe |

18.4% |

EU Green Deal, EVs at 23% of new registrations, rCB investment |

|

North America |

17.6% |

US tire industry, EV tire grades, coatings, and packaging demand |

|

Latin America |

7.0% |

Brazil and Mexico tire manufacturing, packaging plastics growth |

|

Middle East & Africa |

5.9% |

GCC infrastructure spend, South Africa tire industry, cable demand |

Asia Pacific commands a 51.1% global revenue share in 2025. China is the largest single market, producing over 5 million tonnes of carbon black annually across its tire and plastics sectors. India manufactured 28.43 Million vehicles between April 2023 and March 2024 (Invest India), anchoring downstream demand across passenger and two-wheeler tires. Japan and South Korea contribute significant specialty demand for electronics and battery applications.

Europe, at 18.4% in 2025, is shaped by strong environmental regulation and auto sector demand. The European Automobile Manufacturers Association reports over 13.1 million vehicles produced annually, and EVs represented roughly 23% of new registrations in 2023. Producers are aggressively investing in rCB to comply with the EU Green Deal.

North America holds 17.6% in 2025, anchored by the US tire industry, producing over 9 million cars a year. Latin America (7.0%) is driven by Brazil’s 2.3 million car output in 2023 and expanding industrial demand, supporting strong growth in the Carbon Black Market in Brazil, while the Middle East & Africa (5.9%) is advancing on GCC infrastructure investment and South African automotive assembly.

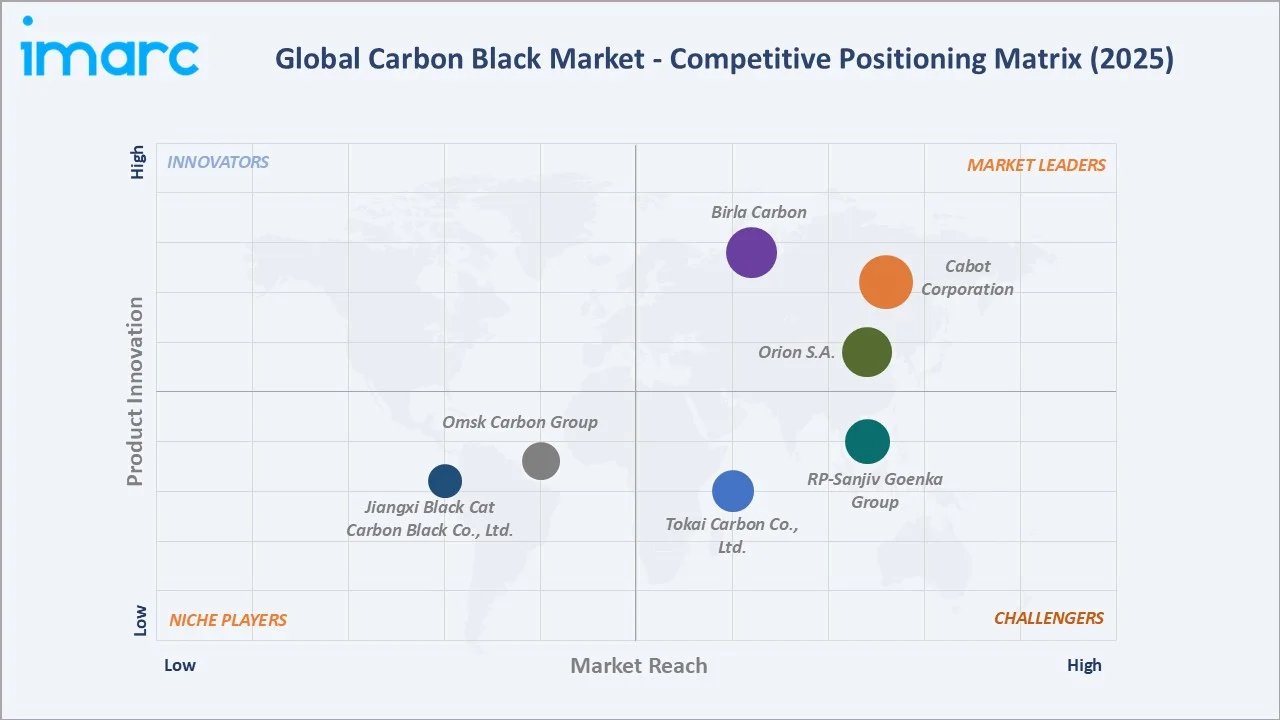

Competitive Landscape

|

Company Name |

Key Brand / Product Line |

Market Position |

Core Strength |

|

Cabot Corporation |

VULCAN |

Leader |

Specialty & conductive grades, global scale |

|

Birla Carbon |

Raven, Conductex |

Leader |

Integrated India base, global plants, rubber grades |

|

Orion S.A. |

HIBLACK |

Leader |

Specialty leader, battery & coatings focus |

|

RP-Sanjiv Goenka Group |

Rubber Black, Specialty Black |

Challenger |

India capacity, specialty pivot, exports |

|

Tokai Carbon Co., Ltd. |

SEAST, TOKABLACK |

Challenger |

Japan/Asia rubber grades, electronics supply |

|

Omsk Carbon Group |

Omcarb |

Emerging |

Russia-based high-volume furnace black |

|

Jiangxi Black Cat Carbon Black Co., Ltd. |

Black Cat |

Challenger |

Largest Chinese producer, APAC exports |

The global carbon black competitive landscape is characterised by a moderately consolidated structure, with a handful of global Tier-1 producers commanding deep OEM relationships alongside ambitious Chinese domestic producers gaining share in the Asia Pacific. Competitive dynamics are shifting from pure cost leadership to a mix of sustainability credentials, specialty portfolio depth, and regional capacity positioning.

Key Company Profiles

Cabot Corporation

Headquartered in Boston, Massachusetts, Cabot Corporation is one of the largest global carbon black producers, with operations across the Americas, Europe, Asia Pacific, and the Middle East.

- Product & Platform Portfolio: VULCAN, REGAL, BLACK PEARLS, ELFTEX, and MONARCH grades covering tires, rubber, plastics, inks, and specialty conductive applications.

- Recent Developments: In February 2026, Cabot Corporation announced that it had completed its acquisition of Mexico Carbon Manufacturing S.A. de C.V. (MXCB) from Bridgestone Corporation. The transaction follows the announcement of a definitive agreement in August and the receipt of required regulatory approvals.

- Strategic Focus: Cabot's strategy centres on specialty premiumisation, battery materials growth, and selective capacity investments that reinforce its leadership in high-value specialty grades serving Asian and US EV cell manufacturers.

Birla Carbon

Birla Carbon, part of the Aditya Birla Group, is one of the world's largest carbon black producers with 16 manufacturing sites across 12 countries.

- Product & Platform Portfolio: Raven, Conductex, and BC1060 grades spanning tire reinforcement, specialty rubber, inks, plastics, and conductive applications.

- Recent Developments: In September 2025, Birla Carbon launched BC1060 at RubberTech 2025 in Shanghai, a low-hysteresis grade optimised for anti-vibration and sealing components in tire and non-tire applications.

- Strategic Focus: Birla Carbon's strategy rests on three pillars: capacity expansion across India and ASEAN, specialty and conductive grade growth, and sustainability-led investments in waste heat recovery and circular production pathways.

Orion S.A.

Orion S.A. is a global specialty carbon black leader headquartered in Luxembourg, with plants across Europe, the Americas, and Asia.

- Product & Platform Portfolio: PRINTEX, HIBLACK, XPB, and conductive specialty grades targeting coatings, printing inks, polymers, and battery applications.

- Recent Developments: In November 2025, Orion S.A. is expanding its business by providing conductive additives for high-voltage cable compounds and battery energy storage systems (BESS).

- Strategic Focus: Orion's strategy lies in specialty mix shift and leadership in battery-grade materials, where pricing and margins outpace standard tire grades, backed by continued R&D investment in high-purity conductive blacks.

Market Concentration Analysis

The global carbon black market is moderately concentrated. The top 5 producers—Cabot Corporation, Birla Carbon, Orion S.A., RP-Sanjiv Goenka Group, Tokai Carbon Co., Ltd.—collectively account for 45–52% of global market revenue in 2025. Chinese producers led by Anhui Black Cat and Jiangxi Black Cat form a second tier with significant regional dominance, particularly within the Asia Pacific.

Fragmentation remains higher at the regional level, especially across the Asia Pacific, where more than 40 mid-sized producers operate across India, China, and ASEAN. Consolidation is expected to accelerate through 2030 as sustainability compliance costs rise and sub-scale assets become uneconomical.

Investment & Growth Opportunities

Fastest-Growing Segments

Specialty Grade carbon black is the highest-growth category at ~4.85% CAGR through 2034, driven by premium pricing in coatings, inks, and battery conductive additives. Acetylene Black follows at ~4.12% CAGR, closely linked to EV battery demand scale-up.

Emerging Market Expansion

India is the single most attractive greenfield destination, with Phillips Carbon Black's announcement of a 450,000 tonnes per year capacity facility in Naidupeta, Andhra Pradesh. Southeast Asia and the Middle East are seeing selective investment tied to downstream tire and plastics clusters.

Venture & Private Investment Trends

Private capital and strategic investors are focused on three themes: recovered carbon black platforms, specialty and conductive grade expansions, and low-carbon production retrofits. Klean Industries' rCB LOI across India and Malaysia, and CSRC–Eco Infinic's North American rCB facility illustrate the scale-up of circular carbon black investment activity.

Future Market Outlook (2026-2034)

The global carbon black market forecast projects steady expansion from USD 18.51 Billion in 2025 to USD 25.54 Billion by 2034 at a CAGR of 3.46%. Volume growth will be underpinned by tire demand in the Asia Pacific, while value accretion will come from mix shift toward specialty grades, premiumisation in coatings and inks, and scale-up of battery-grade conductive carbon.

Three structural shifts are likely to reshape the market through 2034. First, recovered carbon black capacity will expand from under 100,000 tonnes in 2024 to more than 500,000 tonnes by 2028, driven by EU and India regulatory tailwinds. Second, battery-grade carbon black will emerge as a high-margin growth pool linked to EV cell manufacturing scale-up in China, South Korea, and the United States. Third, sustainability-led production retrofits will redefine industry cost curves, rewarding integrated producers with decarbonised processes and penalising sub-scale legacy assets.

Research Methodology

Primary Research

Primary research included structured interviews with carbon black producers, tire and rubber compounders, specialty ink and coating formulators, EV battery cell manufacturers, and trade body representatives across Asia Pacific, Europe, and North America. Insights were used to validate market sizing, segment shares, pricing benchmarks, and competitive positioning.

Secondary Research

Secondary research drew from the International Energy Agency (IEA) EV outlook, Asian Development Outlook 2024, European Automobile Manufacturers Association, European Environmental Agency, Invest India, company annual reports of Cabot, Birla Carbon, Orion S.A., PCBL, and Tokai Carbon, and trade publications covering rubber, plastics, and coatings.

Forecasting Models

Market sizing and forecasts were developed using combined top-down and bottom-up approaches, triangulating tire production volumes, plastics output, ink and coating demand, and battery-grade carbon uptake. Base, optimistic, and conservative scenarios were run to reflect crude oil price volatility, EV adoption pace, and rCB capacity deployment uncertainty.

Carbon Black Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Furnace Black, Channel Black, Thermal Black, Acetylene Black, Others |

| Grades Covered | Standard Grade, Specialty Grade |

| Applications Covered | Tire, Non-Tire Rubber, Plastics, Inks and Coatings, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Cabot Corporation, Birla Carbon, Orion S.A., RP-Sanjiv Goenka Group, Tokai Carbon Co., Ltd., Omsk Carbon Group, Jiangxi Black Cat Carbon Black Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the carbon black market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global carbon black market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the carbon black industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Carbon Black Market Report

The global carbon black market was valued at USD 18.51 Billion in 2025, driven by tire demand, plastics, specialty coatings, and rising battery-grade applications.

The market is projected to reach USD 25.54 Billion by 2034, growing at a CAGR of 3.46% during 2026-2034, driven by specialty grades and circular carbon black capacity.

Furnace Black leads with a 76.6% share in 2025, supported by cost efficiency, scalability, and its dominance in tire and rubber reinforcement applications.

Standard Grade dominates with an 84.3% share in 2025, driven by broad usage in tires, rubber, and plastics, along with cost-effective production and reliable global supply.

Asia Pacific leads with a 51.1% share in 2025, anchored by China's massive production base, India's tire cluster, and strong industrial growth across ASEAN and Northeast Asia.

Key drivers include tire industry expansion, construction activity, EV and battery demand, specialty grade premiumisation, and circular pathways via recovered carbon black.

Specialty Grade is the fastest-growing at ~4.85% CAGR through 2034, led by coatings, inks, high-performance plastics, and lithium-ion battery conductive additive applications.

Leading companies include Cabot Corporation, Birla Carbon, Orion S.A., RP-Sanjiv Goenka Group, Tokai Carbon Co., Ltd., Omsk Carbon Group, and Jiangxi Black Cat Carbon Black Co., Ltd.

Recovered carbon black, produced from end-of-life tire pyrolysis, is scaling rapidly and offers up to 50% lower Global Warming Potential, aligning with sustainability regulations.

EV adoption is boosting demand for acetylene and specialty conductive carbon black used in lithium-ion battery electrodes, while EV tires require premium reinforcing carbon black.

Challenges include feedstock price volatility, tightening environmental regulations, high capital intensity, trade tariffs, and occupational health compliance requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)