Catalyst Market Size, Share, Trends and Forecast by Type, Process, Raw Material, Application, and Region, 2026-2034

Global Catalyst Market Size, Share, Trends & Forecast (2026-2034)

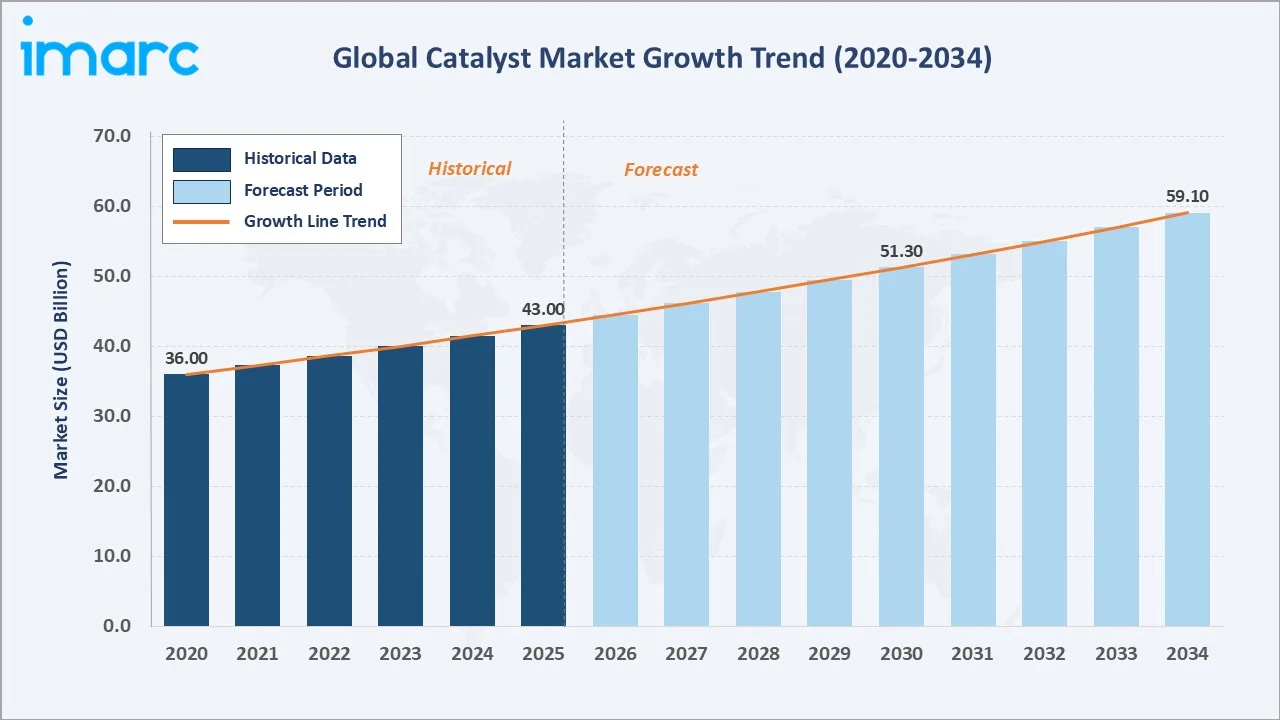

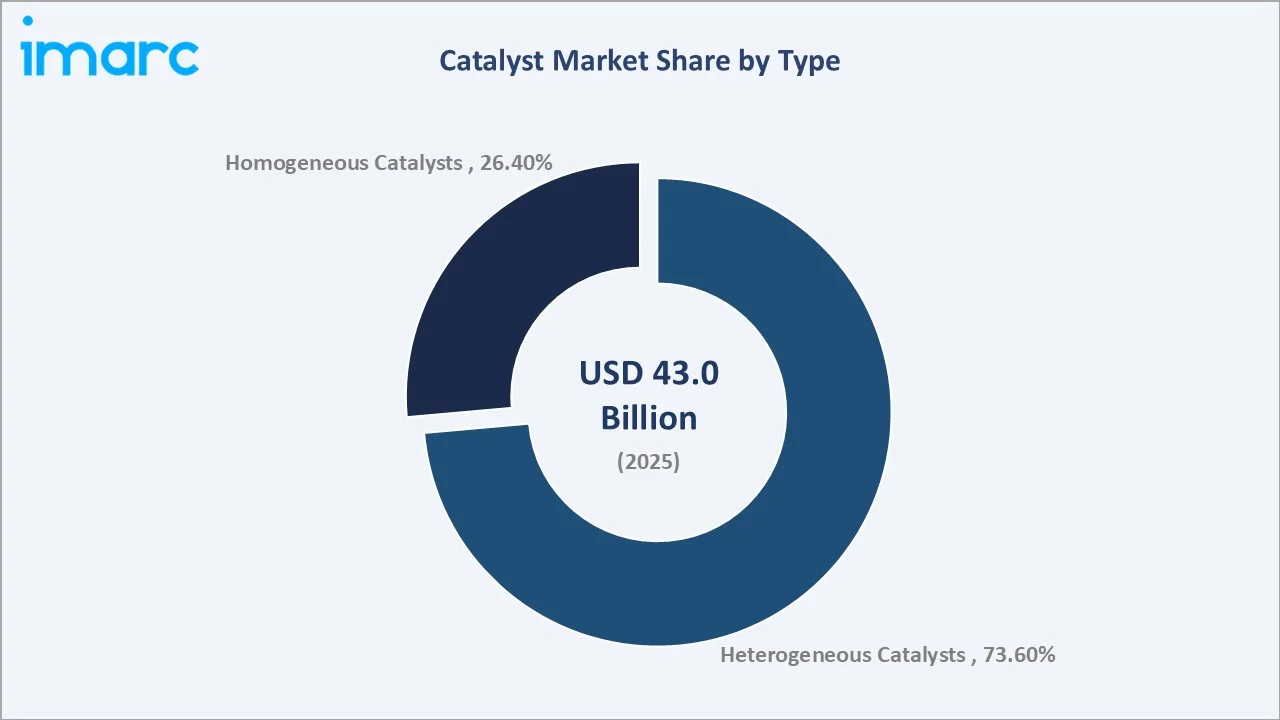

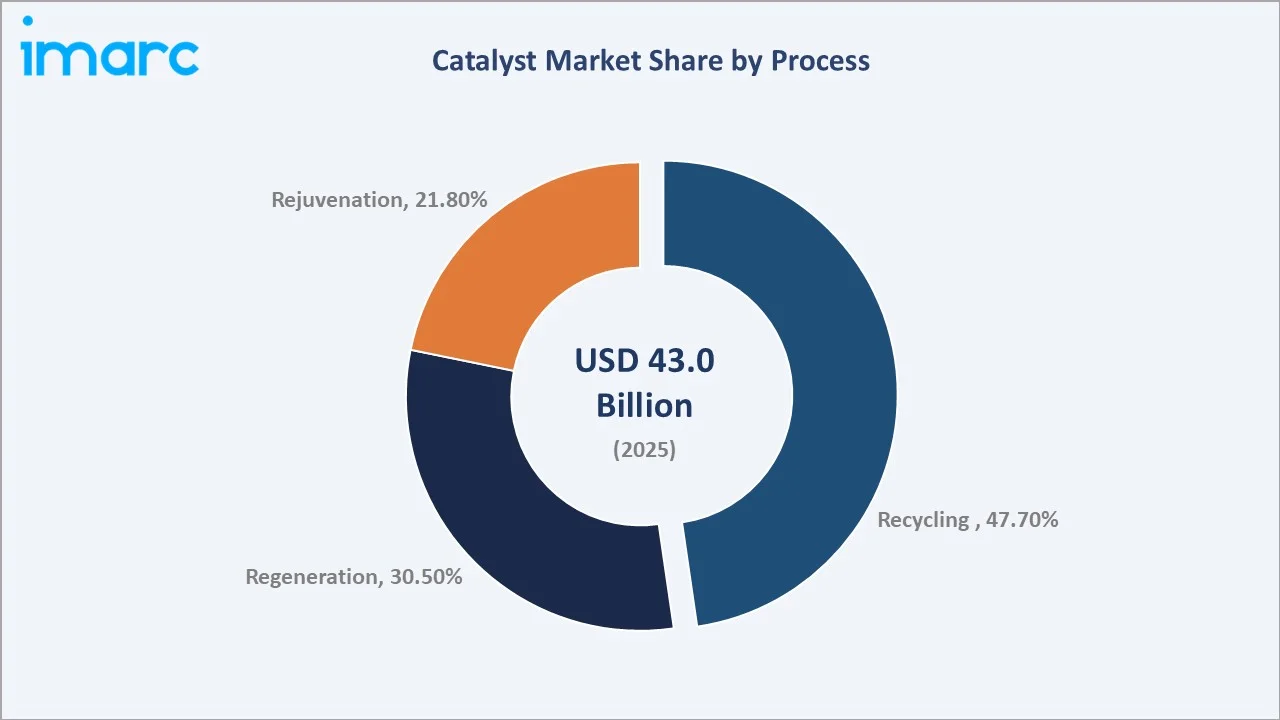

The global catalyst market size was valued at USD 43.0 Billion in 2025 and is projected to reach USD 59.1 Billion by 2034, exhibiting a CAGR of 3.6% during the forecast period 2026-2034. Rising demand from petroleum refining, chemical synthesis, and environmental emission control is fuelling sustained catalyst market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 43.0 Billion |

|

Forecast Market Size (2034) |

USD 59.1 Billion |

|

CAGR (2026-2034) |

3.6% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

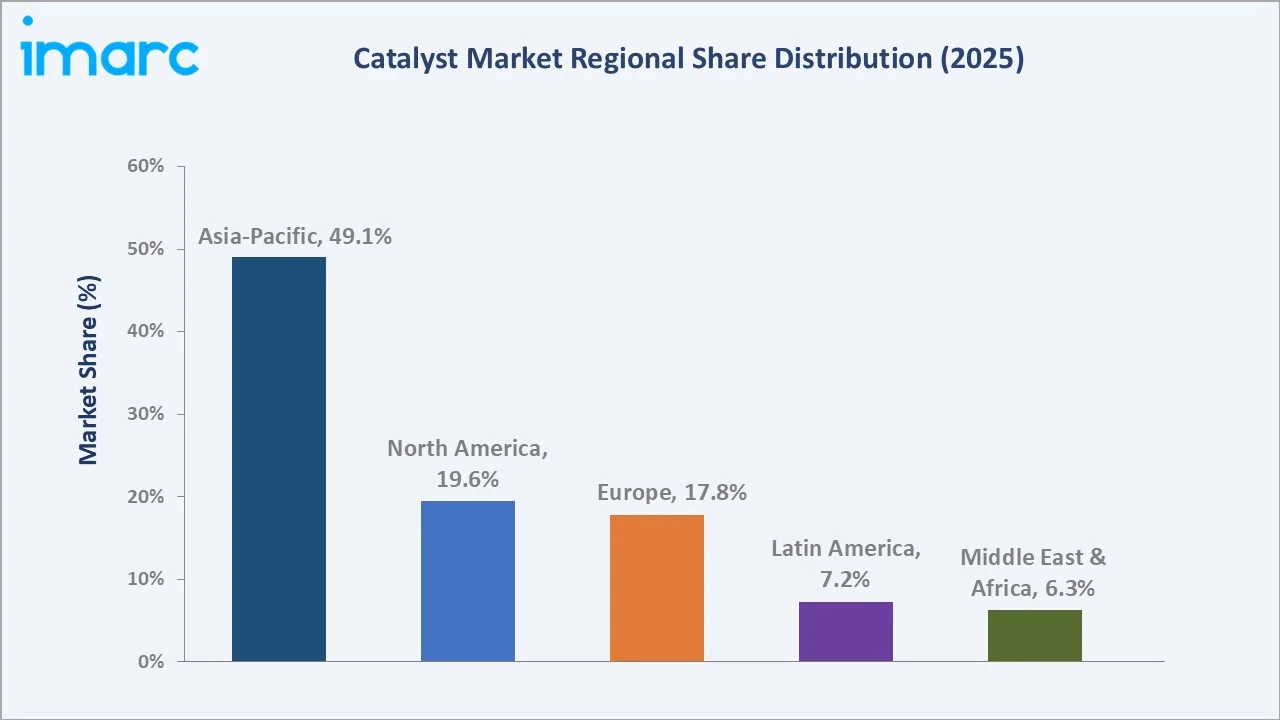

Largest Region |

Asia-Pacific (49.1% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (~4.2% CAGR) |

|

Leading Type |

Heterogeneous Catalyst (73.6%, 2025) |

|

Leading Process Segment |

Recycling (47.7%, 2025) |

The catalyst market growth trajectory from 2020 through 2034 contrasts stable historical expansion USD 36.0 Billion in 2020 rising to USD 43.0 Billion in 2025 against a sustained forecast curve powered by industrial output growth and environmental compliance requirements globally.

To get more information on this market, Request Sample

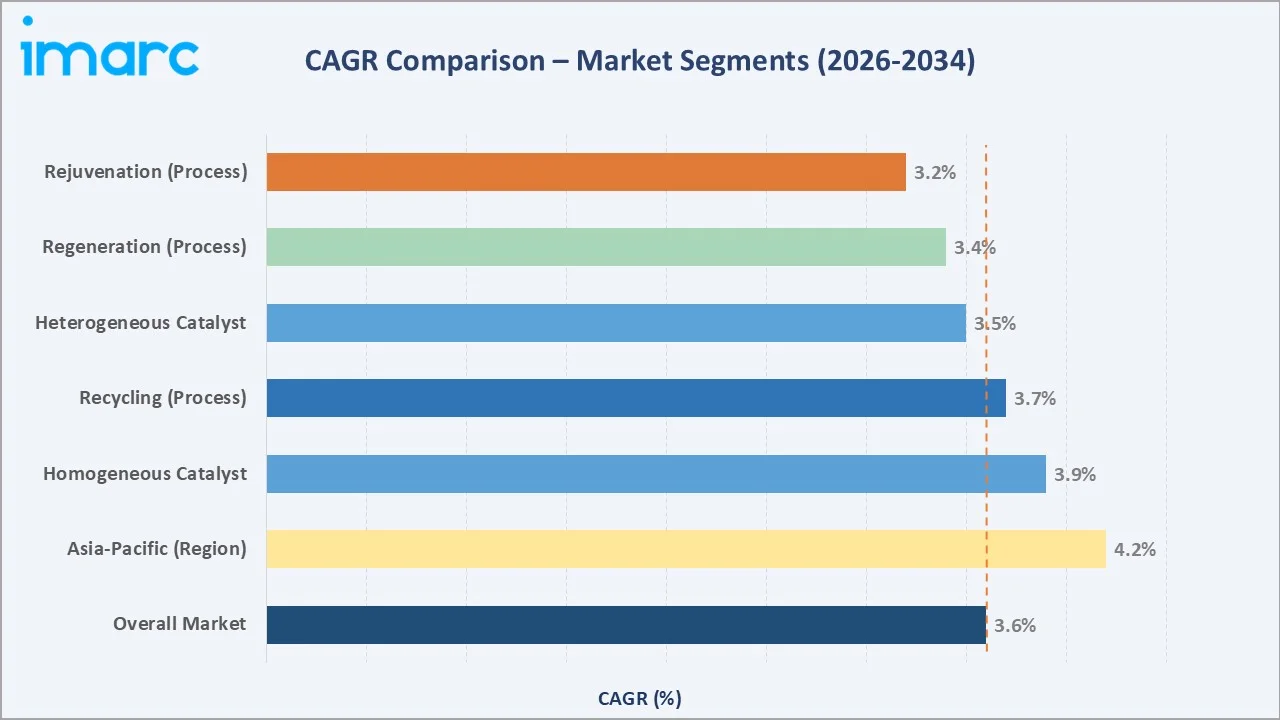

Segment-level CAGR comparisons highlight Asia-Pacific (4.2%) and homogeneous catalysts (3.9%) as the fastest-growing sub-categories within the global catalyst market forecast through 2034, driven by specialty chemical innovation and tightening emission mandates.

Executive Summary

The global catalyst market is undergoing a structural transformation driven by industrial expansion, tightening environmental regulations, and accelerating demand for cleaner production processes. Valued at USD 43.0 Billion in 2025, the market is forecast to reach USD 59.1 Billion by 2034 at a CAGR of 3.6%. Catalysts are indispensable across petroleum refining, chemical synthesis, polymer manufacturing, and emission control applications.

Heterogeneous catalysts command 73.6% share in 2025, benefiting from ease of separation and recyclability advantages in large-scale industrial processes. The recycling segment leads with 47.7% process share, reflecting the industry-wide focus on cost reduction and circular economy principles. Regeneration holds 30.5% and rejuvenation 21.8%, underscoring the shift toward catalyst lifecycle management.

Asia-Pacific commands 49.1% of global revenue in 2025. North America holds 19.6% and Europe 17.8%. The catalyst market outlook remains positive as green chemistry adoption, environmental compliance frameworks, and emerging-market industrialization converge to sustain demand across all major segments through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Heterogeneous Catalyst – 73.6% share (2025) |

|

Second Type |

Homogeneous Catalyst – 26.4% share (2025) |

|

Largest Process |

Recycling – 47.7% share (2025) |

|

Second Process |

Regeneration – 30.5% share (2025) |

|

Leading Region |

Asia-Pacific – 49.1% revenue share (2025) |

|

Top Companies |

BASF, Clariant, Johnson Matthey, Honeywell UOP, Evonik |

|

Market Opportunity |

Green & bio-based catalysts for net-zero industrial processes |

Key Analytical Observations Supporting The Above Data:

- Heterogeneous Catalyst’s 73.6% dominance in 2025 reflects scalability advantages of fixed-bed and fluid catalytic cracking (FCC) systems used across global petroleum refining and polymerization applications.

- Homogeneous Catalyst’s 26.4% share is driven by specialty chemical synthesis, pharmaceutical manufacturing, and fine-chemical applications requiring precise selectivity and mild operating conditions.

- Recycling’s 47.7% process majority reflects cost-efficiency imperatives in refinery operations, where recovered precious metals (platinum, palladium, rhodium) yield significant economic value and reduce raw material dependency.

- Asia-Pacific’s 49.1% global dominance reflects China’s position as the world’s largest refinery and chemical producer, combined with India’s rapid industrial capacity expansion under national refinery modernization programs. This is further reinforced by China’s chemical and pharmaceutical industry, which generated over €2.9 trillion in sales in 2024 and accounted for 41% of the global market.

- Green catalyst innovation represents the primary long-term growth frontier, with EU Green Deal mandates, U.S. Inflation Reduction Act incentives, and carbon-neutral industrial targets driving R&D investment toward novel bio-catalytic and photocatalytic solutions.

Global Catalyst Market Overview

Catalysts are substances that accelerate chemical reactions without being consumed, playing a foundational role in refining, chemical, pharmaceutical, polymer, and environmental sectors. The global market encompasses heterogeneous and homogeneous catalyst categories, serving applications from fluid catalytic cracking (FCC) in petroleum refining to selective catalytic reduction (SCR) in emission control.

The industry operates at the intersection of energy transition, environmental regulation, and industrial productivity. Macro drivers include growing hydrocarbon processing volumes in developing economies, tightening emission standards globally, and accelerating investment in bio-based and green hydrogen production. These forces collectively shape catalyst market trends across all major segments and geographies through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

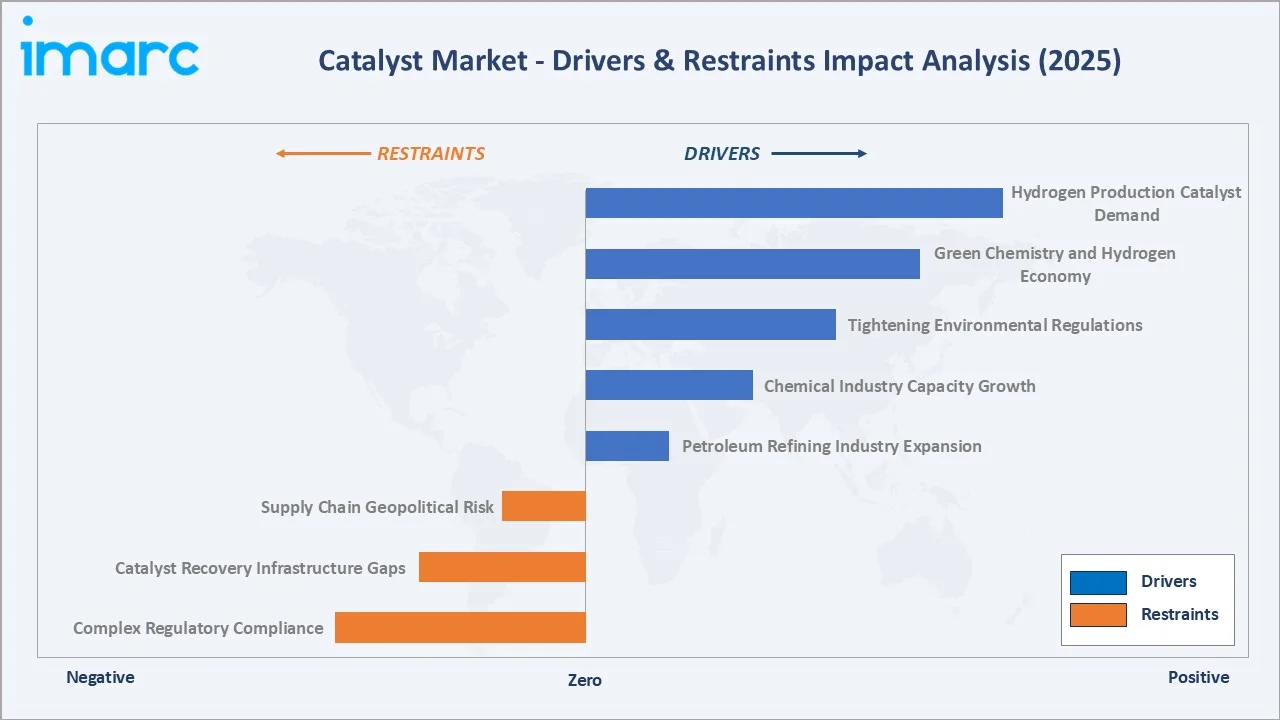

Market Drivers

- Petroleum Refining Industry Expansion: The capacity of the global oil refining sector contracted by 350000 barrels per day in the second quarter of 2025. FCC and hydroprocessing catalysts remain essential in meeting fuel quality mandates, driving sustained demand across Asia-Pacific and Middle Eastern refinery expansions.

- Chemical Industry Capacity Growth: The global chemical industry contribution exceeded USD 5.7 Trillion in 2024. Catalyst consumption for polymerization, ammonia synthesis, methanol production, and specialty chemicals continues to grow in tandem with rising capacity installations, especially in China and India.

- Tightening Environmental Regulations: Euro 7 standards in Europe, EPA Tier 3 norms in the U.S., and China VI emission regulations mandate adoption of advanced automotive and industrial catalysts, structurally driving volume demand for SCR, three-way catalysts (TWC), and diesel oxidation catalysts (DOC).

- Green Chemistry and Hydrogen Economy: Investments in green hydrogen production via electrolysis, bio-based chemical synthesis, and carbon capture are creating new catalyst application frontiers. Global green hydrogen capacity is targeted to reach 40 GW by 2030 under EU hydrogen strategy commitments.

Market Restraints

- Complex Regulatory Compliance: REACH regulations in Europe and TSCA amendments in the U.S. impose extensive testing requirements for novel catalyst formulations. Approval timelines of 2–5 years for new catalyst chemistries slow innovation cycles and raise market entry barriers.

- Catalyst Recovery Infrastructure Gaps: Recovering and regenerating catalysts from complex industrial streams requires advanced infrastructure. Insufficient recycling capacity in emerging markets limits circular economy benefits and increases total cost of catalyst ownership.

Market Opportunities

- Hydrogen Production Catalyst Demand: The global hydrogen economy is attracting USD 500+ Billion in committed investments through 2030. Electrolysis catalysts, methane reforming catalysts, and Fischer–Tropsch synthesis catalysts represent high-growth segments within the green energy transition.

- Emerging Market Refinery Buildouts: India’s refining capacity expansion targeting 310 MMTPA by 2030 alongside Southeast Asian petrochemical complex buildouts will generate sustained multi-year procurement demand for FCC, hydrocracking, and reforming catalysts.

- Biocatalysis and Enzyme Markets: Bio-based and enzyme catalysis applications in pharmaceutical synthesis, biodiesel production, and sustainable chemistry are expanding at double-digit rates, offering premium-priced product opportunities for specialty catalyst manufacturers.

Market Challenges

- Supply Chain Geopolitical Risk: The concentration of platinum-group metal mining in South Africa (~80% of global platinum) and Russia creates supply security vulnerabilities as emission control catalyst demand continues to grow globally.

- Technical Complexity and Customization: Each industrial application demands highly specific catalyst formulations and lifecycle management protocols. Customization costs limit scalability and challenge manufacturers seeking to serve diverse refinery and chemical plant requirements profitably.

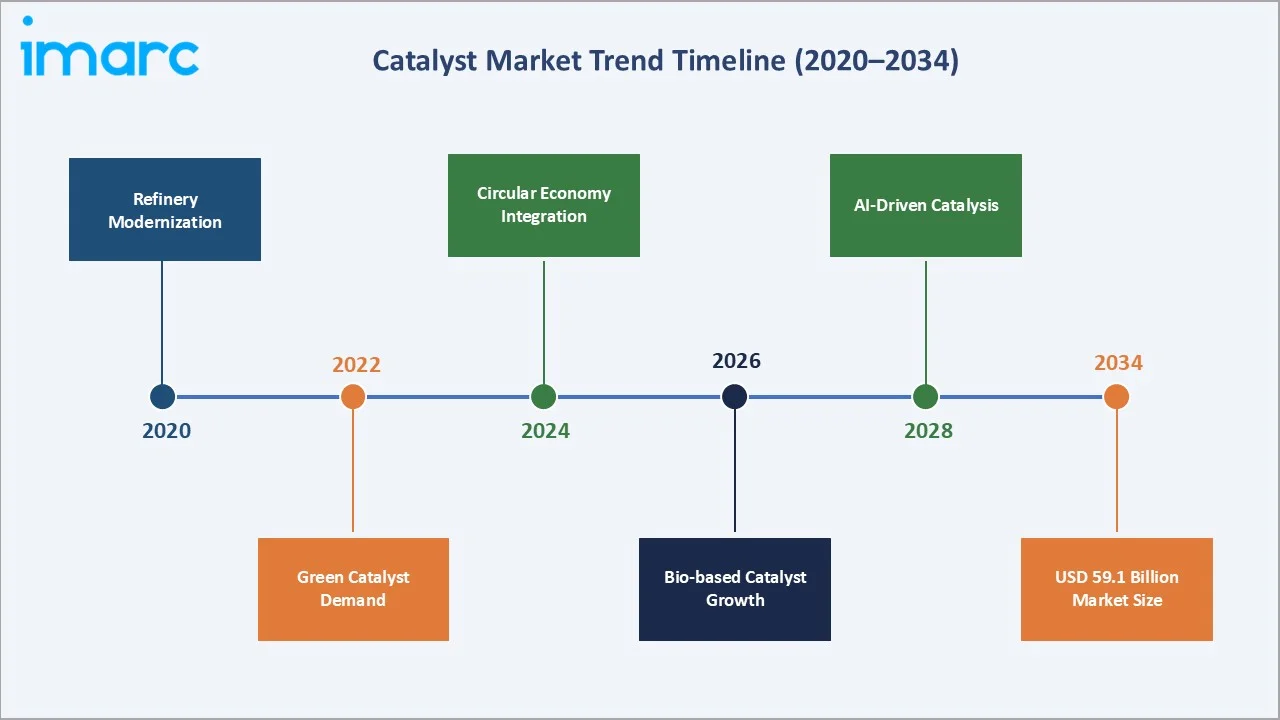

Emerging Market Trends

Figure 4: Catalyst Market – Key Trend Timeline (2020–2034)

1. Accelerating Green and Sustainable Catalyst Adoption

Environmental mandates and corporate net-zero commitments are propelling demand for bio-based, photocatalytic, and enzyme-based catalysts. The European Green aims to cut emissions by at least 55% by 2030, directly incentivizing green catalyst R&D. Manufacturers are investing in low-toxicity, earth-abundant metal catalysts as alternatives to precious-metal-dependent formulations.

2. Circular Economy and Catalyst Recycling Integration

Recycling commands 47.7% process share in 2025, driven by economic and environmental imperatives to recover precious metals from spent catalysts. Advanced hydrometallurgical recovery processes are being industrialized, recovering PGMs with >95% efficiency. The circular catalyst economy is reshaping total cost of ownership models across refinery and chemical applications.

3. Digital Catalyst Optimization and AI Integration

Artificial intelligence and machine learning are transforming catalyst design and process optimization. Computational chemistry tools are accelerating discovery of novel formulations by screening millions of molecular configurations virtually, reducing lab-to-plant timelines by 30–50%. Real-time IoT-sensor monitoring is enabling predictive maintenance and optimal regeneration scheduling in refinery environments.

4. Hydrogen Economy Catalyst Innovation

Proton exchange membrane (PEM) and alkaline electrolyzer catalysts are a primary focus of global innovation investment. Iridium-based anode catalysts remain a bottleneck due to iridium scarcity; multiple manufacturers are developing iridium-reduced alternatives targeting 2026–2028 commercialization windows.

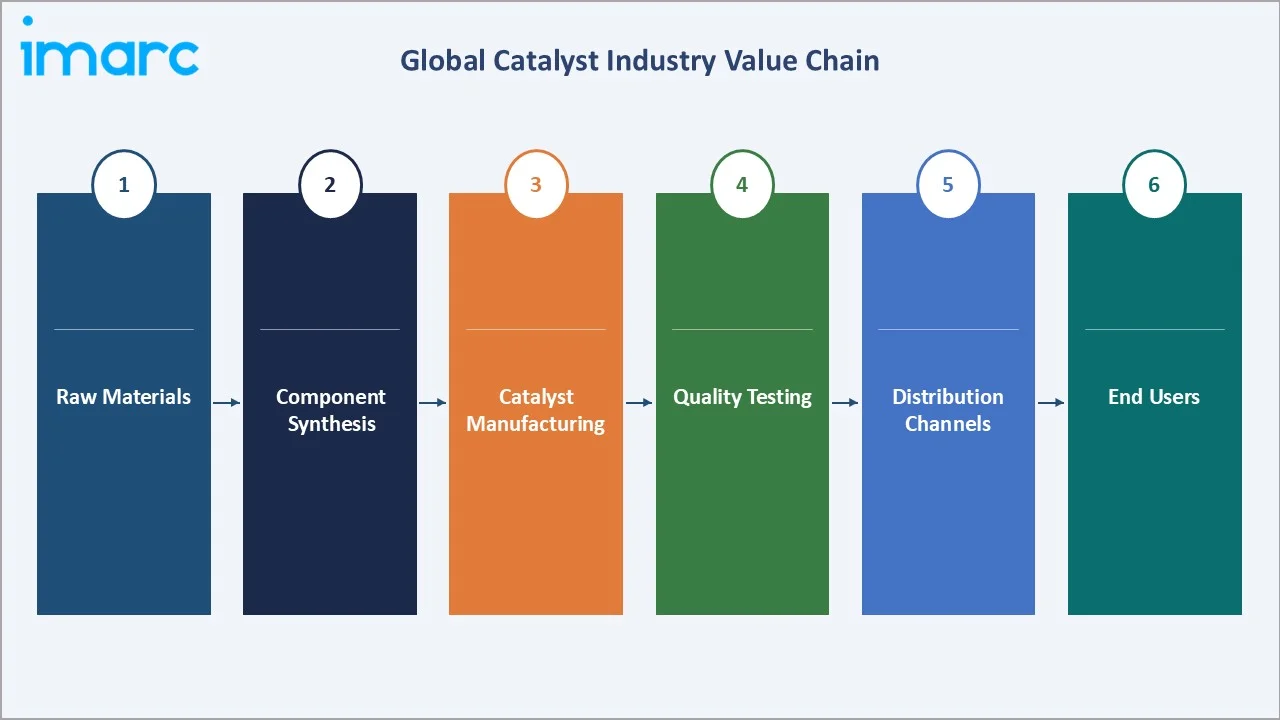

Industry Value Chain Analysis

The global catalyst industry value chain spans six integrated stages from raw material supply through end-user application. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements relevant to overall catalyst market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Platinum-group metals (South Africa, Russia), rare earth elements (China), alumina, silica, zeolites, and transition metal oxides sourced globally |

|

Component Synthesis |

Precursor chemical suppliers synthesizing active metal compounds, support materials, and promoter elements – concentrated in Germany, USA, Japan, and China |

|

Catalyst Manufacturing |

BASF, Clariant, Johnson Matthey, Honeywell UOP, Evonik – full-formulation production, quality testing, and custom catalyst engineering |

|

Technology Integration |

Process engineering firms integrating catalyst systems into FCC units, hydrotreating reactors, and SCR emission control systems |

|

Distribution Channels |

Direct sales to refineries and chemical plants (~68% share), specialty distributors, and catalyst service companies managing regeneration contracts |

|

End Users |

Petroleum refineries, petrochemical complexes, pharmaceutical manufacturers, automotive emission systems, and environmental treatment facilities |

Catalyst manufacturers hold the highest strategic value by integrating active components, support materials, and manufacturing know-how into turnkey solutions. Simultaneously, catalyst recycling and regeneration service providers are reshaping downstream value capture, enabling manufacturers and refiners to reduce precious metal expenditure and comply with circular economy frameworks.

Technology Landscape in the Catalyst Industry

Heterogeneous Catalyst Technology

Heterogeneous catalysts particularly zeolites, metal oxides, and supported metal catalysts dominate at 73.6% market share in 2025. Zeolite-based FCC catalysts remain the workhorse of petroleum refining, with ongoing development focused on increasing selectivity for gasoline and propylene production.

Homogeneous Catalyst Innovation

Homogeneous catalysts organometallic complexes, acid catalysts, and enzyme systems serve 26.4% of the market. Olefin metathesis and cross-coupling reactions using palladium and ruthenium complexes are critical in pharmaceutical API synthesis and fine chemical manufacturing. Immobilized enzyme catalysis is gaining share in biodiesel and specialty biosynthesis applications.

Catalyst Regeneration and Recycling Technology

Advanced hydrometallurgical recovery processes are enabling precious metal recovery rates exceeding 95% from spent automotive and refinery catalysts. Thermal regeneration technologies for FCC catalysts are being optimized for energy efficiency, with next-generation units targeting 15–20% reductions in regeneration energy consumption.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Heterogeneous Catalyst | 73.6% | 2025 |

| Process | Recycling | 47.7% | 2025 |

| Raw Material | Chemical Compounds | 38.0% | 2025 |

| Application | Environmental | 36.2% | 2025 |

| Region | Asia-Pacific | 49.1% | 2025 |

By Type

Heterogeneous catalysts lead the global catalyst market with a 73.6% share in 2025. This dominance reflects the practical advantages of solid-phase catalysts in large-scale continuous industrial processes ease of product separation, thermal stability, and recyclability. FCC catalysts, hydroprocessing catalysts, and ammonia synthesis catalysts are primary volume drivers.

To access detailed market analysis, Request Sample

By Process

Recycling is the dominant process with a 47.7% share in 2025. Economic imperatives to recover high-value platinum-group metals and rare earth elements from spent catalysts drive this segment’s primacy. The recycling process is further incentivized by circular economy regulations in Europe and stringent environmental disposal frameworks in North America.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

49.1% |

China refinery expansion, India petrochemical buildout, Southeast Asia industrialization, emission mandates |

|

North America |

19.6% |

EPA emission standards, U.S. shale-based refinery upgrades, pharmaceutical catalyst demand, green hydrogen investment |

|

Europe |

17.8% |

EU Green Deal mandates, Euro 7 emission standards, specialty chemical catalyst demand, circular economy regulations |

|

Latin America |

7.2% |

Brazil Petrobras refinery modernization, regional petrochemical expansion, growing automotive catalyst demand |

|

Middle East & Africa |

6.3% |

GCC refinery mega-projects, Saudi Aramco downstream expansion, Africa industrial development programs |

Asia-Pacific commands 49.1% global revenue share in 2025. China is the single most critical national market, combining the world’s largest refining capacity (955 million tonnes at end-2024) with the largest chemical production base. India’s national refinery capacity expansion program targets 310 MMTPA by 2030, driving structured multi-year catalyst procurement demand. Asia-Pacific is forecast to be the fastest-growing region at approximately 4.2% CAGR through 2034.

Competitive Landscape

|

Company Name |

Key Brands / Platforms |

Market Position |

Core Strength |

|

BASF SE |

BASF Catalysts |

Leader |

Broadest portfolio, PGM recycling integration, global scale |

|

Johnson Matthey Plc |

JM Catalyst Technologies |

Leader |

Emission control leadership, PGM refining, hydrogen catalysts |

|

Clariant AG |

Clariant Catalysts |

Leader |

Specialty chemicals, syngas & refining catalysts, sustainability |

|

Honeywell UOP |

UOP Catalysts |

Leader |

Refining process integration, zeolite technology, FCC leadership |

|

Evonik Industries AG |

Evonik Catalysts |

Challenger |

Specialty catalyst systems, pharma synthesis, German engineering |

|

W. R. Grace & Co. |

Grace Catalysts |

Challenger |

FCC catalysts, refinery solutions, North America market strength |

|

Axens (IFP Group) |

Axens Technologies |

Challenger |

European refining, hydroprocessing, biofuel catalyst expertise |

|

Albemarle Corporation |

Albemarle Catalysts |

Challenger |

Refinery hydrotreating, PGM processing, lithium integration |

|

Topsoe A/S |

Topsoe Catalysts |

Emerging |

Ammonia & hydrogen catalysis, green energy transition focus |

The global catalyst market competitive landscape is moderately concentrated, with multinational leaders competing alongside regional specialists and growing Asian manufacturers. Leading players compete on formulation technology, process integration capabilities, PGM recycling infrastructure, and sustainability credentials.

Key Company Profiles

BASF SE

BASF SE is the world’s largest chemical company, headquartered in Ludwigshafen, Germany. Its Catalysts division is one of the world’s leading suppliers of environmental and process catalysts, spanning automotive, refinery, chemical synthesis, and precious metal recycling.

- Product Portfolio: BASF’s portfolio includes automotive emission control catalysts (TWC, DOC, SCR), refinery FCC catalysts, hydroprocessing catalysts, polyolefin catalysts, and specialty chemical process catalysts, complemented by one of the largest precious metal recycling operations globally.

- Recent Developments: In 2024, BASF SE inaugurated a new Catalyst Development and Solids Processing Center in Ludwigshafen, Germany. The facility will support pilot-scale catalyst synthesis and advance solids processing technologies, enabling faster delivery of innovative solutions to global customers.

- Strategic Focus: BASF’s strategy centers on sustainability-led catalyst innovation, integrated PGM recycling value chains, and expansion in Asia-Pacific catalyst markets, particularly in China and India where industrial growth is strongest.

Johnson Matthey Plc

Johnson Matthey Plc is a UK-based specialty chemicals and sustainable technologies company with over 200 years of catalysis expertise. Its Clean Air and Catalyst Technologies divisions serve automotive emission control, refining, and hydrogen applications globally.

- Product Portfolio: Company portfolio includes three-way catalysts (TWC), diesel oxidation catalysts (DOC), selective catalytic reduction (SCR) systems, hydroprocessing catalysts, Fischer–Tropsch synthesis catalysts, and PEM electrolyzer catalysts for green hydrogen production.

- Recent Developments:In 2024, Johnson Matthey and Honeywell International Inc. signed an MoU to deliver end-to-end solutions for alternative fuel production from diverse feedstocks, including waste, biomass, biogas, and captured CO₂. The collaboration combines syngas and fuel upgrading technologies to reduce costs and accelerate deployment of sustainable fuel projects.

- Strategic Focus: Johnson Matthey focus is on accelerating the green hydrogen transition through catalyst innovation, divesting non-core assets to concentrate on clean energy and emission control, and leveraging PGM expertise across the full catalyst lifecycle.

Clariant AG

Clariant AG, headquartered in Muttenz, Switzerland, is a global specialty chemicals company with a focused catalyst division serving syngas, refining, and specialty chemical production markets across more than 100 countries.

- Product Portfolio: Clariant Catalysts specializes in syngas production catalysts, methanol synthesis catalysts, ammonia reforming catalysts, and refinery process catalysts.

- Recent Developments: In 2025, Clariant AG has successfully started up its MegaMax 900 methanol synthesis catalyst at European Energy’s e-methanol facility in Kasso, Denmark. The plant utilizes biogenic CO₂ and green hydrogen to produce green methanol, with Clariant providing on-site technical support during catalyst installation and startup.

- Strategic Focus: Clariant’s strategy focuses on expanding its position in syngas and hydrogen-related catalysts aligned with the energy transition, growing specialty catalyst applications in emerging markets, and developing sustainable catalyst formulations with reduced environmental footprint.

Market Concentration Analysis

The global catalyst market exhibits moderate concentration. The top five players – BASF SE, Johnson Matthey Plc, Clariant AG, Honeywell UOP, and Evonik Industries AG collectively account for approximately 35–42% of global market revenue in 2025. The remaining market share is distributed across W. R. Grace & Co., Axens, Albemarle Corporation, Topsoe A/S, and a significant number of regional manufacturers in China, Japan, and India.

The market is experiencing a bifurcated dynamic. At the premium specialty tier, consolidation is occurring around proprietary formulation technology, process integration capabilities, and PGM recycling infrastructure.

Investment & Growth Opportunities

Fastest-Growing Segments

Homogeneous catalysts represent the fastest-growing type segment, advancing at an estimated CAGR of 3.9% through 2034, driven by pharmaceutical and specialty chemical sector expansion. The regeneration process segment is growing at approximately 3.7% CAGR, reflecting increasing refinery operational cost optimization strategies. Green and bio-based catalysts for hydrogen production and sustainable chemistry represent the premium growth opportunity across the forecast period.

Emerging Market Expansion

India represents the highest-potential emerging catalyst market, driven by the national refinery capacity expansion program targeting 309.5 MMTPA by 2030 and rapid growth of domestic pharmaceutical and agrochemical industries. Southeast Asian petrochemical complex buildouts in Vietnam, Indonesia, and Malaysia, combined with GCC downstream expansion programs, collectively represent multi-billion-dollar catalyst procurement pipelines through 2034.

Venture and Strategic Investment Trends

Strategic acquisitions are reshaping the catalyst competitive landscape, with leading players targeting bolt-on acquisitions in PGM recycling, hydrogen catalyst technology, and bio-catalysis. Venture capital and corporate R&D investment is flowing heavily into computational catalyst discovery platforms, AI-driven formulation optimization, and iridium-alternative catalyst development for green hydrogen applications.

Future Market Outlook (2026-2034)

The global catalyst market forecast projects steady value expansion from USD 43.0 Billion in 2025 to USD 59.1 Billion by 2034 at a CAGR of 3.6%. Asia-Pacific will retain regional leadership while structural growth is supported by China’s refinery and chemical sector expansion, India’s industrial buildout, and Southeast Asia’s emerging petrochemical industry base.

Three key shifts will reshape the catalyst market through 2034. First, the energy transition will embed hydrogen and electrolysis catalyst demand into mainstream industrial procurement, with green hydrogen capacity scaling from the gigawatt to terawatt range by 2030–2034.

Second, circular economy integration will elevate catalyst recycling and regeneration from cost center to revenue opportunity as PGM recovery economics improve with scale. Third, computational chemistry and AI-driven catalyst design will compress development timelines, enabling faster commercialization of next-generation sustainable catalyst formulations.

North America and Europe will sustain premium value growth through environmental compliance investment and pharmaceutical sector expansion. The catalyst market outlook remains positive across all segments, with green chemistry, digital optimization, and emerging market industrialization converging to create a sustained demand foundation through 2034.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024–2025 with catalyst industry stakeholders, including R&D directors at catalyst manufacturers, procurement heads at petroleum refineries and chemical plants, regulatory affairs specialists, and institutional investors in specialty chemicals. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include International Energy Agency (IEA) refining and hydrogen data, EPA emission regulation publications, European Chemicals Agency (ECHA) REACH databases, company annual reports, trade publications including Chemical Engineering, Hydrocarbon Processing, and Applied Catalysis, and regional industrial association databases from CPCB (India), NEA (China), and VCI (Germany).

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating industrial output indices, refinery capacity data, environmental regulation timelines, and historical catalyst market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for commodity price uncertainty and regulatory policy variation.

Catalyst Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Heterogeneous Catalyst, Homogeneous Catalyst |

| Processes Covered | Recycling, Regeneration, Rejuvenation |

| Raw Materials Covered |

|

| Applications Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BASF SE, Johnson Matthey Plc, Clariant AG, Honeywell UOP, Evonik Industries AG, W. R. Grace & Co., Axens (IFP Group), Albemarle Corporation, Topsoe A/S, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the catalyst market from 2020-2034.

- The catalyst market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the catalyst industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Catalyst Market Report

The global catalyst market was valued at USD 43.0 Billion in 2025, supported by petroleum refining, chemical synthesis, and environmental emission control applications across major industrial economies globally.

The market is projected to reach USD 59.1 Billion by 2034, driven by industrial expansion, environmental regulations, and green chemistry adoption.

Heterogeneous catalysts lead with a 73.6% share in 2025, favored for large-scale industrial applications due to ease of separation, thermal stability, and recyclability in continuous processes.

Recycling leads the process segment with a 47.7% share in 2025, driven by economic incentives to recover precious metals and growing circular economy regulations in Europe and North America.

Asia-Pacific dominates with a 49.1% share in 2025. China’s refining capacity, India’s industrial expansion, and Southeast Asian petrochemical growth underpin its commanding leadership position.

Key drivers include global petroleum refining demand, chemical industry expansion, tightening emission regulations, green hydrogen investment, and pharmaceutical synthesis growth worldwide.

Major players include BASF SE, Johnson Matthey Plc, Clariant AG, Honeywell UOP, Evonik Industries AG, W. R. Grace & Co., Axens (IFP Group), Albemarle Corporation, and Topsoe A/S.

Key opportunities include hydrogen production catalysts, emerging market refinery buildouts in India and Southeast Asia, bio-catalysis, AI-driven catalyst design platforms, and precious metal recycling services.

Asia-Pacific is the fastest-growing region, advancing at approximately 4.2% CAGR through 2034, led by China’s chemical sector and India’s national refinery capacity expansion program.

Catalyst recycling represents 47.7% of the process market in 2025, driven by precious metal recovery economics and circular economy mandates across Europe and North America.

Green chemistry is a primary growth frontier, with bio-based, photocatalytic, and enzyme catalysts gaining share in pharmaceutical, biodiesel, and sustainable chemical synthesis applications globally.

The global catalyst market is projected to reach USD 51.3 Billion in 2030, driven by industrial growth and regulatory compliance investments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)