Cellulose Fibers Market Size, Share, Trends and Forecast by Fiber Type, Application, and Region, 2026-2034

Cellulose Fibers Market Size, Share, Trends & Forecast (2026-2034)

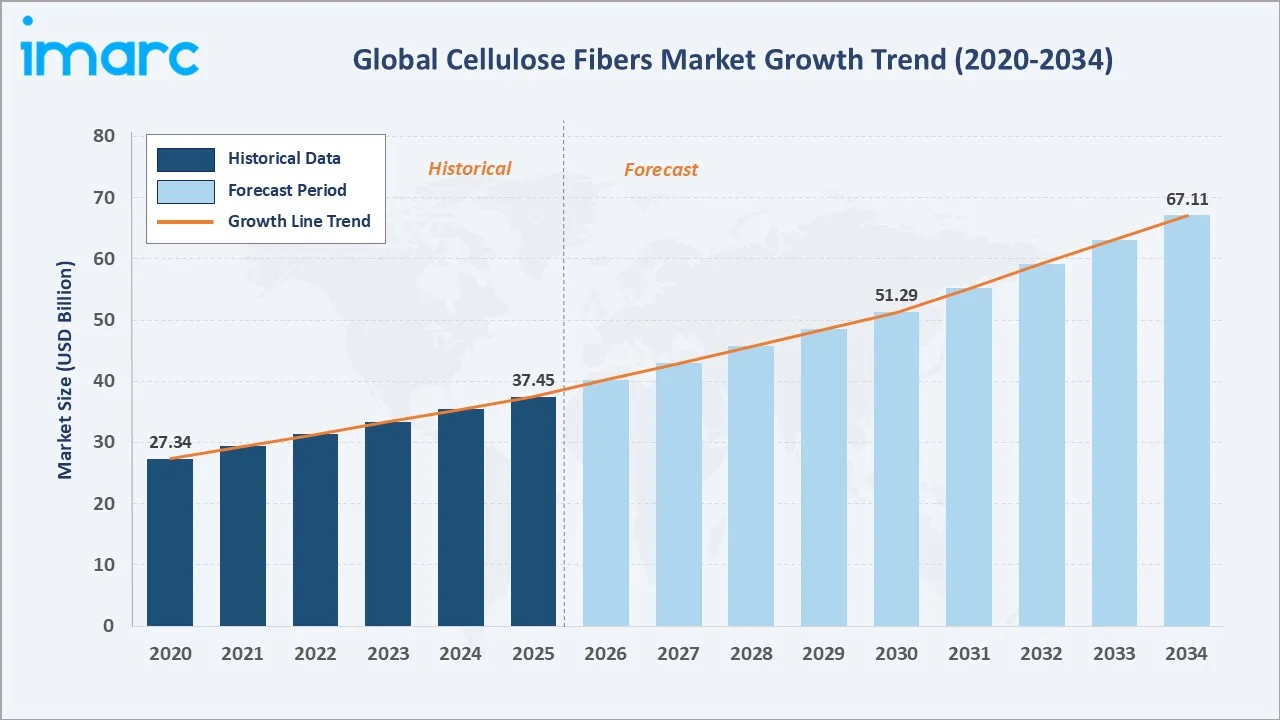

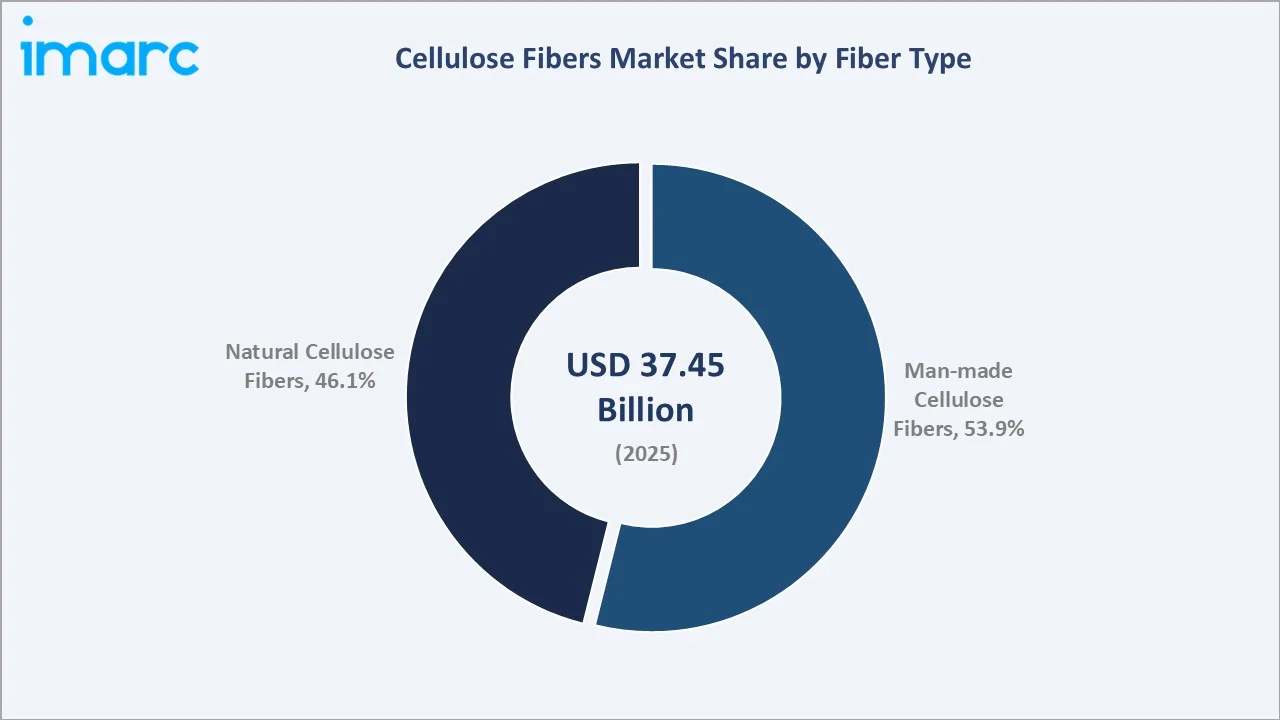

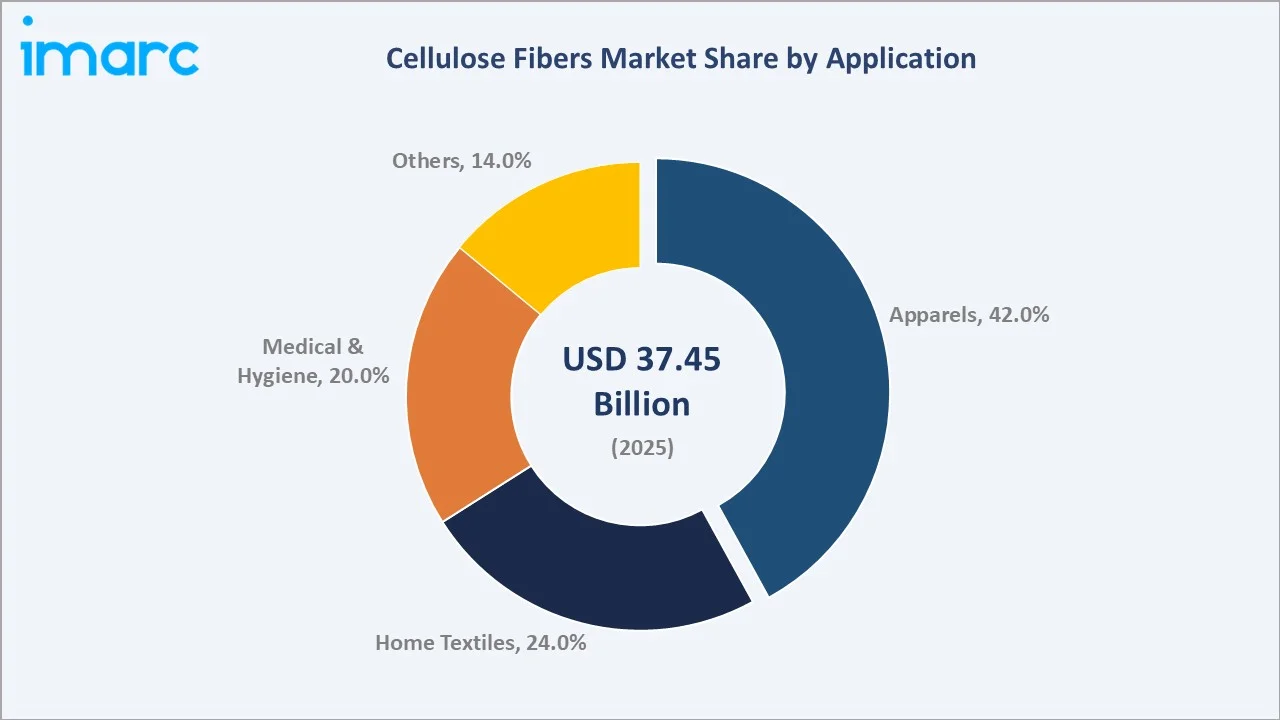

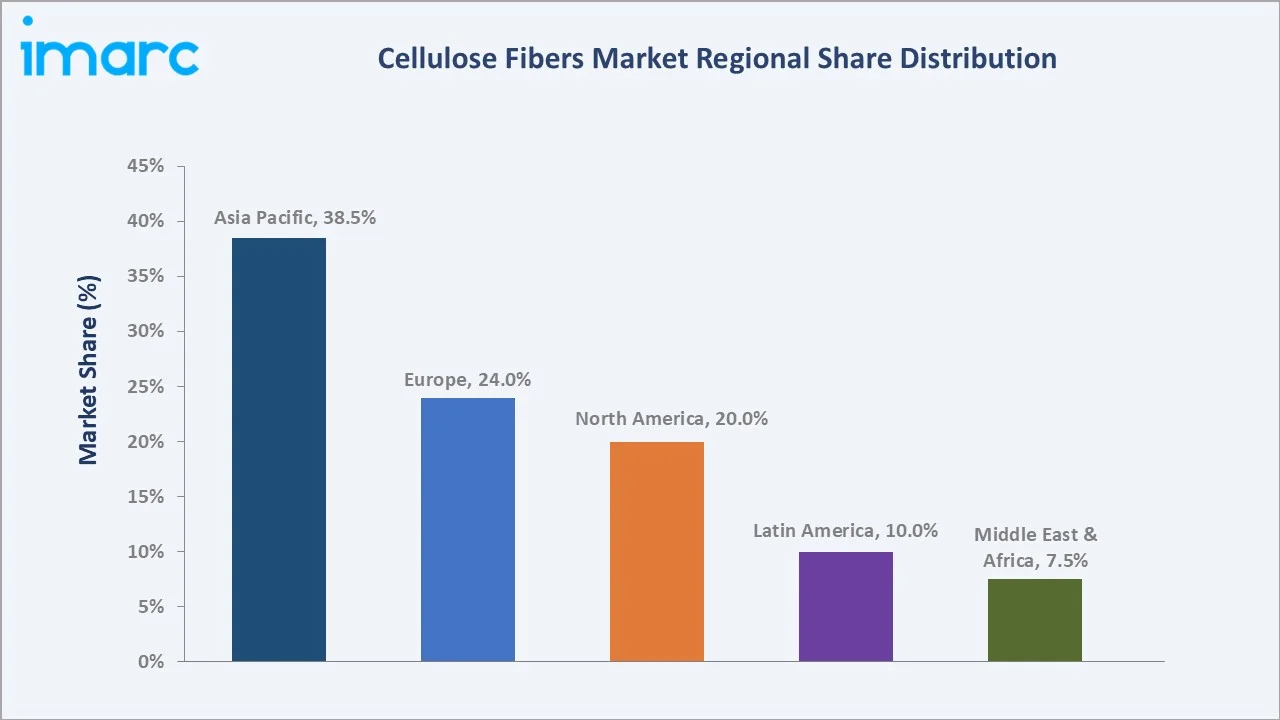

The global cellulose fibers market reached USD 37.45 Billion in 2025 and is projected to reach USD 67.11 Billion by 2034, growing at a CAGR of 6.50% during 2026-2034. The market is driven by rising demand for sustainable, biodegradable, and eco-friendly textile fibers as consumers and brands shift away from synthetic materials. India accounts for approximately 3.9% of global textile and apparel trade, with the United States and the European Union collectively representing around 47% share of the country's total textile and apparel exports. The strong export-oriented textile industry in India is driving demand for cellulose fibers, such as viscose and lyocell, as manufacturers increasingly adopt sustainable and biodegradable materials to meet the environmental and quality standards of international buyers. Man-made cellulose fibers lead at 53.9%. Apparel dominates the application at 42.0%. Asia Pacific commands 38.5% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 37.45 Billion |

|

Forecast Market Size (2034) |

USD 67.11 Billion |

|

CAGR (2026-2034) |

6.50% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Fiber Type |

Man-made Cellulose Fibers (53.9%, 2025) |

|

Dominant Application |

Apparels (42.0%, 2025) |

|

Leading Region |

Asia Pacific (38.5%, 2025) |

The global cellulose fibers market expanded from USD 27.34 Billion in 2020 to USD 37.45 Billion in 2025, anchored at USD 51.29 Billion in 2030, and forecast to reach USD 67.11 Billion by 2034. Cellulose fibers, encompassing both natural fibers and man-made cellulose fibers derived from wood pulp or other cellulose sources, represent the most commercially significant class of sustainable natural-origin textile fibers globally, competing with synthetic petroleum-derived polyester and nylon fibers on both performance and increasingly on environmental footprint.

To get more information on this market, Request Sample

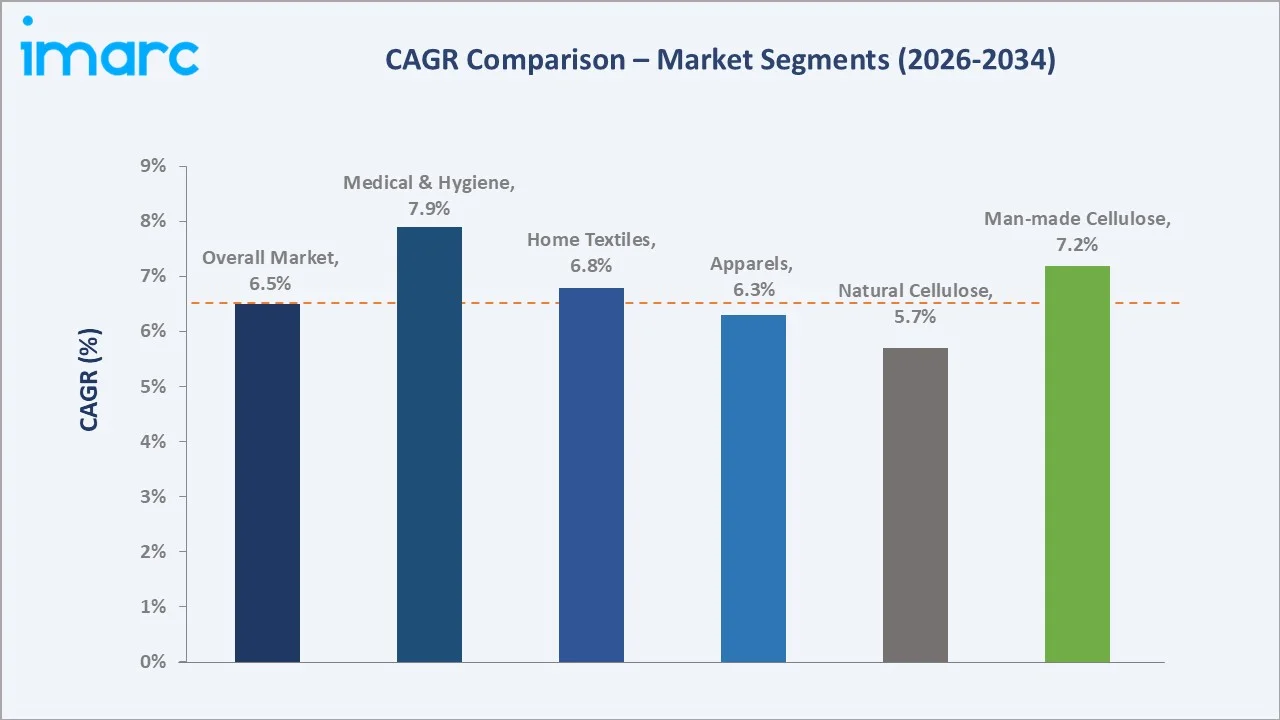

Medical and hygiene applications grow fastest at ~7.9% CAGR through adult incontinence product market expansion, feminine hygiene product penetration in Asia Pacific and Africa, and wound care cellulose fiber specialization. Man-made cellulose fibers grow at ~7.2% CAGR through lyocell technology capacity scaling and fashion industry sustainable fiber commitment above natural cellulose's supply chain constraints.

Executive Summary

The global cellulose fibers market at USD 37.45 Billion in 2025 represents the most commercially dynamic segment of the global textile fiber industry, growing at above-polyester rates through the structural sustainability transition in global fashion, the post-COVID permanent hygiene product demand elevation, and the closed-loop lyocell technology's progressive cost reduction, creating commercial accessibility above historical lyocell premium pricing. Cellulose fibers collectively serve as the natural-origin anchor of sustainable textile supply chains, providing biodegradability, breathability, moisture management, and renewable resource sourcing that petroleum-derived polyester and nylon fibers cannot replicate, while competing effectively against cotton's land and water intensity through man-made cellulose's wood pulp sourcing efficiency. The market is projected to reach USD 67.11 Billion by 2034.

Man-made cellulose fibers at 53.9% lead through viscose's established supply chain across Asia Pacific apparel manufacturing, lyocell's premium sustainable positioning for fashion brands, and modal's growing application in intimate apparel and athleisure. Apparel leads the application at 42.0% through fashion brand cellulose fiber specification. Asia Pacific leads regionally at 38.5%.

Key Market Insights

|

Insight |

Data |

|

Dominant Fiber Type |

Man-made Cellulose - 53.9% share (2025) |

|

Dominant Application |

Apparels - 42.0% market share (2025) |

|

Leading Region |

Asia Pacific - 38.5% share (2025) |

|

Market Opportunity |

Lyocell closed-loop production expansion; recycled cellulose circular economy compliance; bio-based specialty fibers for medical applications; sustainable fashion brand certified fiber supply chains; Asia Pacific hygiene product market growth |

Key Analytical Observations Supporting The Above Data:

- Man-made Cellulose Fibers at 53.9%: Man-made cellulose fibers dominate due to their versatility, cost-effectiveness, and widespread use in apparel, home textiles, and nonwoven products, offering sustainable alternatives to both natural and synthetic fibers.

- Apparels at 42.0%: The apparel segment dominates as fabrics like viscose, lyocell, and modal are widely used in clothing due to their softness, breathability, and eco-friendly appeal, driving high consumer demand globally.

- Asia Pacific at 38.5%: The Asia Pacific region dominates regionally due to its large textile manufacturing base, abundant raw material supply, and strong export demand from major markets like the US and EU.

Cellulose Fibers Market Overview

The global cellulose fibers market operates at the intersection of the world's three most commercially significant material transitions: the fashion industry's sustainability revolution, the healthcare system's growing demand for bio-compatible and biodegradable medical materials, and the bio-based materials economy's progressive cost reduction.

The market ecosystem integrates globally distributed dissolving pulp production, chemically intensive cellulose fiber processing, Asia Pacific's dominant fiber manufacturing concentration, and global fashion and hygiene brand procurement chains. Macroeconomic factors include rising disposable incomes, rapid urbanization, and growing consumer preference for sustainable and eco-friendly textiles.

Market Dynamics

To evaluate market opportunities, Request Sample

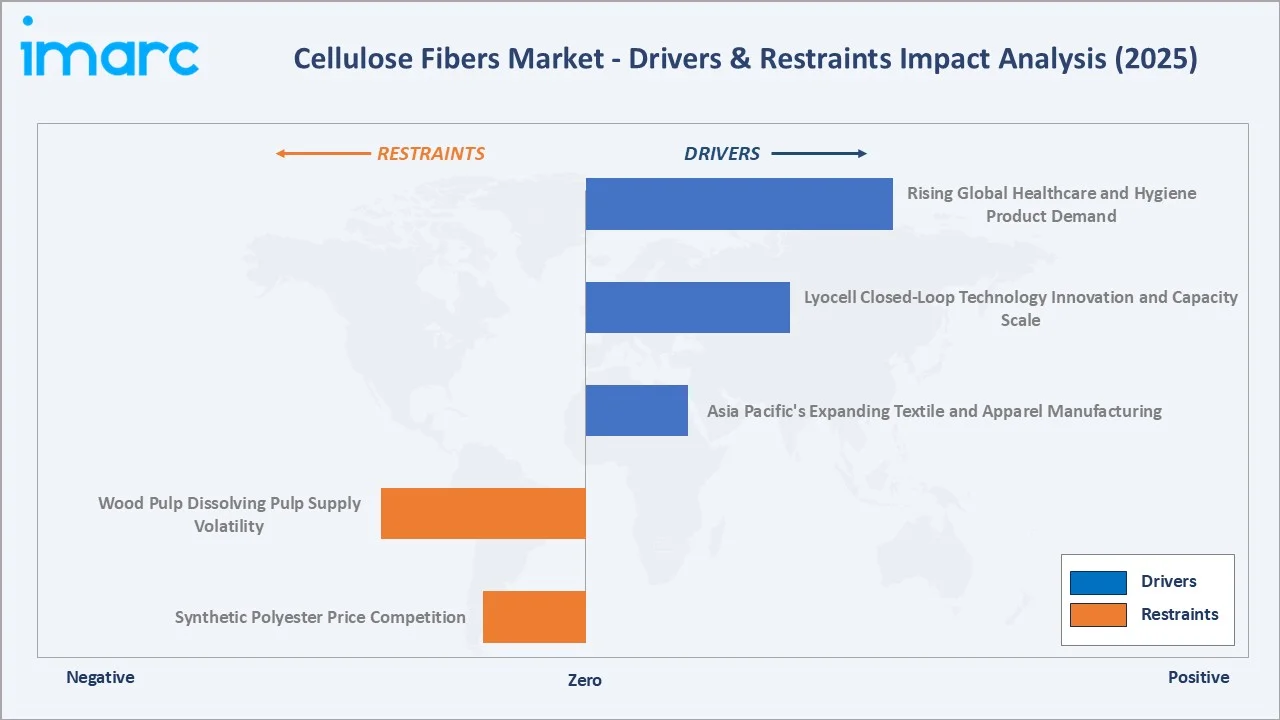

Market Drivers

- Rising Global Healthcare and Hygiene Product Demand: Rising global demand for healthcare and hygiene products is driving the market as these fibers are widely used in items like surgical gowns, wipes, diapers, and sanitary products due to their absorbency, softness, and biodegradability. Increasing awareness of hygiene and stringent health regulations is pushing manufacturers to adopt sustainable, high-performance cellulose-based materials. Between 2015 and 2024, access to basic hygiene services improved for 1.6 billion people, increasing global coverage from 66% to 80%. Despite this progress, 1.7 billion people still lacked essential hygiene services in 2024, including 611 million without any handwashing facilities. This widespread need for improved sanitation and hygiene is fueling demand for healthcare and hygiene products, such as wipes, diapers, sanitary items, and surgical textiles, which extensively use absorbent and biodegradable cellulose fibers.

- Lyocell Closed-Loop Technology Innovation and Capacity Scale: Innovations in lyocell closed-loop technology enabling environmentally friendly production with minimal chemical waste and higher resource efficiency. This sustainable approach reduces water and energy consumption while ensuring high-quality fiber output, appealing to eco-conscious textile manufacturers and consumers. In March 2026, Birla Cellulose launched Livaeco Lyocell, its next-generation sustainable fibre, at Confluence 2026. Expansion of lyocell production capacities by leading players is meeting growing global demand for biodegradable and renewable fibers in apparel, home textiles, and nonwoven products. The combination of technological innovation and scalable manufacturing strengthens the market adoption of cellulose-based fibers.

- Asia Pacific's Expanding Textile and Apparel Manufacturing: Asia Pacific’s expanding textile and apparel manufacturing is increasing the region’s consumption of raw materials like viscose, lyocell, and modal. Countries such as China, India, and Vietnam are scaling up production to meet growing domestic and export demand, particularly from markets in the US and EU. The focus on sustainable and eco-friendly fibers in large-scale manufacturing further boosts the adoption of cellulose-based materials. Combined with cost advantages and abundant raw material availability, this expansion solidifies Asia Pacific’s leading role in the global cellulose fibers market.

Market Restraints

- Wood Pulp Dissolving Pulp Supply Volatility: Volatility in wood pulp and dissolving pulp supply creates raw material shortages and drives up costs for manufacturers. Fluctuations in availability due to environmental regulations, forestry constraints, and geopolitical factors disrupt consistent production of viscose, lyocell, and other regenerated fibers. This uncertainty increases reliance on imports, affects pricing stability, and may limit the expansion of fiber production capacity. As a result, manufacturers face challenges in meeting growing demand from the apparel, home textiles, and nonwoven sectors, slowing overall market growth.

- Synthetic Polyester Price Competition: Intense price competition from synthetic polyester makes cheaper, petroleum-based alternatives more attractive to textile manufacturers. Polyester’s lower production costs, high durability, and established supply chains put pressure on cellulose fiber producers to remain cost-competitive. This price sensitivity can limit the adoption of more sustainable but costlier fibers like viscose, lyocell, and modal, especially in price-driven mass-market apparel and home textile segments. Consequently, the growth of the cellulose fibers market is restrained despite rising environmental awareness and demand for eco-friendly materials.

Market Opportunities

- Recycled Cellulose Fiber Market Development: The development of the recycled cellulose fiber market promotes circularity and sustainability in textile production. By converting post-consumer and post-industrial textile waste into high-quality fibers, manufacturers can reduce reliance on virgin wood pulp and lower environmental impact. Growing consumer and regulatory demand for eco-friendly products further supports investment in recycled cellulose technologies. This expansion enables brands to meet sustainability goals while tapping into the increasing market preference for green and biodegradable textile materials, driving overall market growth.

- Bio-Based Specialty Cellulose Medical Application: Bio-based specialty cellulose fibers for medical applications catering to the growing demand for sustainable, high-performance healthcare products. These fibers are used in surgical gowns, masks, wound dressings, and hygiene products due to their biodegradability, biocompatibility, and superior absorbency. Increasing healthcare standards, stringent regulations, and the rising focus on eco-friendly medical supplies are driving adoption. This trend allows manufacturers to innovate and expand into specialty applications, strengthening the market presence of cellulose-based fibers in the rapidly growing medical and hygiene sector.

Market Challenges

- Cotton Supply Chain Social Compliance: Cotton supply chain social compliance poses a challenge as manufacturers sourcing cotton for regenerated fibers must ensure adherence to labor standards, fair wages, and safe working conditions. Non-compliance risks reputational damage, regulatory scrutiny, and potential trade restrictions, especially in export-oriented markets like the US and EU. Ensuring traceability and certification throughout complex global supply chains increases operational costs and administrative burden. This makes it more difficult for cellulose fiber producers to maintain sustainable and ethically sourced raw materials, potentially slowing market growth.

- Energy and Water Intensiveness: Energy and water intensiveness challenge the market because the production of viscose, lyocell, and other regenerated fibers requires large volumes of water and significant energy, increasing operational costs and environmental impact. High resource consumption also attracts regulatory scrutiny and pressures manufacturers to adopt cleaner, more sustainable processes. In regions facing water scarcity or high energy costs, this can limit production scalability and profitability. Consequently, the need for resource-efficient technologies becomes critical, and traditional energy- and water-intensive methods can hinder market growth.

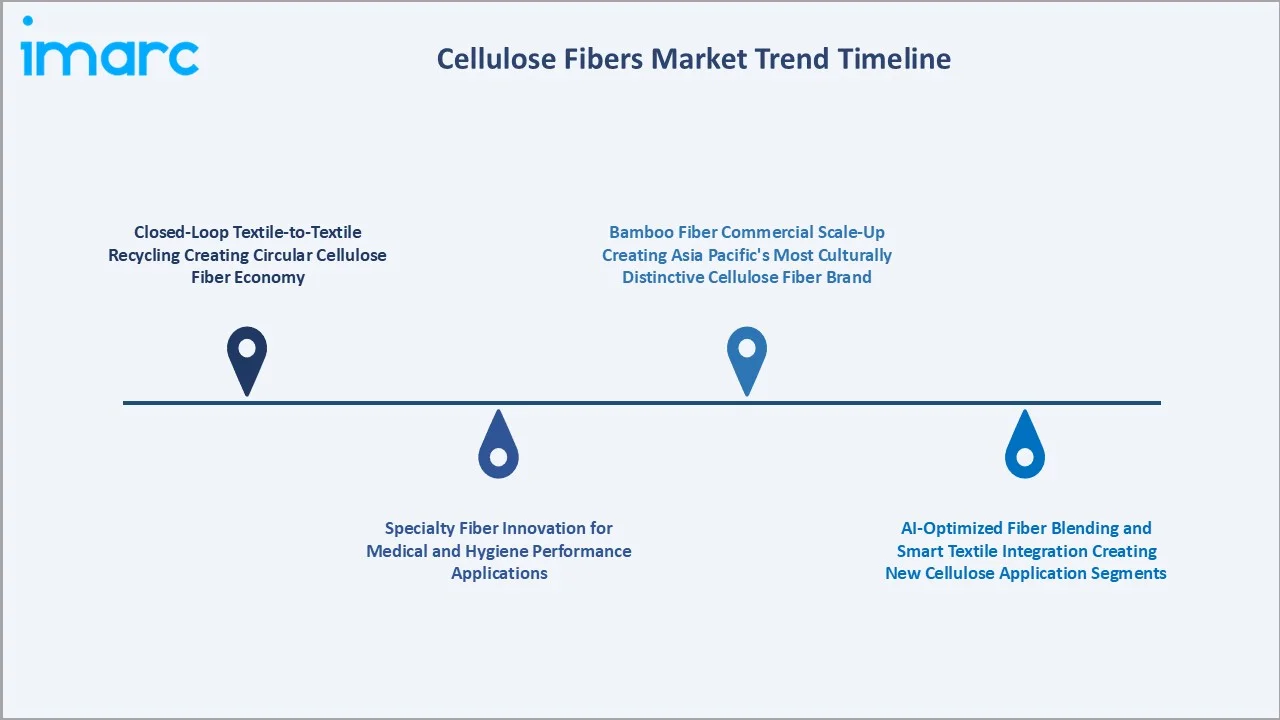

Emerging Market Trends

1. Closed-Loop Textile-to-Textile Recycling Creating Circular Cellulose Fiber Economy

Closed-loop textile-to-textile recycling enables the conversion of post-consumer and post-industrial textile waste back into high-quality fibers. Growing consumer demand for eco-friendly products and stricter regulations on textile waste are accelerating adoption. In November 2025, a significant European research initiative led by Fraunhofer UMSICHT launched to advance integrated solutions for textile waste recycling. The AUTOLOOP project seeks to establish a comprehensive system capable of processing 1.24 million tonnes of textile waste per year by 2050. The project focuses on developing, testing, and integrating automated sorting, traceability, and closed-loop recycling technologies for polyester-based textiles (NRT), tackling the critical issue of textile waste management. This initiative supports the emerging trend of closed-loop textile-to-textile recycling by demonstrating how large-scale, automated recycling systems can recover fibers from post-consumer textiles and reintroduce them into production.

2. Specialty Fiber Innovation for Medical and Hygiene Performance Applications

Specialty fiber innovation for medical and hygiene applications driven by the need for high-performance, biodegradable, and skin-friendly materials. Advanced fibers are being developed for surgical gowns, masks, wipes, and absorbent products, offering enhanced strength, absorbency, and antimicrobial properties. Rising healthcare standards, pandemic preparedness, and increasing demand for sustainable hygiene products are accelerating adoption. This trend allows manufacturers to differentiate products, expand into specialty applications, and capture growth in the rapidly evolving medical and personal care sectors.

3. Bamboo Fiber Commercial Scale-Up Creating Asia Pacific's Most Culturally Distinctive Cellulose Fiber Brand

The commercial scale-up of bamboo fiber transforming bamboo into a sustainable, eco-friendly textile alternative. Leveraging bamboo’s natural softness, breathability, and antibacterial properties, manufacturers are creating culturally distinctive fiber brands that appeal to environmentally conscious consumers. Expansion of production facilities and supply chains enables large-scale adoption in apparel, home textiles, and nonwoven products. This trend strengthens regional brand identity while promoting sustainable cellulose fiber solutions, driving market growth and consumer engagement.

4. AI-Optimized Fiber Blending and Smart Textile Integration Creating New Cellulose Application Segments

AI-optimized fiber blending and smart textile integration enable precise mixing of cellulose fibers with other materials to enhance performance, comfort, and functionality. Leveraging AI and data analytics allows manufacturers to design fabrics with targeted properties, such as moisture management, durability, or thermal regulation. Integration with wearable technologies and smart textiles opens new application segments in sportswear, healthcare, and high-performance apparel. This trend drives innovation, adds value to cellulose fibers, and expands their adoption beyond traditional textile uses.

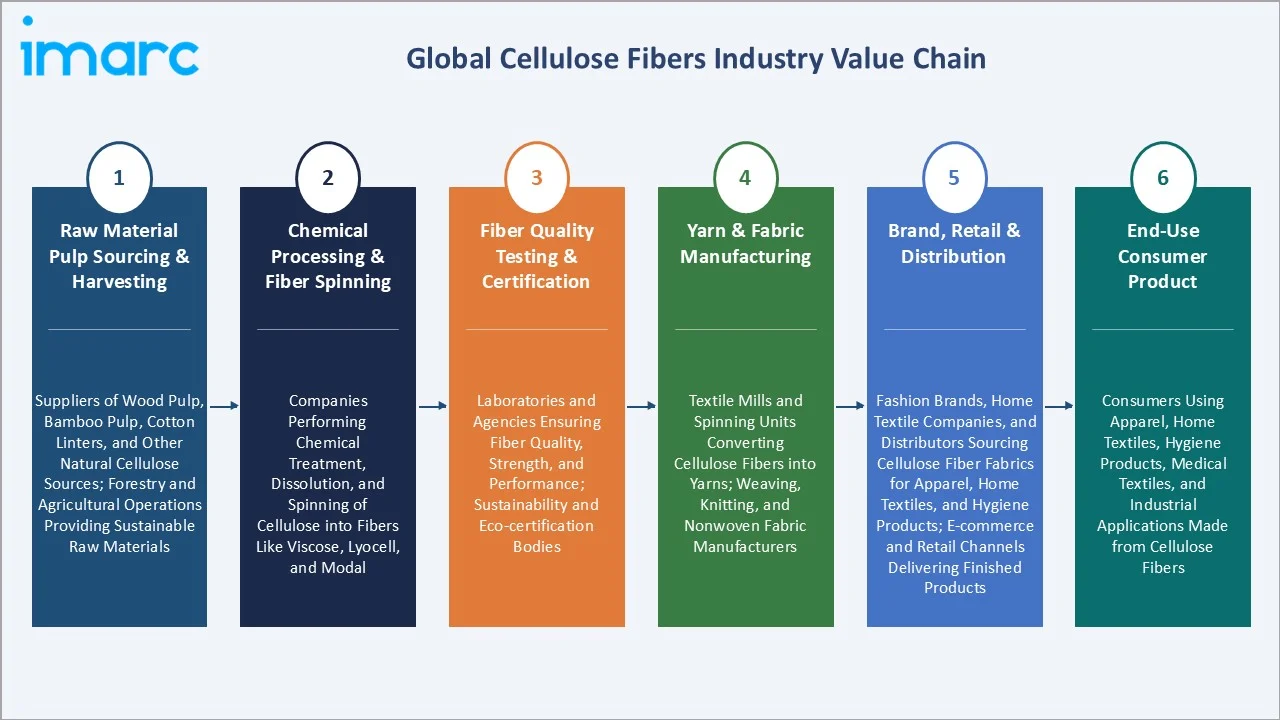

Industry Value Chain Analysis

The global cellulose fiber value chain extends from plantation forest and cotton field raw material through chemically intensive fiber processing to global textile manufacturing and finally to consumer end-use in fashion, home textiles, and hygiene products, spanning production, processing, and consumption in the most geographically distributed consumer goods supply chain of any major industrial material category.

|

Stage |

Key Participants |

|

Raw Material Pulp Sourcing & Harvesting |

Suppliers of wood pulp, bamboo pulp, cotton linters, and other natural cellulose sources; forestry and agricultural operations providing sustainable raw materials. |

|

Chemical Processing & Fiber Spinning |

Companies performing chemical treatment, dissolution, and spinning of cellulose into fibers like viscose, lyocell, and modal |

|

Fiber Quality Testing & Certification |

Laboratories and agencies ensuring fiber quality, strength, and performance; sustainability and eco-certification bodies. |

|

Yarn & Fabric Manufacturing |

Textile mills and spinning units converting cellulose fibers into yarns; weaving, knitting, and nonwoven fabric manufacturers |

|

Brand, Retail & Distribution |

Fashion brands, home textile companies, and distributors sourcing cellulose fiber fabrics for apparel, home textiles, and hygiene products; e-commerce and retail channels delivering finished products. |

|

End-Use Consumer Product |

Consumers using apparel, home textiles, hygiene products, medical textiles, and industrial applications made from cellulose fibers. |

The brand and retail distribution stage is the value chain's most commercially differentiated stage above the commodity processing and raw material stages. The end-use consumer product stage creates the value chain's most commercially visible cellulose fiber application.

Technology Landscape in the Cellulose Fibers Industry

Viscose Xanthation Process Technology

The viscose xanthation process technology enables the transformation of wood pulp into viscose fibers through chemical derivatization. This process allows precise control over fiber properties such as strength, softness, and dyeability, making it suitable for a wide range of apparel, home textile, and nonwoven applications. Innovations in xanthation, including improved chemical recovery and reduced environmental impact, enhance sustainability and efficiency. As a result, this technology underpins large-scale viscose production and supports the adoption of high-performance, eco-friendly cellulose fibers in the market.

Digital Textile Integration

Digital textile integration enables smart fabrics and IoT-enabled textiles that incorporate cellulose fibers for functional applications. This includes sensors, wearable electronics, and performance-monitoring textiles in healthcare, sports, and fashion. Advanced digital printing and automated weaving/knitting technologies enhance customization, precision, and production efficiency. By combining cellulose fibers with smart technologies, manufacturers can create high-value, innovative products, driving adoption and expanding applications beyond traditional apparel and home textiles.

Lyocell Technology

Lyocell technology enables the production of high-quality, biodegradable fibers through a closed-loop, environmentally friendly process. This method uses non-toxic solvents and recycles up to 99% of chemicals, reducing water and energy consumption compared to traditional viscose production. Lyocell fibers offer superior strength, softness, and moisture management, making them ideal for apparel, home textiles, and hygiene products. In October 2025, Lenzing introduced a new cellulose fiber called Tencel Lyocell-HV100. This innovative fiber incorporates intentional irregularities, drawing inspiration from the textured appearance of natural fibers. The adoption of lyocell technology supports sustainability initiatives, enhances production efficiency, and drives innovation in high-performance, eco-conscious cellulose fiber applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Fiber Type |

Man-made Cellulose Fibers |

53.9% |

2025 |

|

Application |

Apparels |

42.0% |

2025 |

|

Region |

Asia Pacific |

38.5% |

2025 |

By Fiber Type

Man-made cellulose fibers lead at 53.9% (2025). The man-made segment encompasses viscose staple fiber, lyocell, modal, and bamboo fiber. Man-made cellulose grows at ~7.2% CAGR through lyocell capacity scaling and sustainable fashion demand above natural cellulose's more moderate cotton supply chain growth.

To access detailed market analysis, Request Sample

Natural cellulose fibers at 46.1% encompass cotton, jute, flax, hemp, and specialty natural fibers. Natural cellulose grows at ~5.7% CAGR through premium organic cotton adoption, hemp and flax sustainable fashion application growth, and natural cellulose's irreplaceable position in traditional home textile and premium apparel applications, where consumer preference for natural fiber is commercially paramount above cost-performance comparison with man-made alternatives.

By Application

Apparels lead at 42.0% (2025). The apparel segment is transitioning from commodity cotton and generic viscose specification toward certified sustainable lyocell, organic cotton, and brand-certified man-made cellulose fibers as fashion brand sustainability commitments progressively mandate certified fiber above uncertified commodity sourcing across global apparel supply chains.

Home textiles at 24.0% represent the most commercially stable cellulose fiber application through bedding and bath towel cotton dominance. Medical and hygiene at 20.0% grow fastest at ~7.9% CAGR through hygiene product market expansion in Asia Pacific and Africa, and advanced wound care specialty fiber demand. Others at 14.0% encompass industrial, automotive, and construction cellulose fiber applications, including tire cord viscose, technical nonwoven, and specialty industrial cellulose.

Regional Market Insights

|

Region |

Share (2025) |

Key Cellulose Fibers Market Drivers & Characteristics |

|

Asia Pacific |

38.5% |

Driven by a highly concentrated textile manufacturing base, abundant raw material supply, and strong export demand. |

|

Europe |

24.0% |

Europe’s market share reflects its position as a leader in cellulose fiber technology innovation and sustainable production practices. |

|

North America |

20.0% |

Supported by large-scale consumption in apparel, home textiles, and hygiene products, with established supply chains and growing demand for sustainable fibers. |

|

Latin America |

10.0% |

Anchored by Brazil’s role as a significant cellulose fiber producer and consumer, with increasing adoption in the regional apparel and hygiene sectors. |

|

Middle East & Africa |

7.5% |

Represents a commercially heterogeneous market with growing awareness of sustainable fibers, emerging textile manufacturing hubs, and gradual adoption of cellulose fibers in apparel and hygiene applications. |

Asia Pacific's 38.5% market leadership reflects its dual role as one of the largest cellulose fiber production geographies and the cellulose fiber-consuming textile manufacturing geography. Europe's 24.0% reflects the commercial significance of regional players as global cellulose fiber technology leaders and Europe's premium sustainable fiber consumption market, creating above-global-average per-capita certified cellulose fiber demand.

North America's 20.0% reflects the USA's world-leading hygiene product market and sustainable fashion brand demand. Latin America's 10.0% is anchored by Brazil's dissolving pulp production leadership and Brazil's large domestic apparel and home textile consumption. The Middle East and Africa's 7.5% are growing fastest regionally through Africa's demographic growth, creating new hygiene product consumers and a sophisticated cellulose fiber textile manufacturing sector serving fashion brand proximity supply chains.

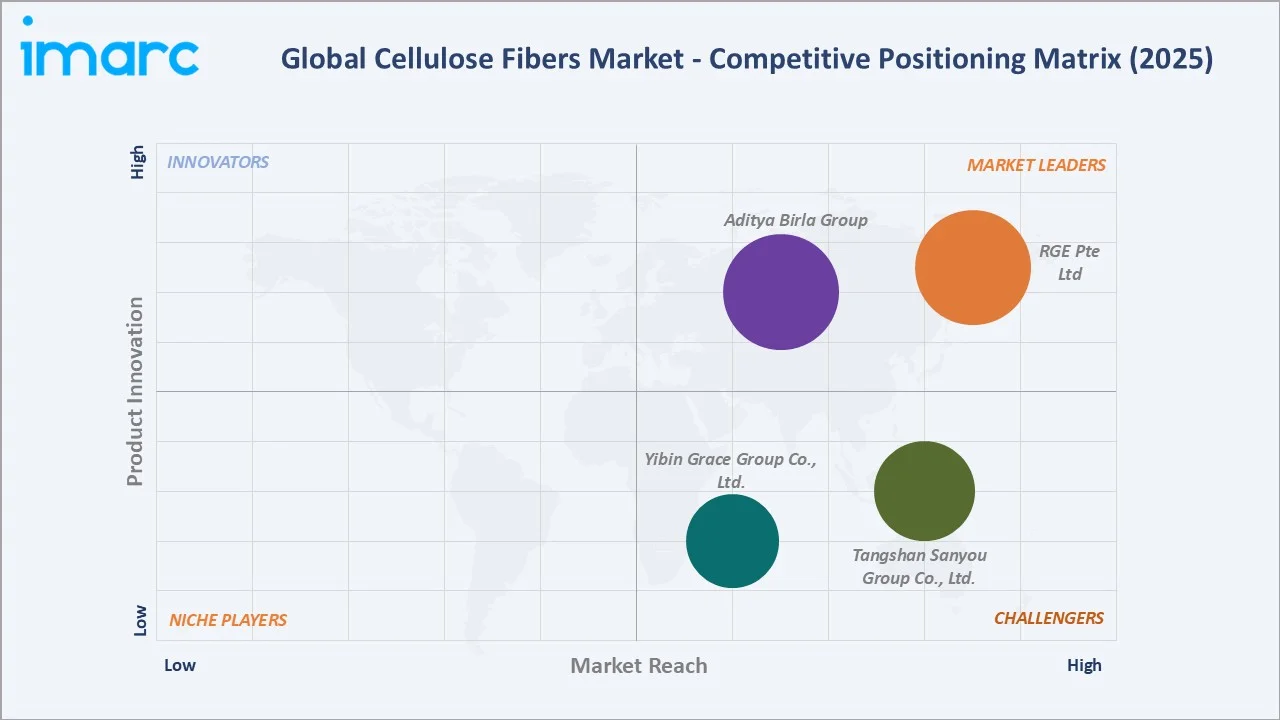

Competitive Landscape

The global cellulose fibers market competitive landscape is stratified between premium technology leaders, volume-scale Asian producers, and specialty niche players, creating a three-tier competitive structure where premium, volume, and specialty compete in largely non-overlapping market segments.

|

Company |

Key Brands |

Market Position |

Core Strength |

|

|

EcoCosy, FINEX |

Market Leader |

RGE Pte Ltd plays a dominant, vertically integrated role in the global cellulose fiber industry with its subsidiary Sateri, operating as one of the world’s largest producers of viscose fiber. |

|

|

Birla Viscose, Birla Modal, Birla Excel, Livaeco |

Market Leader |

Aditya Birla Group, through its subsidiary Birla Cellulose, is a global leader in manufacturing man-made cellulosic fibers, holding a significant share of the global viscose staple fiber market. |

|

|

Tangcell, ReVisco |

Strong Challenger |

Tangshan Sanyou Group Co., Ltd. is a global manufacturer of cellulose fibers, specializing in the production of cellulose fibers through its brand Tangcell. |

|

|

Re-Gracell |

Strong Challenger |

Yibin Grace Group Co., Ltd. is a major global producer of bio-based cellulose fibers, including viscose staple fiber, filament yarn, and lyocell. |

The competitive landscape's most commercially significant dynamics are the sustainable certification arms race and the lyocell market entry by Chinese producers, creating the most commercially resilient supply chain of any single cellulose fiber company above single-geography producers' market access risk.

Key Company Profiles

RGE Pte Ltd

RGE Pte Ltd is the major player in the cellulose fibers market with extensive operations in pulp, dissolving pulp, and viscose/ cellulosic fiber production through its downstream companies such as Sateri.

- Key Brands: EcoCosy, FINEX, and others.

- Strategic Focus: Expanding sustainable viscose and cellulosic fiber production while investing in next‑generation technologies and closed‑loop solutions to support a circular textile economy.

Aditya Birla Group

Aditya Birla Group is a major global conglomerate with a strong presence in the cellulose fibers industry through its textile and fiber division, particularly Birla Cellulose. The group is one of the world’s leading producers of viscose staple fiber and other regenerated cellulose fibers, supplying to apparel, home textiles, and nonwoven segments across global markets.

- Key Brands: Birla Viscose, Birla Modal, Birla Excel, Livaeco, and others.

- Recent Developments: In March 2026, Birla Cellulose, a part of the Aditya Birla Group, launched Livaeco Lyocell, its next-generation sustainable fibre, at Confluence 2026.

- Strategic Focus: Expanding sustainable viscose and regenerated cellulose production, driving eco‑friendly fiber innovation, and partnering with global brands to meet growing demand for responsibly sourced textile solutions.

Market Concentration Analysis

The global cellulose fibers market is moderately concentrated in the premium specialty segment and highly fragmented in the commodity VSF volume segment. The natural cellulose fiber segment is the most structurally fragmented, with cotton production distributed across cotton-producing countries, with no single entity controlling above 5-8% of global cotton fiber supply, creating a competitive structure unique among major industrial commodities. Market concentration is increasing through two mechanisms: the sustainable fiber certification creating commercial concentration and the lyocell capacity expansion progressively de-concentrating lyocell's historic Lenzing near-monopoly.

Investment & Growth Opportunities

Highest Growth Segments

Medical and hygiene (~7.9% CAGR through hygiene product democratization), man-made cellulose fibers (~7.2% CAGR through lyocell scaling and sustainable fashion mandate), recycled cellulose fiber market (~20-25% CAGR from small base through circular textile regulation), lyocell capacity expansion investment (~15% annual capacity growth), Asia Pacific hygiene product market (~10-12% CAGR through first-time hygiene product adoption in India, Indonesia, and Africa), and specialty wound care cellulose fiber (~12-15% CAGR through advanced wound care clinical adoption) represent the highest-growth cellulose fiber investment vectors through 2034.

Emerging Investment Opportunities

The textile-to-textile recycled cellulose fiber market is growing through circular textile regulation, and fashion brand recycled content commitments are the most commercially novel cellulose fiber investment opportunity, creating the commercial technology foundation for recycled cellulose at scale that fashion brand compliance and EU recycled content mandates will institutionalise into mainstream cellulose fiber procurement above the current voluntary recycled content pioneer market.

Investment Themes

- Lyocell capacity expansion targeting the Asia Pacific sustainable fashion market: The most commercially attractive single cellulose fiber capital investment opportunity is lyocell tenter expansion in Asia Pacific that creates locally produced lyocell for the Asia Pacific fast fashion sustainable fiber market.

- Specialty medical cellulose fiber scale-up targeting Asia Pacific's underserved wound care and hygiene product markets: Investment in licensed or independently developed specialty viscose production in India or China creates the most commercially premium per-unit cellulose fiber application with growing structural demand from Asia Pacific's hygiene product market democratization.

Future Market Outlook (2026-2034)

The global cellulose fibers market is projected to grow from USD 37.45 Billion in 2025 to USD 67.11 Billion by 2034, delivering a 6.50% CAGR over the forecast period. The market's anchor value of USD 51.29 Billion in 2030 represents global cellulose fibers at its most commercially consequential structural transition. The completion of the lyocell capacity scale-up toward mainstream sustainable fiber at viscose-competitive pricing, the commercial establishment of recycled cellulose fiber as a material market segment through regulation implementation, and the hygiene product democratization wave in the Asia Pacific and Africa, creating the largest new cellulose fiber demand pool that the industry has seen since China's VSF capacity build-up.

Three structural forces define the cellulose fiber market's growth through 2034: global fashion industry sustainability transition, creating high synthetic-to-sustainable fiber substitution demand by 2030 that cellulose fiber (viscose, lyocell, recycled cellulose) the primary beneficiary of this demand through biodegradable and renewable origin advantages above recycled polyester's technically recycled but not naturally biodegradable positioning, hygiene product market democratization in Asia Pacific and Africa creating new cellulose fiber consuming hygiene product users through 2034 as rising income, health awareness, and modern retail access, and closed-loop lyocell and recycled cellulose technology cost reduction progressively eliminating the sustainable fiber price premium above commodity alternatives.

Research Methodology

Primary Research

Primary research comprised structured interviews with global cellulose fiber industry stakeholders, including R&D directors, sustainability managers, procurement directors, dissolving pulp managers, and consumer apparel brand sustainable fiber sourcing managers across Europe, the USA, and the Asia Pacific. Supply chain survey from cellulose fiber value chain participants (mills, brands, traders).

Secondary Research

Secondary research encompassed International Cotton Advisory Committee Outlook; company annual reports; Food and Agriculture Organization natural fiber statistics; regulation data; law textile implementation guidance; and textile fiber marketing requirements. Over 65 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using an application-segment bottom-up model: global textile fiber demand by application multiplied by cellulose fiber share per application multiplied by average fiber price trajectory. The medical and hygiene segment is modelled separately through hygiene product penetration rate expansion by geography multiplied by per-product cellulose fiber intensity.

Cellulose Fibers Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Fiber Types Covered |

|

| Applications Coverage |

Apparels, Home Textiles, Medical and Hygiene, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | RGE Pte Ltd, Aditya Birla Group, Tangshan Sanyou Group Co. Ltd., Yibin Grace Group Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cellulose fibers market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global cellulose fibers market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cellulose fibers industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cellulose Fibers Market Report

The global cellulose fibers market reached USD 37.45 Billion in 2025, driven by growing global demand for sustainable and biodegradable textiles, rising consumption in apparel, home textiles, and hygiene products, and increasing focus on eco-friendly, high-performance fibers like viscose, lyocell, and modal to meet consumer and regulatory requirements.

The global cellulose fibers market grows at 6.50% CAGR during 2026-2034, reaching USD 67.11 Billion by 2034. The overall growth is sustained by textile sustainability regulation, hygiene product first-time adoption in emerging markets, and circular economy policy, creating mandatory recycled cellulose fiber demand.

Man-made cellulose fibers lead at 53.9% through viscose staple fiber's established fast fashion supply chain and lyocell's premium sustainable positioning.

Apparel leads at 42.0% through the fashion industry's foundational dependence on cellulose fibers for comfort, sustainability, and natural-origin brand narrative.

Asia Pacific leads at 38.5% through China's VSF capacity, India's Aditya Birla Group as one of the largest VSF producers, and the region's dominant global apparel manufacturing, consuming viscose and lyocell for fast fashion supply chains.

Leading companies include RGE Pte Ltd, Aditya Birla Group, Tangshan Sanyou Group Co., Ltd., and Yibin Grace Group Co., Ltd., among others.

The global cellulose fibers market is projected to reach approximately USD 51.29 Billion by 2030, with lyocell capacity completing its commercial scale-up from a premium niche toward mainstream sustainable fiber at Asia Pacific fast fashion-competitive pricing, recycled cellulose fiber growth, and hygiene product market growth.

Three priority investment opportunities: Asia Pacific lyocell capacity expansion targeting sustainable fashion market from below-Lenzing-import-cost regional production, recycled cellulose fiber technology development, and specialty medical cellulose fiber scale-up in Asia Pacific.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)