Ceramic Filters Market Size, Share, Trends and Forecast by Product Type, Application, and Region, 2026-2034

Ceramic Filters Market Size, Share, Trends & Forecast (2026-2034)

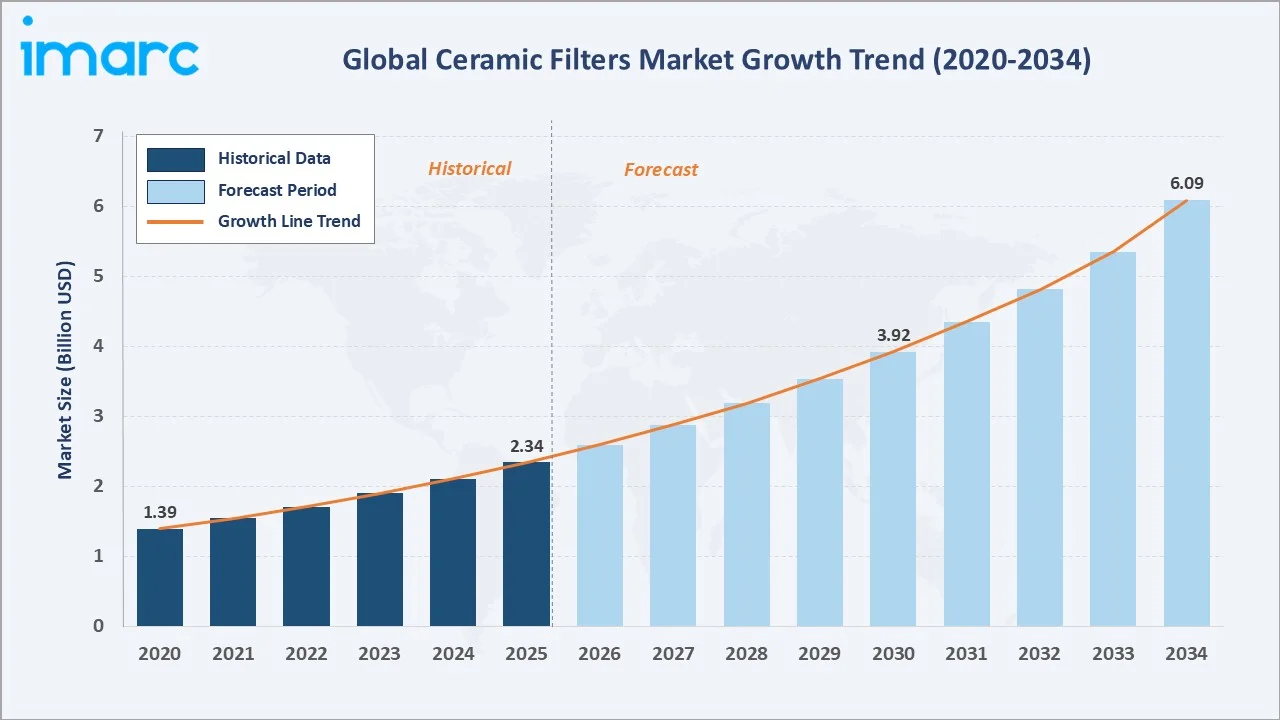

The ceramic filters market was valued at USD 2.34 Billion in 2025 and is projected to reach USD 6.09 Billion by 2034, exhibiting a CAGR of 10.88% during 2026-2034. Rising demand for clean drinking water, tightening air-quality and emission norms, and the durability and reusability of ceramic media are the primary drivers shaping market growth.

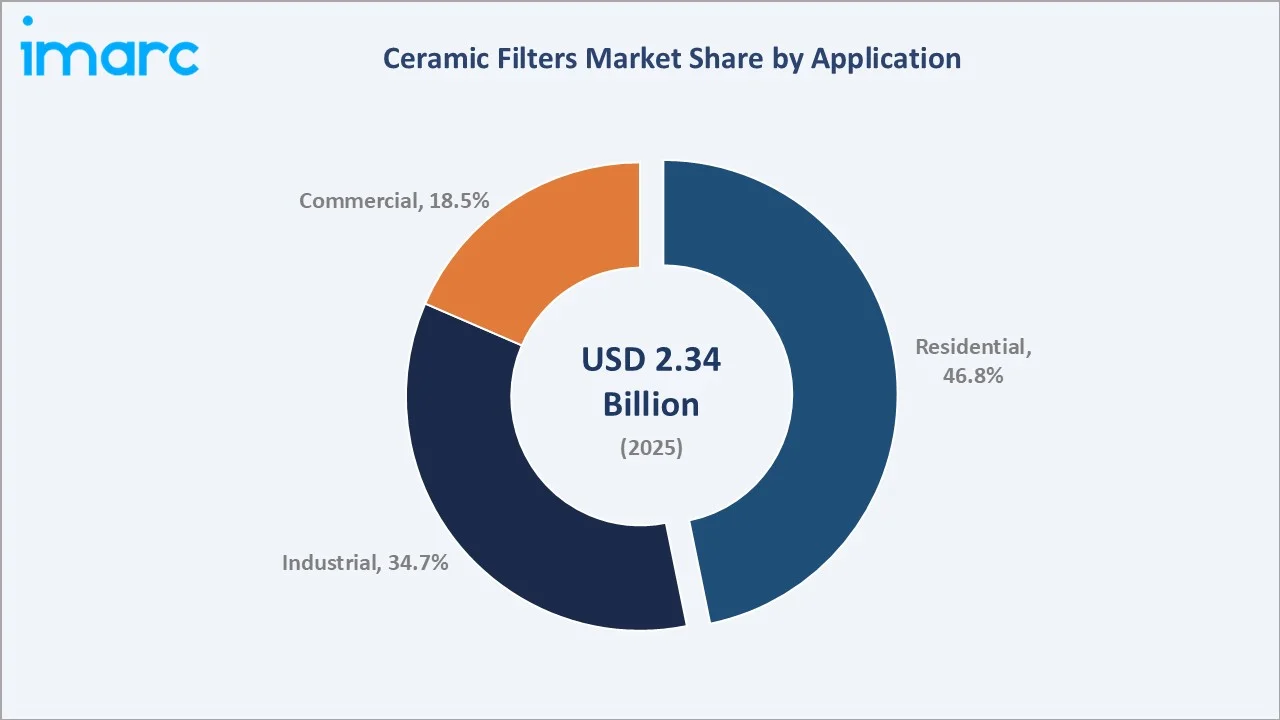

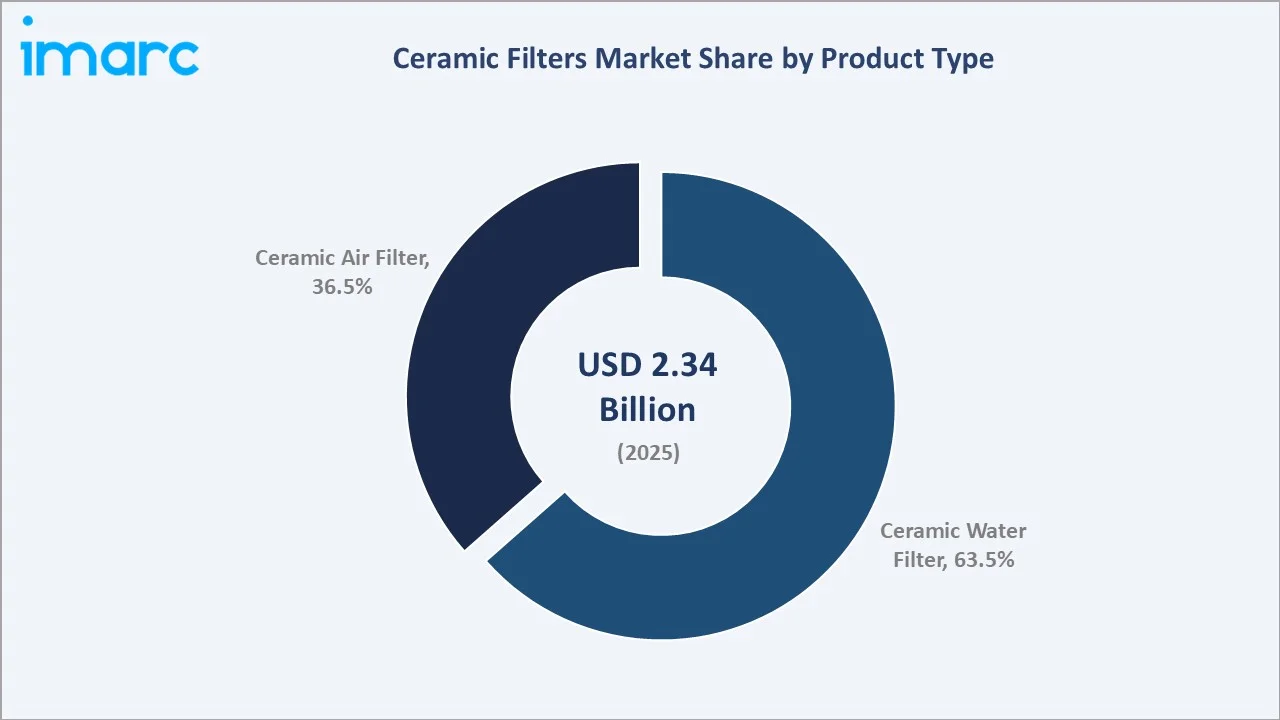

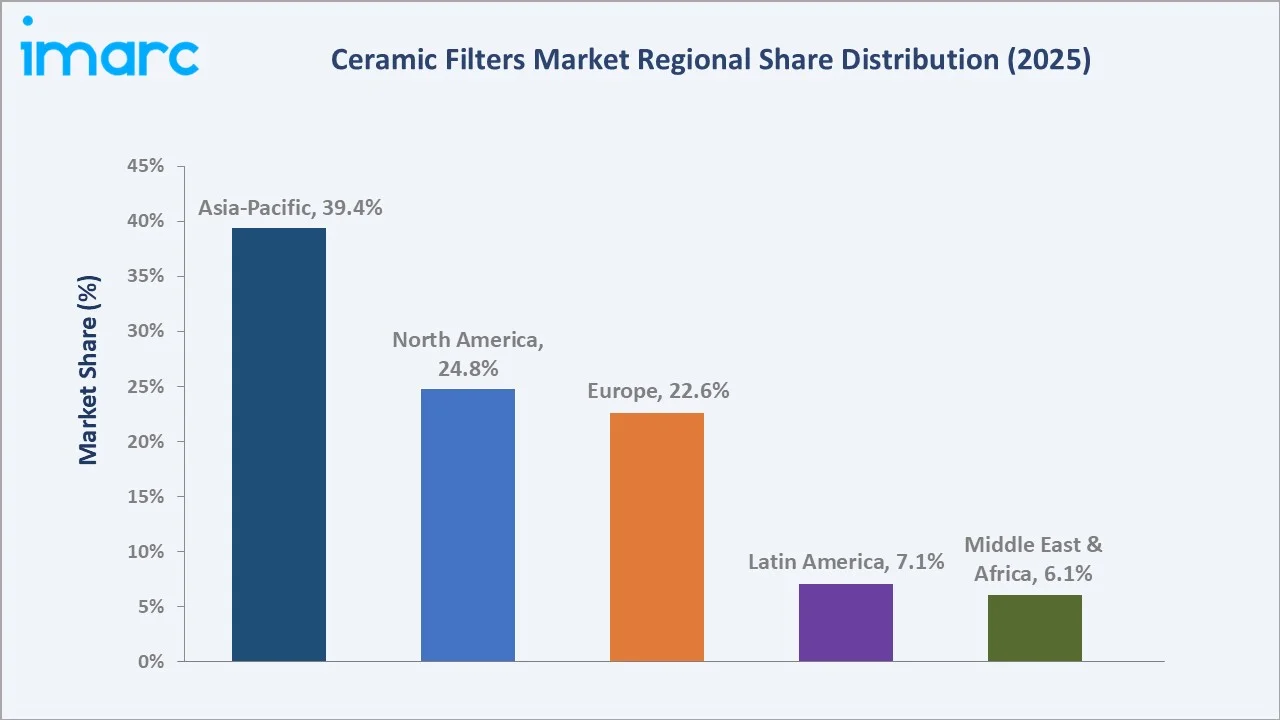

Residential leads the application segment at 46.8%, ceramic water filter dominates the product type segment at 63.5%, and Asia-Pacific commands 39.4% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.34 Billion |

|

Forecast Market Size (2034) |

USD 6.09 Billion |

|

CAGR (2026-2034) |

10.88% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (39.4%, 2025) |

|

Second Largest Region |

North America (24.8%, 2025) |

|

Leading Application |

Residential (46.8%, 2025) |

|

Leading Product Type |

Ceramic Water Filter (63.5%, 2025) |

The ceramic filters market expanded from USD 1.39 Billion in 2020 to USD 2.34 Billion in 2025, driven by stricter water-quality standards, rising industrial emission control, and growing adoption of point-of-use filtration. Anchored at USD 3.92 Billion in 2030, the forecast to USD 6.09 Billion by 2034 is supported by accelerating demand for ceramic membrane technology, expanding diesel and industrial particulate filtration, and sustained investment in clean-water infrastructure.

To get more information on this market, Request Sample

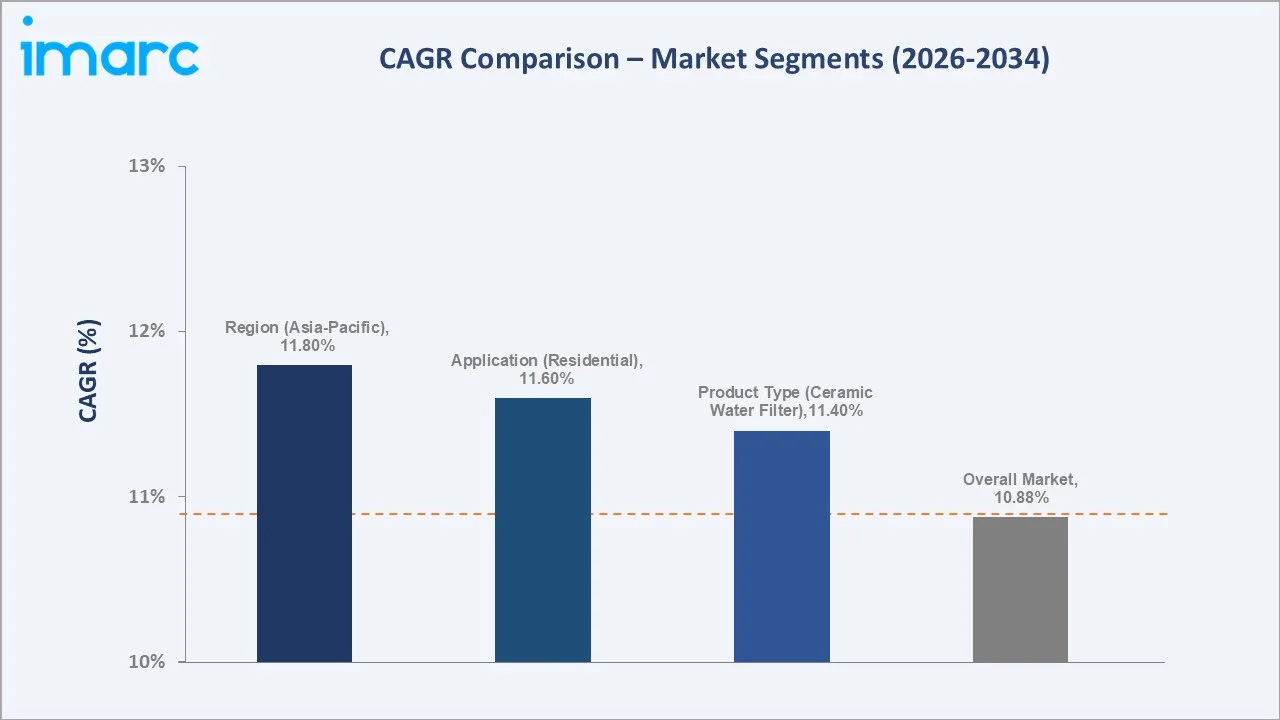

CAGR trajectories across application and product type sub-segments show ceramic water filter and residential expanding faster than the overall 10.88% market CAGR, supported by clean-water demand.

Executive Summary

The ceramic filters market is on a steady growth trajectory from USD 1.39 Billion in 2020 to USD 6.09 Billion by 2034. The industry has moved from basic gravity filtration toward engineered ceramic membranes and monolithic structures used across drinking water, wastewater, power, and automotive emission control. Durable media, high thermal resistance, and precise particle separation are encouraging adoption across residential and industrial settings.

Residential dominates the application segment at 46.8% in 2025, supported by household point-of-use purifiers and rising clean-water awareness. Ceramic water filter leads the product type segment at 63.5%, fueled by demand for chemical-free, reusable purification. Asia-Pacific commands 39.4% of the regional share, led by large populations, rapid industrialization, and expanding water-treatment infrastructure. As per Macrotrends, India's total population in 2025 was 1,454,606,724, reflecting a 0.89% rise from 2024.

Key Market Insights

|

Insight |

Data |

|

Leading Application |

Residential - 46.8% share (2025) |

|

Second Largest Application |

Industrial - 34.7% share (2025) |

|

Leading Product Type |

Ceramic Water Filter - 63.5% share (2025) |

|

Second Largest Product Type |

Ceramic Air Filter - 36.5% share (2025) |

|

Leading Region |

Asia-Pacific - 39.4% share (2025) |

|

Second Largest Region |

North America - 24.8% share (2025) |

|

Top Companies |

Danaher Corporation, Corning Incorporated, NGK Corporation, Porvair plc |

Key Analytical Observations Expanding On The Data Above:

- Residential leadership at 46.8% is supported by household water purifiers, rising awareness of waterborne contaminants, and the appeal of chemical-free ceramic media.

- Industrial share at 34.7% is sustained by process water treatment, flue-gas and dust filtration, and high-temperature applications across power, chemical, and metallurgical plants.

- Ceramic water filter dominance at 63.5% reflects strong demand for durable, reusable media that removes bacteria, sediment, and turbidity without chemicals across residential and municipal use.

- Ceramic air filter share at 36.5% is expanding as diesel particulate filters, hot-gas cleaning, and industrial emission control adopt silicon carbide and cordierite ceramics.

- Asia-Pacific at 39.4% dominates regional share, anchored by China, India, and Southeast Asia, supported by large populations, rapid industrialization, and growing water-treatment investment. As per IMARC Group, the India wastewater treatment market size reached USD 10.4 Billion in 2025.

Ceramic Filters Market Overview

Ceramic filters are porous filtration media manufactured from materials such as alumina, silica, cordierite, and silicon carbide, used to separate particles, microorganisms, and contaminants from liquids and gases. The market spans ceramic water filters for drinking water and wastewater, and ceramic air filters for diesel particulate, hot-gas, and industrial emission control.

The ceramic filters ecosystem integrates raw-material suppliers, filter and membrane manufacturers, sintering and coating technology providers, regulatory authorities, distributors and OEMs, and end-use industries, spanning water utilities, power, chemicals, and automotive. Together they enable reliable filtration within tightening environmental standards.

Market Dynamics

To evaluate market opportunities, Request Sample

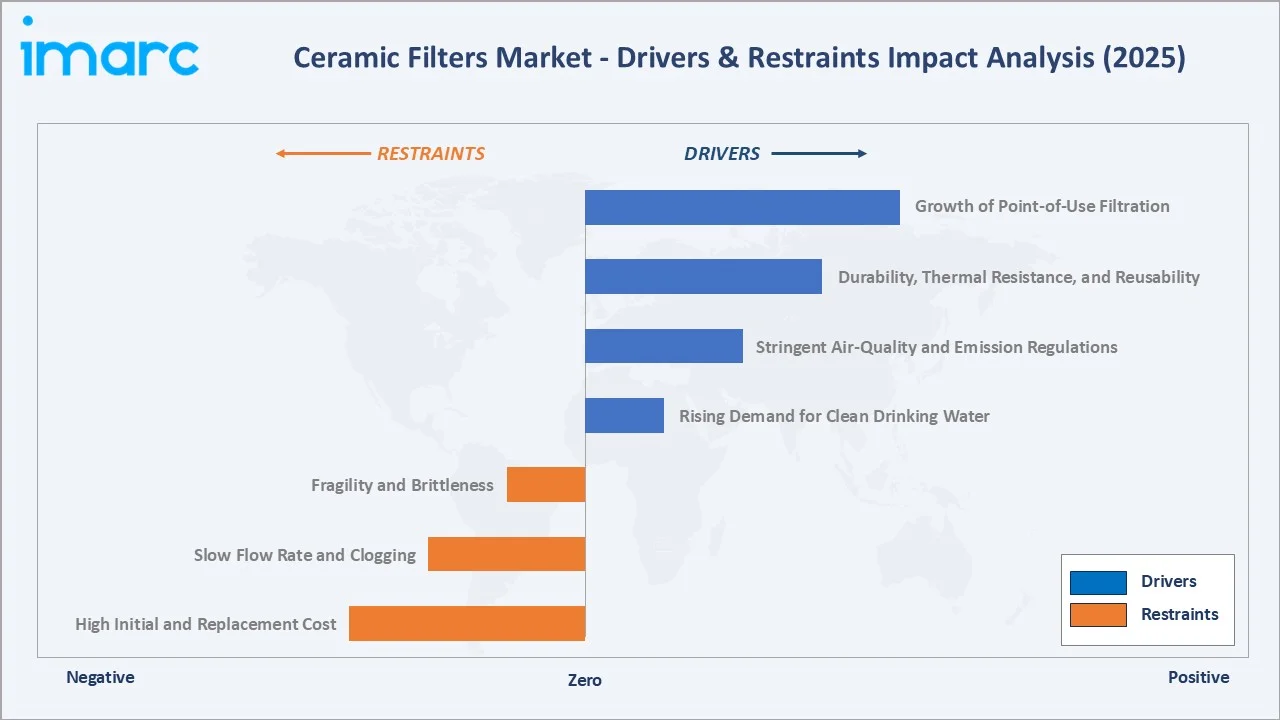

Market Drivers

- Rising Demand for Clean Drinking Water: Growing concern over waterborne contaminants and expanding access programs are lifting demand for point-of-use and municipal ceramic water filtration.

- Stringent Air-Quality and Emission Regulations: Tightening limits on particulate and industrial emissions are driving adoption of ceramic candle and diesel particulate filters across power, cement, and automotive sectors.

- Durability, Thermal Resistance, and Reusability: Ceramic media withstand high temperatures and aggressive chemistries and can be cleaned and reused, lowering lifecycle cost relative to disposable filters.

- Growth of Point-of-Use Filtration: Rising urbanization and household awareness are expanding demand for gravity and counter-top ceramic purifiers, especially in regions with unreliable piped supply.

Market Restraints

- High Initial and Replacement Cost: Ceramic filter production requires sintering at temperatures of roughly 1,000-1,300°C, making it energy-intensive and raising upfront and replacement costs relative to polymeric alternatives.

- Slow Flow Rate and Clogging: Fine ceramic pores can restrict throughput and clog over time, requiring regular backwashing and maintenance in high-turbidity applications.

- Fragility and Brittleness: Ceramic elements can crack under mechanical shock or thermal cycling, limiting use in some mobile and high-vibration settings.

Market Opportunities

- Ceramic Membrane Adoption in Wastewater Reuse: Industrial water recycling and zero-liquid-discharge mandates create demand for robust ceramic ultrafiltration and microfiltration membranes.

- Silicon Carbide and Smart Filtration: New silicon carbide membranes and sensor-enabled filters open higher-flux, longer-life applications across food, beverage, and pharmaceuticals.

Market Challenges

- Competition from Alternative Technologies: Reverse osmosis, activated carbon, and polymeric membranes compete on cost and flow rate, pressuring ceramic adoption in price-sensitive segments.

- Fragmented Regional Manufacturing: A large base of small regional producers creates quality variability and price competition, complicating standardization for nationwide buyers.

Emerging Market Trends

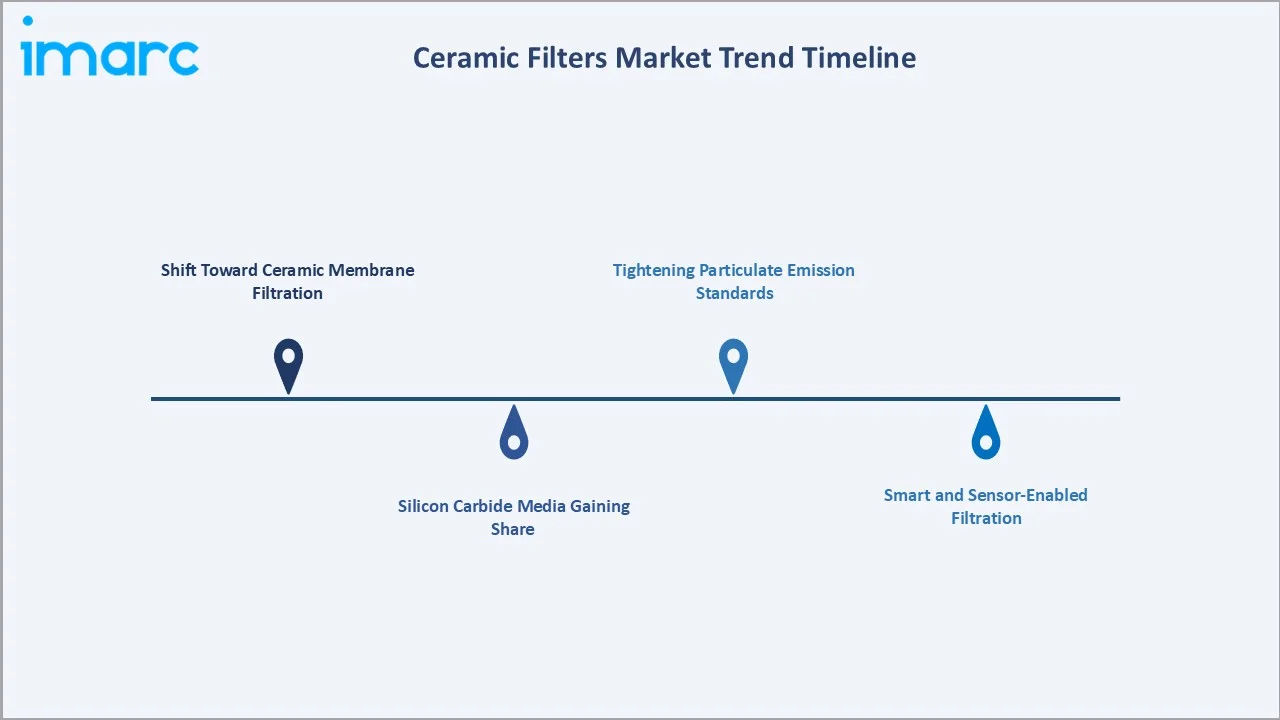

1. Shift Toward Ceramic Membrane Filtration

Manufacturers are moving from simple porous candles toward engineered ceramic ultrafiltration and microfiltration membranes for water reuse and industrial separation. These membranes offer higher flux, longer service life, and resistance to fouling, supporting adoption in municipal and process-water applications.

2. Silicon Carbide Media Gaining Share

Silicon carbide ceramics are increasingly used for their high permeability, chemical resistance, and thermal stability. The material is expanding into oily-water treatment, food and beverage, and high-temperature gas cleaning where conventional media underperform.

3. Tightening Particulate Emission Standards

Regulators are extending particulate limits to new sources, lifting demand for ceramic filtration. Industries are increasingly adopting high-efficiency ceramic filtration systems to meet stricter compliance requirements while maintaining operational performance and reducing emissions.

4. Smart and Sensor-Enabled Filtration

Embedded sensors and IoT monitoring are being added to ceramic filtration systems to track fouling, flow, and replacement timing. The shift supports predictive maintenance, reduces downtime, and improves total cost of ownership for industrial users.

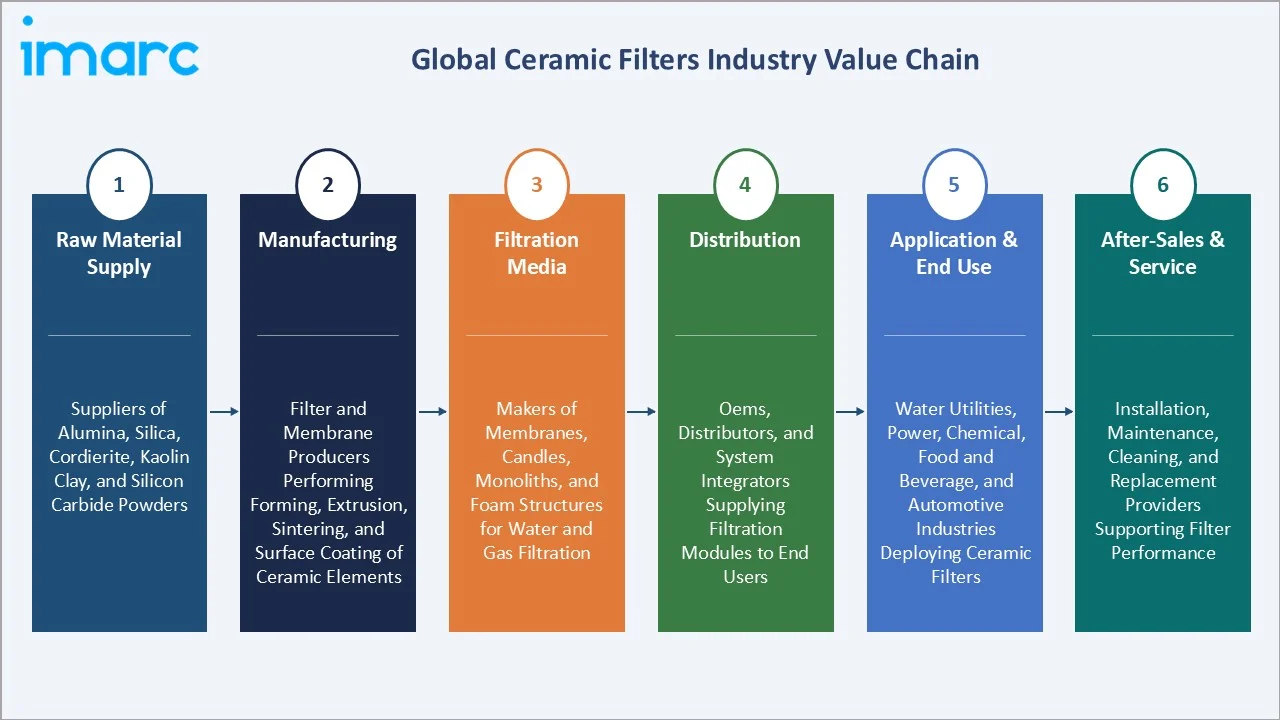

Industry Value Chain Analysis

The ceramic filters value chain spans six stages from raw-material supply through after-sales service. Manufacturing, filtration media engineering, and application integration capture the highest value-add, while quality consistency and compliance increasingly determine competitive position.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of alumina, silica, cordierite, kaolin clay, and silicon carbide powders used as base ceramic materials |

|

Manufacturing |

Filter and membrane producers performing forming, extrusion, sintering, and surface coating of ceramic elements |

|

Filtration Media |

Makers of membranes, candles, monoliths, and foam structures tailored to water and gas filtration needs |

|

Distribution |

OEMs, distributors, and system integrators supplying filtration modules to end users |

|

Application & End Use |

Water utilities, power, chemical, food and beverage, and automotive industries deploying ceramic filters |

|

After-Sales & Service |

Installation, maintenance, cleaning, and replacement providers supporting long-term filter performance |

Vertically integrated players that control raw materials, proprietary sintering and membrane technology, and direct customer relationships are positioned to capture greater value than firms reliant on third-party media.

Technology Landscape in the Ceramic Filters Industry

Membrane Materials and Pore Engineering

Manufacturers are refining alumina, titania, zirconia, and silicon carbide formulations to control pore size and surface charge. Precise pore engineering enables targeted removal of bacteria, viruses, and fine particulates while maintaining flux and mechanical strength.

Sintering, Coating, and Surface Treatment

Advances in sintering profiles and thin-film coatings improve filtration efficiency and fouling resistance. Catalytic and antimicrobial coatings are extending ceramic media into emission control and hygiene-critical applications.

Smart Monitoring and Automation

Sensor integration, automated backwash, and digital monitoring optimize cleaning cycles and predict element life. These systems lower operating cost and improve reliability across municipal and industrial installations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Ceramic Water Filter |

63.5% |

2025 |

|

Application |

Residential |

46.8% |

2025 |

|

Region |

Asia-Pacific |

39.4% |

2025 |

By Application

Residential commands a 46.8% majority share in 2025, driven by household water purifiers, gravity filters, and rising awareness of waterborne contaminants. The segment benefits from low maintenance, chemical-free operation, and broad appeal across urban and rural homes.

To access detailed market analysis, Request Sample

Industrial at 34.7% in 2025 covers process water treatment, flue-gas and dust filtration, and high-temperature gas cleaning across power, chemical, and metallurgical plants. The segment is expanding with tightening emission norms and water-reuse mandates.

By Product Type

Ceramic water filter dominates with 63.5% share in 2025, reflecting strong demand for durable, reusable media that removes bacteria, sediment, and turbidity without chemicals. The format is the default choice for residential and municipal drinking-water applications.

Ceramic air filter at 36.5% is expanding through diesel particulate filters, hot-gas cleaning, and industrial emission control. Its growth is supported by tightening particulate standards and the thermal stability of silicon carbide and cordierite media.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

39.4% |

Large population base, rapid industrialization, expanding water-treatment infrastructure, and rising clean-water investment |

|

North America |

24.8% |

Stringent drinking-water and emission standards, mature industrial base, and strong replacement demand |

|

Europe |

22.6% |

Strict environmental regulations, advanced wastewater reuse, and established automotive particulate filtration |

|

Latin America |

7.1% |

Growing urban water-access programs, expanding industrial activity, and rising point-of-use adoption |

|

Middle East and Africa |

6.1% |

Acute water scarcity, desalination and reuse projects, and increasing demand for durable filtration |

Asia-Pacific at 39.4% in 2025 leads the regional landscape, anchored by China, India, and Southeast Asia. Large populations, rapid industrialization, and growing investment in drinking-water and wastewater infrastructure support sustained leadership across both water and air filtration.

North America at 24.8% is supported by stringent environmental regulations, strong adoption of advanced industrial filtration technologies, substantial investment in emissions control infrastructure, and the presence of a large manufacturing and processing industry base.

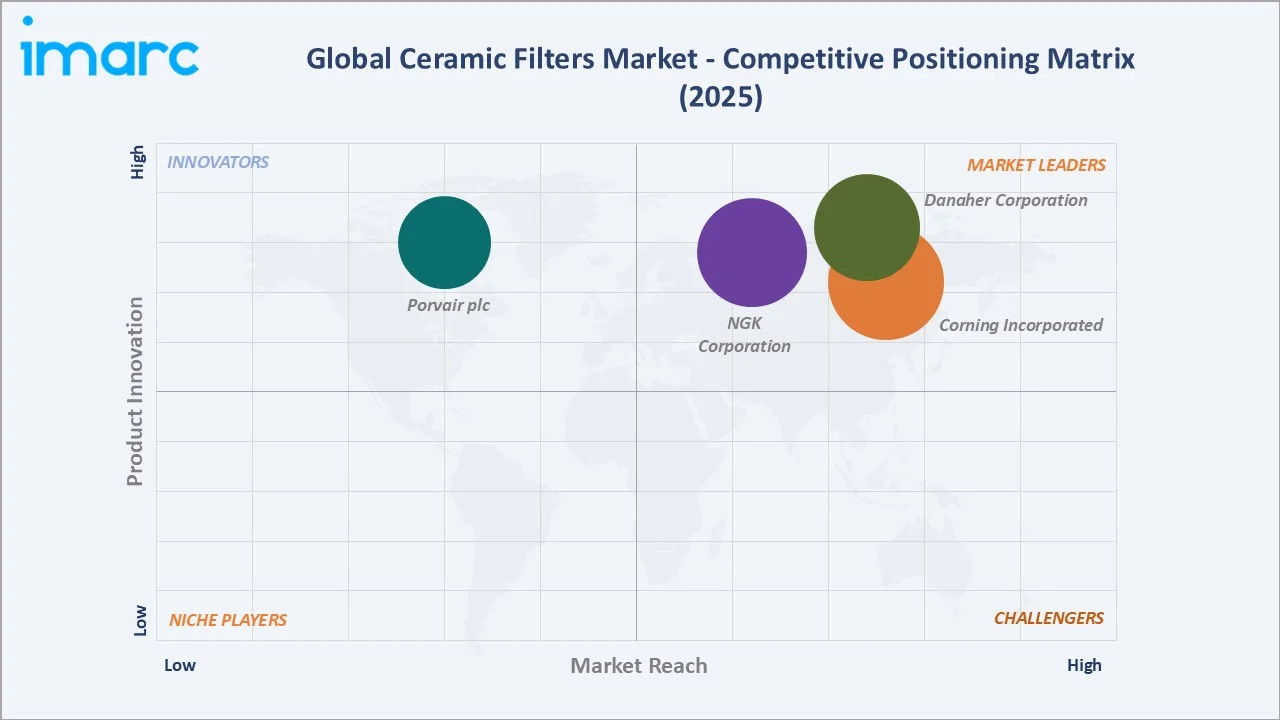

Competitive Landscape

The ceramic filters market is moderately fragmented, with established multinationals leading membrane technology and global reach while regional manufacturers compete on price and niche applications. Material expertise, sintering technology, distribution, and regulatory readiness form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Danaher Corporation |

Pall Membralox Ceramic Membranes |

Leader |

Advancing ceramic and membrane filtration for industrial and process applications |

|

Corning Incorporated |

DuraTrap Ceramic Particulate Filters |

Leader |

Scaling ceramic particulate-filter technology for vehicle emission control |

|

NGK Corporation |

Ceramic Water-Treatment Membranes |

Leader |

Expanding ceramic exhaust-purification and water-filtration technologies |

|

Porvair plc |

Selee Ceramic Foam Filters |

Innovator |

Focusing on specialized ceramic foam filtration for metal casting |

Key players include Danaher Corporation, Corning Incorporated, NGK Corporation, and Porvair plc, among others.

Key Company Profiles

Danaher Corporation

Danaher Corporation is a global science and technology company with a diversified portfolio spanning life sciences, diagnostics, and industrial technologies. Through its filtration and purification operations, it serves industrial and process customers with ceramic and membrane-based filtration solutions.

- Product Portfolio: A broad range of filtration, separation, and purification products, including ceramic membrane filters used across industrial, food and beverage, and process applications.

- Recent Developments: In September 2025, the company’s Pall Corporation business launched its Membralox GP-IC ceramic membrane systems, a graduated-permeability ceramic membrane designed for more efficient, lower-waste processing in food and ingredient production.

- Strategic Focus: Advancing ceramic and membrane filtration for industrial and process applications through ongoing product development and innovation.

Corning Incorporated

Corning Incorporated is a global materials-science company with longstanding expertise in specialty glass and ceramics. It is an established supplier of ceramic substrates and particulate filters used in automotive and industrial emission-control systems.

- Product Portfolio: Ceramic particulate filters and substrates for diesel and gasoline emission control, alongside a broader portfolio of specialty ceramic and glass technologies.

- Recent Developments: The company continues to invest in its ceramic particulate-filter and substrate capabilities to support evolving vehicle emission standards across major markets.

- Strategic Focus: Scaling ceramic particulate-filter technology for vehicle emission control while extending its environmental-technologies platform.

NGK Corporation

NGK Corporation is a Japanese ceramics manufacturer with broad expertise in advanced ceramic materials. It supplies ceramic products and membranes used across automotive emission control, water treatment, and industrial processes.

- Product Portfolio: Ceramic membranes and separators for water and liquid filtration, alongside ceramic products for exhaust purification and industrial separation applications.

- Recent Developments: The company continues to expand its ceramic membrane and filtration technologies to address water-treatment and industrial separation needs.

- Strategic Focus: Expanding ceramic exhaust-purification and water-filtration technologies across its environmental and industrial businesses.

Market Concentration Analysis

The ceramic filters market is moderately fragmented, with leading multinationals such as Danaher Corporation, Corning Incorporated, NGK Corporation, and Porvair plc, accounting for a meaningful share of global ceramic filtration through advanced membrane and emission-control technologies.

Barriers to entry include capital-intensive sintering and manufacturing, materials-science expertise, and the need for regulatory compliance across water and air applications. These factors favor well-capitalized incumbents with proprietary technology and global distribution.

Consolidation is gradual, with larger players acquiring specialist membrane and media capabilities while a broad base of regional manufacturers serves local water and air filtration demand. Partnerships with utilities, OEMs, and industrial users reinforce competitive positioning.

Investment & Growth Opportunities

Fastest-Growing Segments

Ceramic water filter and residential are expanding faster than the overall market, supported by clean-water demand and household adoption. Ceramic air filter is the next-fastest area, driven by tightening particulate-emission standards across automotive and industrial sectors.

Emerging Markets

Middle East and Africa is the fastest growing region, anchored by water scarcity, desalination, and reuse projects. Growing investments in industrial wastewater treatment and stricter environmental regulations are accelerating the adoption of advanced filtration technologies across the region.

Venture & Investment Trends

Investment is concentrated in ceramic membrane technology, silicon carbide media, and smart, sensor-enabled filtration. Capital is also flowing into water-reuse and zero-liquid-discharge projects that favor durable ceramic solutions.

Future Market Outlook (2026-2034)

The ceramic filters market is forecast to expand from USD 2.34 Billion in 2025 to USD 6.09 Billion by 2034 at a CAGR of 10.88%, adding roughly USD 3.75 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: tightening water-quality and emission standards; the shift toward ceramic membranes and silicon carbide media; growth of water reuse and point-of-use filtration; and the integration of smart monitoring across industrial installations.

By 2034, ceramic filtration is expected to be defined by higher-flux membranes, broader emission-control adoption, and digitally monitored systems. Sustainability, durability, and regulatory compliance will further accelerate the transition toward engineered ceramic solutions.

Research Methodology

Primary Research

Primary research included structured interviews with filter manufacturers, water-utility engineers, industrial procurement leads, and materials specialists, validating market sizing, regional demand, application mix, and product-type evolution.

Secondary Research

Secondary sources included publications from the World Health Organization, environmental regulators such as the United States Environmental Protection Agency and the European Union, national water-infrastructure programs, industry associations, and company annual reports and investor presentations.

Forecasting Models

Market forecasts used top-down and bottom-up models combining installed-base estimates, replacement cycles, application mix, regulatory scenarios, and macroeconomic variables. Scenario analysis addressed regulatory pace, raw-material costs, and competing filtration technologies.

Ceramic Filters Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Ceramic Water Filter, Ceramic Air Filter |

| Applications Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Danaher Corporation, Corning Incorporated, NGK Corporation, Porvair plc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the ceramic filters market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global ceramic filters market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the ceramic filters industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Ceramic Filters Market Report

The ceramic filters market was valued at USD 2.34 Billion in 2025, driven by rising clean-water demand, stricter emission standards, and growing adoption of durable ceramic filtration media.

The market is projected to grow at 10.88% CAGR from 2026 to 2034, reaching USD 6.09 Billion, supported by ceramic membrane adoption and expanding industrial emission control.

Residential leads at 46.8% in 2025, driven by household water purifiers and the growing clean-water awareness. Rising concerns regarding water quality, health, and access to safe drinking water continue to support sustained demand across urban and suburban households.

Ceramic water filter dominates at 63.5% in 2025, fueled by chemical-free, reusable purification. The segment also benefits from its effectiveness in removing suspended particles and pathogens without requiring electricity, making it suitable for both urban and rural applications.

Asia-Pacific commands 39.4% in 2025, led by large populations, rapid industrialization, and growing investment in water-treatment infrastructure.

Leading players include Danaher Corporation, Corning Incorporated, NGK Corporation, and Porvair plc, among others.

Key drivers include rising demand for clean drinking water, stricter air-quality and emission regulations, and the durability, thermal resistance, and reusability of ceramic filtration media. Growing industrial adoption across wastewater treatment, chemical processing, and pollution control applications is further supporting market expansion.

Advances in ceramic membranes, silicon carbide media, and smart sensor-enabled filtration are improving efficiency, service life, and monitoring, raising adoption across water and industrial applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)