Ceramic Matrix Composites Market Size, Share, Trends and Forecast by Composite Type, Fiber Type, Fiber Material, Application, and Region, 2026-2034

Ceramic Matrix Composites Market Size and Share:

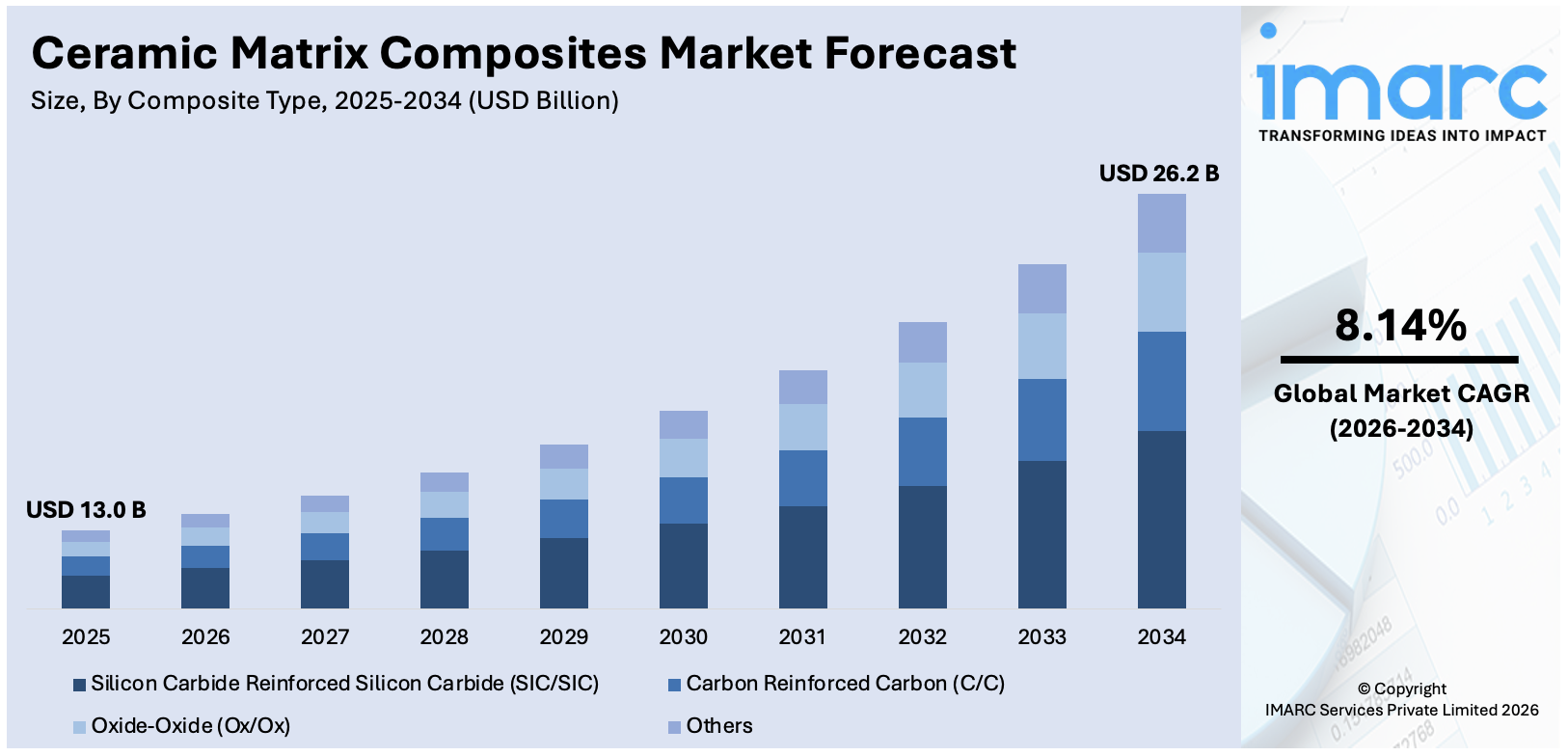

The global ceramic matrix composites market size was valued at USD 13.0 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 26.2 Billion by 2034, exhibiting a CAGR of 8.14% during 2026-2034. North America currently dominates the market, holding a significant market share of around 42.8% in 2025. The market is driven by the development of new CMCs using nanoscience and nanotechnology to improve properties and electrical conductivity. This, along with the expansion of the automotive industry, government initiatives modernizing defense equipment, and the growing need for lightweight, high-strength materials in the aerospace and defense industries, is fueling the ceramic matrix composites market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 13.0 Billion |

|

Market Forecast in 2034

|

USD 26.2 Billion |

| Market Growth Rate 2026-2034 | 8.14% |

The market is experiencing significant expansion due to the increased adoption of power generation turbines, particularly in high-efficiency gas turbines operating at elevated temperatures. Moreover, ongoing research funding by defense agencies into lightweight armor solutions is further accelerating the development of CMC applications. Additionally, the transition toward renewable energy infrastructure, including concentrated solar power systems, is stimulating interest in thermally resilient materials. For instance, on July 4, 2024, the Solar Energy Corporation of India (SECI) announced plans to launch a 500-megawatt concentrated solar thermal (CST) tender by the end of the fiscal year, making it the country's largest such endeavor to date. This project aims to improve round-the-clock renewable energy supply, with possible sites identified in strong solar radiation areas like Andhra Pradesh, Gujarat, and Rajasthan. Apart from this, strategic investments by aerospace suppliers to localize production are also fostering supply chain stability and capacity building, supporting sustained market advancement.

To get more information on this market Request Sample

In the United States, the market is driven by increased collaboration between defense contractors and advanced material manufacturers for next-generation missile and aircraft technologies. Furthermore, the growing emphasis on reducing lifecycle costs in aerospace maintenance is leading to the substitution of conventional alloys with CMCs, especially in turbine and exhaust applications. The United States' goal to lower greenhouse gas (GHG) emissions by 61–66% below 2005 levels by 2035 is playing a pivotal role in accelerating the transition toward cleaner energy solutions. Alongside this, domestic policies that emphasize energy efficiency and carbon emission reduction are indirectly driving the demand for advanced materials, particularly high-performance thermal barrier materials. In addition to this, the expansion of electric vertical takeoff and landing (eVTOL) programs by U.S.-based aviation startups is creating lucrative opportunities for the market.

Ceramic Matrix Composites Market Trends:

Growing Adoption in Next-Generation Aircraft Propulsion Systems

The aerospace sector is experiencing a transformative shift toward advanced propulsion technologies that demand materials capable of operating at unprecedented temperatures while maintaining structural integrity. Ceramic matrix composites have emerged as the cornerstone of this evolution, enabling jet engines to function at temperatures exceeding those tolerable by traditional nickel-based superalloys. Major aerospace manufacturers are integrating CMCs into critical engine components including turbine shrouds, combustor liners, and nozzle assemblies, allowing for reduced cooling requirements and improved thermal efficiency. The ability of these composites to withstand extreme operational conditions while weighing significantly less than conventional materials translates directly into enhanced fuel economy and extended component lifecycles. This strategic material substitution is driving substantial performance improvements across commercial and military aviation platforms, positioning CMCs as an essential enabler of future propulsion architectures that prioritize sustainability alongside performance enhancements.

Accelerating Investment in Defense Modernization Programs

Governments worldwide are channeling substantial resources into upgrading their defense capabilities, with ceramic matrix composites playing an increasingly vital role in next-generation weapon systems and military platforms. The unique combination of high-temperature resistance, ballistic protection capabilities, and lightweight characteristics makes CMCs particularly valuable for applications ranging from hypersonic missile components to thermal protection systems for advanced aircraft. Defense agencies are actively partnering with material science companies and research institutions to accelerate the integration of CMCs into mission-critical applications where performance under extreme conditions is paramount. These initiatives encompass not only the development of new composite formulations but also the establishment of domestic manufacturing capabilities to ensure supply chain resilience and strategic autonomy. The focus on indigenous production and technological self-reliance is fostering innovation ecosystems that combine public sector funding with private sector expertise, creating sustainable demand drivers that extend beyond traditional procurement cycles.

Expansion into Clean Energy and Industrial Decarbonization Applications

The global transition toward sustainable energy systems is creating significant opportunities for ceramic matrix composites in renewable energy infrastructure and industrial efficiency improvements. High-efficiency gas turbines operating at elevated temperatures for power generation increasingly rely on CMC components to achieve performance targets while reducing emissions. Concentrated solar power installations utilize these advanced materials in receiver systems where extreme thermal cycling and corrosive environments demand exceptional durability. The potential for CMCs to enable waste heat recovery in energy-intensive industries such as steel manufacturing represents another emerging application area where thermal management capabilities directly translate into operational cost savings and environmental benefits. Material developers are responding to these opportunities by optimizing composite formulations for specific energy sector requirements, balancing performance characteristics with cost considerations to enable broader commercial adoption across applications where traditional materials face fundamental limitations in meeting simultaneous demands for efficiency, longevity, and environmental compliance.

Ceramic Matrix Composites Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global ceramic matrix composites market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on composite type, fiber type, fiber material, and application.

Analysis by Composite Type:

- Silicon Carbide Reinforced Silicon Carbide (SIC/SIC)

- Carbon Reinforced Carbon (C/C)

- Oxide-Oxide (Ox/Ox)

- Others

Silicon carbide reinforced silicon carbide (SIC/SIC) leads the market with around 35.2% of market share in 2025 due to their exceptional qualities such as high-temperature resistance, mechanical strength, and thermal stability. These composites are widely used in industries such as aerospace, automotive, and energy, where materials must withstand extreme conditions. SiC/SiC composites are known for their lightweight properties, which make them ideal for applications in aircraft engines and turbine systems, where performance and fuel efficiency are paramount. Additionally, their ability to resist wear, corrosion, and thermal shock enhances their durability in high-stress environments. As demand for advanced materials grows, particularly in sectors focused on sustainability and energy efficiency, SiC/SiC composites are expected to experience substantial growth. Their role in replacing metals and other materials in critical applications makes them a key component in the CMC market.

Analysis by Fiber Type:

- Short Fiber

- Continuous Fiber

Continuous fiber leads the market with around 69.4% of market share in 2025 due to its ability to provide improved structural integrity, damage tolerance, and load-carrying capacity. These fibers are usually constructed of silicon carbide, alumina, or other high-performance ceramics. They are oriented in a directional mode within the matrix, yielding higher strength and stiffness along the fiber axis. Continuous fiber-reinforced CMCs are extremely useful for high-stress, high-temperature applications such as aerospace propulsion systems, gas turbines, and engine parts in the automotive industry. In contrast to short or whisker-type reinforcement, continuous fibers allow for designing parts with consistent mechanical response and enhanced fracture resistance. They also accommodate weight reduction strategies by substituting heavier metal components without compromising performance. With increased demands from industries on thermal resistance and longer service life for structural materials, continuous fiber-reinforced CMCs have been increasingly used, making them a vital segment of the market.

Analysis by Fiber Material:

- Alumina Fiber

- Refractory Ceramic Fiber (RCF)

- SiC Fiber

- Others

SiC fiber leads the market with around 43.1% of market share in 2025 due to its high mechanical strength, thermal stability, as well as its ability to resist corrosion and oxidation. SiC fibers are typically applied within high-performance CMCs where materials need to withstand severe temperatures and harsh environments, such as aerospace turbine parts, nuclear reactors, and efficient industrial systems. Their high modulus and heat conductivity properties make them perfectly suited for structural uses, which require both stiffness and heat removal. SiC fiber also plays an important role in both the toughness and fatigue resistance of the composite, allowing for longer life in harsh environments. SiC's performance profile is compared favorably to other fiber forms in having an excellent balance that fits the exacting needs of next-generation propulsion systems and energy technologies. As defense, aerospace, and clean energy innovation proceed, the applications of SiC fiber grow increasingly diverse, solidifying its role in the CMC industry.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Aerospace and Defense

- Automotive

- Energy and Power

- Electricals and Electronics

- Others

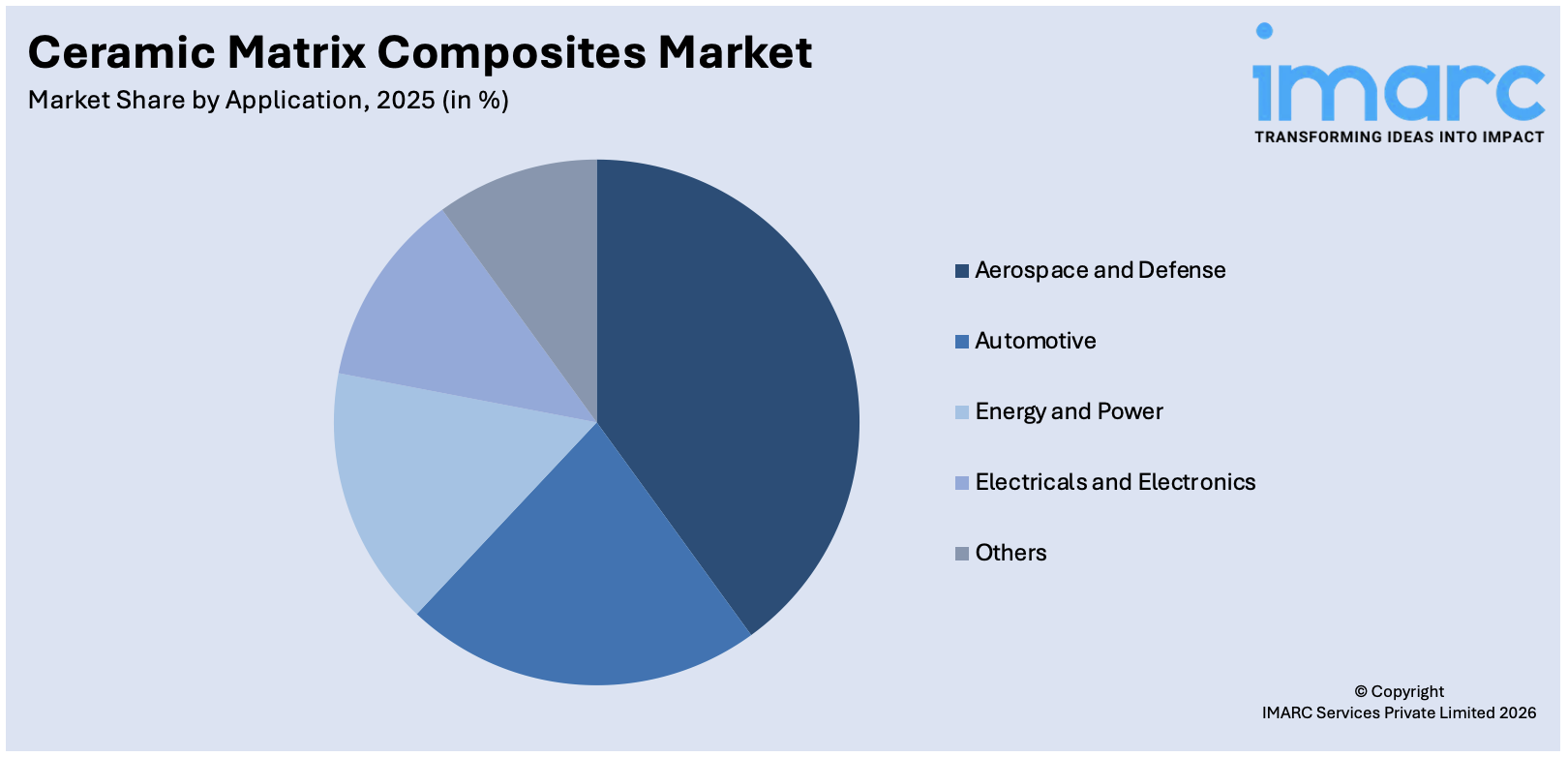

Aerospace and defense lead the market with around 51.1% of market share in 2025 due to the demand for composites that can support extremely high temperatures, mechanical loads, and corrosive conditions. CMCs have several benefits over conventional metals in high-performance aerospace parts like turbine blades, combustor liners, exhaust nozzles, and thermal protection systems. Their light weight adds to fuel efficiency, and the fact that they maintain mechanical strength at high temperatures enhances engine performance and longevity. In defense applications, CMCs are employed in missile parts, hypersonic missiles, and defense armor systems where high thermal shock resistance along with strength-to-weight ratio are essential. The transition to higher efficiency and novel propulsion systems has further enhanced the use of CMCs in defense. As aerospace industries and defense organizations look for stronger and lighter materials, ceramic matrix composites are increasingly becoming a strategic material of choice in key applications.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 42.8% driven by high demand from the aerospace, defense, and energy industries. The region has large aircraft makers, defense contractors, and space exploration organizations that depend on high-temperature, lightweight, and strong components made with advanced materials. The U.S. Department of Defense and NASA have been major contributors to CMC development, supporting research and integration into turbine engines, hypersonic vehicles, and thermal protection systems. Moreover, the presence of established players in North America drives innovation and adoption of CMCs across commercial and military aircraft. The regional emphasis on increasing fuel efficiency, lowering emissions, and boosting engine performance also lends credence to the utilization of CMCs instead of traditional alloys. With continued investment in clean energy and aerospace technologies, the region remains a significant and strategic market for ceramic matrix composites.

Key Regional Takeaways:

United States Ceramic Matrix Composites Market Analysis

The United States ceramic matrix composites market benefits from a robust ecosystem combining world-leading aerospace manufacturers, defense contractors, and advanced materials research institutions that collectively drive innovation and commercial adoption. The aerospace industry's concentration within the country, coupled with substantial defense spending, creates sustained demand for high-performance materials capable of enhancing aircraft engine efficiency and military system capabilities. Collaborative initiatives between government agencies and private sector companies are accelerating the development and qualification of CMC components for both commercial aviation and defense applications, with programs specifically targeting thermal management solutions for next-generation propulsion systems. The domestic emphasis on reducing greenhouse gas emissions is indirectly supporting market expansion by incentivizing the adoption of fuel-efficient technologies where weight reduction and thermal performance improvements directly contribute to environmental objectives. Manufacturing capacity investments are establishing vertically integrated supply chains that encompass fiber production, composite fabrication, and component assembly, enhancing cost competitiveness while ensuring quality control across the value chain. The emergence of commercial space ventures and electric vertical takeoff and landing aircraft development programs is creating additional demand vectors for CMC applications beyond traditional aerospace and defense sectors, positioning the market for sustained growth.

Europe Ceramic Matrix Composites Market Analysis

Europe's ceramic matrix composites market demonstrates strong momentum driven by stringent environmental regulations, ambitious sustainability targets, and significant investments in aerospace and clean energy technologies. The automotive industry's transition toward electrification and emissions reduction is creating demand for lightweight, heat-resistant materials that improve vehicle efficiency and enable advanced thermal management systems. Renewable energy initiatives, particularly wind power expansion and emerging concentrated solar technologies, are driving adoption of CMCs in applications requiring exceptional durability under challenging operational conditions. The amended regulatory framework for renewable energy establishes clear targets that incentivize investment in enabling technologies including advanced materials for energy systems. Defense sector modernization efforts across European nations are supporting development programs that incorporate CMC components into military aircraft and weapon systems where performance advantages justify material qualification investments. Regional cooperation on aerospace programs facilitates technology sharing and joint development activities that accelerate material adoption while distributing development costs across multiple stakeholders. Research institutions throughout Europe are advancing fundamental understanding of composite behavior and developing novel processing techniques that enhance manufacturing efficiency and component performance for diverse application requirements.

Asia Pacific Ceramic Matrix Composites Market Analysis

The Asia Pacific ceramic matrix composites market is experiencing rapid expansion fueled by substantial industrial growth, increasing defense expenditures, and major infrastructure development initiatives across multiple countries. Rapid industrialization in large economies is driving demand for advanced materials across automotive, aerospace, and energy sectors where performance improvements directly impact competitiveness. The aerospace industry's growth trajectory, supported by rising air travel demand and domestic aircraft production capabilities, is creating sustained requirements for lightweight, high-temperature materials in engine and airframe applications. Defense modernization programs throughout the region are prioritizing indigenous development of advanced military capabilities, with ceramic matrix composites identified as strategic materials for next-generation weapon systems and aircraft. High-speed rail network expansions require materials capable of withstanding thermal and mechanical stresses associated with high-velocity operations, creating additional application opportunities beyond traditional aerospace uses. Government investments in research and development infrastructure are building domestic capabilities in composite manufacturing and supporting technology transfer initiatives that reduce dependence on foreign material sources. The renewable energy sector's expansion, driven by sustainability commitments and energy security considerations, is generating demand for CMCs in wind turbines and emerging energy storage technologies where material performance directly influences system economics and reliability.

Latin America Ceramic Matrix Composites Market Analysis

Latin America's ceramic matrix composites market is progressing steadily, supported by expanding aerospace and defense sectors alongside growing interest in renewable energy infrastructure development. Defense modernization initiatives are driving investments in advanced technologies that enhance national security capabilities, with ceramic matrix composites recognized as enabling materials for next-generation military systems. Government programs aimed at strengthening domestic defense industrial capabilities are allocating substantial resources toward technology development in areas including propulsion systems and protective materials where CMCs offer performance advantages over conventional alternatives. The renewable energy sector's expansion, particularly in solar and wind power generation, is creating demand for durable materials capable of withstanding challenging environmental conditions while maintaining operational efficiency over extended service lives. The automotive industry's ongoing evolution toward more fuel-efficient vehicles is gradually increasing awareness of advanced materials including CMCs that contribute to weight reduction and thermal management improvements. Industrial applications in sectors such as chemical processing and manufacturing are beginning to recognize the value proposition of materials offering superior thermal resistance and longevity in harsh operating environments, though adoption rates remain relatively modest compared to more mature markets.

Middle East and Africa Ceramic Matrix Composites Market Analysis

The Middle East and Africa ceramic matrix composites market is influenced significantly by the energy sector's dominance and expanding infrastructure development activities across the region. Oil and gas operations requiring materials capable of withstanding extreme temperatures and corrosive conditions in processing equipment represent established application areas for advanced composites. Infrastructure investments in power generation facilities, particularly combined cycle plants and emerging renewable energy projects, are driving adoption of CMCs in turbine applications where efficiency improvements directly translate into operational cost savings. Defense modernization efforts undertaken by multiple nations within the region are creating demand for high-performance materials that enable advanced military capabilities, with aerospace applications receiving particular emphasis as air forces upgrade equipment and capabilities. The growing number of renewable energy projects, including large-scale solar installations leveraging concentrated solar power technologies, requires materials offering exceptional thermal durability and long-term reliability under intense solar radiation and temperature cycling conditions. Manufacturing sector development initiatives aimed at economic diversification are beginning to recognize advanced materials as enablers of high-value industrial activities, though market development remains at relatively early stages compared to established industrial regions.

Competitive Landscape:

The market is characterized by a growing focus on innovation, proprietary manufacturing technologies, and performance optimization. Market players are investing heavily in research and development (R&D) activities to enhance thermal resistance, reduce weight, and improve mechanical strength across various CMC product lines. Strategic collaborations with aerospace, defense, and energy sector clients are common, enabling tailored solutions that meet stringent regulatory and operational requirements. Moreover, companies compete by differentiating material capabilities, scalability of manufacturing, and lifecycle performance of their offerings. Additionally, geographic expansion and long-term supply agreements with original equipment manufacturers (OEMs) play a critical role in sustaining market position. According to the ceramic matrix composites market forecast, the shift toward sustainable and high-efficiency materials is the shift toward sustainable and high-efficiency materials is expected to intensify market competition further, encouraging the development of advanced composites that balance performance with cost-effectiveness, particularly for emerging applications in the automotive and energy sectors.

The report provides a comprehensive analysis of the competitive landscape in the ceramic matrix composites market with detailed profiles of all major companies, including:

- 3M Company

- Applied Thin Films Inc.

- Axiom Materials Inc.

- CeramTec GmbH

- COI Ceramics Inc.

- CoorsTek Inc.

- Lancer Systems LP

- SGL Carbon SE

- Specialty Materials Inc. (Global Materials LLC)

- Starfire Systems Inc.

- Ultramet

Latest News and Development:

- April 2025: Firefly Aerospace received a contract from the US Air Force Research Laboratory for the development of a ceramic matrix composite rocket engine nozzle extension. This innovative material aims to reduce nozzle mass by over 50 percent, enhancing payload capacity and lowering production costs compared to traditional metal-based extensions.

- February 2025: Tethon 3D acquired Technology Assessment and Transfer Inc., enhancing its ceramic manufacturing capabilities. TA&T specializes in advanced technologies for aerospace, defense, and biomedical sectors, including ceramic matrix composites and additive manufacturing. The acquisition will expand Tethon's portfolio and strengthen its global market presence.

- February 2025: SRI developed scalable, infiltration-free carbon/carbon ceramic matrix composites as part of two U.S. Department of Energy projects. These CMCs were manufactured in 3-5 days with less than 5 percent shrinkage, under 10 percent porosity, and at half the expense of traditional composites, effectively eliminating the expensive infiltration step.

Ceramic Matrix Composites Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Composite Types Covered | Silicon Carbide Reinforced Silicon Carbide (SIC/SIC), Carbon Reinforced Carbon (C/C), Oxide-Oxide (Ox/Ox), Others |

| Fiber Types Covered | Short Fiber, Continuous Fiber |

| Fiber Materials Covered | Alumina Fiber, Refractory Ceramic Fiber (RCF), SiC Fiber, Others |

| Applications Covered | Aerospace and Defense, Automotive, Energy and Power, Electricals and Electronics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | 3M Company, Applied Thin Films Inc., Axiom Materials Inc., CeramTec GmbH, COI Ceramics Inc., CoorsTek Inc., Lancer Systems LP, SGL Carbon SE, Specialty Materials Inc. (Global Materials LLC), Starfire Systems Inc., Ultramet, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the ceramic matrix composites market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global ceramic matrix composites market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the ceramic matrix composites industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Ceramic Matrix Composites Market Report

The ceramic matrix composites market was valued at USD 13.0 Billion in 2025.

The ceramic matrix composites market is projected to exhibit a CAGR of 8.14% during 2026-2034, reaching a value of USD 26.2 Billion by 2034.

The market is driven by increasing demand for lightweight, high-performance materials in aerospace and defense, rising application in automotive and energy sectors, growing preference for fuel-efficient aircraft, and improved heat resistance and structural integrity under extreme conditions, making them ideal for turbines, engines, and braking systems.

North America currently dominates the ceramic matrix composites market with a market share of around 42.8%. The dominance is fueled by strong presence of aerospace and defense manufacturers, significant investments in advanced material R&D, government support for defense upgrades, and rising adoption of energy-efficient technologies in aviation and power generation sectors.

Some of the major players in the ceramic matrix composites market include 3M Company, Applied Thin Films Inc., Axiom Materials Inc., CeramTec GmbH, COI Ceramics Inc., CoorsTek Inc., Lancer Systems LP, SGL Carbon SE, Specialty Materials Inc. (Global Materials LLC), Starfire Systems Inc., and Ultramet, among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)