China Cloud Gaming Market Size, Share, Trends and Forecast by Device Type, Genre, Technology, Gamers, and Region, 2026-2034

China Cloud Gaming Market Overview:

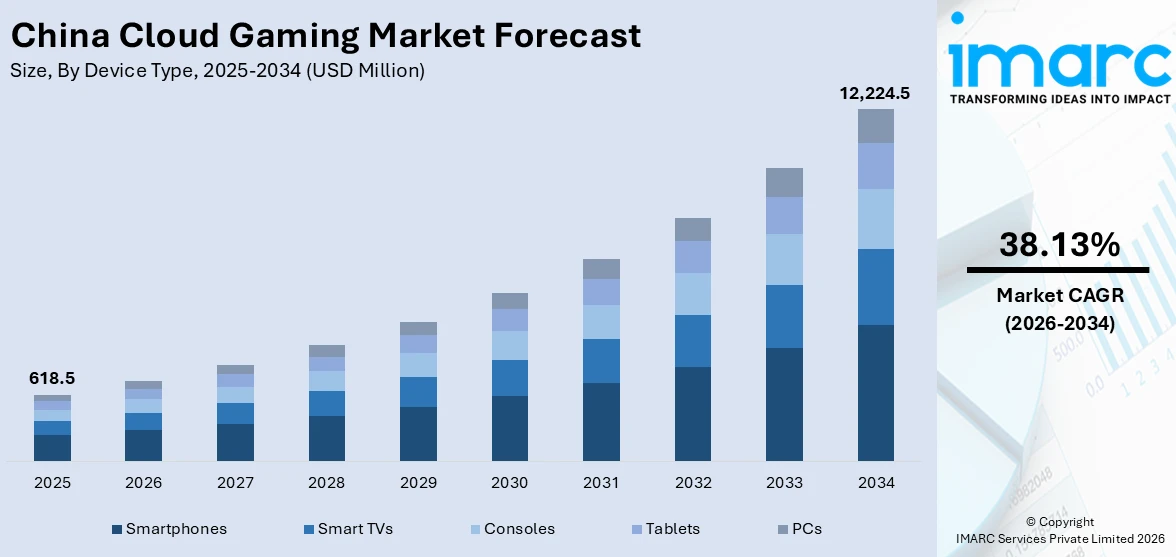

The China cloud gaming market size reached USD 618.5 Million in 2025. The market is projected to reach USD 12,224.5 Million by 2034, exhibiting a growth rate (CAGR) of 38.13% during 2026-2034. The market is fueled by the faster development of 5G infrastructure that supports low-latency online gaming experiences, artificial intelligence integration that revolutionizes game development and player interaction, and heavy government investment in digital infrastructures for hosting cloud computing ecosystems. The increasing usage of mobile phones and mobile devices, along with the rising number of cloud data center deployments in Chinese regions, is also increasing the China cloud gaming market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 618.5 Million |

| Market Forecast in 2034 | USD 12,224.5 Million |

| Market Growth Rate 2026-2034 | 38.13% |

China Cloud Gaming Market Trends:

Fast Rollout of 5G Network Infrastructure and Access to High-Speed Internet

The rapid expansion of 5G networks throughout China is strongly fueling the development of cloud gaming. Low-latency and fast connectivity allow real-time streaming of heavy graphics games without dependence on powerful local hardware, cutting down on entry barriers for players. Telecommunications companies and technology companies are heavily investing in increasing 5G reach, especially in urban and semi-urban pockets, making gameplay smooth and reducing round-trip latency issues that used to lead to hesitation. This is complemented by government programs supporting digital infrastructure development, such as fiber-optic infrastructure and integration of edge computing. Further, 5G-capable data centers enable cloud gaming platforms to handle large-scale multiplayer interactions and intricate game rendering efficiently. The mass adoption of mobile devices and tablets further complements the infrastructure development to enable users to access high-quality gaming sessions on the move. With improved connectivity, the market will have the potential to engage a wider population of casual and competitive gamers, enabling opportunities for differentiation in services through latency, streaming quality, and dependability.

To get more information on this market Request Sample

Investment and Platform Diversification

Major Chinese technology companies are investing heavily in cloud gaming platforms to tap the growing user base. The companies are using proprietary cloud infrastructures and artificial intelligence-based optimization to provide high-quality, scalable gaming experiences. Investment plans include buying smaller gaming studios, collaborating with global developers, and deployment of specialized cloud gaming servers. Platform expansion is a significant trend, with suppliers providing subscription-based models, pay-per-play models, and freemium models to suit diversified consumer segments. The integration of cloud gaming with pre-existing ecosystems, like social media applications, e-commerce sites, and video streaming services, provides a synergistic environment that fosters cross-platform activity and increases monetization possibilities. The focus on proprietary content, exclusive titles, and selective partnerships enables companies to make their services distinct and create dedicated user bases. The trend represents a move away from the historic console and PC gaming model toward one centered around the cloud, which is capable of scaling economically and addressing changing consumer demands for instant access and cross-device usage.

Cutting-Edge Technologies Improving User Experience and Operations

Technological innovation is a trend influencing the China cloud gaming market growth, with the use of AI, edge computing, and enhanced graphics rendering technologies. AI-based algorithms minimize network traffic, forecast user actions, and dynamically modify graphics quality to provide seamless gameplay and low latency. Edge computing enables game data to be processed nearer to end-users, minimizing server response times and enhancing real-time performance, which is essential for aggressive multiplayer gaming. Furthermore, cloud platforms are increasingly integrating virtual reality (VR) and augmented reality (AR) features to provide immersive experiences that were formerly limited to high-end devices. These advances in technology also allow providers to deliver customized gaming experiences, such as adaptive difficulty levels, content suggestions, and social networking, improving user retention and engagement. In addition, automation of backend operations like server load balancing and management of game sessions enhances operational efficiency while lowering costs. The incorporation of these technologies makes cloud gaming a credible, high-quality alternative to conventional gaming systems, stimulating innovation and establishing new benchmarks for the entire gaming ecosystem within China.

China Cloud Gaming Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on device type, genre, technology, and gamers.

Device Type Insights:

- Smartphones

- Smart TVs

- Consoles

- Tablets

- PCs

The report has provided a detailed breakup and analysis of the market based on the device type. This includes smartphones, smart TVs, consoles, tablets, and PCs.

Genre Insights:

Access the comprehensive market breakdown Request Sample

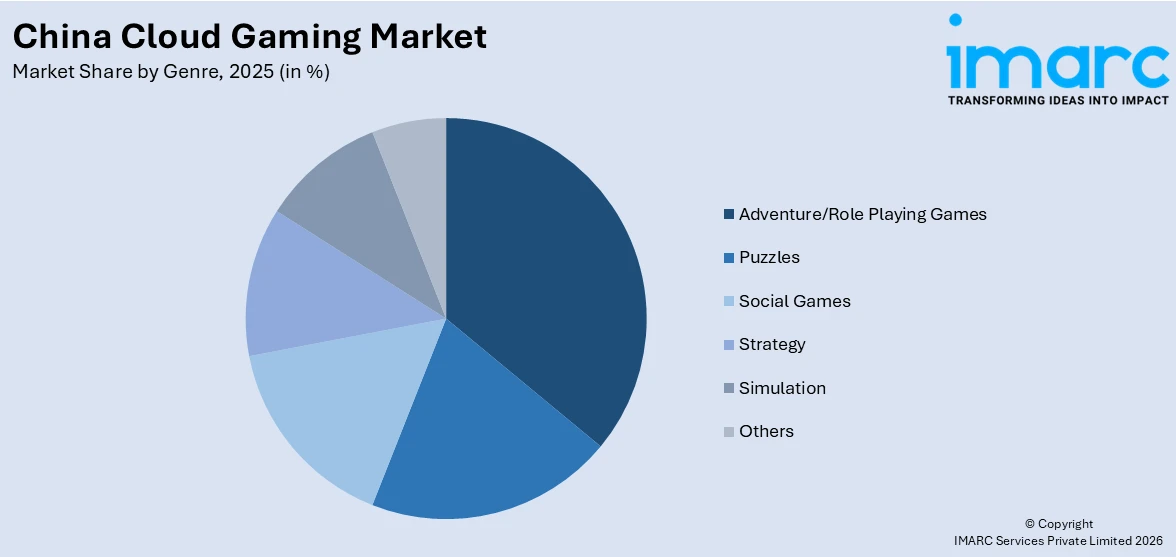

- Adventure/Role Playing Games

- Puzzles

- Social Games

- Strategy

- Simulation

- Others

A detailed breakup and analysis of the market based on the genre have also been provided in the report. This includes adventure/role playing games, puzzles, social games, strategy, simulation, and others.

Technology Insights:

- Video Streaming

- File Streaming

The report has provided a detailed breakup and analysis of the market based on the technology. This includes video streaming and file streaming.

Gamers Insights:

- Hardcore Gamers

- Casual Gamers

A detailed breakup and analysis of the market based on the gamers have also been provided in the report. This includes hardcore gamers and casual gamers.

Regional Insights:

- North China

- East China

- South Central China

- Southwest China

- Northwest China

- Northeast China

The report has also provided a comprehensive analysis of all the major regional markets, which include North China, East China, South Central China, Southwest China, Northwest China, and Northeast China.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

China Cloud Gaming Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Devices Types Covered | Smartphones, Smart TVs, Consoles, Tablets, PCs |

| Genres Covered | Adventure/Role Playing Games, Puzzles, Social Games, Strategy, Simulation, Others |

| Technologies Covered | Video Streaming, File Streaming |

| Gamers Covered | Hardcore Gamers, Casual Gamers |

| Regions Covered | North China, East China, South Central China, Southwest China, Northwest China, Northeast China |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the China cloud gaming market performed so far and how will it perform in the coming years?

- What is the breakup of the China cloud gaming market on the basis of device type?

- What is the breakup of the China cloud gaming market on the basis of genre?

- What is the breakup of the China cloud gaming market on the basis of technology?

- What is the breakup of the China cloud gaming market on the basis of gamers?

- What is the breakup of the China cloud gaming market on the basis of region?

- What are the various stages in the value chain of the China cloud gaming market?

- What are the key driving factors and challenges in the China cloud gaming market?

- What is the structure of the China cloud gaming market and who are the key players?

- What is the degree of competition in the China cloud gaming market?

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the China cloud gaming market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the China cloud gaming market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the China cloud gaming industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)