China Cosmetic Surgery Market Size, Share, Trends and Forecast by Gender, Type, Age Group, and Region 2026-2034

China Cosmetic Surgery Market Size, Share, Trends & Forecast (2026-2034)

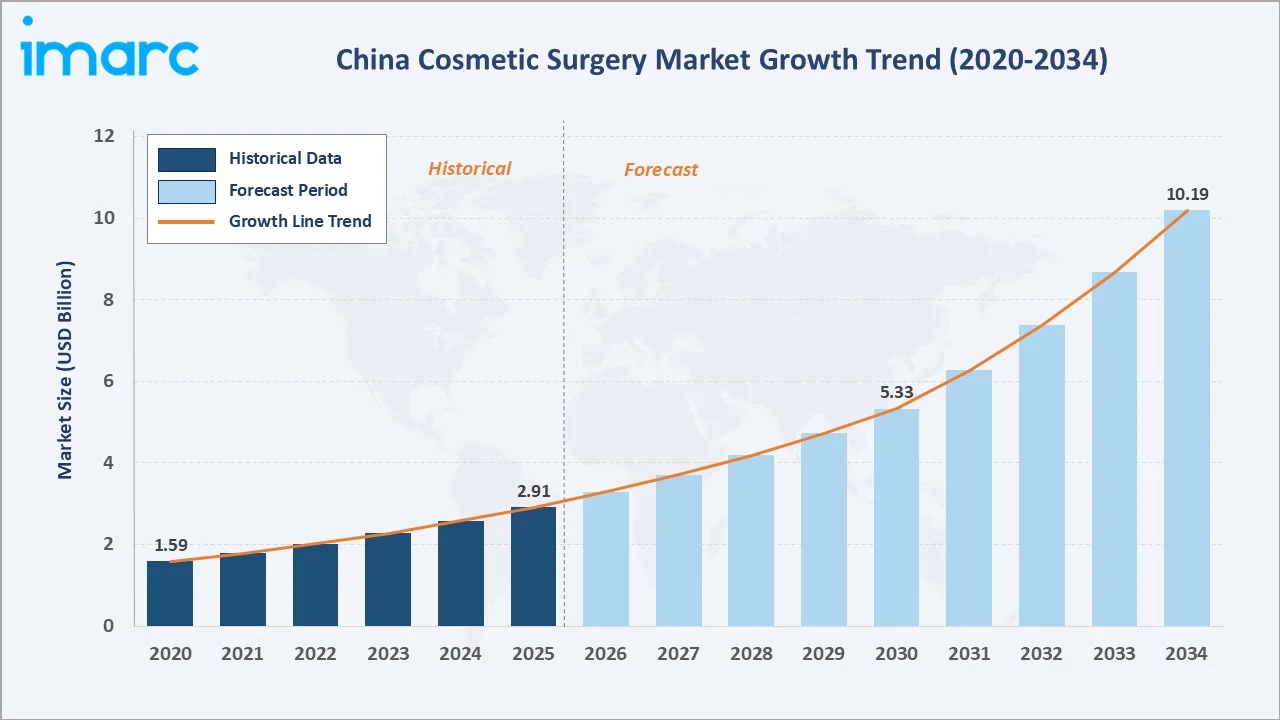

The China cosmetic surgery market size reached USD 2.91 Billion in 2025 and is projected to reach USD 10.19 Billion by 2034, exhibiting a CAGR of 12.86% during 2026-2034. Rising middle-class spending, social media-driven beauty consciousness, rapid adoption of minimally invasive aesthetic procedures, and the proliferation of licensed cosmetic surgery hospitals across tier-1 and tier-2 cities are the primary forces driving market growth.

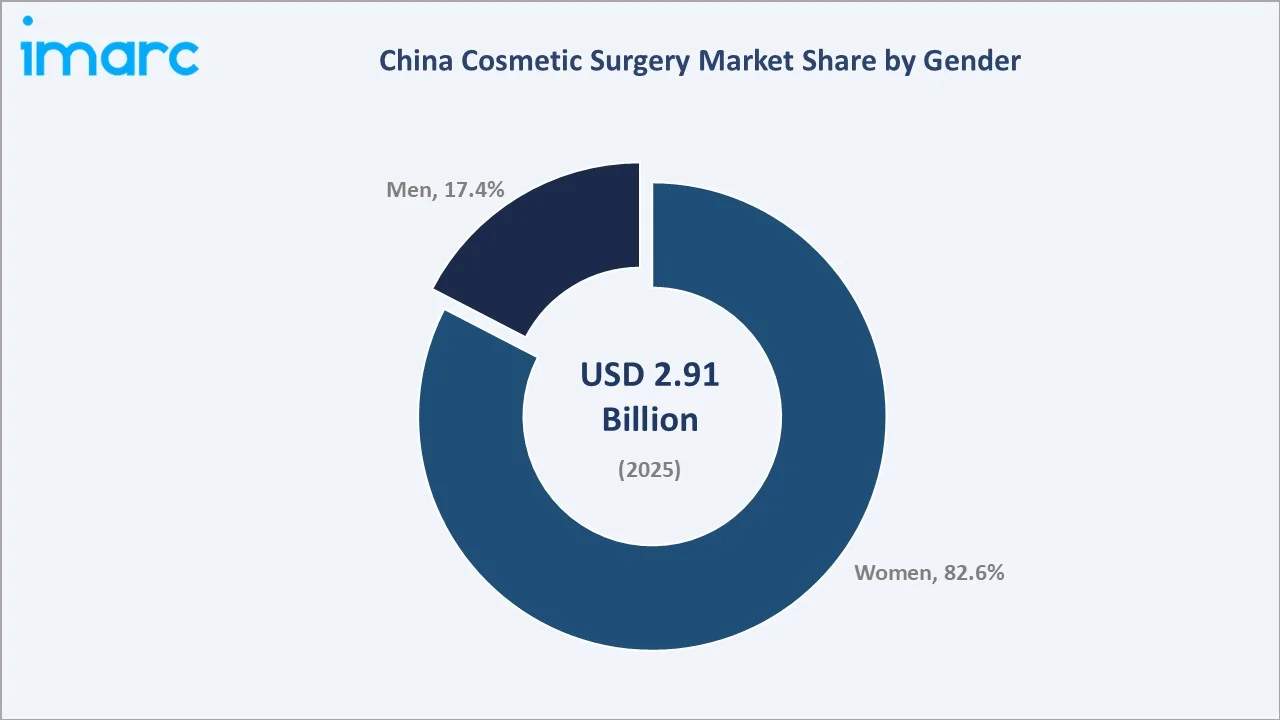

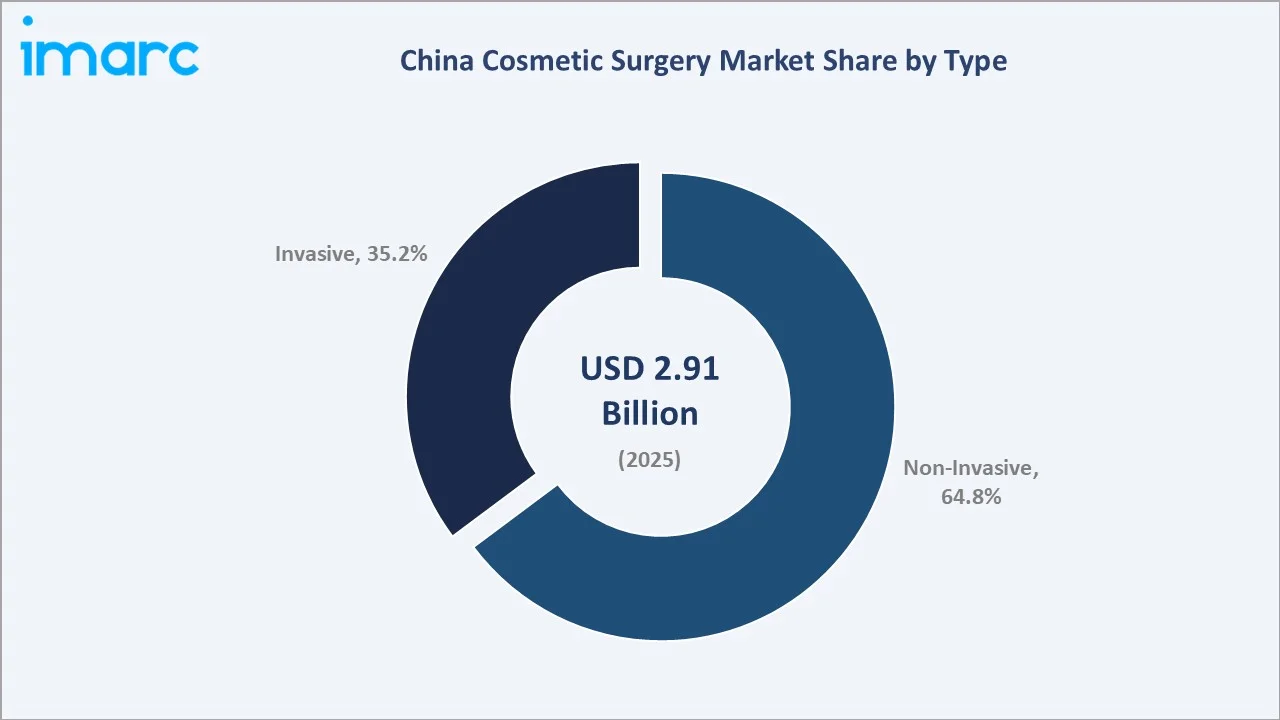

Women dominate the gender mix at 82.6% in 2025, while non-invasive procedures lead the type segment at 64.8%.

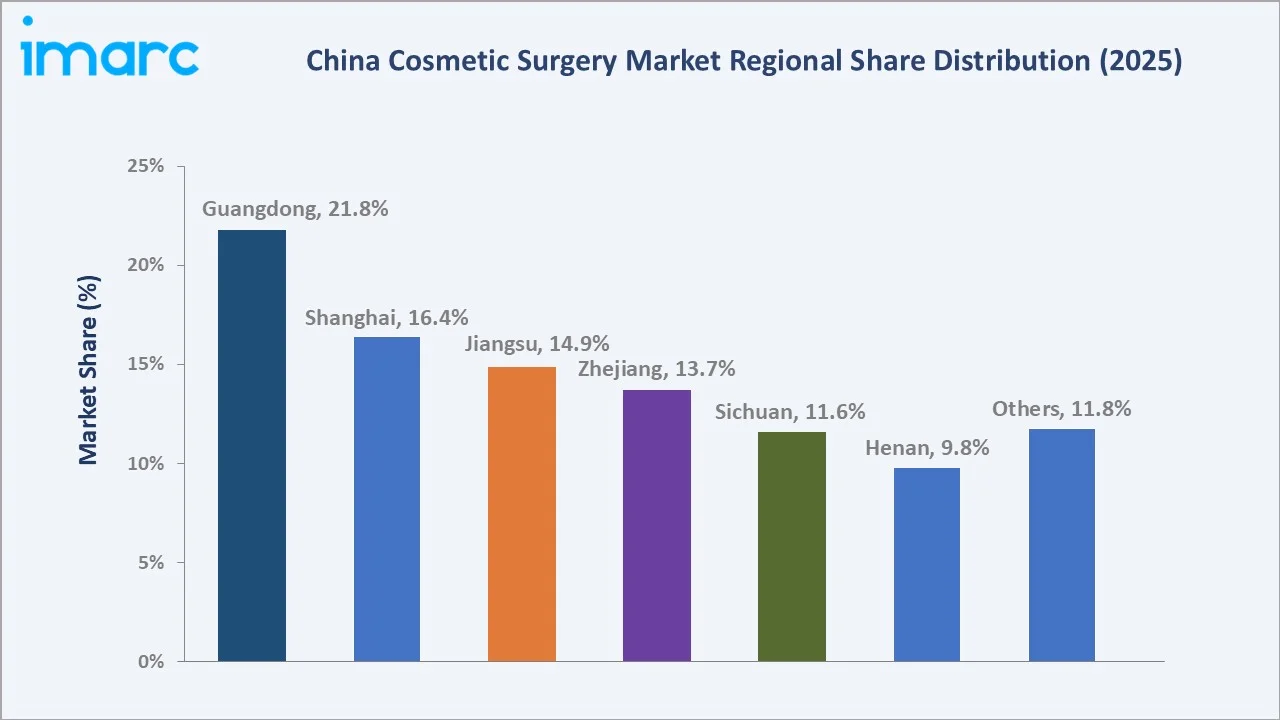

Guangdong commands a leading 21.8% regional share in 2025, reflecting high disposable income and dense licensed clinic concentration across the Greater Bay Area.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.91 Billion |

|

Forecast Market Size (2034) |

USD 10.19 Billion |

|

CAGR (2026-2034) |

12.86% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Guangdong (21.8% share, 2025) |

|

Second Largest Region |

Shanghai (16.4% share, 2025) |

|

Leading Gender |

Women (82.6%, 2025) |

|

Leading Type |

Non-Invasive (64.8%, 2025) |

The China cosmetic surgery market growth trajectory from 2020 through 2034, with historical expansion to USD 2.91 Billion in 2025, reflects sustained aesthetic consumption demand, while the forecast to USD 10.19 Billion captures accelerating non-invasive procedure adoption, medical tourism inflows, and premium clinic expansion.

To get more information on this market, Request Sample

CAGR trajectories across key gender, type, and regional sub-segments, with Guangdong at ~14.2% CAGR and non-invasive procedures at ~13.9% CAGR, are the fastest-growing categories within the China cosmetic surgery industry analysis through 2034.

Executive Summary

The China cosmetic surgery market is on a sustained growth trajectory from USD 2.91 Billion in 2025 to USD 10.19 Billion by 2034. Cosmetic surgery, encompassing invasive reconstruction and a widening range of non-invasive aesthetic procedures, benefits from durable demand anchored in rising income and evolving beauty standards.

Women dominate the gender mix at 82.6% in 2025, reflecting embedded cultural emphasis on facial aesthetics and aggressive targeting by aesthetic clinics through female-oriented digital channels. Men account for 17.4% but are growing faster as male grooming taboos erode and workplace image becomes more important.

Non-invasive procedures lead at 64.8% in 2025, capturing consumer preference for low-downtime treatments such as botulinum toxin, dermal fillers, laser hair removal, and photorejuvenation. Invasive surgeries (35.2%) anchor demand for eye surgery, rhinoplasty, liposuction, and breast augmentation.

Guangdong dominates at 21.8% in 2025, followed by Shanghai (16.4%), Jiangsu (14.9%), Zhejiang (13.7%), Sichuan (11.6%), and Henan (9.8%). Coastal provinces benefit from higher incomes and stronger medical tourism inflows, while inland provinces are emerging rapidly as aesthetic consumption diffuses beyond tier-1 metros.

Key Market Insights

|

Insight |

Data |

|

Leading Gender |

Women - 82.6% share (2025) |

|

Leading Type |

Non-Invasive - 64.8% share (2025) |

|

Leading Region |

Guangdong - 21.8% revenue share (2025) |

|

Second Largest Region |

Shanghai - 16.4% revenue share (2025) |

|

Top Companies |

AbbVie Inc., Aesthetic Medical International Holdings Group Limited, Bloomage Biotech Co., Ltd, Galderma, Hugel, Inc., IMEIK Technology Development Co. Ltd. |

Key Analytical Observations Supporting the Above Data:

- Women, with 82.6% share in 2025, dominate because Chinese aesthetic consumption is driven overwhelmingly by female consumers in the 19-to-50 age bracket. Social commerce platforms such as Xiaohongshu and Douyin concentrate female beauty content, while clinic marketing and procedure design target female buyers.

- Non-invasive procedures, with 64.8% share in 2025, lead because they offer visible results with minimal recovery time, making them accessible to working professionals. Injectables and energy-based devices form the core volume drivers, supported by recurring treatment cycles that create strong clinic lifetime value.

- Guangdong's 21.8% dominance in 2025 reflects the Greater Bay Area's wealth concentration, Hong Kong-linked medical tourism flows, and a dense network of licensed aesthetic hospitals in Shenzhen, Guangzhou, and Dongguan. The province also hosts leading domestic device and injectable manufacturers.

- Shanghai, with 16.4% in 2025, benefits from China's highest per-capita income and concentrated premium clinic infrastructure. International aesthetic brands prioritize Shanghai for flagship launches, while cross-border consumers from Jiangsu and Zhejiang travel there for complex invasive procedures.

China Cosmetic Surgery Market Overview

Cosmetic surgery in China encompasses a broad continuum of aesthetic medical interventions, ranging from invasive procedures such as eye surgery, rhinoplasty, liposuction, fat transfer, breast surgery, and facial sculpting to non-invasive treatments including botulinum toxin, dermal fillers, laser hair removal, photorejuvenation, and microdermabrasion delivered across licensed hospitals and specialized clinics.

The national ecosystem integrates raw material and device suppliers, domestic and imported medical product manufacturers, NMPA regulatory and certification bodies, medical distributors, surgeon and physician training institutions, cosmetic surgery hospitals, boutique medical aesthetic centers, digital booking platforms, and end consumers spanning working-age women, men, and a rapidly growing medical tourism cohort.

Market Dynamics

To evaluate market opportunities, Request Sample

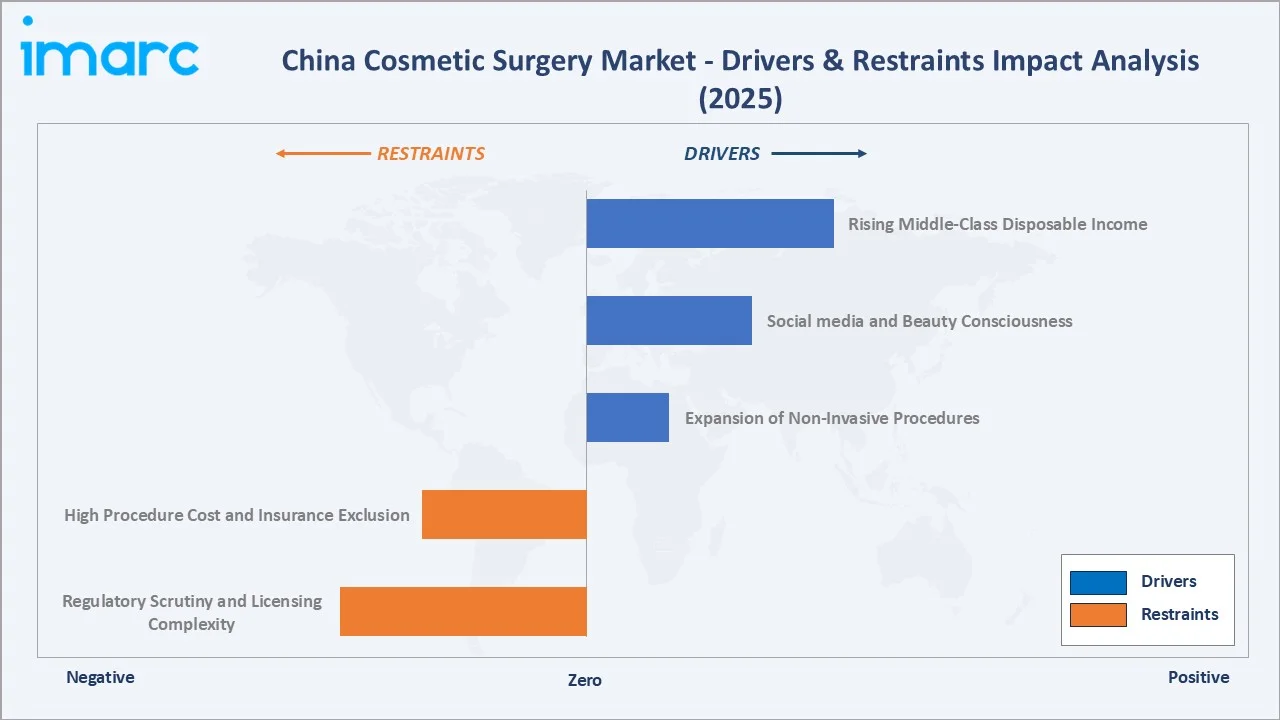

Market Drivers

- Rising Middle-Class Disposable Income: China's urban per-capita disposable income continues to expand, enabling discretionary spending on aesthetic procedures. In 2024, China’s national per capita disposable income reached RMB 41,314 (US$5,734), with real income growth recorded across all income groups. Growing female workforce participation is also translating into higher individual procedure budgets across injectables, laser treatments, and elective invasive surgeries.

- Social media and Beauty Consciousness: Platforms such as Xiaohongshu, Douyin, and Weibo have normalized aesthetic treatments, compressing the marketing funnel from awareness to booking. Influencer content and peer endorsement accelerate first-time conversion and repeat procedure frequency among female consumers aged 19-50.

- Expansion of Non-Invasive Procedures: Rapid adoption of botulinum toxin, hyaluronic acid fillers, photorejuvenation, and energy-based devices is broadening the addressable market by reducing cost, downtime, and procedural risk. Domestic approvals are improving accessibility for tier-2 and tier-3 consumers.

Market Restraints

- High Procedure Cost and Insurance Exclusion: Invasive procedures remain out-of-pocket expenses not covered by public health insurance, creating affordability barriers for middle-income households. Consumer financing options are progressively mitigating cost sensitivity among younger consumers.

- Regulatory Scrutiny and Licensing Complexity: Tightened NMPA oversight of aesthetic devices and injectables, combined with stricter NHC clinic licensing enforcement, is increasing compliance burden. Crackdowns on unlicensed practitioners periodically disrupt supply and slow new clinic openings.

Market Opportunities

- Domestic Injectable and Device Brands: Chinese manufacturers are rapidly gaining share in hyaluronic acid fillers, botulinum toxin, and energy-based devices, supported by lower price points and local clinical data. Continued NMPA approvals for domestic premium products will expand accessible pricing beyond tier-1 markets.

- Male Consumer Segment Expansion: The male cosmetic surgery segment is growing at above-market rates as grooming taboos erode, and workplace appearance concerns rise. Disposable Personal Income in China increased to 54188 CNY in 2024 from 51821 CNY in 2023. Targeted male-oriented clinic formats, hair restoration specialization, and jawline procedures present a high-growth white space.

Market Challenges

- Surgical Complications and Reputational Risk: Media coverage of botched procedures and unlicensed clinic incidents periodically dampens consumer confidence. Clinics must invest in credentialing, insurance, and quality systems to maintain trust, while regulators strengthen adverse-event reporting mechanisms.

- Shortage of Certified Aesthetic Surgeons: Demand for qualified plastic surgeons and trained injectors consistently outstrips supply, particularly in growth provinces. Extended training pipelines constrain clinic expansion, pushing operators toward nurse injector models and standardized non-invasive protocols.

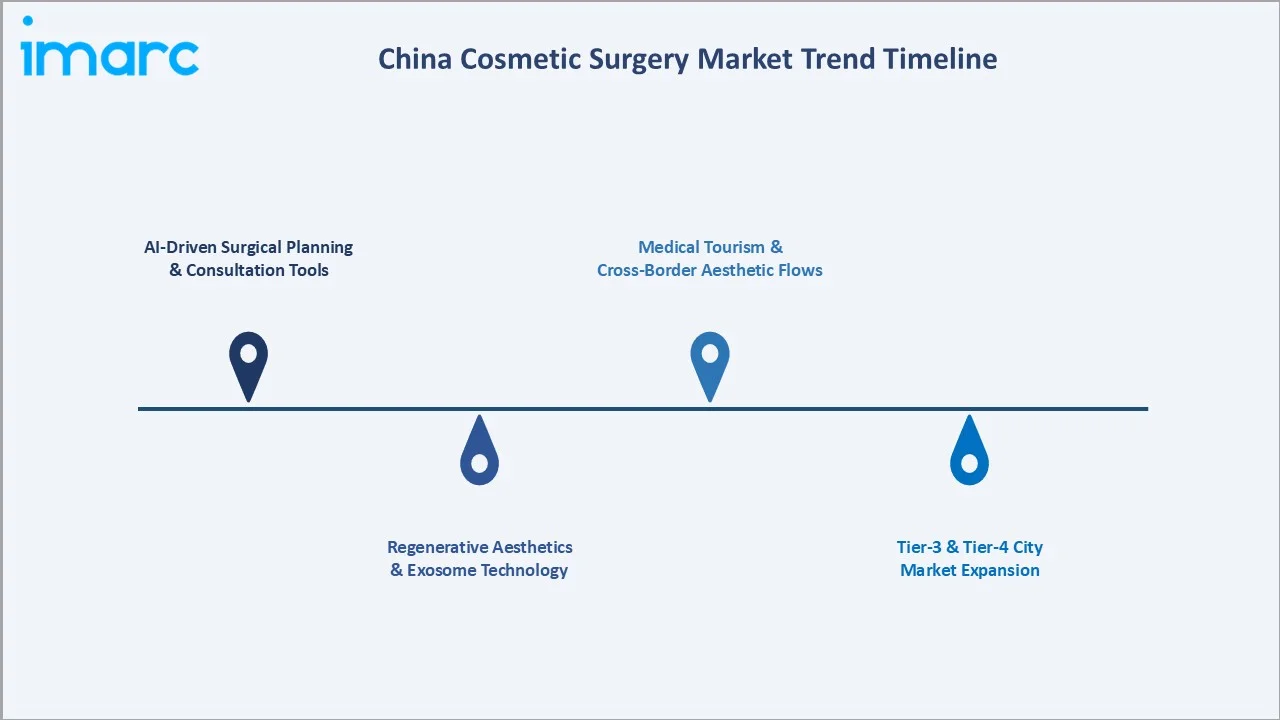

Emerging Market Trends

1. AI-Driven Surgical Planning and Consultation Tools

AI-powered facial analysis and simulation tools are transforming pre-procedure consultations, enabling clinics to visualize post-operative outcomes and align patient expectations. Integration with clinic management software improves consultation conversion and reduces dissatisfaction incidents, supporting data-driven personalization of treatment plans.

2. Regenerative Aesthetics and Exosome Technology

Regenerative aesthetic treatments including platelet-rich plasma, exosome therapy, and growth factor-based skin rejuvenation are gaining traction among premium clinics. These therapies position cosmetic surgery closer to medical regenerative care, commanding higher prices and attracting consumers seeking natural-looking, long-duration results.

3. Tier-3 and Tier-4 City Market Expansion

Aesthetic consumption is diffusing beyond tier-1 metros as clinic chains standardize operating models and roll out smaller-format boutique clinics in inland provinces. Livestream marketing and aesthetic e-commerce platforms reduce geographic friction, enabling consumers in inland cities to access branded procedures previously limited to coastal regions.

4. Medical Tourism and Cross-Border Aesthetic Flows

Shanghai and Guangdong are emerging as medical tourism destinations attracting consumers from Southeast Asia and Chinese diaspora markets. Domestic premium consumers travel to South Korea and Thailand for specialized invasive procedures, shaping two-way cross-border flows influencing clinic pricing, technique adoption, and brand positioning.

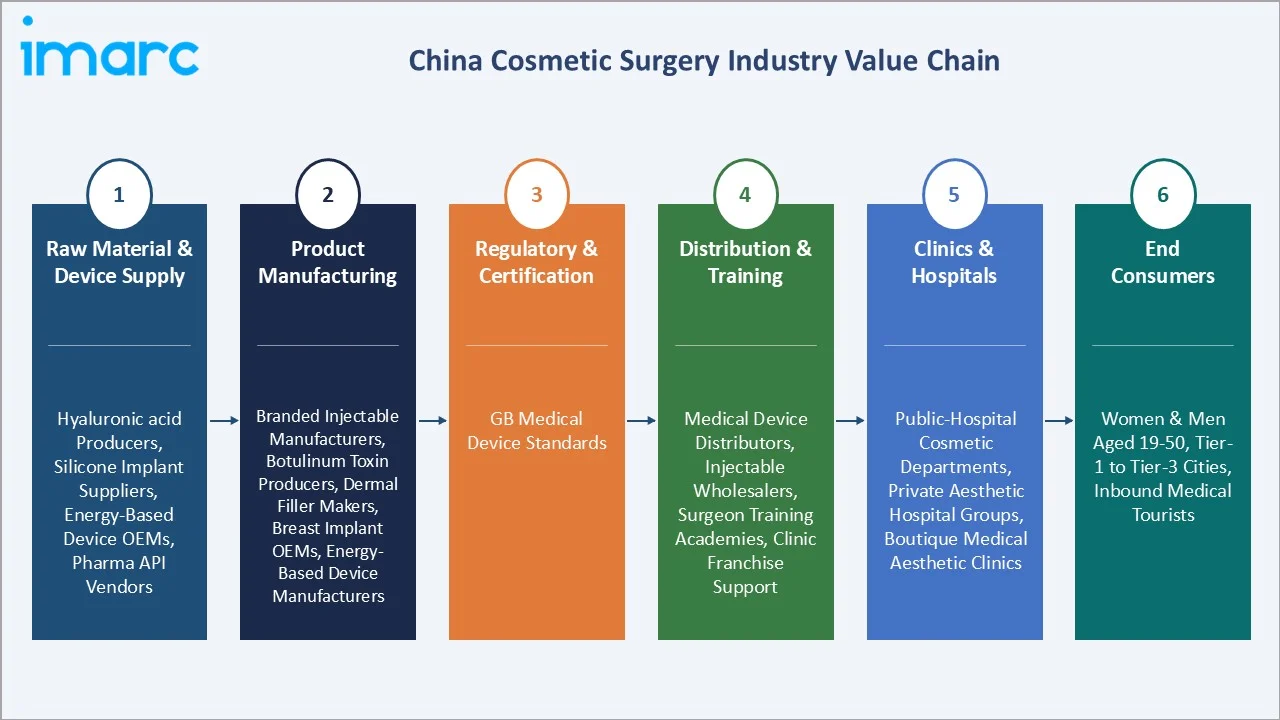

Industry Value Chain Analysis

The China cosmetic surgery value chain spans six stages from raw material and device supply through end-consumer treatment delivery. Product manufacturers and branded clinic operators capture the highest margins, while distribution and surgeon training generate significant working-capital requirements that favor well-capitalized multinational and domestic leaders.

|

Stage |

Key Players / Examples |

|

Raw Material & Device Supply |

Hyaluronic acid producers, silicone implant suppliers, energy-based device OEMs, pharmaceutical API vendors |

|

Product Manufacturing |

Branded injectable manufacturers, botulinum toxin producers, dermal filler makers, breast implant OEMs, energy-based device manufacturers |

|

Regulatory & Certification |

GB medical device standards |

|

Distribution & Training |

Medical device distributors, injectable wholesalers, surgeon training academies, clinic franchise support |

|

Clinics & Hospitals |

Public-hospital cosmetic surgery departments, private aesthetic hospital groups, boutique medical aesthetic clinics |

|

End Consumers |

Women, Men across age groups 19-50, tier-1 to tier-3 cities, inbound medical tourists |

Integrated players combining manufacturing, clinic ownership, and training, such as domestic leaders leveraging captive injectable portfolios with owned or franchised clinic networks, achieve lower unit economics than independent clinics dependent on third-party product procurement. This vertical integration is a meaningful competitive advantage in price-sensitive non-invasive segments.

Technology Landscape in the Cosmetic Surgery Industry

Injectable Technology: Hyaluronic Acid, Botulinum Toxin, and Biostimulators

Hyaluronic acid fillers and botulinum toxin dominate the injectable landscape, supported by domestic brands such as Imeik and Bloomage alongside imports from Allergan, Galderma, Medytox, and Hugel. Biostimulator injectables including poly-L-lactic acid are gaining specification in premium clinics for longer-duration volumizing results.

Energy-Based Devices: Laser, Ultrasound, and Radiofrequency Platforms

Laser hair removal, photorejuvenation, fractional laser, radiofrequency microneedling, and high-intensity focused ultrasound devices form the energy-based technology backbone of non-invasive clinics. Domestic OEMs are narrowing the quality gap with imports, improving accessibility for tier-2 and tier-3 city clinics.

Surgical Innovation: Endoscopic and Minimally Invasive Techniques

Endoscopic facelift, minimally invasive rhinoplasty, and body-contouring techniques such as laser-assisted liposuction are progressively replacing open surgical approaches. Reduced scarring and shorter recovery times are enabling invasive procedure growth among younger consumers who previously avoided surgery due to downtime.

Digital Tools: AI Simulation and Clinic Management Systems

Cosmetic surgery clinics are investing in AI-powered facial simulation software, digital consultation platforms, and integrated clinic management systems to improve consultation conversion and patient retention. Integration with aesthetic e-commerce and livestream channels is standardizing digital-first patient acquisition across branded chains.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Gender | Women | 82.6% | 2025 |

| Type | Non-Invasive | 64.8% | 2025 |

| Age Group | 🔒 | 🔒 | 2025 |

| Region | Guangdong | 21.8% | 2025 |

By Gender

Women command 82.6% majority share in 2025, anchored by deeply embedded cultural emphasis on facial aesthetics, peer-driven beauty norms, and targeted clinic marketing through female-centric digital platforms. The female segment dominates across both invasive and non-invasive procedures, concentrated in the 19-to-50 age bracket.

To access detailed market analysis, Request Sample

Men account for 17.4% in 2025 and represent the faster-growing gender segment. Eroding male grooming taboos, rising workplace image expectations, and targeted clinic formats focused on hair restoration, jawline enhancement, and skincare are driving penetration among urban male consumers aged 25-45.

By Type

Non-invasive procedures dominate at 64.8% in 2025, representing the highest-volume, lowest-downtime category serving working-age consumers. Core procedures include botulinum toxin, dermal fillers, laser hair removal, photorejuvenation, and microdermabrasion, supported by recurring treatment cycles that drive strong customer lifetime value.

Invasive procedures, with 35.2% in 2025, remain anchored in eye surgery, rhinoplasty, fat transfer, liposuction, breast surgery, and facial sculpting. Although lower in volume, invasive procedures command substantially higher per-procedure revenue, making them disproportionately important to clinic profit pools.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Guangdong |

21.8% |

Greater Bay Area wealth concentration; Hong Kong-linked medical tourism; dense clinic networks in Shenzhen and Guangzhou |

|

Shanghai |

16.4% |

Highest per-capita income; premium international clinic brands; inbound consumers from Jiangsu and Zhejiang |

|

Jiangsu |

14.9% |

Yangtze River Delta manufacturing wealth; strong female workforce participation; expanding mid-tier clinic chains |

|

Zhejiang |

13.7% |

E-commerce wealth effect in Hangzhou; Xiaohongshu-driven aesthetic consumption; rising non-invasive procedure adoption |

|

Sichuan |

11.6% |

Chengdu lifestyle hub; domestic injectable brand penetration |

|

Henan |

9.8% |

Inland consumption upgrade; expanding middle-class base; boutique clinic format rollout |

|

Others |

11.8% |

Hubei, Fujian, Shandong; rising tier-3 city clinic expansion; livestream-driven consumer acquisition |

Guangdong's 21.8% market dominance in 2025 is driven by the Greater Bay Area's wealth concentration, dense clinic infrastructure across Shenzhen, Guangzhou, and Dongguan, and significant inbound medical tourism linked to Hong Kong and Macau. The province also hosts leading domestic injectable and device manufacturers.

Shanghai, with 16.4% in 2025, anchors the premium segment through its highest per-capita income, concentration of international aesthetic brands, and status as a preferred destination for complex invasive procedures. Inbound consumers from surrounding Yangtze River Delta provinces strengthen clinic utilization.

Jiangsu and Zhejiang (14.9% and 13.7%) benefit from Yangtze River Delta manufacturing wealth and e-commerce-driven spending, while inland Sichuan and Henan (11.6% and 9.8%) represent emerging aesthetic consumption upgrades as branded clinic chains diffuse beyond coastal metros into inland provincial capitals.

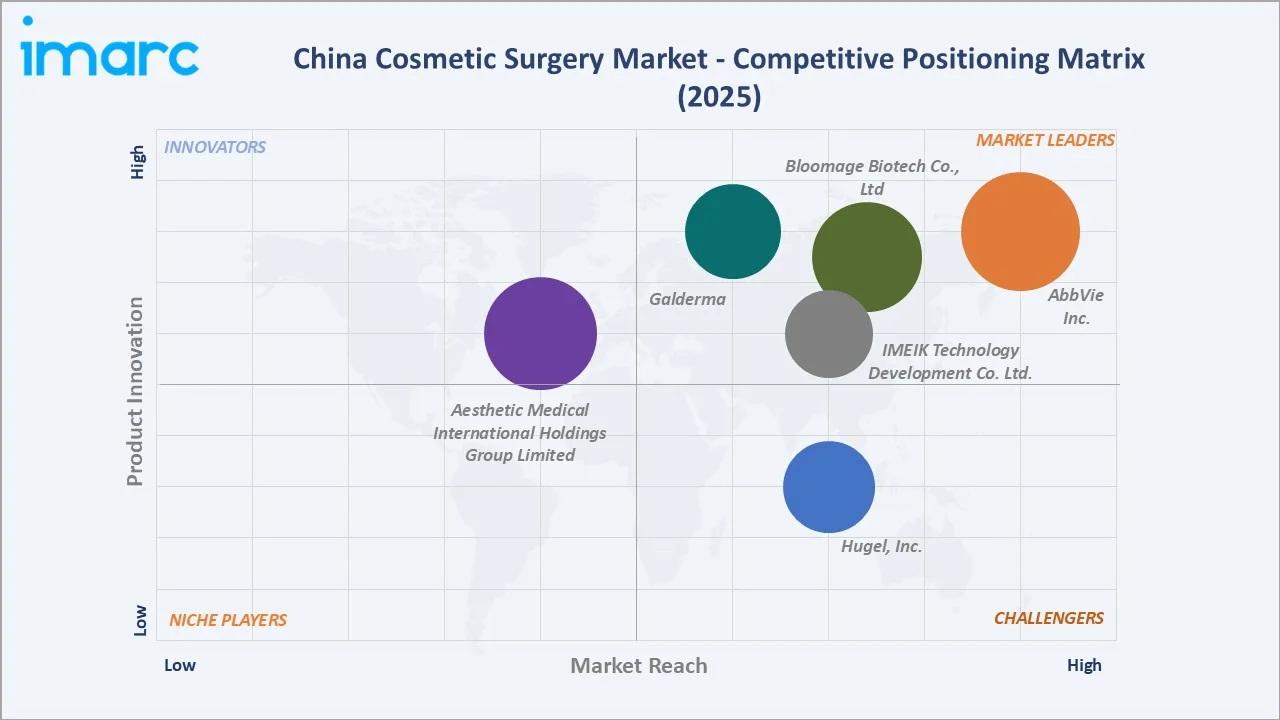

Competitive Landscape

The China cosmetic surgery market is moderately fragmented, with multinational injectable and implant leaders, domestic device and filler manufacturers, large private aesthetic hospital groups, and boutique clinic chains competing across premium and mid-market tiers. Digital platforms such as So-Young influence consumer acquisition and pricing transparency nationally.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

AbbVie Inc. |

Botulinum toxin, hyaluronic acid fillers |

Leader |

Global premium injectable leader; dominant share in imported toxin and filler |

|

Aesthetic Medical International Holdings Group Limited |

Multi-specialty aesthetic clinic network |

Established |

15-city private aesthetic hospital group in mainland China; one-stop surgical + non-surgical services |

|

Bloomage Biotech Co., Ltd |

Hyaluronic acid fillers, skincare actives |

Leader |

Domestic HA leader; upstream raw material integration; export-oriented |

|

Galderma |

Restylane fillers, Dysport toxin, skincare |

Leader |

Premium injectable portfolio; surgeon training; clinical evidence leadership |

|

Hugel, Inc. |

Letybo (letibotulinumtoxinA) |

Challenger |

Korean premium brand; expanding NMPA approvals; tier-1 city penetration |

|

IMEIK Technology Development Co. Ltd. |

Hyaluronic acid fillers, collagen stimulators |

Leader |

Domestic premium filler leader; strong clinical pipeline; expanding injectables |

Key players include AbbVie Inc., Aesthetic Medical International Holdings Group Limited, Bloomage Biotech Co., Ltd, Galderma, Hugel, Inc., IMEIK Technology Development Co. Ltd., and others.

Key Company Profiles

AbbVie Inc.

AbbVie's Allergan Aesthetics division is the global leader in aesthetic injectables and breast implants, with long-established presence in China through premium botulinum toxin and hyaluronic acid filler portfolios distributed to leading clinics.

- Product Portfolio: Offers botulinum toxin products, hyaluronic acid dermal fillers, and others.

- Recent Developments: In September 2024, Allergan Aesthetics, part of AbbVie, has introduced BOTOX Cosmetic (onabotulinumtoxinA) in China for treating masseter muscle prominence (MMP) in adults. This marks the first time a neurotoxin has been approved in the country specifically for this condition, which causes a wider, more square-shaped lower face.

- Strategic Focus: Allergan Aesthetics leverages its premium global brand equity to maintain price leadership in imported injectables while investing in surgeon education and clinical evidence to defend share against domestic challengers.

Imeik Technology Development Co., Ltd.

Imeik Technology is the leading domestic Chinese hyaluronic acid filler manufacturer, anchored by strong NMPA-approved portfolios, premium clinical positioning, and rapid expansion across branded clinics in tier-1 and tier-2 cities.

- Product Portfolio: The company offers premium hyaluronic acid fillers, collagen-stimulating injectables, and next-generation aesthetic biomaterials tailored to the China market.

- Recent Developments: In January 2026, Imeik Technology Development announced that it has secured exclusive distribution rights in China for an injectable botulinum toxin type A product. The product has received official drug registration approval from the national regulatory authority, allowing it to be marketed across mainland China.

- Strategic Focus: Imeik focuses on premium domestic positioning through clinical differentiation, local regulatory agility, and strong clinic relationships, competing directly with imported premium brands at comparable price points.

Bloomage Biotech Co., Ltd

Bloomage Biotechnology is a vertically integrated Chinese hyaluronic acid leader, operating upstream in HA raw material production through downstream finished filler products, medical skincare, and consumer aesthetic lines serving domestic and export markets.

- Product Portfolio: The company offers hyaluronic acid raw materials, finished dermal fillers, medical-grade skincare, and consumer beauty products.

- Recent Developments: In April 2026, Bloomage announced a new development focused on advancing its capabilities in bioactive materials and innovation. The update highlights the company’s continued investment in research, product development, and large-scale application of its technologies, particularly in areas related to hyaluronic acid and other functional bioactive ingredients.

- Strategic Focus: Bloomage leverages upstream HA integration to achieve cost leadership, supporting competitive pricing in finished fillers while expanding medical skincare and consumer brand extensions.

Market Concentration Analysis

The China cosmetic surgery market is moderately fragmented at the national level, reflecting meaningful concentration among multinational injectable and implant leaders in the premium imported segment, while fragmented clinic ownership persists across private hospital chains, boutique clinics, and public-hospital cosmetic surgery departments.

Concentration in the injectable and device product layer is higher than at the clinic layer: AbbVie (Allergan), Galderma, Medytox, and Hugel collectively command a disproportionate share of premium toxin and filler, while domestic leaders Imeik and Bloomage dominate the premium domestic segment. Clinic consolidation through chain expansion is accelerating.

Investment & Growth Opportunities

Fastest-Growing Segments

Non-invasive procedures at ~13.9% CAGR through 2034 represent the highest-growth type segment, driven by injectable expansion, energy-based device adoption, and male consumer penetration. Guangdong province at ~14.2% CAGR represents the fastest-growing region, supported by Greater Bay Area wealth, medical tourism, and clinic network expansion.

Emerging Markets

Inland tier-2 and tier-3 cities, particularly in Henan, Sichuan, and central China, represent the fastest-emerging sub-regional aesthetic consumption frontier through 2034. Standardized clinic franchise models, livestream-driven consumer acquisition, and domestic injectable brand penetration are enabling aesthetic consumption to diffuse from coastal metros into inland provincial capitals and prefecture cities.

Venture & Investment Trends

Private equity and strategic investor interest in consolidating fragmented aesthetic clinic chains is accelerating, with recurring non-invasive treatment revenue and defensible local brand positions making specialist operators attractive platform investments. Digital aesthetic platforms, domestic injectable manufacturers, and AI consultation technology are attracting growth capital.

Future Market Outlook (2026-2034)

The China cosmetic surgery market is forecast to expand from USD 2.91 Billion in 2025 to USD 10.19 Billion by 2034 at a CAGR of 12.86%, adding USD 7.28 Billion in incremental annual market value over the forecast period. This sustained growth reflects structural demographic and consumption drivers supporting durable aesthetic demand.

Three forces will most significantly shape the industry through 2034. First, continued domestic injectable and device substitution will reshape pricing and accessibility beyond tier-1 cities. Second, AI and digital consultation tools will standardize service delivery. Third, male consumer expansion and tier-3 diffusion will broaden the addressable base.

Research Methodology

Primary Research

Primary research encompassed structured interviews in 2024-2025 with China cosmetic surgery stakeholders including aesthetic hospital chain executives, boutique clinic operators, injectable and device manufacturer commercial leads, plastic surgeons, and digital aesthetic platform operators. Primary data validated market sizing, segment shares, and regional estimates.

Secondary Research

Key secondary sources include NMPA device and injectable approval databases, National Bureau of Statistics consumer expenditure data, National Health Commission clinic licensing registries, industry association reports, publicly disclosed financials of listed aesthetic companies, and trade publications covering the China aesthetic industry.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models, incorporating disposable income growth, demographic trends, procedure penetration rates, and historical market patterns. Scenario analysis covering base, optimistic, and conservative cases was performed to account for regulatory and macroeconomic uncertainty.

China Cosmetic Surgery Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Genders | Women, Men |

| Types Covered |

|

| Age Groups Covered | 18 and Below, 19 to 34, 35 to 50, 51 to 64, 65 and Above |

| Region Covered | Guangdong, Jiangsu, Zhejiang, Henan, Sichuan, Shanghai, Others |

| Companies Covered | AbbVie Inc., Aesthetic Medical International Holdings Group Limited, Bloomage Biotech Co., Ltd, Galderma, Hugel, Inc., IMEIK Technology Development Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the China Cosmetic Surgery Market Report

The China cosmetic surgery market reached USD 2.91 Billion in 2025, reflecting strong demand from rising middle-class disposable income, accelerating non-invasive procedure adoption, and expanding licensed clinic infrastructure.

The market is projected to reach USD 10.19 Billion by 2034, growing at a CAGR of 12.86% during 2026-2034, driven by non-invasive procedure expansion, domestic injectable adoption, and tier-3 city diffusion.

Women lead with 82.6% gender share in 2025, anchored by female aesthetic consumption norms, targeted digital marketing on Xiaohongshu and Douyin, and concentrated demand among urban women aged 19-50.

Non-invasive procedures lead at 64.8% in 2025, representing the highest-volume, lowest-downtime category. Core drivers include botulinum toxin, hyaluronic acid fillers, laser hair removal, and photorejuvenation.

Guangdong commands a dominant 21.8% market share in 2025, driven by Greater Bay Area wealth, Hong Kong-linked medical tourism, and dense clinic networks across Shenzhen, Guangzhou, and Dongguan.

Non-invasive procedures are the fastest-growing type segment at approximately 13.9% CAGR through 2034, driven by injectable expansion, energy-based device adoption, and rising male consumer penetration.

Leading companies include AbbVie Inc., Aesthetic Medical International Holdings Group Limited, Bloomage Biotech Co., Ltd, Galderma, Hugel, Inc., IMEIK Technology Development Co. Ltd., and others

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)