China Cybersecurity Market Size, Share, Trends and Forecast by Component, Deployment Type, User Type, Industry Vertical, and Region, 2026-2034

China Cybersecurity Market Overview:

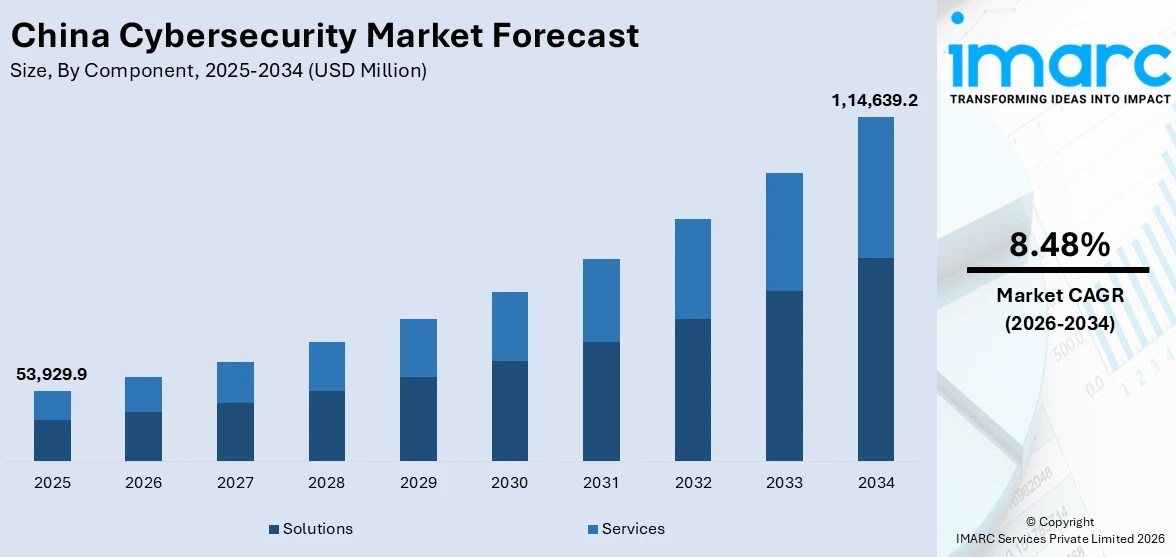

The China cybersecurity market size reached USD 53,929.9 Million in 2025. The market is projected to reach USD 1,14,639.2 Million by 2034, exhibiting a growth rate (CAGR) of 8.48% during 2026-2034. The market is growing steadily, led by increasing adoption of digital technologies in public and private sectors. Increased data protection awareness, regulatory progress, and investment in cyber defense are driving improved demand for security solutions. Cloud migration, working from home, and changing cyber threats are also compelling companies to update their cybersecurity infrastructure. As the country continues to prioritize digital sovereignty and technology resilience, these developments are expected to shape the future of the China cybersecurity market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 53,929.9 Million |

| Market Forecast in 2034 | USD 1,14,639.2 Million |

| Market Growth Rate 2026-2034 | 8.48% |

China Cybersecurity Market Trends:

Strengthened Legal Frameworks and Standards

China is reinforcing its cybersecurity legal landscape with amendments and national standards aimed at improving protection of data, critical infrastructure, and user rights. For instance, in March 2025, draft amendments to the Cybersecurity Law were issued, enhancing penalties, clarifying enforcement, and tightening oversight of network operators and critical infrastructure entities. The government has also released national standards addressing cybersecurity technologies, system software, network security technical controls, and smart device requirements. These improvements are intended to ensure consistent compliance across industries and to reduce regulatory ambiguities. Moreover, measures for protecting personal information, managing data transfers, and securing AI‑related services are becoming more robust. Educational institutions are supporting this shift by expanding cybersecurity curricula, helping to prepare the workforce for stricter requirements. Together, these legal and standardization efforts are promoting better governance, elevating cybersecurity readiness across both public and private sectors. These developments are foundational to China cybersecurity market growth, establishing a stronger baseline for trust, regulation, and technology adoption.

To get more information on this market Request Sample

Governance of AI and Identity in Digital Space

The regulation of artificial intelligence and digital identity is emerging as a core element of cybersecurity policy in China. Authorities have formalized frameworks for the governance of AI, emphasizing safe, transparent, and accountable deployment. In September 2024, a security governance framework for AI was released during China Cybersecurity Week, outlining principles of risk management, technical response, and prevention of misuse. The government is also moving forward with national identity verification measures such as online identity authentication to ensure accountability and traceability in digital interactions. These steps are intended to address emerging risks such as fraud, disinformation, and identity abuse in digital platforms. They also reflect the recognition that identity management and AI oversight must work together to secure online ecosystems. Through these regulatory moves, digital platforms and services are being held to higher standards of transparency and governance. These combined initiatives are key indicators of China cybersecurity market trends, shaped by policy responses to new technology challenges and the demand for trusted digital identity systems.

Emphasis on Talent Development and Institutional Capacity

China is investing significantly in building the human expertise and institutional capacity necessary for maintaining strong cybersecurity posture. A growing number of universities have launched undergraduate programs in cybersecurity, and over ninety higher learning institutions now host schools or departments dedicated to cybersecurity education. Professional training and certification programs are also being expanded to ensure practitioners can respond to evolving threats, including those tied to IoT, cloud systems, and AI. Government agencies are collaborating with standardization bodies to develop institutions capable of enforcing new regulations, auditing network safety, and overseeing incident reporting. Public awareness campaigns and enterprise compliance oversight are being enhanced to ensure that organizations understand their responsibilities under the updated legal frameworks. These investments aim to solidify long‑term institutional resilience and ensure that legal and technical protections are matched by skilled professionals and capable regulatory bodies.

China Cybersecurity Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on component, deployment type, user type, and industry vertical.

Component Insights:

- Solutions

- Identity and Access Management (IAM)

- Infrastructure Security

- Governance, Risk and Compliance

- Unified Vulnerability Management Service Offering

- Data Security and Privacy Service Offering

- Others

- Services

- Professional Services

- Managed Services

The report has provided a detailed breakup and analysis of the market based on the component. This includes solutions (identity and access management (IAM), infrastructure security, governance, risk and compliance, unified vulnerability management service offering, data security and privacy service offering, and others) and services (professional services and managed services).

Deployment Type Insights:

- Cloud-Based

- On-Premises

A detailed breakup and analysis of the market based on the deployment type has also been provided in the report. This includes cloud-based and on-premises.

User Type Insights:

- Large Enterprises

- Small and Medium Enterprises

The report has provided a detailed breakup and analysis of the market based on the user type. This includes large enterprises, and small and medium enterprises.

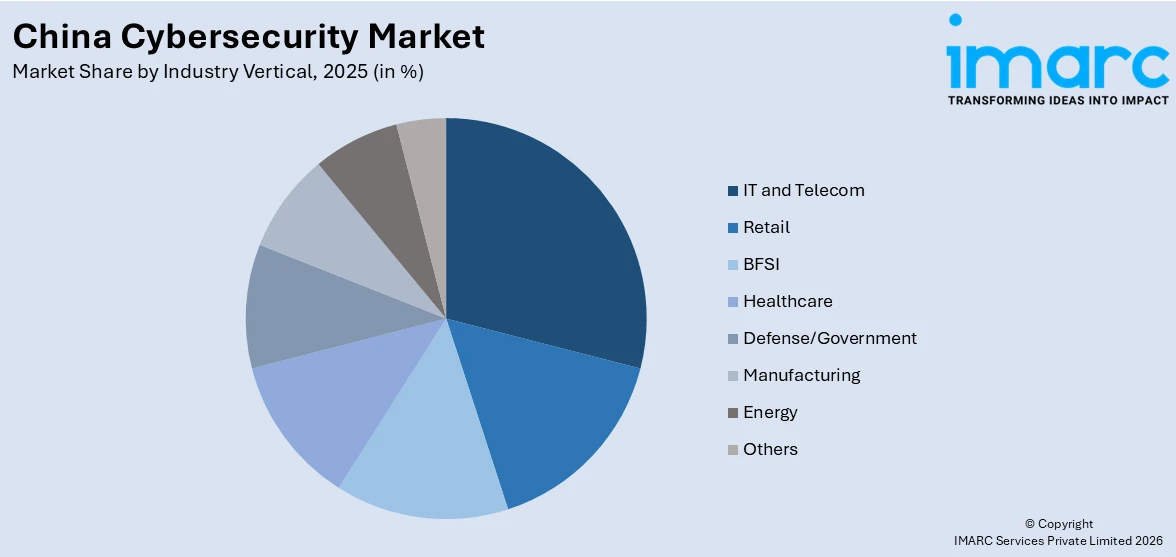

Industry Vertical Insights:

Access the comprehensive market breakdown Request Sample

- IT and Telecom

- Retail

- BFSI

- Healthcare

- Defense/Government

- Manufacturing

- Energy

- Others

A detailed breakup and analysis of the market based on the industry vertical has also been provided in the report. This includes IT and telecom, retail, BFSI, healthcare, defense/government, manufacturing, energy, and others.

Regional Insights:

- North China

- East China

- South Central China

- Southwest China

- Northwest China

- Northeast China

The report has also provided a comprehensive analysis of all the major regional markets, which include North China, East China, South Central China, Southwest China, Northwest China, and Northeast China.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

China Cybersecurity Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Deployment Types Covered | Cloud-Based, On-Premises |

| User Types Covered | Large Enterprises, Small and Medium Enterprises |

| Industry Verticals Covered | IT and Telecom, Retail, BFSI, Healthcare, Defense/Government, Manufacturing, Energy, Others |

| Regions Covered | North China, East China, South Central China, Southwest China, Northwest China, Northeast China |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the China cybersecurity market performed so far and how will it perform in the coming years?

- What is the breakup of the China cybersecurity market on the basis of component?

- What is the breakup of the China cybersecurity market on the basis of deployment type?

- What is the breakup of the China cybersecurity market on the basis of user type?

- What is the breakup of the China cybersecurity market on the basis of industry vertical?

- What is the breakup of the China cybersecurity market on the basis of region?

- What are the various stages in the value chain of the China cybersecurity market?

- What are the key driving factors and challenges in the China cybersecurity market?

- What is the structure of the China cybersecurity market and who are the key players?

- What is the degree of competition in the China cybersecurity market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the China cybersecurity market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the China cybersecurity market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the China cybersecurity industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)