China Diabetes Market Size, Share, Trends and Forecast by Segment and Distribution Channel, 2026-2034

China Diabetes Market Size, Share, Trends & Forecast (2026-2034)

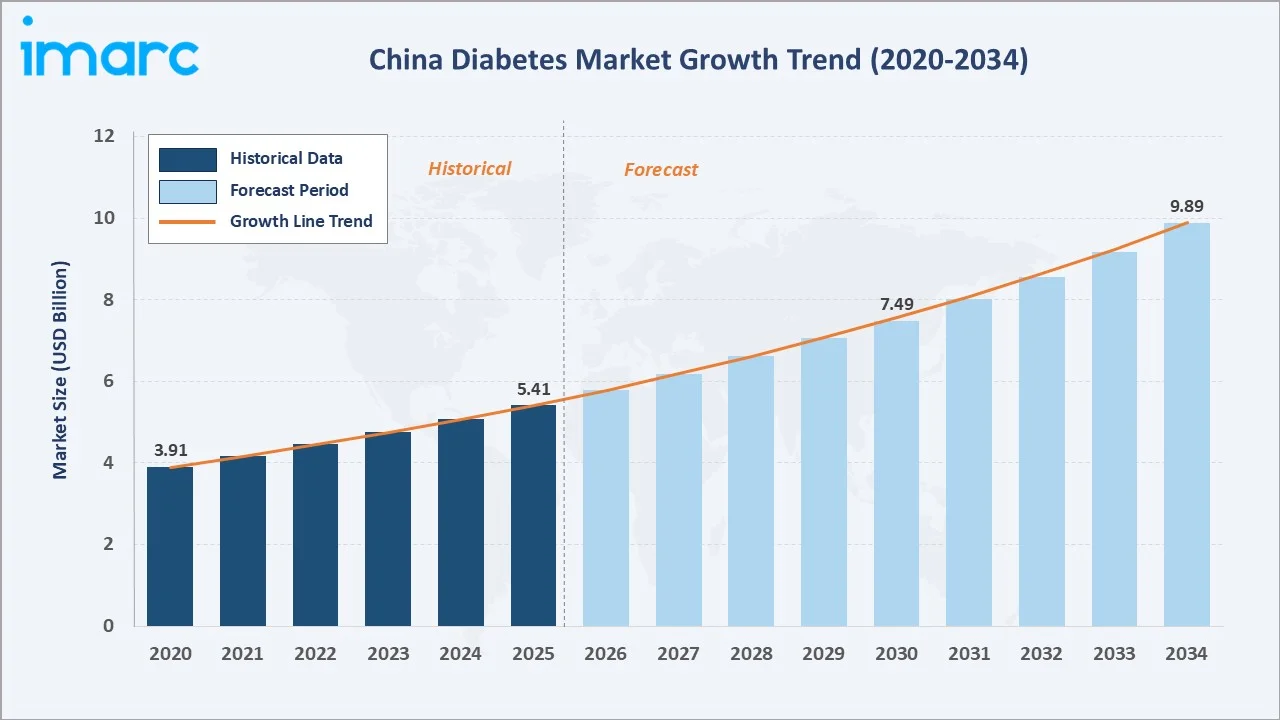

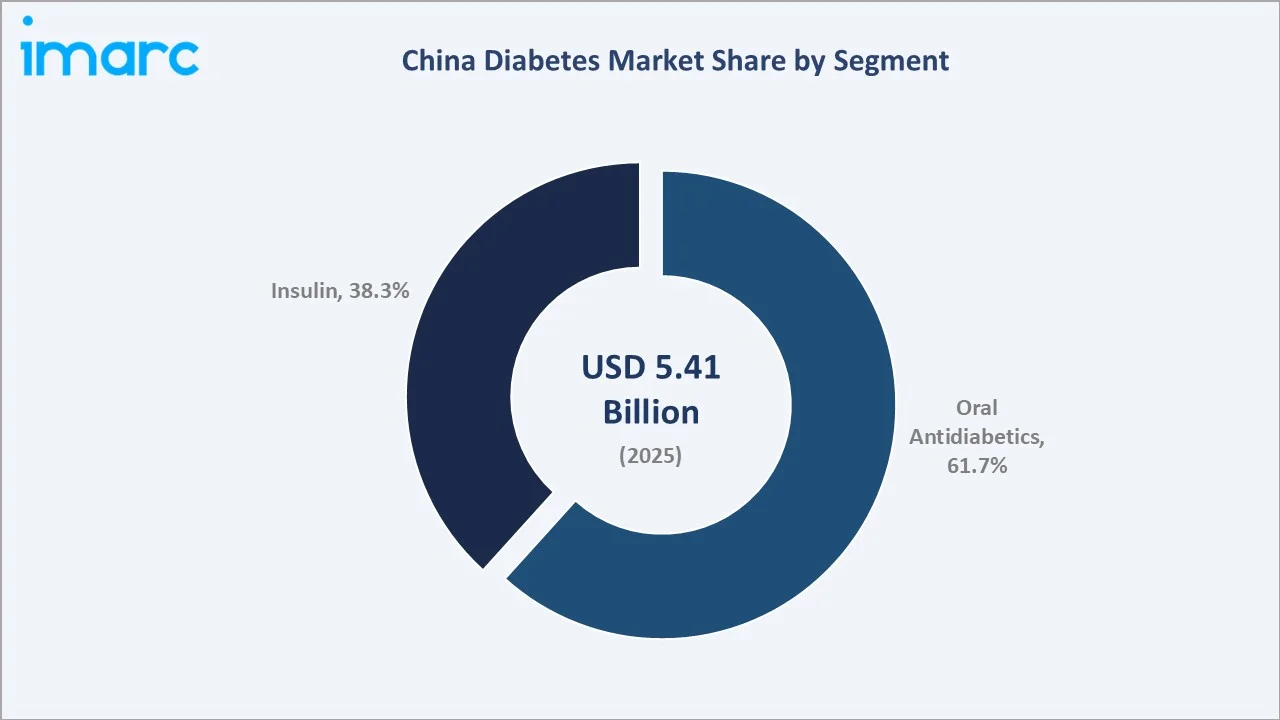

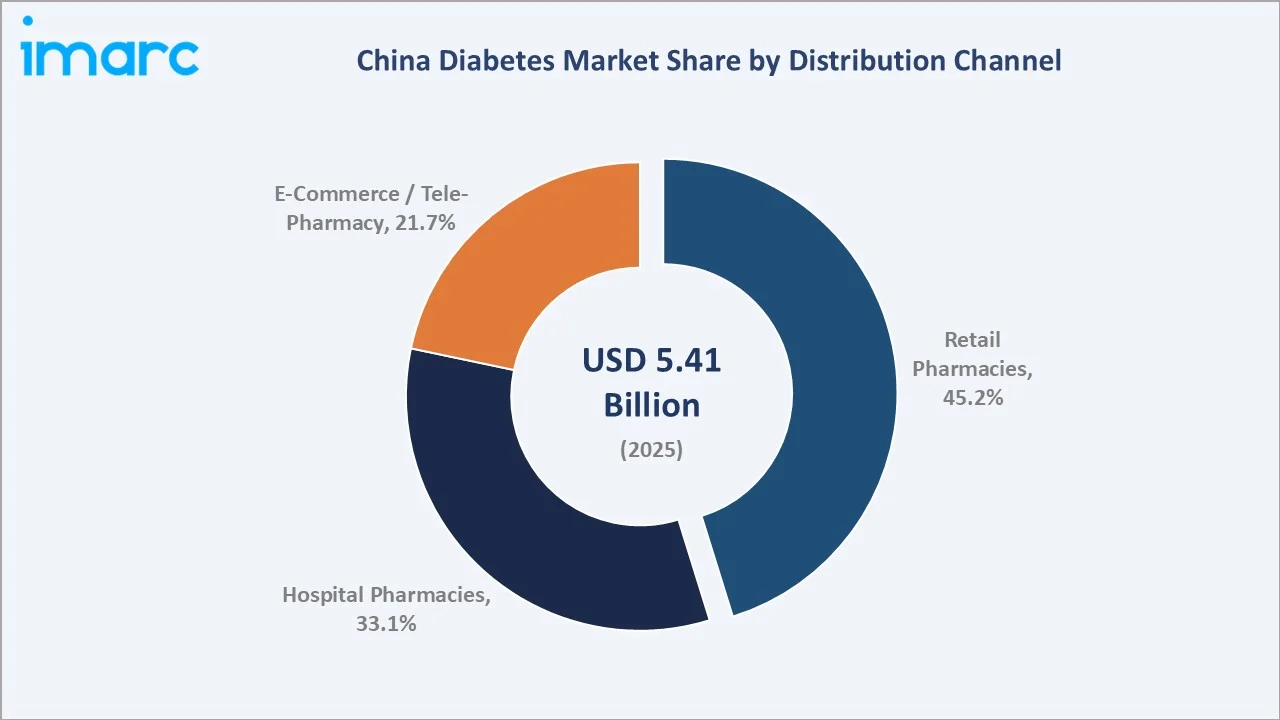

The China diabetes market reached USD 5.41 Billion in 2025 and is projected to reach USD 9.89 Billion by 2034, growing at a CAGR of 6.73% during 2026 to 2034. China hosts the world's largest diabetic population, with over 140 million adults living with the condition in 2025. Rapid urbanization, dietary shifts toward processed foods, and an ageing population are the structural drivers of this market, creating immense and sustained demand for both oral antidiabetics and insulin therapies across the country's expanding healthcare system.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.41 Billion |

|

Forecast Market Size (2034) |

USD 9.89 Billion |

|

CAGR (2026-2034) |

6.73% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Segment |

Oral Antidiabetics – 61.7% share (2025) |

|

Leading Distribution Channel |

Retail Pharmacies – 45.2% share (2025) |

The China diabetes market demonstrated a robust historical CAGR of 6.73% during 2020–2025, propelled by multiple concurrent forces: the rapid expansion of National Reimbursement Drug List (NRDL) coverage to include newer therapeutic classes including DPP-4 inhibitors and SGLT-2 inhibitors; the Chinese government's Healthy China 2030 initiative accelerating NCD treatment infrastructure investment; and the explosive growth of digital health platforms including JD Health and Alibaba Health enabling unprecedented pharmacy access across Tier-3 to Tier-6 cities.

To get more information on this market, Request Sample

Looking ahead, the forecast period 2026–2034, three structural forces will anchor the trajectory: the volume-based procurement (VBP) policy compressing insulin average selling prices while dramatically expanding patient volumes via public hospital channels; the emergence of domestic Chinese GLP-1 and novel OAD pipeline candidates from companies; and the Healthy China 2030 initiative's targeted commitment to reduce diabetes complication rates by 30%.

Executive Summary

The China diabetes market is on a high-growth trajectory driven by the world's largest and fastest-growing diabetic patient population, expanding NHSA reimbursement coverage, and the rapid maturation of China's domestic pharmaceutical innovation ecosystem. The market reached USD 5.41 Billion in 2025 and is forecast to reach USD 9.89 Billion by 2034, reflecting a robust CAGR of 6.73% over the forecast period.

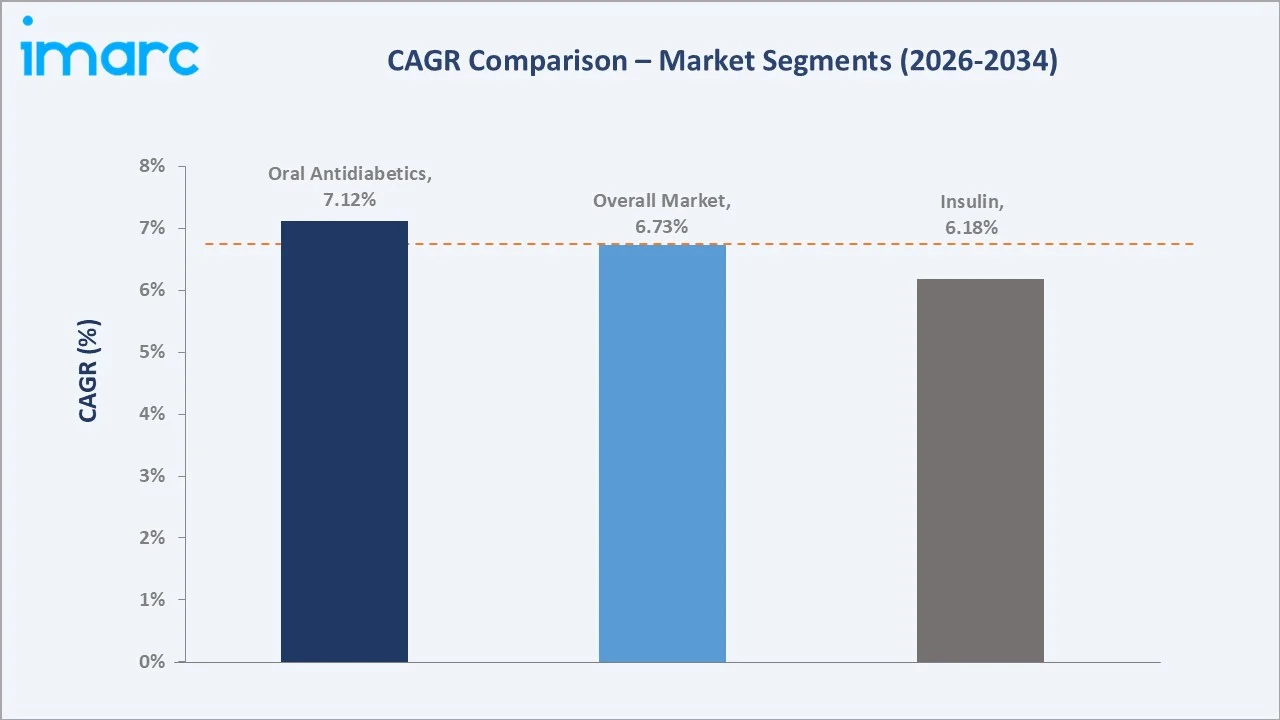

Oral antidiabetics command the largest segment share at 61.7% in 2025, anchored by metformin as universal first-line therapy and the growing penetration of NRDL-listed DPP-4 inhibitors, SGLT-2 inhibitors, and nascent GLP-1 receptor agonist prescriptions in Tier-1 city hospitals. The insulin segment accounts for 38.3%, driven by a large Type-1 patient base and the progressive transition of advanced Type-2 patients to basal insulin therapy.

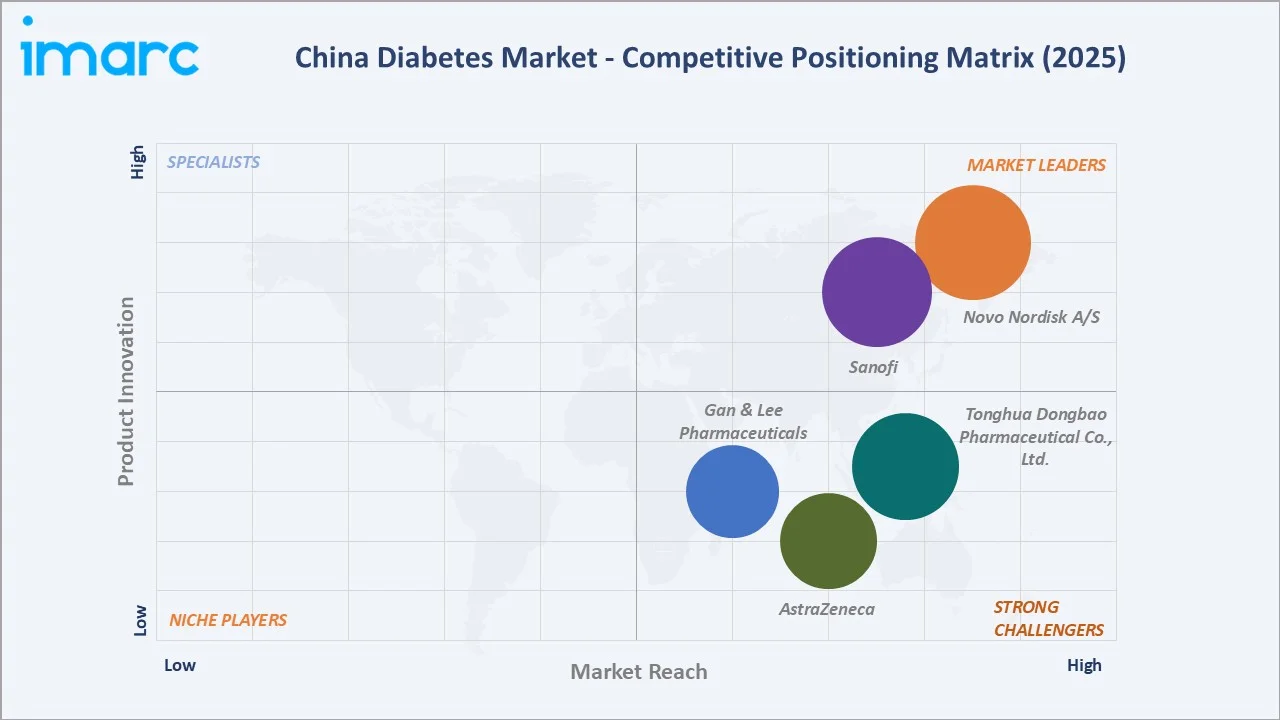

East China leads regionally with approximately 35% of the national market revenue in 2025, concentrated in Shanghai, Jiangsu, and Zhejiang. Key players include global MNCs Novo Nordisk A/S, Sanofi, and AstraZeneca, alongside rapidly growing domestic leaders Tonghua Dongbao Pharmaceutical Co., Ltd. and Gan & Lee Pharmaceuticals, which collectively hold over 40% of China's insulin market by volume.

Key Market Insights

|

Insight |

Data |

|

Largest Segment |

Oral Antidiabetics – 61.7% share (2025) |

|

2nd Largest Segment |

Insulin – 38.3% share (2025) |

|

Leading Channel |

Retail Pharmacies – 45.2% share (2025) |

|

Fastest Growing Channel |

E-Commerce/Tele-Pharmacy – 21.7% share (2025) |

|

Top Companies |

Novo Nordisk A/S, Sanofi, Tonghua Dongbao Pharmaceutical Co., Ltd., Gan & Lee Pharmaceuticals, and AstraZeneca |

|

Market Opportunity |

Domestic GLP-1 & novel OAD segment projected at USD 2.1 Billion by 2034 |

Key Analytical Observations Supporting the Above Data:

- Oral antidiabetics account for 61.7% of the China diabetes market in 2025, the highest segment share among major diabetes markets globally, reflecting China's large treatment-naive Type-2 population entering therapy via government-funded community health programs.

- Insulin holds a 38.3% share in 2025; growth dynamics are shaped by VBP price compression on human insulin and first-generation analogues, offset by volume expansion through public hospital channels and the growing biosimilar glargine segment, where domestic players Gan & Lee and Tonghua Dongbao hold dominant positions.

- Retail pharmacies represent the leading channel at 45.2% in 2025, driven by DTP (Direct-to-Patient) pharmacy chains and over 600,000 licensed retail outlets nationally offering NHSA-insured OAD prescriptions under China's medical insurance electronic prescription system.

- E-commerce and tele-pharmacy channels have reached 21.7% share in 2025, reflecting China's world-leading e-health adoption. JD Health and Alibaba Health each process tens of millions of chronic disease prescriptions annually, with diabetes medications among the top-three categories by volume.

- The domestic GLP-1 and novel OAD innovation pipeline represents the single largest market expansion opportunity, estimated at USD 2.1 Billion by 2034 as domestic Chinese pharmaceutical companies achieve NMPA approval for semaglutide biosimilars and novel dual-receptor agonist candidates between 2026 and 2030.

China Diabetes Market Overview

Diabetes mellitus represents China's most significant chronic disease burden by patient numbers. With an estimated 233 million adults living with diagnosed diabetes in 2023, China accounts for approximately 22-25% of the global diabetic population. Type-2 diabetes comprises over 95% of cases, driven by urbanization-associated dietary shifts, physical inactivity, and the high prevalence of metabolic syndrome across China's middle-income urban cohort.

China's pharmaceutical market operates under the National Medical Products Administration (NMPA), which governs drug approvals via the Center for Drug Evaluation (CDE), while the National Healthcare Security Administration (NHSA) determines reimbursement status through the NRDL and controls drug pricing through volume-based procurement (VBP) rounds.

Market Dynamics

To evaluate market opportunities, Request Sample

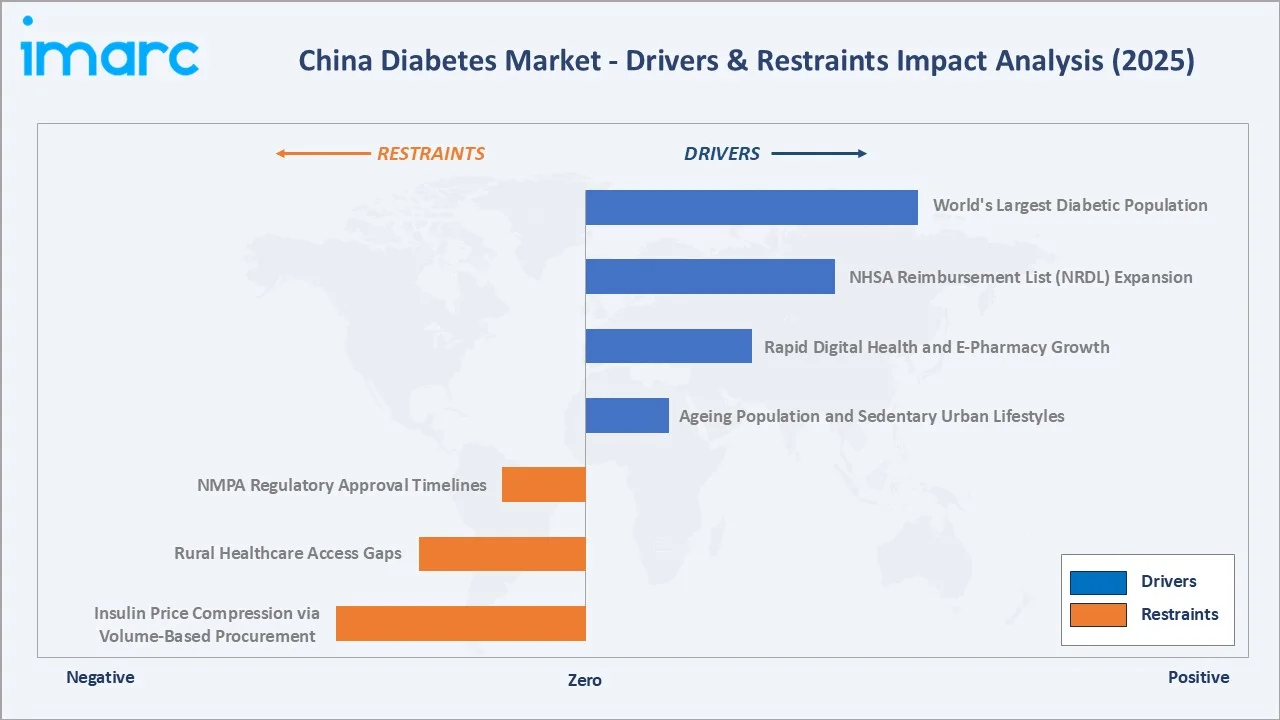

Market Drivers

- World's Largest Diabetic Population: China has the largest diabetes population globally, representing more than one-quarter of all diabetes cases worldwide, with approximately 140 million patients aged 20–79 years. With an additional estimated 40 million in the pre-diabetes high-risk category, the underlying incidence pipeline ensures structural demand growth for diabetes medications across all therapeutic classes through the forecast period.

- NHSA Reimbursement List (NRDL) Expansion: The NHSA's NRDL has progressively expanded reimbursement coverage to include DPP-4 inhibitors, SGLT-2 inhibitors, and selected GLP-1 agents in annual updates from 2020–2025. NRDL listing is critical for market access in China's public hospital system and creates immediate volume uplift for newly listed products.

- Rapid Digital Health & E-Pharmacy Expansion: JD Health serving more than 183 million annual active users as of December 31, 2024, with chronic disease medications, comprising over 35% of prescription volumes.

- Ageing Population & Sedentary Urban Lifestyles: China's population aged 60+ will exceed 400 million by 2035, representing the highest-risk cohort for Type-2 diabetes onset and complications. Simultaneously, the urbanization rate is expected to reach 70% by 2030, bringing dietary and lifestyle risk factors to an additional 100+ million previously rural residents.

Market Restraints

- Insulin Price Compression via Volume-Based Procurement: The average price reduction under the VBP price cap for insulin product groups reached 48.75%. While expanding patient access volumes, this has compressed per-unit revenue for both MNC and domestic insulin manufacturers, creating a structural headwind for insulin segment revenue growth despite strong volume expansion.

- Rural Healthcare Access Gaps: China's vast geography creates stark disparities in diabetes healthcare access between Tier-1 cities and rural counties. Undiagnosed cases account for nearly two-thirds of diabetes among adults in China, representing both a healthcare challenge and an unrealized commercial opportunity that requires significant investment in community health infrastructure.

- NMPA Regulatory Approval Timelines: The NMPA's review timeline for innovative new molecular entities averages 18–24 months from acceptance to approval, with NRDL negotiation adding a further 12–18 months. This creates extended time-to-commercial-peak for novel therapies, particularly impacting MNCs seeking to commercialize next-generation GLP-1 and dual-receptor agonist products relative to the US and EU timelines.

Market Opportunities

- Domestic GLP-1 & Novel OAD Pipeline: Multiple Chinese pharmaceutical companies, including Jiangsu Hengrui, are advancing novel OAD pipeline candidates. NMPA approvals for domestic GLP-1 products are projected between 2026 and 2028, creating a transformative market expansion event.

- Healthcare Reach Expansion to Major Cities: Under the Healthy China 2030 blueprint, the Diabetes Prevention and Treatment Initiative is one of 15 key national programs.

Initiatives such as Shanghai’s SIM and the ROADMAP program spanning 25 provinces across both urban and rural regions highlight that integrated hospital–community care and stronger primary–specialty collaboration significantly enhance diabetes management outcomes. - Digital Health & AI Diabetes Management Innovation: AI-powered CGM platforms, closed-loop insulin delivery systems, and digital diabetes coaching tools are attracting significant venture capital in China, with diabetes digital health receiving CNY 4.2 billion in disclosed VC investment between 2022 and 2025. These platforms are creating new prescription gateway opportunities for pharmaceutical companies.

Market Challenges

- Counterfeit Drug Circulation Risks: China's pharmaceutical distribution and enforcement ecosystem faces persistent challenges with substandard and falsified medications in lower-tier markets. NMPA estimates 2–3% of prescription medications in informal channels may be substandard, creating patient safety risks and undermining confidence in generic diabetes drug markets in Tier-4–6 cities.

- Import Substitution & Domestic Industry Preference: China's pharmaceutical market is subject to the government's preference for domestically manufactured products through procurement incentives, NRDL negotiation leverage, and explicit import substitution policies for therapeutic classes where domestic supply is deemed sufficient.

Emerging Market Trends

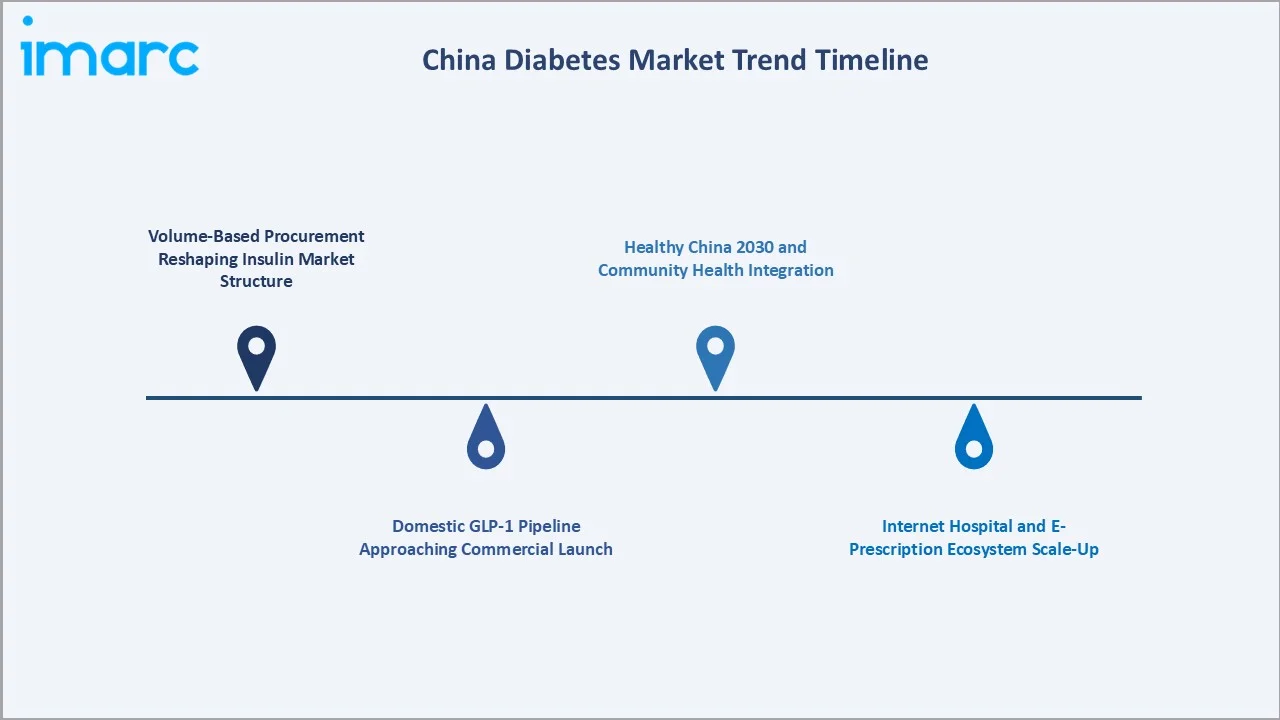

1. Volume-Based Procurement Reshaping Insulin Market Structure

VBP Round 6 (2022) and subsequent insulin-specific procurement tenders have fundamentally restructured China's insulin market. Domestic manufacturers Gan & Lee and Tonghua Dongbao emerged as the primary volume beneficiaries, capturing over 50% of public hospital insulin volumes by 2025. MNCs Novo Nordisk and Sanofi have responded by repositioning premium analogue products not included in VBP tenders, including Tresiba and Toujeo, in the private hospital and DTP pharmacy segments.

2. Domestic GLP-1 Pipeline Approaching Commercial Launch

In July 2025, Hengrui Pharma and Kailera Therapeutics reported positive topline results from the Phase 3 trial (HRS9531-301) of HRS9531, a once-weekly injectable dual GLP-1/GIP receptor agonist for adults with obesity or overweight.

3. Internet Hospital and E-Prescription Ecosystem Scale-Up

China's internet hospital network grew to over 3,000 licensed platforms in 2023 from fewer than 300 in 2019. NHSA-approved electronic prescription systems for chronic diseases now cover all 31 provinces, enabling diabetes patients to renew prescriptions and receive home delivery without hospital visits.

4. Healthy China 2030 and Community Health Integration

By 2030, China aims to build a diabetes prevention and treatment system where over 60% of adults aged 18 and above are aware of the disease. Additionally, standardized management service coverage for type 2 diabetes patients at the primary care level is expected to exceed 70%, according to the National Health Commission (NHC) and other authorities.

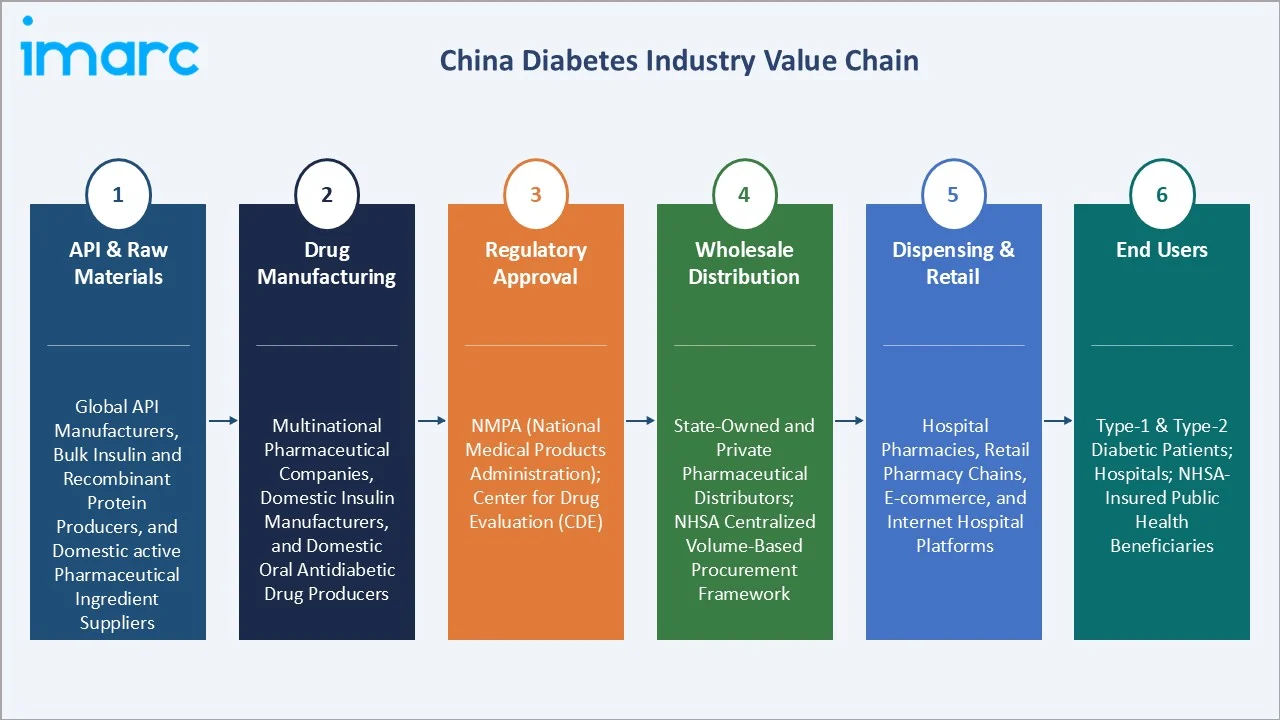

Industry Value Chain Analysis

The China diabetes drug market value chain is shaped by the NHSA procurement framework, NMPA regulatory requirements, and a dual public-private distribution structure spanning government-run hospital pharmacies, private retail pharmacy chains, and China's world-leading e-commerce pharmaceutical platforms.

|

Stage |

Key Players / Examples |

|

API & Raw Materials |

Global API manufacturers, bulk insulin and recombinant protein producers, and domestic active pharmaceutical ingredient suppliers |

|

Drug Manufacturing |

Multinational pharmaceutical companies, domestic insulin manufacturers, and domestic oral antidiabetic drug producers |

|

Regulatory Approval |

NMPA (National Medical Products Administration); Center for Drug Evaluation (CDE) |

|

Wholesale Distribution |

State-owned and private pharmaceutical distributors; NHSA centralized volume-based procurement framework |

|

Dispensing & Retail |

Hospital pharmacies, retail pharmacy chains, e-commerce, and internet hospital platforms |

|

End Users |

Type-1 & Type-2 diabetic patients; hospitals; NHSA-insured public health beneficiaries |

Technology Landscape in the China Diabetes Market

Volume-Based Procurement and Biosimilar Insulin Technology

In November 2025, Gan & Lee Pharmaceuticals announced that its insulin glargine (Ondibta) received a positive CHMP opinion in Europe, paving the way for commercialization as a biosimilar to Sanofi’s Lantus. It marked a milestone for China-developed insulin, with clinical studies confirming comparable efficacy and safety, supporting expanded global access to affordable diabetes treatments.

Digital Diabetes Management and AI Platform Technology

In July 2025, Novo Nordisk partnered with China’s Fangzhou to develop an AI-driven digital healthcare platform aimed at improving diabetes and obesity management through medication guidance, monitoring, and patient engagement tools. The collaboration focused on enhancing early detection, treatment adherence, and overall care delivery by integrating digital health solutions with chronic disease management in China.

Closed-Loop Insulin Delivery and CGM Innovation

SiBionics developed the GS3 CGM platform, unveiled at ATTD 2025, positioning it as the world’s thinnest continuous glucose monitor with a compact, coin-sized design. The company is also working to integrate the CGM with insulin pumps for automated insulin delivery and has partnered with PharmaSens to develop an all-in-one insulin patch pump.

NMPA Fast-Track Approval for Innovative Diabetes Drugs

China's Breakthrough Therapy designation program, implemented by CDE in 2020, dramatically accelerated domestic approval timelines for innovative diabetes drugs. Domestic GLP-1 candidates qualifying under Breakthrough Therapy have seen approval timelines compress from 24–36 months to 12–18 months, positioning domestic products to reach the Chinese market substantially faster than the historic norm and creating intensifying competitive pressure on established MNC portfolios.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Segment | Oral Antidiabetics | 61.7% | 2025 |

| Distribution Channel | Retail Pharmacies | 45.2% | 2025 |

By Segment

Oral antidiabetics dominate the China diabetes market with a 61.7% share in 2025, the highest OAD market share concentration among major global diabetes markets. This reflects the extraordinary scale of China's Type-2 diabetes patient base, the universal prescription of metformin as first-line therapy across all tiers of the healthcare system, and the NRDL's comprehensive listing of DPP-4 inhibitors, including sitagliptin, alogliptin, and saxagliptin.

To access detailed market analysis, Request Sample

Insulin accounts for 38.3% of the market. VBP price compression has significantly reduced average revenue per insulin unit in the public hospital channel; however, strong volume expansion, driven by rising insulin initiation rates among Type-2 patients and Healthy China 2030 treatment coverage targets, is sustaining overall insulin segment revenue growth at a CAGR of approximately 6.18% through 2034.

By Distribution Channel

Retail pharmacies represent the leading channel at 45.2% share in 2025, driven by China's over 600,000 licensed retail pharmacy outlets nationwide and the NHSA's electronic prescription interoperability enabling community pharmacy dispensing of NRDL-listed diabetes drugs.

Hospital pharmacies follow at 33.1%, reflecting the historical dominance of the public hospital system in China's pharmaceutical market and the VBP program's direct linkage to hospital procurement. E-commerce and tele-pharmacy have reached 21.7% share in 2025, as JD Health, Alibaba Health, and Ping An Good Doctor together account for a high number of chronic disease prescription transactions annually, with diabetes medications among the highest-volume categories.

Competitive Landscape

The China diabetes market exhibits a moderately fragmented structure at both the innovative MNC and domestic manufacturer levels. Global leaders Novo Nordisk A/S, Sanofi, and AstraZeneca compete primarily in the premium private hospital segment and through NRDL-listed branded products, collectively accounting for approximately 45–50% of market revenue in 2025.

|

Company Name |

Core Segment |

Market Position |

Core Strength |

| Novo Nordisk A/S | Insulin & GLP-1 | Market Leader | Largest insulin brand in China; Ozempic is gaining rapid traction |

| Sanofi | Insulin | Market Leader | Lantus is dominant in basal insulin; strong hospital pharmacy network |

| Tonghua Dongbao Pharmaceutical Co., Ltd. | Insulin | Strong Challenger | One of the largest domestic insulin makers; leading in generic human insulin volumes |

| Gan & Lee Pharmaceuticals | Insulin | Strong Challenger | Leading domestic insulin analogue, glargine & lispro biosimilar pioneer |

| AstraZeneca | Oral Antidiabetics | Strong Challenger | Forxiga leading the SGLT-2 OAD class; DECLARE-TIMI 58 and DAPA-CKD trial data widely cited. |

Domestic leaders Tonghua Dongbao Pharmaceutical Co., Ltd. and Gan & Lee Pharmaceuticals dominate the public hospital insulin volume segment via VBP tenders, while an emerging cohort of domestic OAD innovators is challenging MNCs in novel therapeutic classes.

Key Company Profiles

Novo Nordisk A/S

Novo Nordisk A/S, headquartered in Bagsvaerd, Denmark, has operated in China since 1994 and remains the market leader in insulin, with a dedicated manufacturing plant in Tianjin producing insulin products for both the Chinese and Asian markets.

- Product Portfolio: Tresiba (degludec), Ozempic (semaglutide), Victoza (liraglutide), NovoRapid (aspart), Rybelsus (oral semaglutide).

- Recent Developments: In March 2026, Novo Nordisk A/S announced that the FDA approved Awiqli (insulin icodec) as the first once-weekly basal insulin for adults with type 2 diabetes, offering a more convenient alternative to daily injections.

- Strategic Focus: GLP-1 premium market leadership in China's Tier-1 city hospitals; insulin portfolio premiumization toward Tresiba to avoid VBP tendering; digital patient engagement programs via WeChat health management platform.

Sanofi

Sanofi, headquartered in Paris, France, maintains a strong position in China's basal insulin market through Lantus (insulin glargine), historically the country's most-prescribed premium basal insulin. Following VBP Round 6 price compression on glargine products, Sanofi has repositioned its China strategy toward Toujeo (glargine U300) and its cardiovascular-metabolic portfolio.

- Product Portfolio: Lantus (glargine), Toujeo (glargine U300), Apidra (glulisine), Amaryl (glimepiride).

- Recent Developments: In September 2025, Sanofi announced that China’s NMPA approved Tzield (teplizumab) as the first disease-modifying therapy for stage 2 type 1 diabetes, capable of delaying progression to stage 3 disease.

- Strategic Focus: Premium insulin analogue positioning via Toujeo to avoid VBP tendering; digital adherence platform partnerships; OAD franchise expansion in Tier-1 and Tier-2 city private hospitals.

Tonghua Dongbao Pharmaceutical Co., Ltd.

Tonghua Dongbao, headquartered in Tonghua, Jilin Province, is China's largest domestic insulin manufacturer by production volume and has been the primary domestic beneficiary of VBP tendering, winning the majority of national procurement contracts for human insulin and first-generation insulin analogues since 2021.

- Product Portfolio: Gansulin (human insulin), Biosim insulin lispro.

- Recent Developments: In May 2025, Tonghua Dongbao announced progress in advancing its innovative diabetes pipeline, highlighting developments in insulin analogues and GLP-1–related therapies to strengthen its product portfolio.

- Strategic Focus: Volume leadership in VBP public hospital insulin tender channel; GLP-1 pipeline investment targeting NMPA approval by 2027–2028; international export expansion to Southeast Asia and Africa.

Market Concentration Analysis

The China diabetes market exhibits a dual-track concentration structure: moderate-to-high concentration among innovative MNCs in the premium hospital and private market channels (top five MNCs holding ~45–50% of value share), and a highly competitive domestic segment in the public hospital volume channel, where Tonghua Dongbao Pharmaceutical Co., Ltd. and Gan & Lee Pharmaceuticals collectively supply over 50% of public-tender insulin volumes following VBP implementation.

Market concentration is expected to evolve materially through 2034 as domestic Chinese GLP-1 and novel OAD candidates receive NMPA approval and achieve NRDL listing. The entry of Jiangsu Hengrui's dual agonist HRS9531 and Zhejiang Beta's semaglutide biosimilar is projected to intensify OAD competition in the premium private market while creating a new high-volume, NRDL-accessible GLP-1 segment that will benefit domestic manufacturers disproportionately.

Investment & Growth Opportunities

Fastest Growing Segments

Domestic GLP-1 receptor agonists and dual GLP-1/GIP agonists (estimated CAGR ~18–22% post-NMPA approval), SGLT-2 inhibitors in Tier-1–2 hospital channels (CAGR ~14%), and e-commerce and tele-pharmacy distribution platforms (CAGR ~16%) represent the highest-growth investment vectors in China's diabetes market through 2034.

Emerging Market Expansion

China's Tier-3 to Tier-6 cities and rural counties represent the frontier of diabetes market expansion. An estimated 45 million currently undiagnosed or untreated diabetic patients in these geographies will become commercially accessible as community health center infrastructure improves under Healthy China 2030. Investment in county-level hospital OAD distribution networks, community pharmacist education programs, and digital-first patient engagement models tailored to lower-income demographics can unlock this opportunity.

Venture and Institutional Investment Trends

- Key investment themes include domestic GLP-1 and novel OAD pipeline assets (Jiangsu Hengrui, Zhejiang Beta), CGM and closed-loop insulin delivery technology, and e-health platform-pharma commercial partnership models.

- China's pharmaceutical VC and PE ecosystem invested over CNY 12 Billion in diabetes-related pharmaceutical and medtech companies between 2022 and 2025, with domestic GLP-1 and biosimilar insulin companies attracting the largest individual funding rounds.

- International pharmaceutical companies are increasing China R&D center investment to accelerate NMPA submissions for next-generation diabetes therapies, with Novo Nordisk, Sanofi, and Eli Lilly all having announced China R&D expansion plans between 2023 and 2025.

Future Market Outlook (2026-2034)

The China diabetes market is positioned to become the world's largest single-country diabetes pharmaceutical market by the early 2030s, surpassing current market leaders on an absolute value basis. From a base of USD 5.41 Billion in 2025, the market is projected to reach USD 9.89 Billion by 2034, representing total incremental value creation of approximately USD 4.48 Billion at a robust CAGR of 6.73%.

The most transformative structural event over the forecast period will be the NMPA approval and NRDL listing of domestic GLP-1 receptor agonist products between 2026 and 2028. This is expected to trigger a GLP-1 market expansion in China analogous to the SGLT-2 class expansion seen between 2018 and 2023, but at significantly higher patient volumes given the scale of China's Type-2 population.

Long-term, China's diabetes market trajectory is underpinned by three irreversible structural forces: the demographic momentum of an ageing population creating 5–8 million new diabetic patients annually through 2034; the government's Healthy China 2030 policy commitment driving systemic diabetes screening and treatment rate improvements; and China's emergence as a genuine pharmaceutical innovation hub with domestic companies increasingly competing at the clinical frontier of diabetes drug development.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 150 industry participants in 2024–2025, including pharmaceutical company executives, hospital endocrinologists, community health center physicians, NMPA regulatory consultants, NHSA formulary experts, and patient advocacy groups across China's five major regions.

Secondary Research

Secondary research encompassed a systematic review of NMPA regulatory filings, NHSA NRDL publications, VBP tender result announcements, National Bureau of Statistics health data, IDF Diabetes Atlas (10th Edition, 2024), IQVIA China pharmaceutical market intelligence, company annual reports, clinical trial registry data from ClinicalTrials.gov and China's CTR portal, and academic literature.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting approaches, incorporating China's diabetes epidemiological prevalence trajectory, NHSA reimbursement coverage expansion modelling, VBP price impact adjustments, and domestic GLP-1 pipeline launch scenario analysis. A base-case CAGR of 6.73% reflects consensus analyst estimates validated against reported pharmaceutical company China segment revenues and IQVIA channel sales data.

China Diabetes Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered | Oral Antidiabetics, Insulin |

| Distribution Channels Covered | E-commerce and Tele-pharmacy, Hospital Pharmacies, Retail Pharmacies |

| Companies Covered | Novo Nordisk A/S, Sanofi, Tonghua Dongbao Pharmaceutical Co., Ltd., Gan & Lee Pharmaceuticals, AstraZeneca, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the China diabetes market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the China diabetes market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the China diabetes industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the China Diabetes Market Report

The China diabetes market reached USD 5.41 Billion in 2025, making it the largest diabetes pharmaceutical market in Asia-Pacific and accounting for approximately 18–22% of the global diabetes drug market by value.

The market is projected to reach USD 9.89 Billion by 2034, growing at a CAGR of 6.73% during 2026-2034, driven by China's expanding diabetic patient population, NRDL coverage expansion, domestic GLP-1 product launches, and digital health platform growth.

Oral antidiabetics lead with a 61.7% market share in 2025. This is the highest OAD market concentration among major global diabetes markets, driven by the universal prescription of NRDL-listed metformin and DPP-4 inhibitors across China's community health system.

Insulin accounts for 38.3% of the market in 2025 (approximately USD 2.07 Billion). VBP price compression has reshaped the insulin competitive landscape, with domestic players Tonghua Dongbao and Gan & Lee capturing over 50% of public hospital volume. Biosimilar glargine is expected to reach 45% of total insulin volume by 2034 as VBP coverage expands.

Retail pharmacies lead with 45.2% share in 2025. However, China's e-commerce and tele-pharmacy channel at 21.7% share in 2025 is among the highest globally and is the fastest-growing channel, driven by JD Health, Alibaba Health, and Ping An Good Doctor, processing hundreds of millions of chronic disease prescriptions annually.

Key players include global MNCs Novo Nordisk A/S, Sanofi, Tonghua Dongbao Pharmaceutical Co., Ltd., Gan & Lee Pharmaceuticals, and AstraZeneca.

VBP has been transformative for China's insulin segment since 2021, compressing average selling prices by 40–70% while dramatically expanding patient access volumes through public hospitals.

Domestic GLP-1 products, including Jiangsu Hengrui's HRS9531 and domestic semaglutide biosimilar candidates, represent the single largest incremental market opportunity in China. NRDL listing following approval could create a USD 800 Million to USD 1.2 Billion annual revenue segment by 2030, transforming the OAD competitive landscape.

Key opportunities include domestic GLP-1 and novel OAD pipeline investment, biosimilar insulin manufacturing scale-up, AI-powered CGM and digital diabetes management platforms, Tier-3–6 city market expansion infrastructure, and e-health platform-pharma commercial partnership models.

Healthy China 2030 targets increasing diabetes diagnosis rates from 46% to 65% and treatment rates from 42% to 60% by 2030. Achievement of these targets would bring an estimated 25–35 million currently undiagnosed or untreated patients into the pharmacotherapy market, creating the single largest volume growth driver for the OAD segment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)