China Last Mile Delivery Market Size, Share, Trends and Forecast by Service Type, Technology, Application, and Region, 2026-2034

China Last Mile Delivery Market Summary:

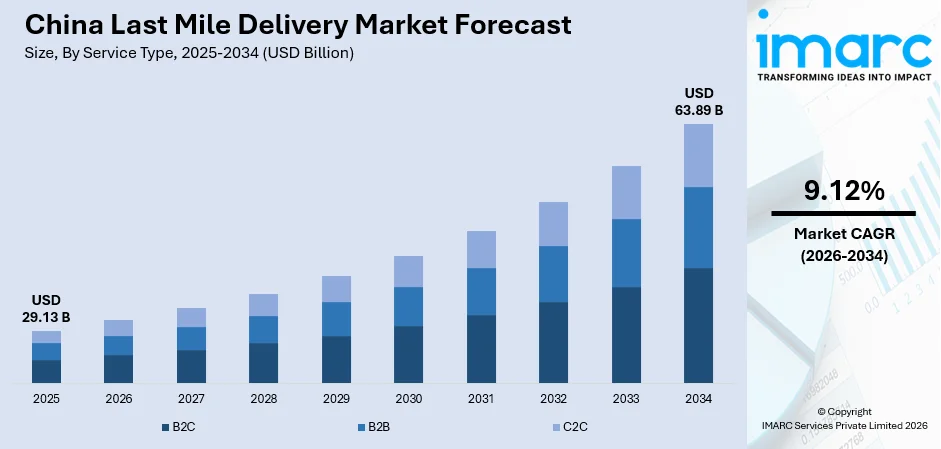

The China last mile delivery market size was valued at USD 29.13 Billion in 2025 and is projected to reach USD 63.89 Billion by 2034, growing at a compound annual growth rate of 9.12% from 2026-2034.

The China last mile delivery market is experiencing robust expansion driven by the rapid growth of e-commerce, rising consumer expectations for faster delivery, and the integration of advanced technologies across logistics networks. Increasing urbanization, widespread digital payment adoption, and the proliferation of instant retail platforms are accelerating demand for efficient fulfillment solutions. Government support for smart logistics, investments in autonomous delivery infrastructure, and the development of low-altitude drone networks are further strengthening the operational ecosystem, positioning China as a global leader in last mile delivery innovation and China last mile delivery market share.

Key Takeaways and Insights:

- By Service Type: B2C dominates the market with a share of 58.9% in 2025, owing to the explosive growth of consumer-focused e-commerce platforms, rising digital payment adoption, and increasing demand for same-day and next-day deliveries across urban and semi-urban areas.

- By Technology: Non-autonomous leads the market with a share of 72.4% in 2025, driven by the well-established courier workforce, extensive manual logistics networks, and cost-effective delivery models that continue to serve a vast majority of fulfillment operations.

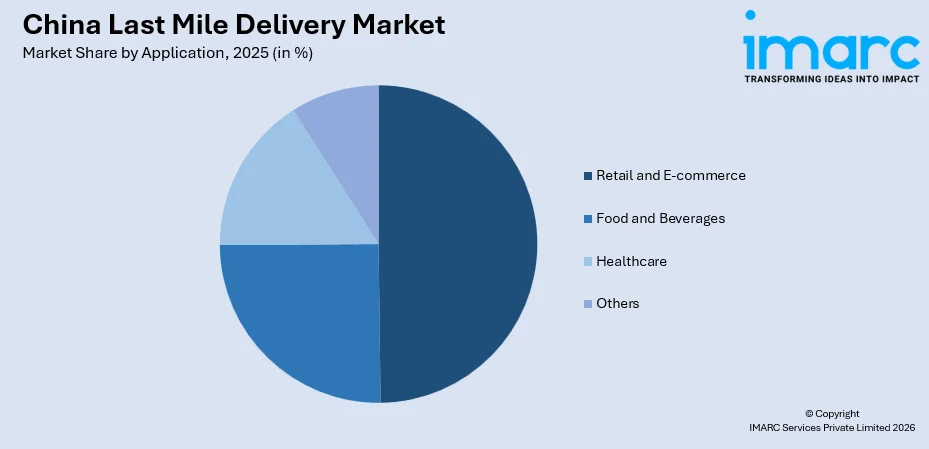

- By Application: Retail and e-commerce represent the largest segment with a market share of 49.6% in 2025, reflecting China's position as the world's largest online retail market with deeply integrated delivery infrastructure that supports billions of transactions annually.

- By Region: East China comprises the largest region with 36.8% share in 2025, driven by the concentration of major e-commerce headquarters, advanced logistics infrastructure, high population density, and strong consumer purchasing power across key provinces and metropolitan areas.

- Key Players: The market is highly fragmented, marked by intense price competition, rapid e-commerce expansion, rising labor and compliance costs, and growing adoption of automation and logistics technologies, as specialists and platform-driven networks compete on speed, coverage, and service quality.

To get more information on this market Request Sample

The China last mile delivery market continues to advance as e-commerce volumes reach unprecedented levels, compelling logistics providers to adopt smarter, faster, and more efficient fulfillment strategies. Consumer expectations for rapid delivery have intensified competitive dynamics among major platforms and logistics operators. According to the State Post Bureau, China's courier sector handled 174.5 billion parcels in 2024, representing a 21% year-on-year increase, with the average Chinese citizen receiving over 100 parcels annually. This massive scale underscores the critical importance of last mile efficiency in sustaining the country's logistics ecosystem. The integration of artificial intelligence, route optimization, and automated sorting technologies is reshaping operational workflows. Government initiatives supporting low-altitude logistics, smart city development, and standardized delivery regulations are providing a foundation for sustained China last mile delivery market growth.

China Last Mile Delivery Market Trends:

Rapid Commercialization of Autonomous Delivery Vehicles

China is witnessing accelerated deployment of autonomous delivery vehicles across urban logistics networks as technology costs decline, and regulatory pathways expand. By mid-2025, over 100 Chinese cities had opened roads to unmanned delivery vehicles, with over 6,000 autonomous units in operation across the country by end of 2024, according to the State Post Bureau. Major logistics platforms and independent manufacturers are scaling fleet operations, integrating artificial intelligence and advanced navigation to reduce labor dependency and improve delivery consistency across high-density corridors.

Emergence of Low-Altitude Drone Delivery Networks

The development of low-altitude logistics is transforming last mile delivery capabilities in China, particularly for time-sensitive and hard-to-reach deliveries. For example, in April 2025, Meituan's fourth-generation drone received the country's first nationwide low-altitude logistics operating certificate from the Civil Aviation Administration of China, enabling commercial drone deliveries across major cities. Investments in drone route infrastructure, payload capacity, and autonomous navigation are enabling faster and more flexible fulfillment options, supporting broader China last mile delivery market growth.

Intensifying Competition in Instant Retail Fulfillment

China's delivery ecosystem is undergoing a structural shift as major technology platforms expand beyond traditional food delivery into comprehensive instant retail services. For instance, Meituan recorded 150 million orders on a single day in July 2025, the highest in China's food delivery history, as the platform expanded its coverage to include consumer goods, electronics, and apparel. The convergence of on-demand logistics, micro-fulfillment warehousing, and AI-powered dispatch systems is compressing delivery windows and reshaping consumer expectations across urban markets.

Market Outlook 2026-2034:

The China last mile delivery market is positioned for sustained expansion, supported by the continuous growth of e-commerce, the development of autonomous delivery technologies and changing consumer demands for faster delivery. The implementation of drone delivery systems, robotic logistics systems and smart warehousing systems will result in operational cost savings and enhanced service reliability for both urban and rural areas. As such, Huawei introduced its SMART Logistics & Warehousing Solution at HUAWEI CONNECT 2025 in Shanghai which demonstrates AI-powered platform-driven logistics functions. The competitive environment will receive additional changes from government initiatives that promote intelligent logistics, develop low-altitude economies and implement labor protection reforms. Moreover, the logistics industry will develop through key trends which include artificial intelligence adoption, real-time analytics implementation and the use of advanced fleet management solutions as logistics providers build AI systems that will allow them to use automated technology across more territories while offering multiple services to meet complex consumer demands. The market generated a revenue of USD 29.13 Billion in 2025 and is projected to reach a revenue of USD 63.89 Billion by 2034, growing at a compound annual growth rate of 9.12% from 2026-2034.

China Last Mile Delivery Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Service Type |

B2C |

58.9% |

|

Technology |

Non-autonomous |

72.4% |

|

Application |

Retail and E-commerce |

49.6% |

|

Region |

East China |

36.8% |

Service Type Insights:

- B2C

- B2B

- C2C

B2C dominates with a market share of 58.9% of the total China last mile delivery market in 2025.

The B2C segment leads the China last mile delivery market, driven by the extraordinary scale of consumer-facing e-commerce transactions across the country. China's online shopping penetration has risen sharply, with online retail accounting for 26.8% of all retail sales of consumer goods in 2024, according to the China Academy of Information and Communications Technology. This structural shift toward digital commerce has created immense demand for efficient, reliable, and fast last mile delivery solutions that connect warehouses and fulfillment centers directly to individual consumers across diverse geographic settings.

The growing sophistication of B2C delivery services reflects evolving consumer expectations for speed, convenience, and transparency. Platforms are investing heavily in micro-fulfillment infrastructure, real-time order tracking, and flexible delivery windows to enhance the customer experience. The expansion of same-day and next-day delivery promises, coupled with seamless integration between online retail platforms and logistics networks, continues to reinforce B2C as the dominant service model in the market.

Technology Insights:

- Autonomous

- Non-autonomous

Non-autonomous leads with a share of 72.4% of the total China last mile delivery market in 2025.

The non-autonomous segment accounts for the largest share of the China last mile delivery market, reflecting the continued reliance on human-operated delivery networks that form the backbone of the country's logistics infrastructure. China's massive courier workforce, supported by electric bikes, motorcycles, and light commercial vehicles, handles the vast majority of parcel deliveries across urban and rural areas. According to the All-China Federation of Trade Unions, the number of workers in new forms of employment, including delivery riders and couriers, surpassed 84 million in 2024, underscoring the scale of labor-intensive logistics operations.

Non-autonomous delivery models continue to evolve through the integration of technology-assisted tools including AI-powered route optimization, digital dispatch platforms, and smart locker networks that enhance productivity without fully replacing human operators. While autonomous technologies are gaining momentum, the affordability, flexibility, and established reach of non-autonomous delivery systems ensure their continued dominance in serving China's high-volume logistics demands.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Food and Beverages

- Retail and E-commerce

- Healthcare

- Others

Retail and e-commerce are the largest segment, accounting for 49.6% of the total China last mile delivery market in 2025.

The retail and e-commerce segment commands the largest application share in the China last mile delivery market, fueled by the country's position as the world's largest online retail market. Consumer spending through digital platforms has expanded consistently, with China's online retail sales reaching CNY 15.52 Trillion in 2024, growing 7.2% year-on-year, according to the National Bureau of Statistics. This sustained growth in digital commerce creates enormous demand for last mile delivery services that connect online marketplaces with consumers across every tier of Chinese cities and rural communities.

The competitive dynamics within China's e-commerce ecosystem are directly driving innovation in last mile logistics. Major platforms including established marketplaces and emerging short-video commerce channels are competing on delivery speed and reliability, pushing logistics providers to adopt advanced sorting systems, distributed warehousing, and intelligent dispatch technologies. During the 2024 Singles' Day shopping festival, total sales across major platforms reached approximately CNY 1.44 Trillion, demonstrating the massive peak-season pressure that demands scalable and resilient last mile delivery networks capable of handling extraordinary order volumes within compressed timeframes.

Regional Insights:

- North China

- East China

- South Central China

- Southwest China

- Northwest China

- Northeast China

East China exhibits a clear dominance with a 36.8% share of the total China last mile delivery market in 2025.

East China represents the largest regional market for last mile delivery, anchored by the presence of major e-commerce headquarters, advanced logistics hubs, and a highly connected consumer base spanning provinces such as Zhejiang, Jiangsu, Shanghai, and Shandong. The region benefits from dense transportation networks, high urbanization rates, and strong digital infrastructure that facilitate efficient fulfillment operations. For example, Yiwu in Zhejiang Province alone ships over 14 million parcels daily through ZTO Express's extensive network, supported by 16 distribution centers each with capacity exceeding one million parcels. East China's concentration of manufacturing, wholesale, and retail activities creates a uniquely high demand for last mile services, with the region serving as the primary origin and destination point for a substantial portion of China's express delivery volume.

In addition, East China’s last-mile delivery market is increasingly leveraging automation, AI-powered route optimization, and smart warehousing solutions to enhance speed and reliability. Growing consumer expectations for same-day and next-day deliveries, coupled with rising e-commerce penetration, are driving logistics providers to adopt innovative technologies and collaborative networks, positioning the region as a testing ground for next-generation urban fulfillment models and a benchmark for efficiency across China’s broader delivery ecosystem.

Market Dynamics:

Growth Drivers:

Why is the China Last Mile Delivery Market Growing?

Explosive Growth of E-Commerce and Digital Consumption

China’s e-commerce ecosystem is rapidly expanding, driving unprecedented demand for last-mile delivery nationwide. The rise of online shopping, live-streaming commerce, and social commerce platforms has generated continuous parcel volumes requiring efficient fulfillment. Industry report states that in China, over 900 million people, about 64.3% of the population, shop online, with 85.4% of women purchasing heavily in beauty, personal care, clothing, and jewelry categories. Consumers increasingly prefer digital channels, while platforms like Douyin and Kuaishou diversify order sources and delivery needs. Growth now spans fresh produce, pharmaceuticals, and specialty goods, necessitating tailored last-mile solutions. Cross-border e-commerce and rural online retail are further expanding delivery networks, prompting logistics providers to invest in broader coverage, faster transit times, automated operations, and advanced tracking systems to meet evolving consumer expectations and maintain competitive service levels.

Advancement of Autonomous and Intelligent Logistics Technologies

Rapid technological innovation in autonomous delivery vehicles, drones, and artificial intelligence is transforming the efficiency and scalability of last mile operations in China. Companies are deploying fleets of self-driving delivery robots and unmanned aerial vehicles to reduce labor dependency, lower operational costs, and improve delivery consistency. For example, in October 2025, autonomous delivery vehicle maker Neolix raised over USD 600 Million in Series D financing, the largest private fundraising in China's autonomous driving sector, to accelerate large-scale commercial deployment of its Level 4 RoboVan solutions serving major express delivery companies. Furthermore, the integration of AI-powered dispatch engines, real-time route optimization, and smart warehousing systems is enabling logistics operators to process higher volumes with greater precision. These technological advancements are creating a foundation for more cost-effective and reliable delivery operations.

Supportive Government Policies and Regulatory Framework

Government support at both national and local levels is providing strong tailwinds for the China last mile delivery market, with policies promoting smart logistics, low-altitude economy development, and standardized delivery practices. Regulatory bodies are creating enabling environments for autonomous delivery deployment, drone logistics integration, and digital infrastructure upgrades. The State Post Bureau has issued industry standards including development guidelines and service specifications for unmanned vehicles to accelerate adoption. Additionally, the Civil Aviation Administration of China approved 150 additional drone routes in 2024, expanding the operational scope for aerial delivery services across urban and rural corridors. These policy measures are reducing barriers to entry, encouraging innovation, and fostering an environment conducive to large-scale adoption of next-generation logistics solutions.

Market Restraints:

What Challenges the China Last Mile Delivery Market is Facing?

Regulatory Complexity for Autonomous Delivery at Scale

Despite growing government support, the deployment of autonomous delivery vehicles and drones faces regulatory hurdles including fragmented local licensing requirements, evolving safety standards, and inconsistent road access policies across different municipalities. The absence of unified national regulations for unmanned delivery operations creates compliance challenges for logistics providers seeking to scale autonomous fleets across multiple cities. Varying requirements for vehicle registration, operational permits, and insurance obligations add complexity and delay the pace of large-scale commercialization.

Intense Price Competition and Thin Profit Margins

The China last mile delivery market is characterized by fierce price competition among major logistics providers, leading to persistently thin profit margins across the industry. Delivery rates per parcel have declined over successive years as operators compete aggressively for volume, compressing revenues and limiting reinvestment capacity. Smaller and mid-tier players face growing pressure to maintain viability as larger platforms leverage economies of scale, technology investments, and vertical integration to offer lower pricing and absorb operational costs.

Last Mile Infrastructure Limitations in Rural and Remote Areas

While China's urban logistics networks are highly developed, significant infrastructure gaps persist in rural, mountainous, and remote regions where population density is low and transportation connectivity remains limited. Delivering parcels to these areas involves higher per-unit costs, longer transit times, and logistical complexities that reduce operational efficiency. The lack of sufficient sorting facilities, relay stations, and charging infrastructure for electric delivery vehicles in these underserved areas restricts the expansion of comprehensive last mile coverage beyond major urban centers.

Competitive Landscape:

The China last mile delivery market features an intensely competitive landscape characterized by the dominance of major integrated logistics platforms alongside a growing cohort of autonomous delivery technology providers. Established express delivery companies are leveraging expansive national networks, advanced sorting infrastructure, and technology-driven optimization to maintain market leadership. Competition is increasingly shaped by investments in autonomous vehicles, drone delivery, and AI-powered dispatch systems that enable faster and more cost-efficient operations. Strategic partnerships between e-commerce platforms and logistics operators, consolidation among mid-tier providers, and the emergence of specialized last mile technology firms are reshaping the competitive dynamics and driving innovation across the entire delivery value chain.

Recent Developments:

- In February 2026, 11Street partnered with JD.com to launch a reverse direct-buy service in H1 2026, enabling 11Street sellers to access Chinese consumers via JD Worldwide. JD Logistics manages cross-border warehousing, customs, and last-mile delivery, reducing entry barriers and creating a permanent Korea–China distribution pipeline.

- In January 2026, Alibaba Group merged its autonomous-driving unit with Zelos Technology in a USD 2 Billion deal, forming Cainiao Robovan. The combined firm will operate 20,000+ autonomous delivery vans, advancing China’s automated logistics, last-mile delivery, and unmanned freight capabilities.

China Last Mile Delivery Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Billion |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Service Types Covered |

B2C, B2B, C2C |

|

Technologies Covered |

Autonomous, Non-autonomous |

|

Applications Covered |

Food and Beverages, Retail and E-commerce, Healthcare, Others |

|

Regions Covered |

North China, East China, South Central China, Southwest China, Northwest China, Northeast China |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the China Last Mile Delivery Market Report

The China last mile delivery market size was valued at USD 29.13 Billion in 2025.

The China last mile delivery market is expected to grow at a compound annual growth rate of 9.12% from 2026-2034 to reach USD 63.89 Billion by 2034.

B2C dominated the market with a share of 58.9%, driven by the massive scale of consumer-focused e-commerce transactions, rising online shopping penetration, and growing demand for fast, reliable doorstep deliveries across urban and rural China.

Key factors driving the China last mile delivery market include explosive e-commerce growth, advancing autonomous delivery technologies, supportive government logistics policies, rising consumer demand for rapid fulfillment, and expanding digital payment ecosystems.

Major challenges include regulatory complexity for autonomous delivery at scale, intense price competition leading to thin profit margins, last mile infrastructure gaps in rural areas, rising labor compliance costs, and fragmented local licensing requirements for unmanned delivery operations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)