China Skincare Market Size, Share, Trends and Forecast by Distribution Channel, Ingredient Type, and Gender, 2026-2034

China Skincare Market Size, Share, Trends & Forecast (2026-2034)

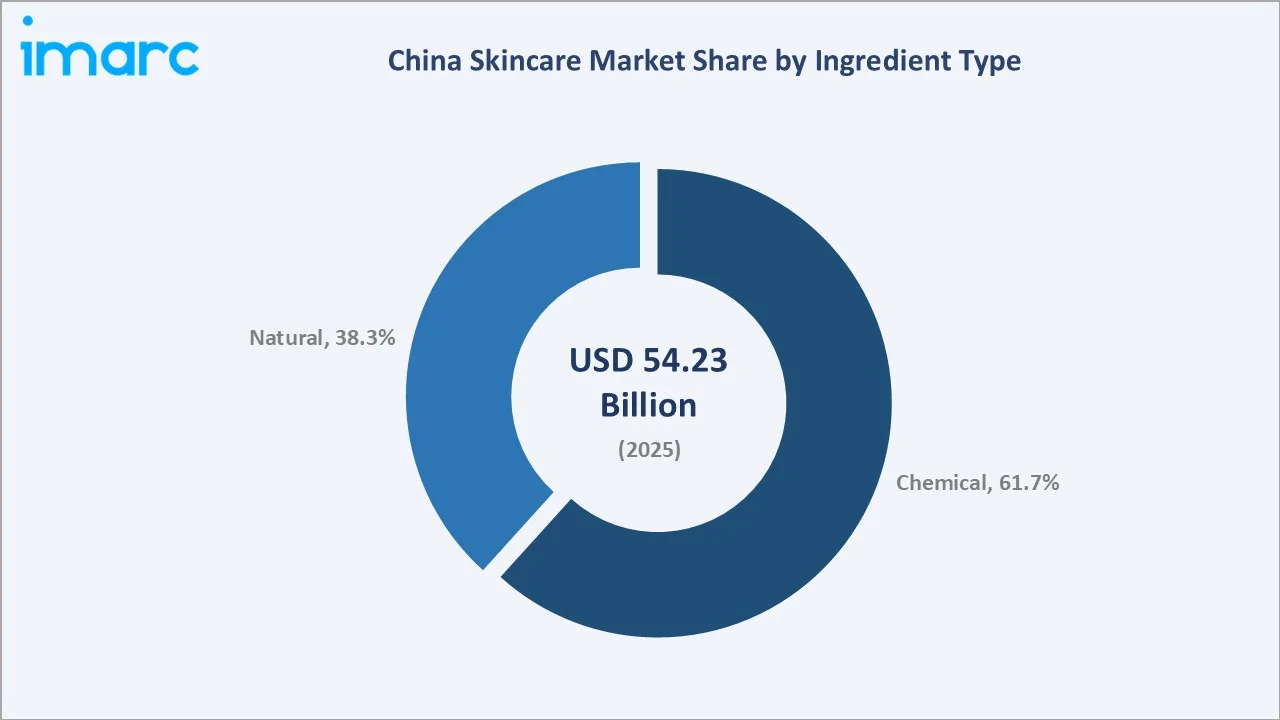

The China skincare market size reached USD 54.23 Billion in 2025 and is projected to reach USD 112.37 Billion by 2034, exhibiting a CAGR of 7.72% during 2026-2034. Rising pollution-driven skin health awareness, robust e-commerce expansion led by Singles' Day and 618 shopping events, and the proliferation of K-beauty and J-beauty multi-step routines are the primary forces driving market growth.

Offline channels dominate distribution at 58.6% in 2025, while chemical formulations lead the ingredient mix at 61.7%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 54.23 Billion |

|

Forecast Market Size (2034) |

USD 112.37 Billion |

|

CAGR (2026-2034) |

7.72% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Distribution Channel |

Offline (58.6%, 2025) |

|

Leading Ingredient Type |

Chemical (61.7%, 2025) |

The China skincare market growth trajectory from 2020 through 2034, with historical expansion to USD 54.23 Billion in 2025, reflects consistent pollution-driven demand, while the forecast to USD 112.37 Billion captures accelerating digital-channel adoption and premium segment penetration.

To get more information on this market, Request Sample

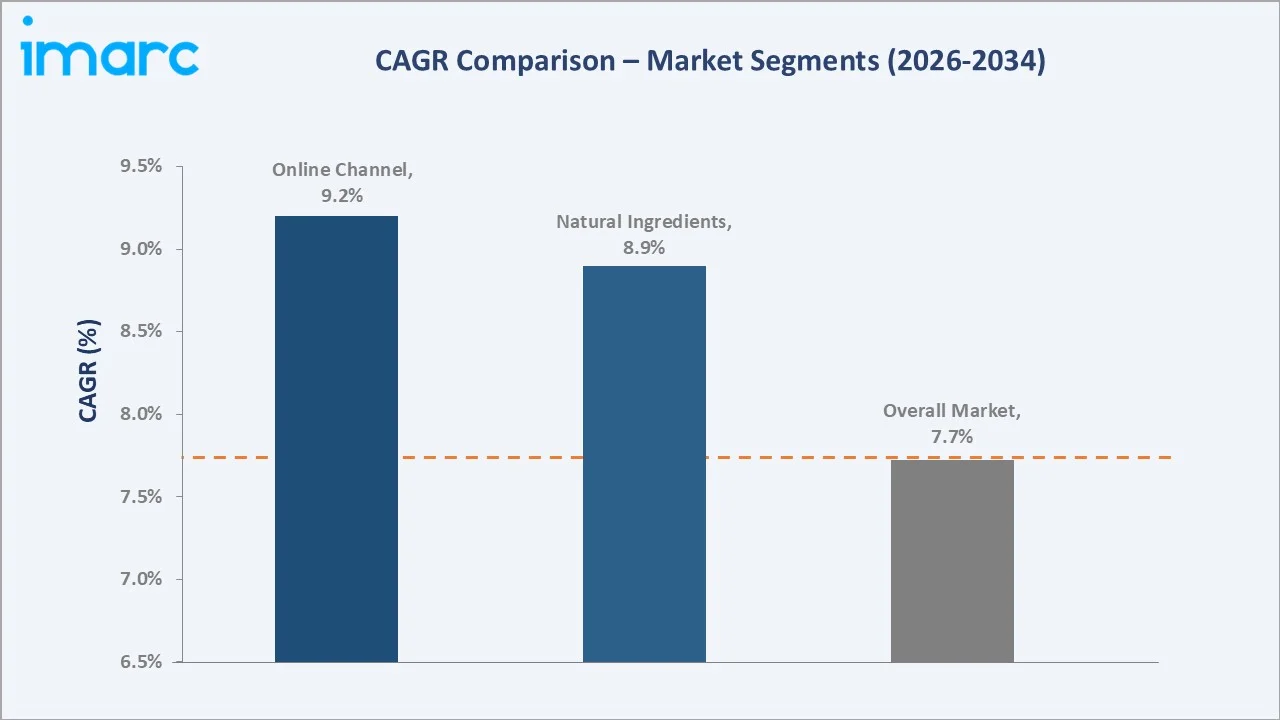

The CAGR trajectories across key channel, ingredient, and demographic sub-segments, with online channel at ~9.2% CAGR and natural ingredients at ~8.9% CAGR, are the fastest-growing categories within the China skincare industry analysis through 2034.

Executive Summary

The China skincare market is on a sustained growth trajectory from USD 54.23 Billion in 2025 to USD 112.37 Billion by 2034. Skincare, deployed across cleansing, moisturizing, anti-aging, sun protection, and specialty treatment routines, benefits from pollution-driven demand and rising beauty consciousness across millennial and Gen Z demographics.

Offline distribution dominates at 58.6% in 2025, owing to experiential shopping preference, expert consultations, and product authentication concerns in a market sensitive to counterfeits. Online channels at 41.4% are growing fastest at ~9.2% CAGR through 2034, propelled by Tmall, JD.com, Douyin livestreaming, and Xiaohongshu content commerce.

Chemical formulations lead ingredient type at 61.7% in 2025, reflecting formulation stability, efficacy in targeted concerns such as pigmentation and acne, and broad mass-market distribution. Natural ingredients at 38.3% represent the fastest-growing ingredient segment, driven by Traditional Chinese Medicine heritage and organic beauty preferences.

Key Market Insights

|

Insight |

Data |

|

Largest Distribution Channel |

Offline - 58.6% share (2025) |

|

Leading Ingredient Type |

Chemical - 61.7% share (2025) |

|

Top Companies |

L'ORÉAL, Estée Lauder Inc, Procter & Gamble, Amorepacific, Jahwa, Florasis |

Key Analytical Observations Expanding on the Above Data:

- Offline channels, with 58.6% in 2025, dominate because Chinese consumers prioritize tactile product testing, authentication assurance, and in-store beauty advisor consultations. Department store counters, specialty chains such as Sephora and Watsons, and pharmacy outlets collectively anchor consumer trust for premium skincare purchases.

- Chemical ingredients, with 61.7% in 2025, lead because they provide formulation stability, longer shelf life, and proven efficacy against specific concerns including acne, hyperpigmentation, and photoaging. Active compounds such as retinoids, niacinamide, and hyaluronic acid anchor most of the anti-aging and corrective skincare specifications across domestic and international brands.

China Skincare Market Overview

Skincare is a personal care category covering cleansers, toners, serums, moisturizers, sunscreens, masks, and targeted treatments formulated to maintain skin health, address specific concerns, and support aesthetic goals. Products span mass, masstige, premium, and luxury price tiers across domestic and international brand portfolios.

The Chinese ecosystem integrates ingredient suppliers, international and domestic brand manufacturers, OEM and ODM contract producers concentrated in Guangdong and Zhejiang, e-commerce platforms, KOL and livestreaming agencies, specialty beauty retailers, pharmacies, and diverse end consumers spanning Gen Z, millennials, and a growing male customer base.

Market Dynamics

To evaluate market opportunities, Request Sample

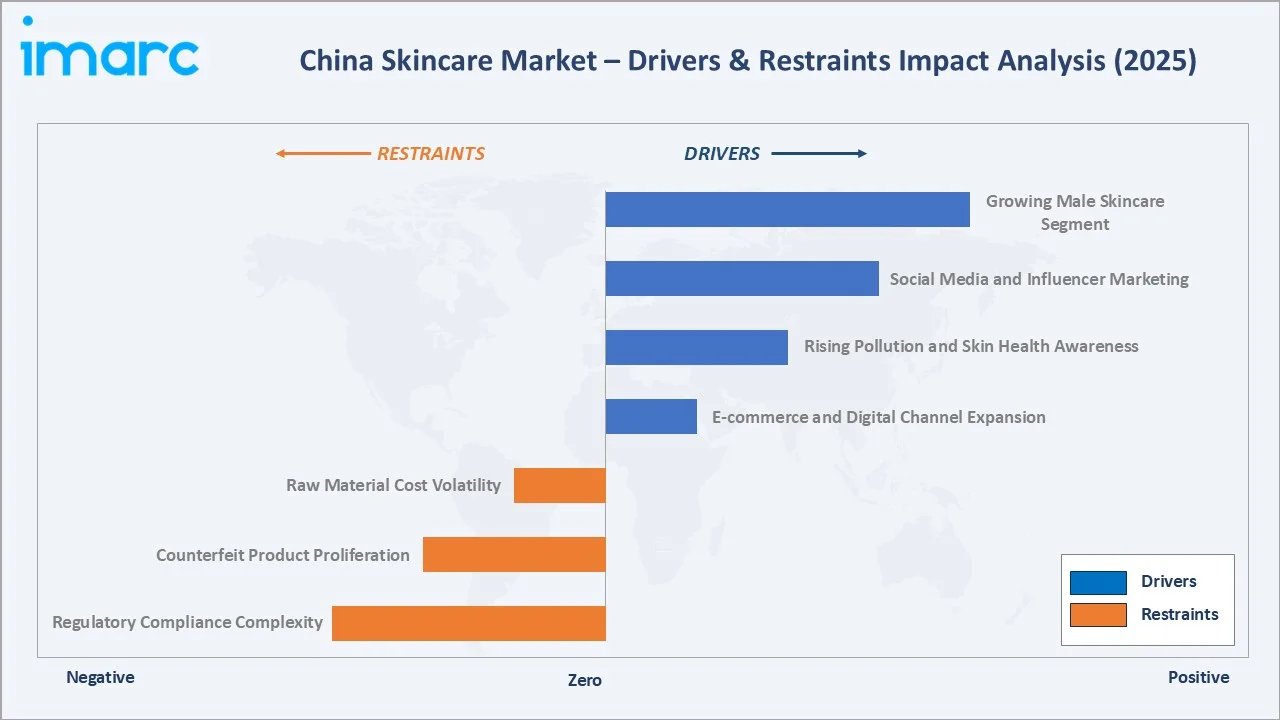

Market Drivers

- E-commerce and Digital Channel Expansion: China's e-commerce sector reached 7.1 trillion yuan in online sales in 2024, up 9.8% year on year. Tmall, JD.com, Douyin, and Xiaohongshu anchor skincare discovery, review, and purchase journeys, with Singles' Day and 618 festivals generating concentrated sales peaks for domestic and international brands.

- Rising Pollution and Skin Health Awareness: Chinese cities exceeding WHO PM2.5 thresholds rose from 98 to 117 in 2023, intensifying consumer demand for anti-pollution cleansers, antioxidant serums, and protective barrier creams. Ingredients such as vitamin C, hyaluronic acid, and detoxifying botanicals have become standard in urban consumer skincare routines.

- Social media and Influencer Marketing: Xiaohongshu, Douyin, and Weibo host dense communities where KOLs, livestreaming hosts, and dermatologist-creators shape skincare purchase decisions. A 2025 survey reported that 45 percent of Chinese consumers made a purchase on social media because of the influencers or celebrities they follow. K-beauty and J-beauty multi-step routines propagated through social content have transformed skincare from an optional into an essential urban lifestyle category.

Market Restraints

- Regulatory Compliance Complexity: China's National Medical Products Administration (NMPA) registration and Cosmetic Supervision and Administration Regulation (CSAR) requirements extend international brand launch timelines by 6 to 18 months and require animal testing exemptions for imports, raising compliance costs and delaying speed-to-market for new product introductions.

- Counterfeit Product Proliferation: Counterfeit premium skincare remains widespread across secondary marketplaces, grey-market channels, and cross-border parallel imports, eroding consumer trust and forcing brands into significant anti-counterfeiting, authentication technology, and brand protection investments, particularly for luxury-tier products sold at department store counters.

Market Opportunities

- Male Skincare Segment Expansion: The male consumer segment is the fastest-growing demographic within China skincare. Chinese men use 2.5 skincare products on average per day, and 7.4 different product categories every two months. Professional grooming norms in Tier-1 cities, male-targeted product launches by L'Oréal, Nivea, and domestic brands, and reduced stigma around male beauty routines are creating material category whitespace.

- TCM-Inspired Natural Formulations: Florasis' 2025 skincare launch, inspired by Traditional Chinese Medicine principles using jade powder, ginseng, and botanical extracts, signals growing consumer appetite for heritage-branded natural products. Domestic brands are leveraging TCM narratives to differentiate from international players and command premium pricing in the natural segment.

Market Challenges

- Raw Material Cost Volatility: Hyaluronic acid, retinol, peptides, and specialty botanical actives face price volatility from supply concentration and currency fluctuations. Active pharmaceutical ingredient sourcing disruptions and packaging material cost increases compress brand margins, particularly for mid-tier domestic manufacturers without scale-driven procurement leverage.

- Market Saturation in Tier-1 Cities: Shanghai, Beijing, Guangzhou, and Shenzhen skincare penetration already exceeds 85% among target female demographics, making Tier-1 city growth a share-shift game. Brands must invest in Tier-2 and Tier-3 city distribution, localized marketing, and price-tier extension to sustain growth rates above category average.

Emerging Market Trends

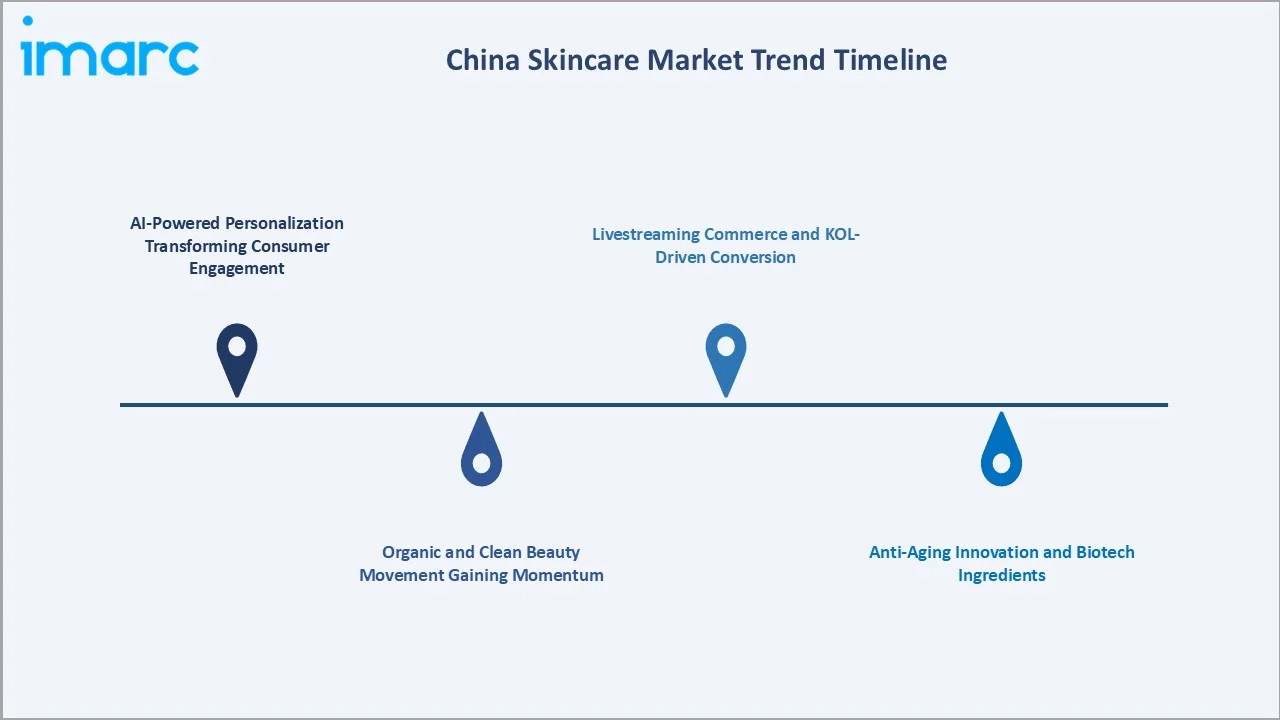

1. AI-Powered Personalization Transforming Consumer Engagement

Artificial intelligence and big data analytics are reshaping how Chinese consumers discover and select skincare. AI-driven skin diagnostics on Tmall and Douyin, virtual try-on features, personalized product recommendations based on purchase history and skin concerns, and chatbot beauty advisors are becoming standard expectations for digitally native Gen Z consumers.

2. Organic and Clean Beauty Movement Gaining Momentum

Consumer demand for paraben-free, sulfate-free, and fragrance-free formulations is rising among millennials and Gen Z, particularly in Tier-1 cities. International clean beauty brands and domestic natural labels such as Herborist and Florasis are capturing share with biodegradable packaging, cruelty-free certifications, and ingredient transparency on packaging and digital storefronts.

3. Anti-Aging Innovation and Biotech Ingredients

L'Oréal's 2024 launch of animal-free collagen skincare in China using recombinant technology marks a broader biotech ingredient shift. Recombinant collagen, peptide complexes, stem cell extracts, and fermented actives are anchoring anti-aging innovation, driving premium skincare pricing.

4. Livestreaming Commerce and KOL-Driven Conversion

Livestreaming on Taobao Live, Douyin, and Kuaishou converts skincare interest into purchase at unprecedented rates, with top beauty hosts moving millions of units in single broadcasts. Brands allocate 20 to 35% of digital marketing spend to KOL collaborations, livestream sessions, and content commerce integrations across the skincare category.

Industry Value Chain Analysis

The China skincare value chain spans six stages from raw ingredient supply through end-consumer purchase. Brand development and distribution and marketing capture the highest value-add margins, while contract manufacturing generates scale economics that favor large OEM and ODM producers in Guangdong and Zhejiang provinces.

|

Stage |

Key Players / Examples |

|

Raw Ingredient Supply |

Specialty chemical suppliers, botanical extract producers, active ingredient manufacturers, biotech ingredient firms |

|

Brand Manufacturers |

International beauty conglomerates, domestic skincare brands, K-beauty and J-beauty entrants, niche natural labels |

|

Contract Manufacturing |

OEM and ODM producers, private-label manufacturers, regional fabrication hubs, specialty formulation houses |

|

Distribution & Marketing |

E-commerce platforms, social commerce networks, KOL and livestreaming agencies, cross-border e-commerce operators |

|

Retail Execution |

Specialty beauty retailers, department store counters, pharmacy chains, drugstores, online marketplaces |

|

End Customers |

Urban millennials, Gen Z consumers, rising male segment, Tier-1 and Tier-2 city professionals |

Vertically integrated brands with captive OEM relationships and proprietary actives, such as L'Oréal's Shanghai research centre and Amorepacific's integrated Korean Chinese production network, achieve lower cost structures and faster speed-to-market than brands dependent entirely on third-party formulation and contract production.

Technology Landscape in the China Skincare Industry

Formulation Technology: Encapsulation and Delivery Systems

Advanced encapsulation technologies including liposomes, niosomes, and microsphere delivery systems enable stable incorporation of sensitive actives such as retinol, vitamin C, and peptides. Time-release encapsulation and pH-triggered delivery improve efficacy and reduce irritation, commanding premium pricing in corrective and anti-aging skincare positioned above USD 80 per unit.

Biotechnology and Recombinant Ingredients

Recombinant collagen, bioengineered peptides, and fermentation-derived actives such as Bifida Ferment Lysate and Galactomyces are replacing conventional animal-sourced ingredients. Chinese biotech firms including Bloomage Biotech and Giant Biogene lead global production, with recombinant collagen penetration rising rapidly across domestic anti-aging launches through 2027.

Personalization and AI-Driven Skin Analytics

AI-powered skin diagnostic apps analyze skin condition, sun damage, hydration, and aging markers through smartphone photography to recommend tailored skincare regimens. Brands including L'Oréal, Shiseido, and domestic players embed diagnostic technology in flagship stores, e-commerce apps, and dermatology clinics to drive personalized product selection.

Digital Commerce and Social Integration

Integration of livestreaming, short-form video, and social commerce with skincare discovery has reshaped the purchase funnel. Platforms enable brands to move from awareness to transaction within single sessions, with AR try-on, dermatologist Q&A, and influencer demonstrations compressing evaluation timelines for skincare purchases significantly.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Distribution Channel | Offline | 58.6% | 2025 |

| Ingredient Type | Chemical | 61.7% | 2025 |

| Gender | Female | 🔒 | 2025 |

By Distribution Channel

Offline commands a 58.6% majority share in 2025 owing to the Chinese consumer preference for tactile product testing, expert consultations, and immediate authentication. Department store counters, specialty beauty retailers including Sephora and Watsons, and local pharmacies provide trusted environments for premium skincare purchase decisions, particularly for products in the premium and luxury tiers.

To access detailed market analysis, Request Sample

Online channels at 41.4% in 2025, growing fastest, capture convenience-oriented and digital-native consumers.

By Ingredient Type

Chemical ingredients dominate at 61.7% in 2025, representing formulation stability, proven efficacy in targeted concerns, and broad mass-market accessibility. Active compounds including retinoids, alpha-hydroxy acids, niacinamide, and peptides anchor the majority of corrective, brightening, and anti-aging specifications across domestic and international brand portfolios at all price tiers.

Natural ingredients at 38.3% in 2025 are growing fastest within the category, driven by Traditional Chinese Medicine heritage, organic beauty preferences, and sustainability-oriented millennial and Gen Z consumers. Botanical extracts, plant-derived actives, fermented naturals, and TCM-inspired formulations from Herborist, Florasis, and Annemarie Börlind represent the fastest-growing ingredient opportunity segment.

Competitive Landscape

The China skincare market is moderately concentrated, with international leaders holding strong premium and prestige positions while domestic brands and K-beauty players compete across mass, masstige, and emerging natural segments. International brands dominate luxury, while Chinese players win in TCM-inspired natural and digitally native segments.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

L'ORÉAL |

L'Oréal Paris, Lancôme, Kiehl's, La Roche-Posay, CeraVe |

Leader |

Market leader; broadest portfolio; recombinant collagen innovation |

|

Estée Lauder Inc |

Estée Lauder, La Mer, Clinique, Origins, Dr. Jart+ |

Leader |

Premium and prestige focus; department store strength; anti-aging lead |

|

Procter & Gamble |

Facial Treatment Essence, LXP range, GenOptics |

Leader |

Japanese luxury; Pitera ingredient; travel retail expansion in Sanya |

|

Amorepacific |

Laneige, Sulwhasoo, Mamonde, Innisfree |

Leader |

K-beauty heritage; Alibaba partnership; technological skincare focus |

|

Jahwa |

Herborist |

Challenger |

Domestic heritage; TCM-inspired formulas; mid-premium positioning |

|

Florasis |

Skincare line |

Challenger |

Digital-native domestic; TCM natural ingredients; Gen Z appeal |

Key players include L'ORÉAL, Estée Lauder Inc, Procter & Gamble, Amorepacific, Jahwa, Florasis, and others.

Key Company Profiles

L'Oréal

L'Oréal is the largest skincare company in China, anchored by L'Oréal Paris, Lancôme, Kiehl's, La Roche-Posay, and CeraVe. The group's Shanghai research center localizes formulations for Chinese skin profiles and pioneers’ biotech launches including recombinant collagen skincare in the anti-aging segment.

- Product Portfolio: Offers cleansers, serums, moisturizers, sunscreens, and anti-aging treatments across mass to luxury tiers.

- Recent Developments: In December 2023, L'Oréal introduced animal-free collagen skincare in China using recombinant technology, launching the Age Perfect Collagen Royal Anti-Aging Face Cream with human-like amino acid sequences.

- Strategic Focus: L'Oréal's strategy leverages biotech-led anti-aging innovation, broad price-tier coverage, and deep retail distribution across Tmall, JD.com, department stores, and specialty chains to maintain market leadership across skincare segments in China.

Estée Lauder Inc.

Estée Lauder operates a premium and prestige portfolio in China anchored by Estée Lauder, La Mer, Clinique, Origins, and Dr. Jart+. The group maintains the country's strongest department store counter presence and prestige travel retail distribution through Sanya and Hainan duty-free channels.

- Product Portfolio: Offers premium and luxury skincare including Advanced Night Repair, Re-Nutriv, and La Mer treatment ranges.

- Recent Developments: In February 2025, Estée Lauder Companies officially introduced its skincare brand The Ordinary into mainland China, marking a major step in its global expansion strategy. The brand made its in-market debut through an exclusive launch with Sephora, bringing a curated selection of products tailored for local regulatory requirements and consumer preferences.

- Strategic Focus: Estée Lauder's strategy differentiates on prestige brand equity, counter-based beauty advisor service, and anti-aging clinical efficacy narrative to command premium pricing across its portfolio in China's luxury skincare segment.

Procter & Gamble

Procter & Gamble offers SK-II, a luxury brand, is one of the most aspirational premium skincare labels in China, anchored by its signature Pitera ingredient derived from yeast fermentation. The brand maintains strong travel retail presence and has expanded flagship experiential retail in Hainan's duty-free zone.

- Product Portfolio: Offers Facial Treatment Essence, LXP range, GenOptics, and other premium age-defying skincare collections.

- Recent Developments: In October 2024, SK-II opened its first travel flagship store in China at Sanya's duty-free complex, featuring multisensory Pitera experiences and interactive art installations.

- Strategic Focus: SK-II's strategy emphasizes Pitera scientific narrative, luxury travel retail expansion, and experiential brand storytelling to sustain its position as a premium Japanese skincare leader in Chinese beauty.

Market Concentration Analysis

The China skincare market is moderately concentrated, with the top five international players holding approximately 35 to 40% combined share and no single company exceeding 12% of total market revenue. International brands lead premium and prestige, while domestic players fragment the mass and natural segments.

Consolidation at the segment level is more advanced than headline concentration suggests. L'Oréal's portfolio dominates derma-cosmetic channels through La Roche-Posay and CeraVe, Estée Lauder anchors luxury department store counters, and Amorepacific leads K-beauty. Domestic consolidation is progressing through Yatsen Group and Shanghai Chicmax acquiring emerging natural labels.

Investment & Growth Opportunities

Fastest-Growing Segments

Online distribution at ~9.2% CAGR through 2034 is the highest-growth channel segment, propelled by livestreaming commerce, AI personalization, and content-driven discovery. Natural ingredients at ~8.9% CAGR represent the fastest-growing ingredient category, driven by TCM heritage narratives and organic beauty preferences among millennial and Gen Z consumers.

Emerging Consumer Segments

The male skincare segment at ~8.6% CAGR is the fastest-growing demographic through 2034, propelled by professional grooming norms in Tier-1 cities, reduced stigma around male beauty, and targeted product launches from L'Oréal Men Expert, Nivea, and domestic male-focused brands capturing working-age consumers aged 22 to 40.

Venture & Investment Trends

Private equity and strategic investor interest in Chinese natural skincare brands is accelerating. Sequoia Capital China, Hillhouse, and GGV have backed domestic D2C skincare platforms leveraging TCM positioning. International strategic buyers including L'Oréal and Unilever pursue bolt-on acquisitions of digitally native Chinese brands to strengthen natural and Gen Z segment portfolios.

Future Market Outlook (2026-2034)

The China skincare market is forecast to expand from USD 54.23 Billion in 2025 to USD 112.37 Billion by 2034 at a CAGR of 7.72%, adding USD 58.14 Billion in incremental annual market value over the forecast period. This sustained growth reflects pollution-driven, demographically-anchored demand characteristics.

Three forces will most significantly shape the China skincare landscape through 2034. Biotech-driven anti-aging innovation, including recombinant collagen and engineered peptides, will anchor premium segment growth. AI personalization will reshape consumer discovery and loyalty. Natural and TCM-inspired formulations will capture cultural preference shifts among Gen Z.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews in 2024-2025 with China skincare industry stakeholders, including brand marketing directors, e-commerce category managers, Tmall and JD.com beauty buyers, dermatology clinic operators, OEM manufacturers in Guangdong, and independent retailers. Primary data validated market sizing, channel shares, ingredient segment estimates, and consumer trend observations.

Secondary Research

Key secondary sources include State Council of the People's Republic of China e-commerce reports, National Bureau of Statistics of China consumer expenditure data, NMPA cosmetic registration databases, CSAR regulatory filings, China Association of Fragrance, Flavor and Cosmetic Industries annual reports, IMARC internal databases, brand annual reports, Tmall Global category data, and trade publications including Jing Daily and BeautyMatter.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, disposable income trends, and historical category evolution. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty.

China Skincare Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Distribution Channels Covered |

|

| Ingredient Types Covered | Natural, Chemical |

| Genders Covered | Male, Female, Unisex |

| Companies Covered | L'ORÉAL, Estée Lauder Inc, Procter & Gamble, Amorepacific, Jahwa, Florasis, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, China skincare market forecasts, and dynamics of the market share from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the China skincare industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the China Skincare Market Report

The China skincare market size was valued at USD 54.23 Billion in 2025.

IMARC estimates the China skincare market to exhibit a CAGR of 7.72% during 2026-2034, reaching USD 112.37 Billion by 2034.

Key factors include rising pollution-driven skin health awareness, e-commerce and livestreaming channel expansion, K-beauty and J-beauty routine adoption, growing male skincare demand, TCM-inspired natural formulation preferences, and biotechnology-led anti-aging innovation.

Offline leads with a 58.6% share in 2025, supported by consumer preference for tactile product testing, expert beauty advisor consultations at counters, and authentication assurance against counterfeit concerns.

Chemical ingredients dominate at 61.7% in 2025, owing to formulation stability, proven efficacy in targeted concerns such as pigmentation and anti-aging, and broad accessibility across mass to luxury price tiers.

Key players include L'ORÉAL, Estée Lauder Inc, Procter & Gamble, Amorepacific, Jahwa, Florasis, and others.

Major challenges include NMPA regulatory compliance complexity, counterfeit product proliferation, raw material cost volatility, and market saturation in Tier-1 cities, requiring brands to expand Tier-2 and Tier-3 distribution and brand protection investments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)