China Warehouse Automation Market Size, Share, Trends and Forecast by Component, End User, and Region, 2026-2034

China Warehouse Automation Market Overview:

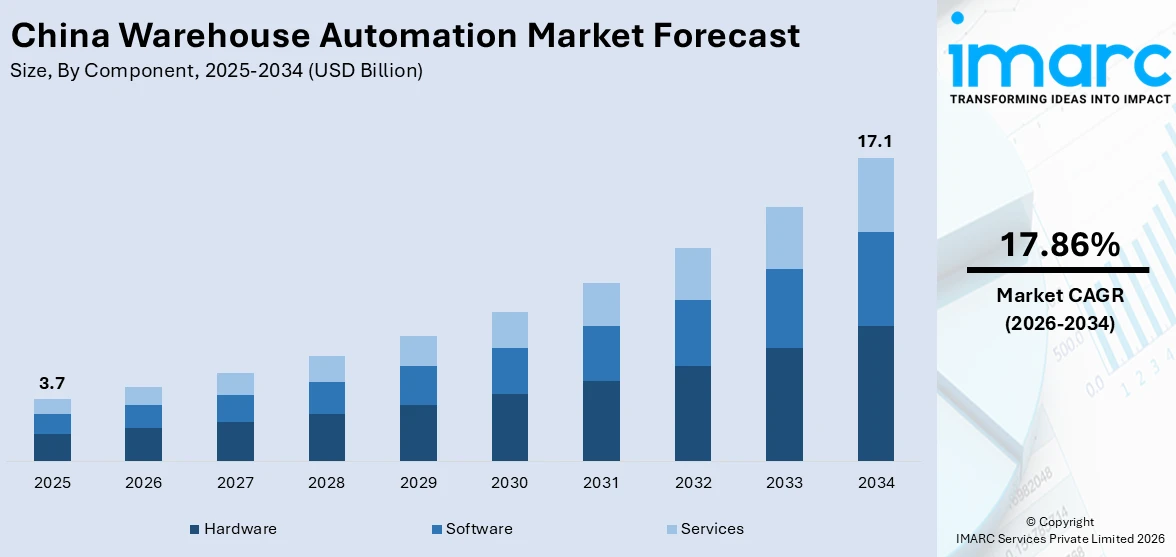

The China warehouse automation market size reached USD 3.7 Billion in 2025. The market is projected to reach USD 17.1 Billion by 2034, exhibiting a growth rate (CAGR) of 17.86% during 2026-2034. The market is growing rapidly, driven by rising labor costs, booming e‑commerce, and increasing demand for speed and efficiency in logistics. Domestic robot and automation producers are expanding their offerings while integrating AI and robotics into warehousing operations. Local supply chains and government incentives are helping lower costs, making automation more accessible for a wider range of businesses. These developments are propelling innovation and wider adoption, influencing China warehouse automation market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 3.7 Billion |

| Market Forecast in 2034 | USD 17.1 Billion |

| Market Growth Rate 2026-2034 | 17.86% |

China Warehouse Automation Market Trends:

Creation of Automated Fulfillment Centers

China is making significant investment into robot-driven fulfillment centers to match the rapid development of e-commerce and the demands of logistics. The centers include advanced technologies such as Automated Storage and Retrieval Systems (ASRS), high-speed sortation machines, and artificial intelligence-driven robots that are focused on enhancing operational efficiency and precision. The government planned in May 2025 to open several smart logistics hubs throughout the nation to allow efficient supply chains and quick delivery services. This is all in the broader national push to modernize the logistics network and provide better overall quality of service. Automation of fundamental warehouse procedures assists companies in reducing the operating cost, improving stock management, and meeting increasing consumer expectations for quicker delivery. Further, these trends help to fill labor shortages by transferring manual labor into automated systems. The ongoing modernization and application of automation solutions in warehouses are major drivers of China warehouse automation market growth, making the country the world leader in the supply chain and logistics sector.

To get more information on this market Request Sample

Integration of Robotics and Artificial Intelligence Technology

Robotics and artificial intelligence (AI) are increasingly becoming integral to warehouse automation in China, revolutionizing traditional logistics operations. AI-based picking systems, autonomous robots, and sorting technology are being used more widely to improve efficiency and accuracy in warehouses. Smart systems enable real-time inventory monitoring, efficient order fulfillment, and resource optimization. China's Ministry of Industry and Information Technology reaffirmed in June 2024 the strategic importance of robotics and artificial intelligence to enhancing the competitiveness of the country in manufacturing and logistics. The government balances this trend with assistance through policies and funding to drive innovation and adoption of advanced automation technologies. Such incorporation also reduces dependency on human manpower and enhances scalability for warehouses handling diverse demand. With enhancements in robotics and artificial intelligence, warehouses become more resilient and agile, adapting quickly to market fluctuations. Those developments are shaping China warehouse automation market trends, driving logistics infrastructure modernization and setting new standards for operational excellence.

Development of Local Robotics Manufacturing

China is emphasizing heavily on the development of its local robotics manufacturing sector to cater to the increasing requirements of warehouse automation. This strategic initiative is intended to eliminate dependence on foreign technologies and stimulate innovation specific to the needs of local markets. Investment in research and development is being incentivized by government policies, with provisions of subsidies, tax benefits, and infrastructure facilitation for robotics companies. Local manufacturers are improving on the production of a variety of automation hardware, such as autonomous mobile robots, robotic arms, and combined warehouse management systems. These technologies are created to be more efficient, lower operational costs, and facilitate easier scalability in warehouses. Development of indigenous robotics expertise also aids in establishing a more robust supply chain ecosystem since companies enjoy quicker innovation cycles and greater proximity to technology providers. This trend toward local production complements wider national goals of technological independence and digitalization. As China continues to value the development of its robotics sector, it is likely to have a profound impact on future warehouse automation trends, facilitating continued industry expansion and competitiveness in foreign markets.

China Warehouse Automation Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on component and end user.

Component Insights:

- Hardware

- Mobile Robots (AGV, AMR)

- Automated Storage and Retrieval Systems (AS/RS)

- Automated Conveyor and Sorting Systems

- De-palletizing/Palletizing Systems

- Automatic Identification and Data Collection (AIDC)

- Piece Picking Robots

- Software

- Warehouse Management Systems (WMS)

- Warehouse Execution Systems (WES)

- Services

- Value Added Services

- Maintenance

The report has provided a detailed breakup and analysis of the market based on the component. This includes hardware (mobile robots (AGV, AMR), automated storage and retrieval systems (AS/RS), automated conveyor and sorting systems, de-palletizing/palletizing systems, automatic identification and data collection (AIDC), and piece picking robots), software (warehouse management systems (WMS) and warehouse execution systems (WES)), and services (value added services and maintenance).

End User Insights:

Access the comprehensive market breakdown Request Sample

- Food and Beverage

- Post and Parcel

- Retail

- Apparel

- Manufacturing

- Others

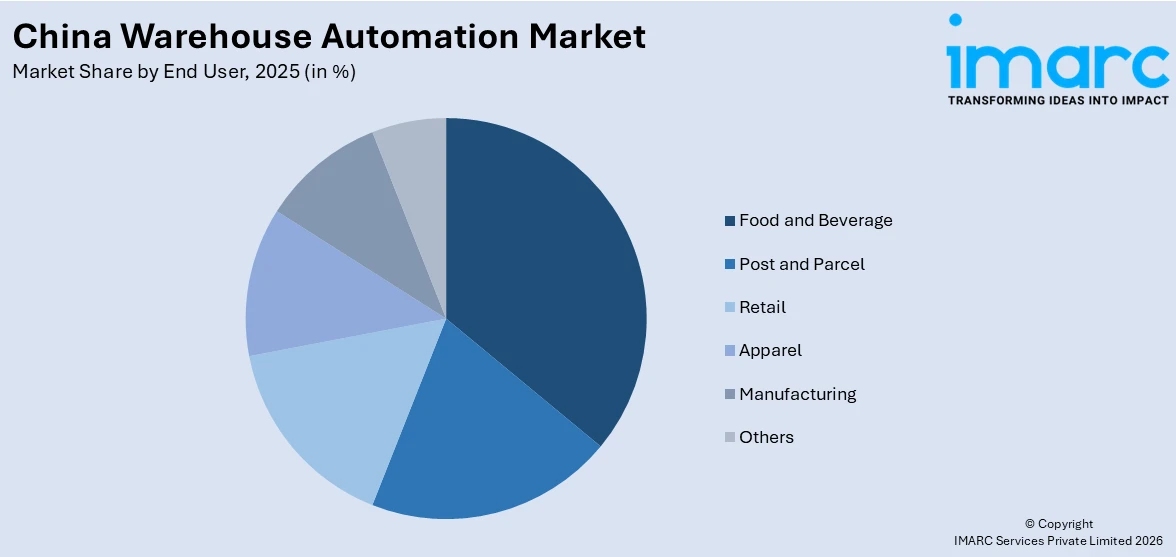

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes food and beverage, post and parcel, retail, apparel, manufacturing, and others.

Regional Insights:

- North China

- East China

- South Central China

- Southwest China

- Northwest China

- Northeast China

The report has also provided a comprehensive analysis of all the major regional markets, which include North China, East China, South Central China, Southwest China, Northwest China, and Northeast China.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

China Warehouse Automation Market News:

- August 2025: KENGIC Intelligent Technology Co., Ltd., a Chinese provider of intelligent logistics and manufacturing solutions, has successfully completed a Smart Automated Storage and Retrieval System (AS/RS) project for CRRC Zhuzhou, a subsidiary of CRRC Corporation Limited. The facility, located in the Dual-carbon Industrial Park, spans over 10,000 storage locations and integrates dual-system synergy between Shuttle Rack Modules (SRMs) and Pallet Four-way Shuttles. This advanced system enhances efficiency and resilience in industrial logistics, meeting the precision demands of rail transit manufacturing.

China Warehouse Automation Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| End Users Covered | Food and Beverage, Post and Parcel, Retail, Apparel, Manufacturing, Others |

| Regions Covered | North China, East China, South Central China, Southwest China, Northwest China, Northeast China |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the China warehouse automation market performed so far and how will it perform in the coming years?

- What is the breakup of the China warehouse automation market on the basis of component?

- What is the breakup of the China warehouse automation market on the basis of end user?

- What is the breakup of the China warehouse automation market on the basis of region?

- What are the various stages in the value chain of the China warehouse automation market?

- What are the key driving factors and challenges in the China warehouse automation market?

- What is the structure of the China warehouse automation market and who are the key players?

- What is the degree of competition in the China warehouse automation market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the China warehouse automation market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the China warehouse automation market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the China warehouse automation industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)