Cogeneration Equipment Market Size, Share, Trends and Forecast by Fuel, Capacity, Technology, Application, and Region, 2026-2034

Cogeneration Equipment Market Size and Share:

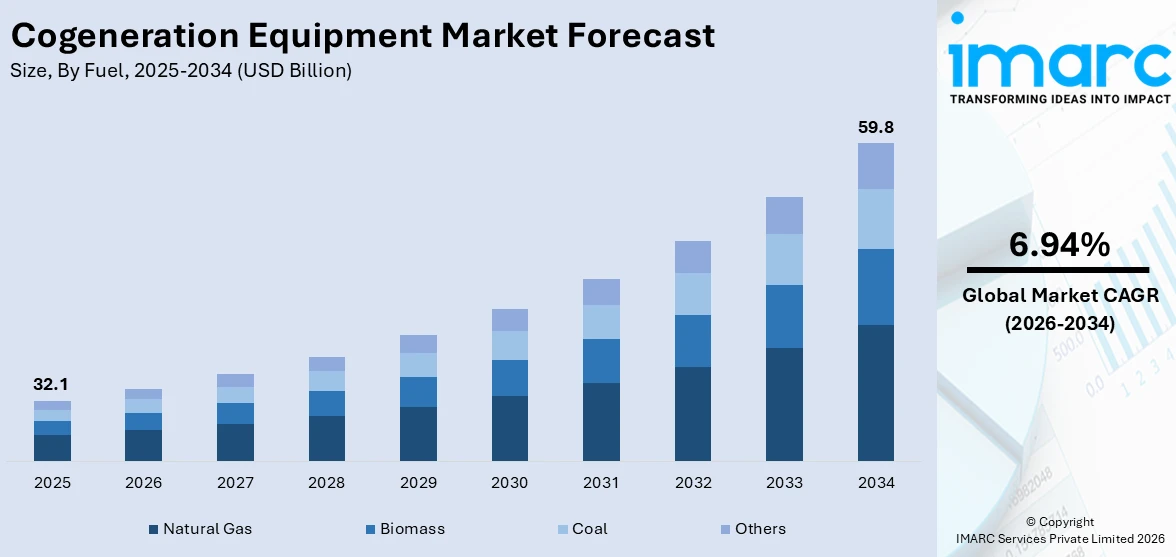

The global cogeneration equipment market size was valued at USD 32.1 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 59.8 Billion by 2034, exhibiting a CAGR of 6.94% during 2026-2034. North America currently dominates the market. The market is growing due to increasing demand for energy efficiency, sustainability, and technological innovations like microturbines, fuel cells, and CHP systems. Government incentives for renewable energy adoption and advancements in IoT for real-time monitoring are driving further market expansion, boosting the cogeneration equipment share across industries.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 32.1 Billion |

| Market Forecast in 2034 | USD 59.8 Billion |

| Market Growth Rate (2026-2034) | 6.94% |

The growing focus on sustainability and minimizing carbon footprints is fueling the expansion of the cogeneration equipment market. Governments and industries are focusing on incorporating renewable energy sources, including biomass, biogas, and even solar, into cogeneration systems. These systems are being made more efficient in terms of using renewable fuels, which is in line with worldwide efforts to achieve environmental standards and reduce greenhouse gas emissions. With nations establishing energy transition targets, companies are inclined towards embracing cleaner energy technology. The continuous development of renewable energy technologies, such as advanced biogas production and enhanced biomass processing, is also rendering cogeneration systems economical and efficient. Accordingly, manufacturing, food processing, and even residential buildings are gradually embracing cogeneration equipment to meet energy needs sustainably. In addition, various governments are providing cash incentives, such as tax rebates and subsidies, to promote the utilization of renewable energy in power generation, thus making these systems affordable.

To get more information on this market Request Sample

The United States is a particularly influential market changer based on the prevalent use of new cogeneration technologies, such as microturbines, fuel cells, and combined heat and power (CHP) equipment. They are increasingly vital to fulfilling energy-efficiency requirements as energy consumption demands continue to escalate, most prominently in industries such as manufacturing, commercial properties, and data centers. As there is a growing demand for sustainability and energy self-sufficiency, the US is benefiting from advanced cogeneration technologies that minimize its carbon footprint while maximizing energy resilience. IoT-powered monitoring systems enable businesses to maximize real-time energy consumption, optimizing the efficiency of cogeneration systems and minimizing wastage. This innovation is especially effective in industrial-scale applications, where exact control over energy usage is paramount. In addition, the US government's leadership in renewable energy and energy efficiency through policies, subsidies, and tax credits also promotes the implementation of such systems.

Cogeneration Equipment Market Trends:

Shift Toward Cleaner and Efficient Energy Solutions

The market is being increasingly driven by the world's move toward cleaner and efficient energy systems. With industries attempting to comply with stringent environmental requirements and save energy, there has been a marked shift away from conventional fossil fuel-based generation. This has prompted strong demand for high-efficiency, integrated cogeneration solutions with the ability to provide both heat and electricity at minimal environmental degradation. One notable development supporting this trend occurred in July 2024, when Kawasaki Heavy Industries received its first Taiwanese order for the L30A 30 MW high-efficiency gas turbine. The turbine will be part of a cogeneration system at Yee Fong Chemical's Taoyuan Plant, where it will replace a current coal-fired steam turbine and boiler. This is part of a wider regional trend, particularly in Asia, towards replacing old infrastructure with new, gas-based systems. The L30A's high efficiency, lower CO₂ emissions, and flexibility for future hydrogen applications make it a leading solution in sustainable industrial processes. Such developments are likely to continue propelling the cogeneration equipment market, particularly in countries dedicated to lowering their carbon footprint while ensuring stable and affordable energy supplies. The trend indicates increasing market demand for equipment that facilitates long-term environmental and economic sustainability.

Adoption of Hydrogen-Compatible Technologies

The adoption of hydrogen-compatible technologies is becoming a defining trend in the cogeneration equipment market. As countries and companies commit to decarbonization, the ability to blend or fully switch to hydrogen in existing systems is becoming a major driver of equipment innovation and investment. Manufacturers and energy providers are increasingly focusing on systems that can support a transition to low-carbon fuels without requiring complete replacement. A clear example of this progress was demonstrated in July 2024 when Yanmar and Daigas Energy successfully evaluated a 400kW EP400G cogeneration system using a 30% hydrogen blend. Conducted at Daigas Energy's Carbon Neutral Research Hub in Osaka, the test confirmed that the unit maintained rated power output, efficiency, and low NOx emissions, even with the hydrogen mixture. The success of this demonstration shows that hydrogen can be introduced into current gas systems through simple retrofits, offering a cost-effective and scalable path toward cleaner energy. This capability is particularly valuable for industrial users seeking future-proof solutions amid evolving regulations and sustainability goals. As hydrogen infrastructure expands globally, cogeneration systems that support hydrogen blending will become increasingly vital, driving sustained market growth and fostering innovation in fuel-flexible, low-emission energy technologies.

Rising Demand for Reliable Power Solutions

The growing energy demand across the globe is the key factor driving the cogeneration equipment market growth. Frequent power outages and growing electricity shortages have led to the advancement of systems designed to provide reliable, continuous, and sustainable power generation and distribution. In 2021 alone, around 350 Million people globally were affected by significant blackouts. Additionally, the expanding use of micro-combined heat and power (micro-CHP) systems across industrial, residential, and SME sectors alongside falling natural gas prices due to its ample availability has driven the demand for such systems. As of 2023, the United States had approximately 33,185,550 small businesses. Government initiatives in both developed and developing countries promoting clean, efficient, and renewable energy are further supporting the market. Technological advancements are also contributing to growth. The emergence of tri- and Quattro-generation technologies, capable of generating three or more types of energy simultaneously, has improved the efficiency of energy conversion processes.

Cogeneration Equipment Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global cogeneration equipment market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on fuel, capacity, technology, and application.

Analysis by Fuel:

- Natural Gas

- Biomass

- Coal

- Others

In 2025, the natural gas segment led the cogeneration equipment market, driven by the increasing focus on cleaner energy sources, lower carbon emissions, and cost-effective fuel options for power and heat generation. Natural gas-based cogeneration systems offer high efficiency, making them a preferred choice over coal and oil alternatives. Industrial and utility sectors adopted these systems for stable energy output and improved operational savings. Government policies supporting low-emission technologies, and the expansion of natural gas infrastructure further encouraged uptake. Additionally, the abundance of natural gas resources and growing energy demand across urban areas created a favorable environment for this segment to maintain leadership in the cogeneration equipment market.

Analysis by Capacity:

- Up to 30 MW

- 31MW -60 MW

- 61 MW- 100 MW

Cogeneration equipment in the up to 30 MW range is typically used for small-scale industrial facilities, commercial buildings, and institutional setups like hospitals or universities. This segment drives market growth due to the increasing adoption of decentralized energy systems, especially in urban areas seeking energy efficiency and reliability. The low initial investment and shorter installation times attract small and medium enterprises (SMEs). Additionally, favorable policies and incentives for clean energy technologies in this capacity bracket make it a key driver in regions with strong environmental regulations. The segment also benefits from rising demand in developing economies for affordable, reliable energy.

The 31 MW – 60 MW range caters to medium-sized industrial operations, such as manufacturing plants, data centers, and district heating networks. These cogeneration systems offer a balanced mix of power and heat generation efficiency, making them a cost-effective solution for industries with continuous power and thermal needs. The segment is driven by growing energy efficiency mandates and sustainability goals across sectors. As energy prices fluctuate, businesses increasingly rely on cogeneration to manage operational costs. Technological advancements in turbine efficiency and digital monitoring systems further support adoption in this range. This segment also sees growth in both retrofits and greenfield projects.

Cogeneration equipment in the 61 MW – 100 MW segment is designed for large-scale industrial complexes, petrochemical plants, and utility providers. This range serves facilities with high and constant energy demands, offering significant fuel savings and emissions reductions. It plays a crucial role in grid stabilization by acting as a distributed generation source. Stringent emission norms, the need for energy security, and aging power infrastructure replacements drive market growth in this range. Additionally, combined cycle technologies and integration with renewable energy systems enhance the efficiency and appeal of this segment. Large investments and longer planning cycles characterize this market tier.

Analysis by Technology:

- Reciprocating Engine

- Steam Turbine

- Combined Cycle Gas Turbine

- Gas Turbine

- Others

In 2025, the reciprocating engine segment led the cogeneration equipment market, driven by its flexibility in handling varied load requirements, quick start-up capabilities, and suitability for small to mid-sized commercial and industrial applications. Reciprocating engines offered an efficient solution for decentralized power generation with lower upfront costs compared to turbines. Their high efficiency at partial loads and minimal maintenance needs made them a preferred choice across facilities requiring reliable energy backup. Supportive regulatory measures promoting efficient generation technologies and increased investments in distributed energy systems contributed to market growth. As organizations sought scalable and adaptable solutions, reciprocating engines remained the most widely adopted technology in the cogeneration equipment market.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Commercial

- Industrial

- Residential

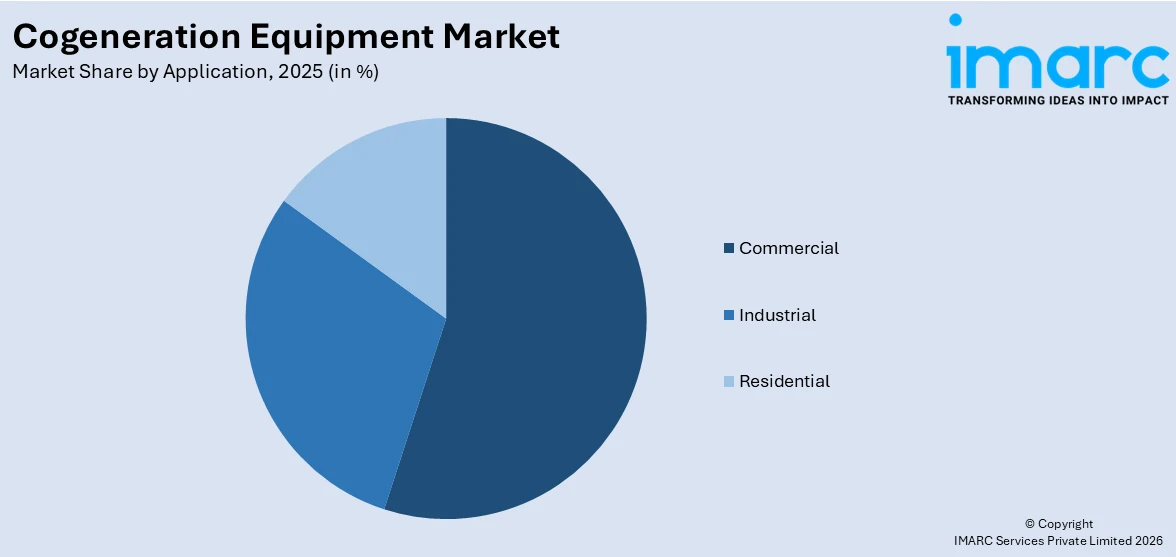

In 2025, the commercial segment led the cogeneration equipment market, driven by rising energy costs, growing emphasis on sustainability, and the need for reliable on-site power in business establishments, hospitals, hotels, and retail complexes. Commercial facilities favored cogeneration systems for their ability to reduce utility bills while ensuring uninterrupted power and heating. Many new commercial buildings integrated cogeneration during design stages, supported by green building norms and government incentives. The growing number of data centers and healthcare facilities also boosted installations. With urban expansion and growing demand for energy efficiency in real estate, the commercial sector played a significant role in shaping adoption trends within the cogeneration equipment market.

Regional Analysis:

- Asia Pacific

- Europe

- North America

- Middle East and Africa

- Latin America

As per cogeneration equipment market outlook, in 2025, the North America led the market, driven by robust investments in clean and efficient energy technologies, along with increasing adoption across industrial and institutional facilities. The region benefited from a well-developed natural gas infrastructure, making cogeneration systems more viable and cost-effective. Federal and state-level programs promoting energy efficiency and emissions reduction supported market growth. Demand from manufacturing plants, universities, and hospitals created strong traction, especially in the U.S. and Canada. Aging power grids and rising electricity prices further pushed businesses toward self-generation options. The combination of favorable regulations, technological advancements, and energy security concerns enabled North America to retain its leading position in the global cogeneration equipment market.

Key Regional Takeaways:

United States Cogeneration Equipment Market Analysis

The demand for cogeneration equipment in the United States is increasing as energy infrastructure expands across various industries. For example, data centers alone are projected to contribute around 44 gigawatts (GW) of additional power demand by 2030, rising from a range of 26–33 GW in 2024 to 60–80 GW by 2030. Efforts to update outdated grid systems, lower transmission losses, and improve on-site energy efficiency are encouraging the integration of cogeneration units. Utilities and businesses are turning to combined heat and power (CHP) systems to strengthen electricity reliability and meet growing consumption needs. The shift toward decentralized energy is further encouraging adoption in areas where dependable and efficient power is essential. Government incentives promoting low-emission technologies and cost-effective energy practices are adding momentum. This convergence of infrastructure modernization, policy support, and rising electricity needs is sustaining the uptake of cogeneration systems across the country.

Asia Pacific Cogeneration Equipment Market Analysis

Cogeneration equipment use is expanding across Asia-Pacific, largely driven by the growing small and medium enterprise (SME) segment. These enterprises are turning to efficient, cost-saving energy systems to manage rising operational loads. High energy demand from SME production units is encouraging the shift toward CHP systems. National policies across the region are pushing SMEs to opt for environmentally friendly power options, and cogeneration fits well with these goals. CHP systems address key concerns of energy reliability and financial savings, increasing their appeal among small businesses. In 2022, electricity generation in Asia-Pacific reached 14,681,495 GWh, marking a 246% jump since 2000. Strong industrial growth and accessible financing schemes are also aiding the transition. As SMEs continue to grow, they remain a major driver for cogeneration adoption in this region.

Europe Cogeneration Equipment Market Analysis

Europe continues to encourage the use of cogeneration systems as part of its strategy for efficient, renewable, and low-emission energy solutions. Eurostat data shows that 45.3% of electricity consumed in the EU in 2023 came from renewable sources, up from 41.2% in 2022. Regional priorities include cutting carbon emissions and achieving energy self-sufficiency, creating favorable conditions for CHP implementation. These systems help optimize fuel use while minimizing waste, making them ideal for Europe’s environmental objectives. Financial incentives and performance-based energy rules are boosting system installations. Industries and urban heating networks are increasingly adopting cogeneration to meet green targets. The development of compact, adaptable CHP units meets Europe’s broad energy needs. With growing demand for localized, clean energy, cogeneration remains a key contributor to the continent’s power strategy.

Latin America Cogeneration Equipment Market Analysis

Interest in cogeneration equipment is rising in Latin America due to a greater reliance on biomass in industrial energy generation. While biomass accounts for only 3% of electricity generation globally, the figure stands at 8.4% in Latin America, representing 5% of the region’s total energy use. Thermal biomass capacity has reached 20.6 GW. The widespread availability of agricultural and forestry byproducts is facilitating the move toward biomass-based CHP systems, reducing dependence on fossil fuels. Companies are using these technologies to boost energy independence and align with sustainable development strategies. With a focus on localized renewable energy, biomass-powered cogeneration is becoming an appealing solution across the region.

Middle East and Africa Cogeneration Equipment Market Analysis

Cogeneration equipment is gaining ground in the Middle East and Africa, driven by commercial and industrial expansion. In the UAE, the Operation 300bn initiative is aimed at strengthening the manufacturing sector and increasing its GDP share from AED 133 Billion to AED 300 Billion by 2031. The push for efficient and cost-effective energy systems is leading to installations in sectors like hospitality, healthcare, and manufacturing. These industries are seeking solutions that offer a continuous power supply and better energy use. As these sectors grow, cogeneration systems are being adopted more widely to support their power and efficiency requirements.

Competitive Landscape:

Ongoing advancements in cogeneration technology, energy delivery methods, and system integration strategies are driving growth in the cogeneration equipment market. Companies in the sector are prioritizing improvements in equipment efficiency, flexibility, and operational reliability to optimize energy output and reduce emissions. Firms compete by offering high-performance, fuel-flexible systems with advanced automation, remote monitoring capabilities, and scalable solutions tailored to diverse industrial and commercial applications. Strategic partnerships, international market expansion, and focused product innovation are accelerating adoption. According to the cogeneration equipment market forecast, demand is expected to rise as industries and utilities emphasize energy efficiency, decentralized generation, and sustainable infrastructure, spurring increased investment in innovation, grid integration, and customer-centric solutions.

The report provides a comprehensive analysis of the competitive landscape in the cogeneration equipment market with detailed profiles of all major companies, including:

- Kawasaki Heavy Industries, Ltd.

- Bosch Group

- Innovative Steam Technologies Inc.

- Kohler Co.

- Mitsubishi Heavy Industries, Ltd.

- Wood PLC (Foster Wheeler AG)

- ANDRITZ AG

- Siemens Aktiengesellschaft

- 2G Energy AG

- ABB Group

- Aegis Energy

- EDF Group

- BDR Thermea Group B.V.

- Baxi Group

- Capstone Turbine Corporation

- Rolls-Royce plc.

Latest News and Developments:

- April 2025: Q8Oils joined COGEN Europe to advance sustainable cogeneration technologies. As a key supplier of high-performance lubricants, including the Jenbacher S Oil 40 developed with INNIO Jenbacher, Q8Oils enhances the efficiency and reliability of cogeneration equipment.

- April 2025: The Odesa City Council allocated UAH 60 Million for the installation of new cogeneration units to ensure the city remains supplied with heat and electricity during blackouts. This decision marks the first phase of a larger project, which will involve the installation of 16 gas-piston cogeneration units with a total capacity of 31.8 MW, contributing to Odesa's autonomous energy supply system.

- February 2025: Ingredion invested over USD 100 Million to enhance efficiency and modernize equipment at its Indianapolis plant, including the installation of an energy cogeneration system. This upgrade aims to support growth in texture solutions while improving sustainability and operational reliability.

- February 2025: Aksa Energy, a Turkish power plant operator, announced plans to build 500 MW cogeneration gas power plants in North Macedonia, valued at USD 1.05 Billion. The plants will generate 4.1 TWh of electricity and 720 GWh of thermal energy annually, with households benefiting from free connections to the gas and heating network.

- January 2025: Catalyst Power expanded its cogeneration services to Connecticut and Massachusetts, targeting businesses with aging heating systems. These modular, on-site systems simultaneously produce electricity and heat, achieving over 90% thermal efficiency by utilizing waste energy. Supported by Inflation Reduction Act tax credits and state policies, the initiative aims to reduce emissions and energy costs for industries like logistics, data centers, and pharmaceuticals.

Cogeneration Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Fuels Covered | Natural Gas, Biomass, Coal, and Others |

| Capacities Covered | Up to 30 MW, 31MW-60 MW, 61 MW-100 MW |

| Technologies Covered | Reciprocating Engine, Steam Turbine, Combined Cycle Gas Turbine, Gas Turbine, and Others |

| Applications Covered | Commercial, Industrial, Residential |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Kawasaki Heavy Industries, Ltd., Bosch Group, Innovative Steam Technologies Inc., Kohler Co., Mitsubishi Heavy Industries, Ltd., Wood PLC (Foster Wheeler AG), ANDRITZ AG, Siemens Aktiengesellschaft, 2G Energy AG, ABB Group, Aegis Energy, EDF Group, BDR Thermea Group B.V., Baxi Group, Capstone Turbine Corporation, and Rolls-Royce plc etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cogeneration equipment market from 2020-2034.

- The cogeneration equipment market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cogeneration equipment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cogeneration Equipment Market Report

The cogeneration equipment market was valued at USD 32.1 Billion in 2025.

The cogeneration equipment market is projected to exhibit a CAGR of 6.94% during 2026-2034, reaching a value of USD 59.8 Billion by 2034.

The cogeneration equipment market is driven by rising energy efficiency demands, strict environmental regulations, cost-saving benefits, and technological advancements. Growing adoption in industrial and commercial sectors, decentralized power generation trends, and supportive government policies further fuel market growth and investment in cleaner, more reliable energy systems.

In 2025, North America dominated the cogeneration equipment market, driven by strong industrial demand, supportive government incentives, and strict environmental regulations. Advancements in energy-efficient technologies and the integration of renewable sources further accelerated adoption, particularly across manufacturing, healthcare, and utility sectors seeking reliable, low-emission power solutions.

Some of the major players in the global cogeneration equipment market include Kawasaki Heavy Industries, Ltd., Bosch Group, Innovative Steam Technologies Inc., Kohler Co., Mitsubishi Heavy Industries, Ltd., Wood PLC (Foster Wheeler AG), ANDRITZ AG, Siemens Aktiengesellschaft, 2G Energy AG, ABB Group, Aegis Energy, EDF Group, BDR Thermea Group B.V., Baxi Group, Capstone Turbine Corporation, Rolls-Royce plc, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade