Cold Storage Construction Market Size, Share, Trends and Forecast by Storage Type, Warehouse Type, End User, and Region, 2026-2034

Cold Storage Construction Market Size and Share:

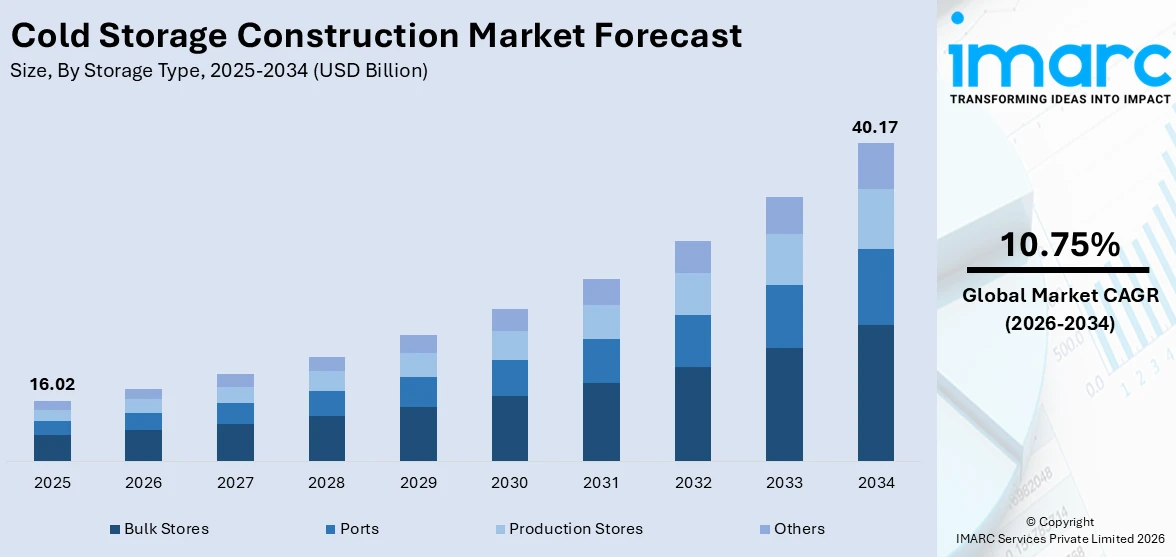

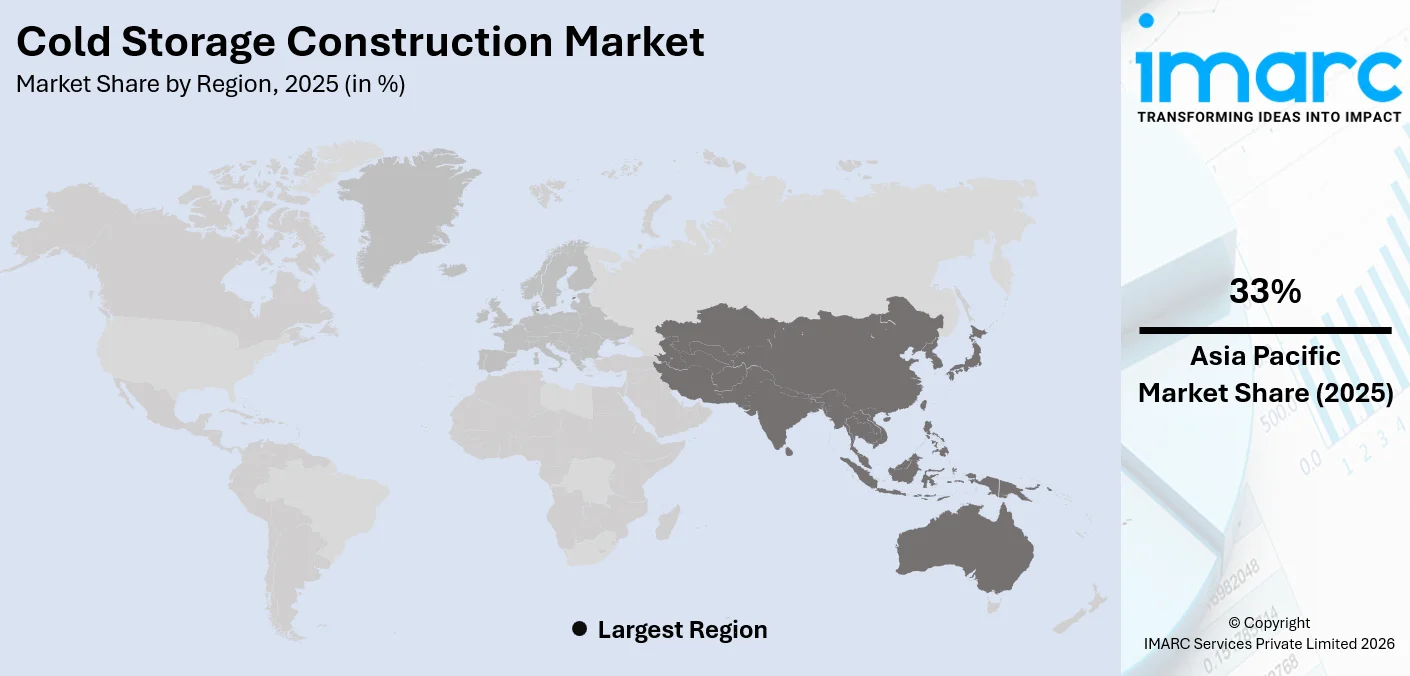

The global cold storage construction market size was valued at USD 16.02 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 40.17 Billion by 2034, exhibiting a CAGR of 10.75% from 2026-2034. Asia Pacific currently dominates the market, holding a market share of 33% in 2025. The region benefits from extensive government investment in cold chain infrastructure, rapid urbanization driving the demand for perishable goods storage. Additionally, robust food processing industry supported by favorable trade policies and rising disposable incomes across major economies is contributing to the expansion of the cold storage construction market share.

The increasing global demand for temperature-controlled storage facilities is a key factor influencing the market. Rising consumption of perishable foods, frozen products, and pharmaceutical items is creating an urgent need for advanced cold chain infrastructure worldwide. The expansion of e-commerce grocery platforms and the growing popularity of online food delivery services are further catalyzing the demand for strategically located refrigerated warehouses near urban centers. Additionally, stringent government regulations concerning food safety and quality standards are encouraging industries to invest in state-of-the-art cold storage systems that ensure compliance and minimize spoilage throughout the supply chain. The growing pharmaceutical sector, particularly the rising demand for biologics, vaccines, and temperature-sensitive medications, is driving additional investment in specialized cold storage facilities equipped with precise temperature control capabilities and advanced monitoring systems to maintain product integrity.

The United States represents a vital region in the cold storage construction market, supported by a robust food processing industry and sustained demand for frozen and fresh food products. Expanding retail distribution networks, the growing e-commerce grocery platforms, and strict food safety standards are encouraging continuous investment in advanced temperature-controlled infrastructure. In 2025, NewCold announced a USD 275 Million investment to develop an automated cold storage warehouse in Hagerstown, Maryland, a project expected to generate between 125 and 150 new jobs while strengthening regional logistics capabilities. The facility’s strategic positioning near the Port of Baltimore is intended to enhance import and export efficiency and support broader supply chain operations. Such large-scale capital commitments reflect ongoing modernization of refrigerated warehousing across the country. Continued expansion of automated, high-capacity facilities is reinforcing the United States’ crucial position in cold storage construction activity.

To get more information on this market Request Sample

Cold Storage Construction Market Trends:

Technological Advancements in Automation and Energy Efficiency

Advancements in warehouse automation, robotics, and energy-efficient refrigeration systems are transforming the cold storage construction landscape. Operators are increasingly adopting automated storage and retrieval systems to maximize space utilization, improve throughput, and reduce labor costs. Energy efficiency measures, including advanced insulation and smart temperature monitoring, help lower operational expenses and environmental impact. The integration of digital control systems enhances performance reliability and compliance with safety standards. These technological improvements are encouraging new facility development and modernization of existing infrastructure, contributing to sustained growth in cold storage construction. In line with this trend, in 2025, NewCold opened its state-of-the-art automated cold storage facility in Nowy Modlin, Poland, with over 95,000 pallet positions. The €112 million investment expanded NewCold's total capacity in Poland to 207,200 pallet positions, strengthening its presence in Central and Eastern Europe. This facility enhanced logistics efficiency with advanced automation, sustainability, and integration with customer systems.

Expansion of Integrated Cold Chain Logistics Networks

Companies are increasingly investing in strategically located facilities that improve distribution efficiency, reduce transportation costs, and support reliable temperature-controlled supply chains for food products and consumer goods. There is a rise in the demand for warehouses equipped with advanced refrigeration systems, rail connectivity, and sustainable operating designs to meet both economic and environmental objectives. For instance, in 2024, CJ Logistics America announced the opening of a 291,000 sq. ft. cold storage warehouse in New Century, Kansas, near Kansas City, developed as a joint venture with Yukon Real Estate Partners and BGO. The facility was designed to serve Upfield’s plant and additional clients, offering rail access and modern refrigeration technology to lower logistics costs and minimize environmental impact. Such developments highlight how integrated infrastructure investments are strengthening cold chain resilience and supporting the cold storage construction market growth.

Rise of Sustainable Multi-Temperature Cold Chain Facilities

The expansion of sustainable, multi-temperature cold chain infrastructure is influencing the market by increasing demand for advanced warehouses that support diverse storage requirements. The rising demand from food distribution, healthcare logistics, and fast-moving consumer goods sectors is driving the need for warehouses that can handle diverse temperature requirements within a single facility. Operators are also prioritizing energy-efficient cooling systems and low-emission designs to meet sustainability targets while reducing operating costs. In 2025, DP World launched a sustainable cold chain facility in Taloja, Navi Mumbai, featuring 11,000 pallet positions across multiple temperature zones within a 110,000 sq. ft. warehouse. The site incorporated advanced cooling technologies to enhance energy efficiency and minimize emissions, supporting DP World’s expanding logistics network across India. Such developments highlight the growing importance of environmentally responsible cold storage solutions in strengthening temperature-sensitive supply chains and offering a favorable cold storage construction market outlook.

Cold Storage Construction Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global cold storage construction market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on storage type, warehouse type, and end user.

Analysis by Storage Type:

- Bulk Stores

- Ports

- Production Stores

- Others

Bulk stores account for 35% of the market share, serving as large-scale facilities designed to accommodate substantial volumes of temperature-sensitive products for extended durations. These facilities play a critical role in supporting seasonal agricultural output, import-export activities, and inventory management for retail and foodservice distribution networks. Their structural design typically includes high clearances and expansive racking systems that optimize storage density while ensuring consistent temperature control across wide floor areas. In 2025, Americold opened a 335,000-square-foot import-export cold storage hub in Kansas City, Missouri, in partnership with Canadian Pacific Kansas City, generating nearly 190 new jobs and strengthening cross-border food trade infrastructure. Such developments demonstrate the importance of centralized bulk storage hubs in facilitating large-scale distribution and international logistics. Continued investment in high-capacity facilities is reinforcing the strategic role of bulk cold storage within global supply chains.

Analysis by Warehouse Type:

- Private and Semi Private Warehouse

- Public Warehouses

Private and semi private warehouse leads the market with a 65% share, reflecting strong demand for dedicated, customized storage solutions. These facilities are designed to meet the specific operational requirements of individual companies or a select group of clients, offering tailored temperature zones, controlled handling processes, and specialized logistics services. Businesses prefer such models to maintain tighter control over inventory management, ensure regulatory compliance, and protect product integrity, particularly in the food and pharmaceutical sectors. In 2025, Interstate Warehousing, a subsidiary of Tippmann Group, expanded its Kingman, Arizona facility by 194,000 square feet, adding 24,000 pallet positions to strengthen dedicated storage capacity. This expansion highlights continued investment in company-specific infrastructure to support long-term supply chain strategies. The cold storage construction market forecast predicts the dominance of private and semi private cold storage facilities owing to the growing emphasis on operational control and reliability.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Food and Beverages

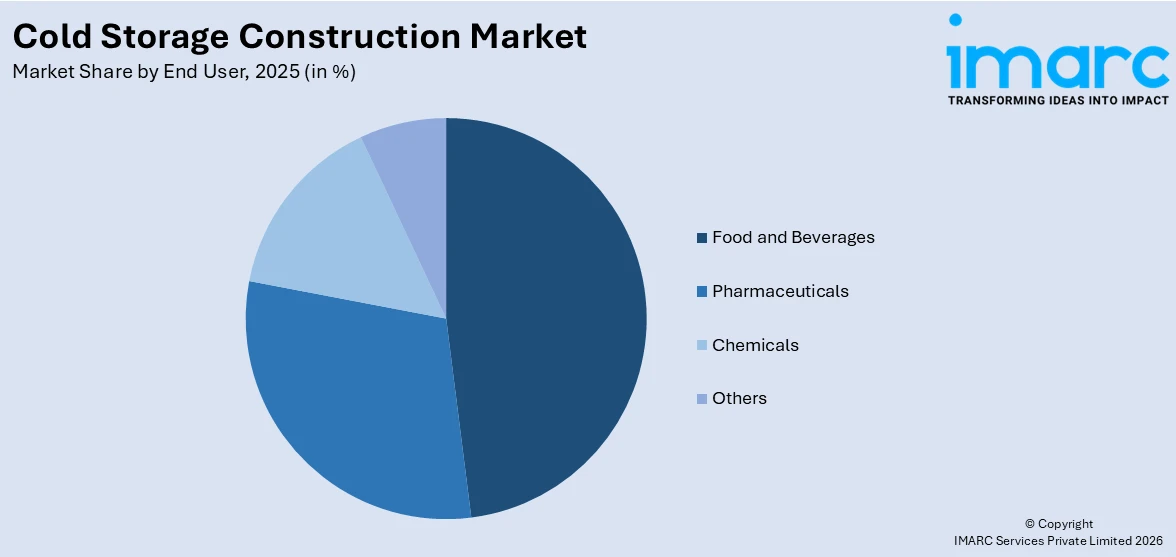

- Pharmaceuticals

- Chemicals

- Others

Food and beverage dominates the market, accounting for 48% of the total share, as the sector requires extensive temperature-controlled infrastructure to maintain product quality, safety, and shelf life throughout distribution networks. The growing consumer demand for fresh produce, frozen meals, dairy products, and ready-to-eat (RTE) items is accelerating investment in advanced facilities equipped with multi-temperature zones and efficient material handling systems. The rapid growth of e-commerce grocery and food delivery services is further increasing the need for strategically located warehouses near major urban centers. In 2025, Vertical Cold Storage opened a new facility exceeding 311,000 sq. ft. in Kansas City, Missouri, offering 47,000 pallet positions dedicated to temperature-controlled food and beverage distribution. The site leverages advanced technology and proximity to key transport hubs to optimize logistics operations. Such large-scale developments underscore the sector’s critical role in driving global cold storage expansion.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia-Pacific, accounting for 33% of the market share, holds a leading position in cold storage construction, supported by rapid urbanization, expanding middle-class populations, and increasing consumption of perishable and frozen food products. Rising disposable incomes and changing dietary preferences are strengthening the demand for organized retail and efficient cold chain networks across major economies. In 2024, Indicold launched India’s first rack-clad Automated Storage and Retrieval System (ASRS) frozen facility in Ahmedabad, offering a capacity of more than 7,000 pallets as part of a broader expansion plan that includes an additional 30,000 pallets in the following year. This project reflects significant investment in automation and high-density storage solutions to meet growing domestic and export requirements. Continued deployment of technologically advanced facilities is reinforcing Asia-Pacific’s leadership in modern cold chain development and large-scale refrigerated warehousing capacity.

Key Regional Takeaways:

United States Cold Storage Construction Market Analysis

The United States remains a pivotal market for cold storage construction, supported by strong demand from the F&B industry, pharmaceutical distribution, and rapidly expanding e-commerce grocery channels. The country’s well-established logistics infrastructure, strict food safety compliance requirements, and high adoption of automation technologies continue to encourage investment in modern temperature-controlled warehousing. The growing consumer preference for fresh, frozen, and RTE products is further driving the need for strategically located cold chain facilities near major transportation hubs. In this context, in 2024, Agile Cold Storage began construction of a 200,000 sq. ft. cold storage warehouse in Joliet, Illinois, scheduled to open in March 2025. The facility was designed to support Midwest distribution with proximity to key intermodal yards and aimed to provide specialized services, including case picking, blast freezing, and import/export handling. This project represents Agile’s first Midwest location and strengthens its broader North American cold storage footprint. Such developments underscore the continued expansion of large-scale cold storage capacity across the United States.

Europe Cold Storage Construction Market Analysis

Europe represents a significant market for cold storage construction, supported by stringent regulatory standards, widespread adoption of advanced technologies, and rising demand for temperature-controlled logistics across food and pharmaceutical supply chains. Strict compliance requirements related to food safety and product traceability are encouraging investments in modern, automated facilities that improve operational efficiency and reduce energy usage. In 2025, Magnavale commenced construction of its fully automated cold store, Magnavale Bristol, in Southwest England, designed to accommodate 90,000 pallets and strengthen regional food supply chain infrastructure. The facility incorporated advanced automation systems and modern refrigeration technologies to enhance storage efficiency and reliability for both existing and new clients. Such projects reflect Europe’s commitment to upgrading cold chain capacity with high-performance infrastructure. These developments are shaping cold storage construction market trends by accelerating the adoption of large-scale automated facilities that prioritize efficiency, compliance, and long-term supply chain resilience across Europe.

Asia-Pacific Cold Storage Construction Market Analysis

Asia-Pacific leads the cold storage construction market, supported by rapid economic growth, accelerating urbanization, and expanding food processing industries across major markets. Rising consumption of perishable goods and increasing organized retail penetration are strengthening the demand for advanced, automated warehousing solutions. In 2025, Indicold launched its second fully automated frozen ASRS facility in Detroj, Gujarat, offering a capacity of 10,000 pallets and incorporating energy-efficient systems with real-time traceability features. This development builds on the company’s earlier automation initiatives and reflects the region’s focus on modernizing cold chain infrastructure. Continued investments in high-capacity, technology-driven facilities are reinforcing Asia-Pacific’s leadership in cold storage expansion.

Latin America Cold Storage Construction Market Analysis

Latin America is experiencing higher investment in cold storage construction, supported by the expansion of food processing industries, rising agricultural export activity, and increasing consumer demand for fresh and frozen products. Strengthening temperature-controlled logistics networks is becoming essential to reduce food waste and improve supply chain efficiency. In 2025, Emergent Cold LatAm opened its first greenfield cold storage facility in Monterrey, Mexico, with a capacity of 23,000 pallets, aimed at supporting regional food producers and retailers. Such projects highlight the region’s accelerating development of modern cold chain infrastructure.

Middle East and Africa Cold Storage Construction Market Analysis

The Middle East and Africa region is witnessing accelerating investment in cold storage construction, supported by government-led modernization programs, rising food import volumes, and expanding pharmaceutical distribution networks. The growing urban populations and higher consumption of perishable goods are increasing the need for advanced temperature-controlled logistics infrastructure. In 2025, Thomsun Mercantile & Marine launched a state-of-the-art cold storage facility in Jebel Ali Free Zone, expanding its total storage capacity to 120,000 cubic meters with mobile racking for frozen storage and multi-tier temperature-controlled systems. Such developments are strengthening regional supply chain resilience and enhancing integrated logistics capabilities.

Competitive Landscape:

The global cold storage construction market is characterized by the presence of several established players and emerging companies competing through technological innovation, strategic partnerships, and capacity expansion. Key market participants are focusing on developing next-generation automated facilities that incorporate advanced refrigeration systems, IoT-enabled monitoring platforms, and sustainable building practices to differentiate their offerings. Strategic acquisitions and consolidation activities are reshaping the competitive dynamics as leading operators seek to expand their geographic footprint and service capabilities. Companies are increasingly investing in proprietary technologies, including automated storage and retrieval systems, digital twin modeling, and predictive analytics platforms, to enhance operational efficiency and attract long-term clients. The emphasis on energy-efficient construction and compliance with evolving environmental regulations is becoming a critical competitive differentiator in the market.

The report provides a comprehensive analysis of the competitive landscape in the cold storage construction market with detailed profiles of all major companies, including:

- Americold Realty Trust Inc.

- Burris Logistics

- Emergent Cold LatAm Management LLC

- Hansen Cold Storage Construction

- Lineage Logistics Holdings LLC

- NewCold B.V.

- Primus Builders Inc.

- RSA Global DWC-LLC

- Tippmann Group

Latest News and Developments:

- In February 2026, Tokyo Tatemono and Mitsui & Co. Urban Development begin constructing the T-LOGI Funabashi Nankai-jin cold storage facility in Funabashi City, Chiba. The multi-tenant, four-story warehouse will feature temperature-variable spaces for frozen, chilled, and fresh goods, and is expected to open by October 2027. The project targets energy efficiency with natural refrigerants and rooftop solar panels.

- In July 2025, Ti Cold and Karis Cold break ground on a USD 60 million cold storage facility in Darien, McIntosh County, Georgia. The facility featured 30,000 pallet positions and environmentally-friendly refrigeration. This marks a major economic development for the region, supporting the state’s logistics industry.

Cold Storage Construction Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Storage Types Covered | Bulk Stores, Ports, Production Stores, Others |

| Warehouse Types Covered | Private and Semi Private Warehouse, Public Warehouses |

| End Users Covered | Food and Beverages, Pharmaceuticals, Chemicals, Others |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Americold Realty Trust Inc., Burris Logistics, Emergent Cold LatAm Management LLC, Hansen Cold Storage Construction, Lineage Logistics Holdings LLC, NewCold B.V., Primus Builders Inc., RSA Global DWC-LLC, Tippmann Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cold storage construction market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global cold storage construction market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cold storage construction industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Cold Storage Construction Market Report

The cold storage construction market was valued at USD 16.02 Billion in 2025.

The cold storage construction market is projected to exhibit a CAGR of 10.75% during 2026-2034, reaching a value of USD 40.17 Billion by 2034.

The cold storage construction market is driven by automation and energy-efficient technologies, expansion of integrated logistics networks, and development of sustainable multi-temperature facilities. Advanced automated warehouses improve storage density and efficiency, strategically located hubs enhance distribution connectivity, and environmentally responsible cooling systems reduce emissions while supporting diverse temperature requirements across food and healthcare supply chains.

Asia-Pacific dominates the cold storage construction market, accounting for a share of 33%. The region's leadership is supported by extensive government investment in cold chain modernization, rapid urbanization driving the demand for perishable goods storage, and expanding food processing industries across China, India, and Southeast Asian nations.

Some of the major players in the cold storage construction market include Americold Realty Trust Inc., Burris Logistics, Emergent Cold LatAm Management LLC, Hansen Cold Storage Construction, Lineage Logistics Holdings LLC, NewCold B.V., Primus Builders Inc., RSA Global DWC-LLC, Tippmann Group, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)