Colonoscopy Devices Market Report by Product Type (Colonoscope, Visualization Systems, and Others), Application (Colorectal Cancer, Lynch Syndrome, Ulcerative Colitis, Crohn’s Disease, and Others), End User (Hospitals, Ambulatory Surgery Center, and Others), and Region 2026-2034

Colonoscopy Devices Market Size:

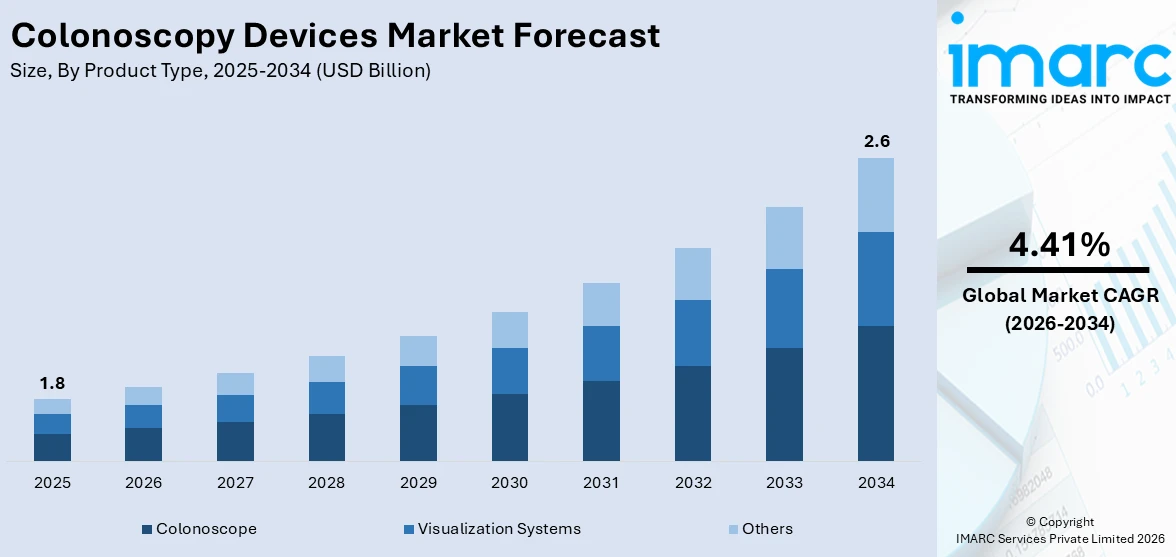

The global colonoscopy devices market size reached USD 1.8 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 2.6 Billion by 2034, exhibiting a growth rate (CAGR) of 4.41% during 2026-2034. The technological advancements in devices, increased awareness and emphasis on preventive healthcare, governmental colorectal cancer screening initiatives, development of cost-effective devices, rising healthcare expenditure, burgeoning per capita income, and expanding healthcare insurance coverage are some of the factors stimulating the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 1.8 Billion |

|

Market Forecast in 2034

|

USD 2.6 Billion |

| Market Growth Rate 2026-2034 | 4.41% |

Colonoscopy Devices Market Analysis:

- Market Growth and Size: The global market for colonoscopy devices is experiencing significant growth, largely driven by the increasing prevalence of colorectal cancer and the growing emphasis on early detection and preventive healthcare. Advancements in colonoscopy technology, along with rising awareness about colorectal cancer screening, are key factors contributing to this expansion.

- Major Market Drivers: The colonoscopy devices market is propelled by several key drivers, including increasing awareness and screening programs, advancements in device technology offering more accurate and less invasive procedures, and a growing elderly population more susceptible to colon diseases. Additionally, increased healthcare expenditure, government initiatives for cancer screening, a shifting preference for minimally invasive (MI) procedures, and a rise in lifestyle-related gastrointestinal disorders are collectively contributing to the dynamic market growth.

- Technological Advancements: Technological advancements in the colonoscopy devices market are revolutionizing diagnostic and therapeutic procedures. Innovations include high-definition video colonoscopes for enhanced imaging, AI integration for improved polyp detection, and developments in endoscopic accessories like biopsy forceps and snares. Miniaturization of devices and advancements in sedation methods are making procedures more comfortable for patients. Additionally, disposable colonoscope developments address concerns regarding cross-contamination.

- Industry Applications: Colonoscopy devices find extensive applications in various healthcare settings, including hospitals, specialized clinics, and ambulatory surgical centers. In hospitals, they are primarily used for diagnostic procedures, cancer screenings, and therapeutic interventions like polyp removal. Specialized clinics often use these devices for routine screenings and follow-up examinations. Ambulatory surgical centers are increasingly adopting colonoscopy devices for outpatient procedures, owing to their convenience and cost-effectiveness. The versatility of these devices in addressing both diagnostic and therapeutic needs across different medical environments underscores their integral role in the healthcare industry.

- Key Market Trends: The increasing adoption of artificial intelligence (AI) and machine learning (ML) for enhanced diagnosis, a shift towards disposable and capsule endoscopes for improved safety, and growing demand for painless and non-invasive procedures are some of the key market trends. In line with this, the integration of advanced imaging techniques for better visualization, the trend towards personalized medicine, the development of self-navigating colonoscopes, and the increasing use of telehealth for consultations post-procedure are other notable trends shaping the market.

- Geographical Trends: North America leads the colonoscopy devices market, attributed to its advanced healthcare infrastructure, high awareness levels about colorectal cancer screening, and strong presence of leading market players. The region's market dominance is further bolstered by favorable reimbursement policies and government initiatives promoting regular screening. Europe follows closely, driven by similar factors. However, Asia-Pacific is emerging as a fast-growing market, due to increasing healthcare expenditure, rising awareness about colon cancer, and improving healthcare facilities, particularly in countries like China and India.

- Competitive Landscape: The competitive landscape of the colonoscopy devices market is characterized by the presence of both established players and emerging competitors. Key players are engaged in strategic partnerships, mergers, and acquisitions to expand their product portfolios and geographic reach. There is also a significant focus on research and development (R&D) to introduce innovative products that offer enhanced efficacy and patient comfort. The market is witnessing an increase in collaboration between companies and healthcare providers to improve product adoption and market penetration.

- Challenges and Opportunities: The colonoscopy devices market faces challenges like high procedure costs, risks associated with colonoscopy procedures, and a shortage of skilled professionals. However, these challenges present opportunities for market growth. There is significant potential for the development of cost-effective and safer devices. The increasing focus on training and education for healthcare professionals offers opportunities for market expansion. Moreover, the rising demand in emerging economies presents significant opportunities for market players to expand their geographical presence and cater to a wider range of audiences.

To get more information on this market Request Sample

Colonoscopy Devices Market Trends:

Rising prevalence of colorectal cancer

Colorectal cancer, a significant public health concern, has been witnessing a steady increase in incidence worldwide. This uptick is attributed to factors such as aging populations, lifestyle changes, and genetic predispositions. As a result, there is a heightened need for early detection and screening, making colonoscopy procedures essential. Colonoscopy, being the most effective method for colorectal cancer screening, plays a crucial role in early diagnosis, directly impacting patient outcomes. The surge in colorectal cancer cases globally is a primary driver for the demand for colonoscopy devices, as healthcare systems emphasize preventive care and early intervention to reduce cancer-related morbidity and mortality.

Technological advancements in colonoscopy devices

The field of colonoscopy devices has seen significant technological advancements, substantially improving diagnostic accuracy and patient comfort. Modern devices feature high-definition imaging and enhanced optical systems, offering clearer and more detailed visualizations of the colon, which is pivotal for detecting abnormalities like polyps. Innovations such as capsule colonoscopy and virtual colonoscopy utilize advanced imaging techniques, providing non-invasive alternatives to traditional methods. Furthermore, developments in sedation techniques and pain management have made the procedure more comfortable for patients, leading to increased acceptance and compliance with screening recommendations.

Escalating aging population

An aging population is a significant driver of the colonoscopy devices market. Older individuals are at a higher risk of developing gastrointestinal diseases, including colorectal cancer. As the global population ages, particularly in developed countries, there is an increasing demand for colonoscopy procedures. This demographic shift is due to longer life expectancies and the aging of large population cohorts, such as the baby boomer generation. With age being a critical risk factor for colorectal cancer, regular screenings via colonoscopy become vital for early detection and treatment. Consequently, the growing number of elderly individuals globally necessitates a corresponding increase in colonoscopy services and devices, making it a key factor in the market's expansion.

Growing awareness and emphasis on preventive healthcare

In recent years, there has been a significant shift towards preventive healthcare, with increased public awareness and education about the importance of early detection of diseases. This shift is particularly evident in the context of colorectal cancer, where regular screenings can significantly reduce mortality rates. Public health campaigns, educational initiatives by healthcare providers, and government programs have played a pivotal role in raising awareness about the benefits of regular colonoscopy screenings. This heightened awareness has led to an increase in the number of individuals undergoing preventive colonoscopies, thereby driving the demand for colonoscopy devices. The emphasis on preventive healthcare not only helps in the early detection of colorectal conditions but also aids in reducing healthcare costs in the long run by avoiding the need for extensive treatments for advanced diseases.

Colonoscopy Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product type, application, and end user.

Breakup by Product Type:

- Colonoscope

- Visualization Systems

- Others

Colonoscope accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the product type. This includes colonoscope, visualization systems, and others. According to the report, colonoscope represented the largest segment.

The colonoscope segment is driven by the increasing demand for advanced and efficient screening tools. Innovations in colonoscope design, such as enhanced imaging quality, flexibility, and user-friendliness, are central to this segment's growth. The development of features like narrow-band imaging and high-definition video enhances the detection of polyps and early-stage cancer, making these devices indispensable in diagnostics. Additionally, the rising incidence of colorectal diseases and the global shift towards minimally invasive procedures contribute significantly to the demand for advanced colonoscopes.

The visualization systems segment is driven by the increasing need for high-accuracy diagnostic tools in colorectal cancer screening. The integration of artificial intelligence (AI) and machine learning (ML) for improved image analysis and decision support further elevates the importance of these systems. Moreover, the growing preference for technologically advanced equipment in healthcare facilities worldwide bolsters the demand for sophisticated visualization systems in colonoscopy procedures.

The others segment, encompassing various accessories and ancillary equipment used in colonoscopy, is driven by the increasing complexity and requirements of colonoscopy procedures. Furthermore, the rising number of colonoscopy procedures performed globally due to growing awareness and preventive healthcare measures substantially fuels the demand for these ancillary products.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Colorectal Cancer

- Lynch Syndrome

- Ulcerative Colitis

- Crohn’s Disease

- Others

Colorectal cancer accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the application. This includes colorectal cancer, lynch syndrome, ulcerative colitis, Crohn’s disease, and others. According to the report, colorectal cancer represented the largest segment.

The colorectal cancer segment is driven by the increasing prevalence of the disease, attributed to factors such as aging populations, sedentary lifestyles, and dietary habits. Advances in screening techniques and heightened public awareness about early detection also contribute to this segment's growth. Additionally, genetic predispositions and increased research into colorectal cancer biomarkers further stimulate demand for diagnostic and treatment options.

The Lynch syndrome segment is driven by the increasing awareness and understanding of genetic risk factors in colorectal cancer. The development of genetic testing and counseling services has significantly contributed to identifying individuals at risk. Additionally, family history as a critical determinant has led to more proactive screenings. Ongoing research and education about Lynch syndrome's implications in colorectal cancer also play a vital role in driving this segment.

The ulcerative colitis segment is driven by the increasing incidence of autoimmune disorders and the chronic nature of the disease, necessitating ongoing management and treatment. Advances in medical therapies and a better understanding of the disease's pathophysiology have led to more effective treatment approaches. Additionally, patient advocacy and awareness initiatives contribute to early diagnosis and treatment, fueling the growth of this market segment.

The Crohn’s disease segment is driven by the rising global incidence of the disease, particularly in industrialized nations. Improved diagnostic methods and a greater understanding of environmental factors have contributed to this increase. The chronic and recurring nature of Crohn’s disease requires continuous medical attention, driving demand for effective treatment solutions.

The others segment, encompassing various gastrointestinal conditions, is driven by the broad spectrum of diseases affecting the digestive tract. Increasing research into these conditions, coupled with advancements in diagnostic and therapeutic modalities, contributes to the growth of this segment.

Breakup by End User:

- Hospitals

- Ambulatory Surgery Center

- Others

Hospitals accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the end user. This includes hospitals, ambulatory surgery center, and others. According to the report, hospitals represented the largest segment.

The hospitals segment is driven by the increasing prevalence of gastrointestinal diseases, the need for advanced medical facilities, and government funding in healthcare infrastructure. Hospitals are often the primary choice for complex medical procedures due to their comprehensive services and advanced technology. The availability of specialized gastroenterologists and state-of-the-art equipment in hospitals makes them ideal for performing colonoscopies, which require skilled handling and precision. Moreover, the growing investments by governments and private entities in hospital infrastructure, particularly in developing countries, enhance their capacity to offer advanced medical procedures, including colonoscopies.

The ambulatory surgery center (ASC) segment is driven by the increasing demand for cost-effective, efficient, and patient-centric healthcare services. ASCs offer a convenient and less expensive alternative to hospitals for outpatient procedures, including colonoscopies. The shift towards minimally invasive procedures, which require shorter recovery times and can be effectively performed in ASCs, contributes significantly to this segment's growth. Additionally, the patient preference for same-day surgical care due to its convenience, coupled with the high-quality care provided at these centers, bolsters the segment growth.

The others segment in the colonoscopy devices market is driven by the increasing utilization of these devices in clinics, diagnostic centers, and nursing homes. This segment benefits from the growing trend of decentralized healthcare, where patients seek services closer to home and in more personalized settings. Furthermore, the increasing preference for community-based healthcare settings, where patients can receive care in a familiar and less intimidating environment, supports the demand for colonoscopy devices in these alternative medical settings.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest colonoscopy devices market share

North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America’s colonoscopy devices market is driven by the increasing prevalence of colorectal cancer, heightened awareness about early detection, and advanced healthcare infrastructure. The presence of leading medical device manufacturers, coupled with significant investments in research and development (R&D), accelerates technological innovation in colonoscopy devices. Additionally, strong governmental support for cancer screening programs and favorable reimbursement policies further stimulates the market growth in this region.

Europe’s colonoscopy devices market is driven by the increasing demand for early cancer detection, an aging population, and robust healthcare systems. Enhanced public healthcare initiatives, combined with high healthcare expenditure, contribute to the growth of the colonoscopy devices market. Additionally, Europe's emphasis on research and development in medical technology, and the presence of key market players, play a vital role in driving innovation and adoption of advanced colonoscopy devices.

The Asia Pacific region is driven by the increasing healthcare awareness, rising incidences of gastrointestinal diseases, and growing healthcare infrastructure. Economic development in countries like China and India has led to increased healthcare expenditure and improved access to healthcare facilities. The region's focus on adopting advanced healthcare technologies, along with a growing middle-class population demanding better healthcare services, significantly boosts the colonoscopy devices market.

Latin America’s market is driven by the increasing prevalence of colorectal diseases, growing public health initiatives, and improving healthcare infrastructure. The rising awareness about the importance of early cancer screening, coupled with increasing healthcare investments in countries like Brazil and Mexico, supports market growth.

The Middle East and Africa colonoscopy devices market is driven by the increasing awareness of colorectal cancer, growing healthcare expenditure, and the development of healthcare infrastructure. The region is witnessing a rise in medical tourism, which demands advanced medical facilities, including colonoscopy services.

Leading Key Players in the Colonoscopy Devices Industry:

In the colonoscopy devices market, key players are actively engaging in a variety of strategic initiatives to strengthen their market position. These include substantial investments in R&D to innovate and improve the functionality and safety of colonoscopy devices, ensuring they are less invasive and more patient friendly. They are also focusing on integrating advanced technologies like AI and ML to enhance diagnostic accuracy and efficiency. Partnerships, collaborations, and mergers with other healthcare companies are common strategies to expand their product portfolio and geographic reach. Furthermore, these companies are actively involved in educational and marketing efforts to raise awareness about colorectal cancer and the importance of early screening. This not only broadens their market base but also contributes to public health initiatives. Additionally, seeking regulatory approvals for new and advanced products in different regions to comply with local health regulations is a key part of their strategy, ensuring a global presence and adherence to medical standards.

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Endomed Systems GmbH

- FUJIFILM Holdings Corporation

- GI-View Ltd.

- HOYA Corporation

- KARL STORZ SE & Co. KG

- Medtronic plc

- Olympus Corporation

- STERIS Corporation

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Latest News:

- In April 2021: FUJIFILM announced the launch of the "ELUXEO® 7000" endoscopy system. The system incorporates advanced image-enhancing technologies, improving the visualization of gastrointestinal tract abnormalities during colonoscopy.

- In October 2021: Medtronic unveiled its "PillCam™ COLON 2" capsule endoscopy system. The device offers a non-invasive alternative to traditional colonoscopy, allowing for the visualization of the colon through a swallowed capsule.

- In January 2022: STERIS Corporation introduced the "Celerity™ GI Endoscope Reprocessing System." It provides high-level disinfection and reprocessing of gastrointestinal endoscopes, addressing the crucial aspect of infection control in the field of colonoscopy.

Colonoscopy Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Colonoscope, Visualization Systems, Others |

| Applications Covered | Colorectal Cancer, Lynch Syndrome, Ulcerative Colitis, Crohn’s Disease, Others |

| End Users Covered | Hospitals, Ambulatory Surgery Center, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Endomed Systems GmbH, FUJIFILM Holdings Corporation, GI-View Ltd., HOYA Corporation, KARL STORZ SE & Co. KG, Medtronic plc, Olympus Corporation, STERIS Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the colonoscopy devices market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global colonoscopy devices market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the colonoscopy devices industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Colonoscopy Devices Market Report

The global colonoscopy devices market was valued at USD 1.8 Billion in 2025.

We expect the global colonoscopy devices market to exhibit a CAGR of 4.41% during 2026-2034.

The rising prevalence of various rectal and chronic disorders, such as cancer, Crohn’s disease, and ulcerative colitis, along with the increasing utilization of colonoscopy devices by practitioners to identify inflammatory bowel and gastrointestinal hemorrhage ailments, is primarily driving the global colonoscopy devices market.

The sudden outbreak of the COVID-19 pandemic had led to the postponement of elective treatment procedures for colorectal cancer, lynch syndrome, and ulcerative colitis to reduce the risk of the coronavirus infection upon hospital visits and interaction with medical equipment, thereby negatively impacting the global market for colonoscopy devices.

Based on the product type, the global colonoscopy devices market can be divided into colonoscope, visualization systems, and others. Currently, colonoscope holds the largest market share.

Based on the application, the global colonoscopy devices market has been categorized into colorectal cancer, lynch syndrome, ulcerative colitis, Crohn’s disease, and others. Among these, colorectal cancer currently accounts for the majority of the global market share.

Based on the end user, the global colonoscopy devices market can be bifurcated into hospitals, ambulatory, surgery center, and others. Currently, hospitals exhibit a clear dominance in the market.

On a regional level, the market has been classified into North America, Europe, Asia Pacific, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global colonoscopy devices market include Endomed Systems GmbH, FUJIFILM Holdings Corporation, GI-View Ltd., HOYA Corporation, KARL STORZ SE & Co. KG, Medtronic plc, Olympus Corporation, STERIS Corporation, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)