Command and Control System Market Size, Share, Trends and Forecast by Platform, Solution, Application, and Region, 2026-2034

Command and Control System Market Size and Share:

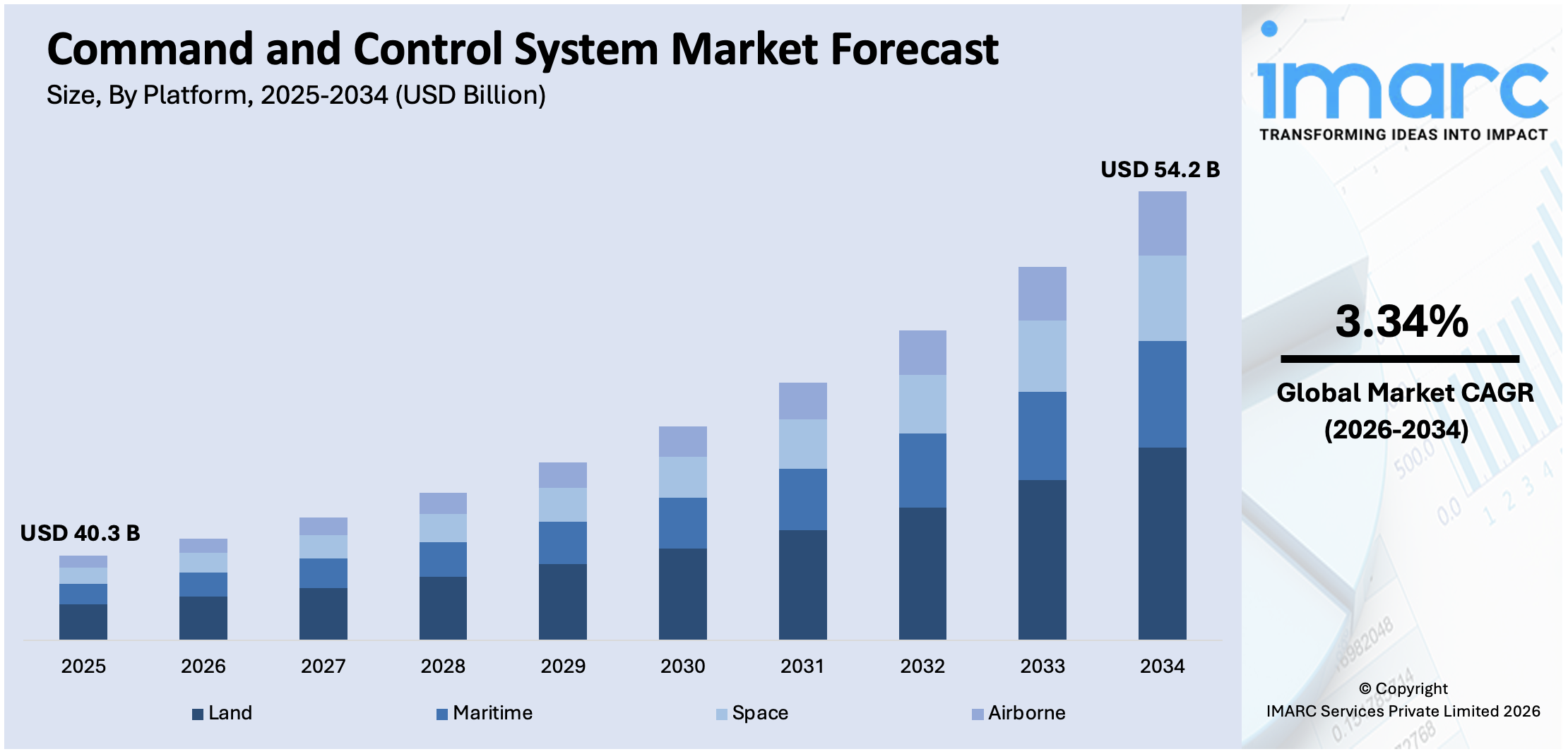

The global command and control system market size was valued at USD 40.3 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 54.2 Billion by 2034, exhibiting a CAGR of 3.34% from 2026-2034. North America currently dominates the market, holding a market share of over 41.7% in 2025. The growing demand for advanced data integration and analytics capabilities, the rising number of security threats, such as cyber threats and terrorism, and the increasing integration of advanced technologies in systems are some of the major factors propelling the market growth in this region.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 40.3 Billion |

| Market Forecast in 2034 | USD 54.2 Billion |

| Market Growth Rate 2026-2034 | 3.34% |

The global command and control system market is growing as demand rises for advanced situational awareness and decision-making capabilities in military and defense operations creates tremendous demand for global command and control systems. The integration of modern technologies, including artificial intelligence (AI), the Internet of Things (IoT), and cloud computing, improves real-time data processing and communication, fueling market growth. Rising geopolitical tensions and defense modernization initiatives further fuel investments in these systems. Additionally, their application in disaster management, public safety, and transportation sectors contributes to the growth, as governments and private organizations focus on improving operational efficiency and response times.

To get more information on this market Request Sample

The United States command and control system market is experiencing robust expansion, holding 89.90% of the market share. This is due to increased defense spending, technological advancements, and evolving security challenges. The Department of Defense's budget has seen consistent growth, reaching $715 billion in 2022, reflecting a commitment to modernizing military capabilities. This includes investments in advanced C2 systems that enhance situational awareness and decision-making. The integration of AI, machine learning (ML), and cybersecurity measures into these systems has become crucial for real-time data processing and threat response. Additionally, the rise in cyber threats and geopolitical tensions has prompted the U.S. to prioritize robust C2 infrastructures to ensure national security, thereby creating a positive outlook for market expansion.

Command and Control System Market Trends:

Rising Number of Security Threats

The increasing number of security threats, including cyberattacks, terrorism, and natural disasters, in an interconnected world, mainly drives the rising demand for command and control systems. In 2023, global cybersecurity threats caused an estimated USD 8 Trillion in damages, according to Cybersecurity Ventures, pointing out the urgent need for robust command and control systems. Terrorism and natural disasters also bring high-security concerns that need to be addressed with better response mechanisms. For example, the U.S. Department of Homeland Security committed USD 2.7 Billion for technology and C2 systems in 2022 for national security challenges. Such systems come with real-time threat detection, response capabilities, and continuous monitoring that reduce the risks associated with critical infrastructure and sensitive data. It also provides easy coordination among governments, military, and businesses. Because the growth of cybersecurity threats alone is anticipated to be at a 15% annual rate, the market for advanced command and control systems is also going to expand greatly.

Increasing Integration of Advanced Technologies in Systems

The incorporation of cutting-edge technologies such as AI, IoT, and cloud computing is transforming command and control systems. AI-powered analytics enable predictive insights. Industrial reports indicate that global AI spending is projected to reach USD 500 Billion by 2024. This facilitates better decision-making through efficient processing of vast amounts of data. IoT devices are enhancing situational awareness through real-time data collection. For instance, sensors used in military operations provide continuous feedback and allow for quicker responses in critical situations. Moreover, cloud computing is providing scale and flexibility, with the global cloud market expected to be valued at USD 1.8 Trillion by 2025, says a leading consulting group, making it possible for systems to be adapted to dynamic needs in operations without hefty infrastructure investments. The integration of 5G, which will reach 2.8 billion 5G connections worldwide by 2025, according to Ericsson, improves the speed and reliability of data transmission, especially in time-sensitive operations such as military communications and disaster response, which is strengthening the market growth.

Growing demand for advanced data integration and analytics capabilities

Command and control (C2) systems are highly valued for their ability to collect, integrate, and analyze data from various sources in a timely manner, thus allowing for real-time monitoring and fast decision-making. These systems provide real-time situational awareness and identify emerging threats or opportunities. In 2023, for instance, L3Harris Technologies was awarded a contract valued at up to USD 182 Million from the U.S. Air Force to deliver advanced situational awareness capabilities, which will include Video Data Link technology. Advanced analytics in C2 platforms facilitate resource allocation and optimize responses in military operations. Moreover, the integration of geospatial information systems (GIS) provides better spatial understanding and thereby significantly enhances decision-making functions in military operations and disaster management.

Command and Control System Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global command and control system market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on platform, solution, and application.

Analysis by Platform:

- Land

- Maritime

- Space

- Airborne

Land leads, holding a majority of the market share. This segment involves systems that are specifically designed for land-based operations, which encompass a wide range of military, security, and civilian applications. These systems are mainly deployed on the ground to coordinate and manage different activities and ensure effective command and control over land-based assets and resources. These platforms play a critical role in troop deployments, battlefield management, and tactical decision-making. They enable commanders to monitor troop movements, communicate with units in real time, and integrate data from various sensors and reconnaissance assets to gain a comprehensive understanding of the battlefield.

Analysis by Solution:

- Hardware

- Software

- Services

Hardware represents the largest market segment. These solutions comprise the physical components and equipment required to build, operate, and maintain these systems effectively. These components enable data processing, communication, and user interaction. They involve servers and data centers, computing devices, and communication equipment. High-performance servers and data centers are essential for processing vast amounts of data in real time. These systems ensure the reliability and scalability of operations, especially in critical applications like military command centers. On the other hand, computing devices include ruggedized computers, workstations, and consoles used by operators and decision-makers to access and analyze data. These devices often feature specialized interfaces and displays for intuitive interaction.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Defense

- Commercial

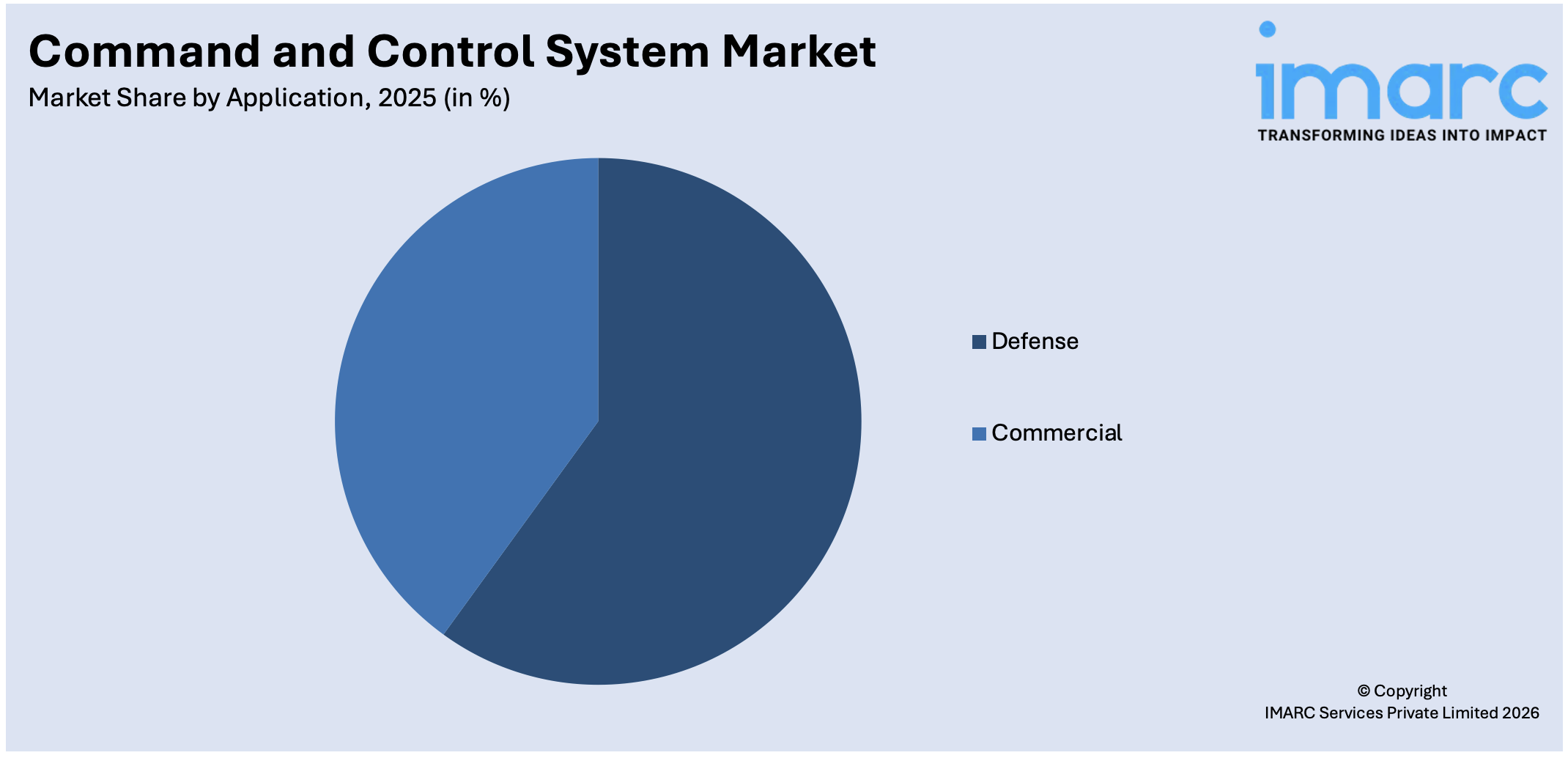

Defense leads the market with around 39.8% of the market share in 2025. In the defense application, these solutions play a vital role in ensuring the effectiveness, coordination, and security of military operations. These systems are tailored to the specific needs of defense forces and are used across all branches, including the army, navy, air force, and special operations. They provide real-time situational awareness to military commanders and enable them to monitor troop movements, logistics, and the battlefield environment. This information aids in making informed decisions and adapting strategies on the fly. These systems also facilitate secure and efficient communication between units, both on the battlefield and within command centers.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 41.7%. North America held the biggest market share due to the increasing adoption of command and control system technologies to ensure the security and effectiveness of military operations. Besides this, the presence of advanced defense industrial bases is contributing to the growth of the market in the region. In line with this, the increasing focus on advanced communication technologies is propelling the command and control system market growth. Besides this, the rising demand for interoperable and standardized command and control system platforms is bolstering the growth of the market in the region.

Key Regional Takeaways:

United States Command and Control System Market Analysis

Robust defense spending, technological developments, and an ever-changing landscape of defense have been fueling the U.S. command and control systems market. According to USA Facts, in 2023, the U.S. defense budget was USD 820.3 billion, and a significant portion has been committed to modernizing command and control systems. The U.S. military is investing much in the integrated systems to enhance its operational effectiveness across all branches such as space, air, and cyber. According to National Institute of Standards and Technology, over USD 10 Billion has been provided in 2023 by the Department of Defense for information and technology modernization, directly influencing command and control infrastructure. Some major leading companies dominating the market for advanced C2 solutions include Northrop Grumman, Lockheed Martin, and Raytheon. As the US military will continue to focus on developing its network-centric warfare capabilities, it will continue to require next-generation command and control systems. Emphasis will be placed on AI and real-time data processing. An example is L3Harris Technologies, which recently won an IDIQ contract valued at up to USD 182 Million from the US Air Force in 2023 for the delivery of advanced situational awareness capabilities, including Video Data Link technology.

Europe Command and Control System Market Analysis

The market for command and control systems across Europe is experiencing rapid growth, influenced by increased defense budgets, regional security issues, and military modernization efforts. According to the European Defence Agency, the member countries allocated about EURO 200 Billion (USD 253 Billion approx.) toward defense in 2022, a significant amount of which were earmarked for C2 system upgrades. Ukraine conflict-induced security crisis and NATO commitments have hastened the pace of military technology adoption. For instance, Germany had pledged an increase in defense spending to USD 107.2 billion in 2022, including investment in next-generation command and control infrastructure. The UK and France are considered at the forefront of developing C2 systems, as these are already embedding cutting-edge AI and real-time communication capabilities in military operations. As NATO focuses on interoperability, companies such as Thales Group and Airbus of Europe are in the lead to providing state-of-the-art command and control solutions for defense as well as non-defense applications.

Asia Pacific Command and Control System Market Analysis

The command and control systems market in Asia Pacific is growing rapidly due to the increasing defense budgets, emphasis on regional security, and technological advancements. The Stockholm International Peace Research Institute reports that China's defense budget amounted to USD 230 billion in 2022, with a focus on modernizing command and control systems for both conventional and cyber warfare. India has also allocated its 2023-2024 defense budget of USD 72.6 Billion, focusing on integrating digital technologies and the C2 system under the country's "Make in India" initiative. Like their counterparts, Japan and South Korea are also making advancements in cutting-edge C2 technologies to combat regional challenges. The Asia Pacific is witnessing a surge in cooperation between local companies and the world's leading tech manufacturers, such as Bharat Electronics with Raytheon for the future defense systems. The shift towards AI-driven C2 systems for real-time decision-making and battlefield management is expected to continue reshaping the region's market dynamics.

Latin America Command and Control System Market Analysis

Latin America is growing their command and control systems market in response to security concerns, regional instability, and the modernization of countries' defense infrastructure. As per Trading Economics, Brazil is also upgrading its defense infrastructure to enhance C2 systems, and in 2022 it expended USD 21.8 Billion on defense. Mexico is also upgrading its technology investment in anti-organized crime. In Colombia, the priority goes to security modernization; this will involve C2 systems for anti-insurgency and border security. An industry report states that the Latin American defense market is likely to expand by a CAGR of 4.2% during the next five years, command and control system modernization will be the highlight. Embraer and Atech, local companies, are increasing their C2 system offering and working closely with international firms to boost their ability in the areas of air defense, surveillance, and communications.

Middle East and Africa Command and Control System Market Analysis

In the Middle East and Africa, the command and control systems market is growing steadily with a surge in defense spending and advancements in technology. According to SIPRI, the defense budget for Saudi Arabia was estimated to be at USD 75.01 Billion in 2022, with a sizeable portion dedicated to upgrading the C2 systems under the Vision 2030 plan. The UAE and Qatar are also investing heavily in military modernization, focusing on air defense and integrated C2 systems. In Africa, the leader is South Africa, where local companies such as Denel and Saab provide advanced C2 solutions for both defense and security applications. According to the International Trade Administration, military investments in this region are expected to continue growing at 5% per year through 2027 and will further boost demand for command and control systems of complexity, especially for peacekeeping and counterterrorism operations.

Competitive Landscape:

Major players are investing in research and development (R&D) activities to stay at the forefront of technology. They continually innovate to incorporate emerging technologies, such as artificial intelligence (AI), machine learning (ML), and advanced analytics in their systems. Additionally, companies are focusing on strengthening the cybersecurity features of their solutions. This includes developing enhanced encryption methods, intrusion detection systems, and secure communication protocols to protect sensitive data, which is increasing command and control system market demand. Apart from this, key providers are offering customization options to cater to the specific needs of different industries and clients. This includes tailoring solutions for military, emergency management, law enforcement, and commercial applications. Moreover, they are working on making their systems adaptable to small, medium, and large-scale operations.

The report provides a comprehensive analysis of the competitive landscape in the command and control system market with detailed profiles of all major companies, including:

- BAE Systems plc

- CACI International Inc.

- Elbit Systems Ltd.

- General Dynamics Mission Systems Inc (General Dynamics Corporation)

- L3Harris Technologies Inc.

- Leonardo S.p.A.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Raytheon Technologies Corporation

- RGB Spectrum

- Saab AB

- Thales Group

- The Boeing Company

Latest News and Developments:

- October 2024: Lockheed Martin announced that they successfully integrated digital C2 capabilities with the DoD's Joint Fires Network prototype during the Valiant Shield exercise. This is the first test of the system that enhances joint operational coordination, demonstrating significant progress in the advancement of military command, control, and communication technologies.

- October 2024: BAE Systems and Kongsberg Defence and Aerospace announced that they have teamed to bring the Integrated Combat Solution, or ICS, to the U.S. defense market. A battlefield situational awareness tool designed for use on combat vehicles, the ICS enables response in minutes to be accelerated into seconds through the integration of video streams, metadata, and target information. The open systems ICS can connect sensors and weapon systems across platforms to provide command and control capabilities. Demonstrations have been made using Amphibious Combat and Armored Multi-Purpose Vehicle platforms.

- July 2024: CACI International Inc announced that they were awarded a USD 414 million task order to provide unmanned systems support for the U.S. Army's DEVCOM C5ISR Center. The contract involves threat assessments, countermeasure evaluations, training, and mitigation strategies to improve force protection and survivability against emerging global threats across operational domains.

- July 2024: Collins Aerospace displayed mobile command and control using AI/ML-enhanced situational awareness to support Mission Command On-The-Move. RTX's BBN Technologies demonstrated DISPERSED middleware reducing Air C2 latency-a key enabler for Agile Combat Employment in contested environments. Both innovations show where distributed operations and joint force collaboration are headed.

- June 2024: Northrop Grumman announced that they delivered the first production IBCS set to the U.S. Army, which contains EOC and IFCN Relay components. A USD 145 million FRP contract awarded in May 2024 supports deployment of advanced multi-domain command and control systems.

Command and Control System Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Platforms Covered | Land, Maritime, Space, Airborne |

| Solutions Covered | Hardware, Software, Services |

| Applications Covered | Defense, Commercial |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BAE Systems plc, CACI International Inc., Elbit Systems Ltd., General Dynamics Mission Systems Inc (General Dynamics Corporation), L3Harris Technologies Inc., Leonardo S.p.A., Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, RGB Spectrum, Saab AB, Thales Group, The Boeing Company etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the command and control system market from 2020-2034.

- The research report study provides the latest information on the market drivers, challenges, and opportunities in the global command and control system market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the command and control system industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Command and Control System Market Report

A command and control (C2) system is a framework that enables real-time monitoring, communication, and decision-making by integrating data from multiple sources. These systems are used in military, defense, public safety, and commercial sectors to ensure effective coordination and response during critical operations.

The command and control system market was valued at USD 40.3 Billion in 2025.

IMARC estimates the global command and control system market to exhibit a CAGR of 3.34% during 2026-2034.

The market is driven by rising security threats, increasing defense spending, adoption of advanced technologies like AI and IoT, and growing demand for data integration and situational awareness capabilities.

In 2025, land represented the largest segment by platform, driven by its critical role in troop deployment, battlefield management, and tactical decision-making.

Hardware leads the market by solution owing to the essential role of physical components like servers, computing devices, and communication equipment in data processing and operations.

The defense sector is the leading segment by application, driven by its reliance on C2 systems for real-time situational awareness and secure communication during military operations.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, wherein North America currently dominates the global market.

Some of the major players in the global command and control system market include BAE Systems plc, CACI International Inc., Elbit Systems Ltd., General Dynamics Mission Systems Inc (General Dynamics Corporation), L3Harris Technologies Inc., Leonardo S.p.A., Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, RGB Spectrum, Saab AB, Thales Group, The Boeing Company, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)