Commercial Aircraft Landing Gear Market Size, Share, Trends and Forecast by Aircraft Type, Landing Gear Types, Arrangement Type, and Region, 2026-2034

Commercial Aircraft Landing Gear Market Size and Share:

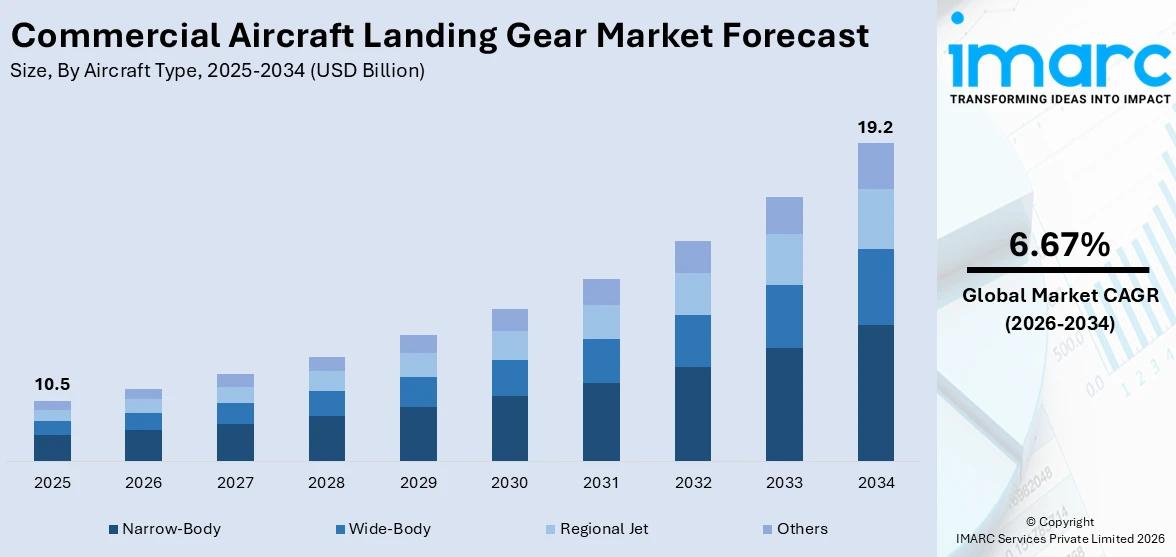

The global commercial aircraft landing gear market size was valued at USD 10.5 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 19.2 Billion by 2034, exhibiting a CAGR of 6.67% from 2026-2034. Asia-Pacific currently dominates the market, holding a market share of 35% in 2025. The region benefits from rapid expansion in air passenger traffic, the growing airline fleets, substantial government investments in airport infrastructure, and a rising middle class, all collectively bolstering the commercial aircraft landing gear market share.

The global commercial aircraft landing gear market is driven by multiple converging factors, including surging international air travel, expanding airline fleets, and the rapid modernization of aviation infrastructure across both developed and emerging economies. Rising aircraft production rates by major manufacturers, fueled by record-breaking order backlogs, are directly stimulating demand for advanced landing gear systems equipped with superior shock absorption, braking, and steering capabilities. The widespread integration of lightweight materials such as titanium alloys and carbon fiber composites into landing gear assemblies is enhancing fuel efficiency and reducing total cost of ownership. Increasing regulatory mandates emphasizing aviation safety and periodic fleet upgrades, combined with accelerating research and development investment across major aerospace economies, are further reinforcing the commercial aircraft landing gear market outlook on a global scale.

The United States has emerged as a major region in the commercial aircraft landing gear market owing to many factors. The country's well-established aerospace manufacturing base, supported by the presence of globally leading aircraft OEMs, MRO service providers, and precision component suppliers, makes the US a central hub for landing gear development and production. The FAA's stringent airworthiness standards mandate regular inspection cycles and timely landing gear replacement, sustaining consistent aftermarket demand. Fleet modernization programs adopted by major US carriers are driving increased acquisition of next-generation landing gear systems incorporating lightweight alloys and predictive maintenance technologies. According to the Federal Aviation Administration, the agency provides services to more than 44,000 flights and 3 million airline passengers daily across more than 29 million square miles of airspace, underscoring the immense scale of aviation operations driving steady demand for reliable landing gear systems. Growing domestic aerospace research and development expenditure, alongside government-backed innovation programs, further strengthen the US position as a pivotal commercial aircraft landing gear market.

To get more information on this market Request Sample

Commercial Aircraft Landing Gear Market Trends:

Growing Air Travel Demand

Growing air travel demand globally is a foundational driver of the commercial aircraft landing gear market. Airlines across all major regions are scaling their fleets to accommodate surging passenger volumes, particularly across Asia-Pacific, the Middle East, and Latin America, where rising disposable incomes are fueling unprecedented aviation adoption. This fleet expansion directly translates into increased procurement of new commercial aircraft equipped with advanced landing gear systems. Leading manufacturers are recording historically high order backlogs, with both narrow-body and wide-body programs seeing sustained demand that extends the commercial aircraft landing gear market forecast well into the next decade. The recovery of international air traffic following pandemic-era disruptions has re-energized aviation sectors globally, motivating airlines to accelerate aircraft acquisition timelines. The replacement of aging legacy fleets with fuel-efficient, next-generation models further multiplies landing gear procurement volumes across both OEM and aftermarket channels. Global air travel demand hits all-time highs in 2025, based on annual passenger statistics published by the International Air Transport Association (IATA). Cruise journey reservations. Overall demand, gauged in revenue passenger kilometers, grows by 5.3% relative to 2024, while total capacity expands by 5.2%, elevating the global passenger load factor to an unprecedented 83.6%.

Significant Technological Advancements

Technological innovation is reshaping the commercial aircraft landing gear market trends, with manufacturers and OEMs deploying advanced materials and digital systems to enhance performance and reduce lifecycle costs. The adoption of titanium alloys and carbon fiber composite materials is enabling landing gear weight reductions of up to 30% compared to conventional steel-based structures, directly improving aircraft fuel efficiency and payload capacity. This transition is gaining momentum as manufacturers seek to meet tightening emissions standards and airline demands for lower operating costs. Additive manufacturing techniques, including industrial-grade 3D printing, are facilitating the production of intricate landing gear geometries that offer superior structural performance while minimizing material waste during fabrication. The integration of health monitoring sensors and AI-driven predictive maintenance platforms is transforming MRO practices, enabling condition-based maintenance cycles that minimize unscheduled downtime and lower total maintenance expenditures for airlines. IMARC Group expects that the global predictive maintenance market will reach USD 91.0 Billion by 2034.

Rising Fleet Modernization Programs

Fleet modernization programs across major global airlines are creating sustained demand across the commercial aircraft landing gear market. As airlines retire older, less fuel-efficient aircraft and replace them with next-generation models equipped with advanced avionics, propulsion systems, and landing gear assemblies, procurement volumes for high-performance systems are increasing markedly. The increasing adoption of aircraft programs such as the Airbus A320neo and Boeing 737 MAX family, both optimized for narrow-body short-to-medium-haul operations, has significantly expanded landing gear replacement and procurement cycles globally. Airlines in emerging markets are particularly aggressive in modernizing their fleets, driven by rising passenger expectations and tightening environmental regulations that incentivize fuel-efficient operations. In September 2024, Air India announced the commencement of its over USD 400 million refit program targeting a phased revamp of 67 legacy aircraft, beginning with 27 narrow-body Airbus A320neo aircraft followed by 40 wide-body Boeing platforms, exemplifying the scale of fleet renewal activity driving the positive commercial aircraft landing gear market outlook across Asia-Pacific and broader global aviation sectors. This widespread modernization wave is expected to sustain elevated landing gear procurement activity across the forecast period.

Commercial Aircraft Landing Gear Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global commercial aircraft landing gear market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on aircraft type, landing gear types, and arrangement type.

Analysis by Aircraft Type:

- Narrow-Body

- Wide-Body

- Regional Jet

- Others

Narrow-body holds 48% of the market share. Narrow-body aircraft, typically configured as single-aisle platforms designed for short to medium-haul routes, are the most widely produced and operated commercial aircraft type globally. Their dominance in commercial aviation is driven by the rapid expansion of low-cost carriers, high operational frequency on high-density routes, and strong procurement demand from airlines in both established and emerging markets. The suitability of narrow-body aircraft for point-to-point operations, combined with their favorable economics in terms of seat-mile costs, has made them the preferred choice for fleet expansion across Asia-Pacific, North America, and Europe. Narrow-body aircraft programs such as the Airbus A320neo and Boeing 737 MAX families command the largest order backlogs in commercial aviation history. Each aircraft in these programs requires dedicated landing gear systems tailored for high-frequency landing cycles, generating proportionally higher maintenance and replacement demand, thereby further propelling commercial aircraft landing gear market growth.

Analysis by Landing Gear Types:

Access the comprehensive market breakdown Request Sample

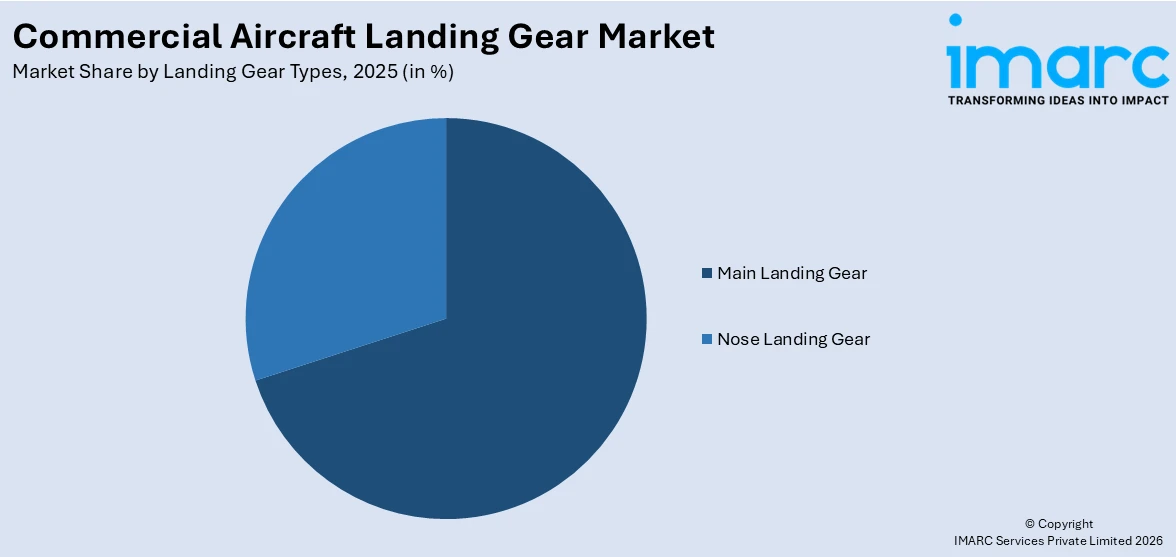

- Main Landing Gear

- Nose Landing Gear

Main landing gear leads the market with a share of 70%. Main landing gear systems are the primary structural load-bearing assemblies responsible for supporting the full weight of an aircraft during ground operations, taxi, takeoff, and landing. Their structural complexity, higher component count, and use of advanced high-strength materials compared to nose landing gear make them significantly more expensive to manufacture and maintain, contributing to their dominant revenue share in the overall market. The main landing gear is engineered to absorb the majority of touchdown impact forces, requiring robust multi-wheel bogies on wide-body and large commercial platforms. Moreover, demand for main landing gear systems is directly correlated with commercial aircraft production rates, particularly for narrow-body platforms with high-frequency operational cycles.

Analysis by Arrangement Type:

- Tricycle

- Tandem

- Tailwheel

Tricycle dominates the market, with a share of 83%. The tricycle landing gear arrangement, characterized by one nose gear unit at the forward fuselage and two main gear units positioned aft of the aircraft's center of gravity, is the universal standard configuration for modern commercial aviation. Its advantages include superior ground stability during taxiing and landing, improved forward visibility from the cockpit during ground operations, and better weight distribution that enables consistent structural load management across the airframe. The tricycle configuration is compatible with both narrow-body and wide-body aircraft designs, making it the default choice for virtually all major commercial aircraft programs worldwide. Its aerodynamic efficiency when retracted into the fuselage further contributes to its widespread adoption. The design's ability to withstand repeated heavy landing cycles, particularly across high-frequency narrow-body operations, ensures its continued dominance for new aircraft deliveries.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific, accounting for 35% of the share, enjoys the leading position in the market. The region's leadership is underpinned by rapid growth in air passenger traffic, fleet expansion programs by major regional carriers, and significant government investment in airport infrastructure development across China, India, and Southeast Asia. Rising disposable incomes and expanding middle-class populations are driving unprecedented demand for commercial aviation services, motivating airlines to aggressively order new aircraft equipped with advanced landing gear systems. China's domestic aviation sector, supported by indigenous aircraft programs such as the COMAC C919, is building localized aerospace supply chains that include landing gear manufacturing capabilities. India's aviation market is among the fastest growing globally, with the country's airline fleet expanding at significant pace driven by rising passenger volumes. Airbus forecasts that the Asia Pacific region will absorb approximately 45% of global commercial jet deliveries over the next two decades, reflecting the structural momentum driving sustained landing gear demand across the region. Increasing MRO activity, driven by a rapidly growing fleet base across China, India, Japan, and Southeast Asia, further amplifies aftermarket demand and positions the region as a pivotal landing gear market.

Key Regional Takeaways:

United States Commercial Aircraft Landing Gear Market Analysis

The United States commercial aircraft landing gear market represents one of the largest and most technologically advanced segments globally, driven by the country's extensive aviation infrastructure and the presence of world-leading aircraft manufacturers and aerospace component suppliers. The US aviation sector operates one of the highest-frequency commercial flight networks globally, sustaining consistent demand for landing gear systems across both OEM manufacturing and MRO aftermarket channels. The Federal Aviation Administration's stringent airworthiness standards mandate rigorous inspection and overhaul schedules for landing gear components, ensuring predictable replacement cycles across the nation's vast commercial fleet. Major US airlines are actively executing fleet modernization programs, replacing aging narrow-body and wide-body aircraft with next-generation models incorporating advanced lightweight landing gear technologies. Defense aviation programs supplement procurement volumes, with dual-use technologies crossing between commercial and military applications. Boeing's landing-gear exchange network currently spans a large number of assets worldwide, reflecting the scale of US-based aftermarket infrastructure and the depth of demand management capabilities developed by American aerospace companies. In 2026, Boeing revealed the most significant landing gear exchange contract in its history during the Singapore Airshow. According to this agreement, Boeing will supply landing gear replacements for over 75 planes within the 737 MAX and 787 fleets utilized by Singapore Airlines (SIA) Group. The landing gear exchange initiative provides flexible scheduling for gear overhauls, enhancing the gears' useful life and reducing aircraft downtime.

Europe Commercial Aircraft Landing Gear Market Analysis

Europe commercial aircraft landing gear market is supported by the presence of globally leading aerospace manufacturers, established MRO service networks, and stringent regulatory standards administered by the European Union Aviation Safety Agency. The region houses two of the world's foremost landing gear system manufacturers, which leverage deep engineering expertise and extensive OEM partnerships to maintain competitive advantages across global programs. Airbus's significant aircraft production activities across France, Germany, and Spain generate consistent demand for landing gear systems integrated into A320neo and A350 family aircraft programs. Collins Aerospace is actively expanding its Tajcina, Poland facility to increase landing gear system output, with construction commencing in November 2024 and completion targeted for February 2026, highlighting the growing scale of production capacity investment within the European supply chain. Eastern European countries, particularly Poland and the Czech Republic, are emerging as important manufacturing hubs for precision-machined landing gear sub-assemblies, attracting aerospace investment from global OEMs seeking to shorten delivery lead times. European Union sustainability mandates are further prompting the development of electric actuation systems and lifecycle impact assessments for landing gear hardware, driving long-term technology investments across the region.

Asia-Pacific Commercial Aircraft Landing Gear Market Analysis

Asia Pacific is the largest and fastest-growing region in the commercial aircraft landing gear market, driven by rapidly expanding commercial aviation sectors across China, India, Japan, South Korea, and Southeast Asia. The region's growing middle-class populations are driving unprecedented demand for air travel, motivating airlines to aggressively expand operational fleets and order new aircraft equipped with advanced landing gear systems. Indigenous aircraft development programs, including China's COMAC C919, are building domestic aerospace supply chains that incorporate landing gear manufacturing capabilities. India's aviation sector is experiencing particularly robust growth, with the country's fleet projected to expand substantially as airlines respond to surging passenger demand. Growing MRO infrastructure investments across South Korea, Australia, and Indonesia are further expanding aftermarket demand and positioning Asia-Pacific as a key hub for landing gear overhaul services.

Latin America Commercial Aircraft Landing Gear Market Analysis

Latin America commercial aircraft landing gear market is experiencing steady growth, supported by expanding air connectivity, growing inbound tourism, and continued fleet modernization efforts among regional carriers. Brazil and Mexico serve as the primary aviation markets in the region, with airlines operating extensive domestic and international networks that sustain consistent demand for landing gear systems. The growing penetration of low-cost carriers across the region is driving procurement of narrow-body aircraft with modern landing gear configurations optimized for high-frequency operations.

Middle East and Africa Commercial Aircraft Landing Gear Market Analysis

Middle East and Africa commercial aircraft landing gear market is driven by the rapid expansion of aviation hubs across the Gulf region and growing air connectivity across sub-Saharan and North Africa. Gulf carriers operating extensive wide-body fleets on long-haul international routes generate significant demand for heavy-duty main landing gear systems and associated aftermarket overhaul services. Africa's aviation sector is emerging as a long-term growth frontier, with increasing investment in airport infrastructure across key aviation markets. In a significant development for the region's manufacturing sector, Safran announced plans to establish a new manufacturing facility for landing-gear equipment in the Casablanca airport zone in Morocco, reflecting growing industry confidence in regional production potential and long-term market development. The establishment of aerospace manufacturing capabilities in North Africa is expected to create new supply chain opportunities and position the region as an emerging contributor to the global commercial aircraft landing gear ecosystem over the forecast period.

Competitive Landscape:

The global commercial aircraft landing gear market is characterized by a moderately consolidated competitive landscape dominated by a handful of specialized aerospace manufacturers with deep OEM relationships, certified engineering capabilities, and extensive aftermarket service networks. Market participants compete across multiple dimensions including material innovation, system integration capabilities, MRO service quality, and the ability to meet stringent regulatory certification timelines for new aircraft programs. Major players are increasingly focusing on forming strategic partnerships and long-term service agreements with airlines and aircraft manufacturers to secure recurring revenue streams across the 25-to-30-year lifecycle of commercial aircraft. Companies are investing significantly in lightweight material technologies, predictive maintenance platforms, and digital service capabilities to differentiate their offerings. The market has witnessed notable consolidation activity, with leading players expanding capabilities through targeted acquisitions and joint venture arrangements to strengthen both OEM supply positions and aftermarket service portfolios. The ongoing shift from metal-cutting capacity toward digital-service propositions, including predictive analytics and rotable pool management, is reshaping competitive dynamics and enabling larger players to extract value across the full airframe lifecycle.

The report provides a comprehensive analysis of the competitive landscape in the commercial aircraft landing gear market with detailed profiles of all major companies, including:

- CIRCOR International, Inc.

- Collins Aerospace

- Héroux-Devtek

- magroup

- Mecaer Aviation Group

- Revima

- Safran SA

- Sumitomo Precision Products Co., Ltd

- Triumph Group

- Whippany Actuation Systems

Latest News and Developments:

- June 2025: Safran Landing Systems extended its long-term collaborative agreement with Revima Group to enhance global landing gear MRO capabilities, with a specific focus on newer Airbus aircraft models. The renewed partnership merges Safran's OEM engineering expertise with Revima's maintenance excellence to strengthen lifecycle support across commercial fleets. In the same month, Safran Landing Systems also inaugurated a new state-of-the-art machining building and advanced surface treatment lines at its Molsheim, France facility, expanding production capacity to meet rising global demand for commercial landing gear systems.

Commercial Aircraft Landing Gear Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Aircraft Types Covered | Narrow-Body, Wide-Body, Regional Jet, Others |

| Landing Gear Types Covered | Main Landing Gear, Nose Landing Gear |

| Arrangement Types Covered | Tricycle, Tandem, Tailwheel |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | CIRCOR International, Inc., Collins Aerospace, Héroux-Devtek, magroup, Mecaer Aviation Group, Revima, Safran SA, Sumitomo Precision Products Co., Ltd, Triumph Group, Whippany Actuation Systems, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the commercial aircraft landing gear market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global commercial aircraft landing gear market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the commercial aircraft landing gear industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Commercial Aircraft Landing Gear Market Report

The commercial aircraft landing gear market was valued at USD 10.5 Billion in 2025.

The commercial aircraft landing gear market is projected to exhibit a CAGR of 6.67% during 2026-2034, reaching a value of USD 19.2 Billion by 2034.

The market is driven by rising global air travel demand, fleet expansion by airlines, technological advancements in lightweight materials and composites, increasing fleet modernization programs, stringent safety regulations mandating regular landing gear overhauls, and the rapid growth of commercial aviation in emerging economies, particularly across Asia-Pacific, stimulating procurement of new aircraft equipped with advanced landing gear systems.

Asia Pacific currently dominates the commercial aircraft landing gear market, accounting for a share of 35%. The region benefits from rapid expansion in commercial aviation fleets, surging air passenger traffic, a rising middle class across China, India, and Southeast Asia, and significant government investments in aviation infrastructure and aircraft manufacturing capabilities.

Some of the major players in the commercial aircraft landing gear market include CIRCOR International, Inc., Collins Aerospace, Héroux-Devtek, magroup, Mecaer Aviation Group, Revima, Safran SA, Sumitomo Precision Products Co., Ltd, Triumph Group, Whippany Actuation Systems, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)