Commercial Greenhouse Market Size, Share, Trends and Forecast by Type, Material Used, Technology, Crop, and Region 2026-2034

Commercial Greenhouse Market Size, Share, Trends & Forecast (2026-2034)

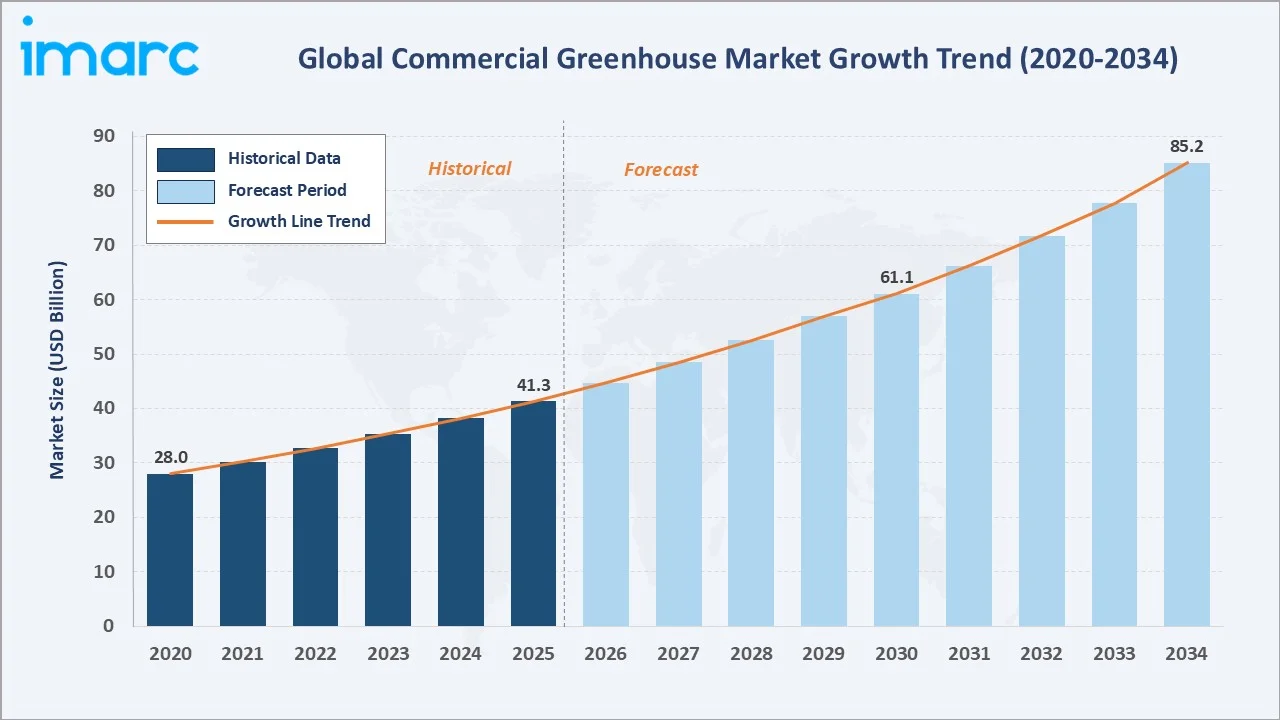

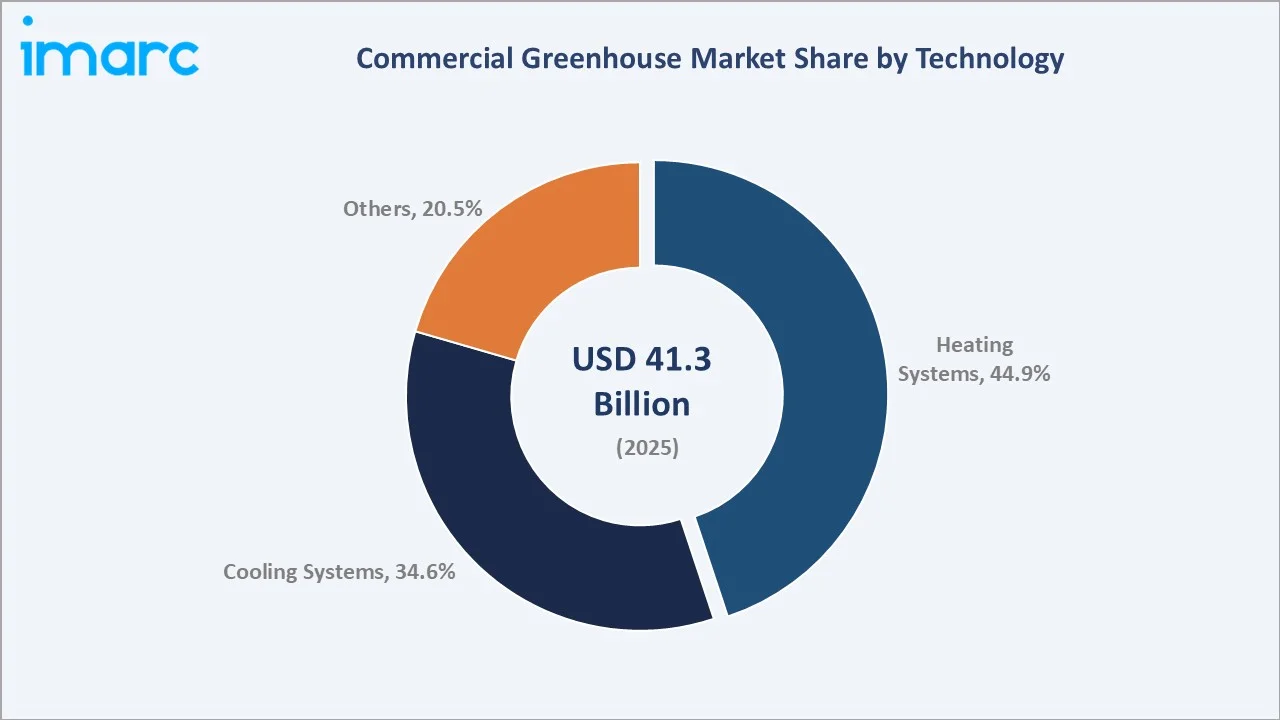

The global commercial greenhouse market reached USD 41.3 Billion in 2025 and is projected to reach USD 85.2 Billion by 2034, growing at a CAGR of 8.12% during 2026-2034. The market is driven by rising demand for high-yield crop production, year-round cultivation, and efficient use of land and water resources. The global harvested area of major primary crops reached approximately 1.5 billion hectares in 2024, increasing by 197 million hectares compared to 2010. This growth in agricultural activity is driving the commercial greenhouse market by increasing the need for efficient and high-yield farming methods, controlled-environment cultivation, and advanced crop management technologies to improve productivity and resource utilization. Gutter-connected greenhouses dominate at 58.6%. Heating system leads technology at 44.9%. Europe commands 34.2% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 41.3 Billion |

|

Forecast Market Size (2034) |

USD 85.2 Billion |

|

CAGR (2026-2034) |

8.12% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Gutter-connected Greenhouses (58.6%, 2025) |

|

Dominant Technology |

Heating System (44.9%, 2025) |

|

Leading Region |

Europe (34.2%, 2025) |

The global commercial greenhouse market expanded from USD 28.0 Billion in 2020 to USD 41.3 Billion in 2025, anchored at USD 61.1 Billion in 2030, and forecast to reach USD 85.2 Billion by 2034. COVID-19 exposed global food supply chain vulnerability in 2020, triggering unprecedented government investment in domestic food production infrastructure globally. The post-COVID food security investment momentum sustained above-trend commercial greenhouse market growth through 2022-2025.

To get more information on this market, Request Sample

Cooling systems grow fastest at ~8.8% CAGR as climate change expands commercial greenhouse viability into historically hot regions where cooling technology investment determines growing feasibility. Gutter-connected greenhouses grow at ~8.5% CAGR through large-scale commercial farming economics.

Executive Summary

The global commercial greenhouse market reached USD 41.3 Billion in 2025, representing one of the world's most dynamic intersections of agriculture, technology, and real estate investment. The market encompasses greenhouse structure construction, climate control technology, irrigation and nutrient systems, lighting systems, and integrated automation and software that converts a basic structure into a controlled environment food production platform.

Gutter-connected greenhouses at 58.6% dominate through commercial efficiency advantages. Heating systems at 44.9% lead technology through the foundational role of heating in extending growing seasons and enabling year-round production in temperate and cold climate regions. Europe, at 34.2%, leads through the Netherlands' global greenhouse technology dominance and Spain's Almeria production scale.

Key Market Insights

|

Insight |

Data |

| Dominant Type |

Gutter-connected Greenhouses - 58.6% share (2025) |

| Dominant Technology |

Heating System - 44.9% market share (2025) |

| Leading Region |

Europe - 34.2% market share |

| Market Opportunity |

Agrivoltaic solar greenhouse; AI climate control; cannabis licensed greenhouse; food security government investment; robotic harvesting; vertical multilayer greenhouse farming |

Key Analytical Observations Supporting The Above Data:

- Gutter-connected Greenhouses at 58.6%: The gutter-connected greenhouses dominate due to their large-scale production capacity, efficient space utilization, and better climate control. These structures are widely preferred by commercial growers for high-yield cultivation, automation integration, and reduced operational costs.

- Heating Systems at 44.9%: The heating systems dominate because temperature control is essential for year-round crop production and protection against cold weather. These systems help maintain optimal growing conditions, improve crop yield, and support consistent production quality.

- Europe at 34.2%: Europe dominates the market due to its strong adoption of advanced controlled-environment agriculture, automation, and energy-efficient greenhouse technologies. The region’s focus on sustainable farming, high-value crop production, and year-round cultivation further supports its leading position.

Commercial Greenhouse Market Overview

The global commercial greenhouse market encompasses the design, construction, equipping, and operation of all permanent and semi-permanent controlled environment structures used for commercial crop production. The market encompasses greenhouse structure, climate control technology, growing systems, lighting, crop management technology, and post-harvest handling.

Macroeconomic factors include rising global food demand, population growth, urbanization, and increasing investments in sustainable agriculture infrastructure. In addition, climate change concerns, water scarcity, and government support for modern farming technologies are accelerating greenhouse adoption worldwide.

Market Dynamics

To evaluate market opportunities, Request Sample

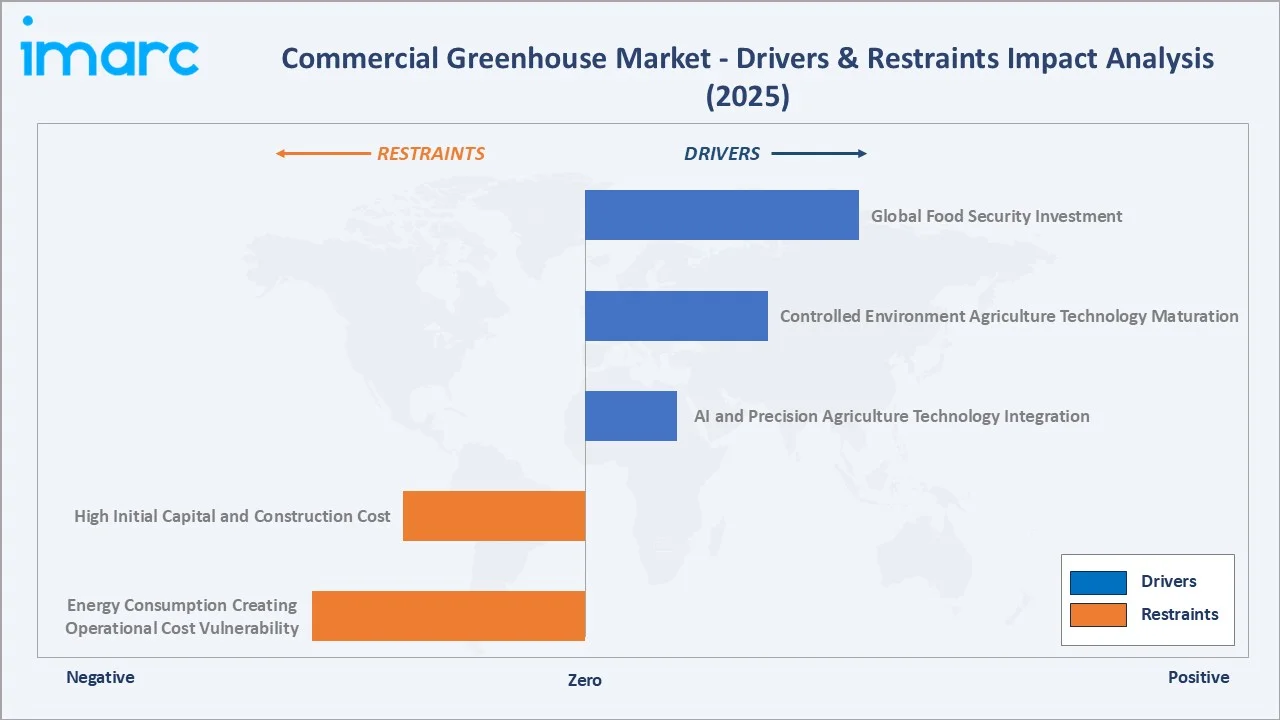

Market Drivers

- Global Food Security Investment: Global food security investment is increasing funding for advanced and high-efficiency agricultural systems. Governments and private organizations are investing in greenhouse farming to ensure stable food production amid climate change, population growth, and shrinking arable land. In April 2025, Panvita Group started operations at its new greenhouse in Nemščak, Prekmurje, built for year-round leafy greens cultivation using advanced farming technologies. The project is among the first major infrastructure developments completed after BOSQAR INVEST’s EUR 50 million majority-stake investment in Panvita Group, finalized in November 2024. Commercial greenhouses enable year-round cultivation, higher crop yields, and reduced dependency on seasonal conditions. These benefits are encouraging large-scale adoption of controlled-environment agriculture worldwide.

- Controlled Environment Agriculture Technology Maturation: Controlled environment agriculture (CEA) technology maturation is improving precision farming, automation, and resource efficiency. Advanced technologies such as climate control systems, hydroponics, IoT sensors, and AI-based monitoring enable growers to optimize crop conditions and increase yields. These innovations reduce water and energy consumption while ensuring consistent year-round production. As CEA technologies become more affordable and scalable, their adoption across commercial greenhouse operations continues to grow.

- AI and Precision Agriculture Technology Integration: AI and precision agriculture technology integration enabling real-time monitoring, automated climate control, and data-driven crop management. AI-powered systems help optimize irrigation, temperature, humidity, and nutrient supply, improving crop yield and reducing resource wastage. Precision agriculture technologies also support early pest and disease detection, enhancing operational efficiency and product quality. In May 2025, Gardin Agritech raised $4.5 million in Seed 2 funding to further develop its precision agriculture solutions. The investment will support the expansion of its photosynthesis sensor and AI-based platform, which enable real-time, large-scale monitoring of greenhouse crop health. These advancements are encouraging greenhouse operators to adopt smarter and more sustainable farming practices.

Market Restraints

- High Initial Capital and Construction Cost: High initial capital and construction costs make adoption difficult for small and medium-scale growers. Setting up greenhouse structures, climate control systems, irrigation, lighting, and automation requires significant upfront investment. High financing costs and long payback periods can discourage new entrants. As a result, market growth is slower in price-sensitive and developing agricultural regions.

- Energy Consumption Creating Operational Cost Vulnerability: Energy consumption is creating operational cost vulnerability due to the high-power requirements of heating, cooling, lighting, and climate control systems. Rising electricity and fuel prices significantly increase production costs, especially in regions with extreme weather conditions. These expenses can reduce profitability for greenhouse operators and limit adoption among small-scale growers. Dependence on a continuous energy supply also creates challenges related to cost fluctuations and sustainability concerns.

Market Opportunities

- Agrivoltaic Solar-Integrated Greenhouse: Agrivoltaic solar-integrated greenhouses combine crop cultivation with solar energy generation. These systems help reduce electricity costs by powering greenhouse operations through renewable energy sources. They also improve land-use efficiency and support sustainable farming practices by lowering carbon emissions. Growing demand for energy-efficient and climate-resilient agriculture is encouraging the adoption of solar-integrated greenhouse infrastructure.

- Vertical Greenhouse and Multilayer Indoor Farming: Vertical greenhouses and multilayer indoor farming enable high crop output in limited land areas. These systems are especially useful in urban and land-scarce regions where traditional farming space is restricted. By using stacked cultivation, controlled lighting, and automated climate systems, they improve yield consistency and resource efficiency. Rising demand for locally grown, pesticide-free, and year-round fresh produce is further supporting their adoption.

Market Challenges

- Dependence on Continuous Power Supply and Climate Control Systems: Dependence on continuous power supply and climate control systems is a major challenge because crops require stable temperature, humidity, lighting, and ventilation conditions for optimal growth. Power outages or system failures can negatively affect crop quality, productivity, and overall yield. In regions with unreliable electricity infrastructure, greenhouse operators often face higher backup energy and maintenance costs. This increases operational risks and reduces profitability, especially for small and medium-scale growers.

- Water Management and Irrigation Challenges: Water management and irrigation challenges are creating difficulties due to the need for precise water distribution and moisture control. Inefficient irrigation systems can lead to water wastage, nutrient imbalance, and reduced crop productivity. In regions facing water scarcity, maintaining consistent irrigation for greenhouse operations becomes costly and operationally challenging. These issues increase production expenses and highlight the need for advanced water-saving technologies and smart irrigation systems.

Emerging Market Trends

1. Dutch Greenhouse Technology Global Diffusion Accelerating Through Turnkey Project Models

Dutch greenhouse technology is spreading globally through turnkey project models, where providers deliver complete greenhouse solutions from design and construction to automation and crop management support. This reduces technical barriers for growers and accelerates the adoption of advanced climate control, irrigation, and cultivation systems. Countries seeking high-yield and resource-efficient farming are increasingly adopting these ready-to-operate models. An India-Netherlands public-private partnership, NLHortiRoad2India, aims to help Indian farmers and entrepreneurs adopt advanced Dutch greenhouse technology for year-round cultivation of high-value horticultural crops. After a successful three-year demonstration in Indian conditions, the initiative is offering a complete package that includes high-tech greenhouse solutions, market linkages, farmer training, education, and long-term financing support. Such integrated solutions reduce adoption barriers and make high-tech greenhouse farming more scalable in emerging markets like India.

2. Commercial Greenhouse Electrification and Decarbonization Transforming Energy Economics

Commercial greenhouse electrification and decarbonization are shifting operations from fossil fuel-based heating and cooling toward renewable electricity, heat pumps, and energy-efficient systems. This helps reduce carbon emissions while improving long-term energy cost stability. Growers are also adopting solar power, battery storage, and smart energy management to lower operating expenses. As sustainability regulations and energy prices rise, decarbonized greenhouse models are becoming increasingly attractive.

3. Robotics Integration Creating Labor-Independent Commercial Greenhouse Operations

Robotics integration reduces dependence on manual labor and improves operational efficiency. Automated robots are increasingly used for planting, harvesting, crop monitoring, spraying, and packaging activities. In March 2026, Eternal.ag launched its first commercial product, Harvester, a fully autonomous harvesting robot designed for tomato greenhouses and offers a solution to widespread industry labor shortages. These technologies help address labor shortages, lower labor costs, and improve precision in greenhouse operations. As automation advances, growers are adopting robotic systems to achieve higher productivity and consistent crop quality.

4. Urban Greenhouse and Rooftop Farming Creating City-Center Food Production Infrastructure

Urban greenhouses and rooftop farming enable fresh food production within city centers. These systems reduce dependence on long-distance supply chains and support local, year-round availability of vegetables and herbs. Rooftop and urban greenhouse models also make better use of unused urban spaces while lowering transportation-related emissions. Growing demand for fresh, sustainable, and locally grown produce is encouraging investment in city-based greenhouse infrastructure.

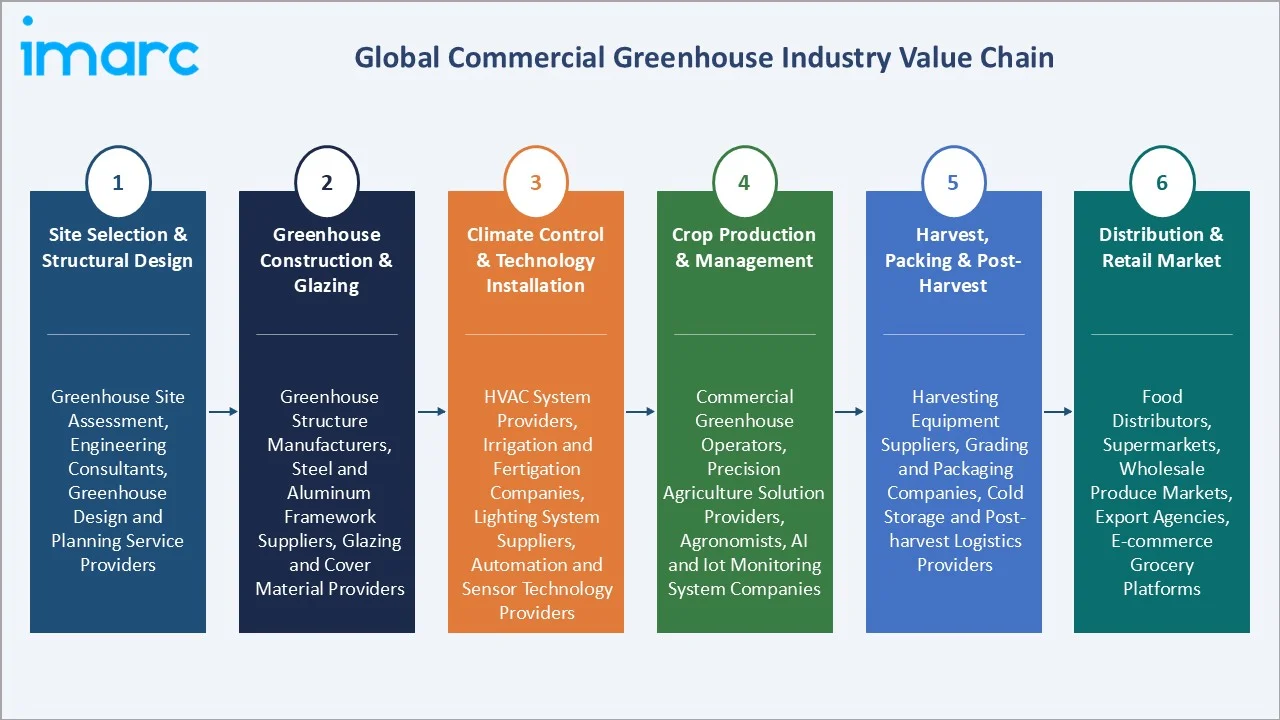

Industry Value Chain Analysis

The commercial greenhouse value chain integrates site selection and structural design, greenhouse construction and glazing, climate control and technology installation, crop production and management, harvest and post-harvest handling, and distribution and retail market supply.

| Stage | Key Participants |

| Site Selection & Structural Design | Greenhouse site assessment, engineering consultants, greenhouse design and planning service providers |

| Greenhouse Construction & Glazing | Greenhouse structure manufacturers, steel and aluminum framework suppliers, glazing and cover material providers |

| Climate Control & Technology Installation | HVAC system providers, irrigation and fertigation companies, lighting system suppliers, automation and sensor technology providers |

| Crop Production & Management | Commercial greenhouse operators, precision agriculture solution providers, agronomists, AI and IoT monitoring system companies |

| Harvest, Packing & Post-Harvest | Harvesting equipment suppliers, grading and packaging companies, cold storage and post-harvest logistics providers |

| Distribution & Retail Market | Food distributors, supermarkets, wholesale produce markets, export agencies, e-commerce grocery platforms |

The climate control and technology installation stage is the value chain's most technically complex and commercially differentiated phase. The substrate growing and nutrient management layer creates the precision growing environment where Dutch greenhouse tomato achieves a high annual yield. Post-harvest handling technology sustains the quality premium that commercial greenhouse produce commands at retail.

Technology Landscape in the Commercial Greenhouse Industry

Glass Venlo Greenhouse Structure Technology

Glass Venlo greenhouse structure technology enables high light transmission, efficient climate control, and large-scale crop production. Its modular design supports automation, advanced ventilation systems, and energy-efficient operations for year-round cultivation. These structures are widely adopted for high-value horticulture due to their durability and productivity advantages. As demand for precision farming grows, Glass Venlo greenhouses are becoming a preferred solution for modern controlled-environment agriculture.

LED Horticultural Lighting Technology

LED horticultural lighting technology enables precise control over light intensity, spectrum, and photoperiod for different crops. It helps improve plant growth, yield, and quality while reducing energy consumption compared to traditional lighting systems. LEDs also support year-round cultivation in low-light regions and indoor greenhouse setups. As growers focus on productivity and energy efficiency, LED lighting is becoming a key technology in modern greenhouse operations. In February 2026, Sollum Technologies launched SF-INFINITE, a new LED fixture for commercial greenhouses.

Climate Computer and AI Crop Management

Climate computers and AI crop management enable automated control of temperature, humidity, CO₂, irrigation, and ventilation. These systems use real-time sensor data and predictive analytics to optimize growing conditions and reduce resource wastage. AI-based platforms also help detect crop stress, pests, and diseases at an early stage. As a result, greenhouse operators can improve yield, quality, and operational efficiency.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Gutter-connected Greenhouses | 58.6% | 2025 |

| Material Used | 🔒 | 🔒 | 2025 |

| Technology | Heating System | 44.9% | 2025 |

| Crop | 🔒 | 🔒 | 2025 |

| Region | Europe | 34.2% | 2025 |

By Type

Gutter-connected greenhouses lead at 58.6% (2025). The gutter-connected segment encompasses premium Dutch Venlo glass greenhouse systems dominating high-value vegetable and floriculture production, as well as large-scale polycarbonate and polythene multi-span connected structures for cannabis and value vegetable production.

To access detailed market analysis, Request Sample

Free-standing greenhouses at 41.4% encompass the world's largest aggregate greenhouse area. Free-standing greenhouse's ~7.6% CAGR is above the historical rate through scale-up of small-scale operators in Latin America, Africa, and Asia-Pacific, where free-standing remains the economically appropriate entry format for emerging commercial greenhouse markets.

By Technology

Heating systems lead at 44.9% (2025). The heating system segment encompasses hot water pipe heating, forced air heating, geothermal heat pump systems, biomass boiler systems, and heat storage buffer tanks. Heating system's ~7.9% CAGR reflects the energy transition, creating heating system technology upgrade investment alongside new greenhouse construction.

Cooling systems at 34.6% grow fastest at ~8.8% CAGR through geographic expansion into hot climate regions and climate change, creating cooling retrofit demand in historically temperate European markets. Others at 20.5% encompasses LED lighting systems, CO2 enrichment equipment, humidity management systems, and integrated climate management software.

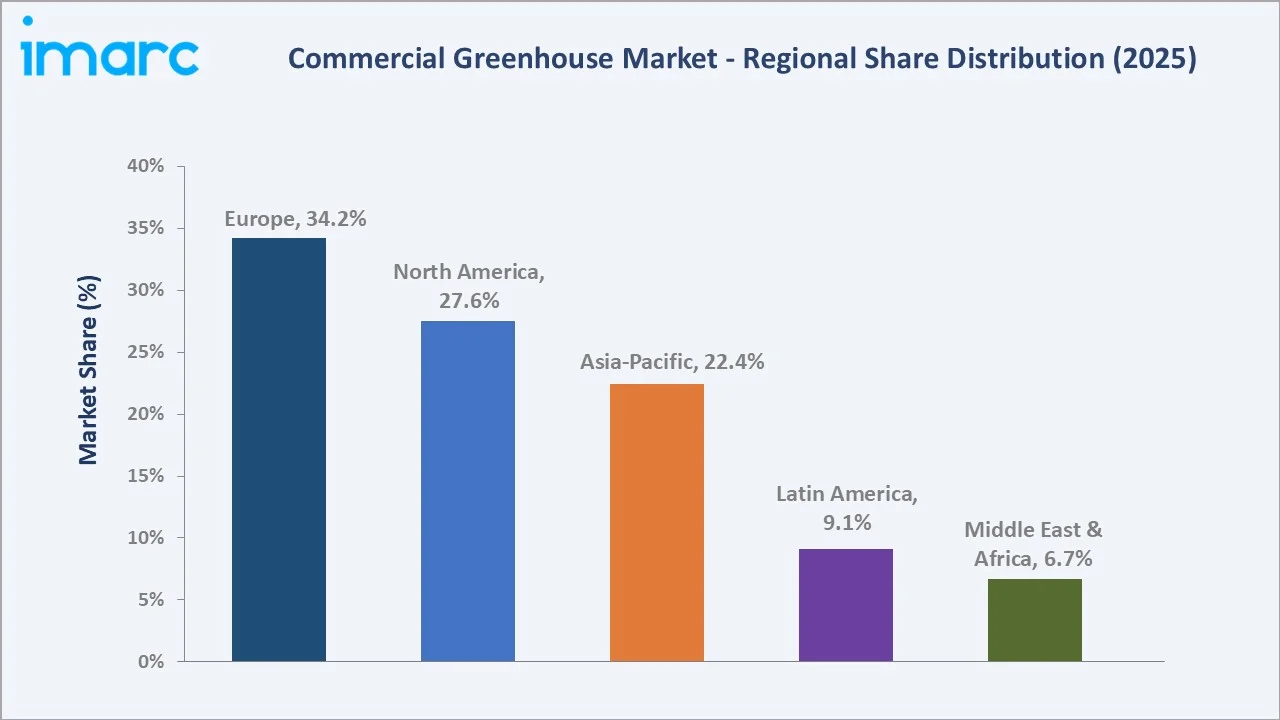

Regional Market Insights

|

Region |

Share (2025) | Key Commercial Greenhouse Market Drivers & Characteristics |

| Europe | 34.2% | Driven by strong adoption of advanced greenhouse technologies, sustainable farming practices, and year-round horticulture production. |

| North America |

27.6% |

Driven by rising demand for locally grown produce, controlled-environment agriculture, and increasing adoption of hydroponic and precision farming technologies. |

| Asia-Pacific |

22.4% |

Driven by rising population, food security concerns, expanding horticulture activities, and government support for modern farming methods. |

| Latin America |

9.1% |

Supported by growing export-oriented horticulture production, favorable climatic conditions, and increasing greenhouse adoption for high-value crops. |

| Middle East and Africa |

6.7% |

Driven by increasing demand for water-efficient agriculture and controlled-environment farming in arid regions. |

Europe's 34.2% market leadership is anchored by the Netherlands' dual position as both the most advanced greenhouse production nation and the dominant greenhouse technology exporter. North America's 27.6% reflects Ontario's glass greenhouse cluster and the US cannabis greenhouse investment.

Asia-Pacific's 22.4% encompasses China's world-largest greenhouse area alongside Japan's world-most-advanced plant factory technology. The Middle East and Africa, at 6.7%, is the most commercially dynamic growth region by CAGR.

Competitive Landscape

The global commercial greenhouse market competitive landscape encompasses distinct tiers: greenhouse technology companies, Dutch turnkey project developers, greenhouse structure manufacturers, and commercial greenhouse operators.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Priva |

Priva Nutri-Line, Priva Operator, Priva FS Performance | Market Leader | Priva plays a central role in commercial greenhouses by providing integrated automation systems, software, and hardware that manage climate, irrigation, and energy, enabling year-round production, consistent quality, and resource efficiency. |

|

Ridder |

Hortimax Pro, Hortimax Go, Smartdrive, Syncore | Market Leader | Ridder plays a central role in commercial greenhouses by providing integrated technology solutions that automate climate control, water management, energy efficiency, and labor. |

| Heliospectra | Mitra X family and Elixia family LED Grow Lights | Established Player | Heliospectra plays a central role in commercial greenhouses by providing advanced, dynamic LED lighting systems, software, and sensors designed to maximize crop quality, yield consistency, and energy efficiency. |

Dutch technology cluster concentration creates geographic concentration of greenhouse technology expertise that sustains Dutch companies' global competitive advantage through knowledge spillover and talent market depth unmatched in any other national greenhouse technology cluster. Consolidation reflects greenhouse technology customers' preference for integrated system suppliers, reducing coordination complexity.

Key Company Profiles

Priva

Priva is a leading provider of climate control, automation, and process management solutions for the global commercial greenhouse market. The company specializes in advanced greenhouse technologies and data-driven crop management platforms.

- Key Products: Priva Nutri-Line, Priva Operator, Priva FS Performance.

- Recent Developments: In January 2026, IUNU and Priva formed a partnership that integrates Priva One’s climate execution data with IUNU’s LUNA AI plant-level insights. The collaboration aims to provide commercial greenhouse growers with accurate yield forecasting and crop prognosis capabilities.

- Strategic Focus: Focuses on advanced climate automation, energy-efficient greenhouse solutions, and AI-driven crop management technologies.

Ridder

Ridder is a prominent technology provider in the commercial greenhouse market, specializing in automation, climate control, water management, and labor management solutions for controlled-environment agriculture. The company offers advanced systems for greenhouse process optimization, including irrigation automation, energy management, crop monitoring, and workflow control.

- Key Products: Hortimax Pro, Hortimax Go, Smartdrive, Syncore.

- Recent Developments: In April 2026, Ridder and RED Horticulture entered into a strategic partnership to enhance integration between greenhouse lighting control and energy management systems. The collaboration focuses on adopting the Horticultural Lighting Protocol (HLP), allowing MyRED lighting software to communicate directly with Ridder’s Hortimax Pro climate computer.

- Strategic Focus: Centered on automation, climate optimization, and smart labor management solutions for controlled-environment agriculture.

Market Concentration Analysis

The global commercial greenhouse market is highly fragmented at the crop production tier, with individual commercial greenhouse operators globally creating a market where no single grower holds above 0.5% of global greenhouse production area. Technology suppliers are moderately concentrated. Dutch turnkey project developers collectively manage approximately 40-50% of high-specification international greenhouse project development. Market concentration is increasing at the technology platform tier through M&A.

Investment & Growth Opportunities

Highest Growth Segments

Cooling systems (~8.8% CAGR), gutter-connected greenhouse in Middle East and Asia-Pacific (~12-15% CAGR), LED lighting retrofit and new installation (~10% CAGR), AI climate management software (~18% CAGR from small base), agrivoltaic solar greenhouse (~25% CAGR from near-zero base), cannabis greenhouse conversion to vegetable (~5% CAGR), and urban rooftop greenhouse (~20% CAGR from small base) represent the highest-growth commercial greenhouse investment vectors through 2034.

Emerging Investment Opportunities

The Middle East and African government food security greenhouse investment represents the largest near-term commercial greenhouse opportunity. Greenhouse technology companies and turnkey project developers who establish preferred supplier relationships with GCC food security programme procurement offices are positioned for above-market revenue growth as government disbursement accelerates.

Investment Themes

- Agrivoltaic greenhouse structure investment capturing dual food and energy revenue from a single land area: Agrivoltaic greenhouse combines commercial food production with solar energy generation from the same land area using purpose-designed semi-transparent PV panel greenhouse structures. Companies investing in agrivoltaic greenhouse project development, project financing structures, and installation capability by 2026-2027 are positioned to capture the commercial deployment wave.

- AI greenhouse management platform development for global commercial greenhouse operator subscription revenue: Greenhouse AI climate management has documented a commercial benefit of 15-25% crop yield improvement. A cloud-based AI greenhouse management platform subscription model creates an above-hardware-sale-margin business model sustaining recurring revenue as the greenhouse fleet grows.

Future Market Outlook (2026-2034)

The global commercial greenhouse market is projected to grow from USD 41.3 Billion in 2025 to USD 85.2 Billion by 2034, delivering an 8.12% CAGR over the forecast period. The market's anchor value of USD 61.1 Billion in 2030 represents a commercial greenhouse industry at its most transformative commercial inflection since the Dutch Venlo system standardization, AI crop management will have achieved mainstream commercial deployment replacing conventional setpoint climate management in high-value commercial greenhouse, agrivoltaic greenhouse will have moved from demonstration to commercial construction scale, and the Middle East food security greenhouse investment wave will have created permanent new greenhouse production capacity progressively displacing temperature-climate-vulnerable field production.

Three structural forces define commercial greenhouse market growth through 2034 with exceptional confidence. Food security as a policy imperative across governments spanning the UAE and Saudi Arabia, the United States, China, Japan, and India creates government-backed greenhouse investment demand that is policy-mandated, multi-decade, and budget-committed regardless of commercial market conditions. Climate change creates agricultural risk in field production zones, simultaneously increasing commercial greenhouse's competitive advantage as the only agricultural production system providing weather-independent year-round crop quality consistency. Technology cost reduction is making premium greenhouse technology commercially accessible.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025) including Chief Technology Officers; Business Development Directors; Horticulture LED Directors; commercial greenhouse operator CEOs; and regional greenhouse market specialists.

Secondary Research

Secondary research encompassed greenhouse technology publications; Dutch greenhouse industry data; protected agriculture statistics; Controlled Environment Agriculture report; company annual reports; Agrivoltaic Technology Review; commercial greenhouse industry data; North American market statistics. Over 65 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a segment bottom-up model: (i) greenhouse structure component; (ii) technology component; (iii) services component.

Commercial Greenhouse Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Free-standing Greenhouses, Gutter-connected Greenhouses |

| Material Used Covered |

|

| Technologies Covered | Heating System, Cooling System, Others |

| Crops Covered | Fruits and Vegetables, Flowers and Ornamentals, Nursery Crops, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Priva, Ridder, Heliospectra, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the commercial greenhouse market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global commercial greenhouse market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the commercial greenhouse industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Commercial Greenhouse Market Report

The global commercial greenhouse market reached USD 41.3 Billion in 2025. The market is driven by rising demand for year-round crop production, increasing food security concerns, and the growing adoption of controlled-environment agriculture technologies. Advancements in automation, hydroponics, LED lighting, and climate control systems, along with the need for efficient land and water utilization, are further supporting market growth.

The market grows at 8.12% CAGR during 2026-2034, reaching USD 85.2 Billion by 2034. Cooling systems grow fastest at ~8.8% CAGR through geographic expansion into hot climate regions and climate change, creating cooling retrofit demand in historically temperate regions.

Gutter-connected greenhouses lead at 58.6% through commercial efficiency advantages, shared gutter construction reducing material cost, connected internal logistics enabling mechanised transport, and energy efficiency from reduced external wall exposure.

Heating systems lead at 44.9% through the foundational role of heat management in enabling year-round crop production in the Netherlands, Canada, Germany, and Scandinavia.

Europe leads at 34.2% through the Netherlands' global greenhouse technology dominance and Spain's Almeria greenhouse production area.

Leading companies include Priva, Ridder, and Heliospectra, among others.

The market is projected to reach approximately USD 61.1 Billion by 2030, with AI greenhouse management achieving commercial mainstream adoption in Dutch and Canadian premium greenhouse, agrivoltaic greenhouse commercial deployment scaling in California and Netherlands, Middle East food security greenhouse investment at peak annual deployment velocity as targets approach, robotic harvesting commercial validation for at least one major crop, and cannabis greenhouse conversions to premium vegetable production creating productive fleet reconfiguration in North American cannabis states with mature markets.

Agrivoltaic greenhouse combines commercial crop production beneath semi-transparent photovoltaic solar panels mounted on the greenhouse roof structure, the panels generating renewable energy while crops grow in the spectrally filtered light transmitted through the panels. The commercial case combines food production revenue with renewable energy revenue from an identical land area.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade