Compound Semiconductor Market Size, Share, Trends and Forecast by Type, Product, Deposition Technology, Application, and Region, 2026-2034

Compound Semiconductor Market Size and Share:

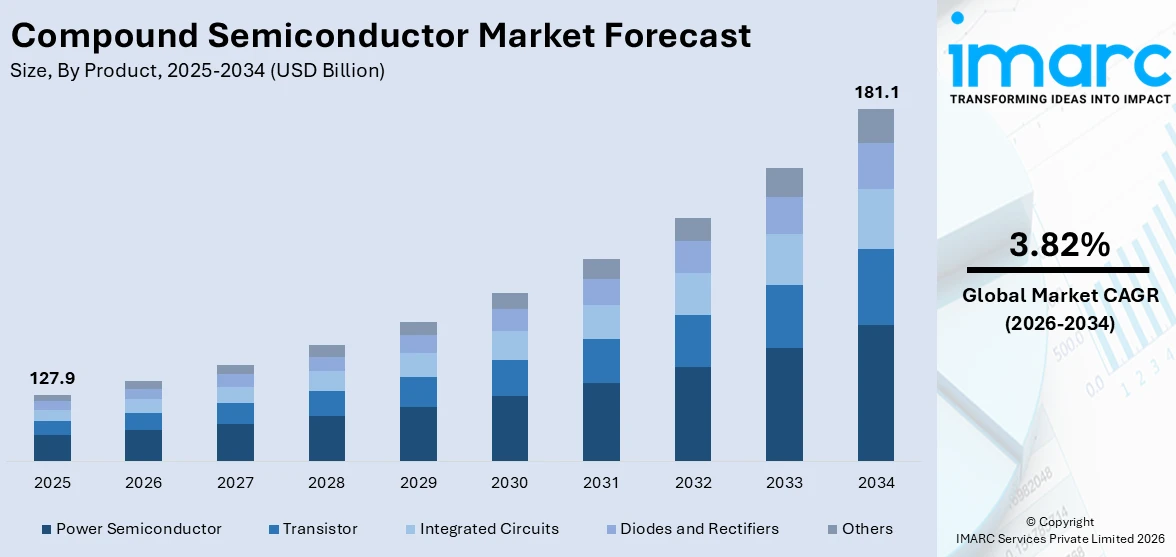

The global compound semiconductor market size was valued at USD 127.9 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 181.1 Billion by 2034, exhibiting a CAGR of 3.82% from 2026-2034. Asia pacific currently dominates the market, holding a market share of over 61.2% in 2025. The need for high-speed electronics, 5G communication, and power-efficient devices, automotive advancements, LED lighting adoption, and emerging applications, including IoT and renewable energy technologies, are propelling the market growth in Asia Pacific.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 127.9 Billion |

|

Market Forecast in 2034

|

USD 181.1 Billion |

| Market Growth Rate 2026-2034 | 3.82% |

The global compound semiconductor market is witnessing notable expansion primarily due to innovations in high-power and high-frequency applications, fostered by magnifying requirement for exceptional-speed electronics, 5G communication, and IoT devices. The rapid inclination toward renewable energy solutions and electric vehicles (EVs) has further magnified the demand for energy-saving semiconductors, including silicon carbide (SiC) and gallium nitride (GaN). For instance, according to the International Energy Agency, electric vehicle sales in markets outside the primary EV hubs are projected to surpass 1 million units in 2024, reflecting a substantial growth of over 40% compared to the sales figures recorded in 2023. Furthermore, expansion in the automotive industry, especially in ADAS systems and EVs, is also impacting the market growth substantially. In addition, the extensive utilization of LED technology in numerous key sectors and advancements in optoelectronic devices are further boosting the market expansion globally.

To get more information on this market Request Sample

The United States holds a significant position in the global compound semiconductor market, driven by advancements in defense technologies, telecommunications, and the automotive industry. The adoption of 5G networks and increasing demand for high-speed, power-efficient electronics are accelerating the use of compound semiconductors in various applications. In addition, key sectors, such as aerospace and renewable energy, also contribute to the market's growth, leveraging these materials for their superior performance and reliability. For instance, in November 2024, the U.S. Commerce Department finalized approximately USD 60 million in government subsidies, allocating funds to BAE Systems (BAESF) for the production of chips utilized in jets and satellites, and to Rocket Lab (RKLB) for the development of compound semiconductors designed for satellites and spacecraft. Moreover, with substantial investments in research and development, the U.S. continues to innovate, fostering a competitive edge in the global landscape of compound semiconductors.

Compound Semiconductor Market Trends:

High-frequency Communication and 5G Networks

The National Library of Medicine reports of 2021 shows that the 5G network is projected to reach 40 percent population coverage and 1.9 Billion subscriptions by the end of 2024. The rise of high-speed, high-capacity communication systems is a crucial step in the establishment of compound semiconductors. Due to the establishment of 5G infrastructure around the world, these semiconductors operate at high frequencies and offer a substantial imperial value addition possibility for the supplier. According to Ericsson Mobility Report, the build-out of 5G continues, with around 320 networks launched worldwide. Global 5G population coverage is expected to reach 55 percent by 2024. Outside mainland China it is projected to increase from 45 percent in 2024 to about 85 percent in 2030. Additionally, the growth of the market is supported by compound semiconductors like gallium nitride (GaN) and gallium arsenide (GaAs), which are displacing elemental semiconductors such as silicon that are unstable at significant frequencies due to their elemental characteristics. Furthermore, the rising employment of GaN in 5G base stations, radar systems, and satellite communication equipment due to its high electron mobility and robust power handling capabilities is strengthening the compound semiconductor market growth.

Power Electronics and Energy Efficiency

As per the International Energy Agency, the global investment in energy efficiency reached USD 560 Billion in 2022, an increase of 16% on 2021. The heightening emphasis on energy saving and the notable inclination towards renewable energy sources are some of the crucial factors bolstering the need for compound semiconductors. For high-voltage and extreme temperature applications, materials including silicon-based semiconductors have certain drawbacks. However, silicon carbide with exceptional thermal conductivity and improved breakdown voltage aid in fostering more effective energy conversion and reducing power losses, which, in turn, is anticipated to fuel the market expansion. Furthermore, SiC is rapidly being employed in both fuel-cell and electric vehicles, as well as in industrial motor and solar inverters to significantly reduce energy consumption and boost sustainability, thereby accelerating the expansion of the compound semiconductor market globally.

Growing Demand for LiDAR

The IMARC Group’s report shows that the global LiDAR market size reached USD 2.6 Billion in 2023. LiDAR technology, which typically utilizes laser light sources to measure distances with high accuracy, is gaining momentum in numerous high-resolution applications, including environmental assessment, autonomous vehicles, and industrial automation. Compound semiconductors, which are mainly integrated with materials such as indium phosphide (InP) and gallium nitride (GaN), are critical components in the manufacturing of optimum-performance and effective laser diodes leveraged in LiDAR systems. In addition, as LiDAR systems are advancing to be useful in major sectors, there is an elevation in the requirement for cutting-edge semiconductor materials that have a better power output, can function at extreme temperatures and are more dependable. Compound semiconductors exhibit all these characteristics, resulting in rising adoption of this technology in the upcoming generation of LiDAR systems.

Compound Semiconductor Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global compound semiconductor market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, product, deposition technology, and application.

Analysis by Type:

- III-V Compound Semiconductor

- Gallium Nitride

- Gallium Phosphide

- Gallium Arsenide

- Indium Phosphide

- Indium Antimonide

- II-VI Compound Semiconductor

- Cadmium Selenide

- Cadmium Telluride

- Zinc Selenide

- Sapphire

- IV-IV Compound Semiconductor

- Others

III-V compound semiconductor stand as the largest component in 2025, holding around 26.4% of the market. III-V compound semiconductors, such as gallium nitride, gallium phosphide, gallium arsenide, indium phosphide, and indium antimonide, are in high demand. They are required because of the unique material characteristics that allow breakthroughs in niche markets. GaN's exceptional power handling capabilities are driving innovations in high-power electronics, RF amplifiers, and 5G infrastructure. GaAs' high electron mobility supports high-speed devices for wireless communication and aerospace applications, thereby impelling the market growth. Similarly, InP is a fundamental material for high-speed optical communication systems since InSb is used in infrared detectors for thermal imaging. The exclusive performance of these specialized applications relies on III-V compound semiconductors.

Analysis by Product:

- Power Semiconductor

- Transistor

- Integrated Circuits

- Diodes and Rectifiers

- Others

Power semiconductor leads the market with around 25.2% of market share in 2025. As per IMARC Group’s report the global power semiconductor market reached USD 43.1 Billion in 2023. The surging demand for power compound semiconductors, such as silicon carbide (SiC) and gallium nitride (GaN), due to their transformative impact on energy efficiency and power electronics is one of the main drivers of the market. Additionally, SiC's high thermal conductivity and breakdown voltage enhance energy conversion in EVs, renewable energy systems, and industrial equipment. GaN's high electron mobility enables compact and efficient power supplies, contributing to smaller form factors in consumer electronics and EV charging systems. As industries seek enhanced performance, reduced energy losses, and greater power density, power compound semiconductors are emerging as crucial enablers, propelling their adoption across a spectrum of applications, aiding in market expansion.

Analysis by Deposition Technology:

- Chemical Vapor Deposition

- Molecular Beam Epitaxy

- Hydride Vapor Phase Epitaxy

- Ammonothermal

- Atomic Layer Deposition

- Others

Chemical vapor deposition leads the market with around 23.7% of market share in 2025. According to IMARC Group’s report, the global chemical vapor deposition (CVD) market is anticipated to reach USD 58.3 Billion by 2032. CVD provides superior uniformity and accuracy in depositing thin film materials, requisite for premium compound semiconductors, which, in turn, is bolstering the market expansion. Moreover, it aids a comprehensive range of materials and is compatible with several substrates, establishing it as a highly adaptable method. In addition to this, CVD's excellent effectiveness and scalability in mass production position it as an ideal option for manufacturers, fulfilling the demand for compound semiconductors in various applications such as electronics, optoelectronics, and photovoltaics.

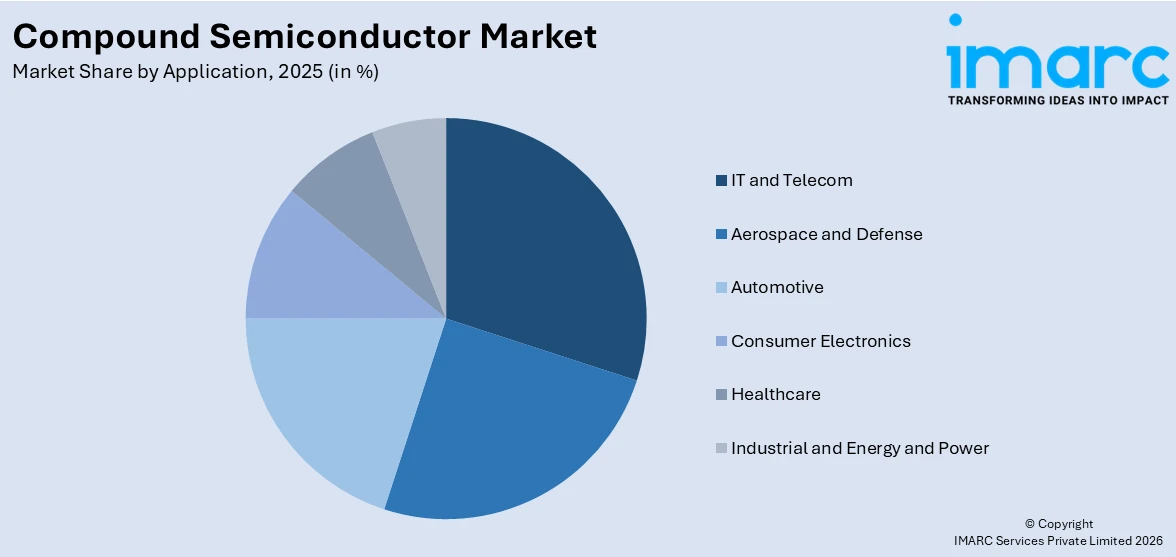

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- IT and Telecom

- Aerospace and Defense

- Automotive

- Consumer Electronics

- Healthcare

- Industrial and Energy and Power

IT and telecom lead the market with around 22.2% of market share in 2025. The utilization of compound semiconductors in the IT and telecom sector is propelled by their capacity to meet the escalating demand for high-speed data transmission, networking, and wireless communication. These materials, such as gallium nitride (GaN) and indium phosphide (InP), enable the creation of high-frequency, high-efficiency devices critical for 5G infrastructure, satellite communication, and broadband expansion, fueling their adoption across various applications in the IT and telecom industry. GaN's superior power handling characteristics enhance the performance of RF amplifiers and base stations, while InP's exceptional optical properties drive advancements in optical communication systems. As the sector continues to seek faster and more reliable connectivity, compound semiconductors play an integral role in enabling the next era of information exchange and digital transformation.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

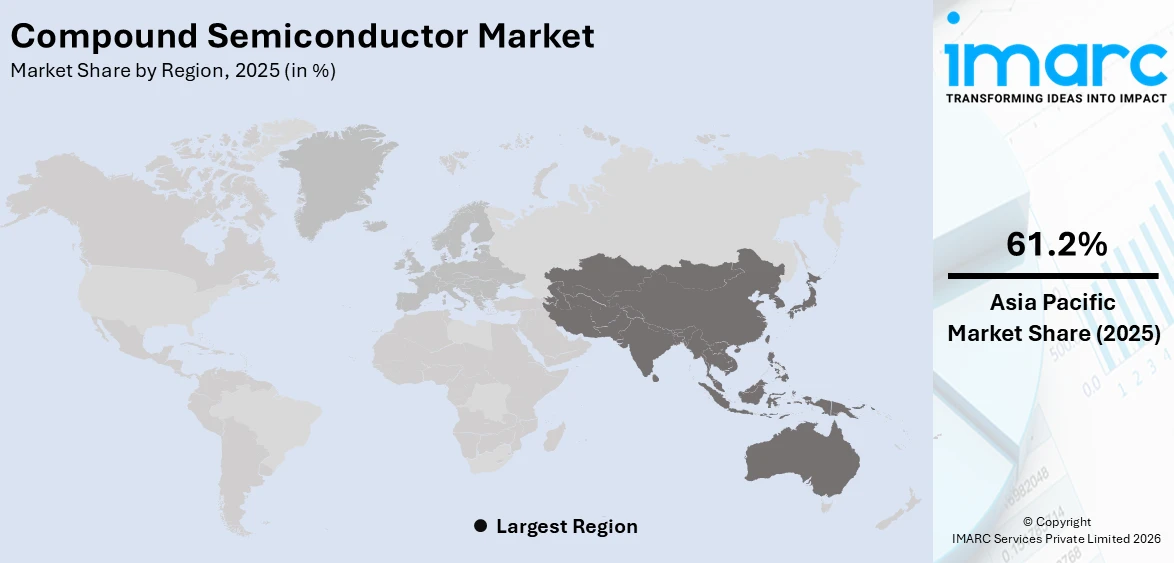

In 2025, Asia Pacific accounted for the largest market share of over 61.2%. Asia-Pacific is a dominant player in the compound semiconductor market, driven by its robust electronics manufacturing sector and government-backed initiatives to develop renewable energy and 5G networks. According to IRENA, the solar photovoltaic energy capability in the South Asian country of India peaked at over 62.8 gigawatts in 2022, up 21.5% from the previous year. China, Japan, South Korea, and Taiwan lead the region in compound semiconductor production and innovation, with their expanding 5G networks and EV adoption contributing to market growth. China, in particular, is heavily investing in semiconductor localization and renewable energy projects, such as solar and wind power plants. Meanwhile, Japan and South Korea are advancing their EV and 5G infrastructure, while India is emerging as a hub for semiconductor production under its "Make in India" initiative. The increasing deployment of renewable energy systems and the growing focus on smart cities across the region are expected to further boost the market. According to the GSMA's Mobile Economy Asia Pacific 2024 report, countries such as Australia, Japan, New Zealand, Singapore, and South Korea are expected to have 5G accounting for a substantial portion of their total mobile connections. Notably, South Korea is anticipated to achieve a 5G adoption rate exceeding 60%, underscoring the region's rapid embrace of advanced mobile technologies.

Key Regional Takeaways:

United States Compound Semiconductor Market Analysis

The United States accounts for 87% of the market share in North America. The compound semiconductor market in the United States is experiencing rapid growth, fueled by advancements in renewable energy, 5G technology, and electric vehicle (EV) adoption. The U.S. government and private sectors are heavily investing in clean energy projects, with compound semiconductors being integral in energy management and smart grid integration. The U.S. is also leading the global 5G rollout, with a focus on mid-band and millimeter-wave spectrum, which is expected to significantly boost the semiconductor industry. According to the CTIA's 2023 Annual Survey, nearly 40% of all wireless devices including phones, smartwatches, and IoT devices now have a 5G connection, marking a 34% increase over 2022. The increasing adoption of EVs, supported by federal incentives and initiatives to expand charging infrastructure, is further driving demand for compound semiconductors. Additionally, domestic manufacturing and the localization of chip production under programs like the CHIPS Act are set to create significant growth opportunities for the compound semiconductor market in the U.S.

Europe Compound Semiconductor Market Analysis

One of the key drivers for the compound semiconductor market in Europe is the European Commission's strategic investment initiatives, including the allocation of up to EUR 1.75 Billion for industry research and innovation, expected to attract an additional EUR 6 Billion in private investments. This significant funding is aimed at accelerating technological advancements and fostering market adoption of compound semiconductors. Moreover, Europe's ambition to increase its global semiconductor market share from 9% to 30% by 2030 underscores the region's commitment to becoming a global leader in semiconductor manufacturing. The establishment of the European alliance on microelectronics, involving major chipmakers, automotive manufacturers, and telecom companies, further bolsters the region's semiconductor ecosystem. Additionally, the goal to produce at least one-fifth of the world’s chips and microprocessors by value is driving substantial innovation and market growth opportunities, positioning Europe as a hub for cutting-edge compound semiconductor technologies.

Latin America Compound Semiconductor Market Analysis

The Latin American compound semiconductor market is driven by the region's increasing integration into the global microelectronics industry and the localization of manufacturing capabilities within its growing electronics markets. The demand for microcomponents has seen steady growth, fueled by the rising need for cloud storage and data centers, as well as the expanding penetration of internet and communication devices. Additionally, industries in Latin America are adopting advanced technologies, including compound semiconductors, to develop green technology products such as LEDs and solar cells, aligning with sustainability goals. The emergence of IoT applications and the growth of autonomous products further support market expansion, creating significant opportunities for innovation and investment in the region.

Middle East and Africa Compound Semiconductor Market Analysis

The compound semiconductor market in the Middle East and Africa (MEA) region is witnessing substantial growth, driven by advancements in renewable energy, telecommunications, and electric vehicle (EV) infrastructure. Key countries like Saudi Arabia, Egypt, and the UAE are implementing extensive renewable energy programs, with compound semiconductors playing a pivotal role in managing energy generation and network integration. Initiatives like Saudi Arabia’s Semiconductor Program, launched by KACST in 2022, underscore the region’s focus on fostering research, development, and local manufacturing capabilities in electronic chip design. Furthermore, the rapid deployment of 5G across the region, led by Gulf nations, is supported by government-backed spectrum access, with mid-band 5G projected to contribute $16 Billion to the MENA region's GDP by 2030, according to GSMA. In South Africa, MTN's $42.25 Million investment in 5G expansion highlights similar progress. Meanwhile, Dubai’s ambitious "Smart Dubai" initiative aims to expand EV infrastructure and achieve a clean energy target of 75% by 2050. Projects like the world’s largest concentrated solar plant and incentives for EV adoption further bolster demand for compound semiconductors, creating a favorable outlook for the market.

Competitive Landscape:

The global compound semiconductor market features a competitive landscape characterized by the presence of key players focusing on innovation, technological advancements, and strategic collaborations. Companies are investing heavily in research and development to enhance product performance and cater to diverse applications in telecommunications, automotive, aerospace, and consumer electronics. Moreover, market leaders are leveraging partnerships and acquisitions to expand their portfolios and strengthen their market position. Furthermore, the rise of emerging players is intensifying competition through cost-effective manufacturing and innovative product offerings. Additionally, strategic geographic expansions and targeted marketing efforts are enabling companies to tap into high-growth regions, ensuring sustained competitiveness in a dynamic and evolving market. For instance, in September 2024, India and U.S. entered into a strategic partnership for the development of a multi-material semiconductor fabrication unit in Uttar Pradesh, India. The upcoming firm will manufacture chips for cutting-edge warfare technologies, including space sensors, electric vehicles, drones, night vision devices, and many more.

The report provides a comprehensive analysis of the competitive landscape in the compound semiconductor market with detailed profiles of all major companies, including:

- Infineon Technologies AG

- Microchip Technology Inc.

- Mitsubishi Electric Corporation

- Nexperia

- NXP Semiconductors

- Onsemi (Semiconductor Components Industries, LLC)

- Qorvo Inc.

- STMicroelectronics

- Texas Instruments Incorporated

- Wolfspeed Inc.

Latest News and Developments:

- October 2024: Bharat Electronics Limited (BEL) and Bharat Semiconductor (3rdiTech) signed a Memorandum of Understanding (MoU) to establish India's first compound semiconductor fabrication plant.

- June 2024: ROHM Semiconductor introduced the EcoSiC™ brand, expanding its 'Power Eco Family' to include silicon carbide (SiC) products. This initiative follows the 2022 launch of EcoGaN™, which focuses on gallium nitride (GaN) devices. ROHM plans to further enhance this family by incorporating high-performance silicon products in the future.

- August 2022: Qorvo, Inc confirmed the release of the highest gain 100-watt L-band (1.2-1.4 GHz) compact solution. It is a GaN-on-SiC PAM aimed for commercial and defense radar applications that provides an integrated two-stage amplifier solution with enhanced efficiency. This exceptional performance cuts total system power usage dramatically.

- August 2022: Infineon Technologies AG entered into a multi-year supply agreement with II-VI Incorporated for wafers. This acquisition of additional access to this vital semiconductor material aims to meet the substantial increase in customer demand in this industry. Furthermore, the deal complements Infineon Technologies AG's approach to multi-sourcing and enhances the resilience of its supply chain.

- August 2022: Infineon Technologies AG and II-VI Incorporated signed a multi-year supply deal for SiC wafers to fulfill the significant rise in customer demand in this sector.

Compound Semiconductor Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Products Covered | Power Semiconductor, Transistor, Integrated Circuits, Diodes and Rectifiers, Others |

| Deposition Technologies Covered | Chemical Vapor Deposition, Molecular Beam Epitaxy, Hydride Vapor Phase Epitaxy, Ammonothermal, Atomic Layer Deposition, Others |

| Applications Covered | IT And Telecom, Aerospace and Defense, Automotive, Consumer Electronics, Healthcare, Industrial and Energy, and Power |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Infineon Technologies AG, Microchip Technology Inc., Mitsubishi Electric Corporation, Nexperia, NXP Semiconductors, Onsemi (Semiconductor Components Industries, LLC), Qorvo Inc., STMicroelectronics, Texas Instruments Incorporated, Wolfspeed Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the compound semiconductor market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global compound semiconductor market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the compound semiconductor industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Compound Semiconductor Market Report

Compound semiconductors are materials formed by combining two or more elements, typically from groups III and V or II and VI of the periodic table. Renowned for superior electrical, optical, and thermal properties, they are integral to advanced applications in telecommunications, optoelectronics, and high-speed electronic devices.

The global compound semiconductor market was valued at USD 127.9 Billion in 2025.

IMARC estimates the global compound semiconductor market to exhibit a CAGR of 3.82% during 2026-2034.

The market is driven by increasing demand for high-performance electronics, advancements in 5G technology, growing adoption in renewable energy systems, and expanding applications in automotive and aerospace sectors. Enhanced efficiency, superior thermal management, and rising investments in research and development further support market growth.

In 2025, III-V compound semiconductor represented the largest segment by type, driven by its superior electronic and optical properties, along with its extensive use in high-speed devices, lasers, and LEDs.

Power semiconductor leads the market by product, driven by its critical role in energy-efficient power management and conversion.

The chemical vapor deposition is the leading segment by deposition technology, driven by its ability to produce high-quality, uniform thin films, along with its scalability, precision in material layering, and efficiency in large-scale production.

The IT and telecom are the leading segment by application, driven by the rising deployment of 5G technology, demand for high-speed data transmission, and advancements in wireless communication systems.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, wherein Asia Pacific currently dominates the global market.

Some of the major players in the global compound semiconductor market include Infineon Technologies AG, Microchip Technology Inc., Mitsubishi Electric Corporation, Nexperia, NXP Semiconductors, Onsemi (Semiconductor Components Industries, LLC), Qorvo Inc., STMicroelectronics, Texas Instruments Incorporated, Wolfspeed Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)