Computational Fluid Dynamics Market Size, Share, Trends and Forecast by Deployment Model, End-User, and Region 2026-2034

Global Computational Fluid Dynamics Market Size, Share, Trends & Forecast (2026-2034)

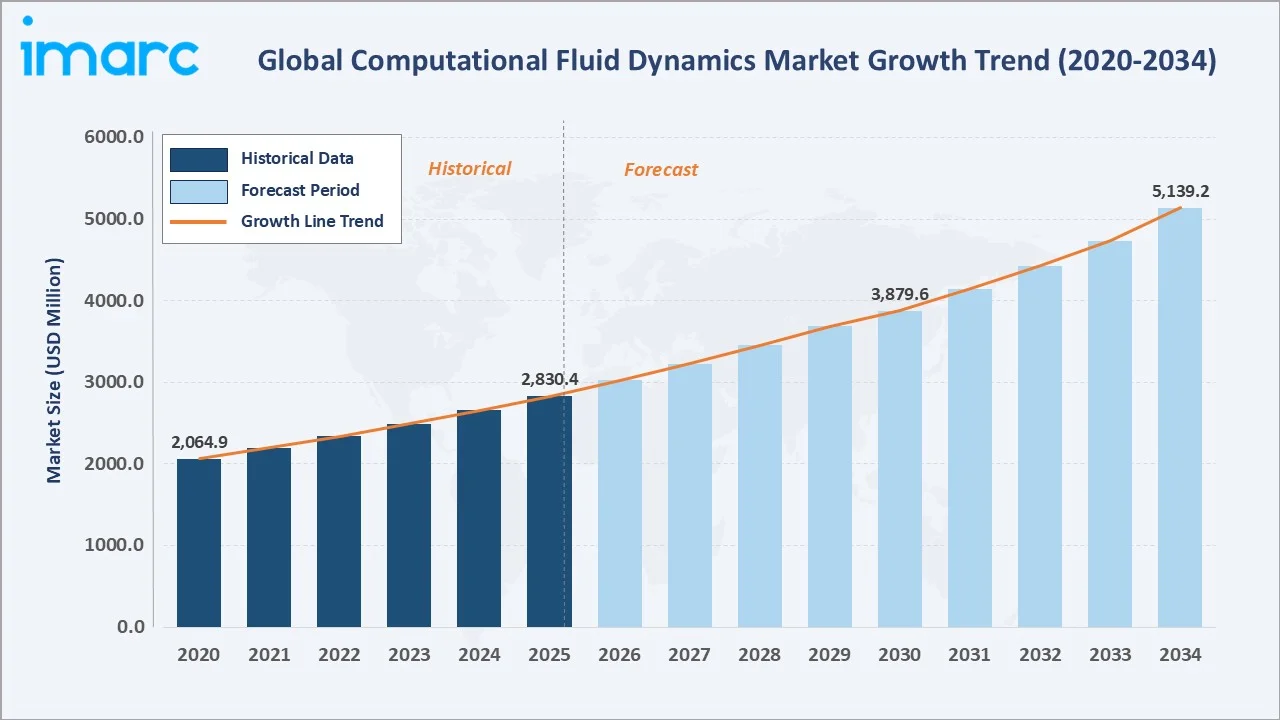

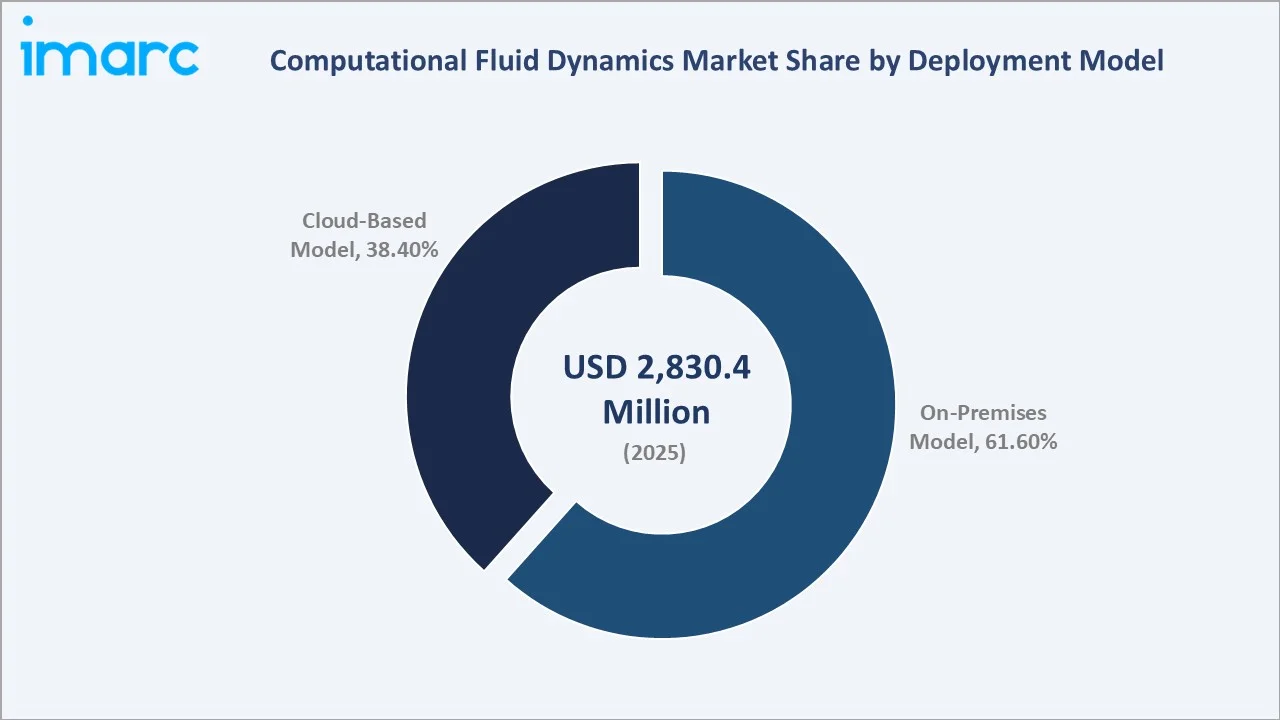

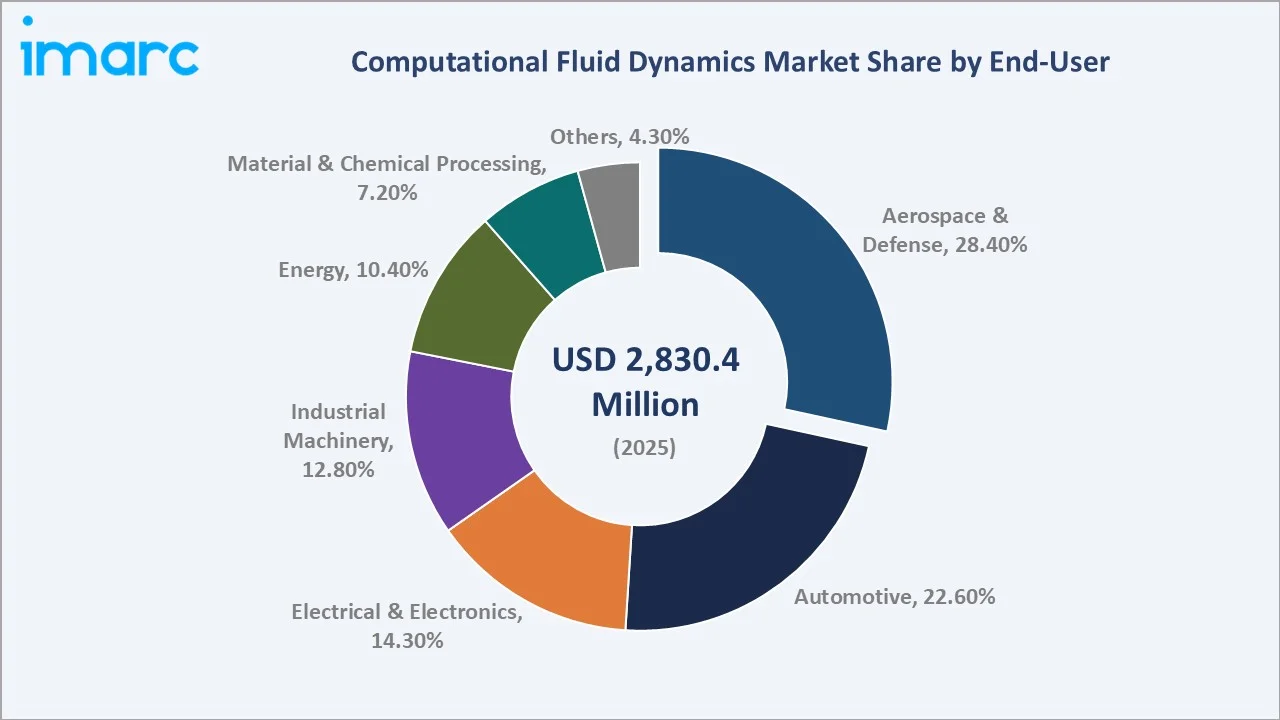

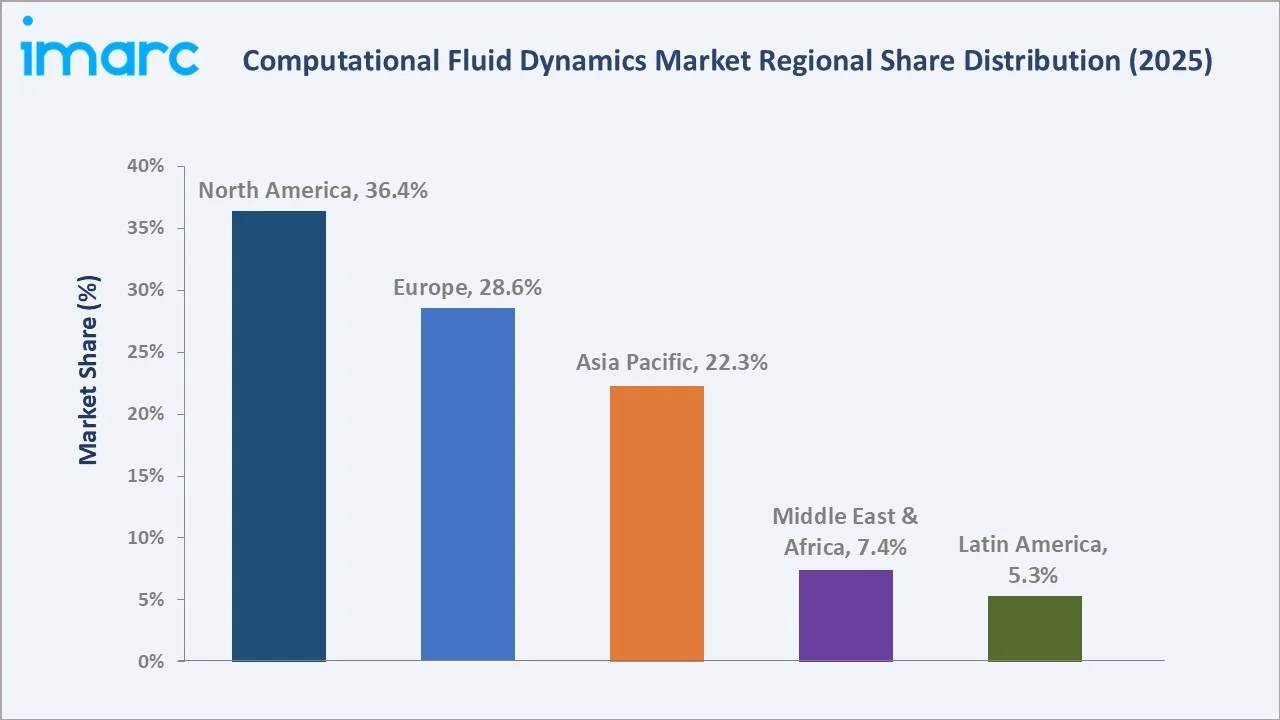

The global computational fluid dynamics (CFD) market was valued at USD 2,830.4 million in 2025 and is projected to reach USD 5,139.2 million by 2034, expanding at a CAGR of 6.5% during the forecast period (2026-2034). Growth is driven by the rising adoption of digital simulation across aerospace, automotive, and energy sectors. 24% of aerospace and defense companies are focusing on digital twins to enhance operations across the entire product lifecycle, with another 50% planning to implement them within the next 1 to 2 years. On-premises deployment leads with 61.6% market share (2025), while aerospace and defense remains the largest end-user at 28.4%. North America dominates with 36.4% revenue share (2025).

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2,830.4 Million |

|

Forecast Market Size (2034) |

USD 5,139.2 Million |

|

CAGR (2026-2034) |

6.5% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.4%, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~8.4%, 2026-2034) |

The computational fluid dynamics market from 2020 through 2034 expanded from USD 2,064.9 Million in 2020 to USD 2,830.4 Million in 2025, anchored at USD 3,879.6 Million in 2030 before reaching USD 5,139.2 Million by 2034.

To get more information on this market, Request Sample

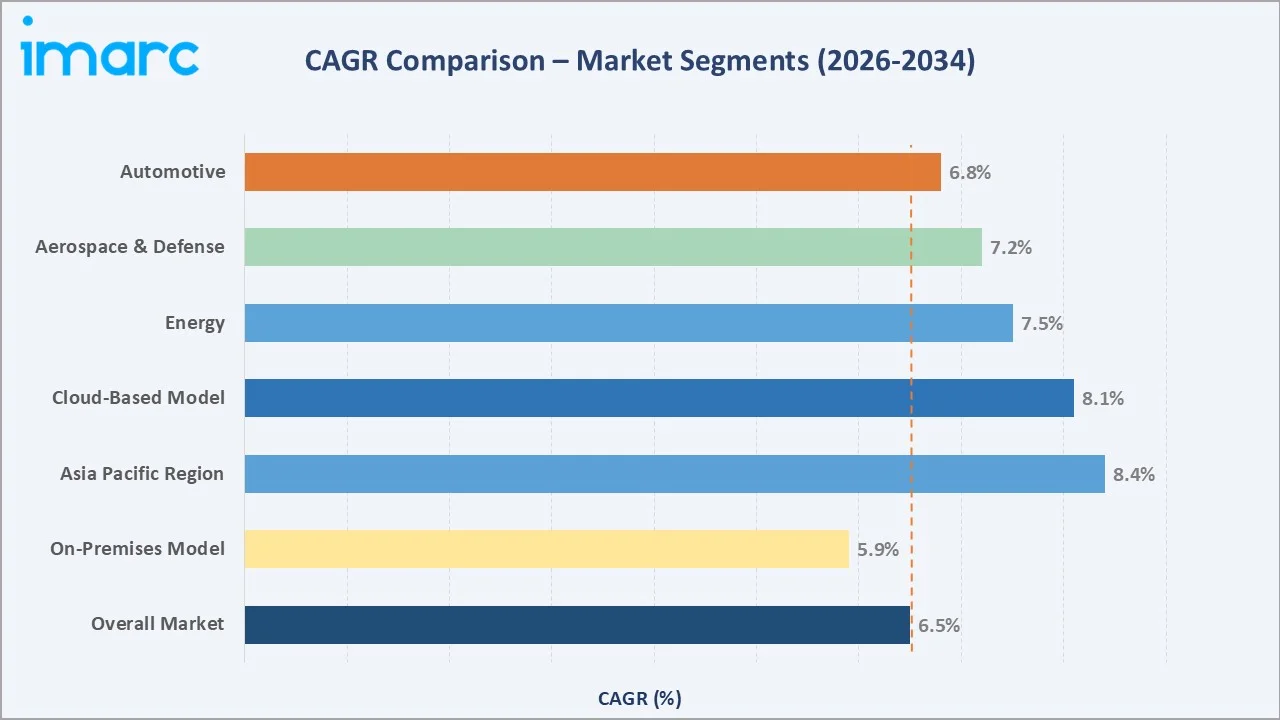

The overall market CAGR is 6.5%, the on-premises model segment is growing at a CAGR of 5.9%, the cloud-based model is growing at a CAGR of 8.1%, the aerospace & defense segment is growing at a CAGR of 7.2%, and the APAC region is growing at 8.4% CAGR.

Executive Summary

The global CFD market continues its strong upward trajectory, underpinned by rapid industrial digitization and growing reliance on virtual prototyping. Valued at USD 2,830.4 million in 2025, the market is set to reach USD 5,139.2 million by 2034 at a 6.5% CAGR. The convergence of AI-enabled mesh generation, cloud HPC resources, and digital twin frameworks is redefining how engineers simulate fluid behavior across complex multi-physics environments.

On-premises deployment commands the largest share at 61.6% (2025), driven by data sensitivity requirements in defense and aerospace. However, cloud-based CFD is the fastest growing model, projected at ~8.1% CAGR through 2034, as SaaS vendors lower the barrier to entry for mid-market engineering firms. Aerospace and defense leads end-user demand at 28.4% (2025), followed by automotive at 22.6%, reflecting growing virtual wind tunnel and crash simulation adoption.

North America holds market leadership with 36.4% revenue share (2025), backed by dense aerospace primes and substantial federal R&D budgets. Europe follows at 28.6%, driven by Airbus, BMW, and EU Horizon research programs. Asia Pacific is the fastest growing region, with China, India, and Japan investing heavily in aeronautical, automotive, and energy simulation capabilities through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Deployment Model |

On-Premises Model – 61.6% share (2025) |

|

Largest End-User |

Aerospace & Defense – 28.4% share (2025) |

|

Leading Region |

North America – 36.4% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~8.4%, 2026-2034) |

Key Analytical Observations Supporting The Above Data:

- On-Premises Model commands 61.6% share (2025), reflecting strict data governance requirements in defense, aerospace, and nuclear sectors where classified simulation data cannot reside on public cloud infrastructure.

- Aerospace & Defense leads end-user demand at 28.4% (2025), with NASA, Boeing, Airbus, and Lockheed Martin processing CFD simulation for aerodynamic design validation and turbulence modeling.

- North America dominates with 36.4% market share (2025), supported by the U.S. Department of Defense simulation mandate and aerospace and defense growth, with the aerospace and defense workforce in 2024 exceeded 2.23 million and a dense cluster of aerospace OEMs generating the highest per-seat CFD software spending globally.

Global Computational Fluid Dynamics Market Overview

Computational fluid dynamics is a branch of fluid mechanics that uses numerical methods and algorithms to analyze fluid flow, heat transfer, mass transport, and related phenomena. CFD software enables engineers to simulate and visualize aerodynamic, hydrodynamic, and thermodynamic behavior of products and systems without physical prototyping. The global CFD ecosystem spans HPC infrastructure providers, algorithm developers, platform vendors, pre/post-processing tool suppliers, and end-user industries spanning aerospace, automotive, energy, and electronics.

Applications range from aircraft wing optimization and automotive drag reduction to HVAC system design, combustion modeling, and wind turbine blade optimization. Macroeconomically, rising R&D spending in the global aerospace sector and accelerating EV development programs create sustained baseline demand.

Market Dynamics

To evaluate market opportunities, Request Sample

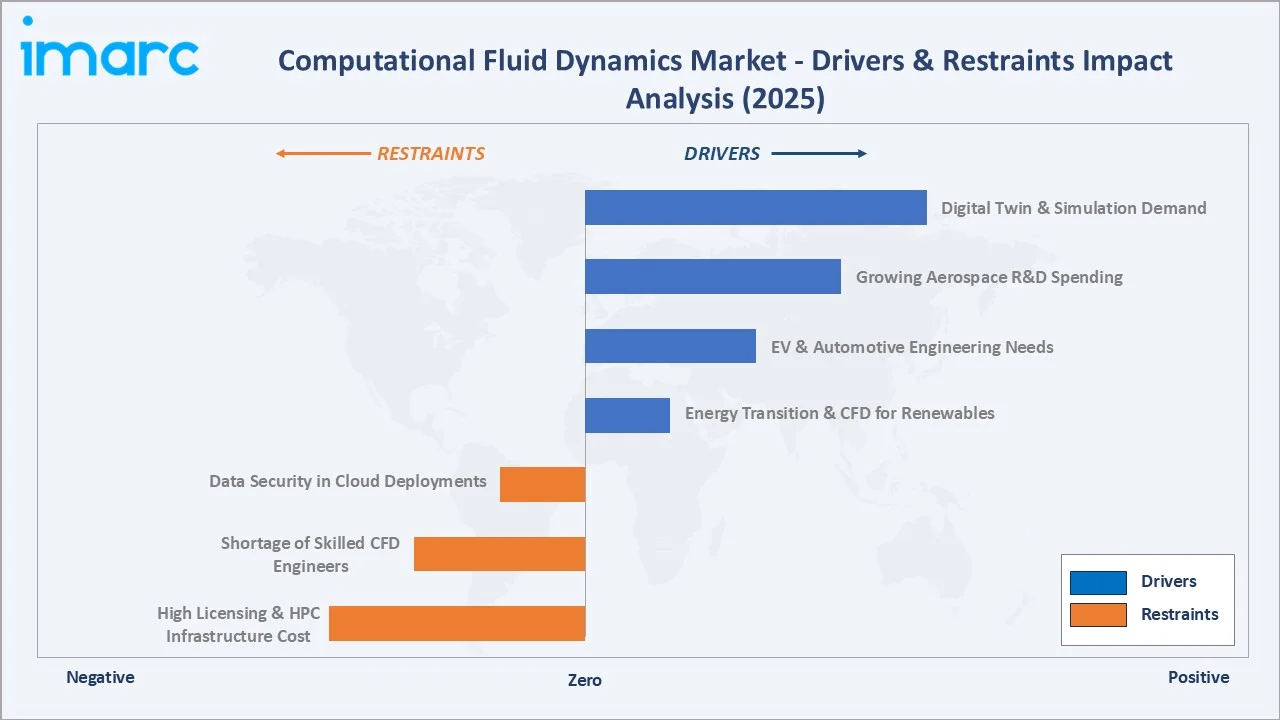

Market Drivers

- Digital Twin & Virtual Prototyping Mandate: Digital Twin, first achieved in the aerospace sector and are more widely used in automotive and aerospace sectors, each requiring high-fidelity CFD as the fluid simulation layer for aerodynamic and thermal behavior modeling.

- Aerospace & Defense R&D Expenditure: India recorded its high defence production of ₹1.54 lakh crore in FY 2024 25, creating a non-discretionary demand stream for commercial CFD licenses.

- EV Aerodynamics and Battery Thermal Management: Electric vehicle range extension targets require 15% aerodynamic drag reduction, achievable only through CFD-intensive design optimization.

Market Restraints

- High Licensing Costs for Enterprise CFD: The high pricing creates a two-tier market where large OEMs dominate deployments while smaller contractors rely on open-source alternatives.

- Shortage of Skilled CFD Engineers: The global shortage of engineers proficient in CFD pre/post-processing hampering the market. Long training cycles of 12–18 months limit the speed of organizational CFD adoption.

- Data Security Concerns in Cloud Deployments: Defense-grade simulation data containing classified aerodynamic profiles cannot be processed on shared cloud infrastructure.

Market Opportunities

- Renewable Energy Design Optimization: With over 1,200 GW of new wind capacity installed globally by 2024, each GW requiring CFD software spend, the addressable opportunity exceeds USD 1.8 billion.

- Emerging Market Manufacturing Growth: The Indian government targets defence manufacturing worth ₹3 lakh crore and defence exports of ₹50,000 crore by 2029 represent high-growth CFD demand pools.

Market Challenges

- Mesh Generation Complexity: Despite advances in automated meshing, irregular geometries such as turbomachinery blades and biomedical implants remain challenging, limiting throughput in engineering workflows.

- Interoperability Between CAD and CFD Platforms: Geometry translation losses between major CAD systems and CFD solvers cause mesh generation failures in industrial projects, increasing iteration costs and reducing engineering team confidence in simulation results.

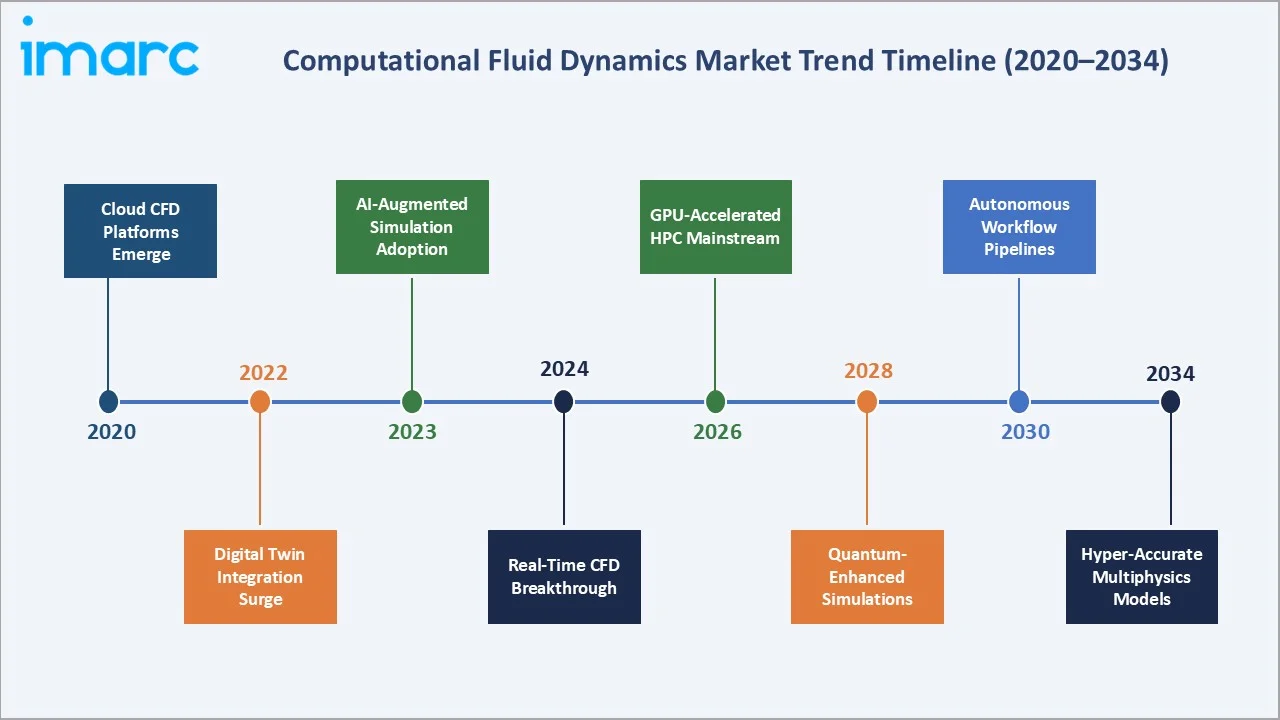

Emerging Market Trends

1. AI and Machine Learning Integration in CFD

Machine learning surrogate models are replacing full CFD runs for parametric design sweeps. ANSYS OptiSLang and NVIDIA Modulus now enable design exploration quickly.

2. Real-Time CFD for Digital Twin Synchronization

Industrial digital twins now require continuous CFD updates synchronized with live sensor data from physical assets. This creates a persistent software revenue stream distinct from traditional one-time licensing.

3. Quantum Computing-Enhanced CFD Exploration

IBM, Google, and Boeing are co-developing quantum algorithms for turbulence modeling that theoretically offer exponential speedup over classical CFD solvers for specific fluid dynamics problems.

4. Open-Source CFD Ecosystem Maturation

Open-source CFD adoption is growing rapidly, driven by the aerospace, academic, and start-up sectors seeking zero-license-cost simulation. This is driving commercial vendors to compete on service, support, and GUI quality rather than solver accuracy alone.

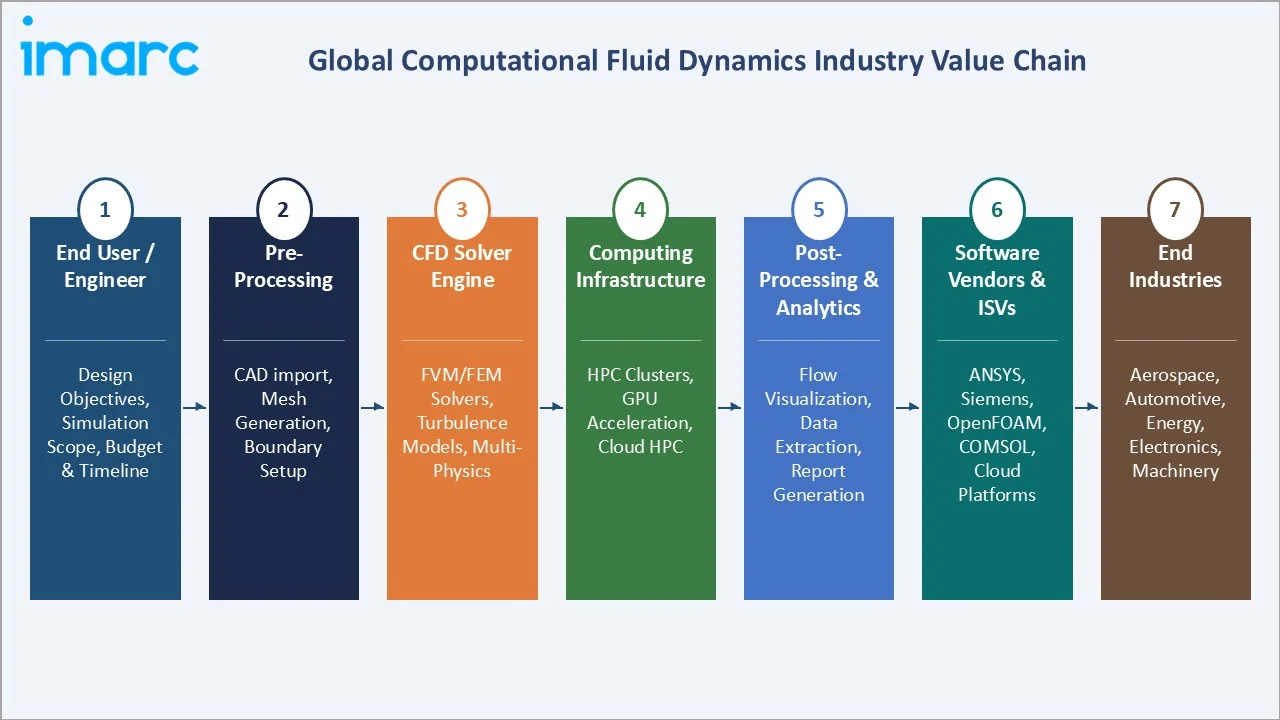

Industry Value Chain Analysis

The CFD industry value chain encompasses six distinct stages from raw computational infrastructure through to end-user engineering outcomes. Each stage involves specialized technical capabilities and creates distinct revenue pools, margin structures, and competitive dynamics.

|

Stage |

Key Players / Examples |

|

HPC & Cloud Infrastructure |

AWS, Microsoft Azure, Google Cloud, NVIDIA |

|

Algorithm & Solver Development |

ANSYS, Siemens |

|

CFD Software Platforms |

ANSYS Fluent, Siemens STAR-CCM+, Dassault SIMULIA |

|

Pre/Post-Processing Tools |

Altair HyperMesh, Pointwise, ParaView |

|

System Integration & Consulting |

Specialized CFD service firms |

|

End Users |

Aerospace OEMs, automotive manufacturers, energy firms, academic labs |

The CFD software platform stage captures the highest margin in the value chain. Pre/post-processing tools and consulting services represent the fastest-growing adjacent revenue streams, with professional services.

Technology Landscape in the CFD Industry

Solver Technology & Numerical Methods

Modern CFD solvers employ finite volume, finite element, and lattice Boltzmann methods to discretize the Navier-Stokes equations across complex geometries. ANSYS Fluent's density-based coupled solver and Siemens STAR-CCM+'s polyhedral meshing deliver convergence rates faster than structured mesh approaches for complex automotive and aircraft geometries.

Cloud & HPC Infrastructure

Cloud HPC has transformed CFD accessibility. At the end of 2021 and the start of 2022, the two leading commercial computational fluid dynamics (CFD) tool providers, Ansys and Siemens, both introduced versions of their flagship CFD software with GPU acceleration support.

AI and Machine Learning Integration

Physics-informed neural networks (PINNs) and convolutional neural network surrogates now enable approximate CFD solutions in milliseconds for parametric geometry variations.

Pre/Post-Processing and Visualization

Advanced meshing tools, including Altair HyperMesh, Pointwise, and ANSYS Fluent Meshing now support automated polyhedral mesh generation with feature-based refinement, reducing manual setup time.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Deployment Model | On-Premises Model | 61.6% | 2025 |

| End-User | Aerospace and Defense | 28.4% | 2025 |

| Region | North America | 36.4% | 2025 |

By Deployment Model

On-premises model dominates with a 61.6% market share (2025). This deployment is preferred by large aerospace primes, defense contractors, and nuclear engineering firms handling classified or proprietary simulation data that cannot transit public cloud networks.

To access detailed market analysis, Request Sample

Cloud-based model holds 38.4% market share (2025) and is growing at ~8.1% CAGR through 2034. Mid-tier automotive suppliers, energy consultancies, and academic institutions are the primary cloud adopters, attracted by zero CAPEX deployment and elastic scaling for peak simulation demand.

By End-User

Aerospace and defense leads with a 28.4% market share (2025). Three CFD solvers used by NASA were employed to generate aerodynamic databases for supporting the launch vehicle design. The segment's growth is further fueled by next-generation aircraft programs including Boeing NMA and Airbus A360 conceptual designs, both requiring extensive high-fidelity turbulence modeling.

Automotive follows at 22.6% (2025), driven by EV aerodynamics and battery thermal management needs. Energy holds 10.4%, with wind turbine wake modeling and nuclear reactor coolant flow simulation as primary applications. Electrical and electronics at 14.3% covers semiconductor thermal management and PCB airflow optimization for next-generation chips.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

36.4% |

DARPA/NASA simulation mandates, aerospace R&D boom, EV design growth |

|

Europe |

28.6% |

Airbus & BMW virtual testing programs, EU Horizon 2025 R&D funding |

|

Asia Pacific |

22.3% |

China Made in China 2025, India aerospace PLI, Japan auto electrification |

|

Middle East & Africa |

7.4% |

Saudi Vision 2030 industrial digitization, energy sector CFD adoption |

|

Latin America |

5.3% |

Petrobras oil & gas simulation, Brazil aerospace expansion (Embraer) |

North America's 36.4% market share (2025) is underpinned by the highest per-seat CFD spending globally. The FY2024 DOD budget requested $37.7 billion for certain programs to upgrade the U.S. nuclear triad for long-range weapon delivery, funding HPC cluster upgrades and commercial license renewals. Canada's NRC aerospace simulation programs and rising start-up activity in air mobility add incremental demand.

Europe's 28.6% share (2025) benefits from Airbus's virtual aircraft development pipeline. Asia Pacific at 22.3% (2025), driven by China's COMAC C919 program. India's DRDO and HAL are scaling CFD capabilities. Japan's Toyota, Honda, and Mitsubishi Heavy Industries operate some of the highest-utilization commercial CFD clusters in the global automotive sector.

Competitive Landscape

The global CFD market is moderately concentrated at the enterprise software tier. ANSYS, Siemens, and Dassault Systèmes collectively control approximately 58–62% of the commercial CFD software market by revenue.

|

Company Name |

Key Brand / Products |

Market Position |

Core Strength |

|

Synopsys, Inc. |

ANSYS Fluent, Ansys CFX, Ansys Rocky, Ansys TurboGrid |

Market Leader |

Largest CFD portfolio, 50,000+ global customers, multi-physics simulation leadership |

|

Siemens AG |

Simcenter STAR-CCM+ |

Market Leader |

End-to-end digital twin integration, strong automotive & aerospace customer base |

|

Dassault Systèmes |

SIMULIA |

Strong Challenger |

3DEXPERIENCE platform synergy, PLM-integrated CFD for aerospace and life sciences |

|

Autodesk |

Autodesk CFD |

Strong Challenger |

SaaS-first architecture, HVAC & building performance CFD, mid-market accessibility |

|

COMSOL AB |

COMSOL Multiphysics |

Specialist Leader |

Unmatched multiphysics coupling, academia leadership, App Builder for custom tools |

|

Convergent Science |

CONVERGE CFD |

Emerging |

Engine combustion CFD leader, adaptive mesh refinement without user input |

|

AVL List GmbH |

AVL FIRE M |

Established |

Hybrid/electric vehicle thermal CFD |

The open-source segment represents an estimated 12–15% of total simulation runs but generates minimal direct revenue. Competitive differentiation is increasingly driven by AI capability, cloud infrastructure partnerships, and integration with broader PLM and digital twin platforms.

Key Company Profiles

Synopsys, Inc.

Synopsys acquired Ansys, the global market leader in engineering simulation software, with CFD as its largest product line by revenue.

- Product Portfolio: ANSYS Fluent, Ansys CFX, Ansys Rocky, Ansys TurboGrid, Ansys EnSight, Ansys Polyflow, Ansys FENSAP-ICE, Ansys Forte, Ansys Vista TF.

- Recent Developments: In July 2025, Synopsys completed its acquisition of Ansys, and in August 2025, Ansys and NVIDIA signed an agreement to license, sell, and support Omniverse technology embedded in Ansys simulation solutions.

- Strategic Focus: AI-first simulation strategy, Synopsys integration for chip-to-system simulation continuity, expanding cloud-native offerings through ANSYS Cloud Direct; mid-market penetration through Startup Program partnerships.

Siemens AG

Siemens operates the Simcenter CFD portfolio, anchored by STAR-CCM+, serving automotive, aerospace, and marine industries globally.

- Product Portfolio: Simcenter STAR-CCM+, Simcenter FLOEFD, Simcenter Flotherm, Simcenter Flotherm XT, Simcenter Battery Design Studio.

- Recent Developments: In December 2025, Siemens released updates to its Simcenter X software, a cloud-based environment that combines simulation and optimization tools in one platform.

- Strategic Focus: Digital twin-centric CFD strategy, automotive electrification simulation, cloud CFD expansion via Xcelerator-as-a-Service, tightening integration with Teamcenter PLM for design-to-simulation traceability.

Dassault Systèmes

Dassault Systèmes operates SIMULIA as its simulation brand, offering PowerFLOW, and XFlow as CFD-specific platforms within the 3DEXPERIENCE environment. The company reported revenues of around EUR 6.0 billion (FY2024) with 3DEXPERIENCE subscriptions growing 14% annually. SIMULIA's Lattice Boltzmann-based PowerFLOW solver is the dominant CFD tool for external automotive aerodynamics globally.

- Product Portfolio: SIMULIA Computational Fluid Dynamics Simulation Software Products includes PowerFLOW and XFlow

- Recent Developments: Integrated cloud rendering for immersive CFD visualization on 3DEXPERIENCE platform, partnered with AWS for automotive aerodynamics-as-a-service.

- Strategic Focus: Life sciences virtual human simulation, automotive aerodynamics leadership via PowerFLOW, expanding SIMULIA into semiconductor and electronics thermal management markets.

Autodesk

Autodesk CFD is the company's primary fluid simulation platform, positioned as a mid-market alternative to enterprise-grade solvers.

- Product Portfolio: Autodesk CFD

- Recent Developments: Integrated AI-powered meshing in Autodesk CFD, launched Autodesk AI for generative design optimization with embedded CFD validation, expanded Fusion 360 Manufacturing cloud CFD for SME market penetration.

- Strategic Focus: SaaS democratization of CFD for non-specialist engineers; Fusion 360 ecosystem lock-in; generative AI-CFD integration for industrial design optimization; HVAC and building performance CFD expansion.

Market Concentration Analysis

The global CFD market exhibits moderate-to-high concentration at the commercial software tier. The top five vendors, Synopsys, Inc, Siemens, Dassault Systèmes, and Autodesk, collectively generate approximately 72–76% of total commercial CFD software revenues. Synopsys, Inc alone commands an estimated 32–34% value share, reflecting its broad product portfolio spanning CFD, FEA, and electromagnetics simulation.

Consolidation activity has intensified. The landmark Synopsys–ANSYS merger signals that electronic design automation and CFD/FEA simulation are converging toward a unified chip-to-system simulation stack. This is expected to trigger further consolidation, with private equity and strategic buyers and specialist niche vendors through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

Cloud-based CFD growing at a CAGR of ~8.1%, AI-enhanced simulation surrogates at a CAGR of ~18%, and real-time digital twin CFD at a CAGR of ~12% represent the three highest-growth investment vectors through 2034. Collectively, these segments address a total incremental revenue pool, with AI-CFD integration attracting the highest venture capital interest globally.

Emerging Market Expansion

India's aerospace PLI scheme creates a first-mover CFD market development opportunity. Saudi Arabia’s NEOM gigacity project and ARAMCO’s digital oilfield programs represent a combined CFD investment pipeline, favoring vendors with regional support infrastructure and Arabic language user interfaces.

Venture Investment Trends

Key investment themes include AI-native CFD platforms, open-source CFD cloud marketplaces, and digital twin-integrated simulation services.

- Key growth bets: AI surrogate model platforms, cloud-native CFD-as-a-Service, and real-time digital twin fluid simulation middleware.

- ESG-aligned investors are targeting CFD vendors with demonstrable renewable energy optimization applications – wind farm wake modeling and hydrogen electrolyzer flow optimization are the most-cited clean tech CFD use cases in 2025 LP presentations.

Future Market Outlook (2026-2034)

The global CFD market is positioned for sustained, high-visibility growth through 2034. From USD 2,830.4 million in 2025, the market is forecast to reach USD 5,139.2 million by 2034, an absolute value addition of USD 2,308.8 million. This expansion is underpinned by four structural forces: industrial digitization mandates, AI-driven simulation acceleration, renewable energy infrastructure build-out, and cloud HPC democratization.

Between 2026 and 2030, the dominant transformation will be the convergence of AI and CFD into unified simulation-optimization platforms. AI surrogate models compressing automotive aerodynamic development cycles from 18 months to 6–8 months. Cloud CFD will surpass on-premises deployment in revenue terms by 2031, as confidential computing advances resolve the remaining data security barriers in defense and pharmaceutical applications.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 160 industry stakeholders in 2025, comprising CFD software executives, HPC infrastructure providers, aerospace and automotive simulation engineers, procurement directors, and financial analysts covering the engineering software sector across North America, Europe, and Asia Pacific. Primary insights validated quantitative market size estimates and identified emerging technology adoption patterns.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, earnings call transcripts, SEC filings, industry databases, government simulation procurement records, trade publications, academic journals, and patent filings across 30+ countries. Over 290 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations were derived using a hybrid bottom-up and top-down methodology. Key input variables include R&D spending trajectories by industry, cloud HPC adoption rates, open-source vs. commercial license ratios, and regional industrial output growth indices.

Computational Fluid Dynamics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Deployment Models Covered | Cloud-Based Model, On-Premises Model |

| End-Users Covered | Automotive, Aerospace and Defense, Electrical And Electronics, Industrial Machinery, Energy, Material And Chemical Processing, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Synopsys, Inc., Siemens AG, Dassault Systèmes, Autodesk, COMSOL AB, Convergent Science, AVL List GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the computational fluid dynamics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global computational fluid dynamics market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the computational fluid dynamics industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Computational Fluid Dynamics Market Report

The global CFD market was valued at USD 2,830.4 million in 2025 and is projected to reach USD 5,139.2 million by 2034, growing at a CAGR of 6.5%.

North America is the dominant region with 36.4% revenue share (2025), supported by U.S. defense simulation mandates and a dense aerospace OEM cluster spending heavily on CFD licenses.

Asia Pacific is the fastest growing region (CAGR ~8.4%), driven by China's COMAC program, India's aerospace PLI, and Japan's automotive electrification simulation investments.

Key drivers include digital twin adoption, aerospace R&D mandates, EV aerodynamic optimization requirements, cloud HPC cost reduction, and AI-accelerated simulation.

On-Premises Model dominates with 61.6% market share (2025), preferred by defense and aerospace firms with classified data requirements that prevent public cloud deployment.

Aerospace and Defense leads with 28.4% market share (2025), driven by FAA/EASA CFD certification mandates and massive simulation investments in next-generation aircraft development.

The leading companies include Synopsys, Inc., Siemens AG, Dassault Systèmes, Autodesk, COMSOL AB, Convergent Science, and AVL List GmbH.

Key trends include AI surrogate CFD models (18% CAGR), cloud-native CFDaaS platforms, real-time digital twin CFD, quantum-classical hybrid solvers, and open-source ecosystem maturation.

Key challenges include high enterprise license costs, a global shortage of 180,000 skilled CFD engineers, mesh generation complexity, and cloud data security barriers for defense applications.

High-growth opportunities include AI-native CFD platforms, cloud-based CFDaaS, wind farm wake optimization, India aerospace simulation infrastructure, and real-time digital twin fluid simulation middleware through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)