Construction Robots Market Size, Share, Trends and Forecast by Type, Automation, Function, Application, and Region 2026-2034

Global Construction Robots Market Size, Share, Trends & Forecast (2026-2034)

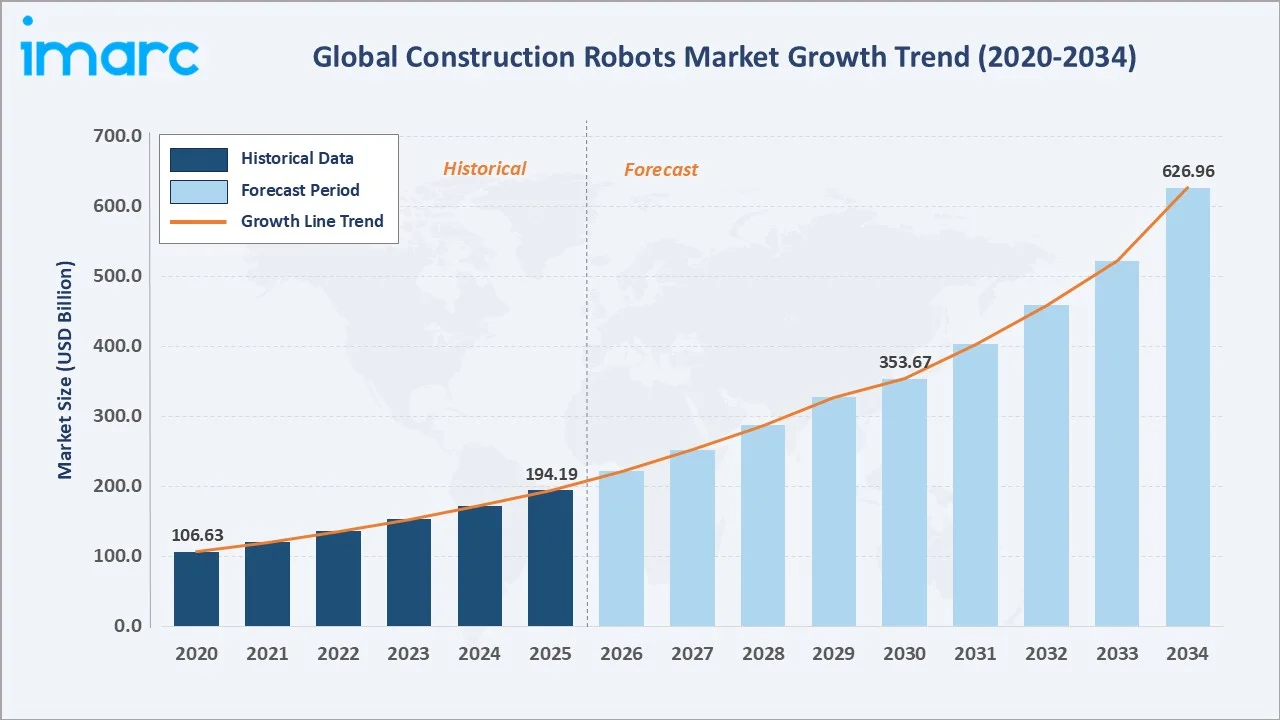

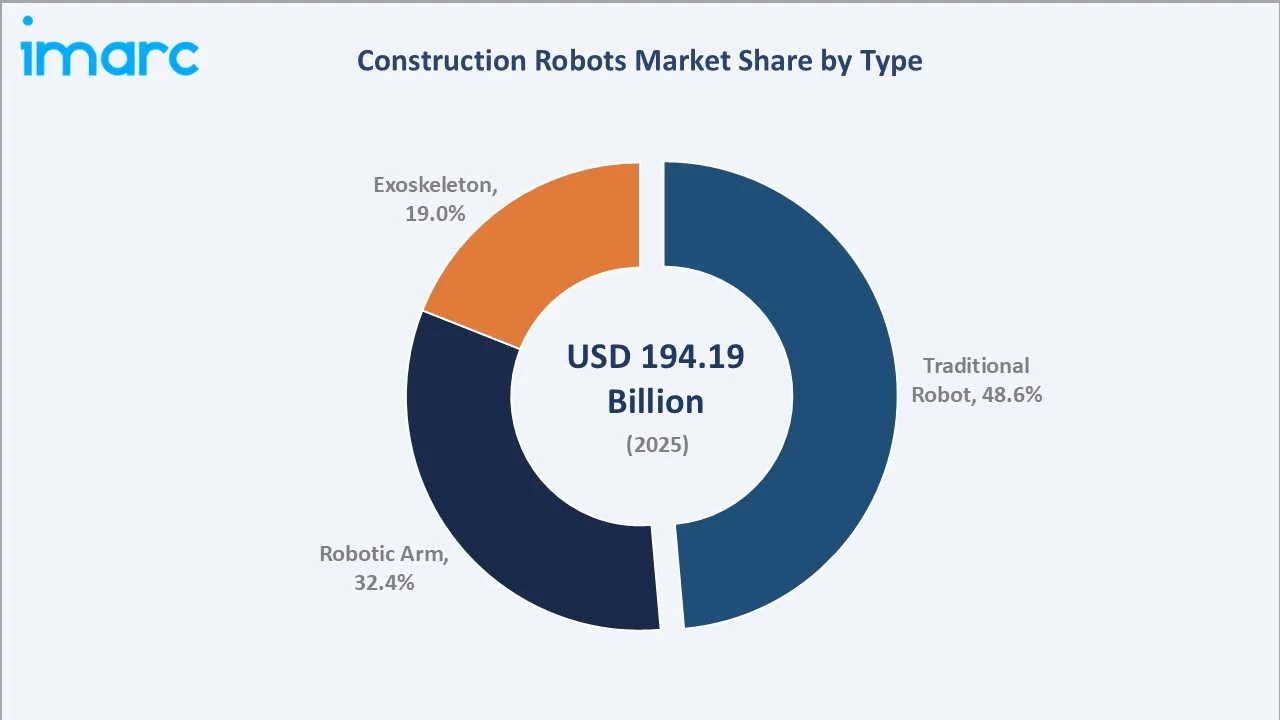

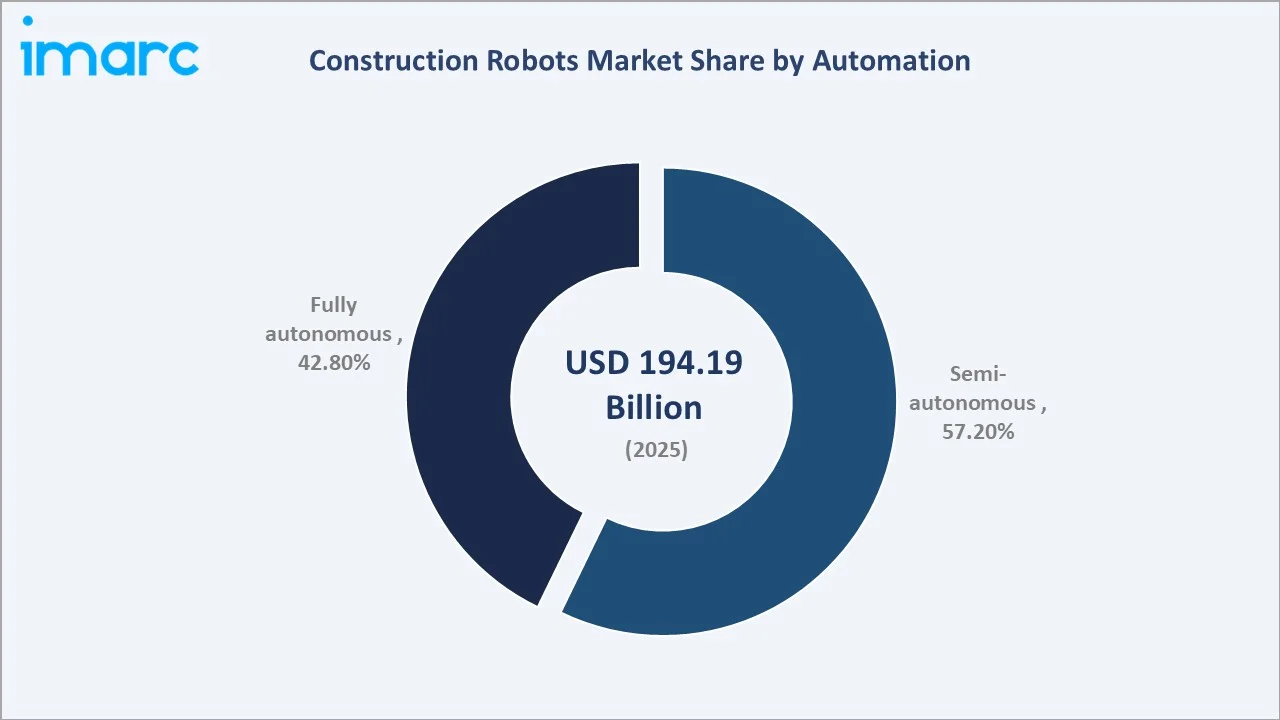

The global construction robots market size reached USD 194.2 Billion in 2025 and is projected to grow to USD 627.0 Billion by 2034, expanding at a CAGR of 12.74% during 2026-2034. Acute labor shortages, rapid advances in artificial intelligence (AI), and intensifying regulatory focus on jobsite safety are the primary demand accelerators. Traditional Robots lead by type at 48.6% market share in 2025, while Semi-Autonomous systems dominate the automation segment at 57.2%. North America holds the largest regional share at 36.8%, while Asia-Pacific emerges as the fastest-growing region.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 194.2 Billion |

|

Forecast Market Size (2034) |

USD 627.0 Billion |

|

CAGR (2026-2034) |

12.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.8% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Type |

Traditional Robot (48.6%, 2025) |

|

Leading Automation |

Semi-Autonomous (57.2%, 2025) |

The chart shows market growth from 2020–2034, highlighting steady historical expansion and a strong future outlook driven by AI-powered robotics, urbanization, and large-scale infrastructure development.

To get more information on this market, Request Sample

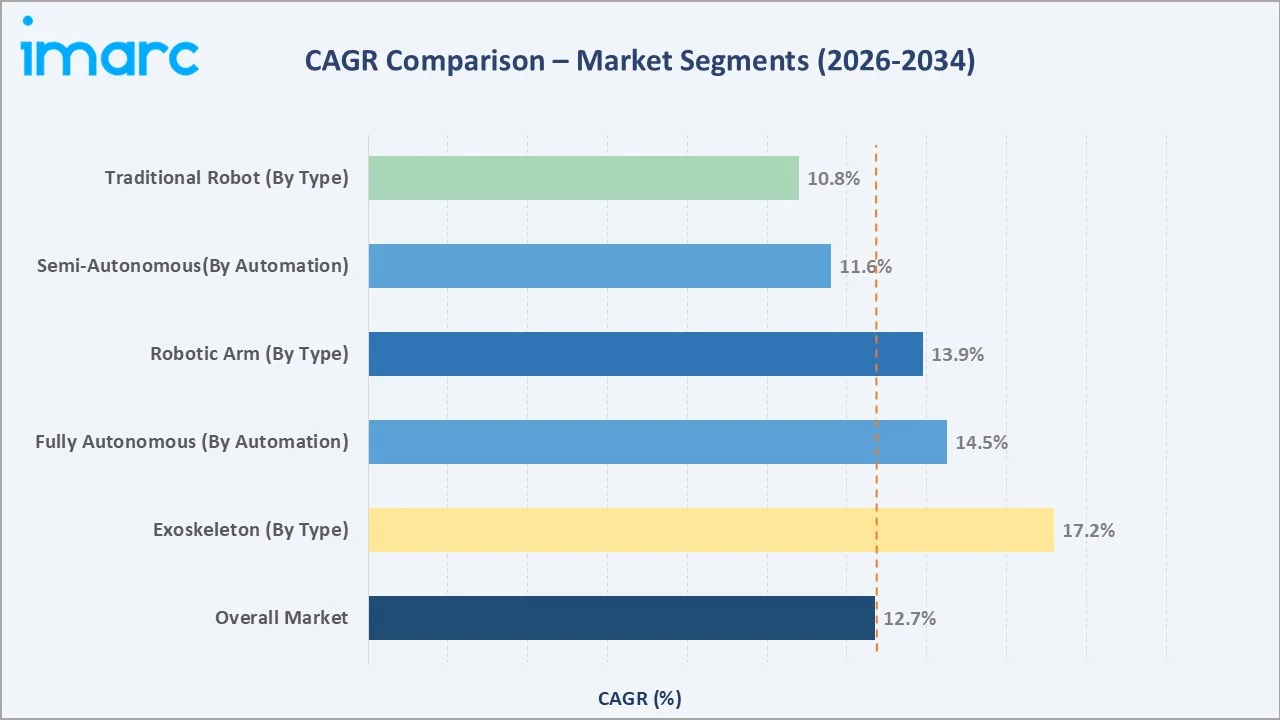

The CAGR comparison shows Exoskeleton and Fully Autonomous as the fastest-growing segments in the global construction robots market through 2034.

Executive Summary

The global construction robots market is undergoing a structural transformation, accelerated by the convergence of AI, robotics, and the worldwide pressure to modernize aging infrastructure. Valued at USD 194.2 Billion in 2025, the market is forecast to reach USD 627.0 Billion by 2034 at a CAGR of 12.74%. Labor shortages remain critical, with the U.S. needing 546,000 workers in 2023, alongside similar shortages in Germany, Japan, and South Korea. This shortage creates compelling economic justification for robotic deployment, as construction robots reduce reliance on manual labor by up to 40% on repetitive tasks.

Traditional robots led with 48.6% revenue share in 2025 due to broad use in demolition, excavation, and material handling. Robotic arms held 32.4% for precision applications. Exoskeletons, at 19.0%, showed fastest growth (~17.2% CAGR). Semi-autonomous systems dominated automation with 57.2%, supported by seamless integration with human workflows.

North America led regional revenue at 36.8% in 2025, supported by large-scale infrastructure bills totaling USD 1.2 Trillion and early adoption by contractors such as Bechtel and Turner Construction. Asia-Pacific at 28.4% represents the highest absolute growth potential, driven by China’s New Infrastructure and Japan’s i-Construction programs are accelerating construction automation, supported by labor shortages, productivity goals, and government-backed digital infrastructure investments. Key players include ABB Ltd., Husqvarna Group, Komatsu Ltd., Boston Dynamics, and Built Robotics.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Traditional Robot – 48.6% market share (2025) |

|

Fastest Growing Type |

Exoskeleton – ~17.2% CAGR (2026-2034) |

|

Leading Automation |

Semi-Autonomous – 57.2% share (2025) |

|

Leading Region |

North America – 36.8% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific – driven by urbanization and govt. investment |

|

Top Companies |

ABB, Komatsu, Husqvarna, Built Robotics, Boston Dynamics |

|

Market Opportunity |

USD 432.77 Billion incremental growth opportunity by 2034 |

Key Analytical Observations Supporting The Above Data:

- Traditional Robots: Traditional Robots hold 48.6% dominance in 2025, reflecting their versatility across heavy-duty outdoor tasks – demolition, excavation, and material transport.

- Semi-Autonomous Leadership: Semi-Autonomous systems lead at 57.2% in 2025 because they allow phased adoption – workers retain supervisory control, easing the transition for contractors without full automation infrastructure.

- Exoskeleton Surge: Exoskeletons are the fastest-growing type at ~17.2% CAGR, driven by occupational health regulations in Europe and North America limiting manual load-bearing above 25 kg without mechanical assistance.

- North America First-Mover: North America's 36.8% share reflects first-mover advantage, underpinned by USD 1.2 Trillion in federal infrastructure spending and the highest density of robotics-adopting general contractors.

- Asia-Pacific Growth Engine: Asia-Pacific's 28.4% share is growing rapidly, as China alone added 59,451.690 sq km in 2022 of new city construction area, demanding automation at unprecedented scale.

Global Construction Robots Market Overview

Construction robots are automated or semi-automated systems performing tasks like demolition, bricklaying, welding, concrete erection, finishing, and 3D printing. The ecosystem includes hardware manufacturers, AI developers, integrators, contractors, and end users across infrastructure, commercial, and high-risk applications.

Applications extend across public infrastructure (roads, bridges, tunnels), commercial and residential buildings, industrial plants, and environments such as nuclear dismantling. Macroeconomic enablers include global construction output projected to reach USD 15.2 Trillion by 2030, government-backed smart city initiatives across 50+ nations, and demographic shifts reducing the supply of manual construction labor in developed economies.

Market Dynamics

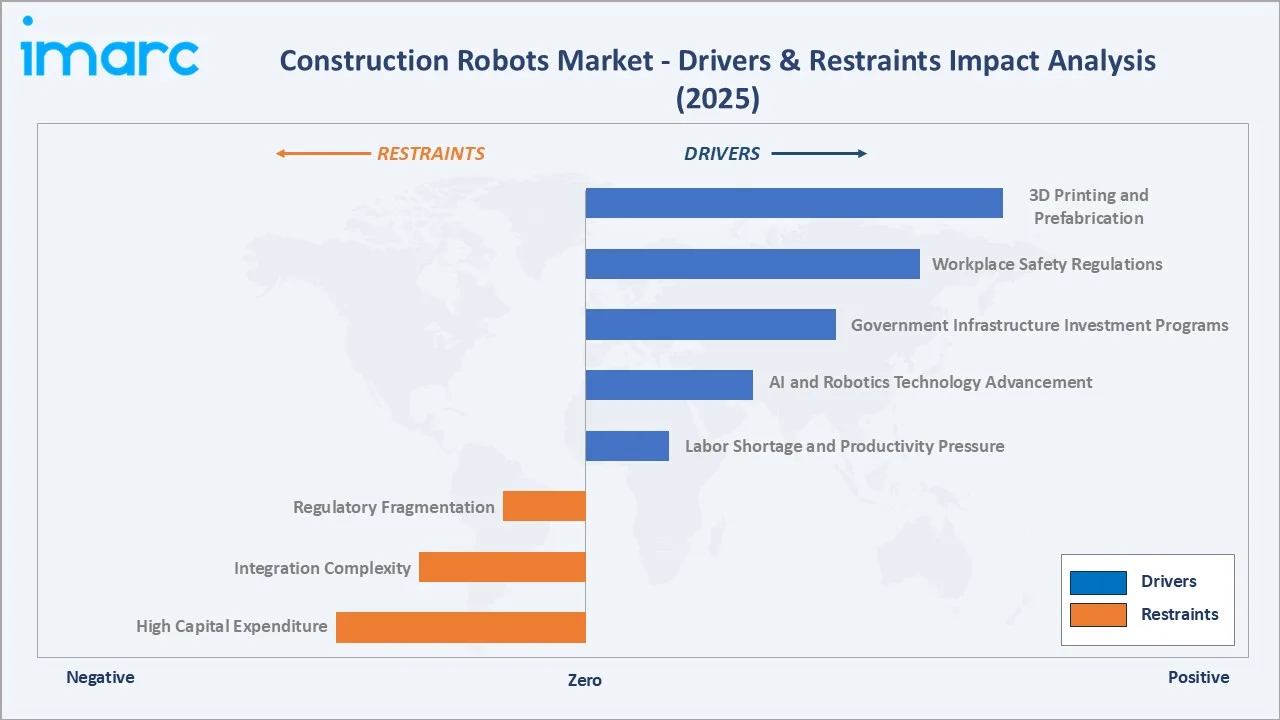

The construction robots market is driven by economic factors, technological advances, and regulations, with the chart showing key drivers and restraints influencing market momentum in 2025.

To evaluate market opportunities, Request Sample

Market Drivers

- Labor Shortage and Productivity Pressure: The construction industry faces significant labor shortages across major regions, including nearly two million workers in India and over 500,000 in the U.S. Bricklaying robots can place up to 3,000 bricks per day compared to 300–500 by human masons, improving productivity and reducing project timelines by approximately 20–25%.

- AI and Robotics Technology Advancement: Integration of AI, computer vision, LiDAR, and IoT has enabled robots to navigate dynamic jobsite environments autonomously. AI-powered construction robots can process 200+ sensor data points per second, enabling real-time obstacle avoidance on unstructured sites.

- Government Infrastructure Investment Programs: The U.S. Infrastructure Act allocated USD 550 billion, while EU Horizon Europe invested EUR 95.5 billion in R&D through 2027. Japan’s Society 5.0 promotes robotics and automation across industries, including construction, rather than mandating adoption.

- Workplace Safety Regulations: Construction accounts for 20% of all U.S. workplace fatalities (OSHA, 2023). Robots deployed in high-risk tasks such as working at heights or in toxic environments reduce human exposure – making safety compliance a structural market driver.

Market Restraints

- High Capital Expenditure: Initial procurement costs for advanced construction robots high, creating significant entry barriers for small and mid-sized contractors.

- Integration Complexity: Retrofitting robotic systems into legacy construction workflows requires site re-engineering, digital twin infrastructure, and workforce retraining, adding 15–25% to total implementation cost.

- Regulatory Fragmentation: Divergent robotics safety standards across jurisdictions – ISO 10218 in Europe versus ANSI/RIA R15.06 in North America – increase compliance overhead, slowing cross-border deployment.

Market Opportunities

- 3D Printing and Prefabrication: Construction 3D printing reduces material waste and enables rapid residential construction within days, supporting faster project execution and growing adoption of prefabricated automation technologies.

- Emerging Markets Urbanization: Asia and Africa are expected to account for nearly 90% of global urban population growth by 2050 (UN), while large-scale housing initiatives in countries like India create strong opportunities for construction robotics.

- Robotics-as-a-Service (RaaS): Robotics-as-a-Service (RaaS) models are gaining traction by lowering capital barriers, with companies expanding flexible autonomous equipment deployment across construction projects.

Market Challenges

- Workforce Displacement Resistance: Labor unions in Europe and North America have strongly opposed the widespread use of robotic automation. Many construction firms have identified worker resistance as a major barrier to adopting robotic technologies.

- Harsh Operating Environments: Construction sites are often unstructured, dusty, and subject to varying weather conditions. Robots must be capable of operating reliably across a wide range of extreme temperatures and in high-particulate environments, which significantly raises design and operational costs.

- Data Security and Connectivity: Autonomous construction robots rely on continuous connectivity for remote operation. Cybersecurity vulnerabilities in industrial IoT environments expose firms to operational disruption – deterring risk-averse contractors.

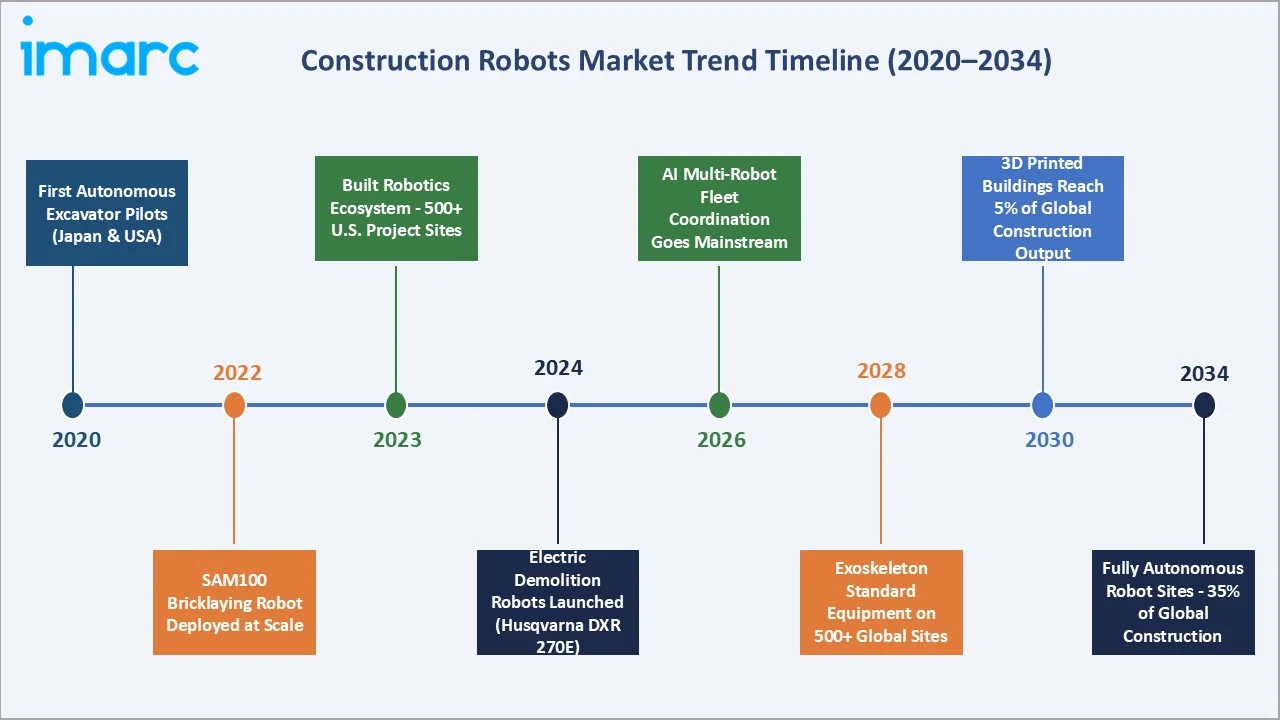

Emerging Market Trends

The construction robots market is rapidly evolving, with key innovations from 2020 to 2034 reshaping industry dynamics across technologies and applications.

1. AI-Powered Autonomous Site Management

AI-powered site management platforms are enabling autonomous excavation, grading, and trenching operations. Companies such as Built Robotics deploy autonomous equipment that reduces manual intervention and improves productivity on large-scale civil infrastructure projects.

2. Collaborative Robots (Cobots) in Construction

Collaborative robots are gaining adoption in interior finishing tasks such as drywall, layout, and painting. These systems operate safely alongside workers, improving productivity and reducing manual labor in precision-intensive construction activities.

3. Wearable Exoskeleton Adoption

Wearable exoskeletons are gaining adoption in construction to reduce worker fatigue and enhance lifting capacity. Systems such as Sarcos Guardian XO enable repetitive lifting and improve worker safety, particularly in labor-intensive construction environments.

4. Digital Twin Integration

Construction robots are increasingly integrated with digital twin environments using LiDAR, drones, and IoT sensors. These technologies improve planning accuracy, reduce rework, and enhance coordination across large construction projects.

5. Sustainable Construction Robotics

Sustainable construction robotics are gaining traction, with autonomous inspection and material handling systems supporting low-carbon construction practices. These technologies improve energy efficiency, reduce emissions, and enhance sustainability across construction operations.

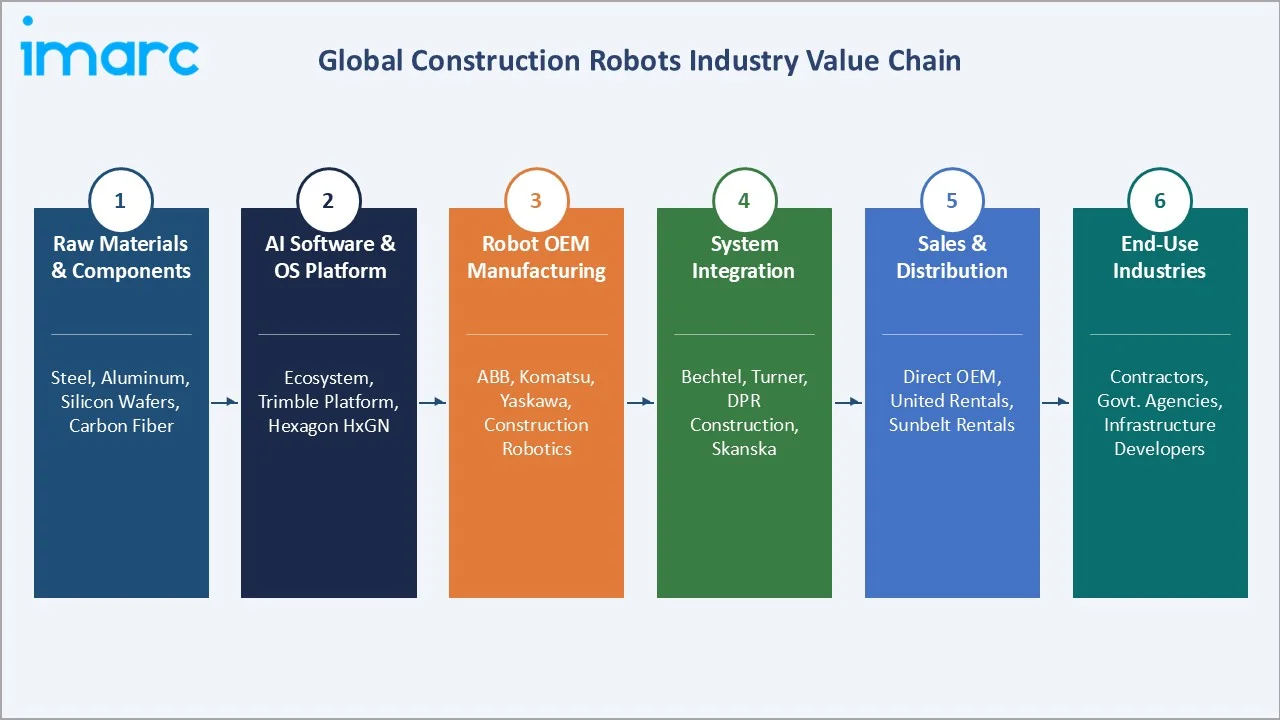

Industry Value Chain Analysis

The construction robots value chain spans six stages from materials to deployment, with system integration delivering the highest value, accounting for about 30–40% of total system costs.

|

Stage |

Key Activities |

Representative Players |

|

Raw Materials |

Steel, aluminum alloys, carbon fiber, semiconductor wafers |

POSCO, Alcoa, Toray, Intel |

|

AI & Software |

Exosystem platform, Trimble, Hexagon HxGN, AI training pipelines |

Built Robotics, Trimble, Hexagon |

|

Manufacturing |

Robot chassis assembly, electronics integration, QA testing |

ABB, Komatsu, Yaskawa Electric |

|

System Integration |

Software loading, AI training, site-specific customization |

Bechtel, Turner, DPR Construction |

|

Distribution |

Direct OEM sales, equipment rental firms, dealer networks |

United Rentals, Sunbelt Rentals |

|

End Users |

General contractors, infrastructure developers, gov. agencies |

Bechtel, Turner, VINCI, Skanska |

Technology Landscape in the Construction Robots Industry

AI and Machine Learning Integration

AI and machine learning are enabling construction robots to operate autonomously in unstructured environments. Computer vision and reinforcement learning improve navigation, object detection, and task optimization, enhancing productivity and reducing manual intervention on construction sites.

Advanced Sensor Systems

Modern construction robots integrate multi-modal sensors including LiDAR, radar, and thermal imaging to enable 3D mapping, proximity detection, and defect identification, improving automation accuracy and operational safety.

5G and Edge Computing Connectivity

5G and edge computing are enabling real-time communication and remote operation of construction robots. Private 5G networks developed by companies such as Ericsson and Nokia are supporting autonomous construction equipment deployment.

Additive Manufacturing and 3D Printing Robotics

Robotic 3D printing using concrete extrusion enables faster construction and reduced material waste. Systems such as ICON’s Vulcan platform have delivered multiple 3D-printed homes in Texas, demonstrating scalability for affordable housing and automated construction.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Traditional Robot | 48.6% | 2025 |

| Automation | Semi-Autonomous | 57.2% | 2025 |

| Function | Demolition | 🔒 | 2025 |

| Application | Public Infrastructure | 🔒 | 2025 |

| Region | North America | 36.8% | 2025 |

By Type

The Type segmentation divides the market into Traditional Robots, Robotic Arms, and Exoskeletons – each serving distinct construction applications. Traditional Robots dominate at 48.6% in 2025, reflecting their broad applicability across heavy-duty outdoor tasks. The segment mix is expected to shift toward Robotic Arms and Exoskeletons as precision work and worker augmentation gain prominence through 2034.

Traditional robots maintain majority share due to proven reliability, lower AI requirements, and cost efficiency in large civil projects. Robotic arms are gaining traction in commercial construction requiring precision, repeatability, and performance within tight tolerances.

To access detailed market analysis, Request Sample

By Automation

Semi-autonomous systems led automation with 57.2% share in 2025, offering human oversight. Fully autonomous systems, at 42.8%, are rapidly growing and expected to surpass semi-autonomous solutions in new unit sales by 2028.

Semi-autonomous systems dominate due to early adoption preferences and operational oversight, while fully autonomous systems grow rapidly in 24-hour operations, delivering higher efficiency and stronger ROI.

Regional Market Insights

The construction robots market shows regional differences driven by infrastructure investment, labor shortages, and technology adoption, with North America leading and Asia-Pacific expected to witness the fastest growth through 2026-2034.

The table below outlines regional market positions, key growth drivers, and leading players in the construction robots industry.

|

Region |

Key Drivers & Regulatory Context |

Major Companies |

|

North America 36.8% | 2025 |

USD 1.2T infrastructure program; labor costs USD 35–55/hr driving automation ROI; OSHA safety mandates |

Built Robotics, Construction Robotics, Bechtel, Turner Construction |

|

Asia Pacific 28.4% | 2025 |

China's New Infrastructure plan; Japan Society 5.0; India 20M homes target; fastest urban growth globally |

Komatsu Ltd., Shimizu Corp., Samsung C&T, Larsen & Toubro |

|

Europe 20.6% | 2025 |

EU Green Deal mandate for low-carbon construction; Germany-Japan bilateral robotics R&D; UK Robots4Build initiative |

ABB Ltd., VINCI SA, Skanska, Hilti Group |

|

Middle East & Africa 7.6% | 2025 |

Saudi Vision 2030 – USD 1T megaprojects; UAE smart city investments; NEOM project robotic mandates |

Consolidated Contractors, Saudi Aramco projects |

|

Latin America 6.6% | 2025 |

Brazil's PAC2 infrastructure revival; Chile and Colombia mining-adjacent construction; growing urbanization rate |

Constructora Conconcreto (Colombia) |

Competitive Landscape

The global construction robots market is moderately fragmented, with established industrial robot manufacturers competing alongside construction-native automation specialists and AI-first startups. The top 5 players collectively held approximately 38–42% of global market revenue in 2025. Companies are pursuing differentiation through AI capability, autonomy level, and deployment flexibility.

|

Company Name |

Brand / Platform |

Market Position |

HQ Region |

|

ABB |

ABB Robotics/ IRB series |

Market Leader |

Europe |

|

Komatsu Ltd. |

Smart Construction |

Market Leader |

Asia Pacific |

|

Husqvarna Group |

DXR Demolition Robots |

Strong Challenger |

Europe |

|

Built Robotics, Inc. |

Exosystem Platform |

Emerging Leader |

North America |

|

Boston Dynamics |

Spot |

Innovator |

North America |

|

Construction Robotics |

SAM100 Bricklaying Robot |

Niche Leader |

North America |

|

Shimizu Corporation |

Shimizu Smart Site |

Challenger |

Asia Pacific |

|

Yaskawa Electric Corporation |

Motoman Series |

Established Player |

Asia Pacific |

The competitive positioning matrix below maps key players by global market presence and strategic investment level, identifying leaders, challengers, and emerging specialists in the construction robots ecosystem.

Key Company Profiles

ABB

Overview: ABB is a global leader in industrial robotics headquartered in Zurich, Switzerland, with revenue of approximately USD 33.2 billion in FY2025. The company provides automation and robotic solutions across manufacturing, logistics, and infrastructure sectors.

- Product Portfolio: ABB’s IRB series robots support material handling, welding, and prefabrication applications, which are increasingly used in modular and automated construction environments.

- Recent Developments: In 2025, ABB Robotics expanded its industrial robot portfolio with the launch of the IRB 6730S, IRB 6750S, and IRB 6760. Combined with 11 next-generation robot families and 60 variants introduced since 2022, the expanded lineup delivers enhanced flexibility, performance, and sustainability benefits for customers across industries.

- Strategic Focus: ABB is expanding robotics applications into construction-related automation, including prefabrication and material handling.

Komatsu Ltd.

Overview: Komatsu is one of the world's largest construction equipment manufacturers, with FY2024 revenue of approximately JPY 4.10 trillion.

- Product Portfolio: Komatsu’s Smart Construction platform integrates autonomous equipment, drone surveying, and digital site data to enable automated earthmoving and site optimization.

- Recent Developments: In 2025, Komatsu Ltd. made its CES debut at the Las Vegas Convention Center, showcasing cutting-edge concepts including a lunar construction excavator and an underwater construction robot. The exhibit highlighted Komatsu’s focus on extreme application innovation and offered opportunities to connect with talent and industry partners, according to Taisuke Kusaba, CTO and President, Development Division.

- Strategic Focus: Komatsu aims to advance automation, electrification, and carbon-neutral construction equipment through digital construction platforms.

Built Robotics, Inc.

Overview: Robotics is a San Francisco-based construction robotics company that retrofits heavy equipment with autonomous technology.

- Product Portfolio: The Exosystem platform converts excavators and track loaders into autonomous machines capable of trenching, grading, and solar infrastructure installation.

- Recent Developments: In 2025, Built Robotics secured $33 million in funding to advance its construction robotics initiatives. The investment will support R&D on proprietary robotic technologies, including autonomous earthmoving systems and fine-tuned integration with traditional heavy equipment, aiming to make construction sites safer, faster, and more productive while addressing industry inefficiencies.

- Strategic Focus: The company focuses on scaling autonomous equipment and expanding global deployment.

Market Concentration Analysis

The global construction robots’ market is moderately fragmented, with key players including ABB, Komatsu Ltd., Husqvarna Group, Built Robotics, Inc., Boston Dynamics, Construction Robotics, Shimizu Corporation, and Yaskawa Electric Corporation collectively holding a 38–42% market share. Large industrial manufacturers compete on scale and distribution, while construction-focused specialists differentiate through AI-driven autonomy. This dual structure is expected to accelerate consolidation, driving several major M&A transactions between 2026 and 2029.

Investment & Growth Opportunities

Fastest Growing Segments

Exoskeletons and fully autonomous systems represent some of the fastest-growing segments, driven by labor shortages and AI advancements. Construction 3D printing robots also offer strong disruption potential, with the market projected to grow rapidly as adoption expands in residential and infrastructure construction.

Emerging Markets

India’s National Infrastructure Pipeline includes over 9,000 projects worth approximately USD 1.4 trillion through 2025, creating significant opportunities for construction automation. Saudi Arabia’s NEOM megacity is investing in advanced construction robotics and automation technologies. Indonesia’s Nusantara capital, with an estimated USD 35 billion investment, also represents a major emerging market for construction robotics deployment.

Venture Investment Trends

Fastest-growing segments include construction exoskeletons, driven by rising demand for worker safety and productivity improvements, followed by fully autonomous systems supported by AI advancements and evolving regulatory frameworks. Construction 3D printing robots offer strong disruption potential, enabling faster builds, reduced labor dependency, and improved material efficiency across residential and infrastructure projects.

Future Market Outlook (2026-2034)

The global construction robots’ market is positioned for sustained high-growth, with the USD 194.2 Billion base in 2025 expected to expand to USD 627.0 Billion by 2034 at a 12.74% CAGR. Three macro forces will shape the trajectory: AI-driven autonomy breakthroughs, regulatory normalization of robotic construction, and the intensifying global infrastructure investment cycle.

By 2034, robotic systems are expected to play a significant role in global construction, shifting the industry from labour-intensive to technology-driven operations. Platform ecosystems integrating AI software, robotic hardware, digital twins, and BIM will increasingly define competitive advantage.

Research Methodology

Primary Research

IMARC Group conducted 180+ in-depth interviews with construction robotics manufacturers, general contractors, technology integrators, regulatory bodies, and institutional investors across North America, Europe, Asia-Pacific, and the Middle East during 2024–2025. Primary research contributed 40% of total data inputs.

Secondary Research

Secondary research encompassed 350+ sources including company annual reports, patent filings, government infrastructure investment databases, industry association publications (CECE, AEM, JETRO), trade press, and academic research from MIT, ETH Zurich, and Waseda University. Historical data covers 2020–2024; forecast covers 2026–2034.

Forecasting Models

Market size estimates were triangulated using bottom-up revenue modeling by segment and region, top-down GDP and construction output correlations, and scenario analysis across base, optimistic, and conservative growth paths. Final estimates represent the base case at 12.74% CAGR.

Construction Robots Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Traditional Robot, Robotic Arm, Exoskeleton |

| Automations Covered | Fully Autonomous, Semi-Autonomous |

| Functions Covered | Demolition, Bricklaying, 3D Printing, Concrete Structural Erection, Finishing Work, Doors and Windows, Others |

| Applications Covered | Public Infrastructure, Commercial and Residential Buildings, Nuclear Dismantling and Demolition, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | ABB, Komatsu Ltd., Husqvarna Group, Built Robotics, Inc., Boston Dynamics, Construction Robotics, Shimizu Corporation, Yaskawa Electric Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the construction robots market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global construction robots market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the construction robots industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Construction Robots Market Report

The global construction robots market reached USD 194.2 Billion in 2025, expanding from USD 160.8 Billion in 2024, driven by labor shortages and AI technology advances.

The market is projected to reach USD 627.0 Billion by 2034, growing at a CAGR of 12.74% during 2026-2034, driven by AI automation and government infrastructure investment.

Key drivers of construction robotics adoption include global labor shortages, advancements in AI technologies, substantial government infrastructure investments, and stringent safety regulations enforced by authorities.

Traditional Robots held 48.6% market share in 2025, reflecting broad applicability in heavy-duty tasks such as demolition, excavation, and material handling on civil infrastructure projects.

Exoskeletons are the fastest-growing type at approximately 17.2% CAGR, driven by occupational health regulations and worker adoption in ergonomically demanding roles in North America and Europe.

North America leads with 36.8% market share in 2025, driven by significant federal infrastructure spending and early adoption of robotic technologies by leading U.S. general contractors.

Semi-autonomous robots require human supervisory input for complex decisions; fully autonomous robots perform complete task sequences without operator intervention – ideal for hazardous or 24-hour operations.

Major companies include ABB, Komatsu Ltd., Husqvarna Group, Built Robotics, Inc., Boston Dynamics, Construction Robotics, SHIMIZU CORPORATION, and Yaskawa Electric Corporation.

Key opportunities include Exoskeleton scale-up, RaaS platforms, AI software development, and deployment in India, Saudi Arabia, and Indonesia with multi-trillion-dollar infrastructure pipelines through 2030.

Asia-Pacific held 28.4% share in 2025 and is the fastest-growing region, driven by China’s New Infrastructure plan, Japan’s robotics initiatives, and India’s ambitious National Infrastructure Pipeline extending through 2030.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade